U.S. Personal Mobility Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

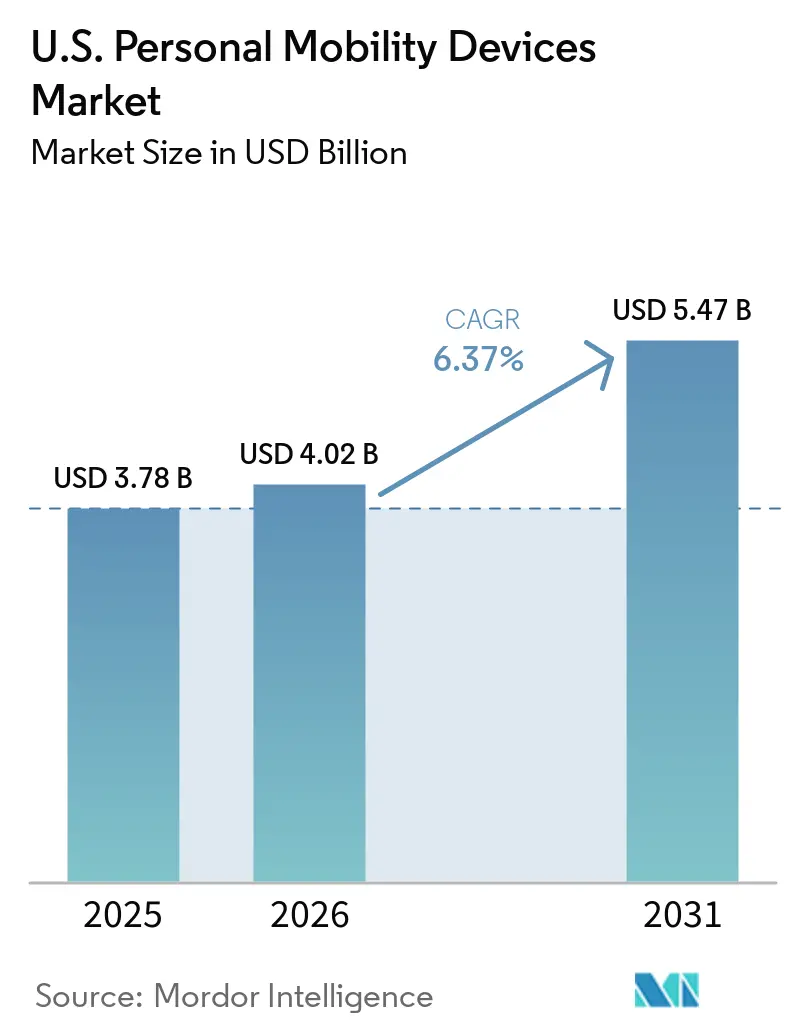

| Base Year Market Size (2025) | USD 3.78 Billion |

| Market Size (2026) | USD 4.02 Billion |

| Market Size (2031) | USD 5.47 Billion |

| Growth Rate (2026 - 2031) | 6.37% CAGR |

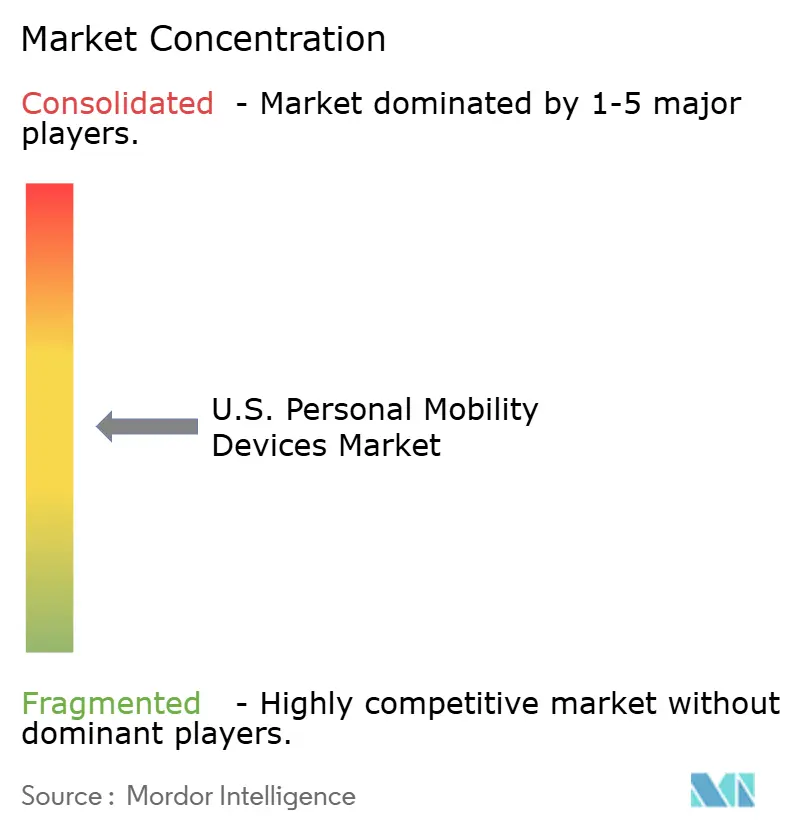

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Personal Mobility Devices Market Analysis by Mordor Intelligence

The U.S. Personal Mobility Devices Market size is projected to expand from USD 3.78 billion in 2025 and USD 4.02 billion in 2026 to USD 5.47 billion by 2031, registering a CAGR of 6.37% between 2026 to 2031.

Demand is shifting toward home settings as households, home healthcare providers, and DME rental networks increasingly manage mobility support. This transition drives broader device ownership and repeat replacement demand. Reimbursement policies are critical, with CMS coverage expansion, seat-elevation reimbursement pathways, and faster prior authorization processes improving access and boosting supplier confidence in high-value products. In 2024, 47.9 million Americans, representing 14.14% of the total United States population of 338.8 million, live with a documented disability. This marks an increase for the second consecutive year.[1]Center for Research on Disability, “2026 Annual Report on People With Disabilities in America,” Research on Disability, researchondisability.org Mobility disabilities remain the most common type among adults, with CDC data showing a sharp rise in incidence, particularly among middle-aged groups who face heavier disability burdens compared to earlier generations at the same age.

Key Report Takeaways

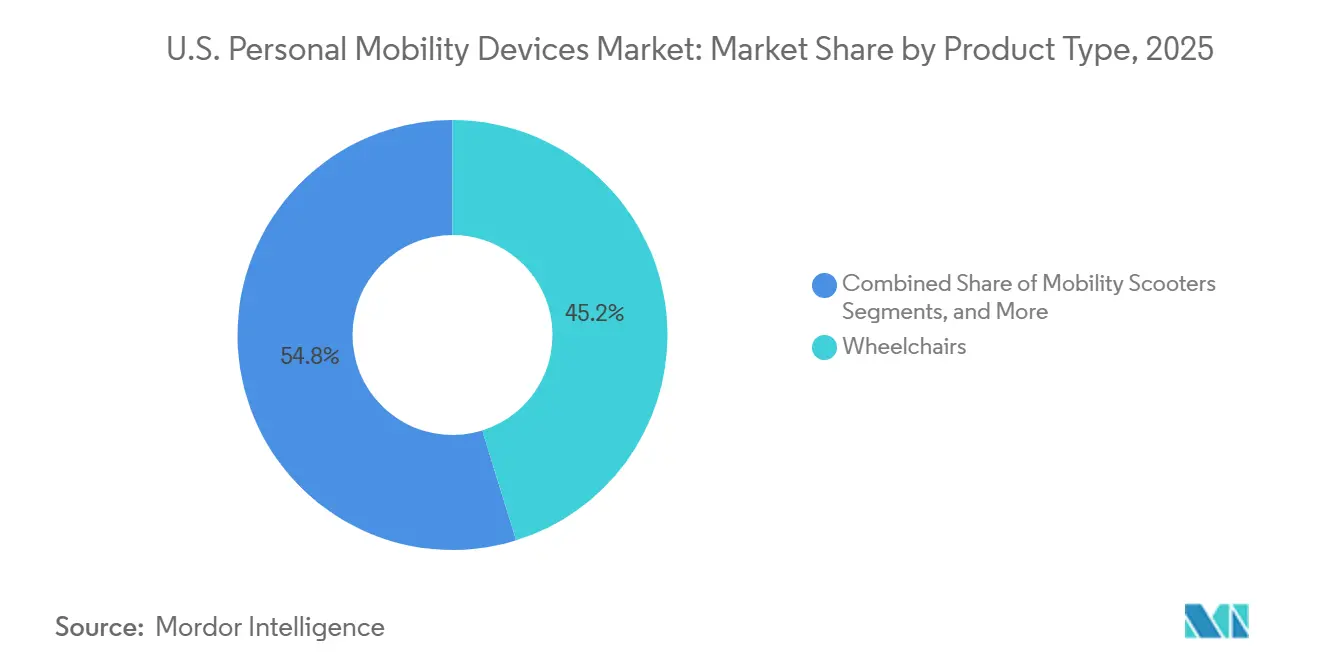

- By product type, wheelchairs held 45.21% of the US personal mobility devices market share in 2025, while mobility scooters are projected to grow at a 6.66% CAGR through 2031.

- By technology, manual devices accounted for 50.45% share of the US personal mobility devices market size in 2025, while powered devices are expected to expand at a 7.12% CAGR through 2031.

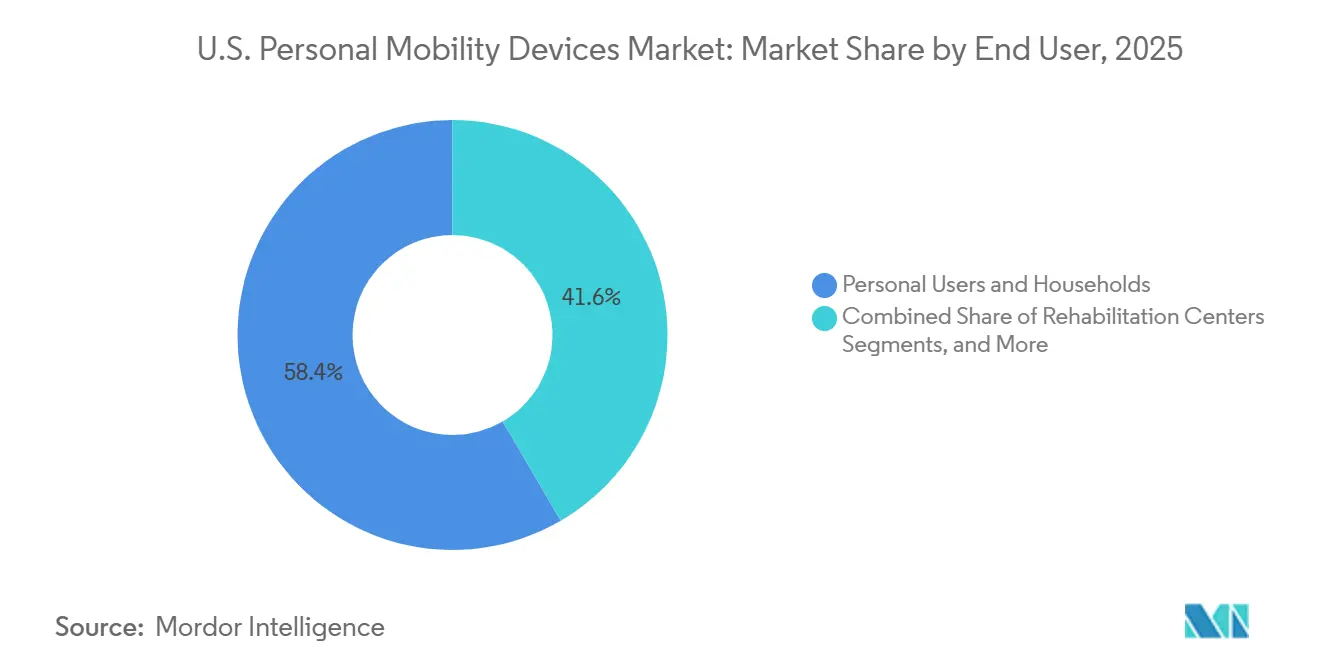

- By end user, personal users and households captured 58.40% of the US personal mobility devices market share in 2025, while home healthcare and DME rental providers are projected to grow at an 8.10% CAGR through 2031.

- By distribution channel, the offline channel accounted for 69.77% share of the US personal mobility devices market size in 2025, while e-commerce is expected to advance at a 9.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Personal Mobility Devices Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Aging population and rising mobility-loss years lived | +1.9% | National, with concentrated demand in Sun Belt states such as Florida, Texas, and Arizona | Long term (≥ 4 years) |

| High disability and arthritis burden expanding addressable users | +1.2% | National, with higher burden in Southern and Midwestern states | Long term (≥ 4 years) |

| Medicare coverage breadth and seat-elevation reimbursement update | +0.9% | National, across all Medicare Part B jurisdictions | Medium term (2-4 years) |

| Shift to lighter, foldable, connected power mobility platforms | +0.8% | National, with stronger pull in urban and suburban markets | Medium term (2-4 years) |

| Airline liability reforms improving travel confidence for device users | +0.4% | National, especially in major air travel hubs such as Atlanta, Chicago, Los Angeles, Dallas, and New York | Short term (≤ 2 years) |

| Rapid e-commerce penetration in DME | +0.7% | National, with disproportionate impact in rural and underserved areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging U.S. Population and Rising Mobility-Loss Years Lived

Motor function impairments among older Americans show a steep age-related pattern. Chair-stand impairments are significant in the 65 to 69 age group, while gait-speed issues dominate among those aged 90 and above.[2]Centers for Disease Control and Prevention, “Disability and Health Data,” CDC, cdc.gov The next wave of retirees carries heavier disability burdens from middle age, leading to earlier adoption of mobility aids. Rising musculoskeletal disorders and fall-related mortalities among adults aged 65 and older indicate increasing reliance on powered support. This trend sustains replacement demand and ties the United States personal mobility devices market to demographic shifts rather than short-term care cycles.

High Disability and Arthritis Burden Expanding Addressable Users

Stroke and osteoarthritis are key drivers of wheelchair and scooter use in the United States, broadening the user base across age groups and care settings. A 2024 study of 64.1 million adults with arthritis found that age over 70, severe pain, and comorbidities significantly limit physical functioning, creating a large pool of intermittent and permanent device users.[3]PLOS One, “Cohort Patterns in Disability Burden,” PLOS One, plos.org The disability share of the United States population rose to 14.14% in 2024, marking a second consecutive year of increase. This growing user base favors lightweight, foldable, and mid-range devices, positioning suppliers with diverse inventories to capture market growth.

Medicare Coverage Breadth and Seat-Elevation Reimbursement Update

CMS now recognizes power seat elevation equipment as reimbursable durable medical equipment for eligible wheelchair users, enhancing the commercial appeal of high-spec chairs and accessories. This policy influences commercial insurers and Medicaid, which often align with CMS standards. From January 1, 2025, CMS reduced the prior authorization review period for DMEPOS items to 7 days, expediting product delivery.[4]Centers for Medicare & Medicaid Services, “National Coverage Determination 280.16,” CMS, cms.gov Additionally, CMS introduced a prior authorization exemption in December 2025 for compliant suppliers, giving an operational edge to vendors with strong documentation and EHR workflows in the United States personal mobility devices market.

Shift to Lighter, Foldable, Connected Power Mobility Platforms

The United States personal mobility devices market is rapidly evolving with manufacturers adopting advanced materials like titanium and aircraft-grade aluminum, along with lithium-ion batteries and app-based controls. In 2026, Permobil launched TiLite TR and TiLite ZR titanium wheelchairs, offering lighter components and enhanced customization for improved manual performance. Sunrise Medical introduced the Empulse M90 wheel add-on in 2025, enabling motorized propulsion for manual wheelchair users. Regulatory acceptance of connected mobility features, such as app-controlled operations, is growing, driving demand for products that combine portability, convenience, and clinical performance.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High out-of-pocket burden for advanced powered devices | -0.8% | National, with sharper pressure in states without full Medicaid expansion | Long term (≥ 4 years) |

| Medicare home-use test and documentation friction limiting approval | -0.6% | National, across all Medicare Part B jurisdictions | Medium term (2-4 years) |

| Repair downtime, battery and caster failures, and weak service density | -0.4% | Rural and non-metropolitan markets | Medium term (2-4 years) |

| Safety recalls and rising litigation on lithium-ion fire risk | -0.3% | National, with consumer-channel devices disproportionately affected | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Burden for Advanced Powered Devices

Advanced complex rehabilitative power wheelchairs often exceed USD 30,000, with Medicare covering only a portion of the cost and secondary insurance varying widely. A 2025 disability-rights survey revealed that Medicare users faced partial reimbursements, delays, and significant out-of-pocket expenses, leading to increased pain, reduced activity, and social isolation. In 2024, the poverty rate for working-age adults with disabilities was 24.8%, compared to 11.1% for non-disabled adults, highlighting financial barriers to accessing premium devices.

Safety Recalls & Rising Litigation on Lithium-ion Fire Risk

Lithium-ion battery thermal runaway remains a key compliance risk in the United States personal mobility devices market, leading to recalls, legal challenges, and higher engineering costs. In April 2026, the FDA issued a Class 1 recall for WHILL Model F powered wheelchairs due to software faults increasing patient harm risks. Similarly, in June 2025, the FDA announced a Class 2 recall for Mobius Mobility’s iBOT PMD, requiring field corrections. While ISO standards emphasize battery safety, compliance inconsistencies persist, particularly outside specialist channels. Budget brands and low-cost scooters face greater risks of service disruptions and liability compared to premium suppliers with advanced battery management systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Power Platform Diversification Reshaping the Category Mix

In 2025, wheelchairs accounted for 45.21% of the United States personal mobility devices market, driven by established reimbursement pathways and urgent clinical needs. Manual and complex rehabilitative power wheelchairs remain key, while power wheelchairs are gaining traction due to expanded coverage and improved designs. Mobility scooters, with a projected CAGR of 6.66% from 2026 to 2031, cater to ambulatory users needing enhanced community and outdoor mobility. Walking aids, including canes, crutches, walkers, and rollators, maintain steady demand due to affordability and ease of purchase. The category mix is evolving as buyers increasingly opt for power-assist and positioning add-ons instead of transitioning directly to powered chairs. Sunrise Medical’s Empulse M90 enables cost-effective upgrades to manual chairs with motorized propulsion.

By Technology: Connected Intelligence Accelerating Premium Tier Growth

Manual devices accounted for 50.45% of the technology split in 2025, reflecting the widespread use of manual wheelchairs, walkers, and rollators. Powered devices, projected to grow at a 7.12% CAGR from 2026 to 2031, are gaining popularity due to reduced self-propulsion ability, better reimbursement support, and higher comfort expectations. Power-assist and hybrid systems bridge the gap, offering motorized support without requiring a full transition to premium powered frames.

Advanced features are increasingly moving from specialized rehabilitation products to standard configurations. Sunrise Medical introduced Dynamic Controls LiNX controls in the QUICKIE Q300 M Mini, narrowing the gap between premium and mid-market products.

By End User: Homecare Migration Concentrating Commercial Opportunity

In 2025, personal users and households represented 58.40% of the end-user segment, reflecting a shift toward home-based mobility support. Home healthcare and DME rental providers, projected to grow at an 8.10% CAGR from 2026 to 2031, are driving demand as post-acute care increasingly moves to residential settings. Products like walkers, rollators, entry-level scooters, and lower-acuity wheelchairs align with this trend due to their quick deployment in households.

Institutional channels remain significant, particularly in long-term care and assisted living, where operators prioritize reliable supply over premium features. A 2025 Mayo Clinic Proceedings study revealed delays in Medicare-listed wheelchair supplier services, prompting some users to seek alternatives outside traditional referral chains.

By Distribution Channel: E-Commerce Acceleration Redefining DME Procurement

Offline channels held 69.77% of the market in 2025, emphasizing the importance of in-person assessments, insurance handling, and supplier-managed setups. E-commerce, with a projected CAGR of 9.05% from 2026 to 2031, is growing rapidly due to broader product assortments, easier comparisons, and better access in underserved areas. This growth is strongest for products requiring minimal clinical customization, such as walkers, canes, and lower-acuity scooters.

The channel shift is uneven, as products requiring CMS prior authorization or complex fittings still favor offline distribution. Lower-acuity products benefit from the privacy and convenience of online ordering, especially in rural markets.

Geography Analysis

Demand in the United States personal mobility devices market varies regionally due to differences in age demographics, disability prevalence, reimbursement access, service density, and housing conditions. The South, led by Florida, Texas, Arizona, and the broader Sun Belt corridor, remains the highest-demand zone. A growing retiree population and aging demographics drive demand for scooters, wheelchairs, and accessories across reimbursed and self-pay channels. Warm climates and retirement migration further boost the need for outdoor mobility devices, keeping the South central to volume demand despite state-specific product preferences.

The Northeast presents a distinct profile, with dense hospital networks, rehabilitation centers, and urban care systems driving institutional demand for transport chairs, advanced rehabilitative power devices, and seating systems. Compact city environments have historically limited outdoor mobility use, but foldable and travel-safe powered devices now offer urban users improved transit compatibility and home storage flexibility.

Western states, including California and Washington, lead in adopting connected and smart mobility devices, supported by a tech-savvy senior population and proximity to innovation hubs. These markets favor premium manual frames, app-integrated controls, and lifestyle-oriented powered products, reflecting consumer willingness to invest in portability and design.

Competitive Landscape

The United States market for personal mobility devices is moderately consolidated in premium powered and complex rehabilitative categories, while manual wheelchairs, walking aids, transport chairs, and entry-level scooters remain fragmented. Permobil, Sunrise Medical, and Pride Mobility Products Corporation lead in higher-specification powered mobility and complex rehabilitation, where factors like reimbursement familiarity, clinical support, and brand trust are critical. Drive DeVilbiss Healthcare and Golden Technologies compete across scooters, transport chairs, and walking aids, enabling access to both institutional and consumer markets.

Strategic initiatives by key players highlight that product variety alone is insufficient. In February 2026, Permobil introduced the Comfort Unite back support line in the United States and Canada, integrating ROHO air technology and a simplified configuration to enhance its power mobility platforms. In April 2025, Sunrise Medical launched the Magic Mobility XT4, a 4x4 outdoor power wheelchair with advanced features like all-wheel suspension and 2,800W motor output, intensifying competition in the all-terrain segment.

Service quality, documentation, and fulfillment speed are now as vital as hardware for securing high-value accounts. CMS policy changes favor suppliers proficient in managing prior authorizations, while increased scrutiny on recalls and battery safety emphasizes engineering quality and compliance. E-commerce is transforming competition in lower-acuity segments, enabling smaller brands and broad-assortment sellers to reach household buyers without traditional branch networks.

U.S. Personal Mobility Devices Industry Leaders

Sunrise Medical LLC

Pride Mobility Products Corporation

Stryker Corporation

Drive DeVilbiss Healthcare

Medline Industries, LP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Sunrise Medical introduced the QUICKIE Q300 M Mini powered wheelchair with Dynamic Controls' LiNX controls alongside the PG Drives R-Net option, enhancing clinical flexibility and expanding its mid-range wheelchair market reach.

- March 2026: Sunrise Medical launched the JAY LitePro skin protection cushion, weighing under 2 lbs and under 2 inches in profile, targeting active users needing pressure management with minimal weight or height.

- March 2026: Permobil released the TiLite TR and TiLite ZR titanium wheelchairs with lighter components, redesigned features, and TiFit customization, reinforcing its premium position in the active manual wheelchair market.

- February 2026: Permobil introduced the Comfort Unite back support line in the US and Canada, consolidating product families and streamlining its seating portfolio with faster clinical setup options.

- April 2025: Sunrise Medical launched the Magic Mobility XT4, a 4x4 outdoor power wheelchair with all-wheel suspension and 2,800W output, addressing the needs of active users in outdoor environments.

U.S. Personal Mobility Devices Market Report Scope

As per the scope of the report, a Personal Mobility Device (PMD) is a compact, motorized or electric vehicle designed to transport a single person over short to medium distances. The term broadly covers two distinct categories: micromobility devices (like e-scooters) for general transit and assistive aids (like motorized wheelchairs) for individuals with disabilities.

The U.S. Personal Mobility Devices Market is segmented by product type, technology, end-user, and distribution channel. By product type, the market includes wheelchairs (manual wheelchairs, powered wheelchairs, robotic/autonomous wheelchairs), mobility scooters (3-wheel scooters, 4-wheel scooters, foldable and portable scooters), walking aids (canes & crutches, walkers & rollators, power-assist and positioning add-ons), and transfer and accessibility mobility devices. By technology, the market is segmented into manual devices, powered devices, power-assist and hybrid devices, and smart and connected devices. By end-user, the market is categorized into personal users and households, hospitals and clinics, rehabilitation centers, long-term care and assisted living facilities, and home healthcare and DME rental providers. By distribution channel, the market is segmented into offline and e-commerce. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Wheelchairs | Manual Wheelchairs |

| Powered Wheelchairs | |

| Robotic/Autonomous Wheelchairs | |

| Mobility Scooters | 3-Wheel Scooters |

| 4-Wheel Scooters | |

| Foldable and Portable Scooters | |

| Walking Aids | Canes & Crutches |

| Walkers & Rollators | |

| Power-Assist and Positioning Add-ons | |

| Transfer and Accessibility Mobility Devices |

| Manual Devices |

| Powered Devices |

| Power-Assist and Hybrid Devices |

| Smart and Connected Devices |

| Personal Users and Households |

| Hospitals and Clinics |

| Rehabilitation Centers |

| Long-Term Care and Assisted Living Facilities |

| Home Healthcare and DME Rental Providers |

| Offline |

| E-Commerce |

| By Product Type | Wheelchairs | Manual Wheelchairs |

| Powered Wheelchairs | ||

| Robotic/Autonomous Wheelchairs | ||

| Mobility Scooters | 3-Wheel Scooters | |

| 4-Wheel Scooters | ||

| Foldable and Portable Scooters | ||

| Walking Aids | Canes & Crutches | |

| Walkers & Rollators | ||

| Power-Assist and Positioning Add-ons | ||

| Transfer and Accessibility Mobility Devices | ||

| By Technology | Manual Devices | |

| Powered Devices | ||

| Power-Assist and Hybrid Devices | ||

| Smart and Connected Devices | ||

| By End User | Personal Users and Households | |

| Hospitals and Clinics | ||

| Rehabilitation Centers | ||

| Long-Term Care and Assisted Living Facilities | ||

| Home Healthcare and DME Rental Providers | ||

| By Distribution Channel | Offline | |

| E-Commerce | ||

Key Questions Answered in the Report

What is the 2026 value of the US personal mobility devices market?

The US personal mobility devices market stands at USD 4.02 billion in 2026 and is forecast to reach USD 5.47 billion by 2031 at a 6.37% CAGR.

Which product category leads demand in 2025?

Wheelchairs lead by product type with a 45.21% share in 2025, supported by strong clinical need and established reimbursement pathways.

Which sales channel is growing fastest through 2031?

E-commerce is the fastest-growing distribution channel with a 9.05% CAGR, driven by wider assortment and better access in underserved areas.

Why are home settings becoming more important for mobility device demand?

Personal users and households held 58.40% share in 2025, and home healthcare and DME rental providers are growing at an 8.10% CAGR as more care shifts into residential settings.

What is pushing powered devices to grow faster than manual products?

Powered devices are projected to grow at a 7.12% CAGR because aging users face lower self-propulsion capacity, reimbursement support has improved, and connected and lighter designs are expanding appeal.

What are the main risks for suppliers in this space?

High out-of-pocket costs can limit access to advanced devices, while recalls, lithium-ion battery safety concerns, and repair-service gaps can raise cost and slow adoption.

Page last updated on: