Sinusitis Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

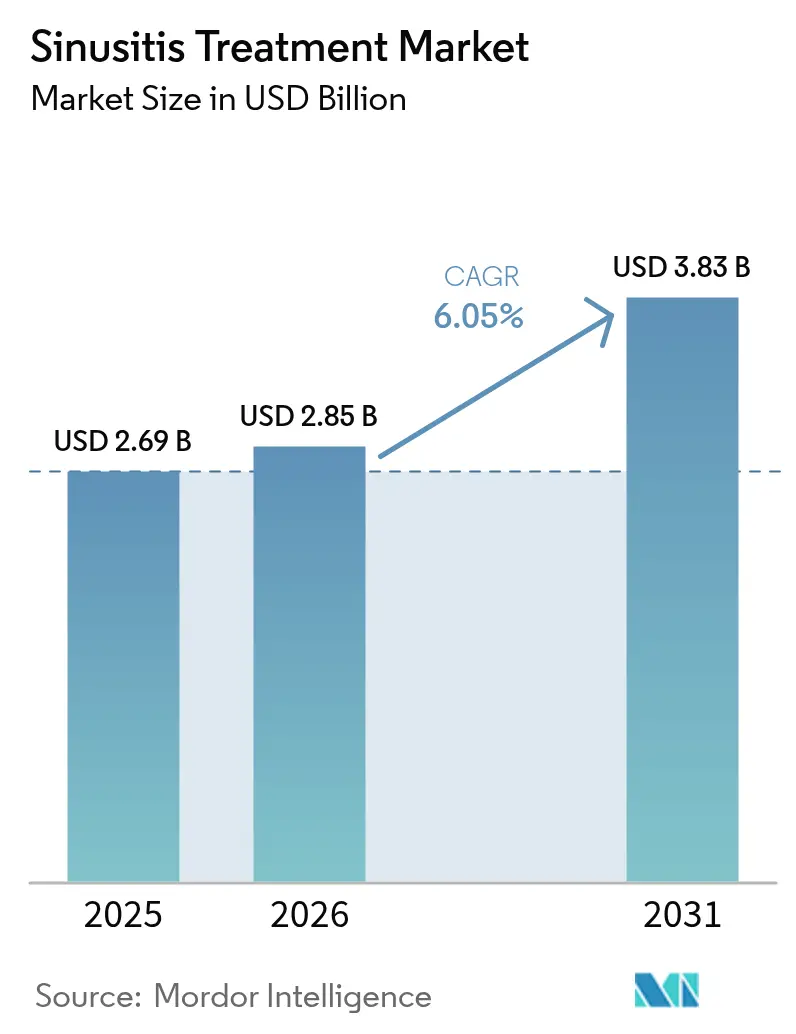

| Market Size (2026) | USD 2.85 Billion |

| Market Size (2031) | USD 3.83 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

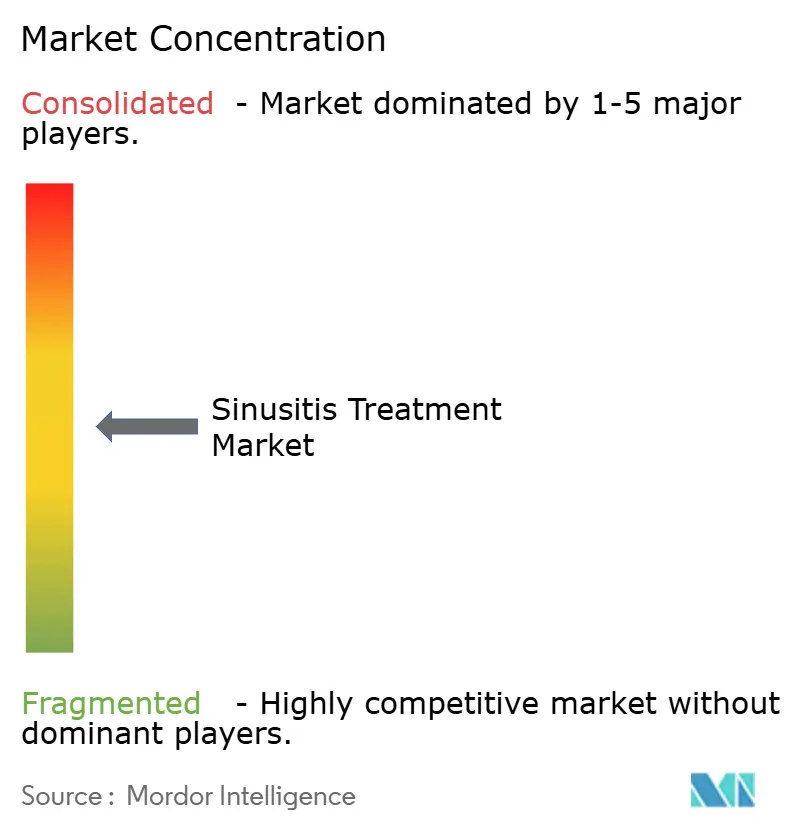

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sinusitis Treatment Market Analysis by Mordor Intelligence

The Sinusitis Treatment Market size is expected to grow from USD 2.69 billion in 2025 to USD 2.85 billion in 2026 and is forecast to reach USD 3.83 billion by 2031 at 6.05% CAGR over 2026-2031. Rising chronic rhinosinusitis prevalence, fast uptake of balloon sinuplasty, and the approval of precision biologics such as dupilumab are accelerating the sinusitis treatment market across all regions. Rapid technological shifts, especially AI-guided navigation systems and robotic functional endoscopic sinus surgery (FESS) platforms, are sharpening surgical accuracy while lowering complication rates, thereby raising procedure volumes and broadening the sinusitis treatment market. At the same time, combination drug regimens and microbiome-modulating probiotics are expanding therapeutic choice, even as antibiotic-resistance pressures and generic competition intensify pricing risk. Post-COVID shifts in sinonasal bacterial ecosystems are creating novel probiotic niches, further reshaping the sinusitis treatment market.

Key Report Takeaways

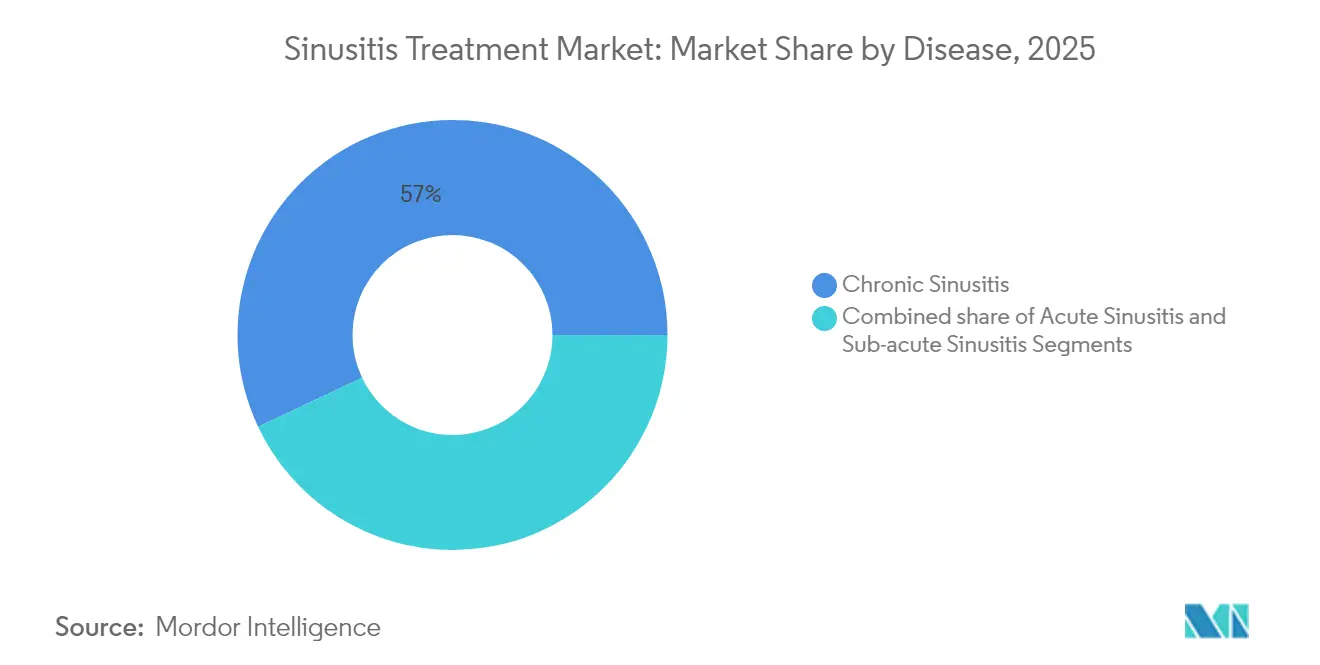

- By disease, chronic sinusitis commanded 57.02% of sinusitis treatment market share in 2025 while acute sinusitis is advancing at a 7.31% CAGR through 2031.

- By modality, antibiotics led with 42.35% revenue share of the sinusitis treatment market size in 2025, whereas analgesics are growing fastest at 7.85% CAGR to 2031.

- By geography, North America held 39.62% share of the sinusitis treatment market size in 2025, while Asia-Pacific records the highest projected CAGR at 8.02% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sinusitis Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Chronic & Acute Rhinosinusitis | +1.2% | Global, with higher impact in developed regions | Medium term (2-4 years) |

| Growing Preference for Minimally-Invasive Balloon Sinuplasty | +1.0% | North America & Europe, expanding to APAC | Short term (≤ 2 years) |

| Expanding Access to Combination Drug Regimens | +0.8% | Global, particularly emerging markets | Medium term (2-4 years) |

| Rapid Uptake of Biologics for CRSwNP | +1.5% | North America & Europe primarily | Short term (≤ 2 years) |

| AI-Guided Endoscopic Navigation & Robotic FESS Platforms | +0.7% | Developed markets initially | Long term (≥ 4 years) |

| Microbiome-Modulating Probiotics & Post-Biotics Emerging | +0.5% | Global, research-driven adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic & Acute Rhinosinusitis

Chronic rhinosinusitis now affects up to 12% of the global population, translating to heavier outpatient loads and higher surgical referrals. COVID-related microbial shifts introduced a cohort with persistent inflammatory symptoms, raising hospital admissions for complicated sinusitis. In the United States, productivity losses average 20.6 workdays per patient per year and drive USD 8 billion in annual medical spending. Urban air pollutants and allergens intensify mucosal inflammation, magnifying demand for durable treatments across every sinusitis treatment market segment. Aging populations and longer life expectancy further solidify a multi-year volume base for biologics, image-guided surgery, and probiotic solutions.

Growing Preference for Minimally-Invasive Balloon Sinuplasty

Balloon sinuplasty has been increasing, showing how tissue-preserving techniques are displacing conventional FESS. Current evidence reports 91% clinical success with fewer postoperative complications, positioning balloon dilation as the first-line surgical option for many patients.[1]Source: Daniel H. Lofgren, “Frontal Sinus Balloon Sinuplasty,” Spartan Medical Research Journal, smrj.scholasticahq.com Office-based execution cuts hospital stay and dovetails with value-based care; Stryker’s analysis shows USD 2,200 per-patient savings compared with traditional FESS, a compelling argument for payers. Image-guided navigation further improves precision, especially inside complex frontal recess anatomy, while disposable microdebriders reduce infection risk and reprocessing costs. These advantages collectively pull incremental procedure volume into the sinusitis treatment market.

Expanding Access to Combination Drug Regimens

First-line therapy increasingly pairs amoxicillin-clavulanate with intranasal corticosteroids, shortening acute exacerbations by up to 66% compared with monotherapy, as demonstrated in the ReOpen program. Optinose’s XHANCE exhalation platform delivers higher steroid deposition into obstructed passages and gained FDA clearance for chronic rhinosinusitis without nasal polyps in March 2024. Updated guidelines in numerous emerging economies now incorporate combination regimens, reflecting better diagnostic capacity and patient education. The trend helps maintain antibiotic efficacy while curbing resistance, supporting sustainable revenue growth for branded formulations despite generic erosion in mature molecules.

Rapid Uptake of Biologics for CRSwNP

Dupilumab drives sustained symptom relief and fewer surgeries, as validated in SINUS-24 and SINUS-52 trials.[2]Source: Philippe Gevaert, “Dupilumab Improves Symptoms in CRSwNP,” Clinical & Translational Immunology, ncbi.nlm.nih.gov The September 2024 FDA extension to adolescents ages 12-17 widens the eligible U.S. population by roughly 9,000 patients. Pipeline agents such as tezepelumab and depemokimab attack upstream inflammatory mediators and posted encouraging Phase 3 data that reduced polyp burden and congestion scores. China’s December 2024 authorization of stapokibart, the first domestically developed biologic, underscores regional acceleration in the sinusitis treatment market. Pharmacoeconomic studies show omalizumab currently offers the most favorable cost-effectiveness ratio in Canada, influencing reimbursement decisions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Penetration of Low-Cost Generics & OTC Decongestants | -0.9% | Global, particularly price-sensitive markets | Short term (≤ 2 years) |

| Rising Antibiotic-Resistance Pressures Curbing Empirical Scripts | -1.1% | Global, with higher impact in developed regions | Medium term (2-4 years) |

| Post-COVID Shifts in Sinonasal Microbiome Dampening Elective Procedure Demand | -0.6% | Global, temporary effect | Short term (≤ 2 years) |

| Shortage of Trained Otolaryngologists in High-Growth Emerging Regions | -0.8% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Penetration of Low-Cost Generics & OTC Decongestants

Generic launches reduce average selling price of azelastine-fluticasone sprays, with U.S. retail erosion exceeding 45% within 12 months of patent expiry.[3]Source: Akash M. Bhat, “Generic Competition for Azelastine-Fluticasone,” pubmed.ncbi.nlm.nih.gov OTC nasal sprays now match prescription efficacy in shortening symptom duration to 6.5 days, adding retail-channel competition. Herbal alternatives such as Sinupret allow delayed antibiotic strategies that trim antimicrobial use by 43.7% in randomized settings. In emerging economies, generics account for over 70% of total scripts, compressing branded margins and pressuring innovators to demonstrate superior outcomes. This price deflation temporarily caps revenue expansion within certain segments of the sinusitis treatment market.

Rising Antibiotic-Resistance Pressures Curbing Empirical Scripts

Guidelines now advocate watchful waiting for uncomplicated acute rhinosinusitis and restrict antibiotics to severe or persistent cases. Meta-analysis in pediatrics shows antibiotics reduce treatment failure by only 41% and risk fostering resistant pathogens. Studies detect multidrug-resistant Klebsiella pneumoniae in postoperative sinus cultures, elevating concern over empirical broad-spectrum usage. Regulators and insurers link reimbursement to antimicrobial stewardship targets, dampening antibiotic volume but opening pathways for rapid diagnostics and targeted agents. This trend moderates growth in the antibiotic-heavy segment of the sinusitis treatment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease: Chronic Sinusitis Drives Market Dominance

Chronic sinusitis controlled 57.02% of sinusitis treatment market share in 2025 thanks to its recurrent profile and higher resource utilization. The segment absorbs biologic spending and revision FESS volumes, underpinning robust revenue streams. Acute sinusitis, while smaller, is projected to expand at a 7.31% CAGR, reflecting better primary-care diagnostics and refined antibiotic protocols. Sub-acute sinusitis serves as the bridge phenotype, often migrating into chronic classification when inadequately resolved.

Chronic disease heterogeneity continues to steer precision medicine. Eosinophilic variants respond strongly to IL-4/IL-13 blockade, whereas non-eosinophilic phenotypes common in Asian populations need alternative pathways. Tissue eosinophilia scoring during surgery now guides postoperative pharmacotherapy, cutting revision risk. Parallel development of biomarkers and next-generation biologics secures long-term growth for the sinusitis treatment market size linked to chronic disease management.

By Drug Class: Antibiotics Lead Despite Analgesic Acceleration

Antibiotics held 42.35% of the sinusitis treatment market size in 2025, driven by the continued burden of bacterial acute exacerbations. However, analgesics are advancing at a 7.85% CAGR as patients and clinicians prioritize symptom control amid antibiotic stewardship pressures. Corticosteroids, especially intranasal, remain critical for inflammation suppression, while antihistamines serve allergic subsets. Emerging modalities, biologics, probiotics, and herbal products introduce diversified revenue pools that temper reliance on volume-driven antibiotic sales.

Surgical modalities sustain high single-digit growth. Image-guided balloon sinuplasty and disposable debriders reduce intraoperative risk and lower postoperative revision rates, pulling new referrals and pushing hospitals to upgrade ENT suites. As AI-enhanced navigation matures, procedural throughput increases, reinforcing device sales in the sinusitis treatment market.

Geography Analysis

North America retained 39.62% of the sinusitis treatment market in 2025 due to early biologic adoption and payer support for minimally-invasive surgery. The September 2024 adolescent dupilumab approval and the June 2025 SONU Band pediatric clearance underscore an innovation-friendly regulatory climate. Balloon sinuplasty delivers USD 2,200 average savings per case compared with traditional FESS, further cementing payer backing. Canada’s rigorous pharmacoeconomic evaluations favor omalizumab as the cost-effective biologic for eligible patients. Mexico’s rising middle class and medical tourism growth broaden procedure and drug uptake, extending North American influence across the sinusitis treatment market.

Asia-Pacific registers the fastest regional CAGR at 8.02%, powered by infrastructure investment and greater awareness of advanced therapies. China demonstrates strong demand for image-guided FESS, showing 100% avoidance of rehospitalization for bleeding and lower overall cost per quality-adjusted life year versus conventional surgery. The December 2024 approval of stapokibart, China’s first indigenous biologic, marks a strategic milestone that improves access and lowers dependence on imported agents. Workforce shortages remain a drag, yet tele-mentoring and robotics partially offset skill gaps, keeping the sinusitis treatment market on a steep trajectory.

Europe shows steady expansion under tight cost-containment regimes. The European Position Paper on Rhinosinusitis supplies unified diagnostic and therapeutic criteria that drive evidence-based utilization. Major markets—Germany, United Kingdom, France—lead biologic uptake, while southern nations accelerate adoption after positive health-technology assessments. Digital health tools support remote follow-up and specialist consultations, widening reach in rural settings and stabilizing growth for the sinusitis treatment market across the continent.

Competitive Landscape

The sinusitis treatment market displays moderate fragmentation, with top pharmaceutical and device players holding overlapping yet differentiated portfolios. Sanofi-Regeneron anchor the biologic segment with dupilumab, now approved for both adult and adolescent CRSwNP populations, and posted head-to-head superiority versus omalizumab in the 2025 EVEREST trial presented at EAACI. Medtronic strengthened its ENT offering through the Intersect ENT acquisition, adding Propel steroid-eluting implants that reduce postoperative adhesions. Stryker leverages an integrated toolkit that spans balloon dilation, navigation, and absorbable implants, supported by real-world economic data that highlights payer savings.

Emerging entrants accelerate innovation. Keymed’s stapokibart introduces a local biologic option for Chinese patients, while Amgen-AstraZeneca’s tezepelumab broadens anti-TSLP coverage after Phase 3 success. Digital and bioelectronic startups, SoundHealth with its FDA-cleared SONU device and Tivic Health’s ClearUP neuromodulation platform, address congestion without drugs, differentiating on safety and adherence.

Olympus’s CELERIS single-use debrider taps into infection-control priorities, giving hospitals a disposables-based cost model. Competitive advantage hinges on proving clinical benefit alongside economic value, forcing incumbents and newcomers alike to pair efficacy data with cost-offset narratives to win formulary acceptance.

Sinusitis Treatment Industry Leaders

Medtronic plc

Cipla Inc.

Dr. Reddy’s Laboratories Ltd.

Stryker Corporation

Sanofi SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Sanofi and Regeneron reported Dupixent outperformed omalizumab across all endpoints in the EVEREST head-to-head CRSwNP study at EAACI, Glasgow.

- November 2024: Amgen and AstraZeneca announced Phase 3 WAYPOINT success for tezepelumab in reducing nasal polyp size and congestion.

- March 2024: FDA approved Xhance (fluticasone propionate) nasal spray for chronic rhinosinusitis without nasal polyps in adults 18 years and older.

Global Sinusitis Treatment Market Report Scope

As per the scope of this report, sinusitis is a condition in which the mucosal lining of the paranasal sinuses becomes inflamed. However, because sinusitis is always accompanied by inflammation of the neighboring nasal mucosa, the term rhinosinusitis is more accurate. Blockage of the sinus ostium, usually the maxillary sinus ostium under the middle turbinate, appears to be the triggering element in acute sinusitis. Sinusitis must be treated well as it can lead to complications like brain abscess and meningitis. The Sinusitis Treatment Market is Segmented by Disease (Acute Sinusitis, Sub-acute Sinusitis, and Chronic Sinusitis), Treatment (Analgesics, Antihistamines, Corticosteroids, Antibiotics, Surgery), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Acute Sinusitis |

| Sub-acute Sinusitis |

| Chronic Sinusitis |

| Drug Class | Analgesics |

| Antihistamines | |

| Corticosteroids | |

| Antibiotics | |

| Others | |

| Minimally-invasive Surgery (Balloon Sinuplasty, FESS) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disease | Acute Sinusitis | |

| Sub-acute Sinusitis | ||

| Chronic Sinusitis | ||

| By Modality | Drug Class | Analgesics |

| Antihistamines | ||

| Corticosteroids | ||

| Antibiotics | ||

| Others | ||

| Minimally-invasive Surgery (Balloon Sinuplasty, FESS) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the global sinusitis treatment market?

The sinusitis treatment market size is USD 2.85 billion in 2026.

How fast is the sinusitis treatment market expected to grow?

It is projected to expand at a 6.05% CAGR through 2031.

Which region will record the highest growth in sinusitis treatments?

Asia-Pacific is forecast to post the fastest CAGR at 8.02% through 2031.

Which therapeutic class is growing fastest within sinusitis care?

Analgesics show the highest projected growth at 7.85% CAGR as patients seek better symptom relief.

Why are biologics important in chronic rhinosinusitis?

Agents like dupilumab reduce polyp size, improve symptoms, and diminish surgery need, providing transformative outcomes for severe cases.

Page last updated on: