Medical Mobility Aids Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 19.23 Billion |

| Market Size (2031) | USD 25.06 Billion |

| Growth Rate (2026 - 2031) | 5.43% CAGR |

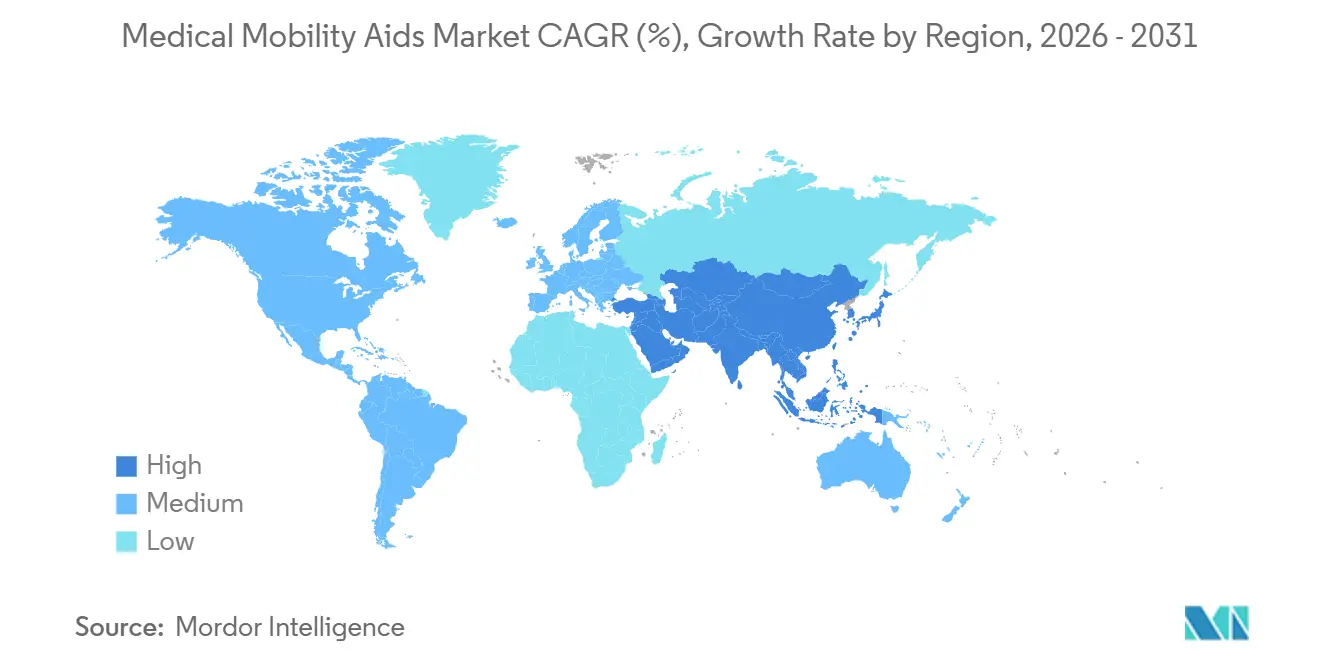

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

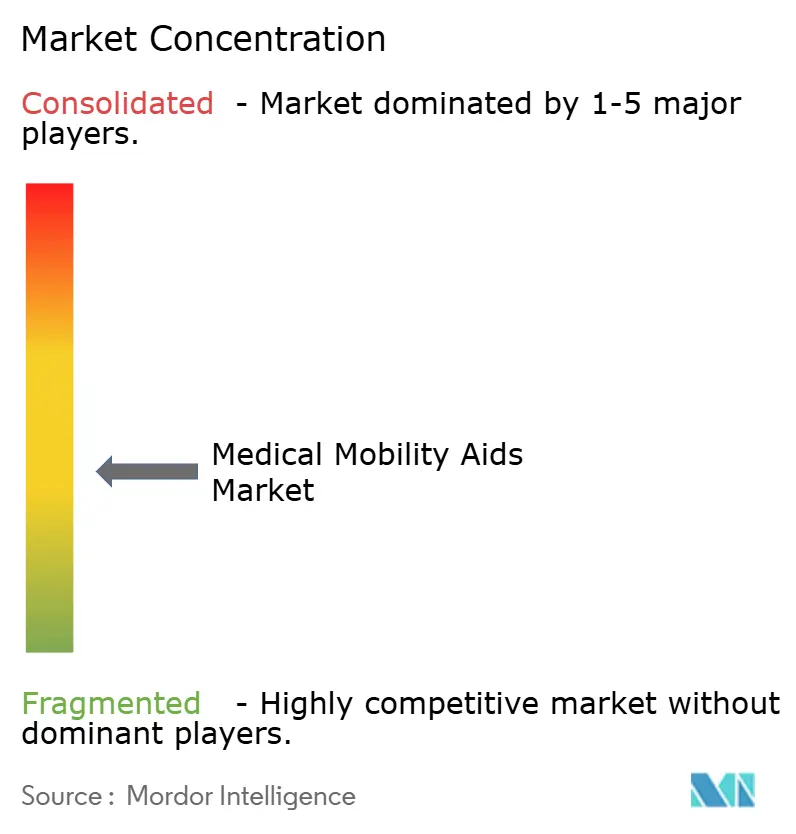

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Mobility Aids Market Analysis by Mordor Intelligence

The Medical Mobility Aids Market size is projected to be USD 18.33 billion in 2025, USD 19.23 billion in 2026, and reach USD 25.06 billion by 2031, growing at a CAGR of 5.43% from 2026 to 2031.

The medical mobility aids market is expanding because two long-running shifts are moving together, which are population aging and a broader move from institution-based care toward home and community use, and both are widening the base of users who need ongoing mobility support. The share of people aged 60 and older continues to rise globally, and that is lifting baseline demand for wheelchairs, walkers, scooters, transfer aids, and related products across both clinical and consumer settings. Competitive activity is increasingly centered on service access, reimbursement alignment, and tighter control of dealer or provider channels, because producers need stronger control over fitting, documentation, and follow-up support to protect margins and maintain utilization. A clear split is also taking shape between premium smart devices and lower-priced manual aids, and that leaves mid-tier powered products under pressure because they face stronger price competition below and more feature-rich alternatives above. The medical mobility aids market, therefore, continues to create room for companies that can support long user lifecycles, combine clinical functionality with residential usability, and build a stronger presence in the service and replacement side of demand.

Key Report Takeaways

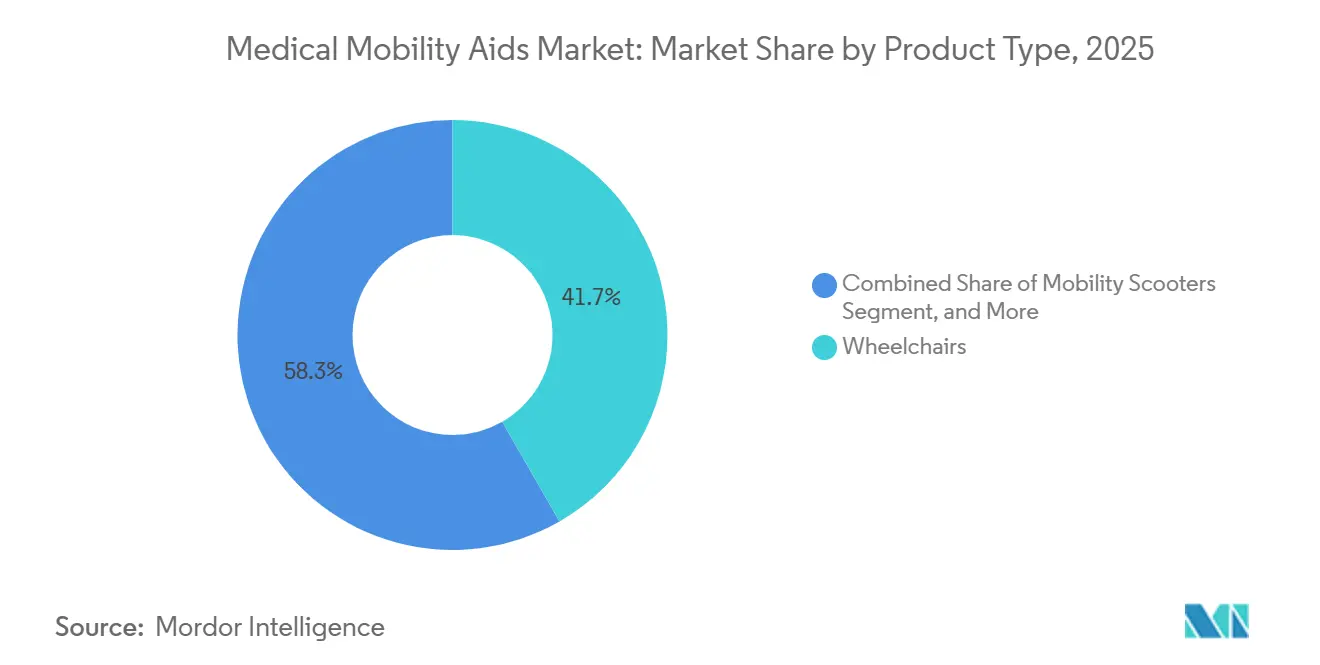

- By product type, wheelchairs led with 41.73% revenue share in 2025 in the medical mobility aids market, while mobility scooters are forecast to expand at a 6.76% CAGR through 2031.

- By technology, manual devices held 50.32% share in 2025, while powered devices recorded the highest projected CAGR at 7.88% through 2031.

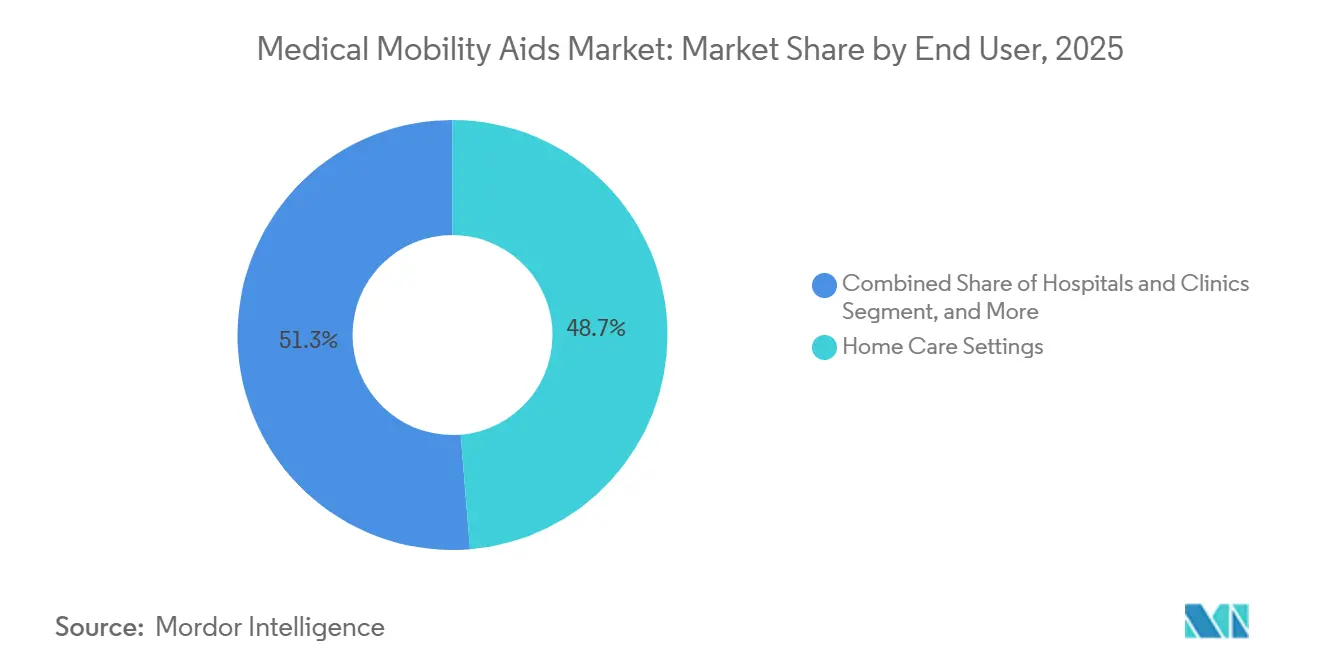

- By end user, home care accounted for 48.72% of demand in 2025 in the medical mobility aids market, while rehabilitation and long-term care centers are advancing at a 7.28% CAGR through 2031.

- By distribution channel, offline retail represented 70.33% of market size in 2025, while online retail is projected to grow at an 8.56% CAGR through 2031.

- By geography, North America held 38.41% of the market in 2025, while Asia-Pacific is forecast to expand at a 6.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Mobility Aids Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population and Longer Mobility Support Horizons | +1.5% | Global, concentrated in North America, Europe, Japan, and South Korea | Long term (≥ 4 years) |

| Rising Chronic Disease and Post-Acute Rehabilitation Demand | +1.2% | Global, with stronger gains in North America and the European Union | Medium term (2-4 years) |

| Shift Toward Home-Based Care and Aging in Place | +1.0% | North America and the European Union, with spillover into Asia-Pacific | Medium term (2-4 years) |

| Smart, Powered, and Connected Device Adoption | +0.8% | North America, Europe, and Asia-Pacific technology corridors | Short term (≤ 2 years) |

| Disability Inclusion, Access Funding, and Public Procurement Support | +0.5% | Global, with stronger national effects in North America, Germany, India, and Australia | Medium term (2-4 years) |

| Micro-Fit and Customization Requirements for Diverse User Physiques | +0.4% | Global, with earlier gains in North America, Germany, and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Population and Longer Mobility Support Horizons

The medical mobility aids market is closely tied to the steady increase in the elderly population, because mobility decline often extends over many years and usually requires repeated product use, replacement, adjustment, and servicing rather than a one-time purchase. By 2030, 1 in 6 people worldwide will be aged 60 or older, and the number of people aged 80 and above is expected to keep rising sharply through 2050, which supports a broader and more durable demand base for mobility support products.[1] World Health Organization, “Ageing and Health,” WHO Fact Sheet, who.int Longer life expectancy also changes the economics of demand, because users remain active for longer periods and premium devices face more cumulative wear, which can shorten practical replacement cycles and lift aftermarket revenue potential. Japan’s long-term care approach continues to stand out because it links municipal coverage to elderly mobility support, and that makes it a visible model for other aging economies that are trying to manage rising care needs over longer support periods. Manufacturers that design modular products with upgradeable parts, adaptable seating, and serviceable frames are better placed in the medical mobility aids market because they can capture more value across a long user relationship instead of relying only on first-unit sales.

Rising Chronic Disease and Post-Acute Rehabilitation Demand

The medical mobility aids market is also supported by a larger population living with functional limitations, rehabilitation needs, and recovery pathways that continue after discharge from hospitals and acute care settings. A 2025 meta-analysis in BMC Geriatrics reported a pooled prevalence of 26.07% for disability in basic daily living activities among older adults globally, while disability in instrumental daily living activities reached 45.15%, which points to a sustained need for supportive mobility solutions across aging populations.[2]Y. Hou et al., “Functional Disability in Basic and Instrumental Activities of Daily Living Among Older Adults Globally: A Systematic Review and Meta-Analysis,” BMC Geriatrics, link.springer.com OECD reporting also showed that self-rated poor or very poor health remained much higher among older adults in lower-income groups across 24 OECD countries, and that reinforces the uneven but persistent need for mobility support and rehabilitation access. Shorter hospital stays are pushing more mobility-related needs into post-acute settings, which means device prescription events are increasingly occurring in rehabilitation centers, long-term care environments, and home discharge pathways rather than staying inside institutional care for longer periods. That shift strengthens rehabilitation demand inside the Medical Mobility Aids Market because providers that can supply clinically suitable devices, documentation support, and faster fulfillment are positioned closer to the point where recovery-driven procurement now takes place.

Shift Toward Home-Based Care and Ageing in Place

The medical mobility aids market is being reshaped by the move toward home-based care, because users increasingly want to remain in familiar environments and families, payers, and care systems are adjusting around that preference. Statistics Canada reported in 2025 that 51.9% of Canadians aged 80 and older had made home adaptations, which shows that residences are being configured more actively around mobility and daily support needs.[3]Statistics Canada, “Aging in the Community: Factors Associated with Home Adaptations and Receipt of Informal Care Among Older Canadians,” Health Reports, statcan.gc.ca As this shift deepens, devices are no longer judged only by clinical suitability, because noise levels, size, turning radius, portability, app support, and ease of caregiver use matter more in residential settings than they did in institution-centered procurement. That is changing product priorities across the medical mobility aids market, since compact designs, quieter operation, and simple monitoring features make home adoption easier for users who may not have considered device use outside formal care settings in the past. The home setting also supports more continuous use and closer caregiver visibility, which gives producers a stronger reason to build products that can fit daily routines, remote follow-up, and long service periods instead of only episodic clinical use.

Smart, Powered, and Connected Device Adoption

The medical mobility aids market is moving toward smarter and more powered products as battery performance, miniaturization, and control systems improve and as users expect better independence, safety, and navigation support from everyday mobility devices. WHILL expanded its autonomous mobility service to Heathrow Airport Terminal 3 in June 2026, and the company stated that it had already delivered close to 1 million autonomous rides globally, which shows that advanced mobility functions are moving beyond pilot visibility into repeated institutional use. A 2025 study in the Journal of NeuroEngineering and Rehabilitation also validated a multifunctional integrated nursing wheelchair that combined powered positioning, standing support, and omnidirectional movement, which supports the case for more integrated device design in rehabilitation settings. Permobil’s SmartDrive MX2+ also shows how power-assist solutions can enter the Medical Mobility Aids Market without fully separating from manual use frameworks, because it reduces manual push effort while staying close to familiar usage and reimbursement pathways. These advances matter because they widen the potential user base, improve usability for people with lower strength or dexterity, and shift competition toward features, data capability, and long-term service support rather than only mechanical durability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Out-of-Pocket Cost for Premium and Powered Devices | -1.8% | Asia-Pacific, South America, and Middle East & Africa, with wider pressure in lower-income groups globally | Medium term (2-4 years) |

| Limited Reimbursement and Fragmented Coverage Rules | -1.5% | Global, with the strongest effect in Asia-Pacific, South America, and Middle East & Africa | Long term (≥ 4 years) |

| Repair, Maintenance, and Battery Service Burden for Powered Devices | -0.8% | Global, concentrated in rural and underserved regions | Medium term (2-4 years) |

| Retail Channel Trust Gaps for High-Value Assistive Devices | -0.5% | Global, strongest in markets without established durable medical equipment networks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Cost for Premium and Powered Devices

The medical mobility aids market still faces a serious affordability barrier, because advanced powered wheelchairs, smart devices, and complex rehabilitation technologies remain expensive relative to household income in many countries and are often only partly covered even where reimbursement exists. The gap between basic coverage and premium feature pricing is especially important because many users can access a functional base model while advanced controls, smart features, or higher-performance components remain self-funded at the point of sale. Germany offers a more favorable access structure at the approved device level, since statutory insurer members face only a limited co-payment for listed aids, but even there, the distinction between covered necessity and optional premium configuration remains important for end users. In lower-income parts of Asia-Pacific and South America, the burden falls much more directly on households, which pushes procurement toward lower-cost manual devices even when powered options could better match functional need. This keeps volume flowing, but it also limits product mix improvement across the medical mobility aids market and creates an advantage for suppliers that offer tiered portfolios, simpler financing options, or lower-cost products built around core functionality.

Limited Reimbursement and Fragmented Coverage Rules

The medical mobility aids market also grows more slowly where reimbursement rules differ across countries, payer types, product classes, and local approval systems, because that raises compliance costs and makes product access less predictable for both providers and users. Fragmentation affects more than patient affordability, because it also shapes which product features are worth developing, which channels are viable, and how much billing infrastructure a company must maintain before it can scale across multiple regions. In Germany, mobility aids flow through a structured statutory listing system tied to certified suppliers, and that supports regulated access while also limiting channel flexibility for products that fall inside the reimbursement framework. In other regions, especially faster-growing emerging markets, the absence of standardized procurement or coverage systems limits the addressable premium segment even when aging and disability needs are rising quickly. This favors larger companies in the medical mobility aids market because they can spread documentation costs across wider portfolios, while smaller manufacturers face more working capital pressure and slower route-to-market execution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wheelchairs Anchor Share, Scooters Define the Growth Curve

Wheelchairs held 41.73% of the medical mobility aids market share in 2025, and that position reflected their broad fit across hospitals, rehabilitation settings, long-term care use, and daily home mobility needs. Their lead also came from established reimbursement pathways and familiar prescription routines, which lower friction for clinicians, payers, and suppliers compared with newer or more lifestyle-oriented device categories. Mobility scooters are projected to grow at 6.76% through 2031, and that growth comes from their ability to sit between medical necessity and consumer convenience, especially for older users who want more community mobility without moving fully into complex clinical devices. The medical mobility aids industry, therefore, shows a clear split inside product type, because wheelchairs remain the default solution for broad clinical use while scooters capture faster growth through aging-in-place behavior and easier access in standard configurations.

Walkers and rollators continue to hold stable demand because they fit early-stage mobility decline, post-surgical recovery, cardiac rehabilitation, and general support needs that are common across outpatient and residential care pathways. Patient lifts and transfer aids are also gaining importance in long-term care and facility settings, where labor shortages, caregiver strain, and safety concerns make assisted transfer solutions more necessary in daily operations. Prosthetics and orthotics mobility solutions remain a more specialized and premium part of the mix, and their growth pattern is shaped by shorter innovation cycles, higher clinical complexity, and more differentiated margin profiles than standard mechanical aids. Crutches, canes, and other ambulatory aids still serve large user groups, but their pricing and volume profile are under pressure, which means value retention depends more on ergonomic upgrades, lighter materials, and better usability than on major shifts in core function.

By Technology: Manual Devices Lead Volume, Powered Segment Reshapes Margin Structure

Manual devices accounted for 50.32% of the market in 2025, and that scale reflected lower acquisition cost, wider reimbursement familiarity, simpler maintenance, and a large user base whose mobility needs do not always require powered assistance. Powered devices are forecast to expand at 7.88% through 2031, which makes them the fastest-growing technology segment as battery costs ease, motors become smaller, and rehabilitation settings gain more confidence in powered outcomes and daily usability. This creates a different margin structure inside the medical mobility aids market because volume still sits with manual products, while faster value growth is moving toward powered and enhanced mobility platforms. The medical mobility aids industry is therefore not shifting in a single step from manual to powered use, because the transition is being shaped by reimbursement, user capability, home suitability, and maintenance requirements at the same time.

Hybrid and power-assist products form an important middle layer in this transition, because they give users some powered benefit while staying closer to the form, weight expectations, and reimbursement familiarity of manual devices. Permobil’s SmartDrive MX2+ is an example of that bridge, since it reduces push effort by up to 80% and shows how assisted mobility can expand without requiring a full jump into traditional powered device categories. Connected and smart aids remain smaller in current share, but they carry strategic weight because they can support remote monitoring, predictive servicing, caregiver coordination, and data-based differentiation over time. The biggest limiting factor is not only hardware readiness, but also the weak integration between mobility devices and health records or provider systems, which means the commercial value of data features will depend on stronger interoperability and evidence generation across the forecast period.

By End User: Home Care Dominates Volume, Rehabilitation Centers Drive Fastest Expansion

Home care settings represented 48.72% of end-user demand in 2025, and that lead reflects a broad preference for aging in place, longer community living, and a care model that increasingly shifts support from institutions to households. Rehabilitation and long-term care centers are projected to grow at 7.28% through 2031, and that pace is supported by faster post-acute discharge flows, more recovery-focused procurement, and stronger use of specialized mobility equipment in structured treatment settings. Statistics Canada’s 2025 findings on home adaptations among people aged 80 and older support the direction of this shift, because they show that residential settings are being modified more actively to support mobility and daily function. The medical mobility aids market size in home care remains strong because each new wave of residential product design, including compact builds, quieter motors, and easier monitoring, reduces the practical barrier for another group of users to adopt devices outside traditional institutions.

Hospitals and clinics still matter as procurement channels, especially for high-acuity equipment, transfer aids, and complex powered devices that require assessment, documentation, and supervised fitting before they move into patient use. Rehabilitation centers and long-term care facilities also need to be viewed separately, because rehabilitation sites often prioritize higher-intensity, faster-turn equipment while long-term care settings look for durable and lower-maintenance solutions that can stay in daily service for longer periods. Public procurement and access support programs across parts of Asia are likely to matter more for institutional demand than for direct household adoption, because structured facility purchasing can move faster than reimbursement reform in consumer channels. For that reason, the medical mobility aids market is seeing a two-track end-user model in which home care leads volume while rehabilitation and long-term care settings shape some of the fastest equipment upgrades and replacement cycles.

By Distribution Channel: Offline Holds the Prescription Core, Online Channels Close the Gap

Offline retail held 70.33% of distribution volume in 2025, and that position remains tied to the documentation-heavy path for prescription devices, where fitting, supplier certification, reimbursement paperwork, and after-sales service are difficult to replicate in a purely digital transaction. Online retail is forecast to grow at 8.56% through 2031, which makes it the fastest channel as more standard products move into direct purchase pathways and users become more comfortable researching and ordering lower-complexity aids digitally. This means the medical mobility aids market size still sits mainly in offline structures today, but future channel growth is increasingly being created by digital discovery, direct ordering, and blended fulfillment models. The dividing line across the medical mobility aids market is product complexity, because standard scooters, walkers, and simpler aids can move online much more easily than complex rehabilitation technology.

Medical equipment suppliers and institutional procurement channels continue to serve demand that is less exposed to consumer shopping behavior, since their role includes fitting support, documentation handling, and coordinated delivery into hospitals, rehabilitation centers, and long-term care settings. Germany shows how reimbursement structure can slow online adoption for covered products, because eligible aids continue to flow through certified brick-and-mortar medical supply channels under the statutory framework. At the same time, digital research and digital configuration are becoming more important before a final in-person fitting, which supports an omnichannel model instead of a simple shift from offline to online. That is why the distribution strategy in the medical mobility aids market is moving toward mixed channel control, where manufacturers want the reach of digital engagement but still rely on provider networks for assessment, claims support, and service continuity.

Geography Analysis

North America accounted for 38.41% of the medical mobility aids market size in 2025, and that led to a mature reimbursement environment, strong durable medical equipment infrastructure, and a large installed base of certified suppliers able to support prescription and documentation workflows. The regional position is also supported by high awareness of assistive products, stronger uptake of premium devices, and a wider pathway for home use and facility procurement than in many developing markets. Canada adds to regional demand through provincial assistive-device support and private insurance participation, though coverage differences by province still affect access and product mix. Mobility scooters appear well placed in this region because consumers can increasingly compare options, purchase standard models more directly, and use them in community and residential settings without moving through the full complexity of high-acuity clinical procurement.

Europe remained the second-largest regional market, and its structure is defined by different national reimbursement systems that create both barriers to entry and clear opportunities for companies with stronger regulatory and channel capabilities. Germany is central to this pattern because its statutory framework routes approved mobility aids through certified supply channels and listed products, which supports access for eligible users while keeping reimbursement-led purchasing closely tied to accredited providers. That structure sustains higher-value sales for covered products, but it also limits how far direct online models can extend into reimbursed categories. Regional competition is also being reshaped by channel consolidation, because manufacturers and larger groups are buying or integrating local distribution assets to gain better control over fitting, servicing, and documentation. The European picture is therefore attractive but demanding in the medical mobility aids market, since commercial success depends on reimbursement navigation, dealer relationships, and compliance discipline as much as on product quality alone.

Asia-Pacific is forecast to grow at 6.51% through 2031, making it the fastest regional market as aging accelerates in Japan, South Korea, China, and other parts of the region while procurement pathways broaden gradually across public and institutional settings. Japan benefits from long-term care coverage for standard mobility aids, and that supports baseline demand even though higher-end smart devices often sit outside routine reimbursement and create a separate premium out-of-pocket layer. South Korea also supports basic mobility devices through national insurance channels, while China’s accessible infrastructure agenda continues to reinforce long-term use conditions for mobility support products. India and Southeast Asia are increasingly relevant because public procurement expansion can bring mobility aids into more structured purchase environments, even when household reimbursement remains limited.

Competitive Landscape

The medical mobility aids market remains moderately fragmented because the leading companies hold strong positions in selected categories and regions, but no single business controls the full product range, the major geographies, and the most important distribution channels at the same time. Permobil AB, Ottobock SE & Co. KGaA, and Sunrise Medical LLC remain central to the premium rehabilitation and mobility space because they combine product depth, clinical relationships, and reimbursement familiarity that smaller companies find difficult to match at scale. Even so, the competitive center of gravity is shifting from pure product manufacturing toward channel control, service support, and long-term user management, since fitting, documentation, and replacement activity now matter more to profitability than simple unit shipment in many categories. The Medical Mobility Aids Market, therefore, rewards companies that can keep close links with providers, dealers, and post-sale service systems rather than competing only on device specification.

Strategic moves show this pattern clearly. Sunrise Medical moved to strengthen its portfolio and channel presence through acquisitions such as Ergoflix in January 2026 and Oracing in January 2025, which broadened its reach in foldable power mobility and premium sports wheelchair categories. Ottobock also stayed active through a EUR 110 million acquisition of Blatchford Norway in 2025 and a USD 5 million strategic investment in Blue Arbor Technologies in December 2025, which extended its patient care footprint while also placing a bet on next-generation prosthetic control. WHILL has built visibility in a different way, because its deployments in high-traffic airport environments show that advanced mobility support can gain institutional acceptance outside traditional reimbursement-centered procurement pathways. These moves suggest that competition in the Medical Mobility Aids Market is widening beyond standard product launches and increasingly includes technology adjacency, controlled distribution, and brand visibility in public-use settings.

A second layer of competition is taking shape around customization and design-led differentiation. Ottobock’s iconiq launch, described as the company’s first 3D-printed silicone prosthetic liner, shows how additive manufacturing is moving into more individualized mobility-related components and not staying limited to small experimental use. WHILL’s repeated airport deployments and Permobil’s push into lighter manual wheelchairs and modular seating support show that usability, portability, and user experience are becoming more important commercial tools alongside clinical performance. Smaller specialists can still hold space where they focus tightly on a niche user need, but the broader medical mobility aids market is moving toward a model where scale, evidence, service, and channel discipline matter more each year.

Medical Mobility Aids Industry Leaders

Arjo AB

Medline Industries, LP

Ottobock SE and Co. KGaA

Stryker Corporation

WHILL, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: WHILL, Inc. launched an autonomous mobility service trial at Heathrow Airport Terminal 3 in partnership with ABM, the largest UK assisted travel provider, expanding its global autonomous mobility network to a major European aviation hub. The deployment, having begun just over a month prior, marks a commercial milestone for AI-powered mobility aids in high-traffic institutional environments.

- May 2026: Ottobock SE & Co. KGaA presented prosthetics and orthotics innovations at OTWorld 2026 in Leipzig, including a new prosthetics solution launching initially across DACH and Benelux markets, with additional markets to follow. The event reinforced Ottobock's strategy of leading with premium technology introductions at the world's largest orthopedic technology trade fair.

- March 2026: Permobil launched the new TiLite TR and TiLite ZR titanium manual wheelchairs globally, featuring lighter components, redesigned machined caster bullets, streamlined CoG systems, and enhanced adjustability. Available across the Americas, Europe, and the Asia-Pacific regions through Permobil's authorized provider network, the launch targets active manual wheelchair users requiring precision customization.

- March 2026: WHILL, Inc. launched the Model C Lite, a lightweight foldable electric wheelchair with advanced Japanese engineering for compact indoor and outdoor performance, now available for purchase in the UK, Germany, France, the Netherlands, and Spain, with in-market test drives at authorized retailers.

Global Medical Mobility Aids Market Report Scope

The Medical Mobility Aids Market is defined as the global industry that develops, manufactures, and distributes devices designed to assist individuals with physical impairments, disabilities, or age-related mobility challenges, enabling them to move independently and safely.

The Medical Mobility Aids Market is segmented across multiple dimensions. By Product Type, it includes Wheelchairs, Walkers and Rollators, Mobility Scooters, Crutches and Canes, Patient Lifts and Transfer Aids, Prosthetics and Orthotics Mobility Solutions, and Other Medical Mobility Aids. By Technology, the market is divided into Manual, Powered, Hybrid and Power-Assist, and Connected and Smart Mobility Aids. By End User, the market serves Home Care Settings, Hospitals and Clinics, Rehabilitation and Long-Term Care Centers, and Other End Users. By distribution channel, it is segmented into Offline Retail, Online Retail, Medical Equipment Suppliers, and Institutional Procurement. Geographically, the market is divided into North America (United States, Canada, Mexico); Europe (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe); Asia-Pacific (China, Japan, India, Australia, South Korea, and Rest of Asia-Pacific); Middle East & Africa (GCC, South Africa, and Rest of Middle East & Africa); and South America (Brazil, Argentina, and Rest of South America).

| Wheelchairs |

| Walkers and Rollators |

| Mobility Scooters |

| Crutches and Canes |

| Patient Lifts and Transfer Aids |

| Prosthetics and Orthotics Mobility Solutions |

| Other Medical Mobility Aids |

| Manual |

| Powered |

| Hybrid and Power-Assist |

| Connected and Smart Mobility Aids |

| Home Care Settings |

| Hospitals and Clinics |

| Rehabilitation and Long-Term Care Centers |

| Other End Users |

| Offline Retail |

| Online Retail |

| Medical Equipment Suppliers |

| Institutional Procurement |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Wheelchairs | |

| Walkers and Rollators | ||

| Mobility Scooters | ||

| Crutches and Canes | ||

| Patient Lifts and Transfer Aids | ||

| Prosthetics and Orthotics Mobility Solutions | ||

| Other Medical Mobility Aids | ||

| By Technology | Manual | |

| Powered | ||

| Hybrid and Power-Assist | ||

| Connected and Smart Mobility Aids | ||

| By End User | Home Care Settings | |

| Hospitals and Clinics | ||

| Rehabilitation and Long-Term Care Centers | ||

| Other End Users | ||

| By Distribution Channel | Offline Retail | |

| Online Retail | ||

| Medical Equipment Suppliers | ||

| Institutional Procurement | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of medical mobility aids by 2031?

The medical mobility aids market is projected to reach USD 25.06 billion by 2031, rising from USD 19.23 billion in 2026 at a 5.43% CAGR over 2026 to 2031.

Which product category leads current revenue?

Wheelchairs led product revenue with 41.73% share in 2025 because they remain widely used across hospitals, rehabilitation, long-term care, and home settings.

Which product type is growing the fastest through 2031?

Mobility scooters are projected to grow the fastest among product types at a 6.76% CAGR, supported by aging-in-place demand and wider use outside formal clinical settings.

Why is home care so important in this sector?

Home care held 48.72% of end-user demand in 2025, and the shift toward aging in place is increasing demand for compact, quieter, and easier-to-use residential mobility solutions.

Which region leads current demand and which region is expanding the fastest?

North America held the largest regional share at 38.41% in 2025, while Asia-Pacific is expected to post the fastest regional growth at a 6.51% CAGR through 2031.

What is changing competition among leading companies?

Competition is shifting toward channel control, customization, service support, and smart features, with companies such as Permobil, Ottobock, Sunrise Medical, and WHILL making product, technology, and distribution moves to strengthen position.

Page last updated on: