HIV/AIDS Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.02 Billion |

| Market Size (2031) | USD 6.64 Billion |

| Growth Rate (2026 - 2031) | 10.56% CAGR |

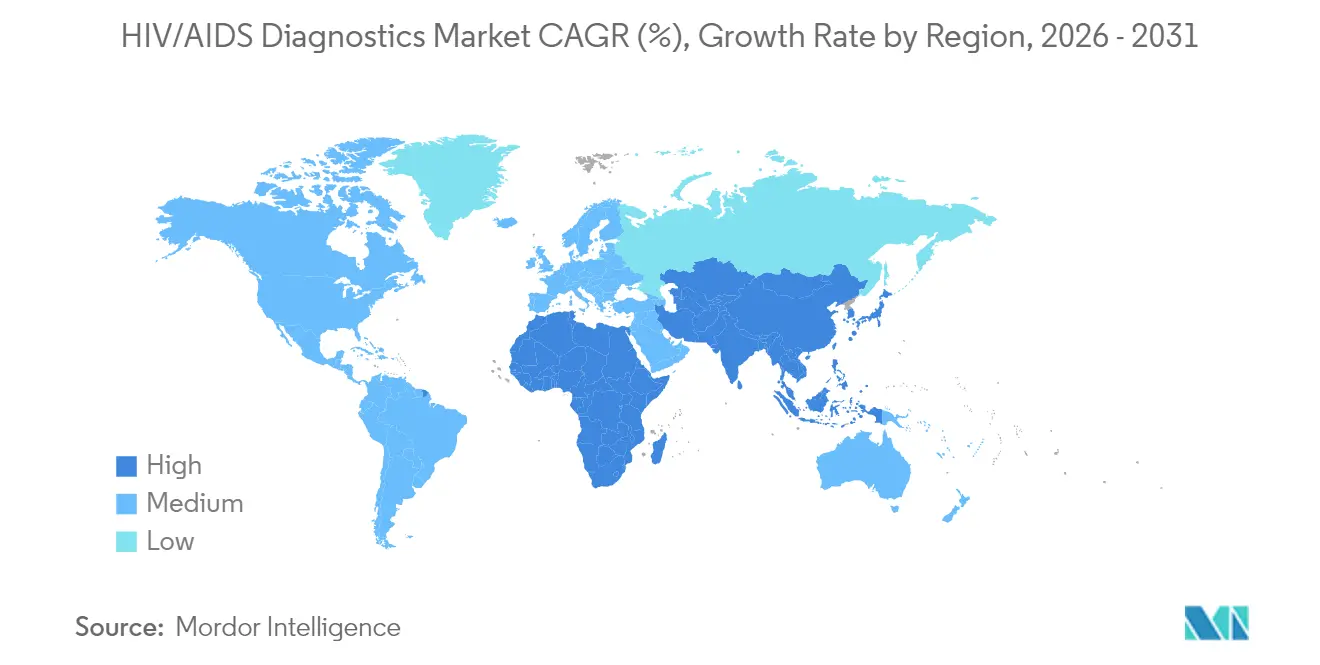

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

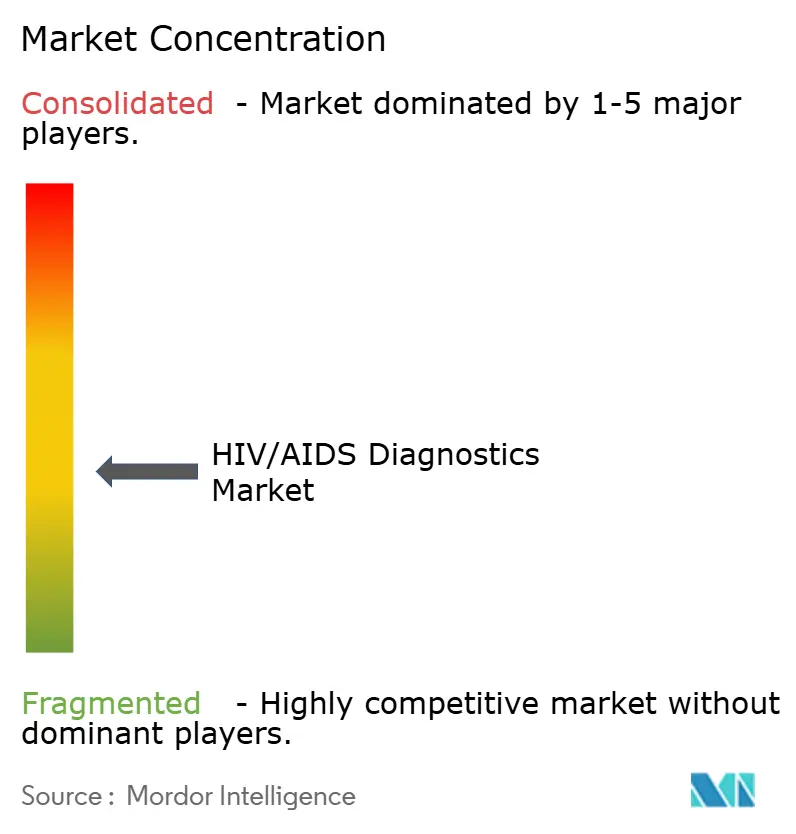

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HIV/AIDS Diagnostics Market Analysis by Mordor Intelligence

The HIV/AIDS diagnostics market size is expected to grow from USD 3.64 billion in 2025 to USD 4.02 billion in 2026 and is forecast to reach USD 6.64 billion by 2031 at 10.56% CAGR over 2026-2031. This pace reflects sustained funding, updated testing guidelines, and rapid technology diffusion that keep the HIV/AIDS diagnostics market well aligned with global 95-95-95 goals. Government-led self-testing programs, rising viral load monitoring volumes, and multi-disease molecular platforms collectively widen the addressable pool of users [1]World Health Organization, “Updated Recommendations on HIV Testing Services,” who.int. At the same time, donor-backed price ceilings, assay sensitivity gaps for new recombinant strains, and the shift to syndromic panels impose competitive and margin pressures that shape product strategy. Platform consolidation by leading firms and AI-enabled result interpretation continue to define how the HIV/AIDS diagnostics market evolves while ensuring reliable access in both mature and resource-limited settings.

Key Report Takeaways

- By product, consumables commanded 61.74% of the HIV/AIDS diagnostics market share in 2025, while instruments are projected to expand at an 11.18% CAGR through 2031.

- By test type, antibody tests led with a 47.92% revenue share in 2025; viral load testing is advancing at an 11.27% CAGR to 2031.

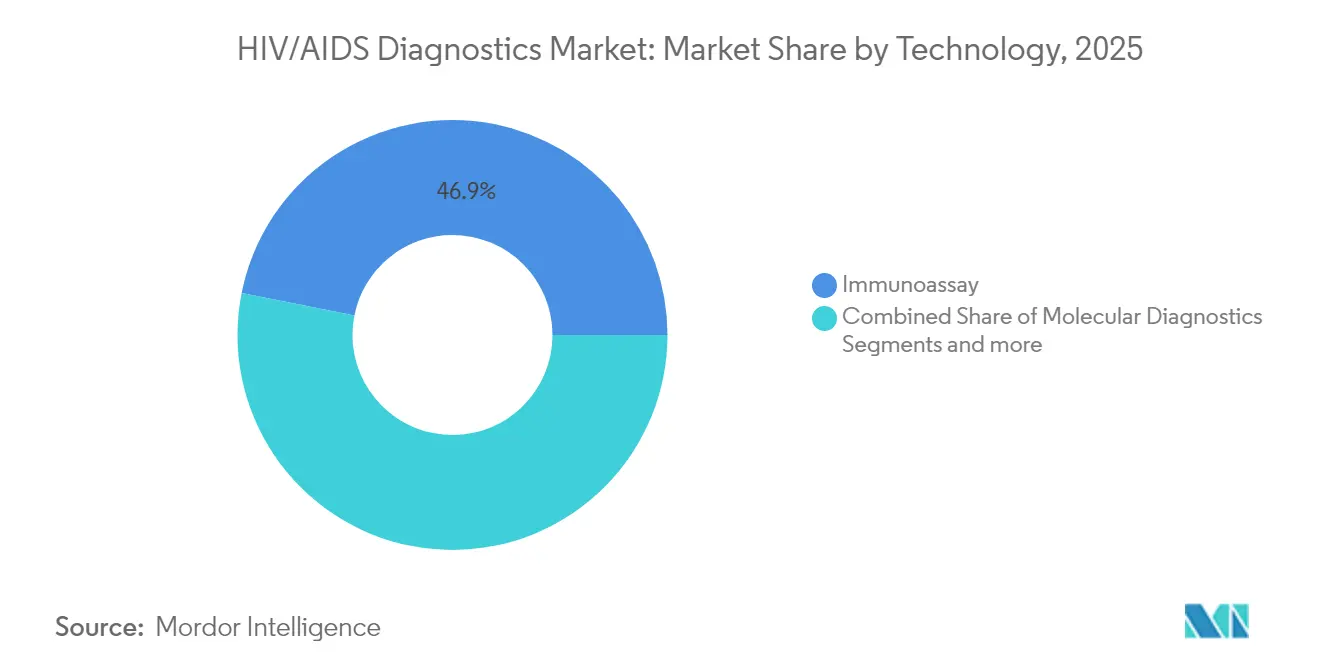

- By technology, immunoassays secured 46.88% share in 2025, whereas molecular diagnostics record the fastest CAGR of 11.22% through 2031.

- By end user, hospitals accounted for 53.35% of the HIV/AIDS diagnostics market size in 2025; at-home use registers the highest CAGR of 11.24% for the forecast period.

- By geography, North America held 38.52% revenue share in 2025, while Asia-Pacific is projected to grow at an 11.49% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global HIV/AIDS Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing HIV prevalence & incidence | +2.1% | Global, with concentration in Sub-Saharan Africa and Asia-Pacific | Medium term (2-4 years) |

| Government funding & initiatives | +2.8% | Global, led by PEPFAR countries and EU initiatives | Short term (≤ 2 years) |

| Expanding adoption of HIV self-testing & at-home rapid tests | +2.3% | North America, Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Integration of HIV in multiplex molecular respiratory/STD panels | +1.4% | North America, Europe, selected Asia-Pacific markets | Long term (≥ 4 years) |

| Scale-up of near-POC viral-load & EID testing in LMICs | +1.9% | Sub-Saharan Africa, South Asia, Latin America | Medium term (2-4 years) |

| Digital connectivity & AI-based result reporting platforms | +1.2% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing HIV Prevalence & Incidence

High-burden regions record continued case growth that widens the screening pool and amplifies demand for new assays. China reported 1.3 million people living with HIV by 2023, virtually all from sexual transmission, which is shifting screening efforts to general adult populations [2]China CDC Weekly, “HIV/AIDS in China — 2023,” chinacdc.cn . South Korea logged a 5.7% rise in new infections in 2023, with two-thirds occurring in adults aged 20-39. Novel recombinants such as CRF85_BC/CRF01_AE discovered in Ningxia, China, challenge assay sensitivity and spur continuous test optimization. India’s expanding PrEP programs also mandate periodic viral load checks to ensure prevention efficacy. These epidemiological shifts collectively enlarge the addressable HIV/AIDS diagnostics market.

Government Funding & Initiatives

Coordinated global and national funding accelerates test uptake. PEPFAR and the Global Fund are supporting lenacapavir access for 2 million individuals, requiring robust baseline screening and follow-up. The United Kingdom allocated GBP 20 million to expand opt-out HIV testing across 47 emergency departments, translating to immediate procurement needs [3]UK Department of Health and Social Care, “Investment to Expand HIV Testing,” gov.uk. West Bengal’s “Triple Elimination” program pairs HIV, syphilis, and hepatitis B screening, creating bundled demand for multiplex test kits. South Africa’s plan to enroll an extra 1.1 million patients in antiretroviral therapy by 2025 further solidifies predictable test volumes. Such funding clarity strengthens the revenue baseline for the HIV/AIDS diagnostics market.

Expanding Adoption of HIV Self-Testing & At-Home Rapid Tests

Consumer-controlled testing is redefining the HIV/AIDS diagnostics market by reaching first-time users and underserved groups. The CDC’s Together TakeMeHome program shipped 440,000 self-test kits in twelve months, with 24.1% going to people who had never tested before. Singapore began selling self-test kits in major pharmacies from January 2025, making walk-in, over-the-counter access routine. The FDA broadened OraQuick’s label to adolescents aged 14 years and older, opening a critical demographic accounting for nearly one-fifth of new U.S. diagnoses. A Canadian pilot of oral-fluid self-testing reported 100% concordance with lab methods plus 97% user satisfaction. Mainstreaming self-testing builds recurring revenue streams and cements the HIV/AIDS diagnostics market as a household-accessible category.

Integration of HIV in Multiplex Molecular Respiratory/STD Panels

Syndromic panels promise operational efficiencies by testing multiple pathogens in a single run. Roche secured FDA clearance for its cobas liat multiplex STI panel, delivering results in under 20 minutes. Multiplex PCR studies record sensitivities of 82%–97.1% and specificities above 94%, demonstrating clinical robustness. WHO’s systematic review found rapid integrated nucleic acid tests achieving ≥95% accuracy, endorsing their use in combined screening programs. Yet higher device pricing and the need for tailored result interpretation limit deployment in low-resource settings, pushing vendors to align dedicated HIV assays with broader syndromic menus to preserve share within the HIV/AIDS diagnostics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited lab infrastructure & skilled manpower in LICs | –1.8% | Sub-Saharan Africa, South Asia, select Pacific Islands | Medium term (2-4 years) |

| Price erosion from donor-driven bulk tenders | –1.4% | PEPFAR and Global Fund recipient countries | Short term (≤ 2 years) |

| Shift to multi-disease devices reducing dedicated HIV test demand | –0.9% | North America, Europe, developed Asia-Pacific markets | Long term (≥ 4 years) |

| Sensitivity gaps vs new HIV recombinants/variants | –0.7% | Global, with concentration in high-burden regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Lab Infrastructure & Skilled Manpower in LICs

Infrastructure gaps hinder implementation of high-complexity assays. A regulatory landscape review in Zimbabwe highlighted shortages in equipment calibration services and trained biomedical engineers, delaying device approvals. Low-cost approaches such as India-ink cryptococcosis screening in Mozambique illustrate demand for ultra-simple diagnostics that may compete with advanced molecular systems. While point-of-care early infant diagnosis in Uganda cut result turnaround from 28 days to 1 day and boosted ART initiation to 95%, scaling similar models requires steady funding for maintenance and training. These structural hurdles temper the near-term expansion pace of the HIV/AIDS diagnostics market in low-income regions.

Price Erosion from Donor-Driven Bulk Tenders

Large-volume procurements curb average selling prices. The Global Fund pushed first-line HIV treatment costs below USD 45 per person annually, signaling similar price expectations for diagnostics. PEPFAR’s planned budget cut of over 6% for fiscal 2025 heightens competition for grant-funded orders and compresses margins. Cost-effectiveness work in sub-Saharan Africa shows HIV self-testing at USD 12.75 per person versus USD 27.64 for campaign testing, reinforcing donor preference for lower-cost modalities. Vendors must therefore optimize scale and supply chain efficiency to stay profitable in the HIV/AIDS diagnostics market while serving donor-funded programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Consumables Maintain Revenue Core

Consumables held 61.74% of the HIV/AIDS diagnostics market share in 2025 and generate steady repeat sales each time a test is performed. Volume predictability secures cash flow and funds R&D. Instruments contribute larger upfront revenue per unit and are forecast to expand at an 11.18% CAGR, reflecting health-system moves toward integrated analyzers that accept multiple assays. Software and service add-ons, including AI-based interpretation dashboards, start to differentiate vendor offerings.

Recurring reagent demand anchors margin sustainability in the HIV/AIDS diagnostics market. Meanwhile, platform acquisitions—such as Roche’s USD 350 million purchase of LumiraDx’s point-of-care technology—signal that incumbents aim to secure future instrument installed bases. Public research funding, exemplified by NIH’s USD 1.3 million grant to Florida Atlantic University for a USD 5 microchip test, underscores how innovation targets both cost containment and usability. Digital services that triage results and guide next steps grow in prominence as manufacturers compete beyond hardware.

By Test Type: Viral Load Accelerates

Antibody assays led revenue at 47.92% in 2025 because they serve as gateway screening tools. Yet viral load testing is set for the highest 11.27% CAGR through 2031 as treatment monitoring drives routine usage. The WHO recommendation that viral load replace CD4 counts for monitoring more than 30 million individuals on therapy materially boosts this subsegment. CD4 and resistance tests remain important adjuncts but at lower growth trajectories.

High-throughput labs such as South Africa’s National Health Laboratory Service processed over 45 million viral load samples in 2022, proving scale economics. Innovations like pooled testing in Cameroon, which raised capacity by 80% while holding accuracy, and Bigtec Labs’ portable micro-PCR platforms illustrate how technology adapts to infrastructure realities. These factors cement the HIV/AIDS diagnostics market size for viral load assays as a prime growth driver.

By Technology: Molecular Diagnostics Gain Momentum

Immunoassays retained 46.88% share in 2025 on the back of mature workflows and favorable cost profiles. Molecular diagnostics, however, are projected to grow 11.22% annually as point-of-care capabilities advance and early-infection detection needs intensify. Flow cytometry occupies a specialized niche within CD4 monitoring, while CRISPR, nanomechanical sensors, and electrochemical biosensors populate the emerging technology pipeline.

Rapid molecular formats provide quantitation, resistance insight, and earlier window-period detection, advantages that justify premium pricing in the HIV/AIDS diagnostics market. CRISPR-based assays demonstrate potential for room-temperature reactions and smartphone readouts. Bio-Rad’s fourth-generation combo tests, reporting 100% sensitivity for acute infection, further bridge immunoassay convenience with molecular accuracy.

By End User: At-Home Testing Scales Fastest

Hospitals delivered 53.35% of total 2025 revenues, underlining their central role in confirmatory and treatment-linked testing. The at-home segment, helped by relaxed regulatory pathways and e-commerce distribution, is forecast to expand 11.24% per year to 2031. Independent laboratories address complex testing such as resistance genotyping, while community settings and retail pharmacies broaden access.

Self-collection kits demonstrate technical reliability and high user satisfaction, validated by Canada’s 100% concordance pilot. Economic analyses in Kenya show cost per self-test under USD 9 when scaled. Digital counselor integration, as implemented in India’s virtual self-testing program, links remote users to clinical care, fortifying the HIV/AIDS diagnostics market against loss to follow-up.

Geography Analysis

North America held a 38.52% revenue lead in 2025 because of strong insurance coverage and proactive public health campaigns. Federal initiatives such as the Together TakeMeHome self-test distribution provide reliable procurement streams and keep the HIV/AIDS diagnostics market expanding steadily in mature settings. Europe sustains moderate growth through emergency-department opt-out programs and integrated care models.

Asia-Pacific is the definitive growth engine, advancing at an 11.49% CAGR to 2031. India’s National AIDS Control Programme conducted 60 million tests in 2023-24 and dispenses free treatment to more than 1.68 million patients. China’s 1.3 million-person HIV cohort and Japan’s 2024 PrEP approval build continuous demand for screening and monitoring. South Korea’s broader healthcare reforms, which include diagnostic capacity upgrades, further bolster market expansion.

Middle East & Africa and South America trail but still represent meaningful opportunities as infrastructure investments rise. PEPFAR and Global Fund financing channels continue to anchor procurement in Sub-Saharan Africa. In Latin America, modernization of public laboratories and the gradual inclusion of self-testing in national guidelines stimulate incremental volumes, rounding out the global HIV/AIDS diagnostics market landscape.

Competitive Landscape

The HIV/AIDS diagnostics market shows moderate concentration, with top manufacturers combining instrumentation, reagents, and digital ecosystems. Roche, Abbott, and Siemens Healthineers continue consolidating point-of-care assets to protect installed bases. Roche’s acquisition of LumiraDx technology exemplifies the strategy to absorb emerging rivals and accelerate product cycles. Danaher’s dual Centers of Innovation sharpen its regulatory and companion-diagnostic capabilities, shortening development timelines.

M&A activity fell to 32 full-company deals in 2023, indicating selectivity and preference for bolt-on assets rather than transformative mergers. BD’s decision to divest its USD 3.4 billion IVD unit could reshuffle competitive rankings if acquired by a rival aiming to scale. AI-first platforms, such as Healthvana’s HIPAA-compliant chatbot for sexual-health clinics, point to a future where result interpretation services differentiate offerings more than hardware attributes.

Disruptors leverage CRISPR, smartphone connectivity, and pan-pathogen cartridges to target underserved niches. Yet recurring consumables revenue and regulatory experience give incumbents resilience. Overall, strategic moves center on portfolio breadth, digital add-ons, and manufacturing scale that can weather donor-driven price compression while sustaining innovation budgets.\

HIV/AIDS Diagnostics Industry Leaders

Siemens Healthineers

F. Hoffmann-La Roche Ltd

Abbott Laboratories

Thermo-Fisher Scientific Inc.

Danaher Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Northwestern University researchers unveiled a nanomechanical platform that could enable a rapid HIV point-of-care test delivering lab-quality results within minutes.

- April 2025: Shelby County Health Department began mailing free in-home HIV test kits to residents to boost screening uptake.

- January 2025: OraSure Technologies secured FDA approval for OraQuick HIV Self-Test use in adolescents aged 14 and above, expanding the market to younger users.

- July 2024: WHO released updated HIV testing guidelines stressing self-testing and integrated service delivery to broaden access.

Global HIV/AIDS Diagnostics Market Report Scope

As per the scope of the report HIV/AIDS diagnostics are used to investigate the existence of the human immune-deficiency virus, in saliva, serum or urine. HIV/AIDS diagnostics helps to detect antibodies, RNA or antigens. Blood tests are the most regular way to make a diagnosis of HIV. HIV is most commonly diagnosed by doing a urine test and blood test. The HIV/AIDS Diagnostics Market is Segment by Product (Consumables, Instruments, and Software & Services), Test Type (Antibody Tests, Viral Load Tests, CD4 Tests, and Others), End User (Diagnostic Laboratories, Hospitals, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Consumables |

| Instruments |

| Software & Services |

| Antibody Tests |

| Viral Load Tests |

| CD4 Tests |

| Others |

| Immunoassay |

| Molecular Diagnostics |

| Flow Cytometry |

| Others |

| Hospitals |

| Diagnostic Laboratories |

| At-Home Settings |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Consumables | |

| Instruments | ||

| Software & Services | ||

| By Test Type | Antibody Tests | |

| Viral Load Tests | ||

| CD4 Tests | ||

| Others | ||

| By Technology | Immunoassay | |

| Molecular Diagnostics | ||

| Flow Cytometry | ||

| Others | ||

| By End User | Hospitals | |

| Diagnostic Laboratories | ||

| At-Home Settings | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the HIV/AIDS diagnostics market?

The HIV/AIDS diagnostics market stands at USD 4.02 billion in 2026 and is expected to reach USD 6.64 billion by 2031.

Which segment is growing fastest within the market?

Viral load testing registers the highest forecast CAGR of 11.27% owing to its central role in treatment monitoring.

Why is Asia-Pacific considered the primary growth engine?

Government initiatives in India and China, rising incidence, and expanding PrEP programs push Asia-Pacific to an 11.49% CAGR through 2031.

How are self-testing trends influencing market dynamics?

Large-scale programs such as the CDC’s Together TakeMeHome have shown that self-testing reaches first-time users, driving volume and shifting demand toward at-home channels.

What challenges do manufacturers face in donor-funded markets?

Bulk tenders from PEPFAR and the Global Fund reduce average selling prices, demanding high manufacturing efficiency to preserve margins.

Who are the leading companies in the HIV/AIDS diagnostics industry?

Roche, Abbott, and Siemens Healthineers hold dominant positions through integrated platforms, while emerging firms focus on AI-based and CRISPR-enabled diagnostics.

Page last updated on: