Patient Journey Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

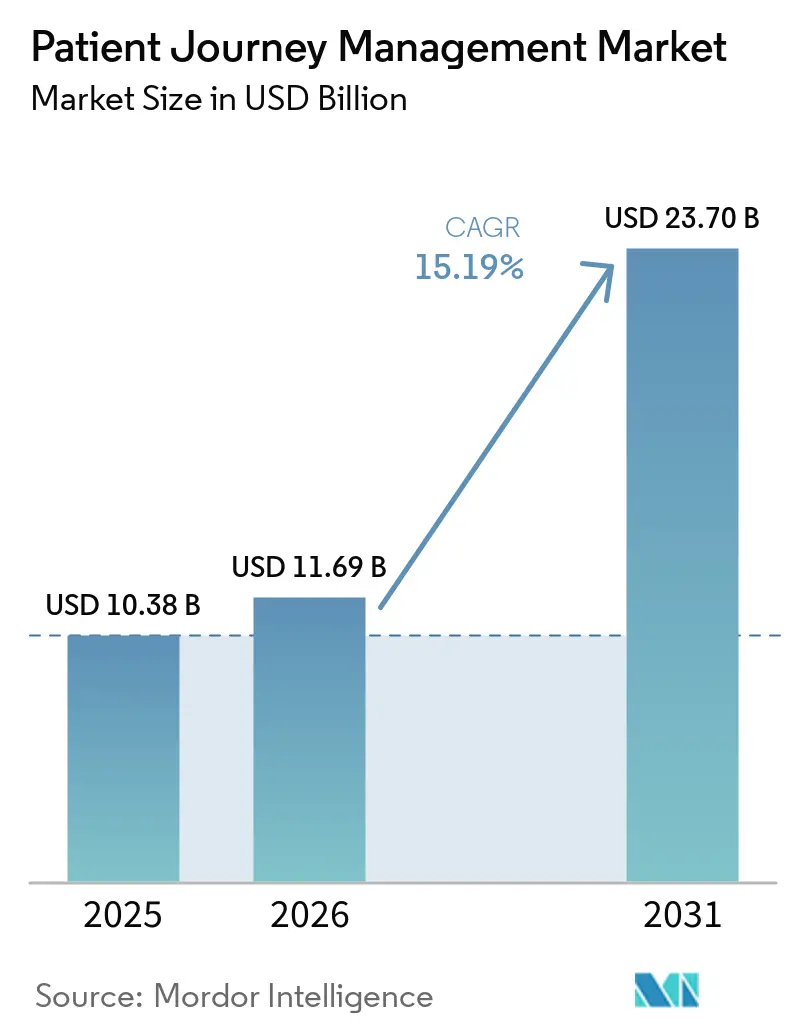

| Market Size (2026) | USD 11.69 Billion |

| Market Size (2031) | USD 23.70 Billion |

| Growth Rate (2026 - 2031) | 15.19% CAGR |

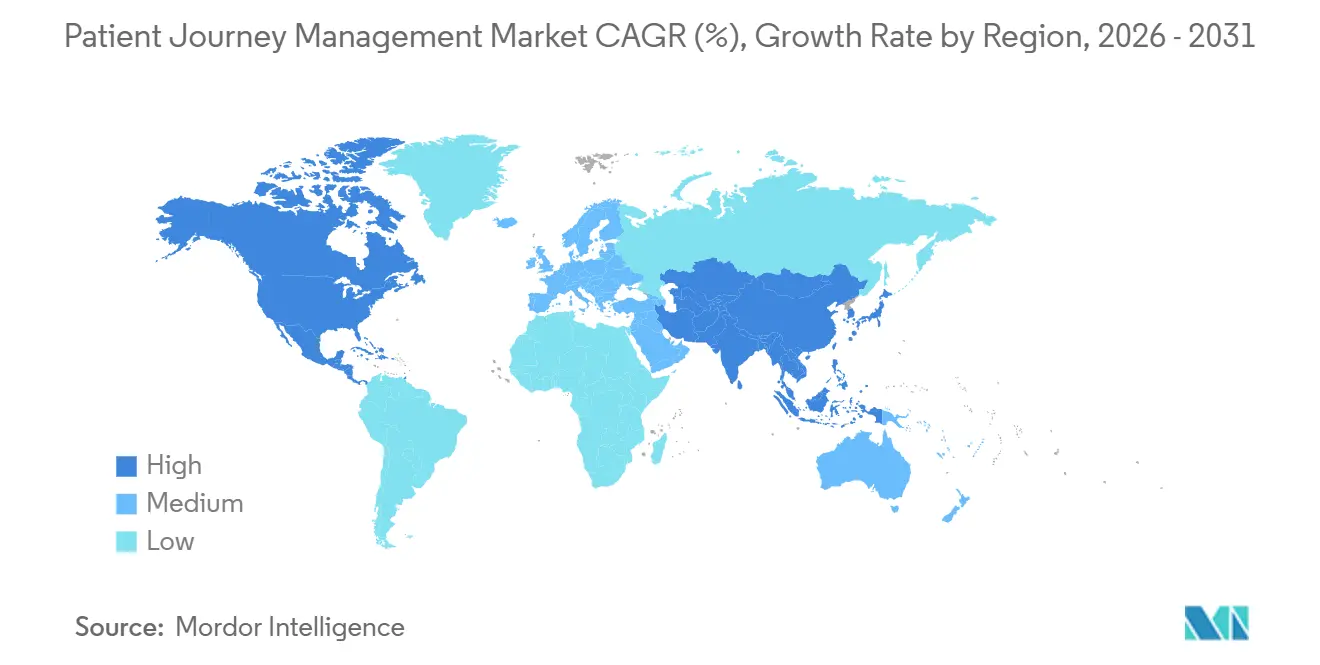

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Patient Journey Management Market Analysis by Mordor Intelligence

The patient journey management market size is projected to expand from USD 10.38 billion in 2025 and USD 11.69 billion in 2026 to USD 23.70 billion by 2031, registering a CAGR of 15.19% between 2026 and 2031. The strongest near-term support for the patient journey management market is the move toward outcome-linked reimbursement, with CMS making episode accountability more immediate for hospitals through TEAM in January 2026. Health systems that built stronger coordination capabilities ahead of this shift were already showing measurable financial returns, including Providence Health, which generated USD 177 million in Medicare savings in 2025 and earned a shared savings award of more than USD 127 million. The patient journey management market is also being lifted by demand for unified engagement, analytics, and workflow tools that reduce friction across communication and care transitions, as shown by new embedded integrations such as NiCE CXone with Epic and Oracle’s expanding interoperability stack. At the same time, structured social risk data, consumer-grade health interfaces, and privacy-preserving data environments are pushing the patient journey management market toward a single platform layer that can support both clinical and commercial workflows. Competitive pressure is rising as larger platforms expand natively into care coordination and patient communication, while the main risk remains that slower reimbursement reform or a rollback in mandatory bundled payment models could reduce the urgency of enterprise deployment.

Key Report Takeaways

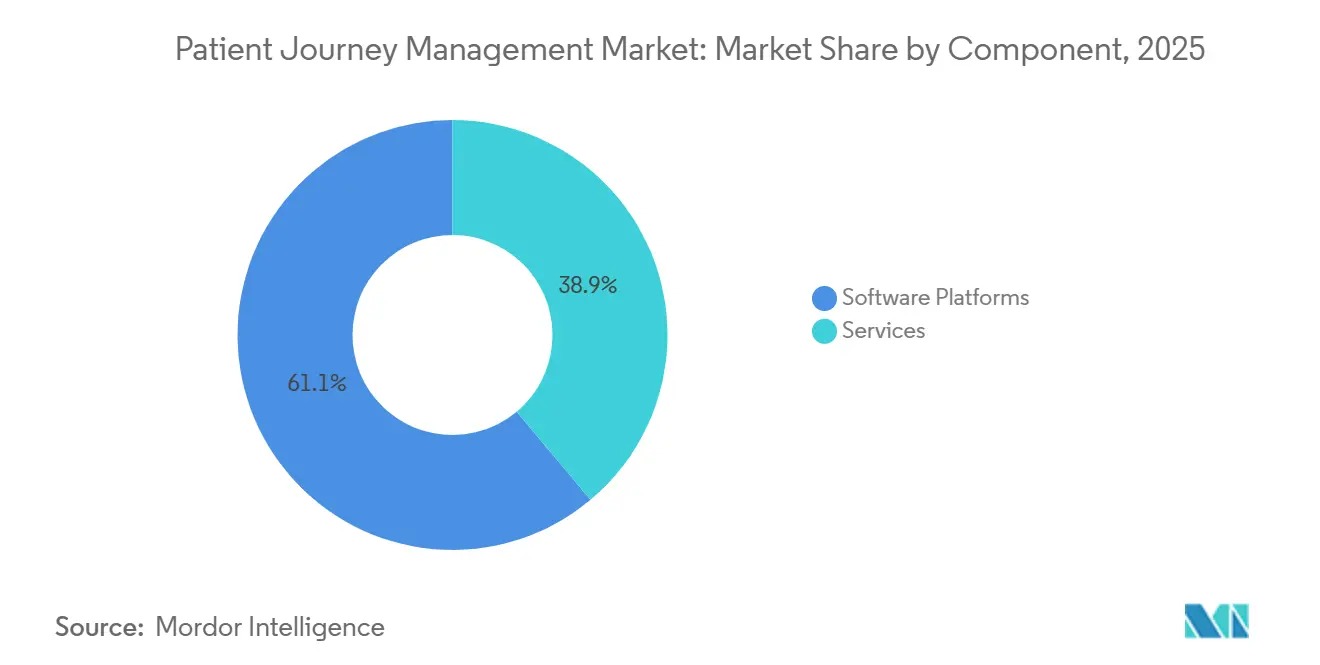

- By component, software platforms held 61.14% of revenue in 2025, while the same segment is projected to record the fastest growth at a 21.33% CAGR through 2031.

- By deployment mode, cloud-based deployment accounted for 63.45% of revenue in 2025 and is also the fastest-growing mode at a 20.57% CAGR through 2031.

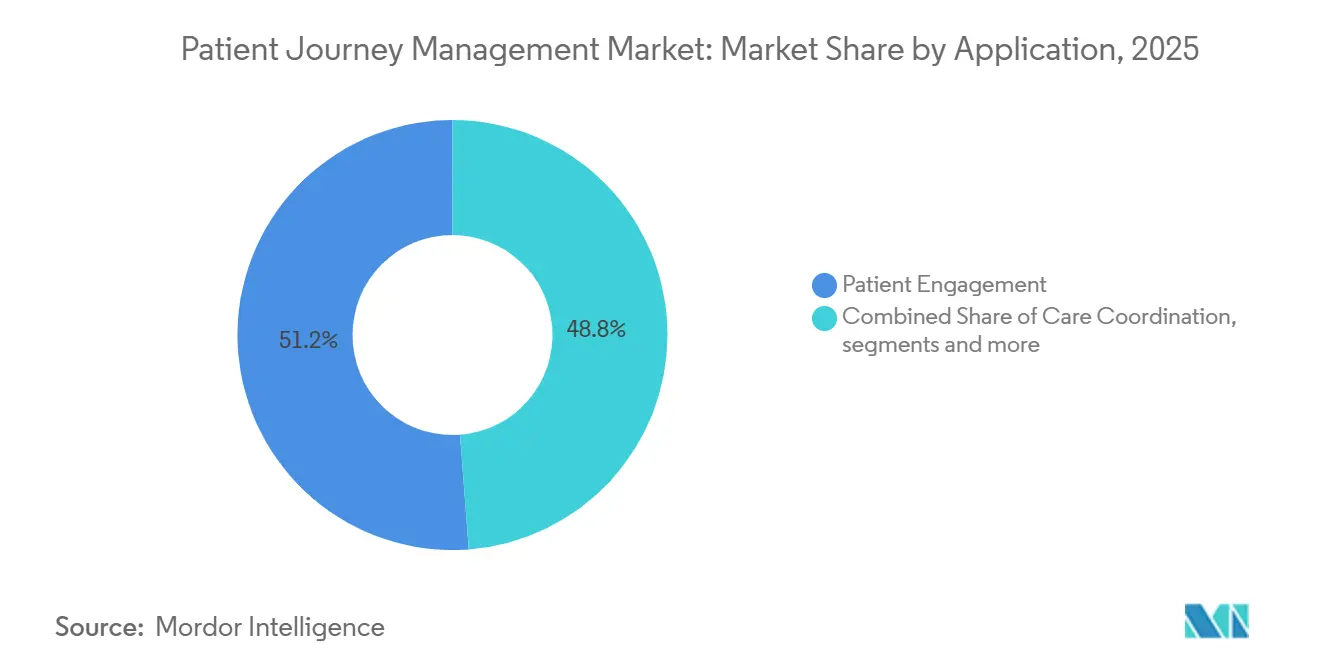

- By application, patient engagement led with 51.24% revenue share in 2025, while workflow automation is forecasted to expand at a 21.41% CAGR through 2031.

- By end user, healthcare providers held 53.23% of revenue in 2025, while healthcare payers are projected to record the fastest growth at a 20.62% CAGR through 2031.

- By geography, North America accounted for 52.36% of the 2026 global revenue base, while Asia-Pacific is projected to expand at a 22.64% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Patient Journey Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Shift Toward Value-Based Care Reimbursement Models | +3.8% | Global, with early acceleration in North America | Short term (≤ 2 years) |

| Growing Adoption of Omnichannel Patient Engagement Platforms | +2.7% | North America and Europe, with spillover to Asia-Pacific private hospitals | Medium term (2-4 years) |

| Integration of Real-Time Analytics With EHRs | +2.4% | Global, with largest effect in North America and Asia-Pacific academic medical centers | Short term (≤ 2 years) |

| Mainstreaming of Consumer-Grade CRM Suites into Healthcare | +1.9% | North America, Western Europe, and core Asia-Pacific markets | Medium term (2-4 years) |

| AI-Driven Social Determinant Insights in Care Pathway Design | +2% | Global, with regulatory concentration in North America | Medium term (2-4 years) |

| Privacy-Preserving Data Clean Rooms for Cross-Provider Journey Stitching | +1.3% | North America and Europe, with spillover to selected Middle East and Africa markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift Toward Value-Based Care Reimbursement Models

The transition to value-based care has moved from optional pilots to a stronger compliance and payment framework, which gives the patient journey management market a direct operating need. CMS launched TEAM in January 2026 across 740 hospitals and HFMA reported that the proposed CJR-X path would extend mandatory bundled payments further from September 2027.[1]Sound Physicians, “Hospital Strategies for Winning Under CMS' New Value-Based Payment Models,” Sound Physicians, soundphysicians.com HFMA also noted that the Hospital Value-Based Purchasing Program continues to reinforce accountability through a 2% payment withhold, which keeps care coordination tied closely to financial performance. Providence Health showed what this can look like at scale by generating USD 177 million in Medicare savings in 2025 and earning a shared savings award of more than USD 127 million across a 51-hospital network. That changes the role of the patient journey management market from a patient experience purchase into a revenue protection layer that influences readmissions, post-acute navigation, and shared savings capture. Health systems that still rely on fragmented coordination tools are therefore entering each new mandated bundle with a structural disadvantage.

Growing Adoption of Omnichannel Patient Engagement Platforms by Large Hospital Networks

Large hospital networks are consolidating call centers, portals, messaging, and front-desk workflows because fragmented communication weakens continuity across the patient journey management market. NiCE announced in April 2026 that CXone now integrates natively with Epic and brings voice, chat, SMS, WhatsApp, and social channels into one workspace.[2]NiCE, “NiCE CXone Integration With Epic Brings Patient Engagement and Context Into One Workspace,” NiCE, nice.com The same platform direction is visible on the payer side, where CVS Health and Salesforce expanded Agentforce Health in May 2026 across call center operations for member navigation and provider interactions. These changes lower training friction because staff can work from a familiar interface rather than move across disconnected tools. The patient journey management market is therefore shifting toward embedded engagement within core operational systems instead of separate outreach layers. Vendors that depend on loose third-party integration face slower adoption as buyers increasingly prefer one operating surface for service, navigation, and follow-up.

Integration of Real-Time Analytics with EHRs to Reduce Revenue Leakage

Revenue leakage from denials, underpayments, and fragmented billing follow-up has become a stronger adoption trigger inside the patient journey management market. FinThrive launched its Denials and Underpayments Analyzer in June 2025 to combine denial management with underpayment detection in a real-time workflow rather than static post-adjudication reporting.[3]FinThrive, “FinThrive Debuts Denials and Underpayments Analyzer at HFMA 2025,” PR Newswire, prnewswire.comThe importance of this use case extends beyond revenue cycle because opaque billing and poor follow-up can weaken trust and reduce future utilization from the same health system. Oracle strengthened this direction in April 2026 by achieving CMS Aligned Network status, which supports standards-based FHIR exchange with Qualified Health Information Networks.[4]Oracle, “Oracle Health Demonstrates Interoperability Leadership, Achieves CMS Aligned Network Status,” Oracle, oracle.com That kind of data access makes the patient journey management market more useful across care settings because analytics can move with the patient instead of stopping at one facility boundary. As operating margins remain tight, health systems are placing more value on tools that connect financial continuity with clinical continuity in one workflow.

AI-Driven Social Determinant Insights Influencing Care Pathway Design

Social risk is becoming a stronger pathway variable inside the patient journey management market rather than a side note in care planning. A May 2026 study in JMIR Medical Informatics found that GPT-5-mini and o4-mini models extracted social determinants of health from unstructured clinical text at performance levels that surpassed traditional rule-based NLP without task-specific fine-tuning. That matters because structured social data becomes cheaper to produce at scale when systems can work directly from clinical documentation. UCSF SIREN also noted that health inequity could cost the United States nearly USD 300 billion by 2050, which puts financial weight behind better social risk identification and response. The patient journey management market stands to benefit because platforms that can organize screening outputs, outreach steps, and follow-up actions in one place are better aligned with current payer and provider priorities. As quality models ask for more documented intervention, social determinant functionality is moving closer to the center of care pathway design.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented IT Landscapes Inside Multi-Facility Health Systems | -2.1% | Global, most acute in United States multi-facility systems and Asia-Pacific public hospitals | Short term (≤ 2 years) |

| High Total Cost of Ownership and Long Payback Period | -1.8% | Global, most restrictive for community and safety-net providers in North America, South America, and Middle East and Africa | Medium term (2-4 years) |

| Provider Liability Concerns Around Algorithmic Treatment Recommendations | -1.3% | Global, concentrated in North America and Western Europe | Medium term (2-4 years) |

| Limited Longitudinal Data Availability in Emerging Markets | -1% | Emerging Asia-Pacific economies, South America, and Middle East and Africa outside GCC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented IT Landscapes Inside Multi-Facility Health Systems

IT fragmentation remains the most immediate operational barrier for enterprise rollout in the patient journey management market. The CHIME Leadership Pulse Survey released in February 2026 found that 80% of health IT leaders named interoperability as a top priority and 76% said too many point solutions were actively impeding operations. The same release said some enterprise systems run more than 100 tools across safety, compliance, provider management, and patient experience functions. Oracle’s April 2026 CMS Aligned Network milestone shows that standards-based exchange is improving, but operational alignment still takes more than technical connectivity. The patient journey management market still slows when multi-facility systems must map data definitions, redesign workflows, and manage local variation across hospitals. Until semantic interoperability becomes more consistent, large deployments will keep absorbing time and cost through custom integration work.

High Total Cost of Ownership & Long Payback Period for Advanced Journey Platforms

High total cost of ownership continues to hold back the patient journey management market, especially outside large integrated delivery networks. CHIME reported in February 2026 that 85% of health IT leaders saw financial limitations as the leading barrier to technology change, while 70% prioritized reduced total cost of ownership in vendor selection. This cost burden comes from more than software because deployment often includes migration, interface redesign, staff training, governance, and support services. Health Catalyst’s August 2024 acquisition of Lumeon made that relationship clear by combining care orchestration with analytics and Tech-Enabled Managed Services in one operating model. Lumeon also stated that its platform had transformed the care journeys of more than 10 million patients in one year and improved care team capacity by 60%, which shows the value case but also the scale of organizational change behind it. The patient journey management market therefore keeps a structural adoption gap between well-funded health systems and community or safety-net providers that face longer payback periods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platforms Drive Consolidation in Patient Journey Management

Software platforms held 61.14% of the patient journey management market share in 2025 and are projected to expand at a 21.33% CAGR through 2031. This combination of scale and speed shows that buyers are leaning toward one software layer that can support engagement, analytics, and care orchestration together. The patient journey management market is moving toward suites that sit close to the EHR and reduce the need for separate applications across outreach, navigation, and billing continuity. Oracle’s AI-powered patient portal and Clinical AI Agent show how large vendors are placing more workflow steps inside native environments rather than leaving them to separate tools. That shift makes differentiation harder for narrow vendors when the same health system can activate similar functions within a broader existing platform.

Services represented the remaining share of the patient journey management market and remained important because enterprise deployment still depends on integration, training, and workflow redesign. Health Catalyst reinforced this point in August 2024 when it finalized the acquisition of Lumeon and integrated care orchestration with analytics and Tech-Enabled Managed Services. Before the acquisition, Lumeon said its Conductor platform had transformed the care journeys of more than 10 million patients in a single year. Lumeon also reported a 60% improvement in care team capacity, which explains why services still shape vendor selection alongside software capability. In the patient journey management industry, implementation support remains central because software value is only realized after operational adoption across scheduling, follow-up, and care coordination teams.

By Deployment Mode: Cloud Accelerates as EHR-Native Integrations Mature

Cloud-based deployment accounted for 63.45% of the 2025 revenue base and is projected to grow at a 20.57% CAGR through 2031. The patient journey management market is favoring cloud delivery because providers want subscription economics, quicker upgrades, and easier scaling across sites. Standards-based data exchange also fits cloud models more naturally when organizations need information to move across facilities and partner networks. As the patient journey management market adds more automation, reminders, routing logic, and self-service interactions, cloud delivery lets vendors update those functions without long release cycles.

On-premise deployment remains relevant in government hospitals and data-sovereign settings across Asia-Pacific and the Middle East. These buyers still place more weight on local control, residency rules, and internal security review than on faster deployment alone. Even so, the patient journey management market is leaning toward hybrid and cloud-first models where interoperability standards are maturing and time to value matters more. Datavant and AWS strengthened that direction in November 2025 when they made privacy-preserving data discovery and analytics available through a clean-room model that supports collaboration without moving raw data between organizations. This leaves on-premise architecture concentrated in cases where policy or infrastructure, rather than product capability, decides the deployment model.

By Application: Patient Engagement Anchors Revenue, Workflow Automation Accelerates

Patient engagement accounted for 51.24% of the patient journey management market size in 2025, while workflow automation is projected to expand at a 21.41% CAGR through 2031. Health systems still begin with engagement because scheduling, pre-visit education, inpatient communication, and post-discharge follow-up are the most visible friction points for patients. The patient journey management market is also seeing engagement tools tied more directly to call center operations, billing support, and digital navigation rather than treated as separate outreach programs. Oracle’s AI-powered patient portal showed this direction by adding conversational support for medical record questions inside the patient interface. That makes engagement not only a communication task, but also a retention and continuity function inside the patient journey management market.

Workflow automation is expanding faster because health systems need to handle labor pressure without matching it with proportional headcount growth. In the patient journey management market, this covers billing follow-up, prior authorization steps, referral movement, care coordination triggers, and routing of next-best actions across teams. The patient journey management market is also placing more weight on applications that can connect quality reporting, social risk response, and utilization workflows in the same operating layer. As payment models ask for more documented follow-up and faster resolution, workflow automation is moving from an efficiency tool to a core system requirement.

By End User: Providers Anchor the Market, Payers Emerge as Journey Orchestrators

Healthcare providers represented 53.23% of 2025 revenue, while healthcare payers are projected to expand at a 20.62% CAGR through 2031. Providers remain the anchor of the patient journey management market because they own the episode workflow across referral, treatment, discharge, and post-acute follow-up. They also face the most direct financial impact when poor coordination affects readmissions, quality scores, or bundled payment performance. Payers are growing faster because they increasingly treat navigation, quality performance, and digital support as competitive tools instead of administrative functions. CVS Health’s May 2026 expansion with Salesforce across member and provider interactions shows that payer-led journey orchestration is moving into core operations at scale.

Pharmaceutical and life sciences companies form a smaller but expanding end-user group in the patient journey management market. Salesforce said in 2026 that Agentforce Life Sciences is being used by more than 140 organizations, including AstraZeneca, Novartis, and Pfizer. These deployments support benefits verification, adherence programs, and service continuity around therapy use. Digital health and telehealth providers also remain strategically relevant because they are structured around longitudinal patient contact rather than one-time visits. Teladoc reported that its integrated care segment generated USD 395.4 million in Q1 2026 revenue, up 2% year over year, which shows that virtual-care-led orchestration still holds commercial weight inside the patient journey management industry.

Geography Analysis

North America represented 52.36% of the patient journey management market share in 2025, which made it the largest regional revenue base. The United States drives most of that demand because TEAM went live across 740 hospitals in January 2026 and made episode-level coordination more urgent. Providence Health’s USD 177 million in Medicare savings during 2025 shows the financial return available when a system operationalizes care coordination at enterprise scale. The region also benefits from stronger interoperability pressure, payer quality incentives, and a mature vendor base spanning CRM, analytics, and care management. Oracle’s CMS Aligned Network status is one example of the standards push that supports broader deployment across the patient journey management market in North America.

Asia-Pacific is the fastest-growing region in the patient journey management market, with a projected 22.64% CAGR for 2026 to 2031. Growth is being supported by smart-hospital build-outs, rising private hospital investment, and broader digital record infrastructure across major healthcare systems. Japan offers a clear example, with TIS and Towa Yakuhin introducing the Healthcare Passport platform at Hiroo Hospital in April 2026 to support patient-controlled records and multi-provider data integration. The patient journey management market in Asia-Pacific also benefits from large patient volumes and growing expectations for digital navigation. Implementation speed still varies by country because data rules, hospital funding, and IT maturity are not uniform across the region.

Europe holds a meaningful position in the patient journey management market because established healthcare IT infrastructure gives providers a stronger digital base. France’s 2025 Digital Health Doctrine and Ségur Numérique Wave 2 are pushing state-backed digitization and interoperability alignment across hospitals and ambulatory physicians. The Middle East and Africa, led by GCC smart-hospital investment, and South America, led by Brazil’s expanding digital health ecosystem, are moving from pilot activity toward wider deployment. Growth outside North America and Asia-Pacific remains uneven because public budget cycles and legacy system replacement still shape timing more strongly than demand.

Competitive Landscape

The patient journey management market remains fragmented at the product level, but it is consolidating around broader platform ecosystems. EHR incumbents and enterprise cloud vendors are extending into engagement, workflow, analytics, and navigation, which raises the bar for smaller standalone vendors. Oracle launched its Clinical AI Agent for emergency and inpatient care in March 2026 and widened its role in workflow automation inside provider settings. These moves show that native integration and interoperability compliance are becoming central competitive levers in the patient journey management market.

Specialist vendors still hold space in the patient journey management market by focusing on care orchestration, access management, analytics depth, and healthcare-specific rollout support. Health Catalyst’s August 2024 acquisition of Lumeon combined a care orchestration platform with analytics and Tech-Enabled Managed Services, which shows how vendors are linking software with delivery capability. Datavant Connect powered by AWS Clean Rooms became broadly available in November 2025 and created a privacy-preserving route to analyze journeys across disconnected datasets. That matters because payer and provider accounts increasingly want longitudinal visibility without moving raw data. The patient journey management market is therefore rewarding vendors that can pair workflow depth with trusted data connectivity.

Salesforce is pushing the patient journey management market toward a more consumer-grade operating model, and its May 2026 expansion with CVS Health showed deployment across member navigation and provider interactions at enterprise scale. Qualtrics added another source of competitive pressure in May 2026 when it acquired Press Ganey Forsta for USD 6.75 billion and linked a very large healthcare experience dataset with its AI-powered experience management platform. Teladoc’s integrated care revenue of USD 395.4 million in Q1 2026 shows that longitudinal digital care models still support commercial scale. As a result, competitive advantage in the patient journey management market now depends on native integration, deployment capacity, and the ability to support both clinical and commercial workflows within one platform layer.

Patient Journey Management Industry Leaders

Salesforce, Inc.

Oracle

Merative

Press Ganey Associates

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Qualtrics completed the acquisition of Press Ganey Forsta for USD 6.75 billion, merging the world’s largest healthcare experience dataset, covering more than 41,000 healthcare facilities, with Qualtrics’ AI-powered Experience Management platform. The combination creates a large AI dataset for human experiential context in healthcare, with direct implications for patient journey benchmarking and voice-of-customer-driven care improvement programs.

- May 2026: Salesforce and CVS Health expanded their collaboration to deploy Agentforce Health across CVS Health’s call center operations, covering member navigation and provider interactions across multiple CVS business lines, including pharmacy, medical benefits, and Medicare Advantage. The partnership signals large payers’ readiness to deploy AI-driven, consumer-grade patient journey infrastructure at population scale.

- April 2026: Oracle Health achieved CMS Aligned Network status, enabling standards-based FHIR data exchange with Qualified Health Information Networks, unlocking more seamless cross-provider patient data sharing and strengthening Oracle’s real-time analytics and care coordination use case.

Global Patient Journey Management Market Report Scope

According to the report’s scope, the patient journey management market refers to the industry focused on digital platforms and solutions that help healthcare providers manage and optimize the entire patient care journey, from appointment scheduling and patient engagement to treatment coordination, follow-up, and post-care support. These solutions improve care continuity, patient experience, operational efficiency, and health outcomes through data-driven communication and workflow management.

The patient journey management market is segmented into component, deployment mode, application, end user, and geography. By component, the market is segmented into software platforms and services. By deployment mode, the market is segmented into on-premise and cloud-based. By application, the market is patient engagement, care coordination, navigation and access management, workflow automation, and others. By end user, healthcare providers, pharmaceutical and life-sciences companies, healthcare payers, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Software Platforms |

| Services |

| On-Premise |

| Cloud-Based |

| Patient Engagement |

| Care Coordination |

| Navigation and Access Management |

| Workflow Automation |

| Others |

| Healthcare Providers |

| Pharmaceutical and Life-Sciences Companies |

| Healthcare Payers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software Platforms | |

| Services | ||

| By Deployment Mode | On-Premise | |

| Cloud-Based | ||

| By Application | Patient Engagement | |

| Care Coordination | ||

| Navigation and Access Management | ||

| Workflow Automation | ||

| Others | ||

| By End User | Healthcare Providers | |

| Pharmaceutical and Life-Sciences Companies | ||

| Healthcare Payers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the patient journey management space and how fast is it growing?

It reached USD 11.69 billion in 2026 and is projected to reach USD 23.70 billion by 2031, growing at a 15.19% CAGR over 2026 to 2031.

Which region leads global revenue and which one is expanding the fastest?

North America leads with 52.36% of the 2026 revenue base, while Asia-Pacific is expected to be the fastest-growing region with a 22.64% CAGR through 2031.

Which application area brings in the most revenue today?

Patient engagement leads applications with 51.24% of 2025 revenue because providers still prioritize scheduling, education, communication, and follow-up across the care journey.

Which end-user group is growing the fastest?

Healthcare payers are projected to be at the fastest at a 20.62% CAGR through 2031 as navigation, quality performance, and digital member support become strategic priorities.

Page last updated on: