Global Smart Medical Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

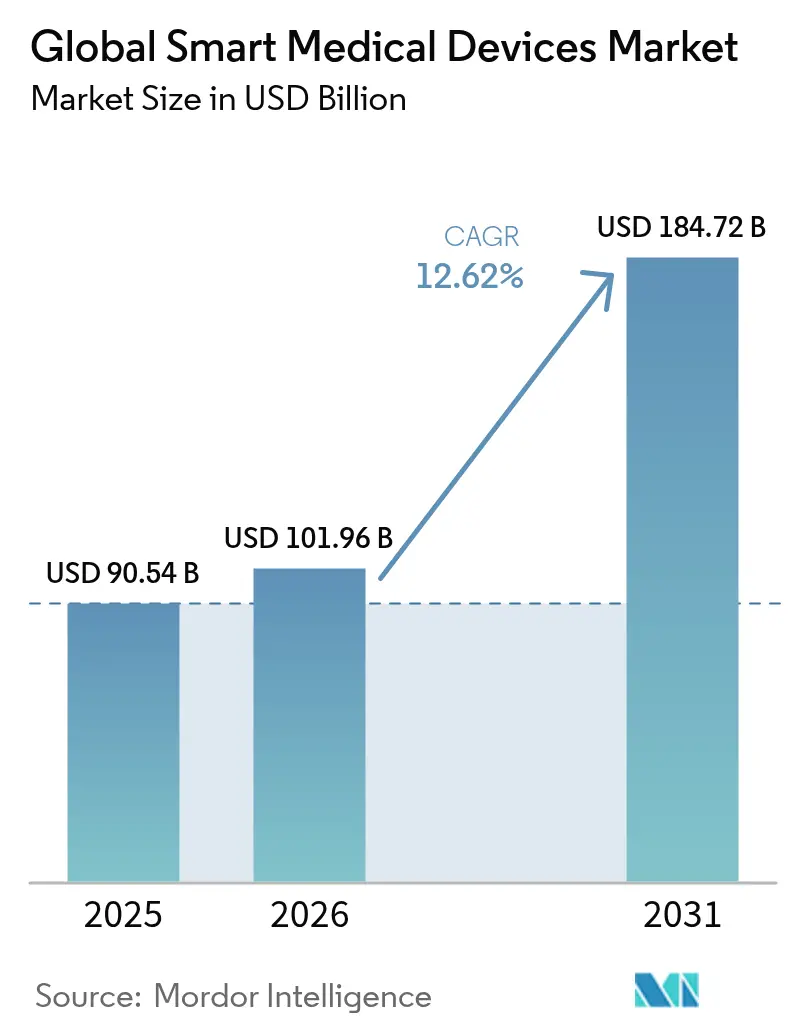

| Market Size (2026) | USD 101.96 Billion |

| Market Size (2031) | USD 184.72 Billion |

| Growth Rate (2026 - 2031) | 12.62% CAGR |

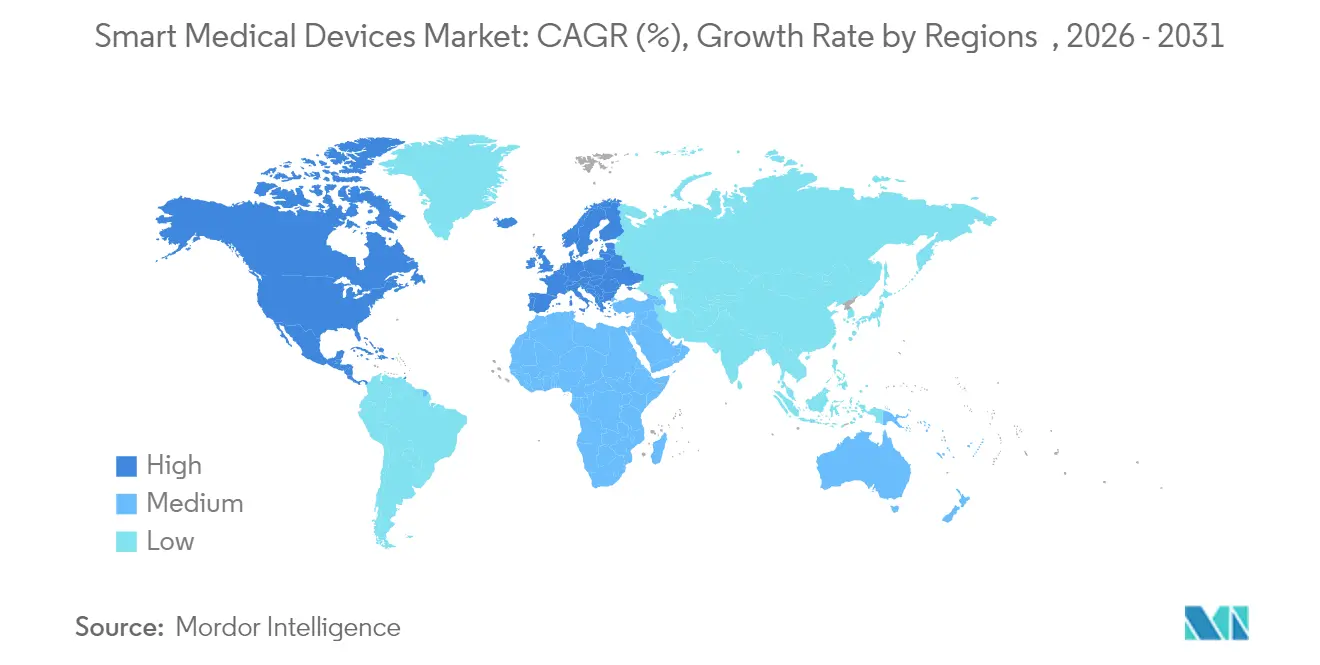

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Smart Medical Devices Market Analysis by Mordor Intelligence

The smart medical devices market size was valued at USD 90.54 billion in 2025 and estimated to grow from USD 101.96 billion in 2026 to reach USD 184.72 billion by 2031, at a CAGR of 12.62% during the forecast period (2026-2031). Continuous progress in artificial intelligence, edge-enabled 5G connectivity and miniaturized sensors is allowing clinicians to pair near-real-time diagnostics with long-range data sharing. Regulatory clarity has improved as the FDA’s 2025 draft guidance sets performance baselines for software-as-a-medical-device, which in turn is lowering investment risk and encouraging broader product pipelines. Accelerating demand for at-home chronic-disease management, combined with large technology firms collaborating with established device makers, is reshaping distribution models and shortening upgrade cycles. Hospitals are using connectivity to reduce readmissions, while value-based payment policies reward providers that deploy continuous monitoring to demonstrate measurable outcome gains. Semiconductor constraints and cybersecurity obligations still add cost pressure, yet component innovation and subscription pricing are helping to offset capital hurdles for smaller facilities.

Key Report Takeaways

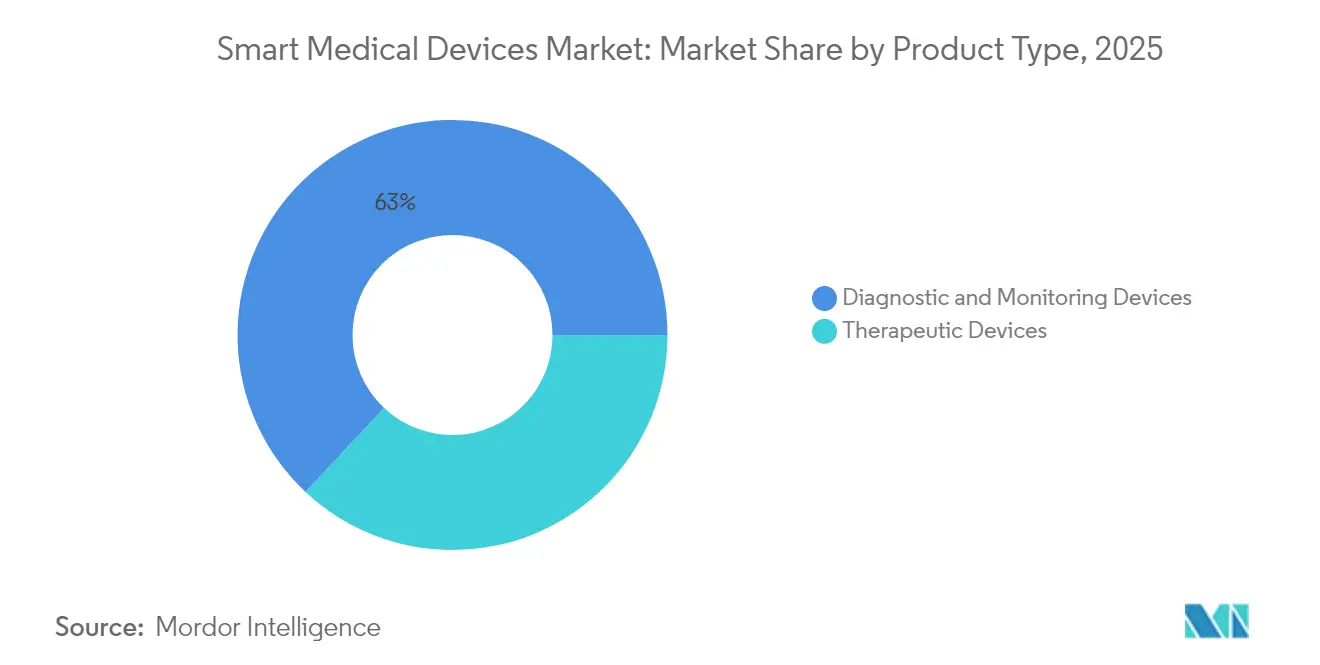

- By product type, diagnostic and monitoring devices captured 63.02% of the smart medical devices market share in 2025, while therapeutic devices are projected to post the quickest CAGR through 2031.

- By end user, hospitals and clinics accounted for 45.74% of the smart medical devices market size in 2025; home-care settings are growing the fastest at 13.72% CAGR.

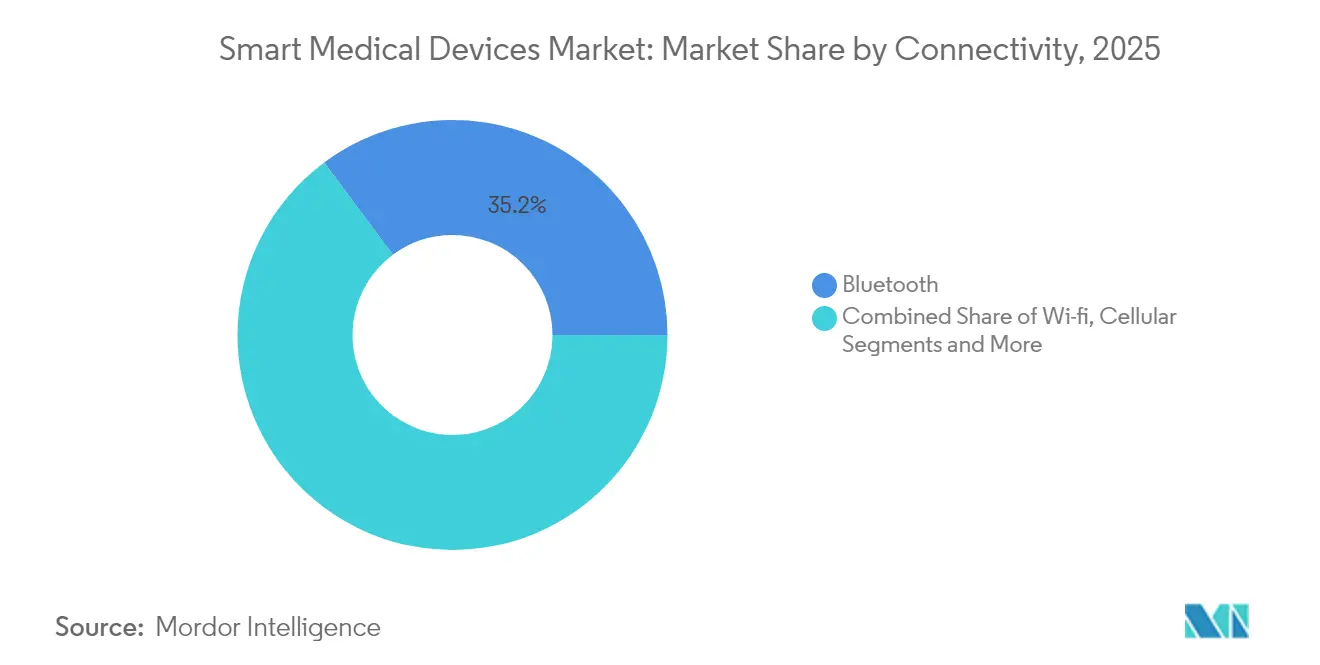

- By connectivity, Bluetooth held 35.18% revenue in 2025, whereas cellular/5G platforms record the steepest adoption curve over the forecast horizon.

- By geography, North America led with 43.02% share in 2025; Asia-Pacific is the fastest-expanding region at a 15.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Medical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone-enabled & wireless adoption surge | +2.1% | Global, with North America & APAC leading | Medium term (2-4 years) |

| Rapid technological breakthroughs in sensors & AI | +2.8% | North America & EU core, spill-over to APAC | Long term (≥ 4 years) |

| Rising fitness & wellness awareness | +1.4% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Growing chronic-disease burden (diabetes, CVD) | +2.3% | Global, with highest impact in aging populations | Long term (≥ 4 years) |

| 5G + edge-AI enabling real-time remote diagnostics | +1.9% | APAC core, expanding to North America & EU | Medium term (2-4 years) |

| Value-based reimbursement rewarding continuous monitoring | +1.7% | North America primary, EU secondary | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Smartphone-enabled and Wireless Adoption Surge

Wearable ownership reached 44.5% of U.S. adults in 2024, reflecting the appeal of mobile-paired health devices that fit daily routines [1]Journal of Medical Internet Research, “Wearable Device Adoption in U.S. Adults,” jmir.org. Device makers now preload HIPAA-compliant encryption and deliver data directly to cloud dashboards that clinicians can audit in near real time. Apple’s FDA-cleared arrhythmia tracking and emergency cardiac-alert features illustrate how consumer electronics firms translate mainstream design into clinical benefit. This mainstreaming of connected sensors is shifting care from episodic encounters to an always-on model, reinforcing patient engagement and lowering non-urgent clinic visits. Insurers have begun reimbursing smartwatch-driven atrial-fibrillation programs that demonstrate lower hospitalization rates, proving the economic value of wireless monitoring.

Rapid Technological Breakthroughs in Sensors & AI

The U.S. FDA had cleared 801 AI-enabled devices by mid-2024, tripling approvals recorded two years prior. Technologies such as Medtronic’s BrainSense Adaptive deep brain stimulation dynamically alter stimulation parameters by reading patient-specific neural signals, improving Parkinson’s symptom control while conserving battery life. Meanwhile, 5G-linked ECG patches deliver latency below 110 ms, fast enough to trigger automated emergency dispatches during myocardial events. Research centers are also piloting battery-free ultrasound implants for chronic pain that combine AI inference with edge energy harvesting, eliminating routine replacement surgeries. These advances collectively increase diagnostic accuracy, shorten intervention times and expand deployment to primary-care environments that once lacked specialty equipment.

Growing Chronic-Disease Burden

An estimated 783.2 million adults are expected to live with diabetes by 2045, elevating the need for continuous glucose monitoring and automated insulin delivery [2]Centers for Disease Control and Prevention, “National Diabetes Statistics Report,” cdc.gov. Cardiovascular disease accounted for 20.5 million deaths in 2021, underscoring rising demand for smart ECG and blood-pressure devices. The Centers for Medicare & Medicaid Services drafted new coverage rules in 2025 that recognize implantable CGM systems as medically necessary for insulin-treated patients, catalyzing broader uptake. Tandem Diabetes Care and Abbott are co-developing dual glucose-ketone sensors that detect metabolic shifts early enough to prevent diabetic ketoacidosis. Machine-learning algorithms integrated into consumer smartwatches have boosted blood-glucose prediction accuracy, opening the door to proactive dosage adjustment without finger-stick confirmation.

5G and Edge-AI for Real-time Remote Diagnostics

Fifth-generation networks paired with edge inference unlock high-bandwidth imaging, bidirectional video and sub-second alerting for stroke and trauma response. Pilot programs in Japan achieved 98% diagnostic concordance between on-site and remote radiologists when using 5G-enabled portable ultrasound. Rural clinics in China leverage low-power LPWAN gateways to forward multi-parameter vitals to provincial hospitals, reducing emergency transfers by 30% during 2024 influenza peaks. U.S. telco–provider collaborations are building network slices dedicated to medical traffic, thereby isolating clinical data streams from consumer congestion. When coupled with edge servers embedded in hospital basements, latency falls below the 200 ms threshold required for haptic telesurgery, a capability now moving from experimental to early commercial deployment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device acquisition & maintenance cost | -1.8% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Patient-data privacy & cybersecurity risk | -1.2% | Global, with regulatory focus in EU & North America | Medium term (2-4 years) |

| Reimbursement lag for AI-driven diagnostic algorithms | -1.5% | North America & EU primary, APAC secondary | Medium term (2-4 years) |

| Sensor-grade semiconductor supply chain bottlenecks | -1.3% | Global, with highest impact in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Device Acquisition and Maintenance Cost

Continuous glucose monitors and implantable cardiac devices still present high upfront prices that challenge budget-constrained hospitals. Semiconductor shortages have pushed component lead times to as long as 52 weeks, inflating bill-of-materials costs and slowing product refresh cycles [3]Frontiers in Health Services, “Semiconductor Bottlenecks in Medical Devices,” frontiersin.org. Because medical components represent only 11% of global industrial semiconductor demand, device makers possess limited negotiating leverage when foundries prioritize consumer electronics. Subscription models now bundle hardware, software and consumables into monthly fees that convert capital expense into operating expense, easing entry for mid-sized providers. Yet transitional Medicare coverage rules still link reimbursement to the completion of post-market evidence studies, delaying revenue capture for breakthrough devices.

Patient-Data Privacy and Cybersecurity Risk

The PATCH Act amendment requires device manufacturers shipping in the United States to provide a Software Bill of Materials and to establish a vulnerability disclosure program, with non-compliance resulting in automatic submission refusal. Healthcare networks experienced record ransomware incidents in 2024, and 74% of provider organizations report that more than half of their connected devices lack segmentation from enterprise IT systems. Bluetooth Low Energy devices mitigate risk by enforcing 128-bit AES encryption and frequent key rotation, yet many legacy deployments still operate on older stacks that lack over-the-air patch capability. The FDA logged over 250,000 wireless interference reports since 2021, including pacemaker malfunctions in magnetic-resonance suites, driving a surge in coexistence testing during pre-market submissions. Insurers are beginning to underwrite cyber liability riders that transfer residual risk, but associated premiums raise total cost of ownership for smaller practices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Diagnostics Drive Innovation Leadership

Diagnostic and monitoring devices accounted for 63.02% of the smart medical devices market share in 2025, a lead built on the proven clinical utility of continuous glucose and cardiac rhythm monitors. AI-enhanced dermatology scanners such as DermaSensor report 96% sensitivity for common skin cancers, speeding specialist referrals and steering treatment earlier in the disease course. Implantable loop recorders that stream arrhythmia data directly to cardiologists now feature smart-alert hierarchies that lower false positives by learning patient-specific signal patterns. Blood-pressure cuffs and pulse oximeters maintain traction in both acute and home settings as telehealth reimbursement normalizes episodic vitals capture.

Therapeutic devices, while representing a smaller revenue base, incorporate adaptive dosing and closed-loop feedback that improve outcomes in insulin therapy, neuromodulation and rehabilitative orthopedics. Simplera CGM’s seamless integration with the MiniMed 780G insulin pump shows how firms combine diagnostic insight and automated therapy in one ecosystem. Spinal cord stimulators with onboard AI categorize pain signatures in real time, allowing clinicians to tailor signal frequencies without repeated clinic visits. Smart hearing aids analyze environmental acoustics and adjust gain instantaneously, a feature that elevates speech intelligibility for complex soundscapes and aligns with demographic ageing trends.

By End User: Hospitals Lead, Home Care Accelerates

Hospitals and clinics represented 45.74% of the smart medical devices market size in 2025, capitalizing on existing telemetry infrastructure and specialized care teams hhs.gov. Smart-hospital blueprints in China integrate IoT sensors, automated drug dispensing and AI triage algorithms within unified command centers that cut administrative task time by 30%. U.S. Accountable Care Organizations deploy remote monitoring kits upon discharge to reduce 30-day readmissions, an initiative shown to save USD 390 million across 2024 program participants.

Home-care settings post the fastest 13.72% CAGR as ageing populations and reimbursement parity for telehealth expand remote-first care pathways. Adjustable beds with embedded respiratory monitors feed data into cloud dashboards where nurses can adjust CPAP settings without a home visit. Direct-to-patient shipment of mobile ECG patches bypasses traditional durable medical-equipment distributors and accelerates therapy initiation. Ambulatory centers and emergency medical services also integrate portable ultrasound and blood-gas analyzers that synchronize to electronic records before the patient reaches the hospital bay, reducing door-to-intervention times.

By Connectivity: Bluetooth Dominance Through Security Excellence

Bluetooth held 35.18% revenue in 2025 on the strength of its low-energy profile and mandated AES encryption, features that align with healthcare’s strict battery-life and privacy demands. Firmware updates over the air have become routine, helping providers close vulnerability windows without withdrawing devices from service. Bluetooth-ready vitals monitors auto-pair with clinician tablets, cutting ward installation time and freeing biomedical staff for higher-value tasks.

Cellular and dedicated 5G modules record the sharpest growth as governments invest in nationwide coverage and network slicing. Real-time ambulance telemetry streams high-resolution ultrasound to hospitals, allowing surgical teams to prep bays before patient arrival. LPWAN formats such as NB-IoT and LoRa serve asset-tracking tags and in-home fall detectors where multi-year battery life is critical. Wi-Fi continues to support bandwidth-heavy modalities like intraoperative imaging and telepresence robotics but cedes some share to private 5G where hospitals seek deterministic latency.

By Distribution Channel: Digital Transformation Reshapes Access

Offline channels retained 58.12% of 2025 revenue through hospital pharmacies and specialty distributors that bundle user training and post-installation service. Group purchasing organizations negotiate multi-year contracts that stabilize supply forecasts and leverage fleet-management portals to monitor device utilization. Institutional buyers still dominate high-acuity equipment where clinical validation and technical support are essential for risk mitigation.

E-commerce expands fastest, lifting online penetration to 15.26% in 2025 as manufacturers open direct stores that feature subscription bundles and teleconsultation add-ons. Consumers select blood-pressure cuffs and fingertip oximeters after viewing comparative dashboards that rank accuracy and compatibility with mobile apps. Digital checkout shortens lead times, and integrated financing spreads payments over the device life cycle, a model attractive to home-care agencies. Regulatory agencies urge marketplaces to flag devices with FDA clearance, ensuring shoppers differentiate between wellness gadgets and regulated medical products.

Geography Analysis

North America held 43.02% of the smart medical devices market in 2025, supported by advanced reimbursement structures and an AI strategic plan that guides public-sector procurement and algorithmic fairness audits hhs.gov. Digital-health investment totaled USD 3 billion in Q1 2025, channeled into startup accelerators partnering directly with university medical centers. Canada’s Pan-Canadian AI Health Strategy promotes standards-based data exchange across provinces, while Mexico’s medical-device export corridors supply cost-effective assembly resources and maintain duty-free status under USMCA.

Asia-Pacific registers the steepest 15.12% CAGR between 2026 and 2031. China’s Trinity smart-hospital program ties state funding to quantified improvements in patient throughput by mandating integrated digital registries and 5G bedside terminals. India’s Ayushman Bharat Digital Mission issues unique health IDs, enabling longitudinal records that simplify device-generated data ingestion into national platforms. Japan’s Medical DX initiative standardizes electronic medical records across 4,000 hospitals and launches nationwide online qualification checks, aligning device interoperability protocols to international FHIR specifications. Singapore’s Synapxe links public institutions with community clinics, piloting fall-detection wearables for seniors that triggered 2,300 timely interventions during 2024 trials.

Europe remains a steady adopter thanks to the Medical Device Regulation’s post-market surveillance rules and GDPR’s strict consent frameworks that boost patient trust. National telehealth agencies integrate outcome dashboards that rank remote-monitoring programs and allocate incentives accordingly. Middle East & Africa and South America trail in installed base but show double-digit growth as infrastructure projects extend broadband coverage and private insurance options proliferate. Development banks are channeling concessional finance into regional OEM assembly plants, aiming to localize supply and cut foreign-exchange exposure.

Competitive Landscape

The smart medical devices industry shows moderate consolidation; top manufacturers pursue adjacent acquisitions while forging coopetition agreements that blur historic rivalries. Johnson & Johnson acquired Abiomed for USD 16.6 billion to secure percutaneous heart-pump technology and complement its electrophysiology line. Boston Scientific purchased Silk Road Medical for USD 1.26 billion, adding transcarotid stent systems that address rising stroke prevention demand. Abbott and Medtronic inked a global partnership that melds Abbott’s continuous glucose monitors with Medtronic insulin pumps, targeting the 11 million patients requiring intensive insulin therapy worldwide.

Interoperability openness emerges as a competitive wedge. Device makers expose APIs that allow third-party analytics to read raw sensor data, accelerating the build-out of specialty algorithm marketplaces. Start-ups such as Oura demonstrate that niche form factors can unlock new engagement models; its smart ring’s AI-based sleep-quality coach rolled out in March 2025 and reached 1.2 million subscriptions within nine months. Cybersecurity capabilities determine contract wins: vendors pre-install hardware root-of-trust modules and commit to 10-year patch windows that satisfy tightened procurement checklists. Patent mapping indicates white-space opportunities in battery-free implant power and real-time metabolite sensing, areas where incumbent portfolios remain thin and venture funding flows rapidly.

Global Smart Medical Devices Industry Leaders

Fitbit Inc.

Medtronic Plc

F. Hoffmann-La Roche Ltd

Omron Corporation

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Sonova launched Audéo Infinio and Audéo Sphere Infinio hearing aids that process ambient sound through real-time AI on a new low-power chip.

- May 2024: Masimo partnered with Medable to integrate MightySat Rx pulse oximeters into oncology trials spanning 3,000 patients across 25 countries.

- May 2024: WS Audiology opened an R&D hub in Hyderabad, India, to expand AI-driven signal-processing research

- October 2023: Demant’s Audika brand acquired Goed Hulpmiddelen’s audiology business to deepen its Belgian presence.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the smart medical devices market as all regulated diagnostic, monitoring, or therapeutic hardware that embeds sensors, processors, or wireless modules enabling real-time data capture and two-way connectivity while remaining portable, wearable, or implantable. Devices span smart glucose meters, wearable ECG patches, connected insulin pumps, and portable oxygen concentrators.

Scope exclusion: general-purpose consumer fitness trackers that lack an approved medical claim fall outside this assessment.

Segmentation Overview

- By Product Type

- Diagnostic & Monitoring Devices

- Blood Glucose Monitors

- Continuous Glucose Monitors

- Heart-Rate Monitors

- Pulse Oximeters

- Blood-Pressure Monitors

- Breath Analyzers

- Other Diagnostic & Monitoring

- Therapeutic Devices

- Portable O₂ Concentrators & Ventilators

- Insulin Pumps (Traditional, Patch, Smart)

- Hearing Aids (Smart & AI-enabled)

- Smart Orthopedic & Other Therapeutic

- Diagnostic & Monitoring Devices

- By End User

- Hospitals & Clinics

- Home-Care Settings

- Ambulatory & Emergency Services

- Others (Sports Medicine, Military, etc.)

- By Connectivity

- Bluetooth

- Wi-Fi

- Cellular/5G

- LPWAN (NB-IoT, LoRa)

- By Distribution Channel

- Offline (Hospital Pharmacies, Retail)

- Online (e-Commerce, DTC)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured interviews with procurement heads at tertiary hospitals, R&D leads at device OEMs, digital-health insurers, and regulatory consultants across North America, Europe, Asia-Pacific, and the Gulf. These conversations validated adoption rates, average selling prices, reimbursement shifts, and yielded qualitative context around cybersecurity hurdles and patient adherence.

Desk Research

We gathered foundational numbers from trusted, open sources such as the US FDA 510(k) database, Centers for Medicare & Medicaid Services reimbursement files, World Health Organization chronic-disease registries, Eurostat trade codes, and industry bodies like AdvaMed and Continua Alliance. Company filings, investor decks, and leading medical journals supplemented market signals, while D&B Hoovers and Dow Jones Factiva offered paid cross-checks on corporate financial streams. The sources cited illustrate our wider desktop sweep; many additional references supported data collection, verification, and clarification.

Market-Sizing & Forecasting

A top-down construct starts with global production and trade data, which are then aligned to treated-patient pools and reimbursable procedure volumes; selective bottom-up roll-ups of supplier revenues and channel checks adjust totals. Key inputs include: 1) continuous-glucose-monitor penetration among diagnosed diabetics, 2) uptake of RPM billing codes 99453-58, 3) average Bluetooth-enabled chipset ASP trends, 4) hospital IoT gateway density, and 5) smartphone adoption in the 55+ cohort. A multivariate regression model links these variables to annual device revenues, allowing scenario analysis under conservative, base, and accelerated connectivity curves. Gaps in bottom-up estimates are bridged with interpolation from nearest verified price-volume datapoints.

Data Validation & Update Cycle

Outputs pass three-tier variance and plausibility checks, followed by senior analyst review. We refresh each model annually and reopen it mid-cycle if regulatory or macro events move the market materially. Before release, an analyst reconfirms all headline numbers.

Why Mordor's Smart Medical Devices Baseline Earns Decision-Maker Trust

Published figures often diverge because firms frame scope differently, apply unlike ASP assumptions, or refresh at varied cadences.

Key gap drivers we observe include inclusion of wellness wearables, omission of implantable devices, and straight-line CAGR projections that ignore reimbursement inflection points. Mordor's disciplined scope, variable set, and annual refresh cadence limit such distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 90.54 B (2025) | Mordor Intelligence | - |

| USD 101.43 B (2025) | Global Consultancy A | counts consumer fitness wearables and applies fixed 12% CAGR without primary validation |

| USD 87.70 B (2025) | Industry Journal B | derives figures from export shipment volumes only, with minimal end-user interviews |

Taken together, the comparison shows that Mordor's numbers sit between optimistic consumer-inclusive views and narrow shipment-only estimates, giving clients a balanced, transparent baseline grounded in verifiable medical-grade demand.

Key Questions Answered in the Report

What is the current Global Smart Medical Devices Market size?

The smart medical devices market size stands at USD 101.96 billion in 2026.

Who are the key players in Global Smart Medical Devices Market?

Fitbit Inc., Medtronic Plc, F. Hoffmann-La Roche Ltd, Omron Corporation and Abbott Laboratories are the major companies operating in the Global Smart Medical Devices Market.

Which is the fastest growing region in Global Smart Medical Devices Market?

Government-backed digital-health programs and large ageing populations are driving a 15.12% CAGR in Asia-Pacific.

What role does 5G play in smart medical devices?

5G connectivity lowers data-transfer latency below clinical thresholds, enabling real-time remote diagnostics and emergency response.

Page last updated on: