Meningococcal Vaccines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

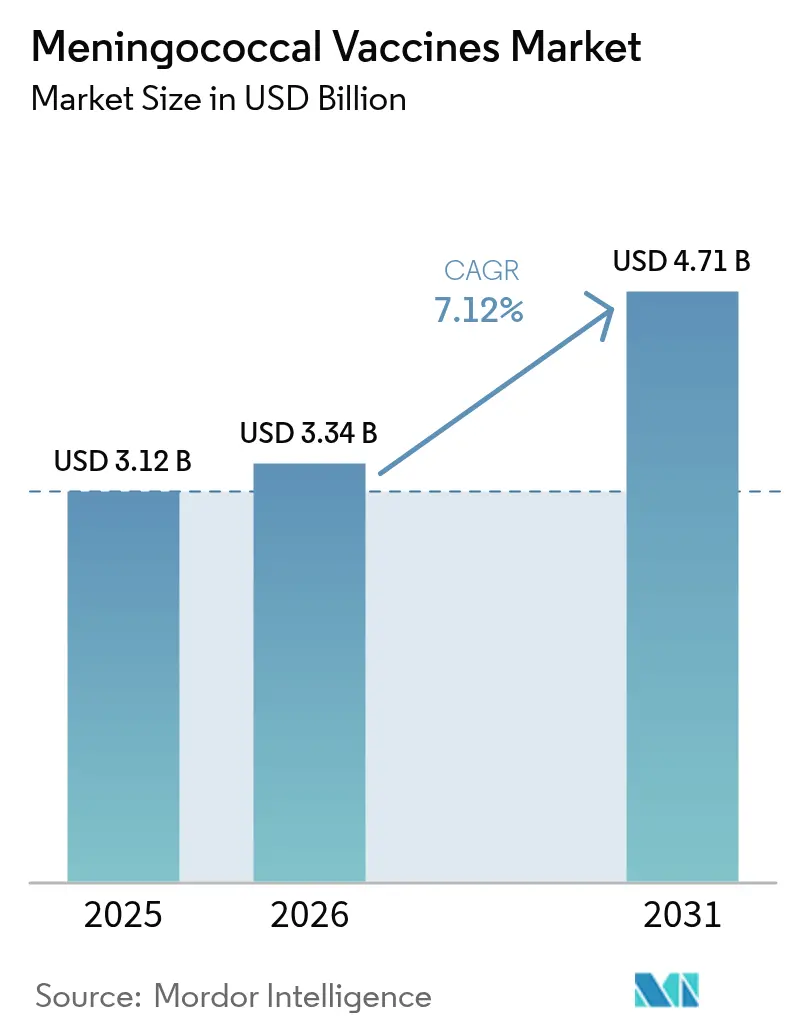

| Market Size (2026) | USD 3.34 Billion |

| Market Size (2031) | USD 4.71 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Meningococcal Vaccines Market Analysis by Mordor Intelligence

Meningococcal vaccines market size in 2026 is estimated at USD 3.34 billion, growing from 2025 value of USD 3.12 billion with 2031 projections showing USD 4.71 billion, growing at 7.12% CAGR over 2026-2031. Pentavalent platforms that combine serogroups A, B, C, W and Y are redefining product strategy, compressing multi-shot schedules into single injections and shifting demand away from older monovalent and quadrivalent brands. GSK registered the first FDA nod for a five-component shot, Penmenvy, in February 2025 [1]GSK, “FDA Approves Penmenvy, the First 5-Component Meningococcal Vaccine,” gsk.com , closely following Pfizer’s Penbraya launch; both approvals have accelerated portfolio realignment among incumbents. Manufacturers now weigh the lure of premium pricing for combination vaccines against the cannibalization of legacy lines. Regionally, North America retains purchasing power, but Asia-Pacific delivers the fastest volume gains on the back of widening national immunization programs and emerging last-mile delivery models such as room-temperature-stable Men5CV in Nigeria. Competitive intensity is rising as biotechnology entrants leverage public-private partnerships and technology transfers to narrow time-to-market.

Key Report Takeaways

- By product type, quadrivalent formulations led with 53.32% of meningococcal vaccines market share in 2025, while bivalent options record the quickest expansion at an 8.01% CAGR through 2031.

- By vaccine type, conjugate technology captured 46.02% of the meningococcal vaccines market size in 2025; combination vaccines register the highest projected CAGR at 8.1% to 2031.

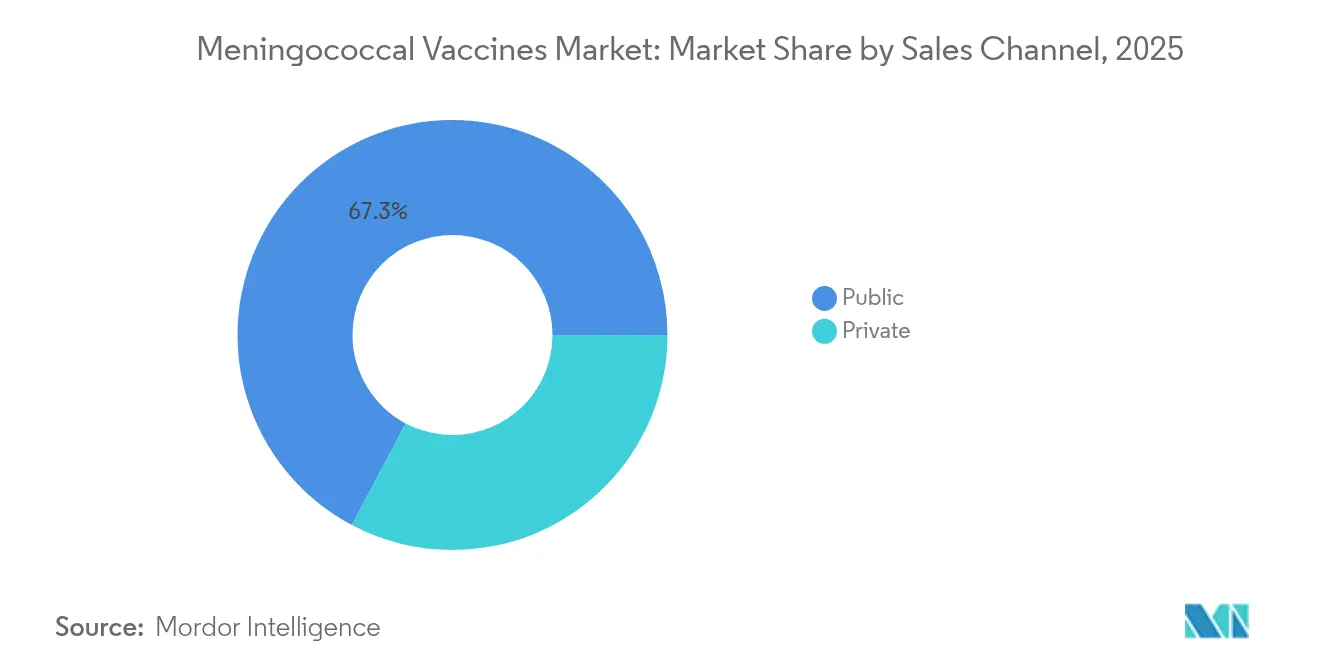

- By sales channel, the public sector commanded 67.25% revenue in 2025, whereas the private segment is projected to grow at an 8.18% CAGR to 2031.

- By age group, children and adults aged ≥2 years held 75.10% of the meningococcal vaccines market size in 2025, but infant programs (0-2 years) advance at an 8.2% CAGR.

- By geography, North America led in 2025 with 40.05% revenue share, yet Asia-Pacific is poised for the highest 8.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Meningococcal Vaccines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising immunization programs & government initiatives | +1.8% | Global, with strongest impact in Asia-Pacific and Africa | Medium term (2-4 years) |

| Increase in public-private partnerships lowering development costs | +1.2% | Global, particularly benefiting low-income countries | Long term (≥ 4 years) |

| Growing incidence of serogroup W & Y outbreaks in high-income nations | +1.0% | North America & Europe | Short term (≤ 2 years) |

| Introduction of multivalent Men5CV & pentavalent conjugate platforms | +1.5% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Room-temperature-stable Men5CV enabling last-mile delivery in Africa | +0.9% | Sub-Saharan Africa, spillover to other tropical regions | Long term (≥ 4 years) |

| mRNA / protein-nanoparticle pipeline accelerating MenB boosters | +0.6% | North America & Europe initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Immunization Programs & Government Initiatives

Government-financed vaccine roll-outs are scaling demand by integrating meningococcal shots into routine schedules and travel requirements. China’s National Immunization Program has moved several WHO-endorsed vaccines, including meningococcal conjugates, into fully funded status, widening access across rural provinces [2]Shu Chen, "Advancing the National Immunization Program in an era of achieving universal vaccine coverage in China and beyond," Infectious Diseases of Poverty, idpjournal.biomedcentral.com. France convened WHO’s first high-level forum on the “Defeating Meningitis by 2030” roadmap in 2024, unlocking new pledges for affordable supply and surveillance harmonisation. Saudi Arabia’s requirement for MenACWY proof among Hajj and Umrah pilgrims continues to stimulate global demand, even though compliance audits show only 54% adherence among foreign travellers. These coordinated programs create predictable tender cycles that allow manufacturers to optimise batch sizes and forecast revenue horizons.

Increase in Public-Private Partnerships Lowering Development Costs

Vaccine developers are increasingly co-funded through alliances that blend academic discovery with industrial scale-up. Serum Institute of India licensed a chimeric protein MenB candidate from the University of Oxford, aiming to supply lower-cost boosters to Gavi-eligible markets [3]Oxford University Innovation, "Serum Institute of India and University of Oxford Strike Landmark Licensing Agreement for Meningitis-B Vaccine," innovation.ox.ac.uk. Gavi’s African Vaccine Manufacturing Accelerator earmarked USD 1.2 billion in 2024 to local production, a shift expected to stabilize long-term supply and reduce lead times. PATH’s collaboration with Serum Institute brought Men5CV to market at roughly USD 3 per dose, well below Western benchmarks, illustrating how risk-sharing compresses end-user prices. These models redistribute R&D exposure, enabling smaller biotechnology firms to advance novel platforms without prohibitive capital outlays.

Growing Incidence of Serogroup W & Y Outbreaks in High-Income Nations

Surveillance data point to a resurgence of serogroups W and Y in the United States and several European countries, driving demand for broader-spectrum conjugates. The CDC logged 422 invasive cases in 2023, the highest national tally in a decade, with serogroup Y ST-1466 disproportionately affecting adults aged 30-60, especially Black individuals with HIV. Virginia’s 36-case outbreak between 2022-2024 carried a 19.4% case-fatality rate, reigniting debate on adult booster recommendations. In Europe, 2022 ECDC data show serogroups Y and W representing 26% of cases, a notable jump from earlier years. These shifts highlight the limitations of legacy monovalent strategies and underscore the commercial urgency for multivalent products.

Introduction of Multivalent Men5CV & Pentavalent Conjugate Platforms

The WHO-prequalified Men5CV and FDA-approved pentavalent conjugates have triggered a new product wave that consolidates protection into a single vial. Nigeria’s nationwide Men5CV rollout in April 2024 served as the first large-scale test of a vaccine covering serogroups A, C, W, X and Y, achieving 96% administrative coverage in priority states. University of Maryland trials demonstrated co-administration safety with infant schedules, a finding that expands use into the high-incidence 9-month cohort. Analysts project Penmenvy sales could reach USD 1.1 billion by 2030, outpacing Pfizer’s Penbraya at USD 606 million, as providers pivot to single-shot regimens. Pentavalent options reduce clinic visits and improve payer economics, widening the competitive moat for early entrants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of cold-chain storage & supply logistics | -1.4% | Global, most severe in tropical and remote regions | Medium term (2-4 years) |

| Stringent regulatory & liability hurdles for novel serogroup combos | -0.8% | North America & Europe primarily | Short term (≤ 2 years) |

| Waning adolescent booster compliance post-COVID vaccine fatigue | -1.1% | Global, particularly in developed countries | Short term (≤ 2 years) |

| Cannibalization risk from pentavalent vaccines on legacy ACWY & B brands | -0.7% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Cold-Chain Storage & Supply Logistics

Full-range refrigeration remains a principal cost driver, especially where ambient temperatures exceed 30 °C. Field studies in Nepal reported the average shipment value per insulated carrier at USD 1,704, with nearly one-third subject to freeze damage during transit. Controlled temperature chain pilots in India cut logistics expense from USD 0.063 to USD 0.026 per dose but demanded capital upgrades and extensive training. Drone-enabled distribution with active thermal containers shows promise yet faces regulatory clearance hurdles and limited payload capacity. Persistent infrastructure gaps translate into higher landed costs and periodic stockouts, constraining timely coverage.

Waning Adolescent Booster Compliance Post-COVID Vaccine Fatigue

Post-pandemic sentiment has dampened booster uptake. A claims review among 16-23-year-olds in the United States revealed MenB series completion at only 56.7% in commercially insured and 44.7% in Medicaid cohorts. Peru’s national survey showed an erosion in schedule adherence from 65.82% in 2018 to 61.77% in 2022, linked to growing risk-benefit scepticism and reduced clinic visits. Providers remain the strongest uptake predictor, yet a study in Turkey found just 81.8% of family physicians routinely recommend meningococcal vaccines owing to cost and knowledge gaps. Sustained hesitancy could flatten adolescent demand curves despite broader label expansions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pentavalent Platforms Challenge Quadrivalent Dominance

Quadrivalent formulations generated 53.32% revenue in 2025, maintaining primacy across adolescent booster programs in North America and Europe. This leadership reflects long-standing clinical familiarity, extensive insurance coverage and robust tender frameworks anchoring the meningococcal vaccines market. Yet bivalent solutions, prized for targeted protection and lower cost, post an 8.01% CAGR through 2031. Pentavalent pipelines represent the fastest-rising “other” category as providers seek single-visit coverage for all five major serogroups.

Momentum around pentavalent approvals marks a structural pivot. Confluences of simplified schedules and broader strain breadth have prompted several states in the United States to reassess school requirements. Early modelling suggests pentavalent uptake could displace nearly 30% of quadrivalent demand by 2028, reshaping revenue distribution inside the meningococcal vaccines market. CanSino Biologics highlighted this shift with RMB 561.7 million (USD 78.5 million) bivalent sales in 2023, a 266% annual rise, signalling how local champions exploit domestic tenders for share gains.

By Vaccine Type: Conjugate Technology Drives Innovation Pipeline

Conjugate products held a 46.02% stake in 2025, underpinned by enduring immunogenicity and herd-immunity benefits that dovetail with paediatric protocols. Combination formats combining conjugate backbones with protein antigens are on a trajectory to post an 8.1% CAGR, opening capacity for higher-margin SKUs within the meningococcal vaccines market size. Polysaccharide shots retain a tactical role in outbreak surges because of cost advantages and quicker release timelines.

Cutting-edge conjugation chemistries now fuse five polysaccharide moieties to mutant diphtheria proteins, preserving antigen integrity while sustaining memory responses for a decade or longer. Men5CV’s room-temperature profile adds a distribution benefit, particularly for Gavi-funded drives in Africa. Outer-membrane vesicle (OMV) and protein-nanoparticle constructs remain developmental but promise thermostability and cross-protection, potentially widening the meningococcal vaccines industry’s future tool kit.

By Sales Channel: Private Markets Accelerate Despite Public Dominance

Government tenders represented 67.25% of 2025 volumes, anchored by UNICEF and Gavi procurement pools that guarantee base-line demand and stabilise pricing. Nonetheless, private demand is expanding at an 8.18% CAGR, supported by wider employer health plans, college matriculation requirements and destination-specific travel advisories. Growth is most evident in urban Asia where affluent parents purchase non-listed pentavalent shots for toddlers, adding incremental volume to the meningococcal vaccines market.

Pricing differentials widen channel stratification: public buyers negotiate unit prices below USD 4 for quadrivalent doses, while private clinics in the United States charge USD 180-210 for the same vial. This contrast finances R&D pipelines yet raises equity debates. Pharmacies and telehealth platforms are entering direct-to-consumer administration, further diversifying access points and sustaining private-channel momentum.

By Age Group: Infant Programs Show Strongest Growth Trajectory

Individuals aged ≥2 years commanded 75.10% of 2025 turnover, reflecting entrenched adolescent mandates and adult travel policies. The meningococcal vaccines market size for infants (0-2 years), however, is projected to climb fastest at an 8.2% CAGR after regulators cleared expanded indications. Sanofi’s MenQuadfi gained FDA approval for infants as young as six weeks in May 2025, positioning it as the only quadrivalent option for this cohort.

Early protection is a critical objective in sub-Saharan Africa and parts of South-East Asia where incidence peaks in the first year of life. Data from University of Maryland show Men5CV co-administration at 9 months achieved non-inferior immunogenicity to standalone dosing, potentially enabling synchronised measles-meningococcal drives. Adult vaccination remains concentrated in high-risk groups—splenectomy patients, complement deficiency cohorts and military recruits—yet pentavalent availability could prompt broader adult booster guidelines.

Geography Analysis

North America generated 40.05% of global revenue in 2025 on the back of universal adolescent scheduling, broad payer coverage and rapid outbreak detection systems. The United States implements a two-dose MenACWY series at 11-12 and 16 years and recommends MenB for high-risk populations; Canada and Mexico track similar approaches with provincial variations. FDA approval of Penmenvy is expected to catalyse formulary reviews and private-payer negotiations, potentially accelerating pentavalent uptake. Recent ST-1466 outbreaks underscore residual vulnerability in older adults, prompting discussions on extending booster age brackets.

Europe displays mature uptake yet dynamic serogroup trends. Surveillance captured 1,149 invasive cases in 2022, of which serogroup B remained dominant at 62%. France’s hosting of WHO’s meningitis summit re-energised regional co-ordination, while Germany’s inclusion of MenB into routine recommendations highlights policy evolution. Travel-linked clusters from Middle East pilgrimages continue to spur demand for quadrivalent boosters at point-of-departure clinics. Reimbursement frameworks remain robust, but incremental growth hinges on integrating pentavalent shots into joint procurement contracts.

Asia-Pacific is the fastest-expanding region at an 8.31% CAGR, driven by China’s policy upgrades, India’s logistic strengthening and Southeast Asian outbreak vigilance. The “meningococcal vaccines market” narrative in the region focuses on equitable access: China’s national plan targets full conjugate coverage by 2028, while Indonesia pilots drone-delivery corridors to remote islands. Domestic producers such as CanSino and Chengdu Institute supply cost-adjusted bivalents and quadrivalents, whereas multinationals prepare local fill-finish lines to sidestep import tariffs. Successful pneumococcal roll-outs provide a replicable blueprint for cross-disease scale-up.

Africa and the Middle East represent sizeable latent demand, with Nigeria’s Men5CV introduction providing proof of concept for thermostable campaigns in the meningitis belt. Gavi, UNICEF and WHO maintain emergency stockpiles, yet funding gaps persist for routine programs outside epidemic-prone corridors. South America records modest growth, constrained by surveillance disparities but buoyed by regional expert consensus on expanding MenACWY coverage, particularly in Brazil and Chile.

Regulatory Landscape

The regulatory environment for meningococcal vaccines is being shaped by faster review and label expansion pathways for higher-valency conjugate and combination products, along with programmatic guidance for outbreak-prone regions. In the United States, the FDA approved GSKs pentavalent Penmenvy (MenABCWY) in February 2025 for ages 10-25, indicating regulator comfort with combined MenACWY and MenB components under a single licensure. The FDA also continues to use BLA supplements to broaden pediatric access for established brands, including expansions for products such as Sanofis MenQuadfi into younger age groups.

In Europe, authorization is centralized through the EMA and European Commission, with post-authorization obligations (including pediatric data submissions under Article 46) influencing lifecycle updates for existing meningococcal vaccines. WHO policy remains an access enabler for low- and middle-income settings: its January 2024 position paper for the African meningitis belt supported use of multivalent conjugates such as Men5CV in routine immunization and mass campaigns, aligning global procurement requirements with broader serogroup coverage and supporting donor-funded introductions.

Competitive Landscape

The meningococcal vaccines market is moderately consolidated. GSK commands a diversified line-up—Bexsero (MenB), Menveo (MenACWY) and Penmenvy—collectively exceeding GBP 1 billion (USD 1.25 billion) in 2024 sales. Pfizer competes with Penbraya and Trumenba, while Sanofi differentiates through MenQuadfi’s expanded infant label. These three account for decent revenue, leaving space for agile regional producers and technology-driven entrants.

Emerging players are leveraging targeted value propositions. Serum Institute’s Oxford-derived MenB candidate aims at low-price-high-volume contracts, while CanSino Biologics capitalises on Chinese provincial tenders. Thermostability remains a frontier: PATH and Serum Institute’s Men5CV can withstand ambient temperatures for up to 12 weeks, slashing cold-chain costs and appealing to donors. mRNA and protein-nanoparticle prototypes from academic spin-outs seek to shorten development cycles and expand strain coverage.

Strategic activity accelerated in 2024-2025. GSK invested in a Belgian pilot plant dedicated to combination vaccine fill-finish lines, and Pfizer announced a phase III head-to-head trial comparing Penbraya with existing MenACWY+MenB co-administration schedules. Licensing deals aimed at region-specific conjugate backbones proliferate, notably between Indonesian state-owned Bio Farma and Korea’s EuBiologics for EuNmCV-5 production.

Meningococcal Vaccines Industry Leaders

-

Novartis AG

-

Pfizer Inc.

-

Sanofi

-

GSK plc

-

Cyrus Poonawalla Group (Serum Institute of India Ltd.)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Pentavalent and broader-coverage strategies are creating whitespace in markets that have historically relied on separate MenACWY and MenB products, particularly where clinics and payers prioritize fewer visits and simplified logistics. The FDA approvals and public-health validation for pentavalent options provide concrete commercialization pathways: GSKs Penmenvy gained FDA approval in February 2025 for ages 10-25, and a CDC MMWR in January 2026 confirmed licensing details, supporting implementation discussions across provider networks. This shift also creates room for lifecycle upgrades to established portfolios, including fully liquid presentations that reduce preparation steps and can improve throughput in immunization settings.

Earlier-in-life protection is another active opportunity as regulators extend labels downward and national programs assess infant scheduling. Sanofi secured FDA approval in 2025 to include infants as young as six weeks for MenQuadfi, expanding the addressable population beyond adolescent and travel-driven demand and strengthening the case for integrating MenACWY protection into routine early-childhood visits. Parallel pipeline work in new modalities (including adenoviral-vectored and self-amplifying mRNA approaches reported in academic and trial-registry sources) points to ongoing efforts to improve strain breadth, dose efficiency, and manufacturing flexibility, which is relevant for both high-income boosters and cost-sensitive public tenders.

Recent Industry Developments

- January 2026: Sanofi and SK Bioscience launched MenQuadfi in South Korea for people aged 6 weeks to 55 years. The launch expands Sanofis reach in an advanced immunization market while leveraging a local partner footprint, strengthening supply and commercial execution beyond North America and Europe.

- May 2025: The US FDA approved Sanofis MenQuadfi for infants as young as six weeks. This broadened age indication increases competitiveness for MenACWY vaccination earlier in life and supports potential inclusion discussions in pediatric schedules where quadrivalent coverage is prioritized.

- November 2024: The European Commission approved a fully liquid, single-vial presentation of GSKs Menveo for individuals from 2 years of age through adulthood. Moving away from reconstitution simplifies administration and can improve clinic workflow, supporting product lifecycle management in mature public and private markets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues from vaccines that prevent invasive meningococcal disease by building active immunity against Neisseria meningitidis. It includes monovalent and multivalent products supplied through public immunization programs and private channels, across all major regions.

Scope exclusions: This sizing excludes antibiotics and other treatments, diagnostic tests, and post-infection care services.

Segmentation Overview

-

By Product Type

- Bivalent

- Quadrivalent

- Others

-

By Vaccine Type

- Polysaccharide Vaccines

- Conjugate Vaccines

- Combination Vaccines

- Other Types

-

By Sales Channel

- Public

- Private

-

By Age Group

- Infants (Aged 0-2 Years)

- Children and Adults (Aged 2 Years and above)

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with mapping demand drivers and policy coverage for meningococcal vaccination by country and age group, then linking those drivers to supply-side availability. We rely on public sources such as immunization schedules and surveillance updates from the CDC, WHO, and ECDC, and we use disease-burden and population series from the World Bank and the UN.

Next, we review vaccine procurement signals and pricing context through government tender portals, national health ministry releases, and customs or trade statistics where relevant. Company annual reports, investor presentations, and peer-reviewed journals help us check product labeling, serogroup coverage (A, B, C, W, Y, and sometimes X), and how planned transitions between older and newer formulations are described. For cross-checking revenues and footprint, we use a paid subscription focused on company financials plus a separate patent database, applied selectively. The sources listed here are not exhaustive, and additional public documents and data points were reviewed during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews are used to pressure-test model assumptions that desk research cannot confirm cleanly, especially around tender timing, coverage expansion, and expected price movement by vaccine type. We speak with vaccine manufacturers, distributors, public health procurement stakeholders, and clinicians, balancing inputs across APAC, EMEA, and the Americas so regional rollout patterns show up in the assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 14% | APAC: 47% |

| Mid tier: 51% | Functional/Unit leaders: 26% | EMEA: 30% |

| Smaller Players: 19% | Managers: 60% | Americas: 23% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs demand from vaccination-eligible populations, schedule recommendations, and country-level uptake, then converts that into doses and value using typical dosing regimens and average selling price bands. Because real uptake differs by age group and country, we adjust the demand pool using indicators such as adolescent coverage rates, infant program adoption, catch-up campaign intensity, and the pace of MenACWY and MenB inclusion in national schedules.

To keep totals realistic, we corroborate results with selective bottom-up approximations, such as supplier revenue splits by region, public tender volumes, and sampled dose price ranges from public procurement documents, then refine totals when gaps emerge. Key inputs tracked in the model include serogroup coverage mix, the share of conjugate versus polysaccharide use, booster frequency assumptions, and the effect of outbreaks on short-term demand. Forecasting uses scenario analysis, with base, faster rollout, and slower uptake paths built from expert views on policy changes, supply availability, and expected price progression. When country-level data is thin, we handle it through proxying with epidemiology and coverage patterns from similar markets, followed by a reasonableness check against regional procurement signals.

Data Validation & Update Cycle

Validation relies on repeated checks that compare model outputs against independent signals, including reported immunization coverage, public purchase announcements, and supplier regional commentary. We review outliers at the country and product-type level, so sudden jumps are tied to a policy change, a tender spike, or a pricing revision rather than left unexplained.

Before sign-off, the work goes through multi-step analyst review, and we recheck assumptions when primary feedback conflicts with desk findings. Reports are refreshed annually, with interim updates when material events occur, such as a new age indication, a major schedule shift, or a large procurement award. Just before delivery, a final pass is completed so clients receive the most current view available at that point in time.

Mordor Intelligence's Meningococcal Vaccines Market Size Compared Against Other Published Estimates

Published market values for meningococcal vaccines can look far apart because studies do not always count the same inputs, even when the titles are similar. Differences usually come from what is treated as a meningococcal vaccine, which year is used as the base, and how demand is connected to immunization schedules and real uptake.

Some external estimates use a wider lens that can include adjacent vaccine revenues and pipeline-led assumptions, which tends to raise the starting value for the current year. For Mordor Intelligence, the value is limited to prophylactic meningococcal vaccines across key serogroups, and it also excludes therapeutics, diagnostics, and post-infection services so the market definition stays aligned with immunization use.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.34 B (2026) | |

| Global Consultancy A | USD 4.05 B (2025) | Uses a different base year and commonly applies earlier ASP scaling tied to new product approvals, which can shift value upward even before adoption becomes visible in schedule uptake and tender timing. |

| Industry Publisher B | USD 4.05 B (2024) | Forecasts from an earlier base year and a faster growth assumption can raise the implied market level, especially when outbreak-driven demand is treated as sustained rather than episodic across countries. |

The spread in the table is mainly explained by base-year choice, how quickly price and uptake are assumed to move, and whether non-vaccine items are indirectly bundled into the revenue view. By keeping the model tied to eligible populations, schedule-driven demand, and observable procurement and coverage signals, we end up with a market size that is easier to trace and replicate.

Key Questions Answered in the Report

What is the current size of the meningococcal vaccines market?

The meningococcal vaccines market stands at USD 3.34 billion in 2026 and is projected to reach USD 4.71 billion by 2031.

Which product segment is growing the fastest?

Bivalent formulations expand at the quickest pace with an 8.01% CAGR, while pentavalent platforms are emerging as the next high-growth niche.

Why is Asia-Pacific the fastest-growing region?

Rapid government-backed immunisation drives, rising healthcare spending and local manufacturing capacity drive the region’s 8.31% CAGR.

How do pentavalent vaccines affect older quadrivalent brands?

Combination shots consolidate protection into one dose, raising cannibalisation risk for existing quadrivalent lines and prompting portfolio shifts.

What are the chief barriers to wider vaccine adoption in low-income settings?

Cold-chain costs, regulatory hurdles for new combinations and post-COVID booster fatigue are the leading constraints, collectively shaving an estimated 3.3 percentage points off CAGR growth potential.

Which companies dominate the competitive landscape?

GSK, Pfizer and Sanofi collectively control decent revenue, while regional players like Serum Institute of India and CanSino Biologics gain share through cost-efficient platforms.

Page last updated on: