Smart Healthcare Products Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 249.23 Billion |

| Market Size (2031) | USD 425.18 Billion |

| Growth Rate (2026 - 2031) | 11.27% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Healthcare Products Market Analysis by Mordor Intelligence

The smart healthcare products market size was valued at USD 223.98 billion in 2025 and estimated to grow from USD 249.23 billion in 2026 to reach USD 425.18 billion by 2031, at a CAGR of 11.27% during the forecast period (2026-2031). Rising deployment of IoT-enabled devices, the convergence of artificial intelligence with clinical workflows, and reimbursement models that now cover remote monitoring solutions are accelerating adoption. Government incentives such as Singapore’s USD 150 million GenAI programme and the European Health Data Space Regulation are standardising data exchange, reducing integration costs, and stimulating supplier investment. Strategic partnerships among device makers, cloud providers, and hospital systems are reshaping competitive strategies, while cybersecurity regulations tighten compliance requirements. Taken together, these forces propel the smart healthcare products market, even as capital-intensive infrastructure and data-privacy concerns temper the growth trajectory.

Key Report Takeaways

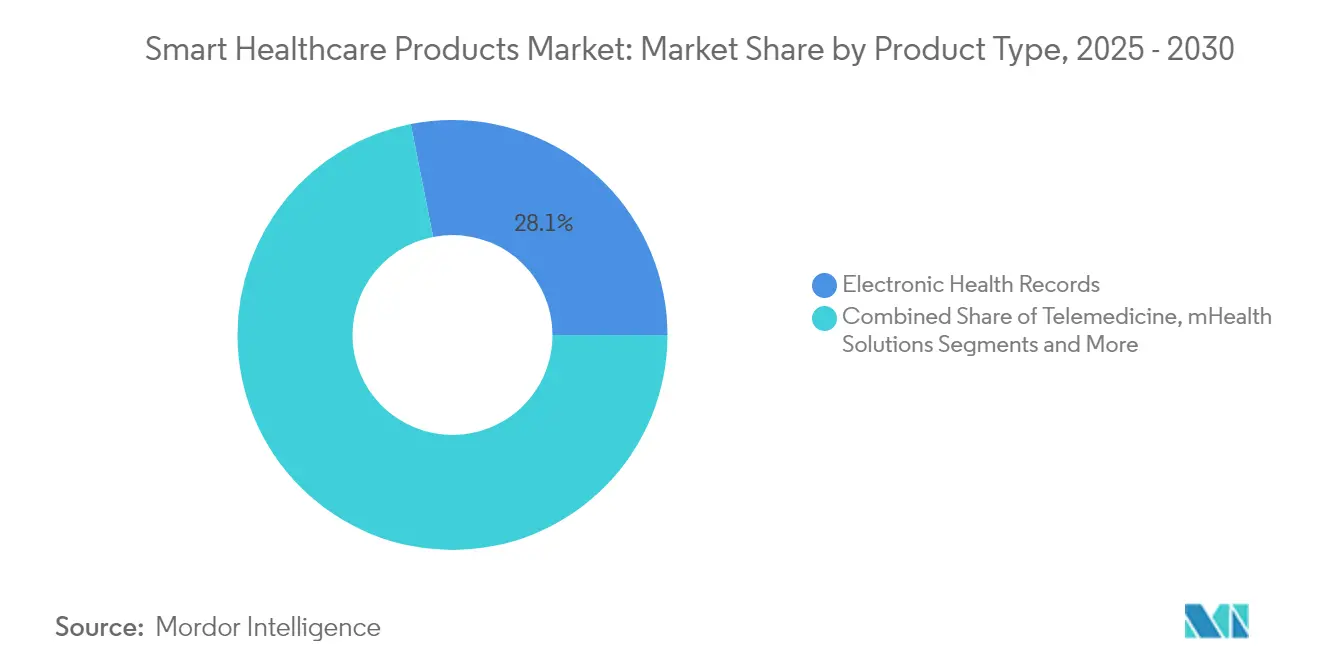

- By product type, Electronic Health Records commanded 28.11% of smart healthcare products market share in 2025; Smart Wearable Devices are projected to grow at a 18.87% CAGR to 2031.

- By application, Remote Monitoring accounted for 41.93% of the smart healthcare products market size in 2025, whereas Wellness & Preventive Care is advancing at a 17.43% CAGR through 2031.

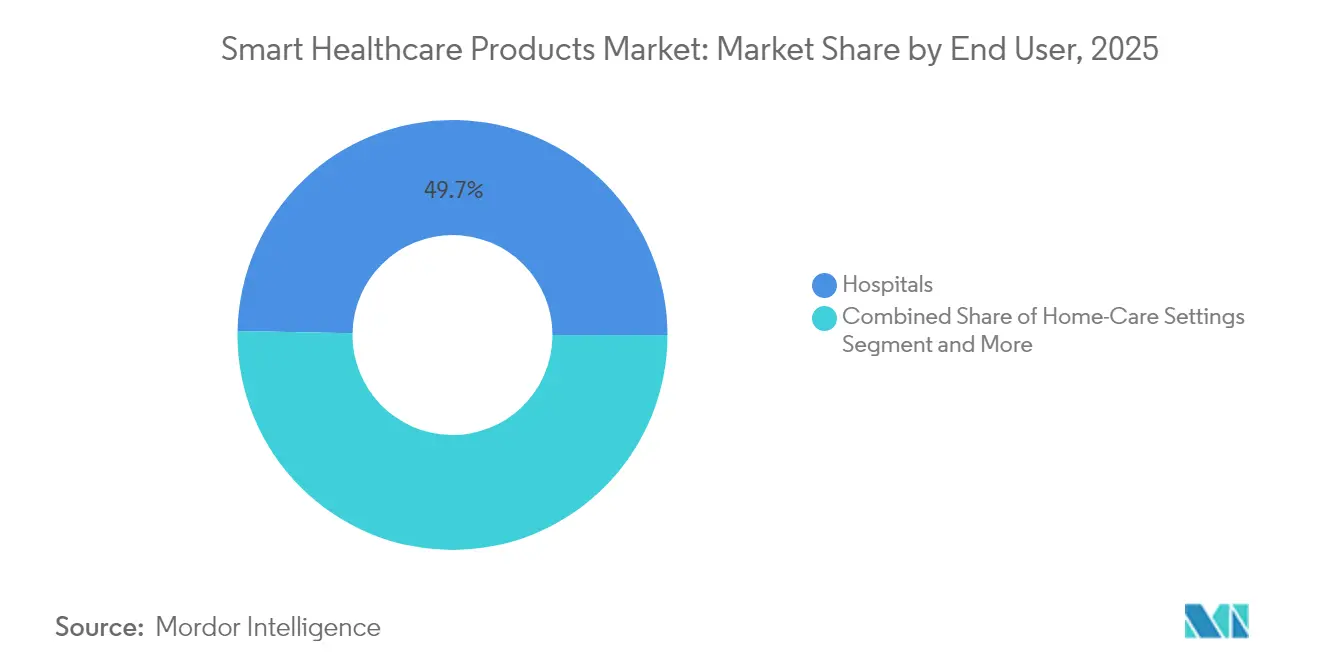

- By end user, Hospitals held 49.71% share of the smart healthcare products market size in 2025, while Home-Care Settings are expanding at a 18.79% CAGR.

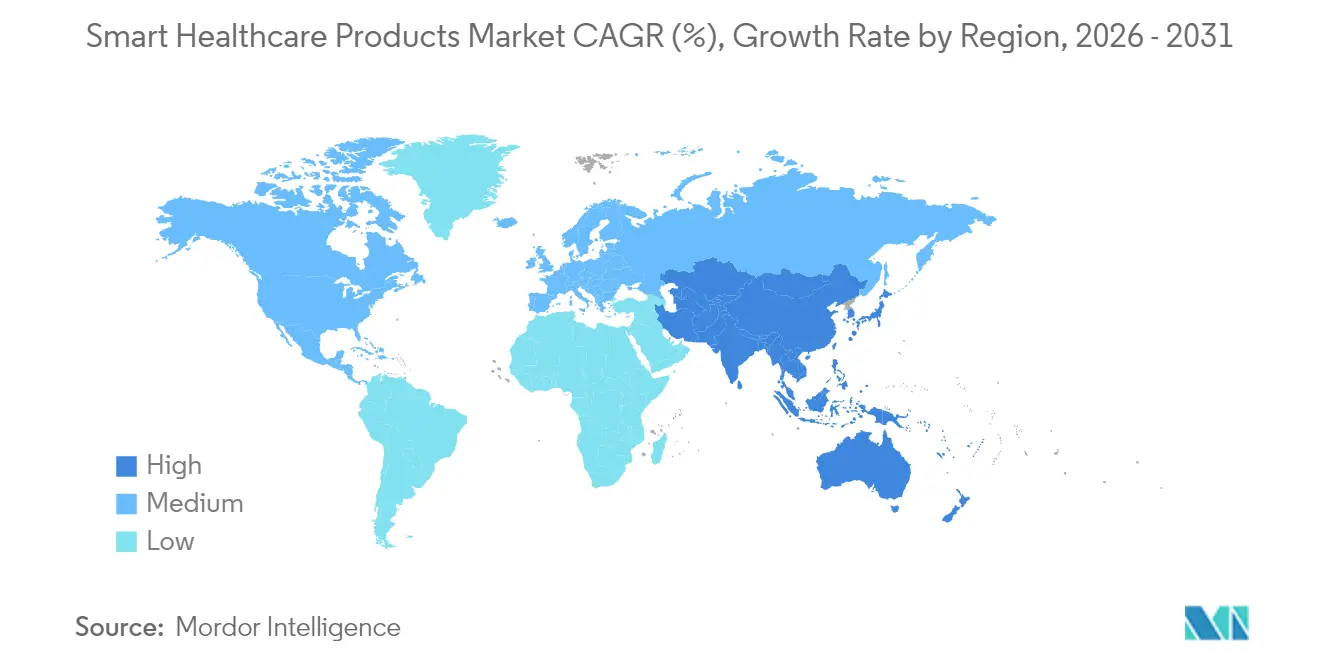

- By geography, North America retained the regional lead with 37.47% share in 2025; Asia-Pacific is the fastest-growing region at a 16.96% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Healthcare Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of IoT-enabled medical devices | +2.8% | Global with APAC leading growth | Medium term (2-4 years) |

| Escalating chronic-disease burden & ageing demographics | +2.1% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Government incentives for digital-health infrastructure | +1.9% | APAC & EU primary, North America secondary | Short term (≤ 2 years) |

| Broader reimbursement for telemedicine services | +1.7% | North America & EU | Medium term (2-4 years) |

| Wearable ultrasound & smart textiles for continuous care | +1.4% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Energy-efficient lightweight cryptography enabling ultra-low-power sensors | +1.1% | Global, technology-driven | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of IoT-Enabled Medical Devices

The proliferation of connected devices is reshaping clinical practice by capturing patient data in real time and delivering actionable insights at the point of care. Remote patient monitoring users in the United States are expected to surpass 71 million by 2025 as 5G networks lower transmission latency to 110 milliseconds, reducing packet loss to 0.07%[1]Nicolai Spicher et al., “Edge Computing in 5G Cellular Networks for Real-Time Analysis of Electrocardiography,” arxiv.org. Healthcare provider spending on edge computing is forecast to reach USD 10.3 billion in 2025, supporting predictive analytics for early-stage intervention. Asia-Pacific suppliers are rolling out AI-driven wearables that detect arrhythmia and glucose anomalies, creating new revenue pools and raising interoperability requirements. Device makers are embedding secure chipsets that consume 30% less power, extending battery life for long-term monitoring. Collectively, these factors improve clinical outcomes and drive volume growth across the smart healthcare products market.

Escalating Chronic-Disease Burden & Ageing Demographics

Chronic diseases accounted for 74% of global deaths in 2024, with the highest burden in Asia-Pacific economies. Continuous monitoring solutions reduce hospital readmissions by 85%, generating tangible savings for payers while enhancing patient satisfaction scores to 97%. An ageing population requires long-term care, triggering demand for smart beds, fall-detection sensors, and AI-enabled imaging. The economic upside is considerable, with AI projected to save up to USD 360 billion annually by trimming diagnostic errors and administrative overhead. Countries with universal healthcare systems are integrating smart healthcare products into chronic-disease programmes, accelerating volume deployment and standardising data exchange protocols.

Government Incentives for Digital-Health Infrastructure

Public-sector funding is catalysing digital transformation across care settings. South Korea has earmarked USD 830 million through 2032 for AI-based emergency care systems, including live bed-capacity dashboards and smart triage. Singapore committed USD 150 million to implement generative AI for clinical documentation and imaging analysis. The European Health Data Space Regulation, effective March 2025, sets interoperability standards, easing cross-border EHR access and fostering vendor competition[2]European Commission, “European Health Data Space Regulation,” europa.eu. These programmes shorten procurement cycles, raise digital-health literacy, and underpin the smart healthcare products market’s expansion phase.

Broader Reimbursement for Telemedicine Services

Medicare telehealth flexibilities extended through March 2025 allow beneficiaries to receive non-behavioral health consultations at home, with more than 250 reimbursable codes listed. The American Medical Association added 17 virtual-care billing codes, while commercial payers introduced payment parity rules. These measures incentivise providers to embed connected devices into chronic-care pathways and broaden access in rural areas. North American health systems now integrate RPM data into EHRs, enabling precise dosing and AI-guided alerts. Reimbursement certainty accelerates device procurement and helps suppliers move beyond pilot projects into scaled deployments across the smart healthcare products market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of smart healthcare ecosystems | -1.8% | Global, more pronounced in emerging markets | Short term (≤ 2 years) |

| Cyber-security & data-privacy concerns | -1.5% | Global, stricter in EU & North America | Medium term (2-4 years) |

| BLE protocol vulnerabilities triggering compliance delays | -1.2% | Global, affecting connected device adoption | Short term (≤ 2 years) |

| Supply-chain fragility for advanced mini-sensors | -0.9% | Global, semiconductor-dependent regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Smart Healthcare Ecosystems

Deploying IoT platforms, edge servers, and cybersecurity layers requires sizable upfront outlays that smaller providers struggle to finance. Proposed HIPAA revisions could cost regulated entities USD 9.3 billion in the first year, covering encryption, multifactor authentication, and training mandates. Legislators introduced the Health Infrastructure Security and Accountability Act, which budgets USD 1.3 billion for standards compliance but still leaves hospitals funding the bulk of upgrades. Capital intensity slows rollouts in emerging markets where reimbursement remains fee-for-service and margins are thinner. Vendors are responding with device-as-a-service contracts that spread costs over multi-year terms. Yet adoption timelines remain contingent on financing availability, weighing on near-term units shipped in the smart healthcare products market.

Cyber-Security & Data-Privacy Concerns

More than 180 million individuals were affected by healthcare data breaches in 2024, underscoring that patient information remains an attractive target. FDA guidance now requires manufacturers to submit software bill-of-materials documentation and implement patch management plans prior to device clearance. The heightened compliance bar increases engineering costs and extends time-to-market. Hospitals must layer zero-trust architectures atop legacy networks, diverting budgets from clinical modernization. Strict EU GDPR penalties further elevate risk, leading some providers to delay cross-border data-exchange projects. Consequently, cybersecurity concerns act as a drag on the smart healthcare products market, especially for smaller entrants with limited security resources.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: EHR Dominance Challenged by Wearable Innovation

Electronic Health Records contributed 28.11% to overall revenue in 2025, underlining their position as the data backbone of clinical workflows. National programmes such as Vietnam’s hospital-wide digitisation of 32 million patient files reaffirm government support, ensuring sustained licensing income for platform vendors. Oracle’s USD 3.5 billion budget application for the Veterans Affairs rollout further demonstrates institutional commitment to enterprise-scale implementations. Continuous user-experience upgrades and HL7 FHIR compliance solidify switching costs. The smart healthcare products market size for EHRs is projected to expand steadily, albeit at a single-digit rate, as penetration in primary care settings plateaus in developed economies.

Smart Wearable Devices, forecast to record a 18.87% CAGR, are capturing unmet needs in ambulatory monitoring. FDA-cleared innovations such as cuffless blood-pressure monitors and wrist-based pulse detection broaden clinical acceptability. Start-ups leverage cloud connectivity and AI algorithms to offer subscription-based analytics, reducing reliance on hardware margins. Device makers embed over-the-air update pipelines that keep software current, extending product life and service revenue. The smart healthcare products market size for wearables is therefore positioned for outsized expansion relative to other device classes.

Parallel segments play supporting roles. Telemedicine Platforms integrate wearables into virtual-care visits, while Smart Pills gain traction in gastrointestinal diagnostics following FDA De Novo clearance for blood detection. Smart RFID Cabinets protect high-value consumables, cutting inventory shrinkage by up to 15% and improving compliance with chain-of-custody mandates. Investments in smart hospital infrastructure, such as Siemens’ deployment of 7,000 IoT sensors at Kantonsspital Baden, illustrate growing end-to-end integration across the smart healthcare products market.

By Application: Remote Monitoring Leads Preventive Care Revolution

Remote Monitoring held 41.93% share in 2025, underpinned by proven reductions in readmissions and payer reimbursement structures that incentivise home-based care. The United States market alone is expected to double from USD 14-15 billion in 2024 to more than USD 29 billion by 2030. Providers integrate RPM dashboards within EHRs to trigger alerts, enhancing care-team efficiency. Commercial insurers now couple premium discounts with validated device utilisation, encouraging patient engagement. Consequently, the smart healthcare products market share associated with remote monitoring retains momentum throughout the forecast window.

Wellness & Preventive Care, advancing at a 17.43% CAGR, benefits from rising consumer interest in proactive health. AI-powered full-body MRI solutions illustrate how early detection reduces downstream treatment costs. Corporate wellness programmes reimburse employees for wearables that track sleep, stress, and activity, expanding addressable demand. Diagnostics segments apply machine-learning algorithms to imaging and laboratory data, cutting false positives and expediting treatment decisions. Treatment & Drug-Delivery applications incorporate smart pills with targeted release, improving adherence. Storage & Inventory Management leverages IoT cabinets to shorten restocking cycles and lower waste, reinforcing operational efficiencies across the smart healthcare products market.

By End User: Hospitals Maintain Leadership as Home Care Accelerates

Hospitals generated 49.71% of total revenue in 2025, leveraging established infrastructure and high patient throughput. Multi-year alliances such as GE HealthCare’s seven-year agreement with Sutter Health cover 300 facilities and integrate AI-based imaging across radiology workflows. Investments in predictive maintenance for imaging scanners and smart operating theatres provide incremental efficiency gains, retaining hospital dominance within the smart healthcare products market.

Home-Care Settings are forecast to grow at a 18.79% CAGR as shifting demographics and reimbursement flexibility favour decentralised care. Medicare policy now allows audio-only telehealth for specific chronic conditions, expanding access for digitally constrained populations. FDA-cleared consumer devices, including over-the-counter glucose monitors and nasal-congestion wearables, empower self-management and reduce clinic visits. Specialty Clinics deploy disease-specific dashboards that integrate imaging AI, while Ambulatory Surgical Centers attach disposable sensors to post-operative patients, lowering complications. Long-Term Care Facilities implement fall-detection beacons and smart mattresses, trimming adverse events. These deployments collectively reinforce revenue diversification across the smart healthcare products market.

Geography Analysis

North America retained 37.47% revenue share in 2025, buoyed by sophisticated payer systems, advanced infrastructure, and sizeable venture capital flows. Federal initiatives such as the ARPA-H Women’s Health Sprint, which committed more than USD 100 million to digital health research, strengthen the innovation pipeline. Medicare’s extension of telehealth flexibilities through 2025 further entrenches remote monitoring usage and stabilises supplier demand. Canada complements the region’s dynamism by launching the Infoway Centre for Clinical Innovation to foster standards-based interoperability. Strong cybersecurity oversight in both countries ensures continued investment despite breach headlines.

Asia-Pacific delivers the fastest CAGR at 16.96% thanks to coordinated national strategies, expanding middle-class populations, and unmet clinical demand in rural areas. Singapore’s five-year USD 150 million GenAI plan fast-tracks imaging AI and automated record transcription across public hospitals. South Korea allocates USD 830 million for AI-enabled emergency systems, setting benchmarks for real-time patient transfer management. Southeast Asia’s digital health revenue is poised to reach USD 6.1 billion in 2024, with investors attracted to high smartphone penetration and supply-demand gaps. Australia’s Health Connect platform promotes seamless data sharing, accelerating provider onboarding.

Europe benefits from the European Health Data Space Regulation, effective March 2025, setting a single market for digital health services and supporting projects such as Xt-EHR and EUVAC. Unified rules reduce vendor fragmentation and encourage cross-border telemedicine. National health systems in Germany and France have rolled out e-prescription mandates, underlining commitment to digitalisation. In the Middle East and Africa, South Africa pilots national e-health strategies, while Gulf Cooperation Council states invest in smart hospital builds. South America shows momentum, particularly in Brazil where urbanisation and private insurance uptake fuel demand, although macroeconomic volatility moderates growth. Overall, geographic diversification balances expansion risks and underpins sustained growth across the smart healthcare products market.

Competitive Landscape

The competitive arena is moderately concentrated, with the top three manufacturers—Philips Healthcare, Abbott, and Medtronic—controlling significant revenue, while a long tail of niche providers supplies specialised hardware and software modules. Industry rivalry centres on platform interoperability rather than outright hardware displacement, prompting alliances between medtech incumbents and cloud hyperscalers.

Strategic partnerships typify current strategy. Abbott linked its continuous glucose monitoring sensor to Medtronic insulin pumps, unlocking an estimated USD 700-850 million incremental market[3]Abbott, “Global Partnership to Connect CGM Sensors with Insulin Delivery Devices,” abbott.mediaroom.com. GE HealthCare collaborates with Amazon Web Services to co-develop generative-AI diagnostic tools, leveraging AWS’s machine-learning stack to analyse multi-modal data. Medtronic’s tie-up with Philips integrates pulse oximetry and capnography into Philips’ monitoring systems, expanding access for hospitals seeking a unified user interface.

Acquisition activity targets digital platforms and AI algorithms. Boston Scientific’s focus on interventional cardiology and Johnson & Johnson’s investment in robotic surgery illustrate buyers’ intent to control data-rich ecosystems. Venture capital funds channel resources into start-ups offering device-agnostic analytics, potentially positioning them as acquisition targets. Price competition remains contained due to regulation and high switching costs, while intellectual-property portfolios provide defensive moats. Continuous product improvements and recurring software upgrades sustain margin profiles and support future cash flow across the smart healthcare products market.

Smart Healthcare Products Industry Leaders

Abbott Laboratories

GE Healthcare

Koninklijke Philips N.V.

Medtronic plc

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Medtronic announced a strategic partnership with Philips to integrate next-generation Nellcor pulse oximetry and Microstream capnography into Philips’ patient-monitoring systems, broadening global access to advanced respiratory insights.

- June 2025: The FDA approved the Sonu Band, an AI-enabled wearable that treats moderate-to-severe nasal congestion in adolescents, providing the first drug-free solution for rhinitis that demonstrates over 80% user improvement within 15 minutes.

Global Smart Healthcare Products Market Report Scope

As per the scope of the report, smart healthcare products improve outcomes related to diagnostic tools and enhance patient treatment, along with improving their quality of life. Smart health products come with embedded communication, sensor technologies, and data analytics techniques. These products are used for monitoring individuals physically for diagnosis and ongoing disease treatments.

The smart healthcare products market is expected to register a CAGR of 8.5% over the forecast period. The smart healthcare products market is segmented by product type (telemedicine, electronic health records, mHealth, smart pills and syringes, and smart RFID cabinets), application (storage and inventory management, monitoring, treatment, and other applications), end user (hospitals, home care settings, and other end users), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the market size and forecasts in value (USD million) for the above segments.

| Telemedicine |

| Electronic Health Records |

| mHealth Solutions |

| Smart Pills |

| Smart Syringes |

| Smart RFID Cabinets |

| Smart Wearable Devices |

| Smart Hospital Infrastructure |

| Storage & Inventory Management |

| Remote Monitoring |

| Diagnostics |

| Treatment & Drug-Delivery |

| Wellness & Preventive Care |

| Hospitals |

| Home-Care Settings |

| Specialty Clinics |

| Ambulatory Surgical Centers |

| Long-Term Care Facilities |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | Saudi Arabia | |

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Product Type | Telemedicine | ||

| Electronic Health Records | |||

| mHealth Solutions | |||

| Smart Pills | |||

| Smart Syringes | |||

| Smart RFID Cabinets | |||

| Smart Wearable Devices | |||

| Smart Hospital Infrastructure | |||

| By Application | Storage & Inventory Management | ||

| Remote Monitoring | |||

| Diagnostics | |||

| Treatment & Drug-Delivery | |||

| Wellness & Preventive Care | |||

| By End User | Hospitals | ||

| Home-Care Settings | |||

| Specialty Clinics | |||

| Ambulatory Surgical Centers | |||

| Long-Term Care Facilities | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | Saudi Arabia | ||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the smart healthcare products market?

The market stands at USD 249.23 billion in 2026 and is projected to reach USD 425.18 billion by 2031 with an 11.27% CAGR.

Which product category holds the largest share?

Electronic Health Records lead with 28.11% revenue share in 2025 due to mandated digitisation programmes.

Why is Asia-Pacific witnessing the fastest growth?

Coordinated government funding, expanding healthcare infrastructure, and rising chronic-disease prevalence drive a 16.96% CAGR in the region.

How do cybersecurity regulations impact adoption?

Stricter HIPAA and GDPR rules raise compliance costs and lengthen development timelines, moderating near-term device rollouts.

What role do strategic partnerships play in market competition?

Alliances allow companies to integrate complementary technologies, accelerate product roadmaps, and enhance interoperability without major acquisitions.

Page last updated on: