Healthcare E-Commerce Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.62 Trillion |

| Market Size (2031) | USD 1.43 Trillion |

| Growth Rate (2026 - 2031) | 18.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

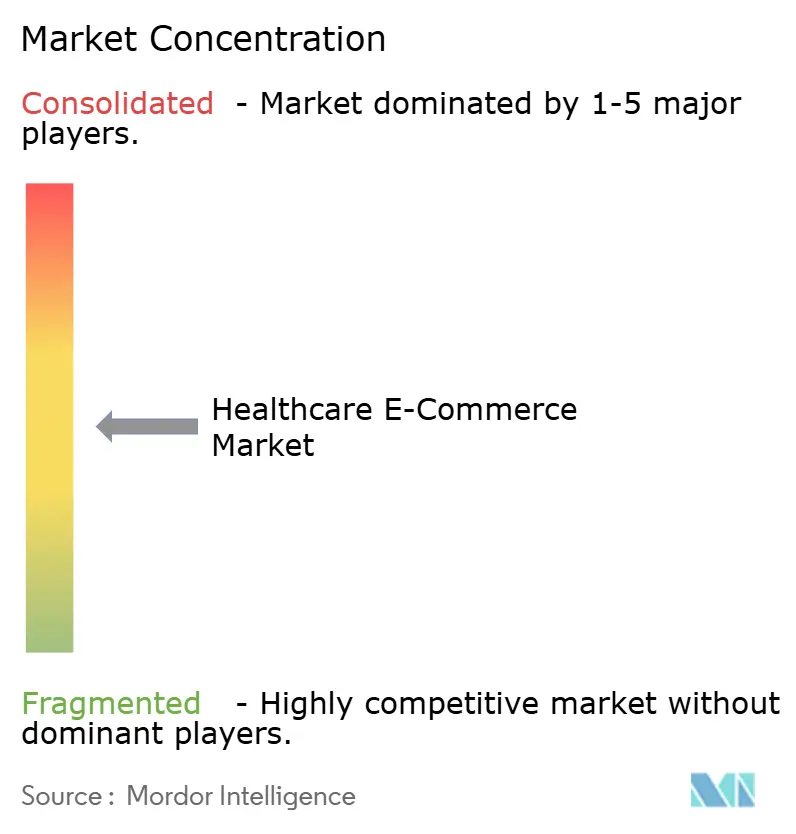

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Healthcare E-Commerce Market Analysis by Mordor Intelligence

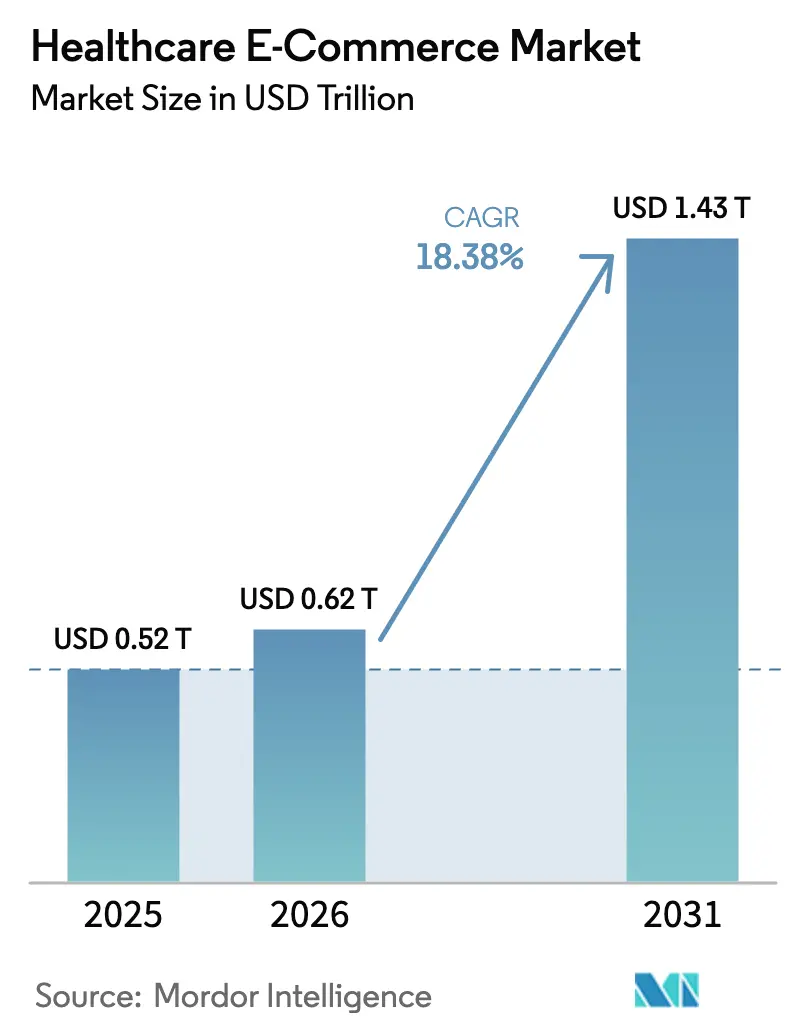

Healthcare E-Commerce Market size in 2026 is estimated at USD 0.62 trillion, growing from 2025 value of USD 0.52 trillion with 2031 projections showing USD 1.43 trillion, growing at 18.38% CAGR over 2026-2031. Growth continues to accelerate as regulators modernize telemedicine rules, technology giants deepen retail-clinic integration, and consumers demand seamless digital care journeys. The DEA’s proposed three-tier telemedicine registration system is creating clear pathways for prescribing controlled substances online, while Amazon’s strong Q4 2024 revenue confirms that scale players can monetize healthcare storefronts alongside retail operations. Prescription drugs remain the highest-volume category, but connected medical devices and consumables are advancing fastest as at-home diagnostics and wearables blur the line between treatment and monitoring. At the same time, caregiving services gain momentum as aging populations favor virtual support models over institutional settings, prompting incumbents to pivot from storefronts to platform-based care delivery.

Key Report Takeaways

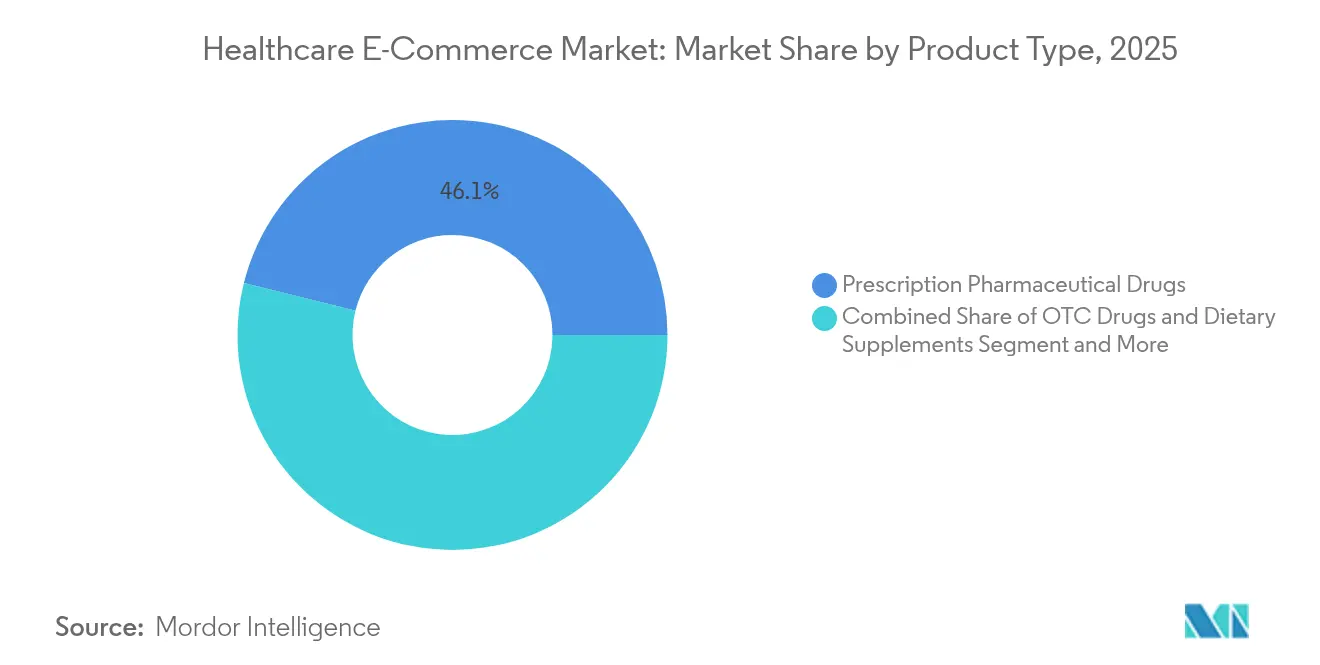

- By product type, prescription drugs led with 46.12% of healthcare e-commerce market share in 2025, while medical devices and consumables are projected to expand at a 19.24% CAGR to 2031.

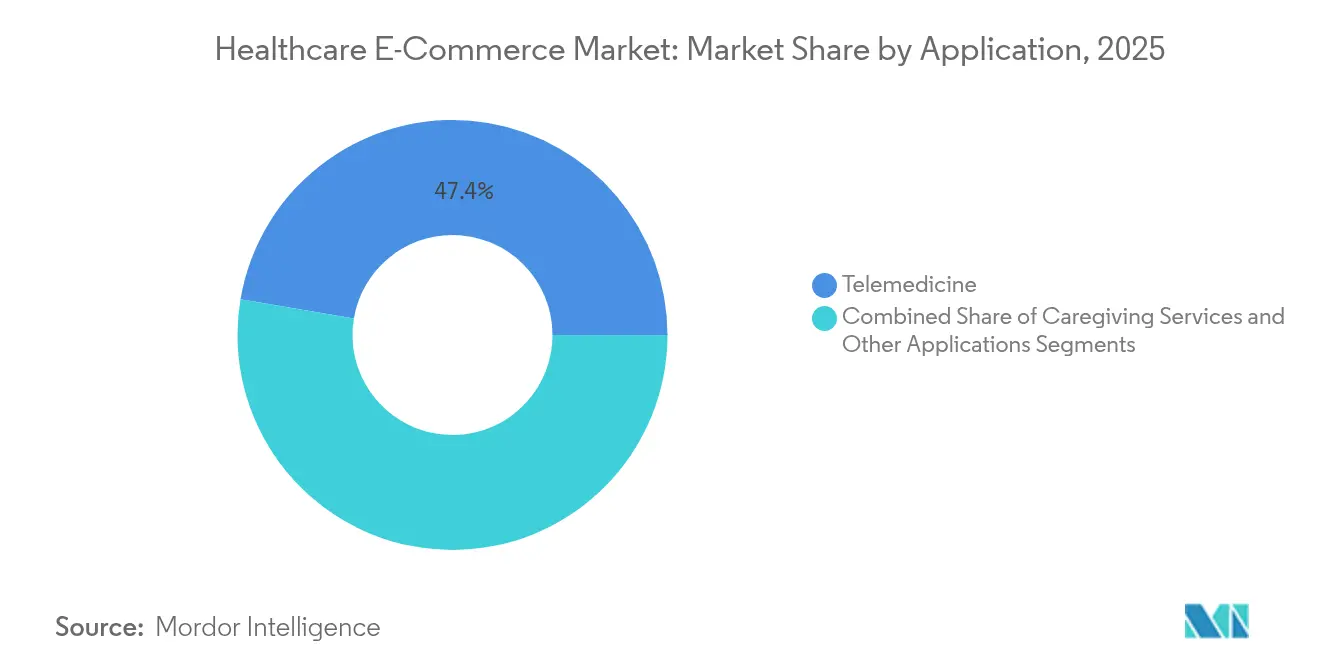

- By application, telemedicine accounted for 47.35% of the healthcare e-commerce market size in 2025; caregiving services are poised for the fastest growth at 20.31% CAGR through 2031.

- By geography, North America commanded 39.55% revenue share of the healthcare e-commerce market in 2025, whereas Asia-Pacific is forecast to post a 20.58% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare E-Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Internet and Smartphone Penetration | +3.2% | Global, with strongest impact in APAC and MEA | Medium term (2-4 years) |

| Escalating Healthcare Costs Driving Online Affordability | +4.1% | North America and Europe core, expanding to emerging markets | Long term (≥ 4 years) |

| Pandemic-Accelerated Consumer Acceptance of e-Pharmacy | +2.8% | Global, with sustained momentum in developed markets | Short term (≤ 2 years) |

| Micro-Fulfilment Robotics Enabling <2-Hour Urban Delivery | +2.4% | North America and Europe urban centers, expanding to APAC | Medium term (2-4 years) |

| AI-Driven Adherence Tools Boosting Refill Compliance | +1.9% | Global, with early adoption in North America and Europe | Long term (≥ 4 years) |

| e-Prescription Fast-lane Laws Unlocking Cross-Border Sales | +3.1% | North America and Europe, with emerging regulatory frameworks in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Internet and Smartphone Penetration

Mobile broadband coverage keeps widening, and affordable handsets now reach price points accepted by mass-market consumers across Southeast Asia and Africa. This connectivity allows real-time video consultations and medicine orders in territories where clinic density is low, creating the network effects that propel early-mover platforms. Growing 5G rollouts add bandwidth for rich clinical data exchanges, reinforcing the expectation that everyday health interactions should be smartphone-first. The shift toward mobile-first healthcare experiences fundamentally alters consumer expectations, demanding seamless integration between health monitoring, consultation, and product fulfillment within unified digital ecosystems.

Escalating Healthcare Costs Driving Online Affordability

United States out-of-pocket spending continues to rise, prompting households to compare prices across web pharmacies. Amazon introduced fixed subscription pricing for conditions such as erectile dysfunction, undercutting traditional clinics and exposing opaque mark-ups. Direct-to-consumer models like Cost Plus Drugs bypass PBMs and publish acquisition costs, which resonates in markets where insurance deductibles leave consumers sensitive to cash prices. As national health expenditures are projected to reach USD 485 billion in 2025, competitive pricing online is becoming a primary lever for both payers and patients.

Pandemic-Accelerated Consumer Acceptance of e-Pharmacy

Lockdowns normalized virtual care and shifted preference structures; 90% of new telehealth users plan to continue post-pandemic services. Regulatory continuity matters: the DEA extended telemedicine flexibilities through 2025, ensuring physicians can keep prescribing without in-person exams.[1]Source: Centers for Medicare & Medicaid Services, “Medicare Prescription Drug Benefit Program; Health IT Standards,” federalregister.gov Providers report higher medication adherence among digitally engaged patients, which further encourages insurers to reimburse virtual channels. Healthcare organizations report that patients who adopted digital services during the pandemic demonstrate higher engagement rates and better adherence to treatment protocols, creating clinical outcomes that justify continued investment in e-commerce capabilities.

Micro-Fulfilment Robotics Enabling <2-Hour Urban Delivery

Walgreens now operates robotic centers that fill 16 million prescriptions each month, cutting fulfillment costs 13% and enabling same-day dispatch to more than 5,000 stores. Simultaneously, drone operators such as Zipline distribute supplies for hospital-at-home programs, demonstrating that medical items can move as quickly as groceries. These investments condition urban patients to expect near-instant access to chronic and acute therapies, making delivery speed a competitive differentiator across the healthcare e-commerce market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Uncertainty and Rx-Compliance Hurdles | -2.7% | Global, with highest impact in emerging markets | Medium term (2-4 years) |

| Data-Privacy and Cybersecurity Concerns | -1.8% | Global, with stricter enforcement in Europe and North America | Long term (≥ 4 years) |

| Escalating Digital-Ad Acquisition Costs | -1.4% | North America and Europe, expanding to competitive APAC markets | Short term (≤ 2 years) |

| PBM / Wholesaler Margin Pressure on e-Pharmacies | -2.3% | North America core, with emerging challenges in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Cybersecurity Concerns

The increasing sophistication of cyber threats targeting healthcare data creates operational risks and compliance costs that constrain platform growth and consumer adoption. Healthcare data remains a prime ransomware target; 725 breaches hit the US sector in 2023 alone. The Health Infrastructure Security and Accountability Act now mandates annual audits, inflating compliance budgets for cloud-hosted pharmacies.[2]Source: Maynard Nexsen, “Health Infrastructure Security and Accountability Act,” maynardnexsen.com The regulatory response includes mandatory breach notification requirements and potential penalties for non-compliance, creating ongoing operational risks that constrain platform expansion and increase customer acquisition costs.

Escalating Digital-Ad Acquisition Costs

Ad inventory has tightened as incumbents and newcomers chase the same patient segments online. Amazon’s national television and streaming blitz supporting same-day prescription delivery set a cost benchmark that niche players cannot match. PBM trade groups launched counter-campaigns urging price reforms, further inflating bidding prices on social channels.[3]Source: Zoey Becker, “PBMs call out big drugmakers in new digital ads,” Fierce Pharma, fiercepharma.com The shift toward performance-based advertising models, where platforms must demonstrate measurable health outcomes to justify marketing investments, increases the complexity and cost of customer acquisition campaigns while potentially limiting reach to patients who might benefit from e-commerce alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Prescriptions Anchor Demand, Devices Accelerate Upsell

Prescription drugs generated 46.12% of healthcare e-commerce market revenue in 2025 as maturing e-prescription rails and consumer habit shifts cemented online ordering. Medical devices and consumables, however, are forecast to expand at 19.24% CAGR to 2031, the highest among all categories. Connected blood-glucose monitors, smart inhalers, and at-home diagnostics illustrate how traditional devices evolve into data-rich services, deepening platform engagement. The FDA’s Digital Health Advisory Committee, created in 2024, offers guidance that encourages AI integration in device software, reducing regulatory ambiguity. Customized 3D-printed orthotics and braces further differentiate online catalogues from brick-and-mortar inventories, supporting premium pricing and subscription-based replenishment models.

IoT connectivity also facilitates automatic resupply prompts, ensuring that high-margin consumables remain in stock without patient intervention. OTC supplements benefit from influencer marketing and wellness subscription bundles, broadening the addressable audience. As manufacturing digitizes, lower batch sizes become economical, enabling niche SKUs such as allergen-free medical consumables to flourish in the healthcare e-commerce market. With these tailwinds, segment leaders are investing in predictive analytics to forecast demand spikes around seasonal ailments, reducing stockouts and enhancing customer satisfaction.

By Application: Telemedicine Plateaus, Caregiving Services Scale Up

Telemedicine retained 47.35% share of the healthcare e-commerce market size in 2025, supported by continued reimbursement parity and renewed patient familiarity with video consultations. Yet caregiving services are on track for a 20.31% CAGR through 2031, reflecting consumer desire for holistic support and the reality of workforce shortages in traditional long-term care. Platforms now bundle medication management, meal delivery, and caregiver coordination inside unified dashboards, transferring administrative burden away from families.

Demographic pressure intensifies the trend: adults over 60 already comprise 22% of the ASEAN population and will keep rising. Uber Health’s logistics-as-a-service, launched in 2024, illustrates how non-traditional entrants can solve transportation gaps and monetize through pay-per-ride or subscription models. AI-enabled social robots such as ElliQ extend companionship and behavioral monitoring, demonstrating the breadth of non-clinical services that now fit comfortably inside the healthcare e-commerce market offer set.

Geography Analysis

North America dominates with 39.55% of 2025 revenue thanks to a well-defined reimbursement route for digital scripts, broad insurance coverage, and consumer familiarity with one-click purchasing. The DEA’s structured telemedicine license proposal plus CMS interoperability standards reduce compliance risk, maintaining investor confidence. Amazon’s same-day prescription service reaches nearly half the US population, illustrating how reliable logistics amplify platform stickiness. Competition among PBMs remains a structural headwind, but it also sparks innovation in transparent pricing models and encourages fresh policy conversation that could benefit digital-first entrants.

Asia-Pacific is the fastest-growing region, forecast at 20.58% CAGR from 2026 to 2031. Government incentives to digitize primary care, such as China’s internet hospital framework, are closing access gaps in remote provinces. Venture funding continues to flow: Indonesian, Vietnamese, and Philippine healthtech startups each raised nine-figure rounds in 2024, focused on mobile triage, e-pharmacy, and chronic disease apps. As middle-class consumers increase discretionary health spending, platform operators tailor vernacular language interfaces and mobile wallets to capture wallet share.

Europe, the Middle East & Africa, and South America exhibit mixed readiness. Gulf Cooperation Council states still lack harmonized e-pharmacy laws, producing both green-field upside for first movers and compliance ambiguity that deters conservative investors. In South America, Brazil and Mexico lead adoption through public-private telemedicine partnerships, but logistics complexity and lower credit-card penetration slow checkout conversion rates compared with peers.

Competitive Landscape

Competition is intensifying as retailers, payers, and tech firms vie for platform primacy in the healthcare e-commerce market. Amazon reorganized its health division into six focused units in 2025 to streamline decision making and accelerate partner integrations, following its USD 3.9 billion One Medical acquisition. CVS Health reported USD 97.71 billion Q4 2024 revenue and leverages insurance subsidiary Aetna’s membership base to cross-sell digital pharmacy services at preferential copay tiers. Walgreens is countering with robotic micro-fulfillment nodes that lower unit costs and free pharmacists for clinical counseling, a tactic expected to process 40% of prescription volume by year-end 2025.

Private equity is embracing consolidation themes: Sycamore Partners agreed to purchase Walgreens for USD 23.7 billion in March 2025, betting that a capital-intensive supply-chain overhaul can unlock value under private ownership. Specialized challengers such as GoodRx rolled out white-label storefronts for regional grocers, capturing traffic from consumers seeking loyalty rewards tied to grocery purchases. Meanwhile, Hims & Hers’ European expansion shows that brand-led telehealth models can scale rapidly once regulatory permissions are in place.

Across all regions, AI is becoming table stakes. Platforms incorporate generative models to automate refill reminders, eligibility checks, and formulary optimization. The FDA’s 2024 guidance on change-control plans has clarified safety documentation, encouraging agile deployment of algorithm updates. As capital costs rise, mid-tier players are forming purchasing alliances and exploring joint micro-fulfillment hubs to achieve scale benefits comparable with category leaders.

Healthcare E-Commerce Industry Leaders

-

Amazon (Amazon Pharmacy)

-

Walmart, Inc.

-

Owens & Minor Inc

-

Alibaba Health

-

CVS Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Wheel and Amazon Pharmacy unveiled an integrated medication-access module that embeds prescription checkout into virtual visit workflows.

- February 2025: Health-E Commerce partnered with LifeMD to discount obesity medications by 50% for FSA and HSA Store customers.

- January 2025: Teladoc Health joined Amazon’s Health Benefits Connector so eligible workers can self-enroll in diabetes and hypertension programs directly from their Amazon account.

- February 2024: NextPlat Corp launched OPKO Health-branded online storefronts in China. This new online store offers wellness products, including nutraceuticals and supplements, to the Chinese people.

Global Healthcare E-Commerce Market Report Scope

As per the report's scope, healthcare e-commerce refers to the online buying and selling of healthcare products, services, and pharmaceuticals through digital platforms and online marketplaces.

The healthcare e-commerce market is segmented by product type, application, and geography. By product type, the market is segmented into pharmaceutical drugs, health and wellness products, and medical devices. By application, the market is segmented into telemedicine, caregiving services, and others. The report also covers the market sizes and forecasts in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Prescription Pharmaceutical Drugs |

| OTC Drugs and Dietary Supplements |

| Medical Devices and Consumables |

| Wellness and Personal-Care Products |

| Telemedicine |

| Caregiving Services |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Prescription Pharmaceutical Drugs | |

| OTC Drugs and Dietary Supplements | ||

| Medical Devices and Consumables | ||

| Wellness and Personal-Care Products | ||

| By Application | Telemedicine | |

| Caregiving Services | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the healthcare e-commerce market?

The healthcare e-commerce market size is USD 0.62 trillion in 2026 and is projected to grow to USD 1.43 trillion by 2031.

Which product category leads healthcare e-commerce sales?

Prescription drugs hold the largest share at 46.12% in 2025, driven by mature e-prescription infrastructure and consumer familiarity.

Why is Asia-Pacific the fastest-growing regional market?

Rapid smartphone adoption, supportive government policies, and rising middle-class health spending push the region toward a 20.58% CAGR between 2026 and 2031.

How are robotics influencing online pharmacy logistics?

Micro-fulfillment centers equipped with robots can process millions of prescriptions monthly, cutting costs 13% and enabling same-day delivery for urban customers.

What regulatory changes could reshape digital prescribing?

CMS e-prescription standards and the DEA’s proposed telemedicine registration tiers will standardize electronic workflows and may open cross-border fulfillment opportunities once fully implemented.

Page last updated on: