Mobile Clinics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

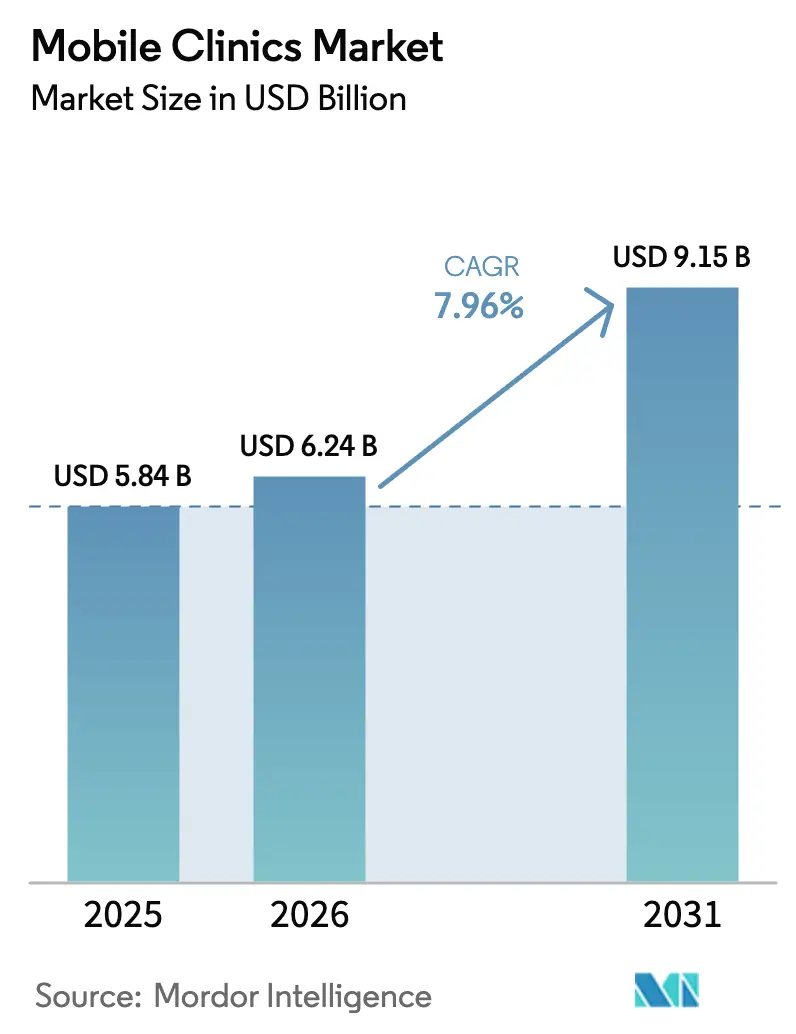

| Market Size (2026) | USD 6.24 Billion |

| Market Size (2031) | USD 9.15 Billion |

| Growth Rate (2026 - 2031) | 7.96% CAGR |

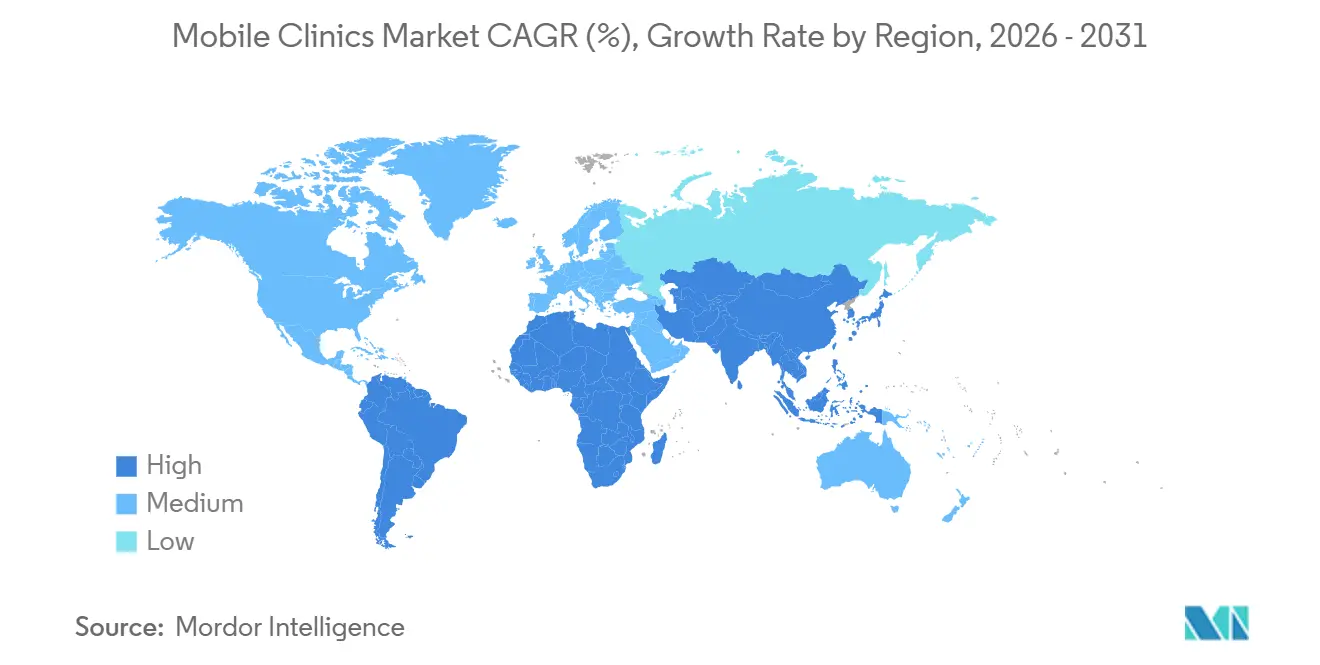

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

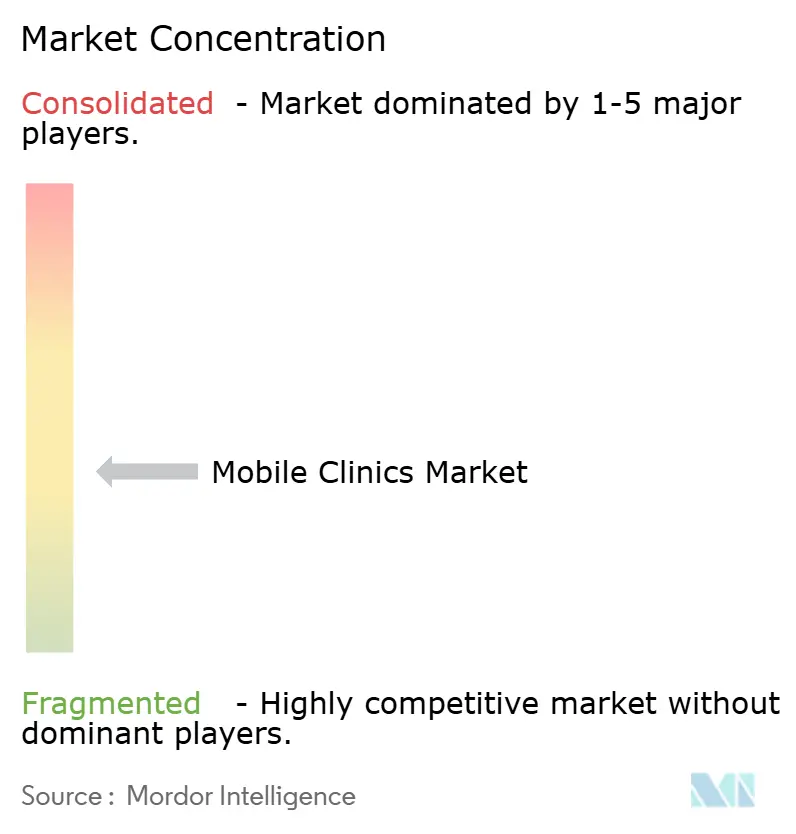

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Clinics Market Analysis by Mordor Intelligence

The Mobile Clinics Market size is expected to grow from USD 5.84 billion in 2025 to USD 6.24 billion in 2026 and is forecast to reach USD 9.15 billion by 2031 at 7.96% CAGR over 2026-2031.

The shift toward distributed care, backed by federal and state incentives, is reshaping capital allocation as health systems look for faster payback alternatives to brick-and-mortar builds. Medicaid parity laws, multi-year rural-health grants, and clearer licensing rules are pushing mobile units into mainstream strategy. Operators are broadening service menus, adding AI diagnostics and telehealth links to raise reimbursement levels while holding down fixed costs. At the same time, cash-flow pressure, workforce shortages, and unit throughput limits temper expansion plans, forcing providers to weigh fleet mix, route density, and staffing models with greater precision.

Key Report Takeaways

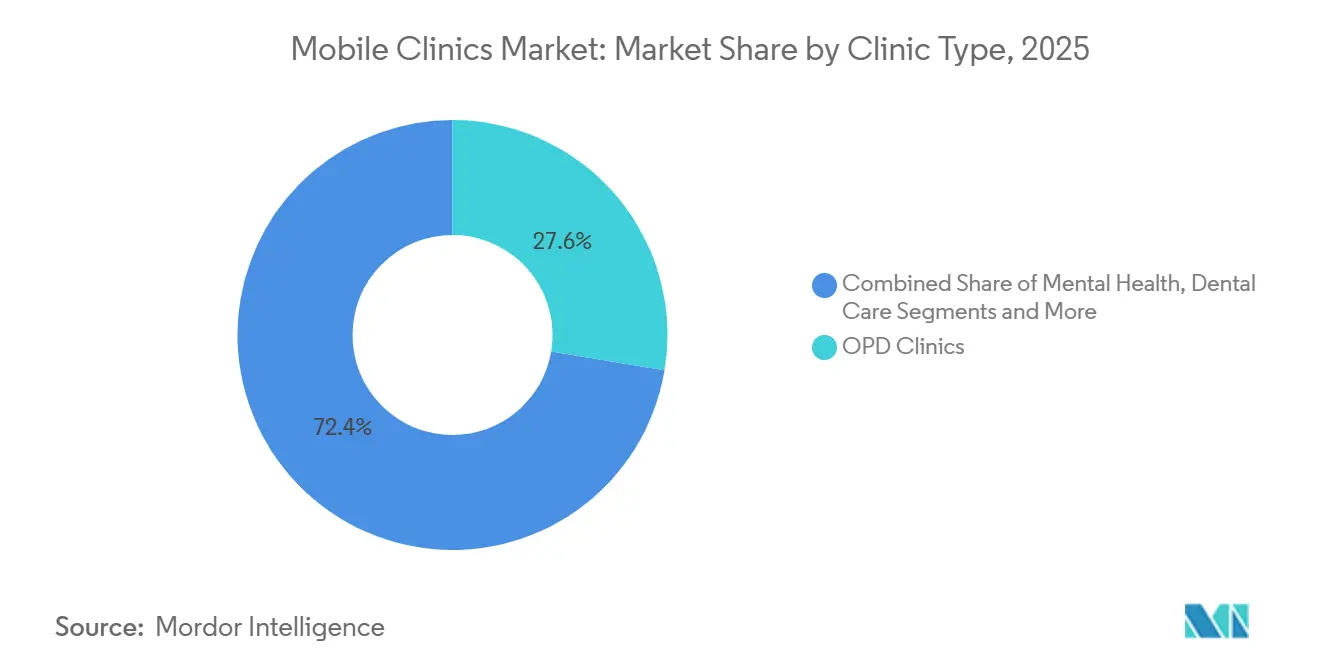

- By clinic type, OPD clinics led with 27.63% revenue share in 2025; maternal health units are projected to grow at a 10.34% CAGR through 2031.

- By vehicle type, mobile medical vans accounted for 49.75% share in 2025; trailers are set to record the fastest 11.33% CAGR to 2031.

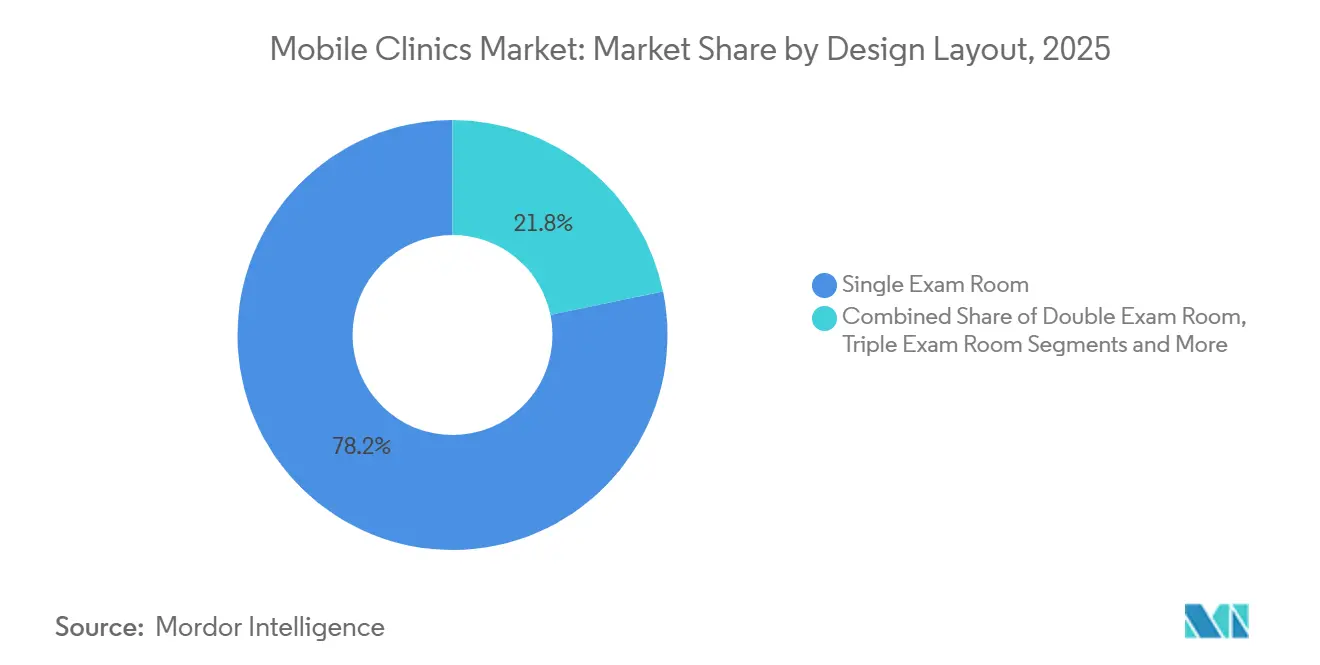

- By design layout, single-exam-room configurations held 78.24% share in 2025; expandable modular pods are poised for a 12.53% CAGR across the forecast.

- By service model, primary and preventive care dominated with 31.63% share in 2025; telehealth-enabled follow-up is forecast to advance at a 12.84% CAGR through 2031.

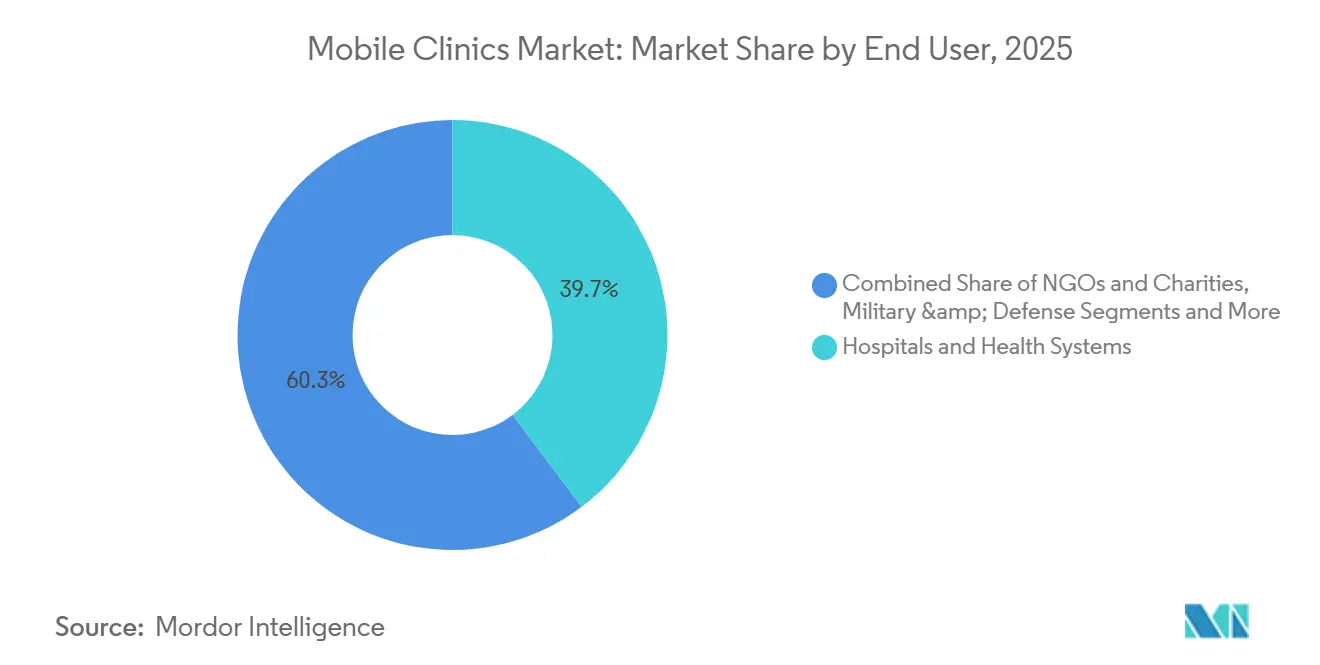

- By end user, hospitals and health systems captured 39.74% share in 2025; military and defense deployments are expected to expand at a 10.44% CAGR to 2031.

- By technology integration, telehealth-enabled units led with 36.37% share in 2025; AI-supported diagnostics configurations are projected to witness an 11.65% CAGR over the period.

- By geography, North America held 35.84% of revenue in 2025; Asia-Pacific is anticipated to grow at a 9.32% CAGR, the fastest among regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mobile Clinics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of chronic diseases & emergencies | +1.8% | North America, Europe | Medium term (2-4 years) |

| Cost-effective remote patient monitoring | +1.5% | United States, India, China | Short term (≤ 2 years) |

| Growth in geriatric population | +1.3% | Japan, Germany, Italy | Long term (≥ 4 years) |

| Government funding for rural outreach | +1.6% | North America, Sub-Saharan Africa, India | Short term (≤ 2 years) |

| AI-enabled portable diagnostics | +1.2% | North America, Europe, urban APAC | Medium term (2-4 years) |

| Shift to zero-emission or solar powertrains | +0.9% | Europe, select U.S. states, East Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic Diseases & Emergencies

Higher rates of diabetes, hypertension, and trauma keep mobile units busy because they shorten the distance between patients and first-line care. A study conducted in the United States in 2025 found that transportation barriers were linked to greater emergency-department use in 2024, highlighting the value of near-home checkups.[1]Fangyuan Chen, “Transportation Barriers, Emergency Department Use, and Mortality Risk Among US Adults: A National Health Interview Survey Analysis,” BMC Public Health, ncbi.nlm.nih.govCommunity paramedicine teams that ride mobile platforms have already cut 30-day revisit rates, proving the model works for value-based contracts. A single USD 150 mobile visit can avert a USD 1,500 ED episode, an equation that resonates with payers. Unit builders are therefore adding medication reconciliation stations, connected diagnostic kiosks, and home-monitoring device kits so chronic-care workflows fit inside small footprints.

Cost-Effective Remote Patient Monitoring Models

Bluetooth blood-pressure cuffs, glucometers, and pulse oximeters handed out during a mobile visit feed continuous data streams to clinicians. Removing follow-up travel lowers the cost to serve by up to 30% compared with repeat walk-in appointments. The World Health Organization’s 2024 toolkit for AI devices in low-resource settings cleared regulatory doubt and accelerated device rollouts. As infectious-disease testing alone passed USD 12 billion in 2024, mobile units became a preferred distribution channel, earning margin on both the initial visit and data-management services.

Government Funding for Rural-Health Outreach

The Health Resources and Services Administration reserved USD 50 million for new mobile access points in its 2025 budget, making vans and trailers eligible for grants that once favored fixed clinics.[2]Health Resources and Services Administration, “Fiscal Year 2025 New Access Points Funding Opportunity for Health Centers,” Health Resources and Services Administration, hrsa.gov Construction of a rural health center costs USD 2-5 million and needs years to break even, while a mobile unit reaching 25 daily encounters can pay for itself within 18 months. Seventeen U.S. states now reimburse mobile encounters at parity, giving providers the confidence to expand fleets.

AI-Enabled Portable Diagnostics Integration

FDA-cleared AI algorithms now guide ultrasound probes and flag anomalies instantly, letting general practitioners handle scans that once required a radiologist. The National Institutes of Health is funding outcome research on these tools through 2027, signaling likely payment upgrades. A visit that includes an AI ultrasound reimburses at USD 200-300, roughly double a basic primary-care encounter, and thus lifts unit economics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited daily patient throughput | -0.8% | Global | Short term (≤ 2 years) |

| High capital and maintenance costs | -1.1% | Low-income markets, global nonprofits | Medium term (2-4 years) |

| Regulatory complexity across jurisdictions | -0.6% | United States, Europe, fragmented APAC | Long term (≥ 4 years) |

| Shortage of dual-licensed driver-clinicians | -0.9% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Daily Patient Throughput

A single exam room supports roughly 32 encounters in an eight-hour shift. Doubling staff without doubling rooms stalls revenue because space, not people, is the pinch point. Expandable pods help, yet setup adds 20 minutes and chips away at route density. Break-even generally needs 25 to 30 encounters per day, which ultra-rural zones struggle to supply.

High Capital and Maintenance Costs

A well-equipped van costs USD 250,000-400,000; imaging trucks can top USD 700,000. Yearly servicing, calibration, and IT updates add another 15-20% of purchase price. Interest costs remain high, and grant cycles can leave units idle when funding lags. Lower-cost vans thus dominated 49.75% of 2025 deployments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Clinic Type: OPD Dominance Masks Maternal Health Surge

OPD units captured 27.63% of the mobile clinics market share in 2025, due to high-volume vaccinations and chronic-care checkups that require light gear. Maternal health units, though smaller today, are set for a 10.34% CAGR through 2031, powered by prenatal funding priorities and higher per-encounter payments. The World Health Organization positions mobile prenatal care as a pillar of maternal-mortality reduction.[3]World Health Organization Staff, “Maternal Health: Overview,” World Health Organization, who.int These units bundle ultrasound, lab draws, and counseling, turning a single stop into a full visit. Workforce scarcity remains the brake, especially in remote regions where certified midwives are in short supply.

By Vehicle Type: Vans Lead, Trailers Accelerate

Vans owned 49.75% of 2025 revenue because they slip into city blocks and rural lanes at a modest price. Trailers are gaining at an 11.33% CAGR since they decouple clinic modules from tow vehicles, letting owners upgrade interiors without replacing the chassis. Amref’s high-throughput Kenyan fleet shows solar-backed trailers can deliver big-bus capacity for less money. Setup time, however, makes them less ideal for multi-stop days.

By Design Layout: Single Rooms Dominate, Modular Pods Surge

In 2025, single-room layouts accounted for 78.24% of installations due to their straightforward design and ease of staffing. At the same time, convertible pods are growing at a 12.53% CAGR. These pods can expand to accommodate telehealth consultations or rapid screening events and retract for convenient transport. However, certain local regulations classify these pods as temporary structures, requiring fire-code approvals, which extends lead times.

By Service Model: Primary Care Anchors, Telehealth Follow-Up Accelerates

Primary and preventive care held 31.63% of revenue in 2025 as payers reward vaccinations and screenings that stop costlier events downstream. Telehealth follow-up, tied to a 12.84% CAGR, uses the first visit to hand out remote-monitoring kits and schedule virtual reviews, stretching limited clinician-hours. Inconsistent telehealth payment rules remain the primary uncertainty.

By End User: Hospitals Lead, Military Surges

Hospitals and health systems controlled 39.74% of 2025 spend, leveraging balance-sheet heft to fund fleets that support community-benefit goals and lower readmissions. Military and defense users, advancing at 10.44% CAGR, deploy modular, air-liftable clinics that put Role 1 care within minutes of frontline troops. Corporate work-site programs are emerging but need large employee bases to break even.

By Technology Integration: Telehealth Leads, AI Diagnostics Surge

Telehealth-enabled units retained 36.37% share in 2025, reflecting wide acceptance of secure video consults. AI-driven diagnostics, projected at an 11.65% CAGR, promise radiologist-level insights in real time, lifting reimbursement per encounter and shrinking referral costs. Staff training and software updates present ongoing hurdles.

Geography Analysis

North America commanded 35.84% of 2025 revenue on the back of USD 10 billion in annual CMS rural-health disbursements and 17 parity states that pay mobile visits at fixed-clinic rates. Workforce gaps push operators to tele-supervision agreements, yet clinician licensing remains a patchwork.

Asia-Pacific posts the fastest expansion at 9.32% CAGR through 2031. India’s National Health Mission assigned INR 37,000 crore (USD 4.4 billion) for 2024-25, directing mobile fleets into tribal districts. China’s Healthy China 2030 plan funds elder-care vans in rural counties. Regulation, however, varies by country, so local joint ventures often beat direct imports.

Europe, the Middle East and Africa, and South America trail in value but deliver niche upside. The EU’s stricter medical-device rule raises the bar and filters out low-grade imports. Uganda’s USD 5 million solar-clinic program validates renewables in off-grid zones. Brazil and Argentina invest in community outreach to favelas and remote pampas, though currency swings complicate procurement.

Competitive Landscape

The mobile clinics market remains moderately fragmented. Full-service integrators who bundle chassis, medical gear, EHR links, and maintenance win bigger contracts because they simplify procurement. Small converters survive by tailoring specialty builds such as dental or veterinary vans. Technology is the new battleground. Vendors that drop FDA-cleared AI scanners and telehealth suites into turnkey packages command higher margins. Long build cycles, often six to 12 months, stress cash flow for smaller firms, encouraging future roll-ups.

Mobile Clinics Industry Leaders

ADI Mobile Health

Medical Coaches

Matthews Specialty Vehicles

Odulair LLC.

Farber Specialty Vehicles

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: CanSupport, backed by Optum India, unveiled two palliative-care vans to serve underserved cancer patients around Gurgaon.

- March 2025: Fujifilm introduced its “NURA Express” screening bus in Kozhikode, Kerala, expanding its preventive-health service footprint.

- January 2025: Aster Volunteers rolled out two mobile medical units in Gujarat to serve Sankari, Surat, and Khedbrahma districts.

- January 2025: India’s Artemis Hospital and Signature Global Foundation launched two AarogyaRise buses offering cancer screening, X-ray, and ICU services.

Global Mobile Clinics Market Report Scope

As per the scope of the report, mobile clinics are customized vehicles capable of traveling to different communities, both rural and urban, to offer healthcare and prevention services. In other words, mobile clinics are movable and independent healthcare units within or from which healthcare services are provided to individuals directly. The mobile clinics market is segmented by Clinic Type (Emergency care, Maternal Health, ICU and Surgery, Infant and Neonatal Health, Geriatric Care, Diagnostic/screening, and Others), Vehicle Type (Mobile Medical Vans, Mobile Medical Bus, and Others), Design Layout (Single Exam Room, Double Exam Room, and Triple Exam Room), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Emergency Care |

| Maternal Health |

| ICU & Surgery |

| Infant & Neonatal Health |

| Geriatric Care |

| Diagnostic / Screening |

| Mental Health |

| Dental Care |

| OPD |

| Reproductive & Contraceptive Services |

| Others |

| Mobile Medical Vans |

| Mobile Medical Buses |

| Trailers |

| Self-Propelled Trucks |

| Others |

| Single Exam Room |

| Double Exam Room |

| Triple Exam Room |

| Expandable Modular Pods |

| Primary & Preventive Care |

| Specialty Care |

| Diagnostic Imaging Services |

| Screening & Vaccination |

| Emergency & Disaster Response |

| Telehealth-Enabled Follow-Up |

| Hospitals & Health Systems |

| Government & Public-Health Agencies |

| NGOs & Charities |

| Private Healthcare Providers |

| Military & Defense |

| Corporate / Work-Site Programs |

| Basic (Minimal Tech) |

| Telehealth-Enabled |

| AI-Supported Diagnostics |

| Advanced Imaging-Equipped |

| Renewable / Zero-Emission Powertrain |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Clinic Type | Emergency Care | |

| Maternal Health | ||

| ICU & Surgery | ||

| Infant & Neonatal Health | ||

| Geriatric Care | ||

| Diagnostic / Screening | ||

| Mental Health | ||

| Dental Care | ||

| OPD | ||

| Reproductive & Contraceptive Services | ||

| Others | ||

| By Vehicle Type | Mobile Medical Vans | |

| Mobile Medical Buses | ||

| Trailers | ||

| Self-Propelled Trucks | ||

| Others | ||

| By Design Layout | Single Exam Room | |

| Double Exam Room | ||

| Triple Exam Room | ||

| Expandable Modular Pods | ||

| By Service Model | Primary & Preventive Care | |

| Specialty Care | ||

| Diagnostic Imaging Services | ||

| Screening & Vaccination | ||

| Emergency & Disaster Response | ||

| Telehealth-Enabled Follow-Up | ||

| By End-user | Hospitals & Health Systems | |

| Government & Public-Health Agencies | ||

| NGOs & Charities | ||

| Private Healthcare Providers | ||

| Military & Defense | ||

| Corporate / Work-Site Programs | ||

| By Technology Integration | Basic (Minimal Tech) | |

| Telehealth-Enabled | ||

| AI-Supported Diagnostics | ||

| Advanced Imaging-Equipped | ||

| Renewable / Zero-Emission Powertrain | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the mobile clinics market in 2026?

The mobile clinics market size is USD 6.24 billion in 2026.

What is the expected CAGR for mobile clinics through 2031?

The market is forecast to expand at a 7.96% CAGR to 2031.

Which clinic type is growing the fastest?

Maternal health units are projected to post a 10.34% CAGR between 2026 and 2031.

Why are trailers gaining popularity?

Trailers let operators upgrade clinical modules without replacing the tow vehicle and are growing at an 11.33% CAGR.

Which region is expanding the quickest?

Asia-Pacific is the fastest-growing region, advancing at a 9.32% CAGR through 2031.

Page last updated on: