Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 55.7 Billion |

| Market Size (2031) | USD 114.09 Billion |

| Growth Rate (2026 - 2031) | 15.41% CAGR |

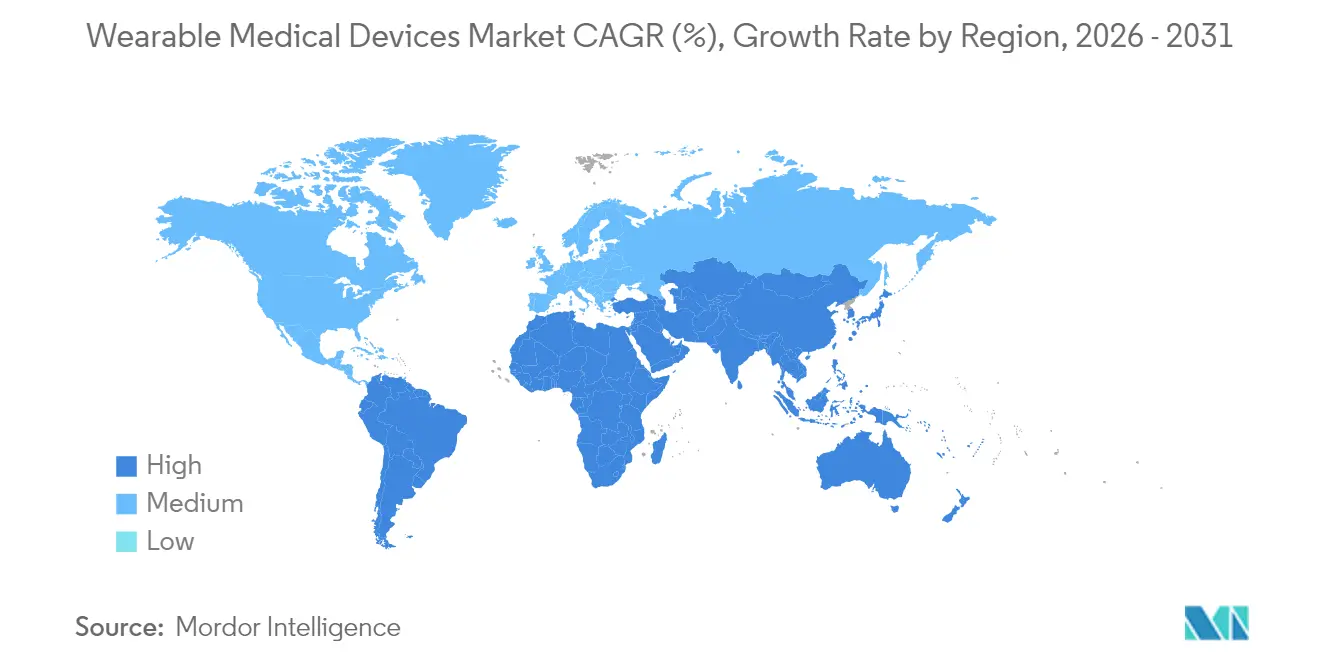

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

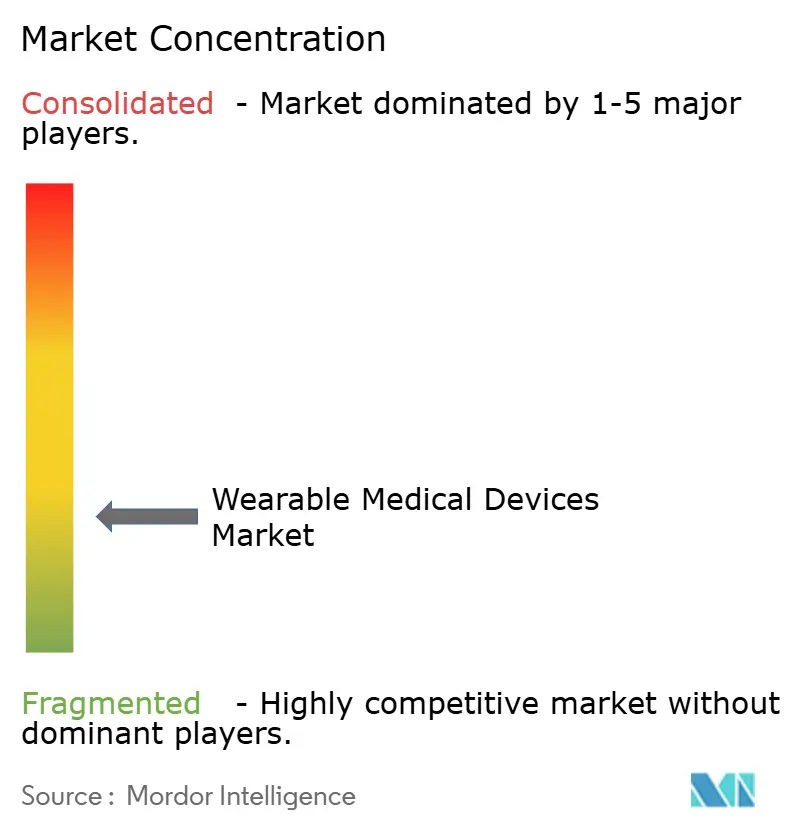

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wearable Medical Devices Market Analysis by Mordor Intelligence

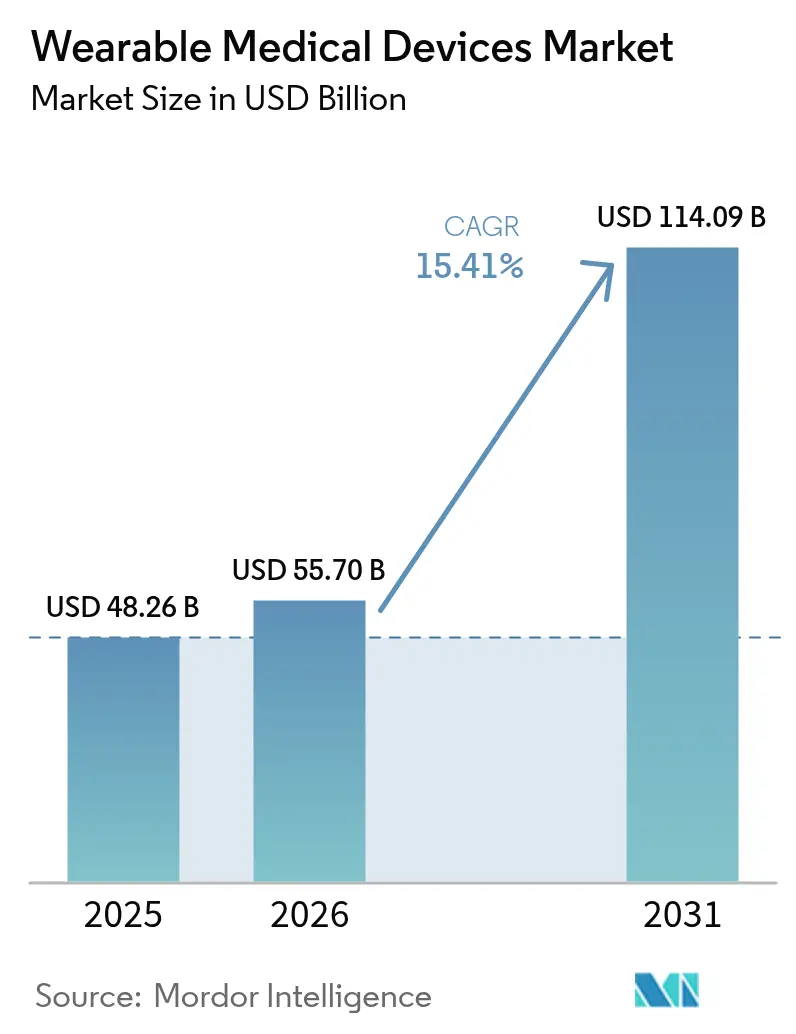

The wearable medical devices market size in 2026 is estimated at USD 55.7 billion, growing from 2025 value of USD 48.26 billion with 2031 projections showing USD 114.09 billion, growing at 15.41% CAGR over 2026-2031. Growth accelerates as regulatory bodies create fast-track pathways for connected diagnostics and expand Medicare reimbursement that recognizes wearable data within clinical decision support. Continuous innovation in biosensors, battery miniaturization, and cloud interoperability strengthens clinical adoption, while consumer-tech ecosystems such as Apple HealthKit amplify user engagement. Strategic partnerships between traditional med-tech firms and software leaders unlock new intervention-capable product lines, and Asia-Pacific manufacturing clusters support lower production costs that enable wider geographic reach. Cyber-security mandates and physician skepticism about consumer-grade accuracy temper momentum, yet clearer regulatory guidance and payer acceptance continue to translate pilot projects into broad hospital programs.

Key Report Takeaways

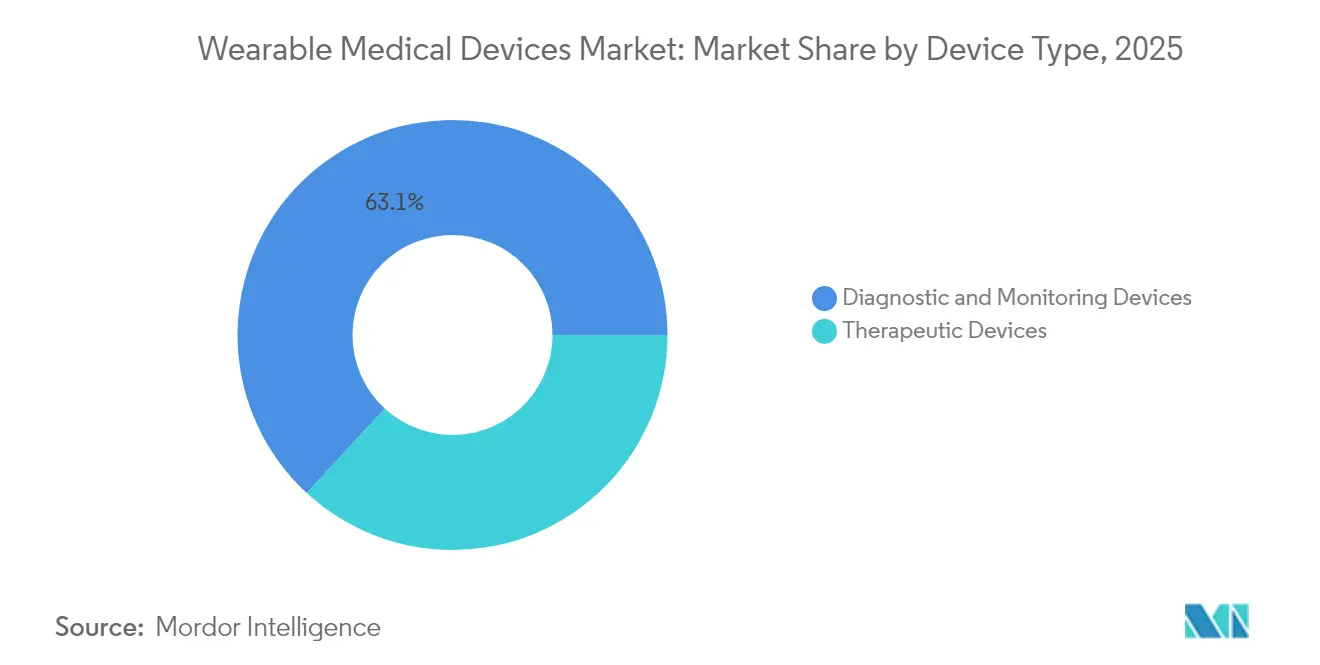

- By device type, diagnostic and monitoring devices held 63.15% of the wearable medical devices market share in 2025; therapeutic devices are poised to grow at a 15.72% CAGR through 2031.

- By age group, adults aged 18-60 commanded 61.02% share of the wearable medical devices market size in 2025, while the under-18 cohort is set to expand the fastest at a 16.18% CAGR to 2031.

- By distribution channel, offline prescriptions and pharmacy sales captured 54.05% revenue in 2025; online channels are projected to rise at a 15.60% CAGR owing to direct-to-consumer models.

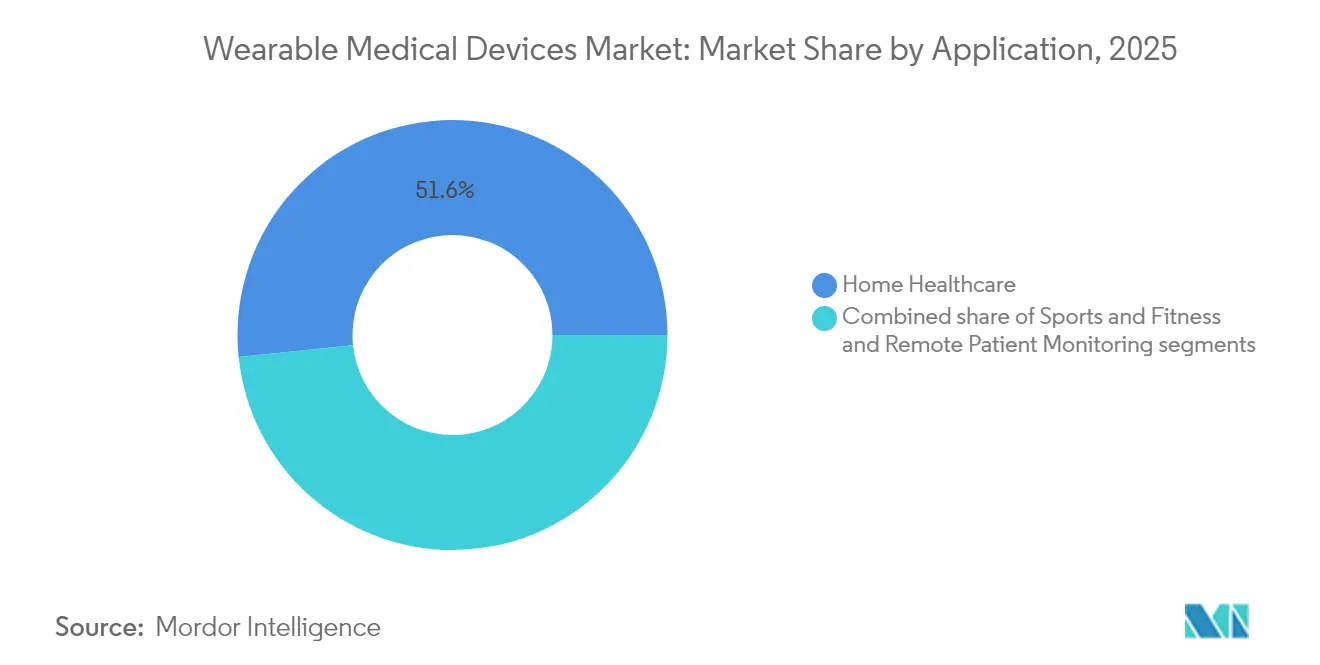

- By application, home healthcare retained 51.63% share of the wearable medical devices market size in 2025, whereas sports and fitness applications are advancing at a 15.84% CAGR.

- By end-user, consumers dominated with 63.58% share in 2025 as hospitals accelerate adoption under new remote-patient-monitoring reimbursement codes.

- By geography, North America led with 34.12% revenue share in 2025, yet Asia-Pacific is forecast to be the fastest-growing region at a 16.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Wearable Medical Devices Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic diseases & home-healthcare demand | +3.5% | Global, accelerated in aging populations | Long term (≥ 4 years) |

| Increasing adoption of AI-enabled biosensors for disease-specific monitoring | +3.2% | Global; early gains in North America & EU | Medium term (2-4 years) |

| Growing reimbursement for remote patient-monitoring programs | +2.8% | North America core; expanding to EU & APAC | Short term (≤ 2 years) |

| Integration with consumer-tech ecosystems boosting user engagement | +2.4% | North America & EU, expanding globally | Medium term (2-4 years) |

| Miniaturization of battery technology lowering form-factor constraints | +2.1% | Global, led by Asia-Pacific hubs | Long term (≥ 4 years) |

| Regulatory fast-track pathways for connected devices | +1.8% | North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases & Home-Healthcare Demand

Population aging and value-based care reimbursement accelerate chronic-disease programs that rely on continuous monitoring to reduce unplanned admissions. Commercial continuous glucose monitors such as Abbott’s Freestyle Libre allow diabetes patients to self-manage while providing clinicians with real-time trend data. Governments promote “hospital-at-home” models that require validated biosensors for round-the-clock vitals, making the wearable medical devices market essential to cost containment. Early anomaly alerts improve therapeutic outcomes and lower emergency department utilization. Asia-Pacific, where the elderly population rises fastest, demonstrates strong demand for fall-detection and cardiac-rhythm patches. These structural forces underpin a long-run uplift of roughly 3.5 percentage points in projected CAGR.

Increasing Adoption of AI-Enabled Biosensors for Disease-Specific Monitoring

AI embedded in flexible electronics shifts wearables from generic wellness trackers to diagnostic platforms capable of 98% arrhythmia-detection sensitivity in FDA-cleared algorithms. Nanowear’s SimpleSense-BP captures dozens of biomarkers on a textile substrate to deliver clinical-grade blood-pressure readings. Edge-computing designs from the University of Hong Kong process data locally, preserving privacy and cutting cloud latency. Machine learning refines photoplethysmography to near-clinical accuracy for SpO₂ and blood pressure. Predictive analytics flag exacerbations hours before symptomatic onset, transitioning care paradigms from reactive to proactive. These capabilities raise physician confidence and spur procurement across cardiology and neurology units.

Growing Reimbursement for Remote Patient-Monitoring Programs

CMS expanded CPT codes 99453, 99454, 99457, and 99458 to compensate clinicians for reviewing remotely generated physiologic data, transforming pilots into nationwide rollouts. The 2025 Medicare Physician Fee Schedule further adds allowances for digital mental-health therapeutics[1]Centers for Medicare & Medicaid Services, “Calendar Year 2025 Medicare Physician Fee Schedule Final Rule,” Centers for Medicare & Medicaid Services, cms.gov, enlarging the addressable scope of the wearable medical devices market. Compliance rules that mandate at least 16 data transmissions per-30 day period stimulate constant patient engagement and higher device utilization. Private insurers echo CMS policies, accelerating commercial coverage. Hospitals encountering staffing shortages deploy wearables to monitor discharged patients, capturing actionable data streams without on-site resources. Reimbursement removes a cost barrier that had historically limited scale.

Integration with Consumer-Tech Ecosystems Boosting User Engagement

Health-data frameworks such as Apple HealthKit and Google Fit allow certified devices to synchronize seamlessly with smartphones, enabling patients to visualize progress alongside fitness metrics. Unified dashboards lower behavioral-change friction and drive adherence[2]Athanasios A. Armoundas, “Data Interoperability for Ambulatory Monitoring of Cardiovascular Disease,” Circulation: Genomic and Precision Medicine, ahajournals.org in chronic-care pathways. Developers leverage standardized APIs to reduce integration effort. Collaboration between Dexcom and Oura demonstrates the fusion of medical-grade glucose telemetry with lifestyle insights, yielding a holistic metabolic-health platform. Combined ecosystems extend device lifecycles and open subscription revenue for analytics services. Improved engagement translates into higher data fidelity, which clinicians use to titrate therapies more precisely.

Restraints Impact Analysis of Wearable Medical Devices Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security & data-privacy compliance costs | -1.8% | Global; stricter in EU under GDPR | Short term (≤ 2 years) |

| Fragmented device-data standards hindering interoperability | -1.5% | Global; acute in multi-vendor settings | Medium term (2-4 years) |

| Low physician trust in consumer-grade data accuracy | -1.2% | North America & EU | Medium term (2-4 years) |

| Battery-longevity and e-waste concerns | -0.9% | Global; environmental regulations in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security & Data-Privacy Compliance Costs

Healthcare ranks among the most targeted sectors for ransomware, prompting regulators to tighten requirements. The FDA now mandates software bill-of-materials disclosures and lifecycle patch plans[3]Healthcare Information and Management Systems Society, “Advancing Medical Device Cybersecurity Beyond Compliance: Managing Risk Governance,” HIMSS, himss.org in pre-market submissions, adding as much as USD 1 million in extra development outlays for complex wearables. EU GDPR rules require explicit consent and right-to-forget protocols, forcing vendors to invest in encryption, key management, and audit trails. Smaller innovators, though technically agile, often encounter capital constraints when meeting enterprise-grade security benchmarks. Delays in certification can defer commercialization and erode competitive positioning.

Fragmented Device-Data Standards Hindering Interoperability

Clinical value arises when wearable streams integrate into electronic health records, yet proprietary protocols and inconsistent adoption of ISO/IEEE 11073 generate interface silos. Hospitals juggling multi-vendor fleets must license middleware or develop custom connectors, raising the total cost of ownership. The IEEE WAMIII program[4]IEEE Standards Association, “Wearable and Medical IoT Interoperability Initiative (WAMIII),” IEEE Standards Association, standards.ieee.org advances a common schema for medical IoT, but deployment remains uneven across global suppliers. Until industry convergence materializes, providers commit to a smaller vendor set to minimize integration risk, which limits open-market competition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Wearable Medical Devices Market Segment Analysis

By Device Type:

Diagnostics Lead, Therapeutics AccelerateDiagnostic and monitoring devices accounted for 63.15% of the wearable medical devices market size in 2025, buoyed by widespread heart-rate, blood-pressure, and continuous glucose monitors that satisfy reimbursable chronic-care pathways. The segment’s leadership reflects mature sensor accuracy and broad regulatory clearances. Vital-sign patches remain preferred in cardiology wards, while overnight oximetry wearables support sleep-apnea screening. Closed-loop glucose systems received strong uptake after CMS broadened coverage, anchoring continued growth across endocrinology departments.

Therapeutic wearables, although smaller today, are advancing at a projected 15.72% CAGR as form factors evolve from passive patches to active drug-delivery or neuromodulation devices. Heat-therapy pads equipped with AI-guided exercise libraries illustrate convergence between physiotherapy and consumer convenience. Implantable EEG monitors such as Epiminder’s Minder extend continuous seizure tracking outside clinical settings, signalling the market’s shift toward intervention. These breakthroughs underscore how the wearable medical devices market size for therapeutics will expand markedly through 2031 as algorithms personalize dosage or stimulus intensity in real time.

By Age Group:

Youth Adoption Outpaces DemographicsAdults aged 18-60 represented 61.02% of the wearable medical devices market share in 2025, driven by chronic-disease incidence in working populations and employer wellness incentives. Devices balance lifestyle insights with FDA-cleared metrics, satisfying both preventive health and clinical monitoring. Seniors embrace simplified user interfaces and fall-detection smart clothing that embed motion sensors in natural fabrics, boosting compliance among less tech-savvy users.

Pediatric adoption, though smaller, carries a 16.18% forecast CAGR. FDA clearance for the Sonu Band, a drug-free nasal-congestion therapy for children over 12, exemplifies regulatory openness to child-specific designs. Parents value non-invasive vitals patch kits that transmit alerts to smartphones, reducing clinic visits. Gaming-style feedback and colorful form factors entice younger users, while school tele-health pilots showcase early success. Taken together, youth-focused innovation enlarges the wearable medical devices market size in segments traditionally underserved by medical technology.

By Distribution Channel:

Digital Transformation AcceleratesOffline medical-supply chains—hospital pharmacies, durable medical-equipment distributors, and specialty clinics—captured 54.05% of the wearable medical devices market size in 2025, reflecting physician-led prescribing and insurance billing workflows. Clinician facilitation remains critical for complex devices such as closed-loop insulin pumps that demand professional training. Hospital purchasing committees prioritize suppliers with strong post-market surveillance support and cybersecurity credentials.

Conversely, online marketplaces are predicted to grow at 15.60% CAGR as manufacturers leverage e-commerce storefronts and tele-health partnerships. Direct-to-consumer fulfillment abbreviates lead times and offers subscription bundles that include sensor replenishment and cloud analytics. Hybrid “click-and-collect” models allow consumers to compare products digitally yet finalize covered transactions through provider networks, creating omnichannel cohesion. Expansion of virtual-care reimbursement incentivizes clinicians to remotely prescribe wearables, strengthening the role of online channels in the wearable medical devices market.

By Application:

Healthcare Dominance, Fitness ConvergenceHome healthcare held 51.63% of the wearable medical devices market share in 2025 as payers reward post-discharge virtual wards that rely on continuous vitals to avoid readmissions. Remote patient-monitoring dashboards integrate real-time alerts into nursing workflows, protecting hospital capacity. Certified devices such as single-lead ECG patches enable early detection of arrhythmias during recovery.

Sports and fitness products, however, are advancing at a 15.84% CAGR through 2031, spurred by advanced biomechanics analytics previously reserved for elite athletes. Photonic sensors embedded in smart rings evaluate recovery readiness, and pressure insoles quantify gait asymmetry to prevent overuse injuries. As these consumer-first devices achieve clinical validation, fitness and medical functions converge. This overlap enlarges the wearable medical devices market share claimed by multi-function platforms that serve both wellness and therapeutic endpoints.

By End-User:

Consumer Dominance, Clinical IntegrationConsumers accounted for 63.58% of the wearable medical devices market share in 2025, with smartphones acting as central hubs that display actionable dashboards and share reports with physicians. Insurance plans begin subsidizing FDA-listed wearables for diabetes and cardiac rehabilitation, reinforcing mass-market penetration. Mobile app updates push algorithm improvements without hardware changes, extending product lifecycles.

Hospitals and clinics deploy enterprise deployments of continuous monitoring patches to minimize nurse workloads and track surgical recovery. Integration with electronic health records via HL7 FHIR supports automated risk stratification. Long-term-care facilities use geofencing wristbands to reduce wandering incidents among dementia residents. This clinical uptake augments consumer momentum, embedding the wearable medical devices industry more deeply into every layer of the care continuum.

Geography Analysis

North America Wearable Medical Devices Market

North America generated 34.12% of global revenue in 2025 owing to robust reimbursement frameworks and streamlined FDA pathways that hasten commercialization. Uptake of CMS-approved remote patient-monitoring codes encourages hospitals to distribute certified sensors at discharge, driving further penetration across primary-care networks. U.S. tech giants foster vibrant developer ecosystems that enrich device functionality with third-party applications. Canada scales similar models through provincial tele-health mandates, while Mexico leverages cross-border supply chains to make certified devices accessible at lower cost.

Europe Wearable Medical Devices Market

Europe maintains momentum with a 15.08% CAGR, anchored by GDPR-aligned privacy assurance that elevates patient trust. Germany’s DiGA program reimburses digital therapeutics, including cardiac-rhythm patches, through statutory insurance. France adopts nationwide electronic prescription services that automate device ordering, and Italy pilots public-private partnerships to integrate fall-detection wearables in elderly-care homes. The Medical Device Regulation’s post-market surveillance obligations heighten vendor accountability, elevating the reputation of CE-marked products across the wearable medical devices market.

APAC Wearable Medical Devices Market

Asia-Pacific is forecast to be the fastest-growing territory at 16.21% CAGR. China’s broader medical-device sector is trending toward USD 210 billion by 2025 as local champions secure National Medical Products Administration clearance for glucose monitors and AI-aided arrhythmia patches. Japan’s health-ministry guidance endorses smartwatch-derived ECG data for preliminary triage, while South Korea subsidizes smart-clothing factories under its Bio-Healthcare 2030 plan. India’s digital-health mission promotes Bluetooth-enabled vitals devices in rural clinics, enhancing accessibility. Regional contract manufacturers supply global brands, reinforcing Asia-Pacific’s influence on production scale and cost leadership within the wearable medical devices market.

Regulatory Landscape

Wearable medical devices face tightening rules around software, cybersecurity, and clinical claims, with approval and enforcement pathways differing by region. In the United States, the FDA updated its General Wellness: Policy for Low Risk Devices guidance in January 2026, sharpening the boundary between low-risk wellness wearables and products that trigger medical-device oversight when they claim to diagnose, treat, or drive clinical decisions. In parallel, revised FDA guidance for Clinical Decision Support software clarified how software functions are regulated as they are increasingly embedded in connected wearables.

In Europe, the EU Medical Device Regulation (MDR) remains the central framework for wearable medical devices, with growing operational focus on device registration and lifecycle traceability. EUDAMED registration for new MDR/IVDR devices became mandatory from May 28, 2026, while updated MDCG guidance, including classification and EMDN updates, increased documentation and coding expectations for manufacturers selling connected diagnostic and therapeutic wearables across EU member states. In China, the National Medical Products Administration (NMPA) maintains a registration and standards-driven regime; its 2026 industry standards revision plan (covering AI and software) raises update requirements for technical files, and new medical-device GMP requirements taking effect on November 1, 2026 lift quality-system expectations for companies supplying or manufacturing wearables for the Chinese market.

Value Chain Analysis

The wearable medical devices value chain spans (i) upstream component suppliers, including biosensors, MEMS, electrochemical sensing elements, microcontrollers, batteries, and flexible substrates, (ii) device OEMs that integrate hardware, firmware, and enclosures, (iii) connectivity and cloud infrastructure providers that enable continuous transmission and storage, (iv) AI and analytics developers that translate signals into actionable insights, and (v) clinical workflow and interoperability integrators that connect wearable outputs to electronic health records and remote patient monitoring dashboards. In this market, differentiation increasingly comes from device-plus-software performance, including algorithm validation, interoperability, and cybersecurity, rather than sensor hardware alone.

Manufacturing and fulfillment depend heavily on contract manufacturing organizations focused on miniaturization and wireless integration, while distribution splits between offline clinical channels (hospitals, clinics, pharmacies, durable medical equipment) and direct-to-consumer pathways that bundle subscriptions and replenishment. Key bottlenecks include constrained capacity in specialized sensor fabrication, competition for electronics components with consumer sectors, and regulatory throughput limits, particularly MDR conformity assessment constraints and Notified Body capacity that can extend assessment lead times beyond six months for certain categories. Traceability and compliance also shape post-market operations, including rollout of Unique Device Identification requirements, with Class I UDI implementation effective May 26, 2025, which adds labeling, data management, and partner-system integration steps across the chain.

Competitive Landscape

The wearable medical devices market is moderately fragmented, blending med-tech incumbents and consumer-electronics leaders with agile start-ups. Abbott, Medtronic, and Dexcom capitalize on established clinical distribution channels and deep regulatory proficiency, prioritizing accuracy and interoperability with hospital information systems. Apple and Samsung leverage operating-system control to embed FDA-cleared ECG or SpO₂ algorithms in mass-market smartwatches, converting consumer loyalty into healthcare engagement.

Strategic alliances shape competitive dynamics. Dexcom’s USD 75 million investment in Oura marries continuous glucose telemetry with sleep and activity metrics to create integrated metabolic-health services. Medtronic collaborates with Samsung to display insulin pump alerts on smartphones, enhancing patient convenience. Nanowear co-develops machine-learning pipelines with cloud providers to expedite algorithm validation and regulatory submissions.

Start-ups target specialized niches. Element Science’s Jewel Patch Wearable Cardioverter Defibrillator brings AI-cut false-alarm technology to sudden-cardiac-arrest prevention, while Epiminder pioneers implantable, multi-month EEG monitoring. IEEE WAMIII conformity acts as a differentiator by simplifying hospital IT deployment. Acquisition activity intensifies as conglomerates fill portfolio gaps for pediatric or neurological segments. Vendors that deliver proven cybersecurity, low-maintenance operation, and data-science toolkits are set to sustain competitive advantage in the evolving wearable medical devices industry.

Wearable Medical Devices Industry Leaders

Abbott Laboratories

Alphabet Inc.

Apple Inc.

Omron Corporation

Samsung Electronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Wearable Medical Devices Market Companies Covered in this Report

- Abbott Laboratories

- AIQ Smart Clothing Inc.

- Alphabet Inc.

- Apple

- Biobeat Technologies Ltd.

- Dexcom

- Garmin

- Huawei Technologies

- imec

- Intelesens

- Koninklijke Philips

- Lifesense Group

- Masimo

- Medtronic

- MINTTI Health

- OMRON

- Resmed

- Samsung Group

- Withings SA

- Xiaomi Corporation

Market Opportunities and Future Outlook

Opportunities cluster where reimbursement, interoperability, and validated analytics translate continuous data into billable and scalable care pathways. Remote patient monitoring workflows benefit from established CMS reimbursement constructs, including CPT 99453, 99454, 99457, and 99458, and the Medicare Physician Fee Schedule updates referenced in the report context, which create practical whitespace for vendors combining clinically validated sensors with low-friction data capture, at least 16 transmissions per 30-day period compliance, and EHR-ready outputs (for example via HL7 FHIR). Interoperability initiatives such as Apple HealthKit, alongside efforts like IEEE WAMIII to reduce device-data fragmentation, also support platform-style offerings where device fleets and analytics subscriptions expand across home healthcare, hospitals, and long-term care settings.

Product whitespace is visible in multi-analyte sensing and next-generation form factors that improve adherence and clinical relevance. Abbott securing CE Mark in May 2026 for dual glucose-ketone sensing, including Libre Duo and Libre Duo 10 Day, points to movement toward richer metabolic monitoring beyond single-parameter wearables. The technology pipeline highlighted across recent research includes skin-applied conductive sensors, thread-based electronics, microneedle patches for continuous drug monitoring, and wearable ultrasound-based stimulation concepts, which map to new diagnostic and therapeutic segments once clinical validation and regulatory positioning are established. On the platform side, larger players are also investing to connect consumer engagement with clinical programs, including Abbott participating in a sizable financing round for WHOOP (reported in 2026), which reinforces the commercial pathway for subscription-led models that link lifestyle metrics with clinically meaningful monitoring.

Recent Industry Developments in Wearable Medical Devices Market

- June 2026: Medtronic expanded its collaboration with Abbott to integrate Abbott's dual glucose-ketone sensing capability with MiniMed smart dosing systems. The integration supports more comprehensive metabolic monitoring within insulin-delivery workflows. It also strengthens closed-loop ecosystem differentiation and widens the clinical utility of connected wearables in diabetes management.

- June 2025: The US FDA approved Sonu Band, an AI-enabled wearable that provides drug-free therapy for pediatric nasal congestion. The clearance broadened the therapeutic wearable category into child-focused indications. This encouraged product developers to pursue pediatric-specific designs and evidence packages.

- November 2024: Dexcom invested USD 75 million in Oura to integrate continuous glucose monitoring with smart-ring lifestyle analytics. The partnership advanced the convergence of clinical-grade sensing with consumer engagement layers. It also supports combined data products that can feed remote monitoring programs and personalized coaching services.

Wearable Medical Devices Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the wearable medical device market covers body-worn devices that measure clinically relevant health data or provide a therapeutic function, and that can store data or transmit it to a caregiver or system for monitoring.

Scope exclusions: General wellness wearables that are not positioned for medical use and do not support clinical monitoring or therapy are excluded.

Segments Covered in This Report

- By Device Type

- Diagnostic & Monitoring Devices

- Vital-sign Monitoring Devices

- Sleep-monitoring Devices

- Continuous-Glucose Monitors

- Blood-pressure Monitors

- Other Diagnostic & Monitoring Devices

- Therapeutic Devices

- Pain-management Devices

- Rehabilitation Devices

- Respiratory-therapy Devices

- Insulin-delivery Devices

- Other Therapeutic Devices

- Diagnostic & Monitoring Devices

- By Age Group

- Under 18

- 18 - 60

- Above 60

- By Distribution Channel

- Online

- Offline

- By Application

- Sports & Fitness

- Remote Patient Monitoring

- Home Healthcare

- By End-User

- Consumers

- Hospitals & Clinics

- Long-term Care Centres

- Ambulatory Surgical Centres

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

We start with desk research to map demand signals, the regulatory context, and device adoption patterns that typically move wearable medical device revenues. Public sources such as the US FDA device databases, CDC health statistics, OECD health data, World Bank population indicators, and WHO digital health publications are used to anchor assumptions around patient pools and monitoring needs.

Then the sizing inputs are refined using company annual reports, investor presentations, product and reimbursement updates on official portals, and reputable press coverage of new launches and approvals. Where helpful, we also use paid subscription sources for company financials and for patent and innovation tracking to understand where revenue is being created and which use cases are scaling. These examples are illustrative only, and we used additional public sources for data collection, validation, and clarification.

Primary Interviews and Surveys

Our primary work focuses on checking real-world pricing, channel mix, and adoption rates for medical-grade wearables, because these details are not consistently visible in public data. We speak with a mix of device manufacturers, component and software ecosystem participants, distributors, and healthcare delivery stakeholders across APAC, EMEA, and the Americas, so pricing assumptions, adoption timing, and channel throughput can be challenged before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 15% | APAC: 51% |

| Mid tier: 47% | Functional/Unit leaders: 29% | EMEA: 31% |

| Smaller Players: 17% | Managers: 56% | Americas: 18% |

Market-Sizing & Forecasting

The market is sized using a top-down build that starts from the addressable pool for remote monitoring and therapeutic wearable use. We reconstruct that pool through prevalence and care-setting adoption signals, then convert into value using device ASP ranges and replacement cycles. To keep outputs practical, we cross-check totals with selective bottom-up approximations such as sampled brand-level price points, channel checks for unit throughput, and supplier-side volume indicators, and we tune the model when gaps show up.

Key inputs used in the model include chronic disease prevalence trends (notably diabetes and cardiovascular conditions), the share of patients moving into remote monitoring programs, average device lifetimes and replacement timing, regional pricing bands by device category, and the mix shift between diagnostic and monitoring wearables versus therapeutic wearables. Where unit data is incomplete for smaller countries, we use proxy indicators such as healthcare spend per capita, connected device penetration, and rollout pace of remote monitoring, then apply interview-based corrections.

Forecasting is done through scenario analysis supported by multivariate regression, with the main drivers being adoption rates, price progression, and expansion of reimbursed monitoring pathways. We review scenarios with experts so unrealistic growth curves are avoided, particularly in years where regulatory or reimbursement changes are expected to be the swing factor.

Data Validation & Update Cycle

Results are validated through triangulation across independent signals, then stress-tested with variance checks at the region and device-type levels so a single assumption does not dominate the total. If an output looks unusual, we re-check the underlying drivers, revisit the conversion steps, and re-contact sources when the gap cannot be explained by documented inputs.

Before publication, the model and narrative go through multi-step analyst reviews that focus on consistency of definitions, currency handling, and forecast logic. Reports are refreshed annually, and interim updates are made when material events occur, followed by a final pre-delivery pass so clients receive the latest view.

Mordor Intelligence's Global Wearable Medical Device Market Market Size Compared Against Other Published Estimates

Published market sizes for wearable medical devices often do not match, even when they appear to cover the same space. The gap usually comes from how narrowly a study defines medical-grade wearables, which years are used as the base, and how pricing and adoption are carried forward in the forecast.

By tracking device replacement cycles, reimbursed monitoring adoption, and clinical-grade inclusion rules, Mordor Intelligence keeps the 2026 value tied to devices that generate clinically relevant data or deliver therapy, rather than mixing in broader wellness-only wearables that inflate totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 55.7 B (2026) | |

| Industry Research Publisher A | USD 45.0 B (2024) | Uses a different base year and a shorter forecast window, and the scope appears to be wider across product and channel groupings, which can pull in adjacent wearables beyond strict clinical monitoring or therapy. |

| Global Research Portal B | USD 53.73 B (2025) | Treats 2025 as the base and applies a longer, more aggressive forecast arc to 2035, and it explicitly mixes consumer-grade and clinical-grade devices, which can raise the starting pool and accelerate the growth curve. |

The spread across these estimates is mainly explained by scope boundaries and time framing, not arithmetic differences. When the market is limited to medical-grade monitoring and therapeutic devices and is checked against replacement timing and adoption signals, the yearly total becomes easier to reproduce and track through updates.

Key Questions Answered in the Report

What clinical factors are driving hospitals to adopt wearable medical devices?

Hospitals prioritize wearables because continuous data streams help lower readmission rates and support outcome-based reimbursement models focused on chronic-disease management and post-surgical recovery.

How are consumer-tech ecosystems influencing medical-grade wearables?

Open APIs from smartphone platforms allow FDA-cleared sensors to sync seamlessly with everyday apps, boosting patient engagement and giving clinicians richer lifestyle context without adding workflow complexity.

Which device functionality is seeing the fastest innovation edge?

AI-enabled biosensors that detect multiple biomarkers on a single patch or textile are advancing rapidly, enabling disease-specific monitoring and early intervention through predictive analytics.

Why is pediatrics emerging as a promising niche for therapeutic wearables?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Wearable Medical Devices Market?

Recent FDA clearances for child-focused devices demonstrate regulatory openness, and parents value non-invasive tools that reduce clinic visits while offering real-time symptom relief or monitoring.

What cybersecurity measures are now mandatory for new wearable devices?

Regulators require a detailed software bill of materials, data-at-rest encryption, and post-market patch management plans, compelling manufacturers to design security into every stage of product development.

How are reimbursement policies shaping the competitive landscape?

Coverage for remote patient-monitoring codes has prompted both established med-tech firms and start-ups to form partnerships with payers, accelerating device integrations into routine clinical workflows.

Page last updated on: