US Smart Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 84.61 Billion |

| Market Size (2026) | USD 100 Billion |

| Market Size (2031) | USD 234.27 Billion |

| Growth Rate (2026 - 2031) | 18.50% CAGR |

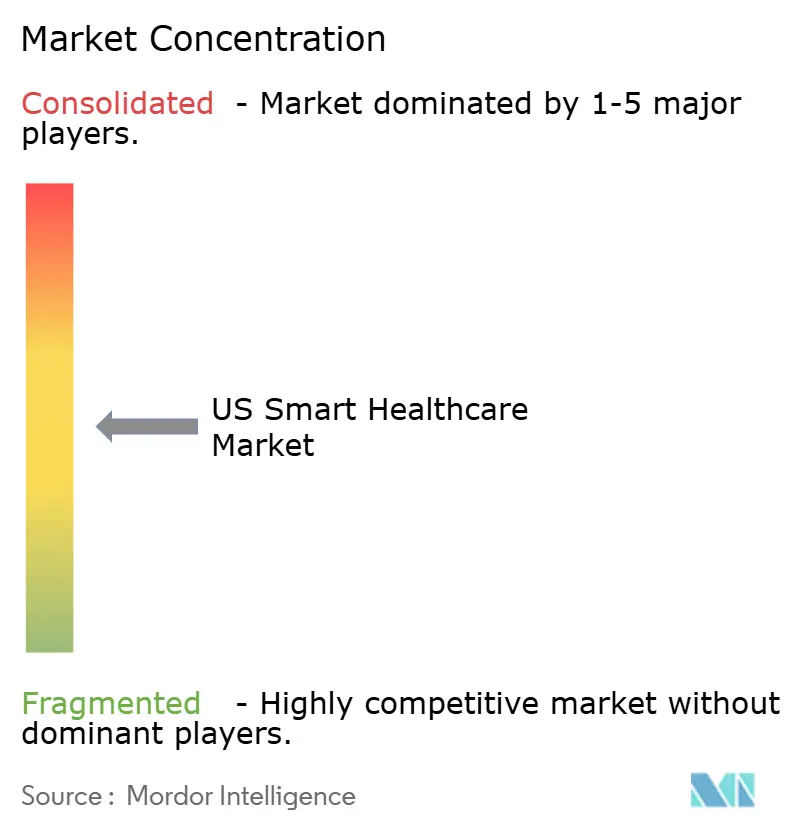

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Smart Healthcare Market Analysis by Mordor Intelligence

The US Smart Healthcare Market size is projected to be USD 84.61 billion in 2025, USD 100 billion in 2026, and reach USD 234.27 billion by 2031, growing at a CAGR of 18.5% from 2026 to 2031.

The market is transitioning from episodic, facility-centered care to a continuous model focused on connected devices, home care, wearables, and cloud platforms. Growth is driven by the chronic disease burden, increasing pressure on care teams, and payment models rewarding outcomes over service volume. Federal policies are accelerating this shift, with CMS launching the ACCESS model on July 5, 2026, for 26 million beneficiaries addressing hypertension, diabetes, musculoskeletal pain, and depression. The 2026 Medicare Physician Fee Schedule also expanded billable remote monitoring use cases.[1]Centers for Medicare & Medicaid Services, “ACCESS (Advancing Chronic Care with Effective, Scalable Solutions) Model,” CMS Innovation Center, cms.gov These changes are prompting providers, payers, and vendors to invest in interoperable data exchange, recurring service contracts, and tools integrated into clinical workflows.

Key Report Takeaways

- By technology, IoT held 40.45% of the US smart healthcare market share in 2025, while artificial intelligence is projected to expand at a 22.8% CAGR through 2031.

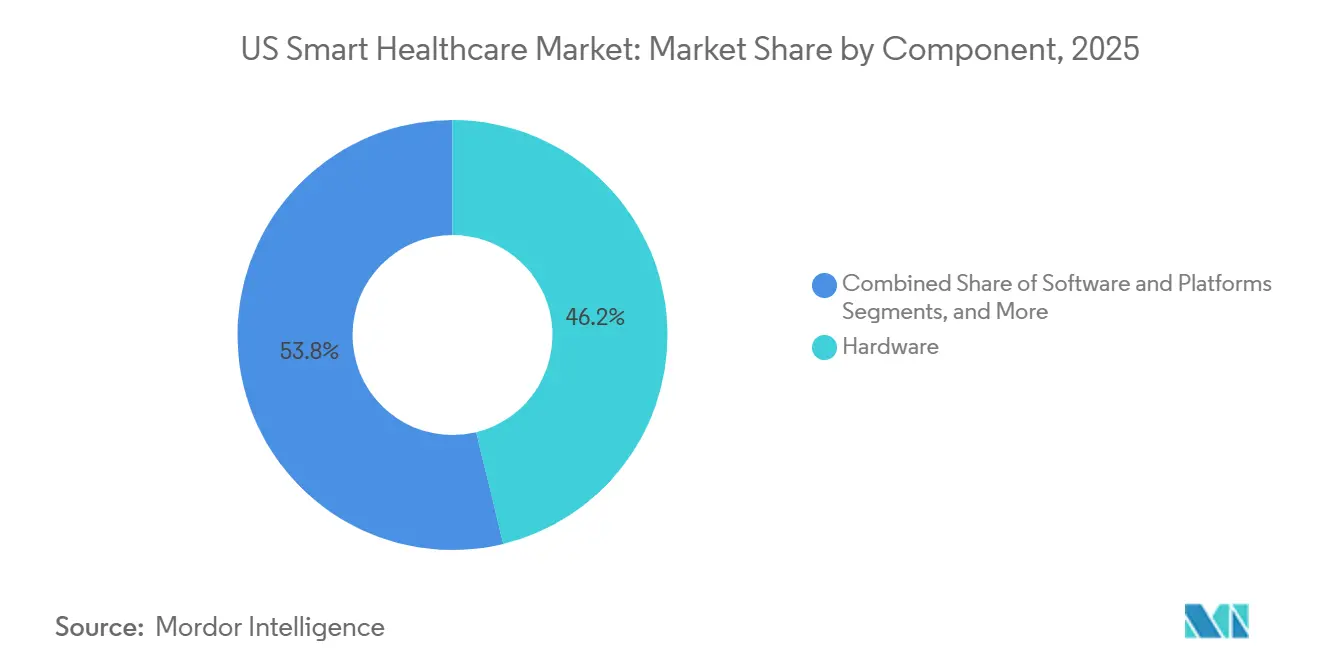

- By component, hardware commanded 46.21% of the market in 2025, while services are projected to grow at the fastest rate of 21.2% through 2031.

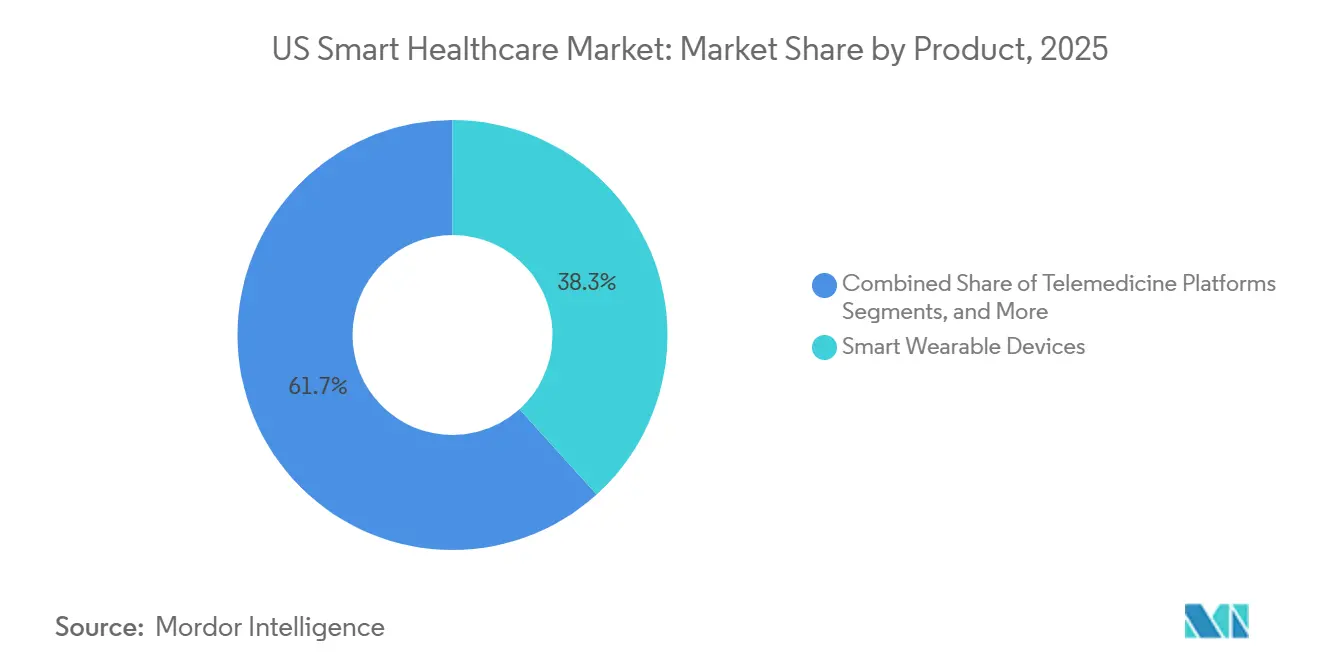

- By product, smart wearable devices held 38.3% of the market in 2025, while telemedicine platforms are forecasted to grow at a 23.5% CAGR through 2031.

- By deployment model, cloud-based or SaaS accounted for 54.66% of the market in 2025, while hybrid is projected to advance at a 20.9% CAGR through 2031.

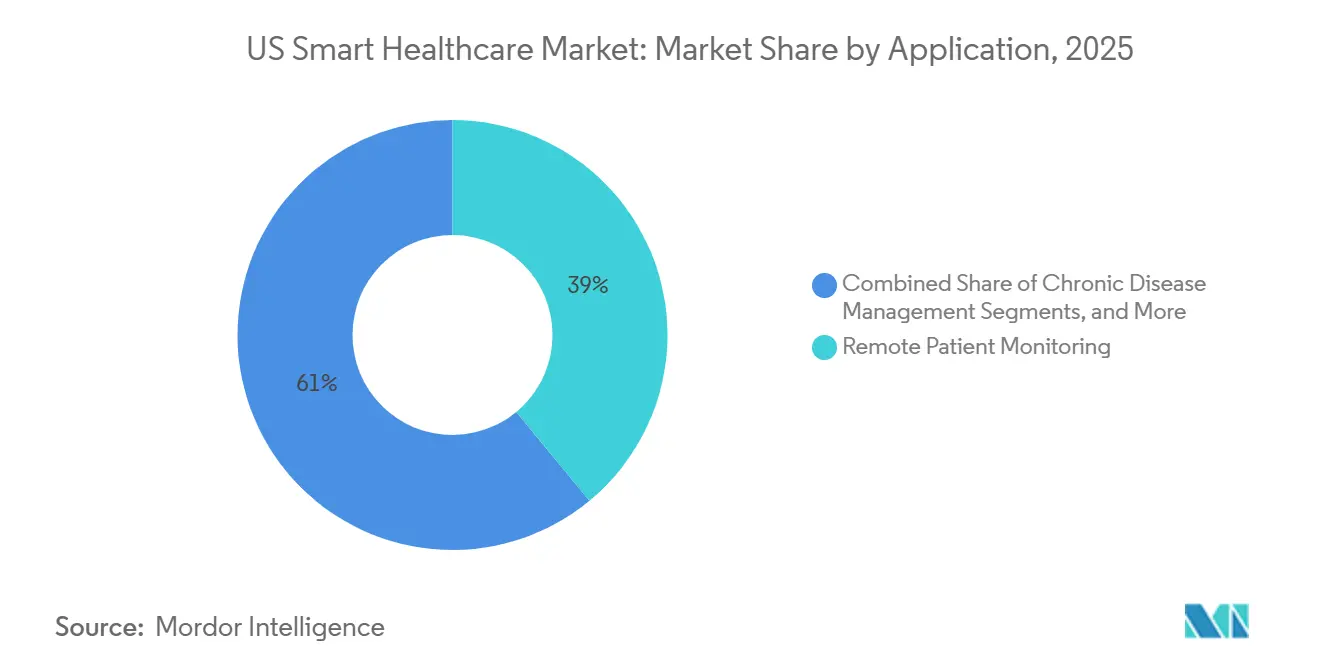

- By application, remote patient monitoring accounted for 38.99% of the market in 2025, while chronic disease management is expected to grow at 21.7% through 2031.

- By end user, hospitals and clinics held 42.1% of the market in 2025, while home healthcare settings are projected to expand at a 22.3% CAGR through 2031.

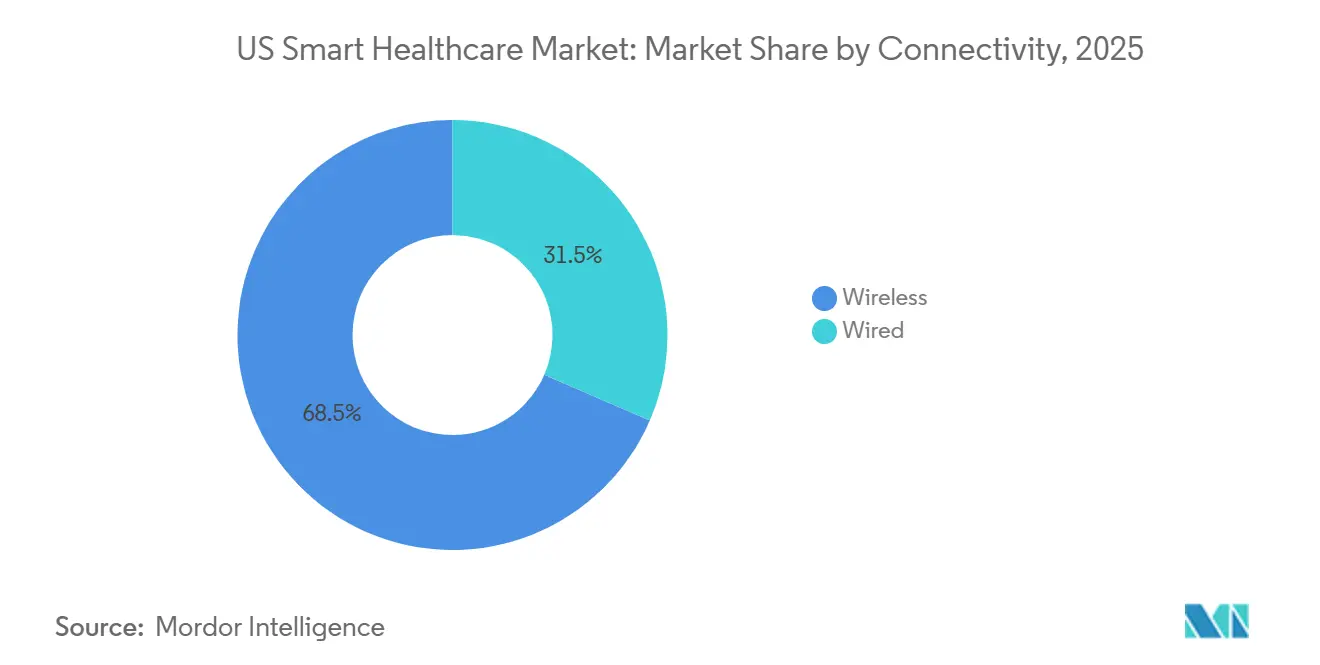

- By connectivity, wireless held 68.5% of the market in 2025 and is also forecasted to record a 24.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

US Smart Healthcare Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| FHIR API and interoperability compliance spending | +2.8% | US-wide, driven by CMS and ONC federal mandates | Medium term (2-4 years) |

| Chronic-disease-led RPM and virtual care demand | +3.9% | US-wide, with highest intensity in Sun Belt and Southern states | Long term (≥ 4 years) |

| Care-team productivity and ambient clinical AI adoption | +3.2% | US-wide, concentrated in metropolitan and large nonprofit hospitals | Short term (≤ 2 years) |

| Home-based care and hospital-at-home digital stack expansion | +2.4% | US-wide, with strong uptake in Northeast and Pacific Coast | Medium term (2-4 years) |

| CMS ACCESS model outcome-aligned reimbursement | +1.8% | US-wide (Original Medicare), with rural-adjusted supplemental payments | Medium term (2-4 years) |

| TEFCA, QHIN, and patient-directed data mobility acceleration | +1.5% | US-wide, with implementation led by network states and early-adopter QHINs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

FHIR API and Interoperability Compliance Spending

Interoperability spending has shifted from a long-term IT goal to an immediate operational priority in the United States smart healthcare market. Providers and payers face increasing pressure to modernize workflows for prior authorization, patient access, and data exchange as federal regulations demand effective digital connections. Compliance costs extend beyond initial milestones, requiring middleware, testing, workflow redesigns, and version upgrades. Legacy systems in hospitals and payer organizations struggle to integrate modern interfaces, driving ongoing investments in integration services, workflow automation, and platform upgrades. This creates a sustained revenue cycle for interoperability vendors.

Chronic-Disease-Led RPM and Virtual Care Demand

Remote monitoring demand in the United States smart healthcare market is driven by chronic care economics rather than device innovation. The 2026 Physician Fee Schedule introduced CPT codes 99445 and 99470, expanding billing eligibility to shorter monitoring windows and episodic care settings.[2]American Hospital Association, “6 Health Systems Enhancing Care Delivery with Ambient AI Scribes,” AHA Center for Health Innovation Market Scan, aha.org This change allows more patients to enroll outside traditional long-term programs. Providers are incentivized to track patients proactively, as payments are tied to measurable outcomes for conditions like hypertension and diabetes. Vendors now have opportunities in episodic, post-discharge, and near-adherence monitoring workflows.

Care-Team Productivity and Ambient Clinical AI Adoption

Care-team productivity has become a key driver in the United States smart healthcare market. By June 2025, 62.6% of hospitals using Epic adopted ambient AI documentation tools, with higher adoption in nonprofit metropolitan hospitals. Organizations like Mass General Brigham and Emory Healthcare reported reduced burnout and improved documentation quality after implementing these tools. Vendors offering AI solutions integrated directly into EHR workflows are in higher demand as these tools enhance documentation, coding quality, and clinician retention.

Home-Based Care and Hospital-at-Home Digital Stack Expansion

Home-based care is a growing focus in the United States smart healthcare market, with providers shifting monitoring and follow-up activities to patients' homes. Payment models now support virtual and asynchronous care delivery, encouraging vendors to develop comprehensive digital solutions combining devices, connectivity, alerts, and care coordination. The focus has shifted from basic post-acute monitoring to managing chronic conditions like cardiovascular and respiratory diseases. Homes are becoming primary hubs for health data collection, ensuring reliable data flow and timely clinician responses over extended care cycles.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Cybersecurity breach exposure and remediation burden | -2.1% | US-wide, highest financial impact in large health systems and payers | Short term (≤ 2 years) |

| Legacy integration and budget pressure in community providers | -1.7% | US-wide, concentrated in rural and community hospitals | Medium term (2-4 years) |

| Rural broadband and digital-literacy access gaps | -1.3% | South, Appalachia, Mountain West, and tribal lands | Long term (≥ 4 years) |

| Consent fragmentation in behavioral and substance-use data exchange | -1.0% | US-wide, particularly acute in behavioral health and SUD treatment networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity Breach Exposure and Remediation Burden

Cybersecurity remains a critical challenge in the United States smart healthcare market. The 2024 Change Healthcare ransomware attack highlighted systemic risks, affecting 190 million records and resulting in USD 2.457 billion in costs through Q3. In 2026, HHS OCR imposed USD 1,165,000 in HIPAA settlements across four ransomware cases, reflecting stricter enforcement. Providers and payers are diverting budgets to security upgrades, audits, and recovery planning, delaying investments in monitoring devices, analytics tools, and care platforms. Cyber risks also make buyers cautious about expanding endpoints in home care and remote monitoring.

Legacy Integration and Budget Pressure in Community Providers

Legacy integration and budget constraints continue to hinder technology adoption among community providers in the United States smart healthcare market. Smaller hospitals and physician groups often retain older EHRs while adding point solutions for remote monitoring or telehealth, leading to fragmented data and workflow challenges. Information-sharing requirements further strain organizations with limited IT resources. Budget pressures are driving many providers toward bundled platforms and phased migrations instead of comprehensive best-of-breed solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Outpace Hardware as Platform Economics Shift

In 2025, hardware accounted for 46.21% of the United States smart healthcare market, driven by investments in connected devices across hospitals, diagnostic centers, and homes. While hardware is essential for remote monitoring and diagnostics, its long-term value declines as programs scale, shifting focus to software and services that ensure connectivity and compliance.

Services are projected to grow at 21.2% through 2031, the fastest among components. Subscription monitoring, implementation support, and platform administration are transforming one-time device sales into recurring revenue. Bundled solutions combining hardware, software, and managed services offer a scalable alternative to standalone devices.

By Technology: IoT Anchors the Data Layer While AI Lifts Value Creation

IoT held 40.45% of the United States smart healthcare market share by technology in 2025, serving as the core data layer for patient monitoring, asset tracking, and workflow automation. Its structural importance lies in enabling consistent data capture, which supports other intelligence layers.

Artificial Intelligence is expected to grow at a 22.8% CAGR through 2031, making it the fastest-growing technology segment. AI tools are increasingly integrated into hospital workflows, reducing clinician burnout and improving documentation, which accelerates enterprise adoption and enhances the value of connected infrastructure.

By Product: Wearables Lead Installed Use While Telemedicine Builds Faster Momentum

Smart Wearable Devices led the United States smart healthcare market in 2025 with a 38.3% share, driven by their use in clinical monitoring and consumer health engagement. Their ability to support continuous data collection and multiple care pathways ensures their central role in patient monitoring and engagement.

Telemedicine Platforms are forecast to grow at a 23.5% CAGR through 2031, the fastest among products. The flexibility to deliver care in-person, virtually, or asynchronously has elevated telemedicine from a convenience tool to a critical component of chronic care and care coordination models.

By Deployment Model: SaaS Leads Today While Hybrid Supports the Transition

Cloud-based or SaaS deployments accounted for 54.66% of the United States smart healthcare market in 2025, driven by scalability, easier updates, and reduced infrastructure needs. SaaS enables unified models integrating remote monitoring, telehealth, and analytics, making it ideal for providers with limited IT resources.

Hybrid deployment is projected to grow at a 20.9% CAGR through 2031, reflecting a phased transition from legacy systems to cloud environments. This model allows organizations to modernize without disrupting ongoing operations by balancing existing systems with new digital services.

By Application: Chronic Disease Management Gains Weight as Payment Incentives Improve

Remote Patient Monitoring accounted for 38.99% of the United States smart healthcare market in 2025, reflecting its established use in cardiology, nephrology, and endocrinology. Its versatility across acute and long-term care models ensures its position as the largest revenue generator in this segment.

Chronic Disease Management is forecast to grow at a 21.7% CAGR through 2031, driven by outcome-focused remote care management. Expanded reimbursement codes and shorter monitoring windows are increasing the patient pool for continuous condition management, integrating monitoring, engagement, and care coordination.

By End User: Hospitals Lead Revenue While Home Healthcare Expands the Fastest

Hospitals and Clinics held 42.1% of the United States smart healthcare market in 2025, maintaining their central role in procurement and standardization of clinical technologies. Their influence shapes product selection, integration standards, and market timing.

Home Healthcare Settings are projected to grow at a 22.3% CAGR through 2031, driven by cost pressures and broader reimbursement support. The shift toward home-based monitoring and care coordination presents growing opportunities for vendors beyond traditional institutional settings.

By Connectivity: Wireless Deepens Its Lead as Clinical Mobility Expands

Wireless connectivity dominated the United States smart healthcare market in 2025 with a 68.5% share, driven by its necessity for wearable devices, mobile health applications, and remote monitoring systems. Its flexibility supports distributed care settings and clinician mobility.

Wireless is projected to grow at a 24.1% CAGR through 2031, supported by advancements in 5G, Wi-Fi 6, and Bluetooth Low Energy. Improved broadband availability is enhancing telehealth utilization, further solidifying wireless as the backbone of connected healthcare.

Geography Analysis

In the United States smart healthcare market, regional disparities exist in adoption rates, infrastructure readiness, and vendor opportunities. The Northeast leads as an early adopter due to major academic medical centers in Massachusetts, New York, and Pennsylvania. These centers, with their scale and complex workflows, are well-suited for deploying interoperable systems and ambient AI. Large nonprofit health systems in the region also possess the clinical expertise and financial capacity for multi-solution contracts.

In the South, the high prevalence of chronic diseases and limited care access drive demand for chronic disease management, remote monitoring, and telehealth services. Emory University noted strong hospital adoption of ambient AI in the region, highlighting its leadership in deployment momentum. Memorial Hermann Health System partnered with Cadence in April 2026 to implement AI-driven Remote Patient Monitoring and Advanced Primary Care Management in Greater Houston, targeting hypertension, congestive heart failure, and type 2 diabetes.

The West Coast, including California, Washington, and Oregon, serves as the innovation hub of the United States smart healthcare market. This region combines large health systems with a strong digital talent pool, enabling the development and validation of new software, devices, and data models before national expansion. The Midwest, while lagging coastal benchmarks in ambient AI and telehealth adoption, faces growing pressure for community providers to adopt cost-efficient SaaS and workflow tools.

Competitive Landscape

The United States smart healthcare market is moderately consolidated at the EHR and platform layer but remains fragmented across AI applications, remote monitoring, telemedicine, and wearable devices. Epic Systems, Oracle Health, and MEDITECH set workflow standards that other vendors must integrate with in hospital settings. This creates switching costs and increases the value of products that integrate seamlessly into clinical systems, allowing platform vendors to influence the scalability of new applications through integration and operational fit.

At the device and diagnostics level, Medtronic, iRhythm Technologies, Masimo, ResMed, and GE HealthCare compete in cardiac monitoring, respiratory management, and continuous vital-sign surveillance. Differentiation is shifting from hardware to analytics software, algorithms, and reimbursement alignment. Medtronic acquired CathWorks in April 2026 for USD 585 million, adding AI-guided coronary artery disease diagnostics through the FFRangio System. Roche entered a merger agreement in May 2026 to acquire PathAI for USD 750 million upfront and up to USD 300 million in milestone payments, enhancing its AI-enabled digital pathology capabilities.

White space exists in integrated care management for independent physician practices and mid-market hospitals, where enterprise pricing remains challenging. Innovaccer, Veradigm, NextGen Healthcare, and eClinicalWorks are active in this segment, addressing the need for simpler deployment and clearer operational returns. Universal Health Services announced in March 2026 its acquisition of Talkspace for approximately USD 835 million enterprise value, reflecting growing interest in scaled digital behavioral health.

US Smart Healthcare Industry Leaders

GE HealthCare

Koninklijke Philips N.V.

Abbott

Siemens Healthineers AG

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Roche acquired PathAI, a US-based AI digital pathology company, for USD 750 million upfront and up to USD 300 million in milestone payments, enhancing AI-driven anatomic pathology capabilities for US laboratory and biopharma workflows.

- May 2026: Innovaccer completed the acquisition of CaduceusHealth, expanding its Flow AI suite into autonomous revenue cycle management for approximately 4,000 US ambulatory providers managing USD 5 billion in annual patient charges.

- April 2026: Memorial Hermann Health System partnered with Cadence to implement AI-enabled Remote Patient Monitoring and Advanced Primary Care Management services for patients with chronic conditions in Greater Houston.

- April 2026: Medtronic completed its acquisition of CathWorks for USD 585 million, expanding AI-guided fractional flow reserve analytics for coronary artery disease diagnostics and clinical decision-making in cardiac catheterization workflows.

- April 2026: IKS Health acquired TruBridge, a healthcare technology solutions provider, to enhance digital infrastructure access for rural and community hospitals across the US.

US Smart Healthcare Market Report Scope

As per the scope of the report, smart healthcare is a digital ecosystem that integrates advanced technologies like the Internet of Things (IoT), artificial intelligence (AI), and cloud computing, with medical services. It transforms traditional medicine by enabling real-time remote monitoring, personalized treatments, and highly efficient healthcare delivery.

The US Smart Healthcare Market is segmented by component, technology, product, deployment model, application, end-user, and connectivity. By component, the market includes hardware, software and platforms, and services. By technology, the market is segmented into artificial intelligence (AI), internet of things (IoT), big data analytics, cloud computing, blockchain, telehealth technologies, and wearable technologies. By product, the market is categorized into smart wearable devices, smart monitoring devices, electronic health records (EHR), mHealth applications, telemedicine platforms, and smart pills & connected devices. By deployment model, the market includes on-premise, web-based or hosted, cloud-based or SaaS, and hybrid models. By application, the market is segmented into remote patient monitoring, chronic disease management, fitness & wellness, clinical workflow management, medication management, diagnosis & treatment, and elderly care. By end-user, the market includes hospitals & clinics, home healthcare settings, diagnostic centers, healthcare payers, pharmaceutical & biotechnology companies, ambulatory surgical centers, and patients/consumers. By connectivity, the market is segmented into wired and wireless. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Hardware |

| Software and Platforms |

| Services |

| Artificial Intelligence (AI) |

| Internet of Things (IoT) |

| Big Data Analytics |

| Cloud Computing |

| Blockchain |

| Telehealth Technologies |

| Wearable Technologies |

| Smart Wearable Devices |

| Smart Monitoring Devices |

| Electronic Health Records (EHR) |

| mHealth Applications |

| Telemedicine Platforms |

| Smart Pills & Connected Devices |

| On-premise |

| Web-based or Hosted |

| Cloud-based or SaaS |

| Hybrid |

| Remote Patient Monitoring |

| Chronic Disease Management |

| Fitness & Wellness |

| Clinical Workflow Management |

| Medication Management |

| Diagnosis & Treatment |

| Elderly Care |

| Hospitals & Clinics |

| Home Healthcare Settings |

| Diagnostic Centers |

| Healthcare Payers |

| Pharmaceutical & Biotechnology Companies |

| Ambulatory Surgical Centers |

| Patients/Consumers |

| Wired |

| Wireless |

| By Component | Hardware |

| Software and Platforms | |

| Services | |

| By Technology | Artificial Intelligence (AI) |

| Internet of Things (IoT) | |

| Big Data Analytics | |

| Cloud Computing | |

| Blockchain | |

| Telehealth Technologies | |

| Wearable Technologies | |

| By Product | Smart Wearable Devices |

| Smart Monitoring Devices | |

| Electronic Health Records (EHR) | |

| mHealth Applications | |

| Telemedicine Platforms | |

| Smart Pills & Connected Devices | |

| By Deployment Model | On-premise |

| Web-based or Hosted | |

| Cloud-based or SaaS | |

| Hybrid | |

| By Application | Remote Patient Monitoring |

| Chronic Disease Management | |

| Fitness & Wellness | |

| Clinical Workflow Management | |

| Medication Management | |

| Diagnosis & Treatment | |

| Elderly Care | |

| By End User | Hospitals & Clinics |

| Home Healthcare Settings | |

| Diagnostic Centers | |

| Healthcare Payers | |

| Pharmaceutical & Biotechnology Companies | |

| Ambulatory Surgical Centers | |

| Patients/Consumers | |

| By Connectivity | Wired |

| Wireless |

Key Questions Answered in the Report

What is the 2031 outlook for US smart healthcare?

The US smart healthcare market is forecast to reach USD 234.27 billion by 2031 from USD 100.26 billion in 2026, growing at a CAGR of 18.50%.

Which technology category leads adoption today?

IoT leads by technology with 40.45% share in 2025 because it forms the data-collection base for monitoring, tracking, and workflow systems.

Which product area is growing the fastest through 2031?

Telemedicine Platforms are projected to grow at a 23.5% CAGR through 2031, supported by reimbursement flexibility and stronger use in longitudinal care.

Why is chronic disease management becoming more important?

Chronic Disease Management is forecast to grow at 21.7% through 2031 as CMS ties more payment to outcomes and expands the use of remote care models.

Which end-user group remains the biggest buyer?

Hospitals and Clinics held 42.1% of end-user demand in 2025, although Home Healthcare Settings are growing faster at 22.3% through 2031.

What is the biggest operational risk for providers adopting connected care tools?

Cybersecurity remains a major constraint because healthcare organizations face high breach exposure, stronger enforcement, and added compliance costs that can delay technology investment.

Page last updated on: