Global Self Care Medical Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

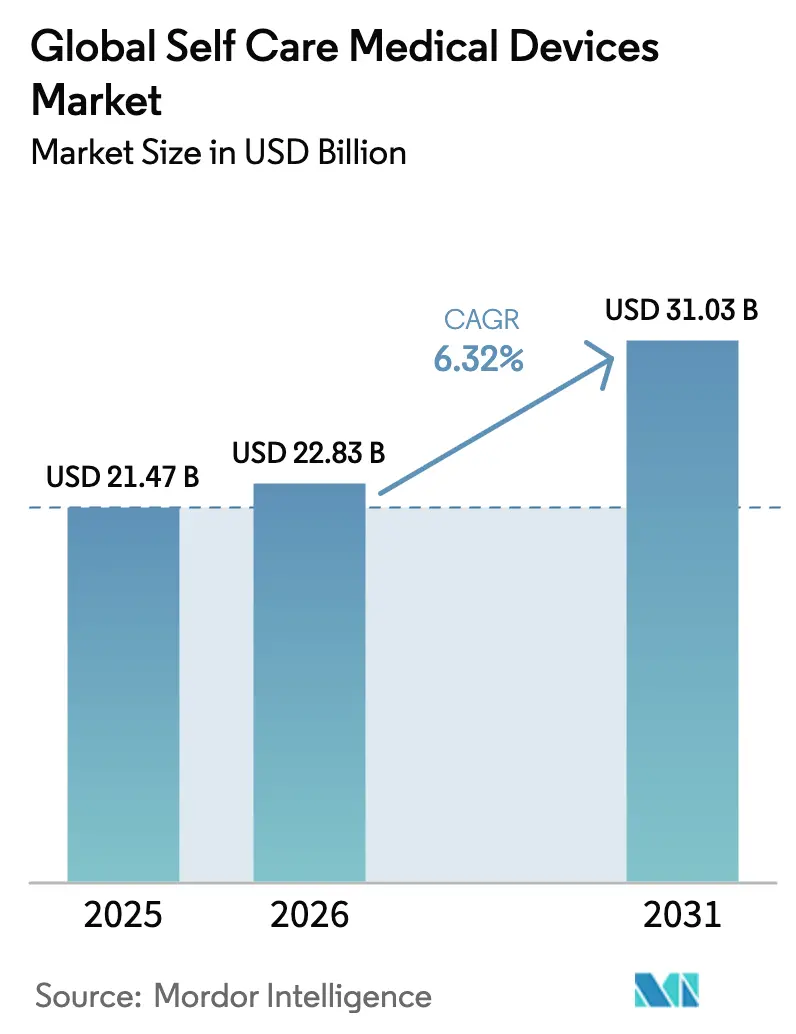

| Market Size (2026) | USD 22.83 Billion |

| Market Size (2031) | USD 31.03 Billion |

| Growth Rate (2026 - 2031) | 6.32% CAGR |

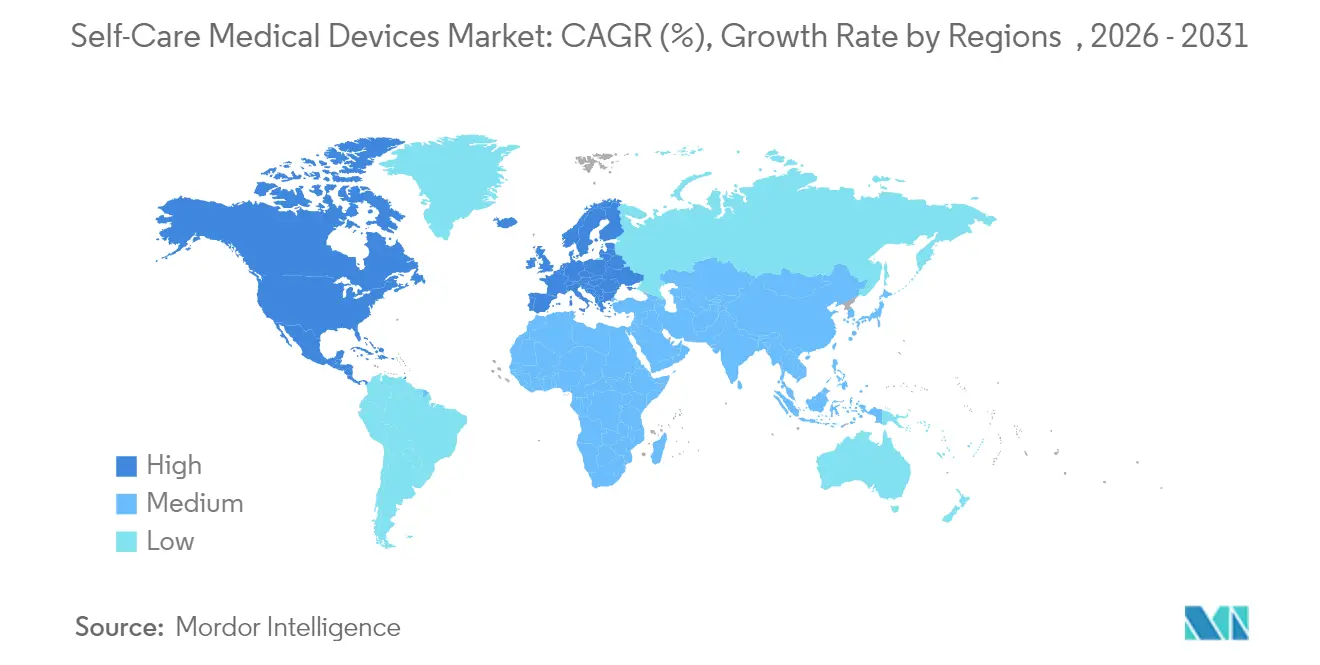

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

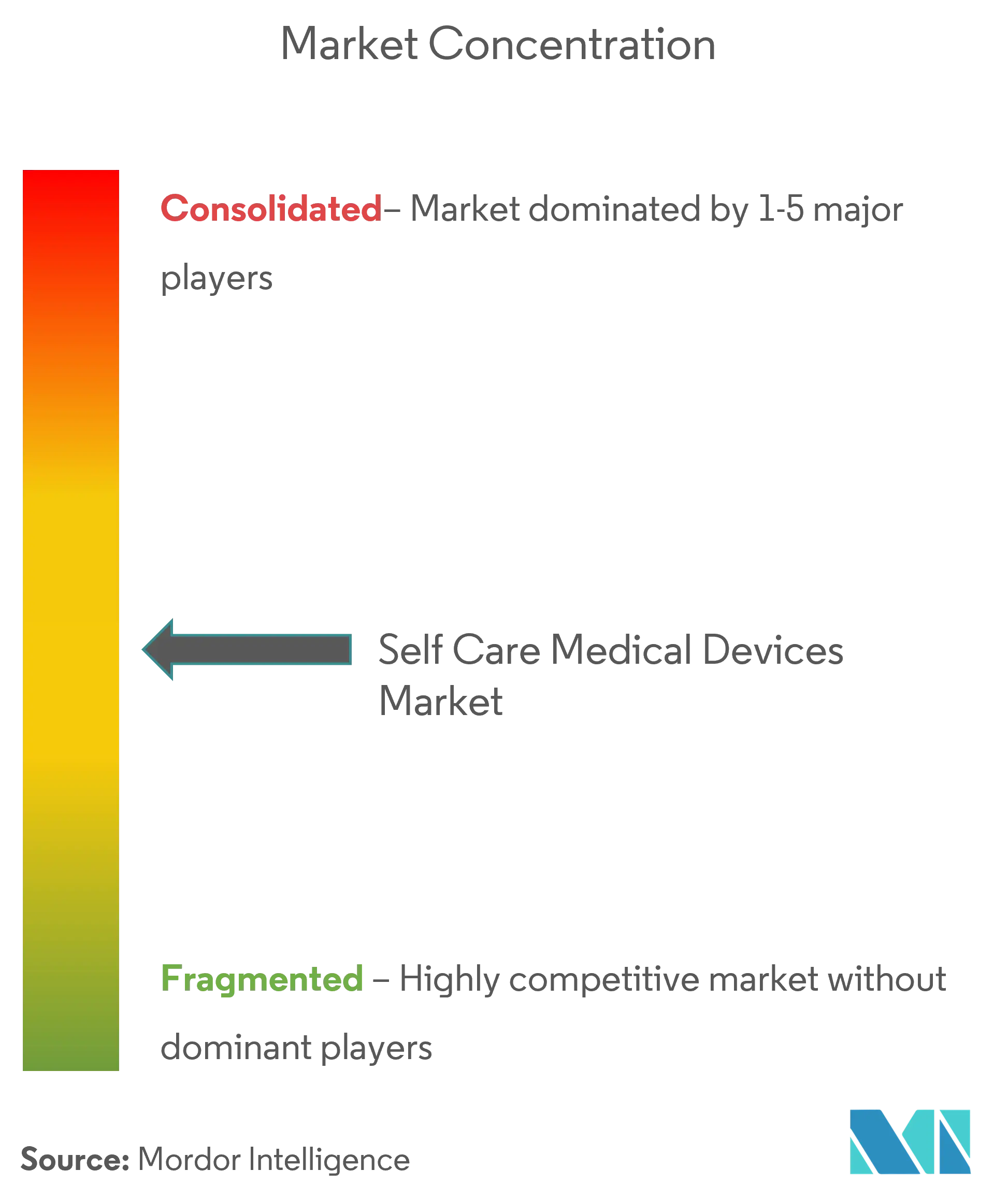

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Self Care Medical Devices Market Analysis by Mordor Intelligence

The self care medical devices market size is expected to grow from USD 21.47 billion in 2025 to USD 22.83 billion in 2026 and is forecast to reach USD 31.03 billion by 2031 at 6.32% CAGR over 2026-2031. Rising chronic-disease prevalence, rapid device miniaturization, and supportive reimbursement reforms are converging to keep demand steady. Diabetes management remains the dominant clinical application, accounting for 42.54% of 2024 revenue, while smart wearable patches post the fastest device-level expansion at 8.23% CAGR on the back of microneedle and sensor breakthroughs. Regulatory alignment is visible in the United States, where the FDA cleared the first over-the-counter continuous glucose monitor and embraced “Home as a Health Care Hub,” sending strong market-validation signals. Remote patient-monitoring incentives introduced by the Centers for Medicare & Medicaid Services in the 2025 Physician Fee Schedule further reinforce connected-device uptake, pushing IoT penetration from a 38.05% revenue base toward higher single-digit growth.

Key Report Takeaways

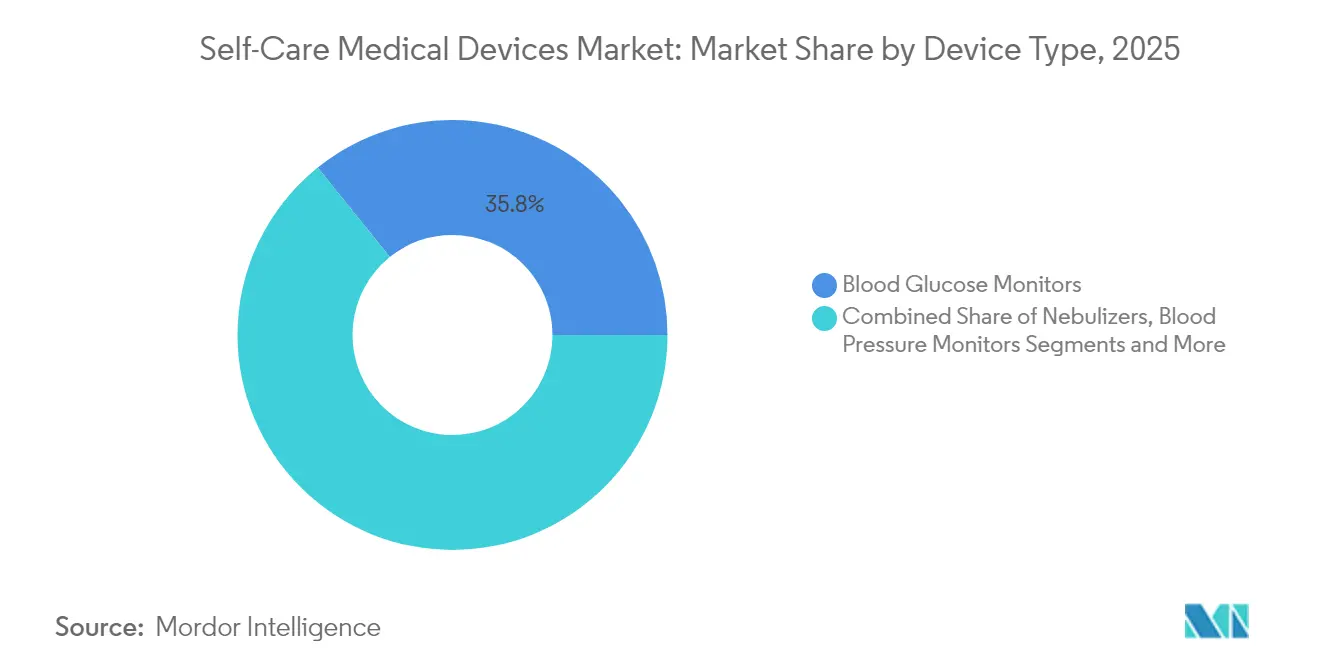

- By device type, blood glucose monitors led with 35.78% of the self care medical devices market share in 2025, while smart wearable patches are on track for a 7.78% CAGR to 2031.

- By application, diabetes management captured 41.92% of the self care medical devices market share in 2025; women’s health devices are forecast to expand at a 6.87% CAGR through 2031.

- By connectivity, non-connected products held 61.35% of 2025 revenue; IoT-enabled devices are advancing at a 7.12% CAGR on the strength of new Medicare RPM codes.

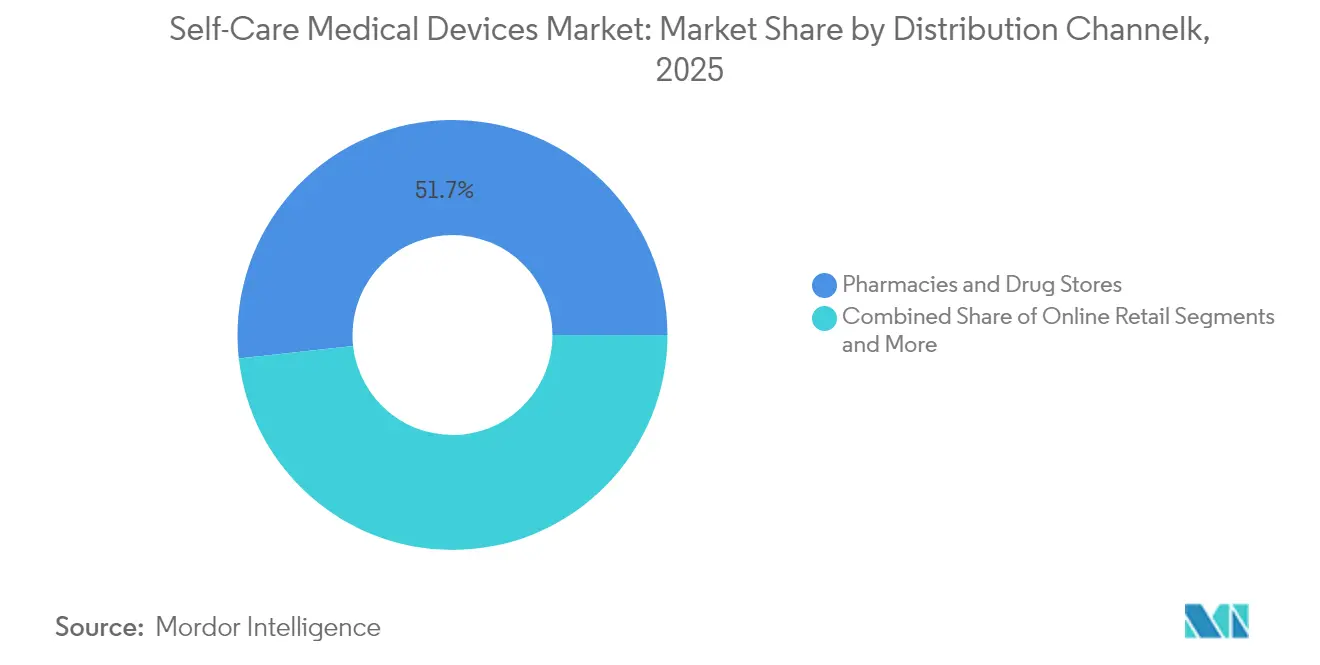

- By distribution channel, pharmacies and drug stores controlled 51.74% of 2025 revenue, yet online channels exhibit the quickest climb at 7.45% CAGR through 2031.

- By end-user, home-care users accounted for 56.11% of 2025 revenue, whereas long-term care facilities are poised for a 7.19% CAGR thanks to predictive-analytics rollouts.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Self Care Medical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic-disease & geriatric burden | +1.8% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Home-based care preference | +1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Device miniaturization & wireless tech | +1.5% | Global, led by technology hubs in US, EU, Asia | Medium term (2-4 years) |

| Healthcare-cost pressure on payers & patients | +0.9% | Global, acute in US healthcare system | Short term (≤ 2 years) |

| AI-driven personalized self-monitoring | +0.8% | North America & EU early adoption, APAC following | Long term (≥ 4 years) |

| Reimbursement-linked remote monitoring codes | +0.6% | Primarily North America, expanding to EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic-Disease & Geriatric Burden

Population aging and the rising incidence of long-term conditions are steering care from episodic interventions to continuous, home-based monitoring. More than 11 million insulin-dependent individuals worldwide depend on automated glucose monitors that cut clinic visits while safeguarding glycemic control [1]Abbott, “Assert-IQ Insertable Cardiac Monitor Gains FDA Clearance,” abbott.com. Similar momentum is unfolding in cardiology, where battery-efficient implantable monitors such as Abbott’s Assert-IQ deliver six-year rhythm surveillance and improve early detection of arrhythmia. Payers value these tools because they avert emergency admissions, a dynamic that keeps the self care medical devices market on a widening trajectory.

Home-Based Care Preference

Public-health emergencies accelerated comfort with tele-monitoring, but the behavior has become entrenched. The FDA formally acknowledged domestic settings as integral to care delivery via its “Home as a Health Care Hub” framework in 2024, encouraging manufacturers to tailor usability, infection-control features, and training materials for laypersons. CMS now requires remotely monitored devices to transmit at least 16 data points every 30 days, effectively setting a performance floor that propels technology refinement. Women’s health illustrates the trend: at-home hormone-monitoring pads validated by the agency allow discreet, routine testing and broaden engagement for underserved groups.

Device Miniaturization & Wireless Tech

Advances in materials and chip design continue to shrink form factors without compromising clinical fidelity. Research from the University of Washington introduced earring-sized thermometers able to log body temperature continuously while remaining unobtrusive. Self-healing electronic skin created by the Terasaki Institute restores 80% conductivity within seconds, addressing durability concerns in high-motion environments [2]Terasaki Institute for Biomedical Innovation, “Self-Healing Electronic Skin Survives Wear and Tear,” terasaki.org. Wearable ultrasound patches highlighted in Nature extend non-invasive imaging to ambulatory settings. Edge AI chips embedded in these wearables lower latency for real-time alerts and ease privacy worries by processing biometrics locally.

Healthcare-Cost Pressure on Payers & Patients

Inflation in medical spending is sparking broad adoption of technology that safely shifts monitoring away from high-cost sites. Analyses by the Center for Telehealth & e-Health Law show remote monitoring can cut episode-of-care costs by 30%, savings that appeal to insurers and self-insured employers. CMS’s 2025 Physician Fee Schedule adds Advanced Primary Care Management codes paying up to USD 107.07 monthly for complex patients, reinforcing provider ROI on device deployment. The FDA simultaneously eased Class II thermometer premarket requirements, trimming regulatory overhead and stimulating price competition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device cost & cheaper alternatives | -0.7% | Global, particularly price-sensitive emerging markets | Medium term (2-4 years) |

| Adverse events from implantables | -0.4% | Global, with heightened scrutiny in EU & US | Long term (≥ 4 years) |

| Data-privacy adoption barriers | -0.5% | EU (GDPR), US (state-level), expanding globally | Long term (≥ 4 years) |

| Chip-supply volatility & price spikes | -0.6% | Global, acute impact in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Device Cost & Cheaper Alternatives

Premium connected devices often carry multi-year ownership costs that exceed budgets in low- to middle-income economies, hampering penetration. Semiconductor tariffs under discussion in several major jurisdictions threaten additional price rises given that more than half of medical devices require advanced chips, potentially lifting component costs across production lines. Manufacturers are countering with tiered portfolios that strip non-essential features for emerging markets, though the approach risks narrowing margins.

Data-Privacy Adoption Barriers

Europe’s forthcoming Health Data Space imposes rigorous technical and consent obligations on all connected devices that handle identifiable data, potentially extending time-to-market and certification expense. In the United States, HIPAA does not shield data from consumer wearables, leaving devices in a patchwork of state rules that 82% of residents describe as confusing. Recent enforcement action, including an FTC fine of USD 7.8 million levied on a mental-health app, signals growing financial and reputational exposure for non-compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Glucose Monitors Lead, Smart Patches Surge

The segment for blood-glucose monitors generated 35.78% of 2025 revenue, making it the cornerstone of the self care medical devices market. Reimbursement stability and clinical guidelines requiring continuous glucose data sustain predictable demand. At the same time, microneedle-based smart patches are forecast to rise 7.78% annually as they move beyond sensing to on-demand drug delivery, evidenced by an FDA-cleared smartphone-controlled patch able to dispense multiple medications. Blood-pressure monitors show mid-single-digit growth driven by hypertension screening programs, whereas wearable temperature sensors gain relevance in pediatric remote-fever management.

Proliferating respiratory solutions such as the FDA-cleared SIMEOX 200 airway clearance system leverage pulse-pressure wave technology to assist mucus evacuation in chronic obstructive pulmonary disease cohorts. Commodity pedometers and fitness trackers face value erosion, but advanced models integrating ECG and oxygen saturation data retain pricing power through clinical validation. Fertility and pregnancy kits now employ quantitative hormone analytics rather than colorimetric strips, appealing to women seeking data-rich insights. Emerging acoustic-therapy devices targeting nasal congestion and sleep apnea broaden non-pharmaceutical respiratory care, illustrating continuous product-pipeline diversification across the self care medical devices market.

By Application: Diabetes Dominance, Women’s Health Acceleration

Applications linked to diabetes management captured 41.92% of 2025 revenue and anchor recurring consumable demand for sensors and infusion sets. Insulin dosing algorithms embedded in closed-loop systems reduce hypoglycemia risk and create ecosystem stickiness, enlarging the self care medical devices market size for diabetes by 6% through value-added software subscriptions. Women’s health constitutes the most dynamic frontier, expanding at a projected 6.87% CAGR as regulatory agencies green-light home tests for sexually transmitted infections and hormone panels that previously required clinic visits. Cardiovascular monitoring benefits from the roll-out of extended-life implantables and AI arrhythmia detection that improves post-discharge outcomes.

Respiratory-care use cases are shifting from episodic nebulization to smart inhalers equipped with flow sensors that guide technique and adherence. Integrated wellness platforms converge multiple biomarkers—glucose, blood pressure, heart rate variability—into one dashboard, cutting the number of individual devices a consumer needs. Predictive-analytics engines embedded within applications convert historical biometrics into individualized risk scores, positioning the self care medical devices industry for a future where preventive alerts precede symptom onset.

By Connectivity: Non-Connected Leads, IoT Devices Accelerate

Non-connected products still account for 61.35% of 2025 revenue because they offer reliable readings at lower prices and avoid cybersecurity complexity. Nevertheless, connected wearables and sensors are advancing at a 7.12% CAGR, catalyzed by reimbursement requirements demanding data transmission at least 16 times per month. Edge-AI chips installed in next-generation devices shrink latency and preserve privacy by processing signals on-device, an advantage for providers wary of cloud vulnerabilities. Bluetooth Low Energy and Zigbee upgrades are extending battery life beyond one week between charges, reducing friction in daily use.

Emergent energy-harvesting techniques capture body heat or kinetic energy to power low-draw sensors, foreshadowing battery-less devices that further expand the self care medical devices market. Adoption of 5G allows wider spectral bandwidth, facilitating real-time video dermatology consultations and continuous ultrasound streams. The FDA’s draft cybersecurity guidance articulates lifecycle responsibilities for vulnerability disclosure and patch management, compelling manufacturers to bake security updates into product roadmaps.

By Distribution Channel: Pharmacies Dominate, Online Growth Accelerates

Pharmacies & Drug Stores captured 51.74% of 2025 revenue, benefiting from pharmacist counseling and trusted brand equity. They also serve as rapid-logistics nodes for consumables such as glucose-sensor applicators, a high-frequency replenishment category within the self care medical devices market size. Online channels, however, grow fastest at 7.45% CAGR as consumers embrace doorstep delivery and price-comparison engines. Digital pharmacy sales are projected to eclipse USD 95.75 billion by 2030, pressuring traditional outlets to launch e-commerce storefronts.

Hospital outpatient clinics maintain relevance for sophisticated fittings—such as titrating continuous positive airway pressure masks—yet their share erodes where telehealth enablement is strong. Mass merchandisers broaden assortments beyond fitness trackers to FDA-cleared blood-pressure cuffs as health monitoring integrates with everyday retail. Subscription bundles offering monthly sensor refills and companion-app analytics create sticky revenue for vendors operating direct-to-consumer models.

By End-User: Home-Care Users Lead, Long-Term Care Facilities Expand

Home-care users generated 56.11% of 2025 revenue, illustrating the gravitational pull toward self-directed management of chronic conditions. Continuous monitoring aligns with consumer expectations for on-demand insight and independence, solidifying the self care medical devices market as a core component of household health budgets. Long-term care facilities post a 7.19% CAGR outlook as sensor networks integrated into wearables and mattresses predict falls or dehydration hours in advance, reducing nurse call-outs and hospitalization.

Ambulatory surgery centers adopt self-care devices to track vitals during recovery at home, cutting readmissions and aligning with bundled-payment models. Elder-specific wearables add large-format screens, audible alerts, and one-button emergency calls, enhancing usability. Companion robots equipped with vitals sensors support cognitive engagement and remote monitoring, adding a social layer to device ecosystems. Policymakers in multiple jurisdictions are crafting standards to govern sensor deployment in communal living settings, balancing autonomy with privacy.

Geography Analysis

North America secured 42.19% of 2025 self care medical devices market revenue by combining robust reimbursement, tech-sector innovation, and supportive regulation. Updated CMS codes for Advanced Primary Care Management reimburse device-generated data reviews, improving financial justification for remote-monitoring dashboards. The FDA’s harmonization of Quality System Regulation with ISO 13485 expedites dual market access and lowers redundant auditing costs. Venture investment channeled into Silicon Valley and Boston med-tech clusters fuels sensor miniaturization, clinical-grade firmware, and edge-processing breakthroughs. Potential semiconductor tariffs loom as a cost headwind, yet strategic on-shoring of chip fabrication is underway to secure supply.

Asia-Pacific is the fastest-growing region, tracking an 8.31% CAGR through 2031. Governments are enlarging public-insurance coverage for digital-health tools, and local manufacturing scale keeps price points attractive. China’s updated medical-device law enhances transparency on post-market surveillance and label requirements, simplifying pathways for foreign entrants. Japan, valued at USD 40 billion, leans on self-monitoring as part of its Healthy Life Extension vision, with large payers subsidizing continuous glucose monitors for older adults . Australia’s adoption of mutual-recognition schemes for CE-marked devices trims review cycles, further boosting regional competitiveness.

Europe delivers steady mid-single-digit expansion underpinned by aging populations and universal-coverage systems willing to reimburse evidence-based wearables. The European Health Data Space proposal, expected to enter force during 2026, will standardize health-data interoperability while mandating high encryption standards that favor companies with strong security credentials. Sustainability requirements drive interest in biodegradable sensor substrates such as nanocellulose ECG patches developed with Finnish research funding. Meanwhile, emergent Gulf and Latin American markets broaden addressable demand as infrastructure investment and regulatory overhauls attract multinationals looking for growth adjacencies.

Competitive Landscape

The self care medical devices market features moderate concentration, with top brands blending hardware portfolios with software ecosystems. Abbott deepened its alliance with Medtronic in 2024 to integrate glucose-sensor streams into automated insulin-delivery pumps, anchoring a closed-loop diabetes platform. Philips leverages its HealthSuite Cloud to unify data across sleep, cardiac, and respiratory devices, positioning itself as an end-to-end remote-care orchestrator. Technology conglomerates—most visibly Apple and Samsung—advance consumer-grade wearables with FDA-cleared ECG functions, escalating rivalry at the wellness-medical border.

Acquisition momentum remains strong. Stryker’s USD 4.9 billion purchase of Inari Medical opened a peripheral-vascular foothold and diversified beyond orthopedics. Investors channel funds into specialists such as Level Zero Health, which raised USD 6.9 million for hormone-tracking biosensors focused on female physiology, signaling confidence in vertical-niche strategies. Edge computing and embedded-AI stacks represent key differentiation levers; companies offering on-device analytics reduce latency and compliance risks, resonating with providers wary of cloud dependence.

Supply-chain resilience is a new competitive metric. Manufacturers restructure toward dual-sourcing of chips and relocate final assembly closer to demand centers to mitigate logistics shocks and geopolitical restrictions. Firms that secure preferential wafer allocations from foundries can shield margins when global chip shortages reemerge, translating procurement strength into market-share preservation within the self care medical devices market.

Global Self Care Medical Devices Industry Leaders

Medtronic plc.

Koninklijke Philips N.V.

ResMed, Inc.

Roche Pharmaceutical

GE Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Mankind Pharma launched RAPID NEWS self-test kits addressing dengue, urinary-tract infections, and early menopause in India.

- March 2024: The FDA cleared Dexcom’s Stelo over-the-counter continuous glucose monitor for adults not using insulin.

- January 2024: OraSure Technologies led Series B funding and signed distribution pacts with Sapphiros to broaden consumer diagnostic access.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the self-care medical devices market as all patient-operated equipment used outside clinical supervision to measure or manage vital signs, chronic-condition markers, and simple respiratory therapies. Devices covered include blood glucose meters, arm-cuff and wrist blood-pressure monitors, smart thermometers, handheld nebulizers, pedometers, and connected wearable patches that relay data to companion apps.

Scope exclusion: Large stationary clinical analyzers, implantable pumps, and non-health wellness gadgets are not part of this assessment.

Segmentation Overview

- By Device Type

- Blood Glucose Monitors

- Blood Pressure Monitors

- Body Temperature Monitors

- Nebulizers

- Pedometers & Activity Trackers

- Pregnancy/Fertility Test Kits

- Smart Wearable Patches

- Others

- By Application

- Diabetes Management

- Cardiovascular Health

- Respiratory Care

- Women’s Health & Fertility

- Fitness & Wellness

- By Connectivity

- Connected / IoT-enabled Devices

- Non-connected Devices

- By Distribution Channel

- Pharmacies & Drug Stores

- Online Retail

- Hospital Outpatient & Clinics

- Mass-merchandisers & Others

- By End-user

- Home-care Users

- Ambulatory Care Centres

- Long-term Care Facilities

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Analysts interviewed device engineers, home-health nurses, and pharmacy buyers across North America, Europe, and Asia-Pacific. These discussions refined penetration rates for connected wearables, validated online-channel mark-ups, and highlighted reimbursement triggers that desk sources lacked.

Desk Research

We began with public datasets from bodies such as the International Diabetes Federation, WHO, and the United Nations Population Division, which clarified disease prevalence, aging trends, and home-care adoption. Trade statistics from UN Comtrade and customs portals helped size global flows of glucometers and nebulizers, while regulatory portals (FDA 510(k), EU MDR) indicated annual product clearances. Company filings and investor decks provided average selling prices and shipment volumes to be paired with news archives in Dow Jones Factiva and firm profiles in D&B Hoovers. This list is illustrative; many additional open documents informed triangulation.

Market-Sizing & Forecasting

A blended top-down approach converts production and trade units to retail revenue, then cross-checks results with sampled bottom-up roll-ups of supplier shipments and pharmacy sell-out audits. Key variables like diabetes prevalence, older-adult share, internet connectivity, average device life, and price erosion feed a multivariate regression that projects demand through 2030. Where bottom-up gaps emerge, regional expert inputs adjust utilization factors before final lock-in.

Data Validation & Update Cycle

Model outputs face variance checks against independent shipment tallies and retail scanner signals. Senior reviewers scrutinize anomalies, and we refresh each dataset annually, issuing interim updates when regulatory or macro shocks alter baseline assumptions. Before a report ships, one analyst re-runs the last quarter of data to ensure clients receive the most current view.

Why Our Self-Care Medical Devices Baseline Commands Reliability

Published estimates often differ because firms mix wellness wearables with medical-grade tools, apply divergent price assumptions, or refresh data on uneven schedules.

Key gap drivers include broader product scopes, varying ASP deflators, and one-off survey extrapolations. Mordor narrows focus to FDA-cleared or CE-marked home-use devices, tracks country-level ASP shifts quarterly, and reruns the model every twelve months.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 21.47 B | Mordor Intelligence | - |

| USD 27.45 B | Regional Consultancy A | Adds fitness bands and consumer smartwatches |

| USD 24.69 B | Industry Association B | Includes therapeutic pumps and mobility aids |

| USD 18.61 B | Global Consultancy C | Excludes connected patches, limits to five regions |

The comparison shows that when the right device list, consistent currencies, and annual refresh cadence are combined, Mordor delivers a balanced baseline that decision-makers can replicate and trust.

Key Questions Answered in the Report

How big is the Global Self Care Medical Devices Market?

The Global Self Care Medical Devices Market size is expected to reach USD 22.83 billion in 2026 and grow at a CAGR of 6.32% to reach USD 31.03 billion by 2031.

Which device category is growing fastest?

Smart wearable patches lead growth with an expected 7.78% CAGR through 2031 due to advances in microneedle delivery and integrated sensors.

Who are the key players in Global Self Care Medical Devices Market?

Medtronic plc., Koninklijke Philips N.V., ResMed, Inc., Roche Pharmaceutical and GE Healthcare are the major companies operating in the Global Self Care Medical Devices Market.

How dominant is diabetes care within the market?

Diabetes applications held 41.92% of 2025 revenue, making them the single largest clinical use case.

Which region offers the highest growth potential through 2031?

Asia-Pacific is projected to grow at 8.31% CAGR, supported by expanding healthcare infrastructure and supportive regulatory reforms.

Page last updated on: