Meniscus Repair Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.79 Billion |

| Market Size (2031) | USD 1.49 Billion |

| Growth Rate (2026 - 2031) | 13.49% CAGR |

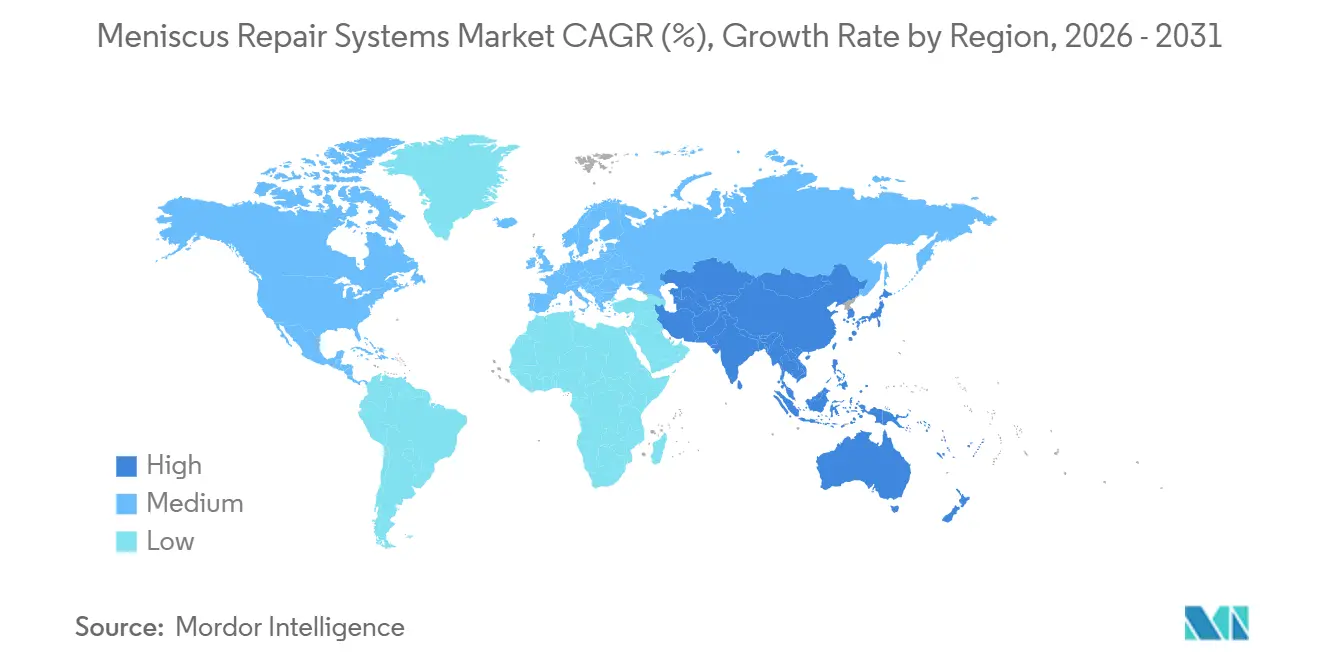

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

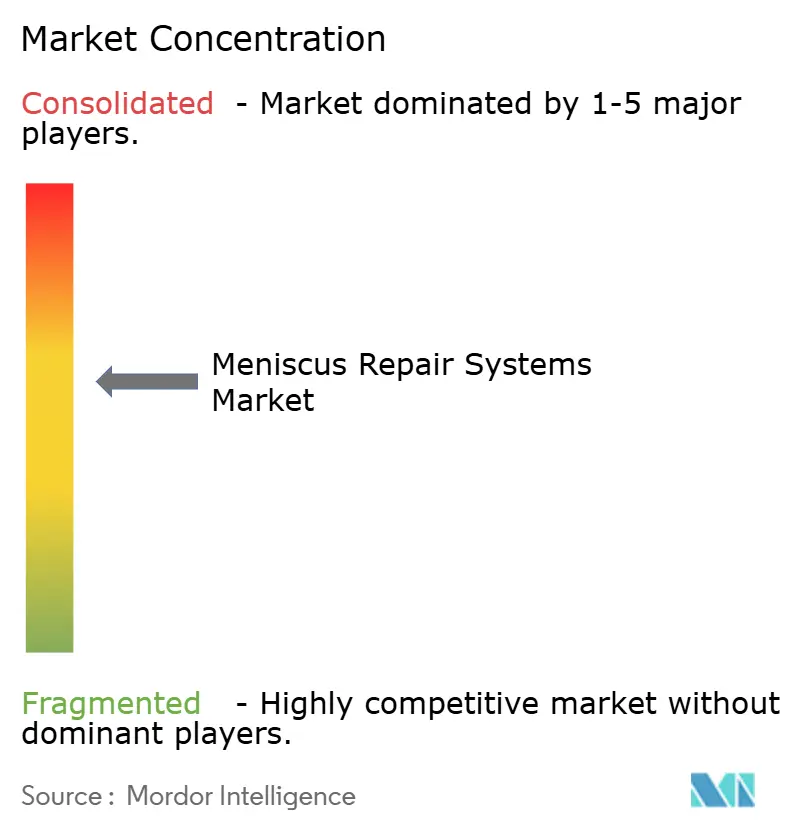

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Meniscus Repair Systems Market Analysis by Mordor Intelligence

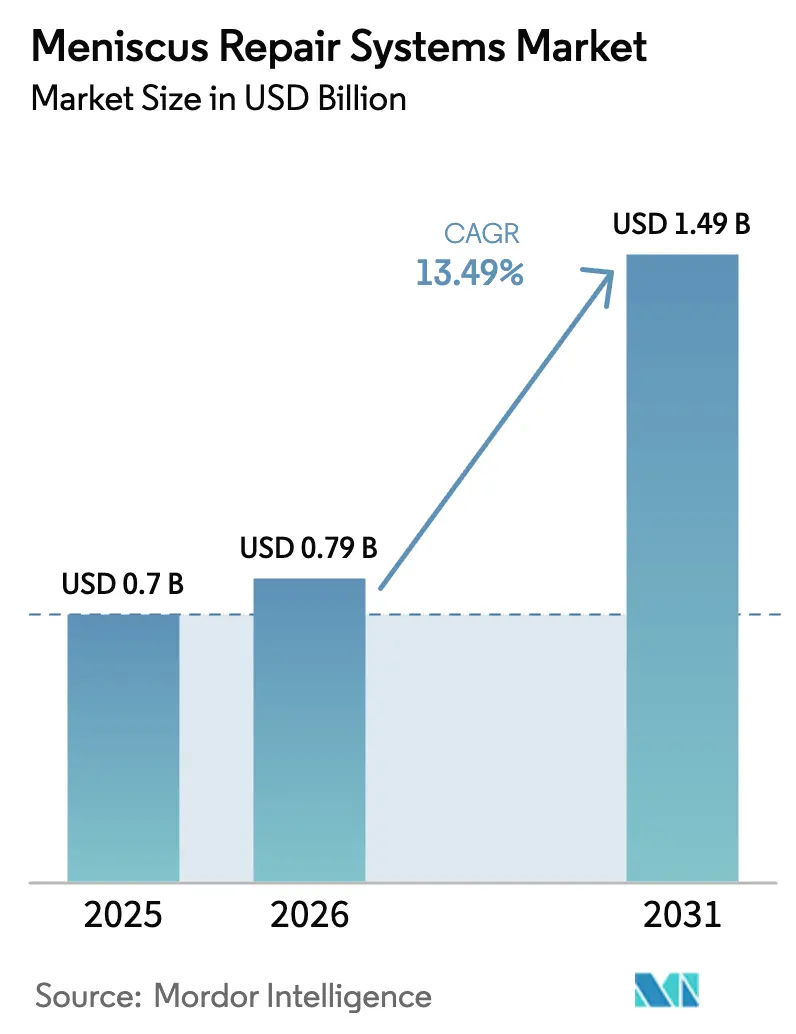

The Meniscus Repair Systems Market size is projected to expand from USD 0.7 billion in 2025 and USD 0.79 billion in 2026 to USD 1.49 billion by 2031, registering a CAGR of 13.49% between 2026 to 2031.

Rapid growth stems from a clinical shift toward tissue-preserving repair that halves osteoarthritis progression, wider adoption of all-inside knotless platforms that lower re-tear risk, and faster device clearances by the U.S. Food and Drug Administration. Increasing sports participation, expanding arthroscopy capacity in outpatient centers, and surgeon education programs are also accelerating procedure volumes. At the same time, group purchasing organizations (GPOs) are exerting downward pricing pressure, and concerns about long-term durability in degenerative tears remain on payer watch lists.

Key Report Takeaways

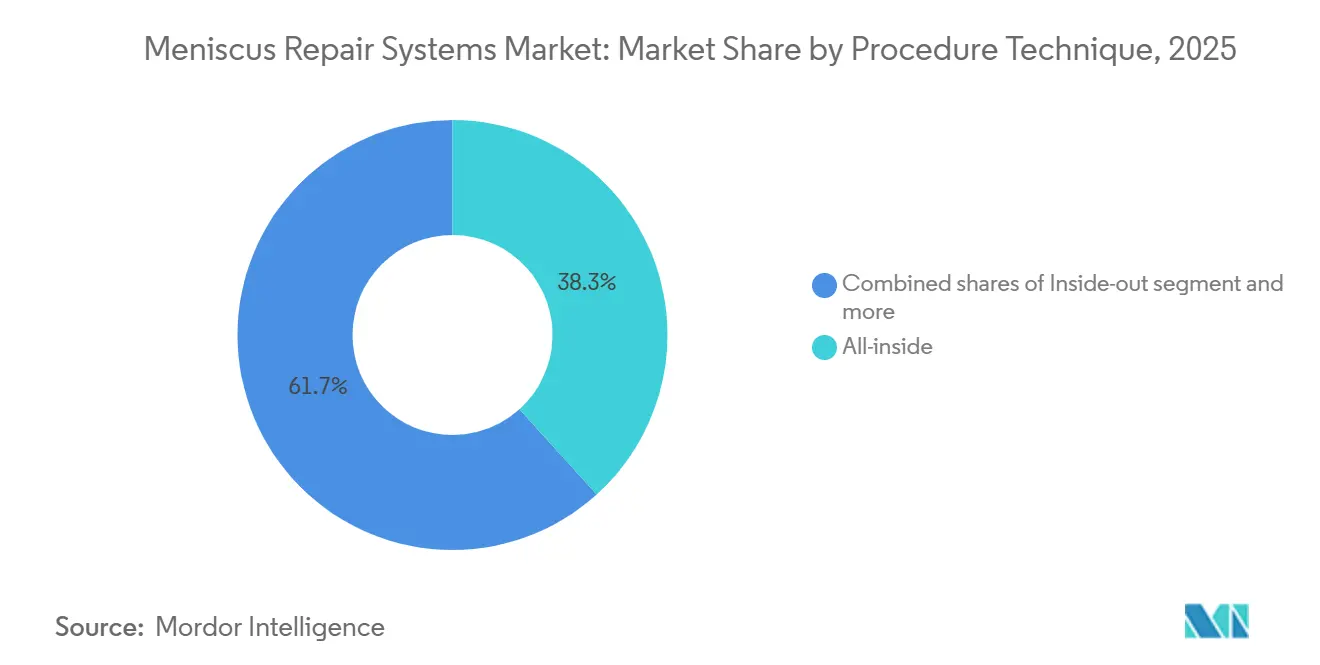

- By procedure technique, all-inside systems captured 38.30% of the meniscus repair systems market share in 2025, and the same segment is forecast to grow at a 15.40% CAGR through 2031.

- By end user, hospitals held 56.18% share in 2025, while specialty orthopedic clinics are projected to expand at a 14.98% CAGR by 2031.

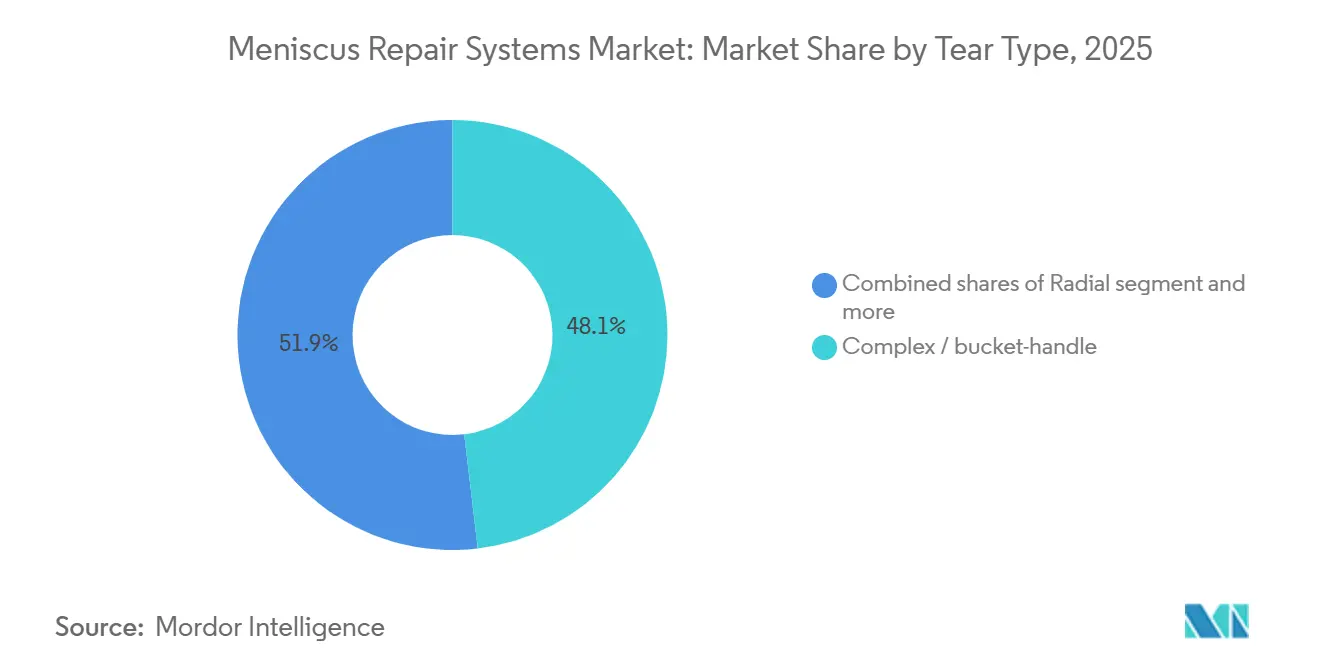

- By tear type, complex and bucket-handle tears accounted for 48.13% share in 2025 and are on track to rise at a 14.68% CAGR through 2031.

- By geography, North America led with 42.13% share in 2025, whereas Asia-Pacific is set to post the fastest 15.12% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Meniscus Repair Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift From Meniscectomy to Repair to Reduce OA Progression and Preserve Function | +3.2% | North America, Western Europe | Medium term (2-4 years) |

| All-Inside And Knotless All-Suture Systems Enable Broader Tear Indications | +2.8% | North America, Asia-Pacific | Short term (≤ 2 years) |

| Increasing Arthroscopy Volumes and Sports Injury Incidence | +2.1% | Asia-Pacific, MEA, South America | Long term (≥ 4 years) |

| Outpatient/ASC Adoption Accelerating Knee Arthroscopy Throughput | +1.9% | North America, Europe, APAC urban centers | Short term (≤ 2 years) |

| Specialized Root-Repair Recognition and Dedicated Systems Expand Addressable Cases | +1.6% | North America, Europe, Japan, South Korea | Medium term (2-4 years) |

| Surgeon Education Ecosystems and Technique Standardization Improve Adoption | +1.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift From Meniscectomy to Repair to Reduce OA Progression and Preserve Function

A 2024 meta-analysis found that meniscal repair reduced the 10-year incidence of radiographic osteoarthritis by 51% compared with partial meniscectomy [1]B.M. Castel et al., “Meniscus Repair Versus Partial Meniscectomy for Traumatic Tears,” BMC Musculoskeletal Disorders, bmcmusculoskeletdisord.biomedcentral.com. The data spurred orthopedic societies in North America and Europe to update their guidelines in favor of repair. Payers are realigning reimbursement, and bundled payment models are rewarding centers that opt for preservation. As value-based contracts proliferate, surgeons are increasingly repairing tears once considered marginal, propelling the meniscus repair systems market.

All-Inside and Knotless All-Suture Systems Enable Broader Tear Indications

Biomechanical studies show that knotless all-suture repairs achieve 98.6% deployment success with only 6.35% failure rates across diverse tears [2]H. Lee et al., “Clinical Outcomes of All-Inside Meniscus Repair Using Knotless Devices,” PubMed, pubmed.ncbi.nlm.nih.gov. FDA clearances for Arthrex FiberTak (March 2025) and GMReis MENISCUS VERSAFLEX (February 2026) cement regulatory confidence. The simplified workflow—fewer portals, no risk of hardware removal, and shorter operative time—has widened indications to include complex, radial, and horizontal cleavage tears, expanding the meniscus repair systems market.

Increasing Arthroscopy Volumes and Sports Injury Incidence

Global sports participation is rising among youth and aging populations, lifting meniscus tear incidence. Elective knee procedure counts surpassed pre-2020 levels by mid-2024, with outpatient centers adding capacity. China, India, and Southeast Asia are opening new arthroscopy suites, and improving MRI access detects tears earlier. These factors are adding steady volume to the meniscus repair systems market.

Outpatient/ASC Adoption Accelerating Knee Arthroscopy Throughput

The Centers for Medicare & Medicaid Services added 302 orthopedic codes to the ASC list in 2026, reinforcing regulatory momentum toward same-day surgery. Managed-care plans now routinely steer beneficiaries to lower-cost ASCs. Device vendors that offer pre-loaded, single-use systems are winning contracts because the format trims room turnover times and reduces reprocessing costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost pressure from GPOs/procurement and bundling with towers/instruments | -1.8% | North America and Europe, emerging in APAC institutional buyers | Short term (≤ 2 years) |

| Long-term repair failure/rehab burden in complex/degenerative tears | -1.4% | Global, with heightened scrutiny in value-based care markets | Medium term (2-4 years) |

| EU MDR-driven product withdrawals and intermittent device availability in Europe | -1.2% | Europe core, spillover to markets requiring CE Mark reciprocity | Short term (≤ 2 years) |

| Biomechanical/chondral-risk concerns for certain implant constructs and techniques | -0.9% | Global, with heightened regulatory focus in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost Pressure From GPOs, Procurement, and Bundling with Towers/Instruments

GPOs now influence more than USD 250 billion in U.S. hospital spending and negotiate double-digit discounts by bundling repair devices with arthroscopy towers. Mid-tier suppliers with narrow portfolios face margin compression or exclusion from formularies. ASCs, operating on lean budgets, prefer single-use kits that minimize reprocessing costs but increase manufacturing costs. These dynamics temper near-term pricing power in the meniscus repair systems market.

Long-Term Repair Failure/Rehab Burden in Complex/Degenerative Tears

Re-tear rates can exceed 20% in degenerative or multi-plane lesions, triggering revisions that strain bundled payment models. Rehabilitation requires up to 6 months of restricted loading, which deters low-demand patients. Payers are scrutinizing indications, and some borderline cases revert to partial meniscectomy, limiting the total addressable meniscus repair systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Procedure Technique: Knotless Platforms Simplify Workflow

All-inside systems dominated segment revenue with 38.30% of the meniscus repair systems market size in 2025 and are growing at a 15.40% CAGR. Knotless all-suture constructs eliminate hardware complications and require only standard anteromedial and anterolateral portals, reducing operative time. Inside-out methods retain a niche among academic surgeons citing marginally higher ultimate load-to-failure values, yet share is eroding as cadaveric data show biomechanical parity. Outside-in techniques, once preferred for anterior horn tears, are losing traction because all-inside devices can treat the same pathology through fewer incisions. Root repair, a subset tracked separately, is the fastest-advancing micro-segment; dedicated pull-out systems cleared in 2024-2025 have made fixation reproducible. Hybrid repairs that pair sutures with compression implants or biologic scaffolds are entering early adoption, targeting revision or poor-quality tissue cases and adding premium price layers to the meniscus repair systems market.

Market adoption is reinforced by surgeon education, virtual-reality simulation, and design enhancements such as self-punching tips that remove pre-drilling steps. Manufacturers are packaging implants in sterile, single-use trays aligned with ASC workflows. The interplay of reliability, shorter learning curves, and throughput gains keeps all-inside devices at the center of capital planning for hospitals and surgery centers alike, securing their lead within the meniscus repair systems market.

By End User: Outpatient Channels Capture Throughput Gains

Hospitals accounted for 56.18% of the meniscus repair systems market in 2025, as they manage polytrauma and revision cases that require overnight monitoring. However, specialty orthopedic clinics are expanding at a 14.98% CAGR, driven by payer incentives for same-day surgery and lower facility fees. CMS’s 2026 expansion of ASC-covered orthopedic codes unlocked a larger pool of reimbursable cases, and Medicare Advantage penetration above 50% channels more beneficiaries to outpatient sites. Physician-owned clinics apply bundled pricing attractive to self-pay and high-deductible patients, and they favor knotless, pre-loaded devices that cut sterilization steps.

Hospitals respond by bundling repair systems with arthroscopy towers and imaging packages in multi-year tenders, leveraging their volume to extract discounts. Yet every meniscus repair systems industry forecast shows clinics increasing share because their cost profile, nimble scheduling, and newer infrastructure resonate with surgeons and payers. Manufacturers must therefore balance two divergent channels—high-volume hospital networks that prize portfolio breadth and cost, and agile outpatient centers that demand speed, simplicity, and single-use formats.

By Tear Type: Complex Patterns Fuel Premium Solutions

Complex and bucket-handle tears represented 48.13% of procedures in 2025 and grew at a 14.68% CAGR as surgeons repair cases once considered suitable only for meniscectomy. Vertical longitudinal tears remain a stable baseline, still often treated with inside-out or contemporary all-inside methods. Radial lesions move into mainstream repair via circumferential suture constructs that restore hoop stress. Horizontal cleavage tears lag due to higher re-tear risk, but biologic scaffolds and augmentation devices validated in 2024-2025 trials may improve outcomes.

Root tears, though a smaller count, post the highest growth rate in the segment. Dedicated transtibial pull-out systems restore meniscal extrusion, and insurance coverage is widening after publication of favorable contact mechanics studies in 2025. As surgeons refine MRI diagnostic criteria, the identification of root avulsions increases, expanding the market share of root-specific meniscus repair devices. The shift toward more complex patterns underpins higher average selling prices because these repairs often require multiple sutures or hybrid implants.

Geography Analysis

North America commanded 42.13% of the meniscus repair systems market in 2025, driven by high arthroscopy penetration, broad sports participation, and the world's fastest regulatory cycle. The FDA cleared multiple next-generation systems in 2025-2026, giving regional surgeons early access to knotless and root-specific technologies. ASC migration is well advanced; payers favor lower-cost settings and bundled payments, a structural driver that continues to lift procedure volumes and sustain premium pricing for pre-loaded kits.

Europe’s growth is steadied by robust surgeon training networks and universal coverage, but faces friction from Medical Device Regulation timelines averaging 2.5 years [3]European Federation of National Associations of Orthopaedics and Traumatology, “MDR Survey Report,” efort.org. Device withdrawals due to certification backlog create intermittent supply gaps that favor incumbents with deep regulatory resources. Nonetheless, Germany, the United Kingdom, and France remain high-value markets where well-maintained registries furnish long-term data supporting repair, anchoring demand even as pricing pressure from centralized tenders intensifies.

Asia-Pacific is the fastest-growing region, posting a projected 15.12% CAGR. China streamlined Class III orthopedic approvals, encouraging both multinationals and local firms to launch cost-matched versions of all-inside platforms. India benefits from rising insurance coverage and government investment in tier-2 city surgical infrastructure. Japan and South Korea, already saturated with advanced arthroscopy capacity, are early adopters of root-specific and hybrid repairs, while Australia’s sports culture sustains steady volume. Middle East & Africa and South America remain nascent but gain traction as private hospitals in the Gulf Cooperation Council, Brazil, and Argentina install modern arthroscopy suites.

Competitive Landscape

The meniscus repair systems market is moderately consolidated. Arthrex, Smith+Nephew, Stryker, and DePuy Synthes leverage broad portfolios, bundled capital equipment, and surgeon education programs to safeguard share. Each is layering biologics, scaffolds, and circumferential compression add-ons that command premium pricing and open the door to revision indications. Zimmer Biomet’s USD 177 million acquisition of Monogram Technologies in 2025 signals its intent to integrate robotics into soft-tissue workflows, although the initial focus remains on arthroplasty.

Disruptors challenge incumbents on agility and cost. Arcuro Medical’s SuperBall platform, backed by its 2025 Series A raise, surpassed 7,000 clinical uses with 98.6% deployment success and no hardware complications. Native Orthopaedics, Healthium Medtech, and BIOTEK target Asia-Pacific and Latin America with lower-priced, easy-to-deploy kits that leverage surgeons' familiarity with all-inside workflows. Technology diffusion is accelerated by virtual reality, cadaveric workshops, and open-access technique videos that shorten adoption curves for mid-volume community surgeons, broadening the user base of the meniscus repair systems market.

Price competition intensifies as GPOs bundle tenders across consumables, and ASCs favor single-use kits over reusable inside-out sets. Suppliers without tower or shaver portfolios must partner or face exclusion. Yet innovation headroom remains, especially in pediatric indications, degenerative menisci, and biologic augmentation areas where no dominant solution has emerged, leaving room for next-wave entrants.

Meniscus Repair Systems Industry Leaders

Arthrex

Smith+Nephew

Stryker Corporation

Johnson & Johnson

Zimmer Biomet

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The FDA cleared GMReis MENISCUS VERSAFLEX, a knotless all-inside system with a single-handed delivery handle, positioning the Brazilian firm to compete in high-throughput U.S. ASCs.

- February 2026: Arthrex launched TightRope SB, extending its tensionable suture platform into ACL reconstruction and signaling a portfolio approach across knee soft-tissue fixation.

- July 2025: Zimmer Biomet closed the Monogram Technologies acquisition for USD 177 million, adding robotic planning tools that could migrate into arthroscopy suites.

Global Meniscus Repair Systems Market Report Scope

As per the scope of the report, meniscus repair systems are advanced arthroscopic tools used by surgeons to repair torn knee cartilage rather than removing it. The primary goal is to "save the meniscus" to preserve the knee’s natural shock absorption and prevent early-onset osteoarthritis.

The meniscus repair systems market is segmented by procedure technique, end users, tear type, and geography. According to the procedure technique, the market is segmented into all-inside, inside-out, outside-in, meniscal root repair, and hybrid/augmented repairs. By end users, the market is segmented into hospitals, ambulatory surgical centers (ASCs), and specialty orthopedic clinics. By tear type, the market is segmented into radial, vertical longitudinal, horizontal cleavage, complex / bucket-handle, and root tears. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| All-inside |

| Inside-out |

| Outside-in |

| Meniscal root repair |

| Hybrid/augmented repairs |

| Hospitals |

| Ambulatory Surgical Centers (ASCs) |

| Specialty Orthopedic Clinics |

| Radial |

| Vertical longitudinal |

| Horizontal cleavage |

| Complex / bucket-handle |

| Root tears |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Procedure Technique | All-inside | |

| Inside-out | ||

| Outside-in | ||

| Meniscal root repair | ||

| Hybrid/augmented repairs | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers (ASCs) | ||

| Specialty Orthopedic Clinics | ||

| By Tear Type | Radial | |

| Vertical longitudinal | ||

| Horizontal cleavage | ||

| Complex / bucket-handle | ||

| Root tears | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is demand for meniscus repair devices growing between 2026 and 2031?

The meniscus repair systems market is forecast to grow at a 13.49% CAGR over 2026-2031, nearly doubling in value during that span.

Which procedure technique holds the largest share today?

All-inside knotless systems led with 38.30% share in 2025 due to their simplified workflow and hardware-free design.

Why are outpatient centers important for future sales?

Ambulatory surgical centers prefer single-use, pre-loaded kits that shorten room turnover time, and procedure migration to these sites is expanding device demand at a double-digit rate.

What is driving rapid adoption in Asia-Pacific?

Faster regulatory approvals, rising sports injuries, and investments in arthroscopy infrastructure are propelling a projected 15.12% CAGR for the region through 2031.

Page last updated on: