Textile Implants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.99 Billion |

| Market Size (2031) | USD 9.53 Billion |

| Growth Rate (2026 - 2031) | 6.39% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

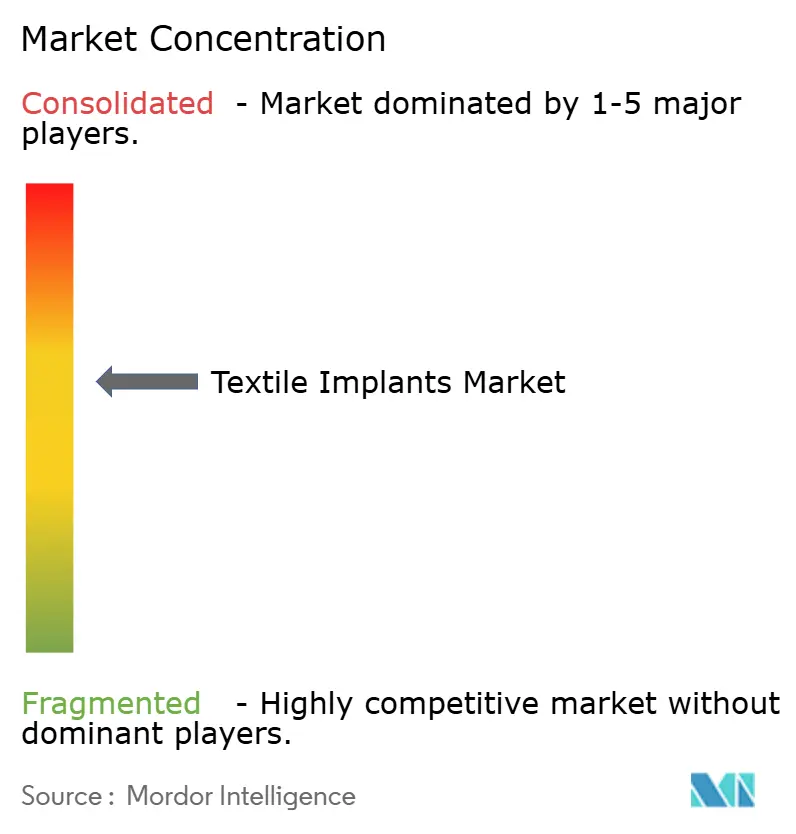

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Textile Implants Market Analysis by Mordor Intelligence

The textile implants market was valued at USD 6.60 billion in 2025 and estimated to grow from USD 6.99 billion in 2026 to reach USD 9.53 billion by 2031, at a CAGR of 6.39% during the forecast period 2026-2031. The textile implants market is being supported by a larger elderly patient pool, which is sustaining procedure volumes across hernia repair, orthopedic reconstruction, cardiovascular surgery, and soft tissue reinforcement. The textile implants market is also benefiting from a steady move toward outpatient surgery, where lighter implant formats, simpler deployment, and faster case turnover matter more in everyday clinical practice. Woven and knitted implant structures continue to hold relevance in the textile implants market because they offer tunable porosity, mechanical compliance that better matches host tissue, and compatibility with robotic delivery pathways used in minimally invasive procedures. The shift toward bioresorbable and bioengineered meshes is adding another layer of demand in the textile implants market, as commercial launches show that absorbable reinforcement products are moving into wider clinical use. The textile implants market is also being shaped by 3D textile engineering, which is improving patient-conforming mesh geometries and reducing intraoperative fitting challenges in complex repair settings.

Key Report Takeaways

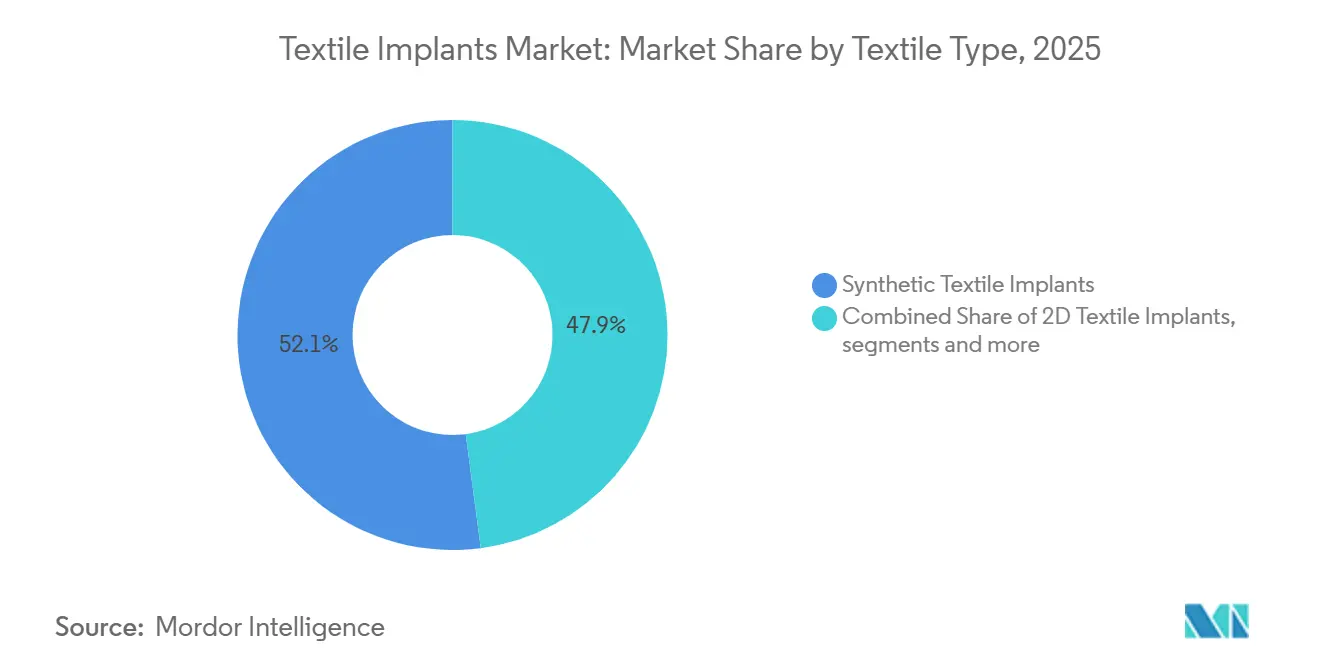

- By textile type, synthetic textile implants held 52.10% of the textile implants market in 2025, while 3D textile implants are projected to expand at a 7.19% CAGR through 2031.

- By indication, hernia repair accounted for 50.90% of the textile implants market in 2025, while orthopedic surgery is forecast to grow at an 8.23% CAGR through 2031.

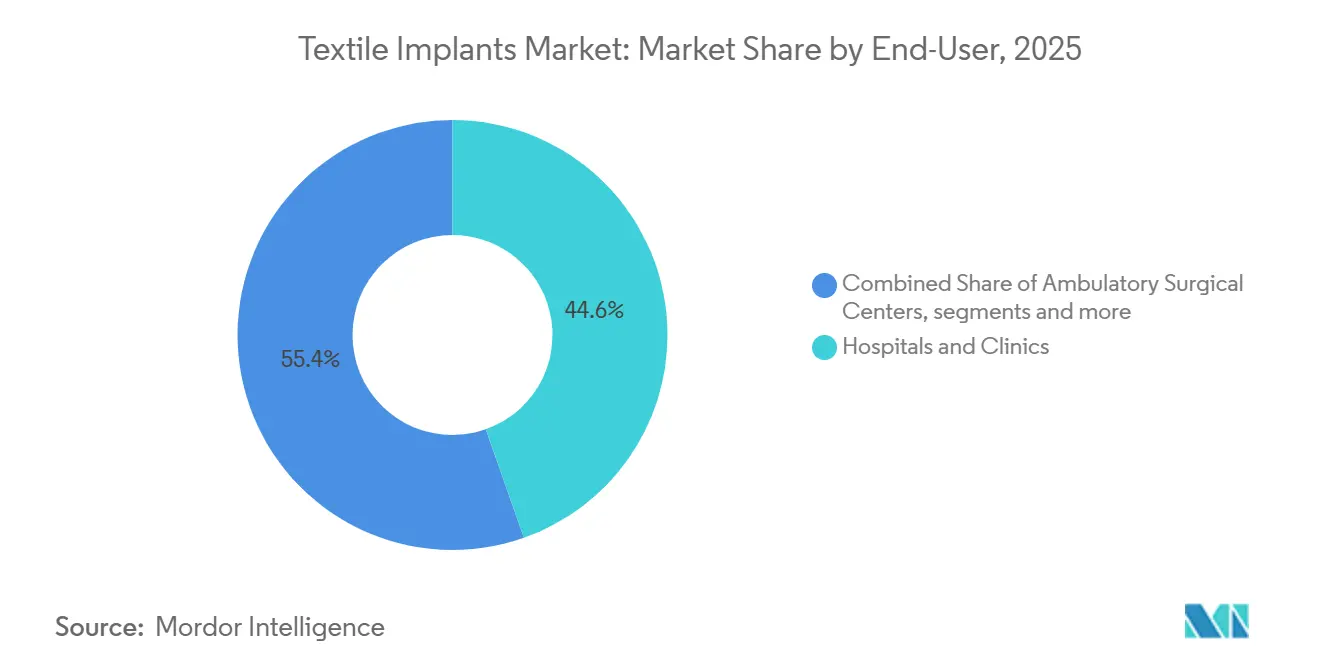

- By end-user, hospitals and clinics held 44.60% of the textile implants market in 2025, while ambulatory surgical centers are projected to advance at a 6.71% CAGR through 2031.

- By geography, North America accounted for 46.80% of the textile implants market in 2025, while Asia-Pacific is expected to expand at an 8.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Textile Implants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Preference for Bioengineered Meshes and Reinforcement Textiles | +1.1% | Global, concentrated gains in North America and EU | Medium term (2-4 years) |

| Higher Surgical Volumes in Hernia, Orthopedic, and Cardiovascular Reconstruction | +1.4% | Global, with North America, Europe, and South Asia as core demand centers | Medium term (2-4 years) |

| Improved Clinical Adoption of Resorbable and Hybrid Textile Implants | +0.8% | North America and EU, with early spillover to Asia-Pacific | Medium term (2-4 years) |

| Expansion of Outpatient and Ambulatory Surgical Workflows | +1.0% | North America as the core market, with growth markets in Asia-Pacific | Short term (≤ 2 years) |

| Advancements in Biomaterial Engineering and Smart Textile Technologies | +0.7% | Global, concentrated in R&D-intensive markets | Long term (≥ 4 years) |

| Growing Aging Population and Rising Incidence of Tissue Degeneration Disorders | +1.3% | Global, with strongest exposure in East Asia, Southern Europe, and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Preference for Bioengineered Meshes and Reinforcement Textiles

The textile implants market is seeing a clear move away from legacy polypropylene mesh toward poly-4-hydroxybutyrate, collagen-reinforced, and other bioresorbable textile constructs. This change is not only about surgeon preference, because liability exposure tied to permanent synthetic mesh has also pushed hospitals and suppliers toward newer materials. In 2025, BD received FDA 510(k) clearance for the Phasix ST Umbilical Hernia Patch, which was positioned as the first fully absorbable hernia mesh designed specifically for umbilical repair, showing that scale commercialization is becoming more practical in the textile implants market.[1]BD, “BD Launches Industry-First Bioabsorbable Mesh Designed for Umbilical Hernia Repair,” BD Newsroom, news.bd.com Product innovation is also moving beyond absorbability alone, because multifunctional mesh designs now incorporate antimicrobial and anti-adhesive features directly into textile architecture. That broader value proposition matters in the textile implants market because it supports outcome improvement while keeping textile-based reinforcement central to repair strategies. As more evidence builds around these formulations, procurement decisions in the textile implants market are likely to reflect both risk management and clinical performance.

Higher Surgical Volumes in Hernia, Orthopedic, and Cardiovascular Reconstruction

The textile implants market continues to draw its largest procedural demand from hernia repair, and that demand base is set to expand over time. A 2025 study in BMC Gastroenterology projected that global hernia case incidence will rise by 19.7% in absolute terms by 2050, with population growth and aging acting as the main drivers.[2]S. Markar et al., “Spatiotemporal Trends in Hernia Disease Burden and Health Workforce Correlations in Aging Populations: A Global Analysis with Projections to 2050,” BMC Gastroenterology, link.springer.comThe textile implants market is also moving up the value chain because growing procedure volumes are increasingly paired with more advanced implant specifications in robotic and laparoscopic settings. That matters because higher-volume surgical pathways are no longer relying only on standard mesh, and premium constructs with tighter stiffness, unfolding, and delivery requirements are gaining ground. Cardiovascular and orthopedic procedures add further support to the textile implants market by widening the number of clinical scenarios where textile architectures remain necessary. The result is a bifurcated textile implants market, where standard synthetic products keep volume in high-throughput settings while advanced textile formats capture stronger pricing in more specialized care pathways.

Expansion of Outpatient and Ambulatory Surgical Workflows

The textile implants market is being reshaped by the shift of elective procedures from inpatient settings into ambulatory and same-day surgical environments. This is not a short-lived adjustment, because the care setting itself is changing how implant packaging, handling, and deployment are evaluated during procurement. In the textile implants market, there are products that favor self-fixating meshes, streamlined kits, and preconfigured delivery formats that reduce procedure time and simplify use in tightly managed workflows. The same trend also increases the value of lighter constructs that support faster discharge protocols and less handling complexity in hernia and orthopedic repair. For manufacturers in the textile implants market, the channel shift is as important as the material shift, because product format now influences commercial success as much as core implant performance. Companies that adapt their portfolios to outpatient needs are likely to gain share faster than peers that continue to rely on hospital-centered formats in the textile implants market.

Growing Aging Population and Rising Incidence of Tissue Degeneration Disorders

The textile implants market is closely tied to demographic aging because older patient groups account for a larger share of hernia, joint reconstruction, cardiovascular grafting, and soft tissue repair procedures. A 2025 systematic review on joint arthroplasty documented very strong long-term growth across major registries, showing that procedure demand is rising materially as populations age. Further support comes from the Journal of Orthopedic Surgery and Research, which reported that disability-adjusted life years for musculoskeletal disorders in the population aged 70 and above are projected to rise through 2050.[3]Springer Nature, “Global Burden of Disease for Musculoskeletal Disorders in All Age Groups, from 2024 to 2050,” Journal of Orthopaedic Surgery and Research, link.springer.comIn the textile implants market, this demand is especially relevant for ligament and tendon reconstruction, where woven and braided scaffolds are used in procedures that are expanding within orthopedics. The aging curve, therefore, supports both volume growth and product mix change in the textile implants market, instead of only increasing the count of routine procedures. This makes demographic pressure one of the most durable demand supports for the textile implants market through 2031.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory Approval and Clinical Evidence Requirements | -0.5% | Global, with EU MDR and U.S. FDA as the strictest frameworks and additional layers emerging in Asia-Pacific | Medium term (2-4 years) |

| Procedure and Device-Related Complication Risk | -0.4% | Global, with legacy product markets most exposed | Medium term (2-4 years) |

| High Cost of Advanced Textile Implant Materials and Procedures | -0.3% | Asia-Pacific, Middle East and Africa, and South America | Medium term (2-4 years) |

| Risk of Post-Surgical Infections and Foreign Body Reactions | -0.3% | Global, with higher exposure in markets that have limited post-operative surveillance | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Approval and Clinical Evidence Requirements

The textile implants market faces rising compliance pressure because implantable products now require stronger post-market follow-up and broader evidence packages than many legacy portfolios were built to support. This is particularly relevant for pelvic floor and related mesh categories, where historical complication patterns have already led to product withdrawals and tighter scrutiny. In the textile implants market, the regulatory burden is heavier for newer silk-based, collagen-based, and 3D knitted constructs because they must show durable in vivo performance before broader adoption can follow. That requirement lengthens development timelines and raises the cost of commercialization, which can slow smaller innovators more than diversified medtech companies. As a result, the textile implants market increasingly rewards manufacturers that already have quality systems, long-term evidence programs, and device traceability infrastructure in place. This does not stop innovation in the textile implants market, but it does raise the threshold for who can scale it efficiently.

High Cost of Advanced Textile Implant Materials and Procedures

The textile implants market still faces a pricing gap between standard polypropylene mesh and newer textile constructs that use bioresorbable, silk, collagen-based, or 3D engineered formats. A 2025 study in the Journal of Biomedical Engineering showed that bioabsorbable warp-knitted spacer fabrics made from PLA and P4HB require specialized equipment and tight process controls that differ materially from commodity mesh manufacturing. That cost structure limits the near-term reach of premium products in the textile implants market, especially in price-sensitive procurement systems across emerging regions. The barrier is not limited to the implant itself, because advanced procedures that use these materials can also require more specialized surgical capability and support. This keeps the textile implants market on a dual-track path where standard materials remain dominant in cost-sensitive settings while premium products stay concentrated in better-funded systems. Over time the textile implants market may see some of this gap narrow, but current economics still constrain how quickly advanced textile formats can scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Textile Type: Synthetic Leads, 3D Architectures Accelerate

Synthetic textile implants accounted for a 52.10% share of the textile implants market size in 2025, supported by polypropylene, polyester, and expanded polytetrafluoroethylene constructs that remain widely used across hernia repair, vascular grafting, and soft tissue reinforcement. Their position in the textile implants market reflects long clinical histories, standardized sterilization practices, and broad familiarity among surgeons and procurement teams. For many providers in the textile implants industry, established regulatory pathways and predicate-based product development still favor synthetic variants over newer alternatives. That creates a structural advantage for incumbent suppliers that already serve high-volume repair categories in the textile implants market.

3D textile implants are projected to grow at a 7.19% CAGR from 2026 to 2031 in the textile implants market, because they can provide patient-conforming geometries and controlled pore profiles that flat 2D mesh cannot always achieve in complex reconstructions. Natural textile implants such as silk and collagen variants remain smaller in volume, but the textile implants market is seeing stronger research and clinical interest in applications where tissue integration matters more than simple cost comparison. The textile implants market is therefore moving toward a broader mix where synthetic products keep the base and advanced architectures drive the next layer of value creation.

By Indication: Orthopedic Demand Reshaping the Revenue Mix

Hernia repair held 50.90% of the textile implants market share in 2025, which kept it as the largest indication because inguinal, ventral, and incisional hernias continue to generate steady procedure demand across adult populations. That dominant position is still central to the textile implants market, but the value mix is beginning to shift as pricing pressure affects standard mesh in high-volume public systems. The textile implants market is also seeing stronger demand for bioresorbable and robotic-friendly upgrades within hernia repair, rather than growth coming only from commodity products. Cardiovascular surgery and soft tissue reconstruction remain important adjacent demand pools, where woven grafts and braided scaffolds continue to support procedure-based consumption. This keeps the textile implants market diversified across multiple clinical pathways even while hernia repair remains the largest revenue anchor.

Orthopedic surgery is projected to expand to an 8.23% CAGR from 2026 to 2031 in the textile implants market, driven by aging-related musculoskeletal disease, rising ligament and tendon reconstruction volumes, and wider use of scaffold-based augmentation in rotator cuff and anterior cruciate ligament repair. The orthopedic opportunity matters because these procedures are moving into ambulatory settings faster than many abdominal repairs, which supports better pricing for advanced implant formats.

By End-User: Hospital Dominance Faces Growing ASC Competition

Hospitals and clinics accounted for 44.60% of the textile implants market size in 2025, because many cardiovascular grafts, abdominal wall reconstructions, and revision procedures still require inpatient infrastructure and closer post-operative monitoring. This keeps hospitals at the center of the textile implants market even as lower-acuity elective procedures continue to migrate outward. The textile implants market also remains tied to hospital procurement in cases where surgeon preference, implant inventory depth, and multidisciplinary support influence product selection. Complex procedures in the textile implants industry still depend on inpatient settings more than outpatient channels, which protects a large baseline of hospital demand.

Ambulatory surgical centers are forecasted to grow at a 6.71% CAGR through 2031 in the textile implants market, reflecting payer, employer, and patient support for value-based elective care. The textile implants market is therefore facing a gradual shift in purchasing logic, where ease of storage, single-use packaging, and quick setup become more commercially important. Specialty surgical centers remain smaller by volume, but they can serve as early adoption sites for robotic-compatible and patient-specific textile constructs. As the end-user mix evolves, the textile implants market is likely to reward companies that redesign implant formats for outpatient workflows instead of relying only on hospital-optimized portfolios.

Geography Analysis

North America held 46.80% of the textile implants market share in 2025, supported by high procedure volumes, mature reimbursement systems, and a dense installed base of advanced surgical platforms. The United States remains the main revenue driver in the textile implants market across hernia mesh, vascular grafts, and orthopedic textile scaffolds. The region also benefits from established commercialization pathways and broad clinical familiarity with synthetic as well as premium reinforcement options. In the textile implants market, this creates a favorable setting for suppliers that can serve both high-volume routine repair and higher-value specialized reconstruction. Europe also holds a substantial position in the textile implants market, supported by strong specialist surgical infrastructure and steady demand across Germany, the United Kingdom, France, Italy, and Spain.

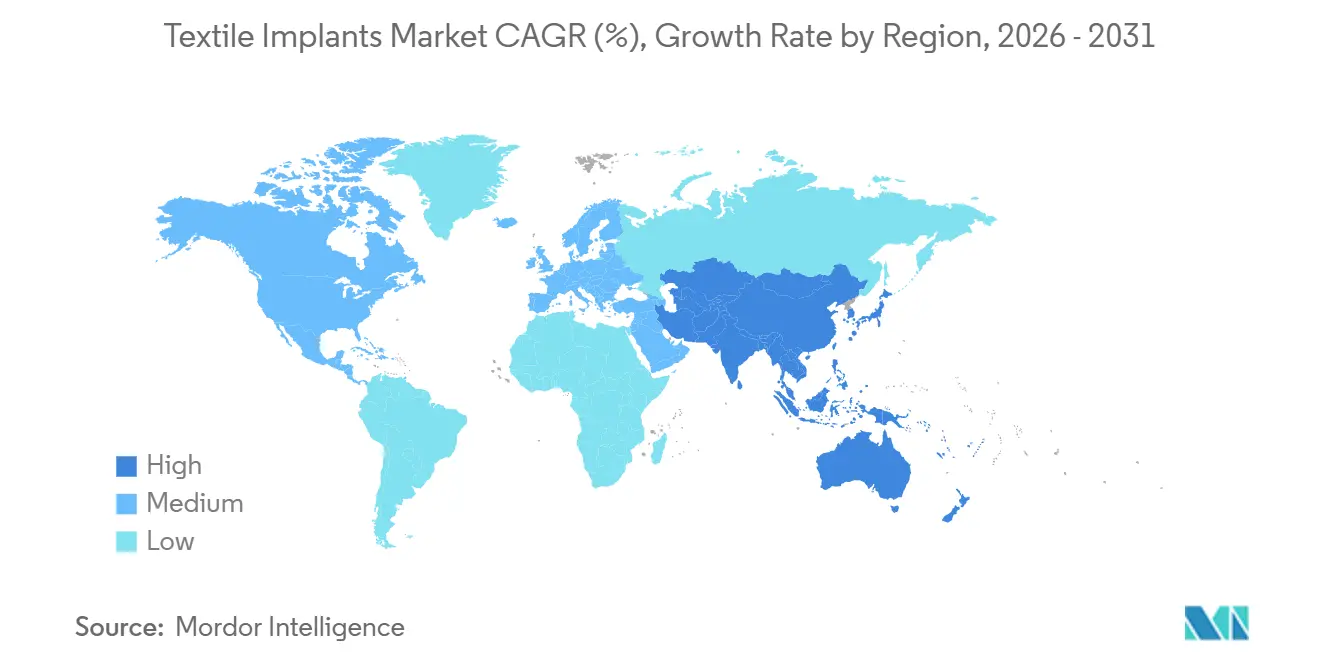

Asia-Pacific textile implants market is projected to expand at an 8.22% CAGR between 2026 and 2031, making it the fastest-growing geography in the textile implants market. Growth in the region is being supported by expanding surgical capacity in China, India, South Korea, and Australia, along with rising chronic disease prevalence that increases hernia and cardiovascular procedure volumes. The textile implants market in Asia-Pacific is also gaining from a growing orthopedic reconstruction base, which broadens the need for woven and braided implant formats. Japan adds a premium demand layer to the textile implants market because its older population supports steady use in cardiovascular and orthopedic procedures. India and South Korea are also strengthening their positions in the textile implants market through medical tourism inflows and healthcare infrastructure investment that widens access to both standard and advanced implant categories.

The Middle East and Africa remain smaller in the textile implants market, but private hospital investment in GCC countries is improving tertiary surgical capacity and opening space for premium implant formats. South Africa continues to anchor sub-Saharan demand in the textile implants market through its private healthcare network, although public procurement is still highly cost-sensitive. South America is led by Brazil and Argentina in the textile implants market, with hernia repair remaining the main clinical use and hospital-based procedures accounting for most implant consumption. A gradual increase in laparoscopic capability across secondary cities could still expand the reachable base for standard textile implants market products beyond what demographics alone would suggest. Overall, the textile implants market shows a clear split between mature high-value regions and faster-growing markets where infrastructure expansion is driving the next wave of adoption.

Competitive Landscape

The textile implants market is moderately concentrated, with large medtech groups such as Johnson & Johnson through Ethicon, Medtronic, W. L. Gore & Associates, B. Braun Melsungen, and Smith+Nephew holding broad product portfolios across hernia, cardiovascular, and orthopedic applications. The presence of these diversified companies gives the textile implants market a stable upper tier with strong distribution reach, regulatory experience, and procedure coverage. At the same time, the textile implants market also includes specialist manufacturers such as Aran Biomedical Teoranta, Cousin Biotech, Corza Medical, and Titanium Textiles AG, which compete through material science depth and indication-specific clinical positioning. This combination keeps the textile implants market concentrated enough for scale to matter, but open enough for niche innovation to remain commercially relevant. Mid-tier suppliers that rely mainly on older polypropylene mesh face the greatest pressure in the textile implants market because pricing compression and product liability concerns are both working against undifferentiated portfolios.

Strategic moves in 2026 show how the textile implants market is evolving toward higher-value specialized repair. Smith+Nephew completed the acquisition of Integrity Orthopedics in January 2026, adding the Tendon Seam rotator cuff repair system and strengthening its sports medicine offering. Earlier, W. L. Gore launched GORE SYNECOR Preperitoneal Biomaterial in EMEA in April 2025, reflecting continued product investment in reinforced biomaterial formats. These moves suggest that scale players in the textile implants market are prioritizing portfolio depth, adjacent technology access, and differentiated repair systems over pure volume expansion.

Another competitive boundary in the textile implants market is forming around patient-specific implant production and digital surgical planning. Only a limited number of companies currently combine textile engineering with additive manufacturing capability, which keeps that white space relatively open. Research published in Frontiers in Bioengineering and Biotechnology in 2025 showed that warp-knitted silk-fibroin vascular grafts achieved compliance and suture retention that matched autograft performance, highlighting how next-generation materials could redefine competition in vascular applications. As innovation spreads across hernia, orthopedics, pelvic repair, and vascular use, the textile implants market is likely to reward companies that can pair evidence generation with manufacturable textile design. The resulting competitive picture is one where broad portfolios matter, but technical specialization still creates meaningful room for selective outperformance in the textile implants market.

Textile Implants Industry Leaders

Medtronic plc

Johnson and Johnson

Boston Scientific Corporation

B. Braun Melsungen AG

W. L. Gore and Associates, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Medtronic completed the acquisition of Scientia Vascular for USD 550 million, integrating neurovascular access and therapeutic textile-based device portfolios. The acquisition adds specialized guidewire and catheter technologies to Medtronic's interventional textile implant pipeline.

- April 2026: W. L. Gore's Excluder TAMBE thoracoabdominal branch endoprosthesis received CE Mark approval and launched in European hospitals as an off-the-shelf endovascular textile implant solution for complex aortic aneurysm repair involving visceral aorta.

- January 2026: Smith+Nephew completed its acquisition of Integrity Orthopedics for an initial cash payment of USD 225 million, plus performance-based payments of up to USD 225 million, adding Tendon Seam, a rotator cuff repair system using patented micro-anchors and individually locked stitches, to its sports medicine textile implant portfolio.

Global Textile Implants Market Report Scope

According to the report’s scope, the textile implants market refers to the segment of implantable biomedical textiles used in surgical procedures for tissue reinforcement, repair, and replacement. The textile implants market is segmented into textile type, indication, end-user, and geography. By textile type, the market is segmented into synthetic textile implants, 2D textile implants, 3D textile implants, hybrid textile implants, natural textile implants, collagen-based textile implants, and silk-based textile implants. By indication, the market is segmented into hernia repair, cardiovascular surgery, orthopedic surgery, dental grafts, soft tissue reconstruction, pelvic floor repair, and other indications. By end-user, the market is segmented into hospitals and clinics, ambulatory surgical centers, and specialty surgical centers. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Synthetic Textile Implants |

| 2D Textile Implants |

| 3D Textile Implants |

| Hybrid Textile Implants |

| Natural Textile Implants |

| Collagen-Based Textile Implants |

| Silk-Based Textile Implants |

| Hernia Repair |

| Cardiovascular Surgery |

| Orthopedic Surgery |

| Dental Grafts |

| Soft Tissue Reconstruction |

| Pelvic Floor Repair |

| Other Indications |

| Hospitals and Clinics |

| Ambulatory Surgical Centers |

| Specialty Surgical Centers |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Textile Type | Synthetic Textile Implants | |

| 2D Textile Implants | ||

| 3D Textile Implants | ||

| Hybrid Textile Implants | ||

| Natural Textile Implants | ||

| Collagen-Based Textile Implants | ||

| Silk-Based Textile Implants | ||

| By Indication | Hernia Repair | |

| Cardiovascular Surgery | ||

| Orthopedic Surgery | ||

| Dental Grafts | ||

| Soft Tissue Reconstruction | ||

| Pelvic Floor Repair | ||

| Other Indications | ||

| By End-User | Hospitals and Clinics | |

| Ambulatory Surgical Centers | ||

| Specialty Surgical Centers | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of textile implants by 2031?

The textile implants market is projected to reach USD 9.53 billion by 2031, rising from USD 6.60 billion in 2025 to USD 6.99 billion in 2026 at a 6.39% CAGR.

Which application area currently leads revenue generation?

Hernia repair remained the largest indication in 2025 with 50.90% share, supported by persistent procedure demand across adult populations.

Which segment is expected to grow the fastest through 2031?

Orthopedic surgery is projected to post the fastest growth at an 8.23% CAGR through 2031, driven by aging-related musculoskeletal disease and higher ligament and tendon reconstruction volumes.

Which region offers the strongest near-term expansion opportunity?

Asia-Pacific is expected to deliver the fastest regional growth at an 8.22% CAGR through 2031, supported by surgical capacity expansion and a rising orthopedic reconstruction base.

Page last updated on: