Meningitis Diagnostic Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

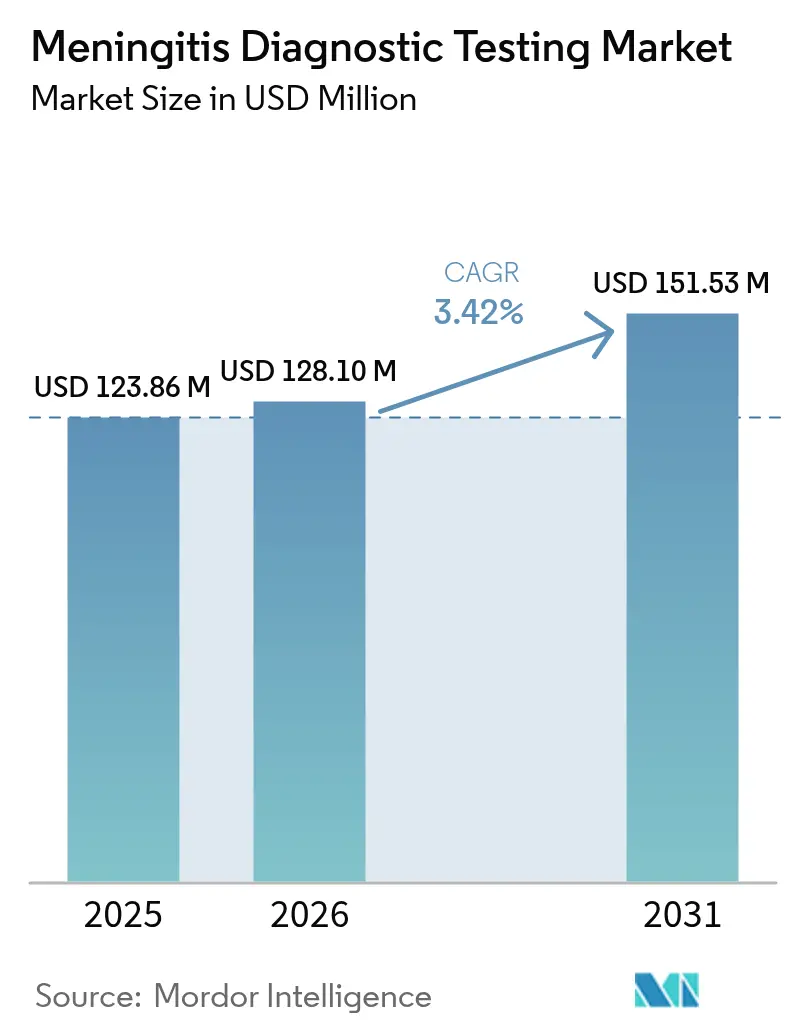

| Market Size (2026) | USD 128.1 Million |

| Market Size (2031) | USD 151.53 Million |

| Growth Rate (2026 - 2031) | 3.42% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Meningitis Diagnostic Testing Market Analysis by Mordor Intelligence

The meningitis diagnostic testing market size was valued at USD 123.86 million in 2025 and estimated to grow from USD 128.1 million in 2026 to reach USD 151.53 million by 2031, at a CAGR of 3.42% during the forecast period (2026-2031). Modest growth reflects a mature technology base balanced against cost pressures in many health systems. Rapid molecular innovations, rising syndromic panel uptake, and public programs that elevate newborn screening sustain demand. At the same time, high instrument costs, fragile cold-chain logistics, and pediatric cerebrospinal fluid (CSF) sampling limits temper adoption. Hospitals remain the principal buyers, yet academic centers and decentralized clinics are accelerating purchases as point-of-care platforms shrink turnaround times and broaden access. North America leads revenue thanks to robust reimbursement and stewardship mandates, whereas Asia-Pacific offers the fastest expansion as governments upgrade laboratory infrastructure. Competitive intensity rises as incumbents defend PCR and culture franchises against next-generation sequencing (NGS), CRISPR assays, and heat-stable reagents tailored for low-resource settings.

Key Report Takeaways

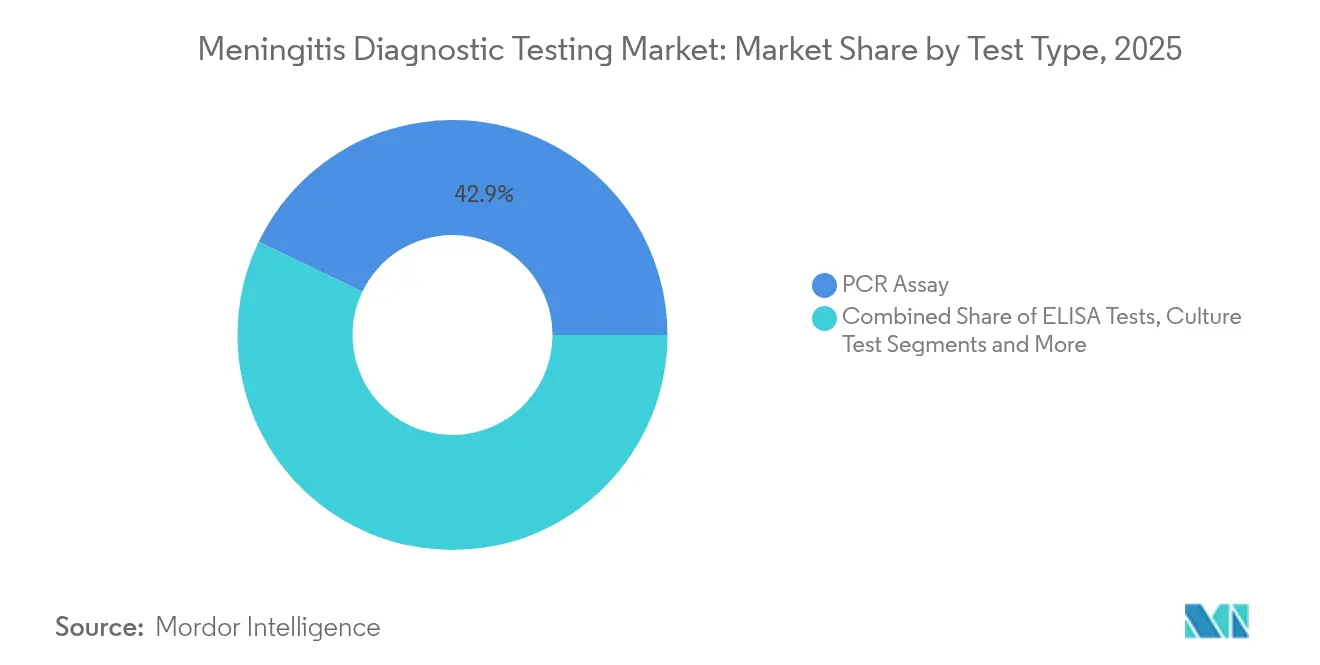

- By technology, molecular diagnostics led with 49.12% of the meningitis diagnostic testing market share in 2025; next-generation sequencing is poised for a 6.88% CAGR to 2031.

- By test type, PCR held 42.87% share of the meningitis diagnostic testing market size in 2025, while CRISPR-based assays are set to grow at 6.49% CAGR.

- By sample type, CSF accounted for 61.95% revenue in 2025; blood/serum testing is expected to expand at 5.18% CAGR through 2031.

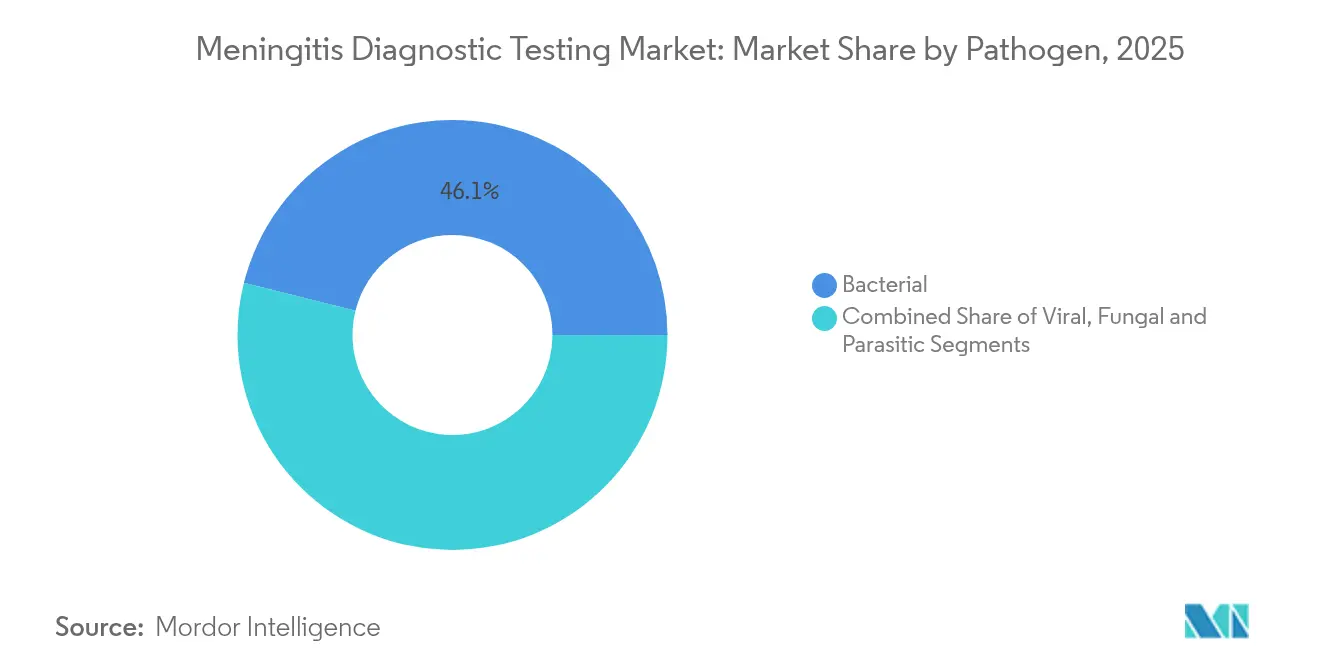

- By pathogen, bacterial detection dominated with 46.10% share in 2025; viral detection is projected to rise at 4.75% CAGR.

- By end user, hospitals commanded 55.74% of demand in 2025, whereas academic and research laboratories record the highest forecast CAGR of 5.32%.

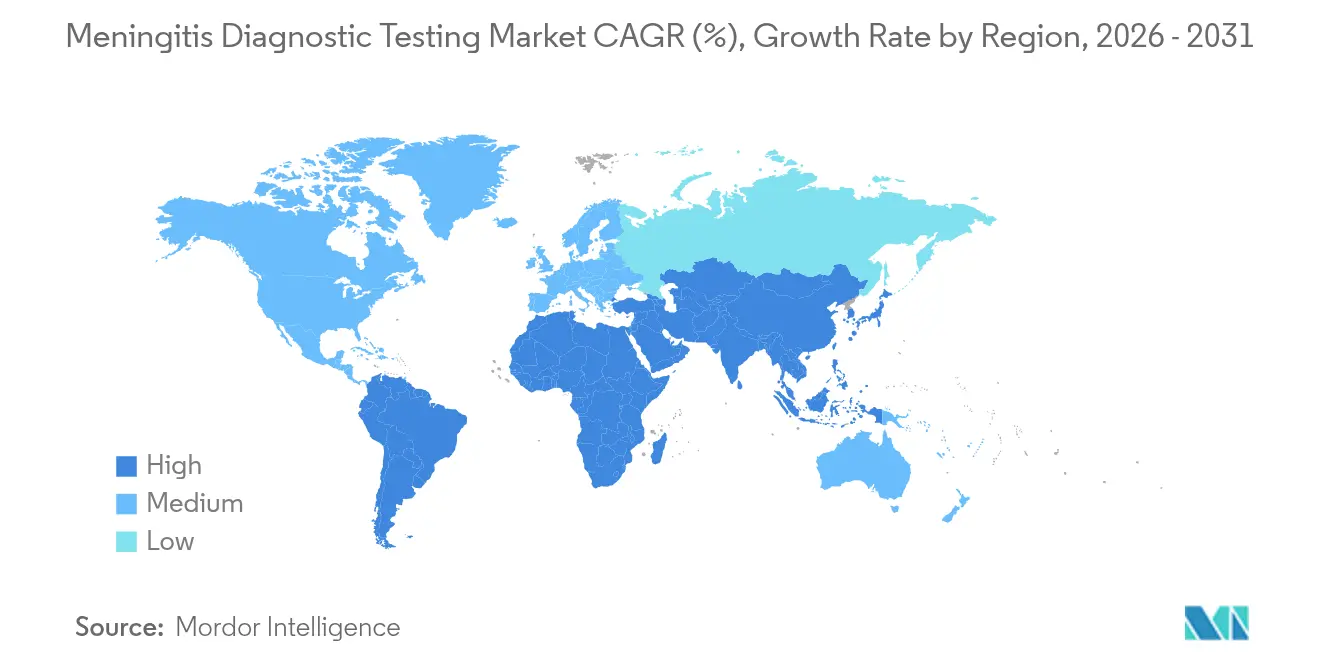

- By geography, North America held 37.65% share in 2025; Asia-Pacific is the highest-growth region at 5.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Meningitis Diagnostic Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in global meningitis incidence | +0.8% | Sub-Saharan Africa, Asia-Pacific | Long term (≥ 4 years) |

| Growing adoption of syndromic multiplex PCR panels | +1.2% | North America, EU, expanding into Asia-Pacific | Medium term (2-4 years) |

| Hospital stewardship programs targeting rapid rule-out | +0.7% | North America, EU, pilot programs in Asia-Pacific | Short term (≤ 2 years) |

| Decentralization toward point-of-care testing in low-resource settings | +0.9% | Sub-Saharan Africa, South Asia, Latin America | Long term (≥ 4 years) |

| National newborn screening mandates for bacterial meningitis | +0.5% | North America, EU, middle-income countries | Medium term (2-4 years) |

| Pandemic-driven investment in molecular infrastructure | +0.6% | Global, emphasis on Asia-Pacific and Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise In Global Meningitis Incidence

Surveillance confirms that bacterial meningitis still claims 10–15% case-fatality despite vaccine progress.[1]World Health Organization, “Global Meningitis Weekly Bulletin,” who.intSub-Saharan Africa reported 2,370 suspected cases and 178 deaths in the 2023–2024 season, underscoring the persisting diagnostic need. Antimicrobial resistance in Streptococcus pneumoniae and Neisseria meningitidis increases urgency for rapid pathogen identification. Asia-Pacific remains under-diagnosed owing to weak surveillance, hinting at latent volume once labs scale up. Urbanization and climate shifts may alter transmission patterns, making early detection integral to outbreak control. Together, these forces keep the meningitis diagnostic testing market on a steady growth track.

Growing Adoption Of Syndromic Multiplex PCR Panels

Hospital systems now favor panels that detect up to 14 meningitis pathogens from one CSF specimen in under an hour. Academic centers adopting the BioFire FilmArray panel trimmed median antibiotic courses from 3 days to 2 days while boosting de-escalation rates by 46%.[2]Amanda L. Harrington, “Impact of Multiplex PCR Panels on Antimicrobial Stewardship Outcomes,” Clinical Infectious Diseases, ncbi.nlm.nih.gov Faster rule-out improves bed turnover and supports value-based care. Pediatric wards gain assurance, as sensitivity for Group B Streptococcus tops 100% in culture-negative cases. Cost-offset studies find savings through shorter stays that outweigh kit expense. These operational wins move multiplex PCR into routine practice, lifting the meningitis diagnostic testing market.

Hospital Stewardship Programs Targeting Rapid Rule-Out

Antimicrobial stewardship metrics push emergency departments to embed rapid meningitis assays in triage. Studies note 52-hour cuts in time to targeted therapy, translating to fewer adverse events and lower broad-spectrum antibiotic use.[3]Susan C. Winchell, “Integrating Rapid Diagnostic Tests into Antimicrobial Stewardship Programs,” Food and Drug Administration, fda.govAs regulators tie reimbursement to stewardship performance, hospital administrations budget for on-demand testing. Combined diagnostic and antimicrobial stewardship teams generate iterative protocols that refine empiric therapy within hours rather than days. This alignment accelerates commercial uptake, especially in integrated health networks.

Decentralization Toward Point-Of-Care Testing In Low-Resource Settings

Portable platforms priced below USD 10 per test now deliver 88% sensitivity and 90% specificity for bacterial meningitis at district clinics.[4]Michael M. Wanzira, “Point-of-Care Cerebrospinal Fluid Lactate Testing for Bacterial Meningitis in Uganda,” American Journal of Tropical Medicine and Hygiene, ajtmh.org Freeze-preventive cold boxes and solar power modules keep reagents stable off-grid, enabling consistent outreach in the African meningitis belt. With 80 near-point-of-care molecular systems already catalogued, suppliers see a 63.6 million-test annual addressable volume across low- and middle-income countries. Decentralization therefore expands the meningitis diagnostic testing market beyond tertiary centers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX/OPEX of multiplex molecular instruments | -0.9% | Global, acutely felt in low- and middle-income countries | Long term (≥ 4 years) |

| Limited CSF sample availability in pediatric settings | -0.6% | Global, higher impact in resource-limited hospitals | Medium term (2-4 years) |

| Persisting reimbursement gaps for rapid point-of-care tests | -0.7% | North America, EU, emerging markets | Medium term (2-4 years) |

| Cold-chain logistics constraints in low-resource markets | -0.5% | Sub-Saharan Africa, South Asia, remote regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX/OPEX Of Multiplex Molecular Instruments

PCR systems range from USD 100,000 to 300,000 and charge USD 50-150 per cartridge, locking out small laboratories. Ethiopian hospitals report FilmArray reagent costs exceeding annual budgets even when clinical benefits are clear. Leasing schemes exist, but few institutions possess financing capacity. Low-volume sites cannot amortize fixed costs, making price a brake on the meningitis diagnostic testing market.

Limited CSF Sample Availability In Pediatric Settings

Lumbar puncture in neonates yields low volumes, restricting test menus. Many emergency departments must triage which assays run on <0.5 mL, delaying comprehensive diagnosis. Vendors now engineer cartridges needing 0.2 mL, yet labs require training on micro-handling steps. Until micro-sampling becomes routine, sample scarcity continues to curb market expansion, especially in children.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: CRISPR Innovation Challenges PCR Dominance

CRISPR assays log the fastest 6.49% CAGR yet PCR retains 42.87% of 2025 revenue. The meningitis diagnostic testing market continues to lean on PCR because clinicians trust its sensitivity, and hospital labs already own compatible cyclers. However, CRISPR-Cas split-luciferase methods now detect attomolar nucleic acid directly from CSF in 20 minutes, matching syndromic panel breadth. Lateral-flow strips stay relevant in outreach campaigns where no electricity is guaranteed. ELISA gradually declines as molecular specificity rises. Culture’s share erodes further when patients arrive pre-treated with antibiotics that inhibit growth.

Demand shifts toward rapid rule-out: multiplexed isothermal assays reach 10 fg detection of Neisseria meningitidis, aiding outbreak triage in the African belt. Latex agglutination still gives value in field tents because it stores ambient, though sensitivity limits remain. Artificial-intelligence imaging that reads culture plates promises to salvage legacy workflows by automating detection, so legacy and novel technologies coexist, creating layered opportunities within the meningitis diagnostic testing market.

By 2031, CRISPR penetration in mid-income hospitals will challenge PCR’s leadership, yet the coexistence of low-tech and high-tech solutions reflects buyer heterogeneity. Vendors therefore maintain mixed portfolios, balancing high-complexity panels for tertiary centers with robust lateral-flow kits for outreach. This dual strategy enlarges addressable volumes and mitigates single-technology risk.

By Technology: NGS Disrupts Molecular Diagnostics Leadership

Molecular diagnostics represented 49.12% share in 2025, but NGS’s 6.88% CAGR positions it as a prime disruptor. Metagenomic sequencing achieved 60.6% positivity versus 20.2% for conventional CSF methods in one hospital cohort. Its aptitude for unknown or mixed infections drives adoption in neurologic ICUs where unexplained encephalitis persists. Immunoassays defend niche point-of-care roles thanks to minimal training needs, while classic culture remains essential for susceptibility profiling even as throughput declines.

NGS now returns actionable reads in <6 hours on low-capacity benchtop sequencers, letting clinicians target therapy within the admission window. Cloud bioinformatics portals handle analytics, reducing local staffing dependencies. However, costs per sample still average USD 175, limiting routine use outside research centers. Over the forecast, reagent price drops and pay-per-sample business models are likely to send NGS deeper into routine microbiology, lifting the meningitis diagnostic testing market size devoted to sequencing applications.

By Sample Type: Blood Testing Gains Ground Against CSF Dominance

CSF retained 61.95% revenue in 2025, yet blood/serum assays grow 5.18% annually as clinicians seek less invasive options. Plasma NGS identified causative agents in 36% of pediatric meningitis cases ahead of CSF culture results. Nasopharyngeal swabs help detect respiratory pathogens linked to secondary meningitis. Other matrices such as urine and saliva remain experimental.

C-reactive protein measurement in CSF can differentiate bacterial from viral meningitis within 30 minutes at the bedside, offering a cost-effective adjunct. Point-of-care lactate readings also show 88% sensitivity, making handheld meters valuable in rural clinics. The meningitis diagnostic testing market now sees vendors packaging multi-specimen panels where one cartridge handles CSF, blood, or swab, streamlining logistics and broadening the addressable patient pool.

By Pathogen: Viral Detection Accelerates Amid Bacterial Dominance

Bacterial detection delivered 46.10% market revenue in 2025 as immediate antibiotic intervention makes rapid ID vital. Viral assays, however, post a 4.75% CAGR because stewardship requires distinguishing viral cases that need no antibiotics. Multiplex PCR now picks up enteroviruses, herpesviruses, and parechoviruses concurrently, cutting empiric therapy. Fungal assays, especially cryptococcal antigen tests, remain indispensable in HIV-heavy geographies. Parasitic testing is niche but essential in regions where cerebral malaria or angiostrongyliasis overlaps meningitis symptoms.

Comprehensive panels that share reagents across pathogen classes improve inventory management and laboratory workflows. By 2031, viral testing volumes could approach bacterial in specialized centers, although revenue skew will persist due to higher cartridge prices for bacterial resistance markers. This diversity keeps the meningitis diagnostic testing market resilient to pathogen-specific demand swings.

By End User: Academic Labs Drive Innovation Beyond Hospital Dominance

Hospitals held 55.74% spend in 2025, reflecting integrated lab systems and stewardship mandates. Nonetheless, academic and research labs show a 5.32% CAGR as grant-funded projects validate CRISPR, NGS, and AI analytics. Diagnostic reference centers act as overflow for community hospitals, shifting complex panels off-site. Point-of-care clinics, military bases, and humanitarian NGOs form the fastest-rising “other” segment as portable devices become rugged and battery-operated.

Academic partnerships frequently determine early market entry for novel technologies. Collaborations with engineering departments accelerate cartridge miniaturization and cost reduction, which later migrate into hospital procurement cycles. Thus, innovation diffusion through academia materially shapes future growth paths of the meningitis diagnostic testing industry.

Geography Analysis

North America commanded 37.65% revenue in 2025, enabled by payer coverage and FDA pathways that fast-track infectious disease assays. Hospitals integrate rapid panels into stewardship dashboards, trimming average length of stay and unlocking bed capacity. Canada expands coverage through provincial lab modernization grants, while Mexico’s Seguro Popular reforms channel funds to regional diagnostic hubs. Despite leadership, budget scrutiny prompts negotiations on reagent pricing to maintain sustainable volumes in mature markets.

Asia-Pacific is the top growth engine at 5.95% CAGR through 2031. China funds hospital laboratory automation in its Healthy China 2030 plan, boosting uptake of NGS and multiplex PCR. India scales newborn screening under Ayushman Bharat, increasing routine bacterial panels. Japan emphasizes rapid viral differentiation in pediatric wards to cut antibiotic misuse. Southeast Asian nations upgrade meningitis surveillance post-COVID-19, aligning vaccine programs with better diagnostic confirmation. These initiatives collectively swell the meningitis diagnostic testing market in the region.

Europe posts steady gains as antimicrobial resistance watchlists drive molecular demand. Germany and France pilot metagenomic sequencing reimbursement, and the United Kingdom applies value-based procurement for point-of-care kits across the National Health Service. Eastern European modernization grants fund cold-chain upgrades that support reagent stability. Cross-border data sharing through the European Centre for Disease Prevention and Control harmonizes testing protocols, providing scale benefits to suppliers. Market uptake thus remains consistent, though pricing pressures persist under single-payer systems.

Competitive Landscape

The market is moderately fragmented. Abbott, bioMérieux, and Thermo Fisher Scientific leverage broad menus across PCR, culture media, and automated lines to serve tier-one hospitals. bioMérieux partnered with Oxford Nanopore Technologies in 2025 to co-develop nanopore-based meningitis diagnostics targeting 30-minute sample-to-result times. Abbott extends its ID NOW molecular platform with a meningitis panel suited for emergency rooms. Thermo Fisher integrates meningitis assays into its Amplitude high-throughput system bought widely during COVID-19, amortizing equipment among multiple diseases.

Disruptors employ CRISPR, AI, and lyophilized reagents that bypass cold-chain, courting NGOs and field clinics. Start-ups focus on microfluidic chips needing <50 μL CSF and priced under USD 8, addressing pediatric sampling restrictions. Suppliers differentiate via bundled analytics dashboards that feed stewardship metrics directly into hospital electronic medical records, improving procurement justification.

Strategic alliances reduce go-to-market timelines. Instrument manufacturers license assay content from academic labs, and reagent firms bundle logistics solutions with solar refrigerators in Africa. Competitive positioning thus hinges on solution breadth, cost-to-serve, and adaptability to mixed infrastructure levels across countries. These dynamics foster innovation yet spread revenue across many players, sustaining a fragmented but vibrant meningitis diagnostic testing market.

Meningitis Diagnostic Testing Industry Leaders

Seegene Inc.

IMMY

Thermo Fisher Scientific Inc

Siemens Healthineers

bioMérieux

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The World Health Organization issued its first global guidelines for meningitis diagnosis, treatment, and care, targeting faster detection and improved long-term outcomes.

- November 2024: QIAGEN received U.S. FDA clearance for the QIAstat-Dx Meningitis/Encephalitis Panel, expanding its syndromic testing portfolio.

Global Meningitis Diagnostic Testing Market Report Scope

As per the scope of the report, meningitis is a disorder that affects the gentle membranes known as meninges, which cover the spinal cord and brain. The causes of meningitis disease are mainly of three types which include bacterial, fungal, and viral. Bacterial-associated meningitis is the most lethal type of meningitis disorder and can be transferred between people in close contact with each other.

The meningitis diagnostic testing market is segmented by test type, end-user, and geography. By test type, the market is segmented by latex agglutination test, lateral flow assay, PCR assay, ELISA tests, culture test, and others. By end-user, the market is segmented by hospitals, diagnostics centers, and others. By geography, the market is segmented by North America, Europe, Asia Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (USD) for the above segments.

| Latex Agglutination Tests |

| Lateral-Flow Assay |

| PCR Assay |

| ELISA Tests |

| Culture Test |

| CRISPR-based Assay |

| Molecular Diagnostics |

| Immunoassays |

| Microbiology / Culture |

| Next-Generation Sequencing |

| Cerebrospinal Fluid (CSF) |

| Blood / Serum |

| Nasopharyngeal Swab |

| Others (Urine, Saliva) |

| Bacterial |

| Viral |

| Fungal |

| Parasitic |

| Hospitals |

| Diagnostic Centers |

| Academic & Research Labs |

| Others (POC Clinics, Military, NGOs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Type | Latex Agglutination Tests | |

| Lateral-Flow Assay | ||

| PCR Assay | ||

| ELISA Tests | ||

| Culture Test | ||

| CRISPR-based Assay | ||

| By Technology | Molecular Diagnostics | |

| Immunoassays | ||

| Microbiology / Culture | ||

| Next-Generation Sequencing | ||

| By Sample Type | Cerebrospinal Fluid (CSF) | |

| Blood / Serum | ||

| Nasopharyngeal Swab | ||

| Others (Urine, Saliva) | ||

| By Pathogen | Bacterial | |

| Viral | ||

| Fungal | ||

| Parasitic | ||

| By End User | Hospitals | |

| Diagnostic Centers | ||

| Academic & Research Labs | ||

| Others (POC Clinics, Military, NGOs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the meningitis diagnostic testing market?

The meningitis diagnostic testing market size stands at USD 128.1 million in 2026 and is projected to reach USD 151.53 million by 2031 at a 3.42% CAGR.

Which technology leads revenue in meningitis diagnostics?

Molecular diagnostics holds the largest share at 49.12% in 2025, driven by hospital reliance on PCR and multiplex panels.

Why is Asia-Pacific the fastest-growing region?

Asia-Pacific records a 5.95% CAGR due to large investments in laboratory infrastructure, expanded newborn screening, and rising awareness of meningitis’s public health burden.

How do CRISPR assays influence market growth?

CRISPR assays grow at 6.49% CAGR by offering rapid, highly sensitive detection that challenges traditional PCR dominance and supports decentralized testing.

What are the main restraints facing the market?

High capital and operating costs of multiplex instruments, limited pediatric CSF volumes, reimbursement gaps for rapid tests, and cold-chain weaknesses in low-resource areas restrain wider adoption.

Page last updated on: