Radiology Positioning Aids Market Size and Share

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

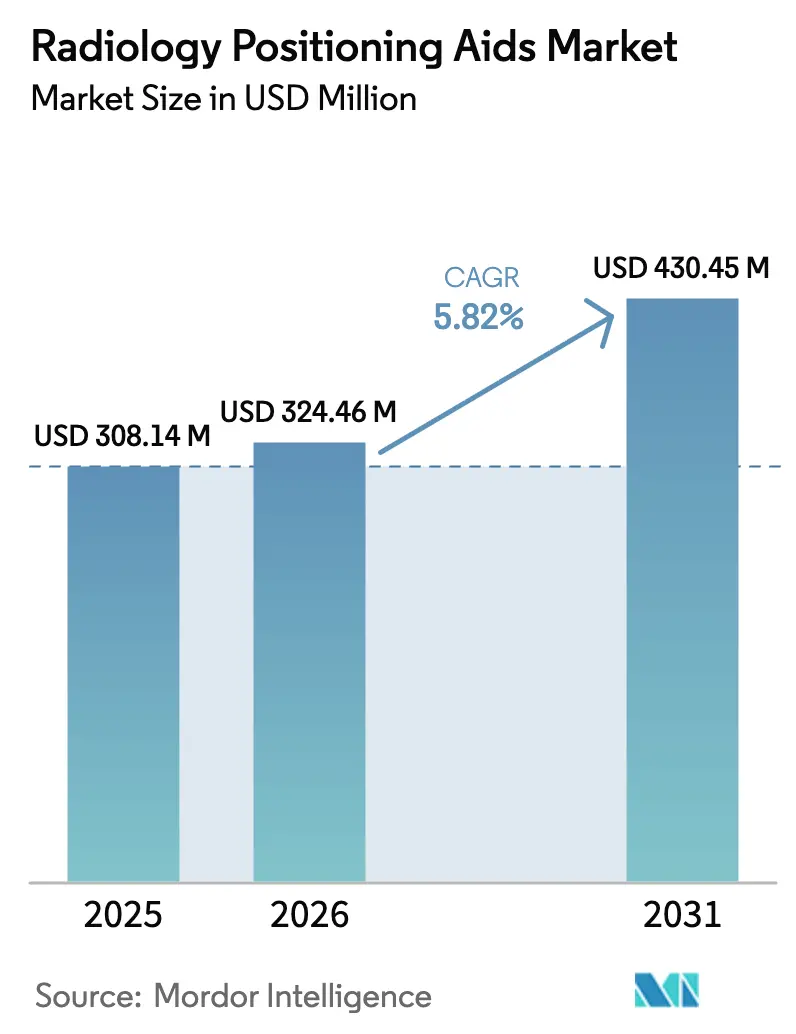

| Market Size (2026) | USD 324.46 Million |

| Market Size (2031) | USD 430.45 Million |

| Growth Rate (2026 - 2031) | 5.82% CAGR |

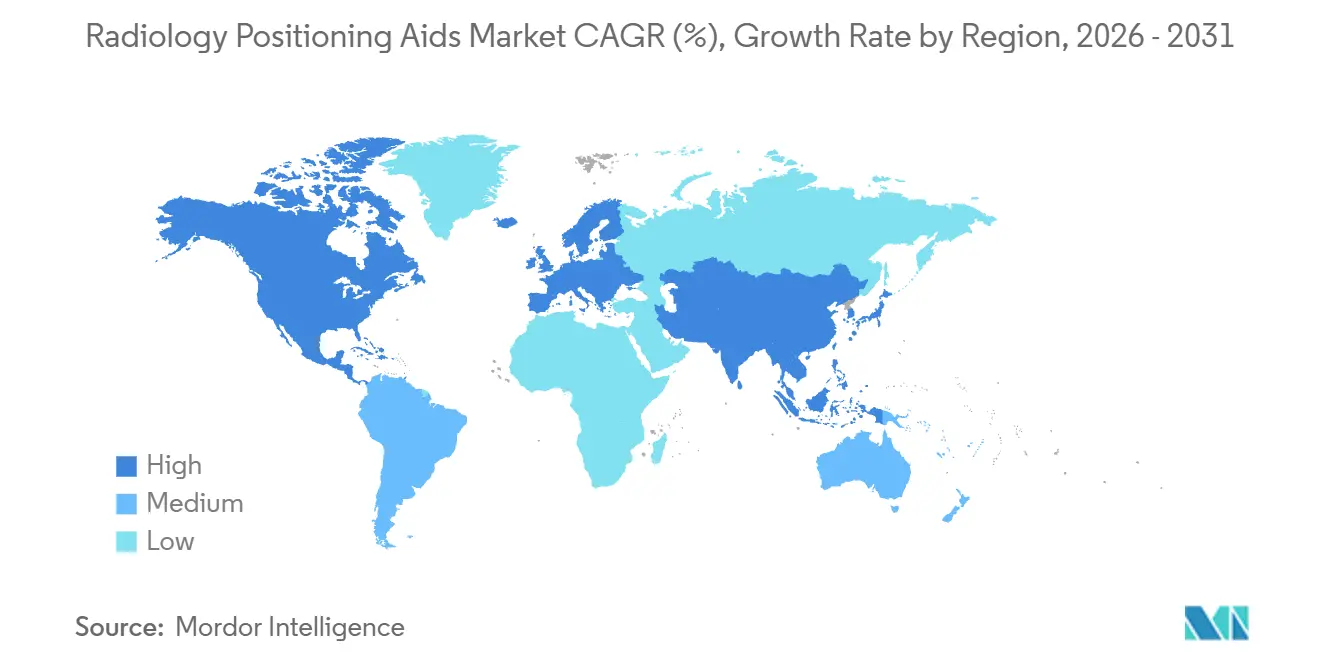

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Radiology Positioning Aids Market Analysis by Mordor Intelligence

Radiology Positioning Aids Market size in 2026 is estimated at USD 324.46 million, growing from 2025 value of USD 308.14 million with projections showing USD 430.45 million, growing at 5.82% CAGR over 2026-2031.

Hospitals, ambulatory surgical centers, and diagnostic imaging centers are accelerating capital spending on antimicrobial wedges, blocks, and pediatric immobilizers because first-pass image quality now drives reimbursement, while AI-enabled auto-positioning compresses scan times and lifts daily throughput. Vendors are embedding artificial intelligence and robotics directly into imaging tables, a shift that cuts repeat scans caused by misalignment, and antimicrobial surface treatments address infection-control mandates that grew in the post-pandemic era. North America remains the revenue leader, yet Asia-Pacific is the fastest-growing territory as governments fund portable X-ray programs that extend diagnostics into rural areas. Competitive intensity is rising as oncology device majors cross-sell diagnostic positioning portfolios, niche suppliers commercialize modular kits that integrate with planning software, and 3D-printing specialists offer patient-specific immobilizers at the point of care.

Key Report Takeaways

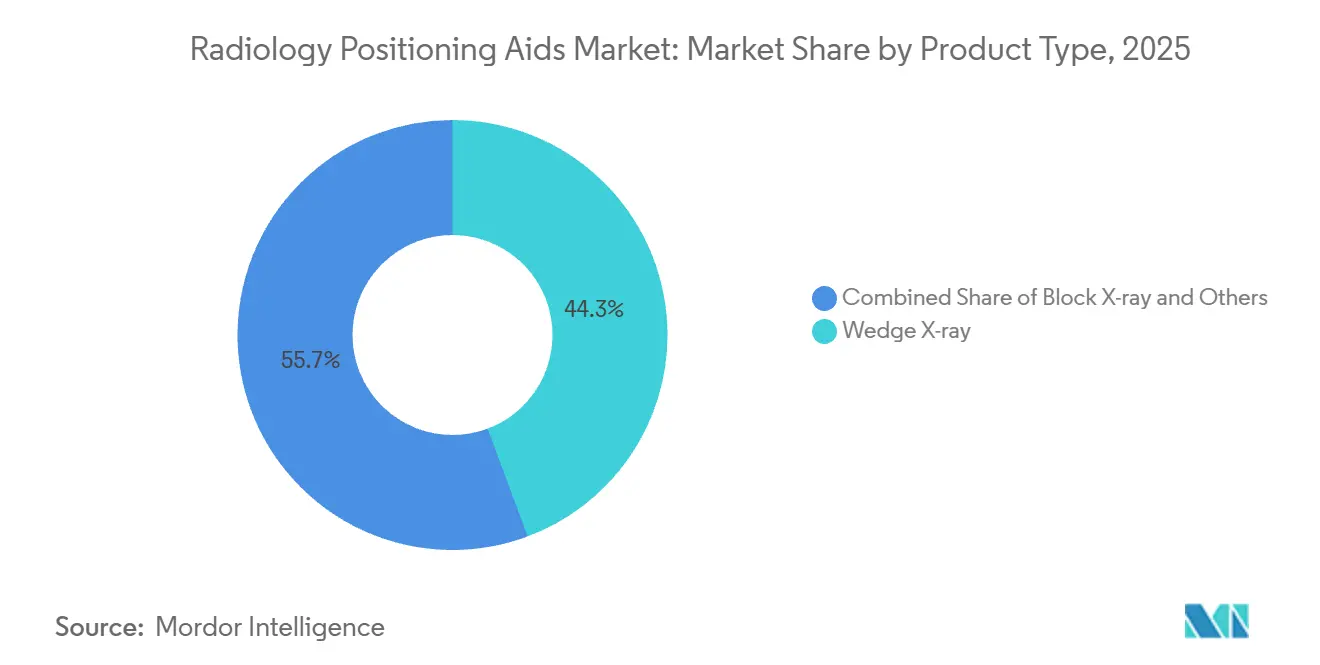

- By product type, wedge X-ray positioners led with 44.31% of the radiology positioning aids market share in 2025, and block X-ray devices are forecast to expand at a 6.15% CAGR through 2031, the fastest growth among product types.

- By product, head/neck/brain devices commanded 39.67% of the radiology positioning aids market size in 2025, while pediatric positioners are projected to grow at a 6.75% CAGR through 2031.

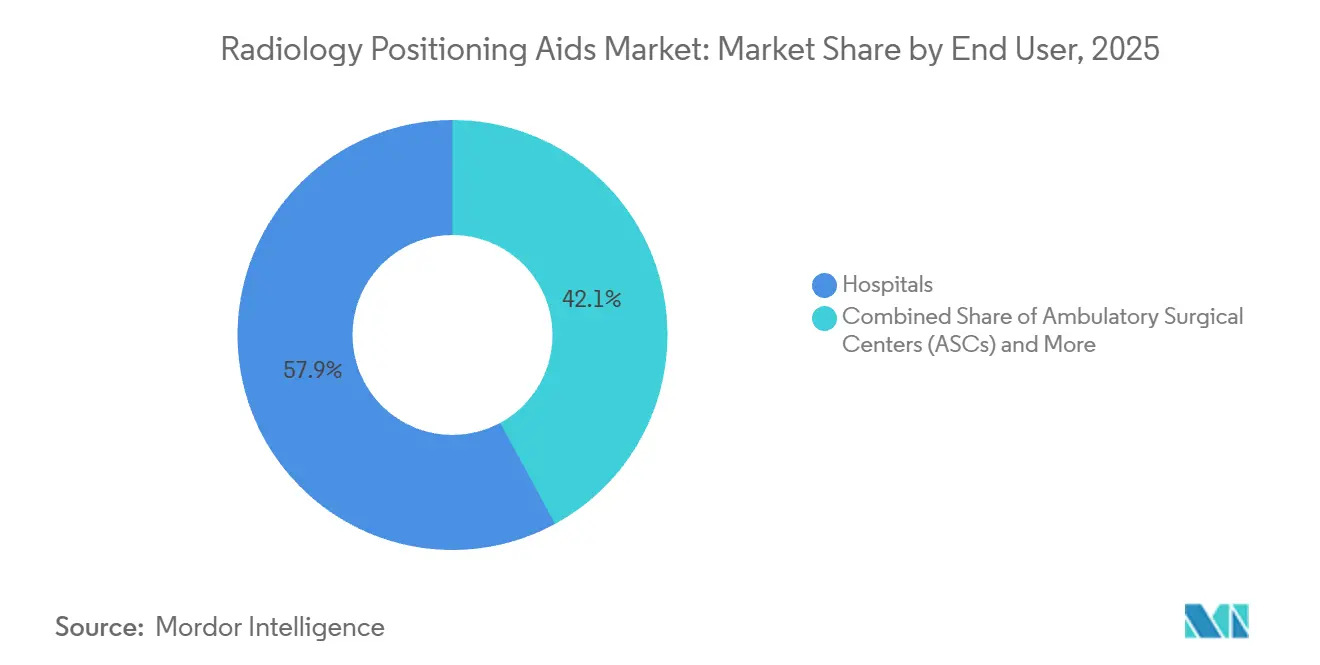

- By end user, hospitals accounted for 57.92% of 2025 spending; diagnostic imaging centers are advancing at an 8.40% CAGR through 2031.

- By geography, North America accounted for 38.03% of revenue in 2025; Asia-Pacific is expected to grow at an 8.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Radiology Positioning Aids Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological Advancements in Imaging Modalities | +1.2% | North America, Western Europe | Medium term (2-4 years) |

| Rising Diagnostic Imaging Volumes and Aging Population | +1.5% | Asia-Pacific, South America | Long term (≥ 4 years) |

| Intensified Focus on Patient Safety and Comfort | +0.9% | North America, European Union | Short term (≤ 2 years) |

| Availability of Disposable and Antimicrobial Aids | +0.8% | Global, premium uptake in GCC | Medium term (2-4 years) |

| AI-Enabled Robotic Auto-Positioning Adoption | +1.0% | North America, Western Europe, Japan, South Korea | Medium term (2-4 years) |

| Portable/Ultra-Portable X-Ray Programs in LMICs | +0.4% | APAC (India, Indonesia, Vietnam), Sub-Saharan Africa, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Technological Advancements in Imaging Modalities

Auto-positioning logic is now embedded in CT, MRI, and fluoroscopy consoles. Philips Precise Position uses ceiling cameras to check patient alignment before exposure and cuts repeat acquisitions by 12% across eight European networks. Siemens FAST 3D Camera lets technologists adjust table height and lateral offset on a touchscreen, trimming setup by 3 to 4 minutes per patient.[1]Siemens Healthineers, “FAST 3D Camera,” siemens-healthineers.com GE HealthCare’s Revolution Apex CT employs prior exams to replicate anatomical landmarks, a feature that supports longitudinal oncology follow-up. These capabilities curb demand for basic foam wedges in tertiary centers, yet they expand the overall radiology positioning aids market by documenting productivity gains that justify budget approvals. Software-defined upgrades also allow hospitals to retrofit legacy scanners, prolonging fleet life cycles while modernizing positioning performance.

Rising Diagnostic Imaging Volumes and Aging Population

Asia-Pacific scan volumes are climbing in tandem with demographic aging. Japan recorded a 29.1% share of the population aged 65-plus in 2024, which correlated with a 6.8% year-on-year jump in MRI and CT volumes. [2]World Health Organization, “Global Aging Data 2024,” who.int China reported 1.2 billion diagnostic procedures in 2025, a 9.3% rise, fueled by insurance expansion that funds screening for stroke, cardiovascular, and cancer. India earmarked USD 1.8 billion in 2025 for rural mobile X-ray units under Ayushman Bharat, with specifications that prioritize lightweight positioners. Higher imaging volumes strain existing inventory, prompting the adoption of disposable foam to eliminate sterilization delays. Older patients also face musculoskeletal fragility, so ergonomic wedges with pressure-relief surfaces now command premiums of 8-12% over commodity foam.

Intensified Focus on Patient Safety and Comfort

The FDA’s 2024 paediatric CT guidance underscores the importance of immobilization to avoid repeat scans that could triple cumulative radiation in children under five.[3]U.S. Food and Drug Administration, “Paediatric CT Guidance,” fda.gov Manufacturers launched adjustable kits with head cradles and torso straps that grow with the child, eliminating the need for multiple SKUs. The Joint Commission now requires documentation of positioning techniques, which drives demand for RFID-tagged aids that automatically log usage. Silver- or copper-infused antimicrobial wedges are entering baseline tenders because infection committees view them as low-cost insurance against healthcare-associated infections. Memory foam overlays and warming elements elevate patient satisfaction, a metric that directly impacts reimbursement in outpatient centres.

Availability of Disposable and Antimicrobial Aids

Single-use aids gained traction in ambulatory centres that lack reprocessing teams. Medline’s sterile foam wedges sell for USD 8-15 per unit and are intended for facilities handling up to 50 studies daily. ACR surveys showed 62% of U.S. imaging centres ranked infection risk among the top three purchase criteria in 2025, almost double the pre-pandemic figure. Technology such as AliMed Protecta-Coat embeds antimicrobial agents into polyurethane at the molecular level and already appears in 18% of new U.S. hospital construction specifications. Disposable demand also reflects supply-chain diversification after polyurethane shortages in 2023-24.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory and Certification Hurdles | -0.9% | North America, European Union | Medium term (2-4 years) |

| High Upfront Cost of Advanced Devices | -1.1% | Asia-Pacific, South America, Middle East and Africa | Short term (≤ 2 years) |

| Competition From Refurbished or Low-Cost Substitutes | -0.7% | North America, Europe | Medium term (2-4 years) |

| Limited Clinician Training and Workflow Integration | -0.5% | Global, acute in ambulatory settings | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory and Certification Hurdles

FDA 510(k) clearance takes 9.8 months on average and costs USD 75,000-150,000 per submission, expenses that weigh heavily on small producers. ISO 13485 quality mandates annual audits, while EU MDR demands clinical evaluation reports for antimicrobial claims, delaying 23% of planned launches in 2025. Powered tables must pass IEC 60601-1 testing, adding four-to-six months to timelines. These requirements curb innovation in niche pediatric and bariatric segments where volumes may not offset compliance costs.

High Upfront Cost of Advanced Devices

Robotic tables priced at USD 150,000-300,000 exceed annual equipment budgets for 70% of U.S. community hospitals. Import duties and currency swings inflate landed costs by up to 35% in emerging markets. Leasing models bundle hardware, maintenance, and upgrades for USD 3,000-5,000 monthly, but adoption remains limited to centralized health systems. Secondary markets offer refurbished wedges and blocks at 30-50% discounts, yet unknown maintenance histories increase total-cost-of-ownership risks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wedge Dominance Meets Block Growth

Wedge X-ray devices accounted for 44.31% of the radiology positioning aids market in 2025, reflecting their universal use in CT, MRI, and fluoroscopy workflows, where quick angle adjustment matters. Blocks are projected to expand at a 6.15% CAGR through 2031, as interventional vascular and orthopaedic procedures demand rigid immobilization to eliminate motion during real-time image guidance. Wedges benefit from low unit costs of USD 15-40 and compatibility with legacy scanners. Blocks, priced USD 50-120, justify their premium through carbon-fibre or polystyrene cores that minimize X-ray attenuation.

Manufacturers enhance wedges with antimicrobial coatings and color-coded sizes to curb setup errors. Pearl Technology ProFoam demonstrated a 99.9% bacterial kill rate, winning multihospital contracts. Block makers shift toward modular designs that stack for bariatric patients and comply with ISO 80601-2-43 radiolucency standards. This versatility drives uptake in academic surgery suites, where case mix demands rapid configuration changes.

By Product: Neuro Imaging Anchors, Pediatrics Accelerates

Head/neck/brain devices accounted for 39.67% of the radiology positioning aids market share in 2025, as neuroimaging accounted for 28% of all U.S. CT and MRI exams that year. Pediatric positioners are projected to grow at a 6.75% CAGR as children’s hospitals adopt age-specific immobilization to avoid sedation and reduce radiation exposure. Thorax and breast aids target mammography and radiation therapy; demand tracks screening programs that reach 60-70% participation in North America but lag in Asia-Pacific.

Pediatric acceleration follows FDA emphasis on immobilization over anesthesia, prompting suppliers to offer adjustable cradles and cartoon themes that slash sedation by 18% in pilot studies. Head and neck devices now incorporate 3D-printed shells that conform to skull anatomy, achieving sub-millimeter reproducibility favored in radiation therapy. Breast positioners evolve toward dual-modality supports for diagnostics and prone biopsy, consolidating equipment investments in ambulatory breast centers.

By End User: Hospitals Lead, Imaging Centers Surge

Hospitals contributed 57.92% of 2025 revenues, leveraging scale to secure bundled deals that include service contracts and consignment inventory. Diagnostic imaging centres will grow at an 8.40% CAGR through 2031, propelled by outpatient migration and pay-for-performance metrics that penalize repeat scans. Ambulatory surgical centres adopt aids selectively for interventional pain and orthopaedic cases where immobilization governs outcomes.

Hospitals extend replacement cycles yet invest in premium antimicrobial foams when infection committees flag surface decontamination risks. Imaging centre chains, such as RadNet, standardized antimicrobial wedges across 350 facilities in 2025, prompting independents to follow suit. Ambulatory centres still grapple with training gaps that slow the uptake of AI-enabled tables. Across all segments, ISO 13485 certification is a non-negotiable tender requirement.

Geography Analysis

North America accounted for 38.03% of 2025 revenue, driven by replacement demand as hospitals migrate to wide-bore CT and MRI systems that require compatible tables. Widespread infection-control mandates mean antimicrobial wedges win 62% of U.S. tenders. Reimbursement structures reward first-pass image quality, so facilities invest in AI-enabled positioning to compress setup time.

Asia-Pacific is projected to expand at an 8.91% CAGR through 2031 as China, India, and Southeast Asia build diagnostic infrastructure. China allocated USD 2.1 billion in 2025 for county-hospital upgrades, bundling positioners with scanners. India made imaging a covered benefit under Ayushman Bharat in 2024, fuelling a 22% jump in equipment tenders that include wedges and paediatric kits. Japan’s aging population drives demand for ergonomic foams that prevent skin breakdown during long scans.

Europe faces mixed dynamics. Austerity in parts of Southern Europe delays purchases, yet Germany, the UK, and Scandinavia specify antimicrobial coatings and RFID tracking. EU MDR slows product launches, consolidating the supplier base toward firms that can absorb regulatory overhead. The Middle East and Africa see growth driven by GCC construction booms and donor-funded portable X-ray programs in Sub-Saharan Africa. At the same time, South America faces tariffs that raise equipment costs.

Competitive Landscape

The top five suppliers, Elekta, Varian, CIVICO, Qfix, and Klarity, control an estimated significant share of the radiology positioning aids market, indicating moderate fragmentation. Technology differentiation revolves around AI-enabled auto-positioning, antimicrobial polymers, and integration into oncology treatment workflows. Elekta and Varian cross-sell diagnostic kits into their linear-accelerator installed base, cementing customer loyalty yet drawing antitrust attention in concentrated hospital districts.

Regional specialists capture contracts through flexible consignment models. Qfix offers modular kits that integrate with treatment-planning software, while Klarity pushes patient-specific immobilizers that 3D-print onsite. Patent activity in 2025 highlighted pressure-sensor-embedded foams and RFID-tagged wedges that auto-document technique for Joint Commission compliance. Cost and regulatory hurdles keep small entrants at bay, but innovation in lightweight, rugged wedges for LMIC portable programs opens white-space opportunity.

Technological bifurcation persists. Academic centres spend USD 150,000-300,000 on robotic tables, whereas community hospitals and surgical centres purchase USD 15-120 foam units. This split yields dual value chains with minimal overlap. Market entrants that master both low-cost foam and high-end robotics may bridge the gap and grow share across segments.

Radiology Positioning Aids Industry Leaders

Qfix Medical India Private Limited

Medline Industries, LP.

AliMed Inc.

CDR Systems Inc.

David Scott Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Fujifilm India launched four diagnostic imaging and IT solutions at IRIA 2026 to expand workflow-centric offerings across Indian hospitals.

- March 2025: GE HealthCare and NVIDIA expanded collaboration to pioneer autonomous X-ray and ultrasound applications.

- February 2024: Varian, a Siemens Healthineers company, introduced the TrueBeam Edge system with AI-based alignment, reducing setup time by 18%, and it is now adapted for diagnostic CT in hybrid ORs.

Global Radiology Positioning Aids Market Report Scope

The Radiology Positioning Aids Market encompasses products and technologies that assist healthcare providers in correctly positioning patients for radiological examinations. These aids include foam immobilizers, wedges, blocks, thermoplastic masks, straps, cushions, and laser-guided alignment systems. Their primary role is to stabilize patients, reduce movement, and ensure precise anatomical alignment, which is essential for accurate imaging and effective treatment planning.

The Radiology Positioning Aids Market Report is Segmented by Product Type (Wedge X-ray, Block X-ray, Others), Product (Head/Neck/Brain Devices, Thorax & Breast Devices, Tables & Couch Tops, Paediatric Positioners, Others), End User (Hospitals, Ambulatory Surgical Centers, Diagnostic Imaging Centers), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

| Wedge X-ray |

| Block X-ray |

| Others (Foam, Cushions, Immobilizers) |

| Head / Neck / Brain Devices |

| Thorax & Breast Devices |

| Tables & Couch Tops |

| Pediatric Positioners |

| Others |

| Hospitals |

| Ambulatory Surgical Centers (ASCs) |

| Diagnostic Imaging Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Wedge X-ray | |

| Block X-ray | ||

| Others (Foam, Cushions, Immobilizers) | ||

| By Product | Head / Neck / Brain Devices | |

| Thorax & Breast Devices | ||

| Tables & Couch Tops | ||

| Pediatric Positioners | ||

| Others | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers (ASCs) | ||

| Diagnostic Imaging Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the radiology positioning aids market in 2031?

The radiology positioning aids market size is forecast to reach USD 430.45 million by 2031.

Which product type currently holds the largest share?

Wedge X-ray positioners led with 44.31% market share in 2025.

Why is Asia-Pacific considered the fastest-growing region?

Government-funded diagnostic programs in China, India, and Southeast Asia drive an 8.91% CAGR through 2031.

How do AI-enabled robotic tables improve imaging efficiency?

They reduce patient setup time by 15-20%, enabling facilities to complete 8-10 additional scans daily.

What regulatory hurdles affect new entrants?

FDA 510(k), ISO 13485, and EU MDR impose testing, audits, and clinical reporting that add cost and delay.

Page last updated on: