Global Personal Mobility Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

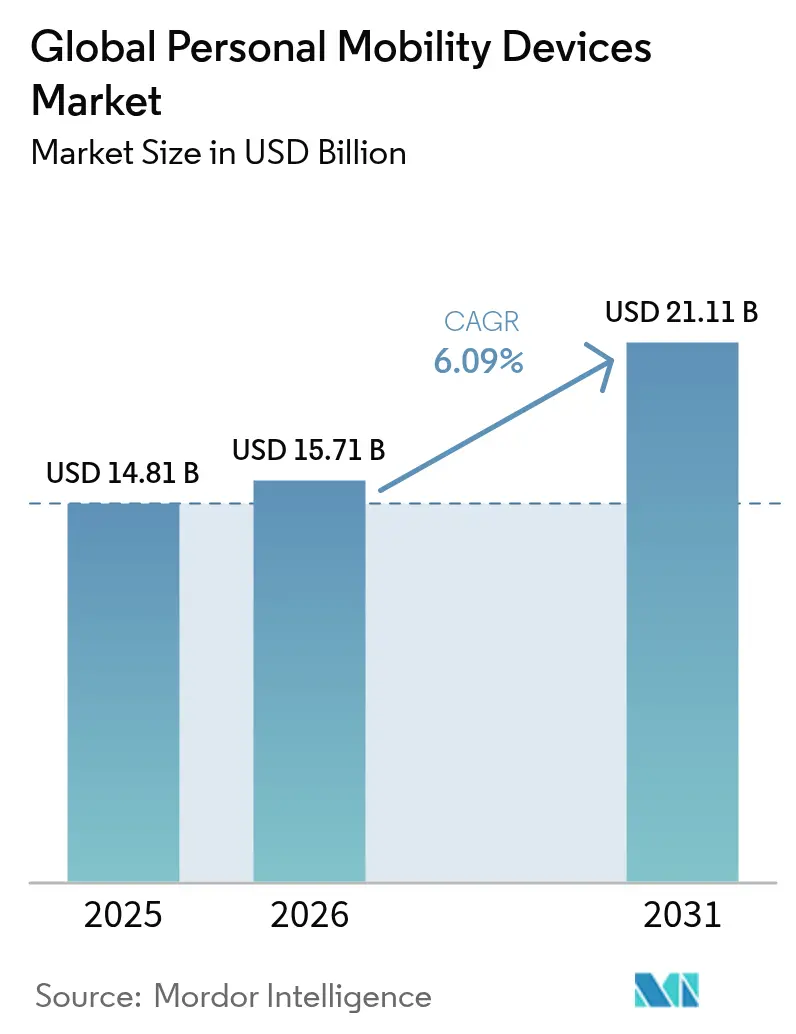

| Market Size (2026) | USD 15.71 Billion |

| Market Size (2031) | USD 21.11 Billion |

| Growth Rate (2026 - 2031) | 6.09% CAGR |

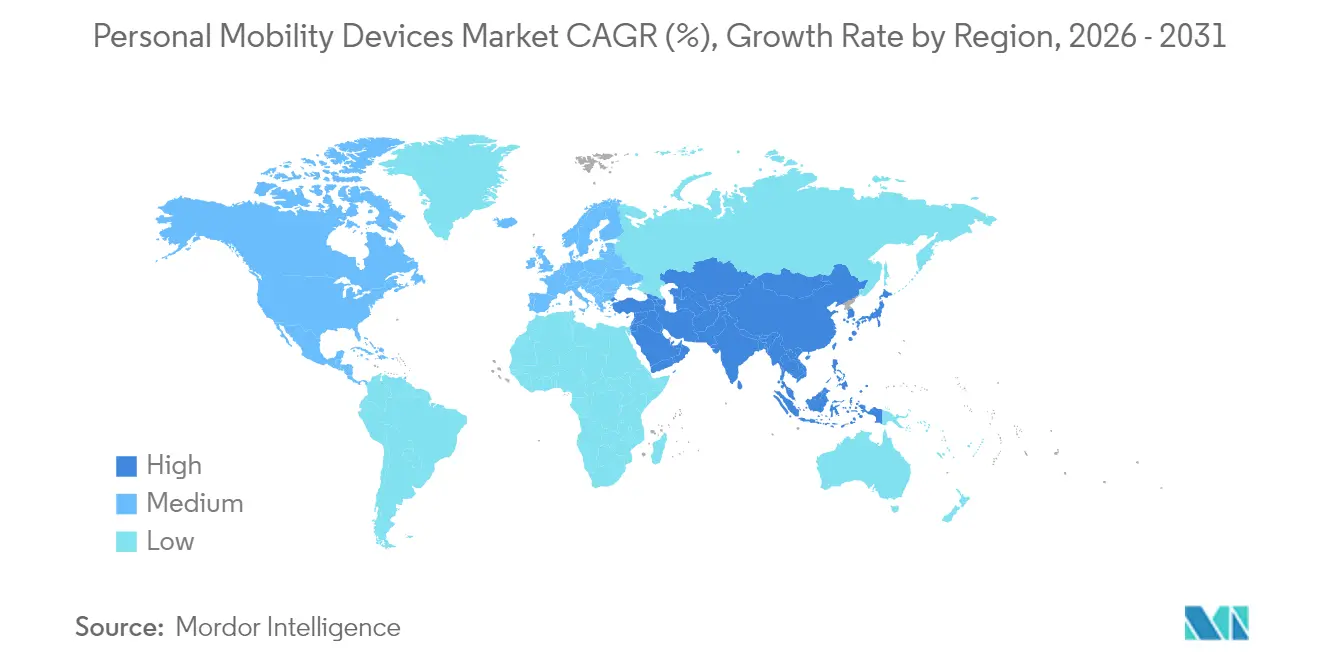

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Personal Mobility Devices Market Analysis by Mordor Intelligence

The personal mobility devices market size was valued at USD 14.81 billion in 2025 and estimated to grow from USD 15.71 billion in 2026 to reach USD 21.11 billion by 2031, at a CAGR of 6.09% during the forecast period (2026-2031). Demand accelerates as home-care reimbursement expands, AI-driven wheelchairs reach mainstream price levels, and battery density improvements extend powered-device range. Wheelchairs remain the volume backbone, while mobility scooters gain traction among seniors who want independence outdoors. Manual devices still outsell powered units, yet power-assist technologies narrow the affordability gap and tempt first-time buyers. North America retains leadership thanks to established coverage rules, but the personal mobility devices market in Asia-Pacific grows fastest as its elderly population swells and consumer spending power rises.

Key Report Takeaways

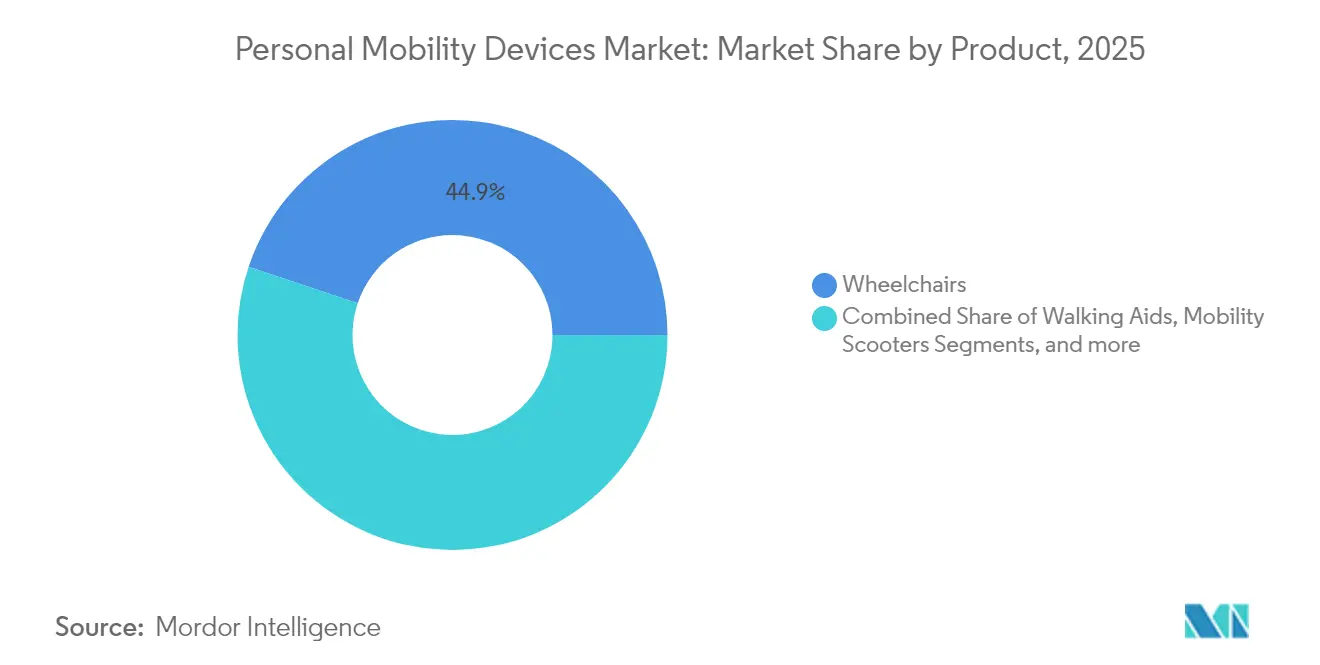

- By product category, wheelchairs led with 44.85% revenue share in 2025; mobility scooters are forecast to expand at a 6.48% CAGR to 2031.

- By technology, manual devices held 50.10% of the personal mobility devices market share in 2025, while powered solutions are projected to post the highest CAGR at 6.4% through 2031.

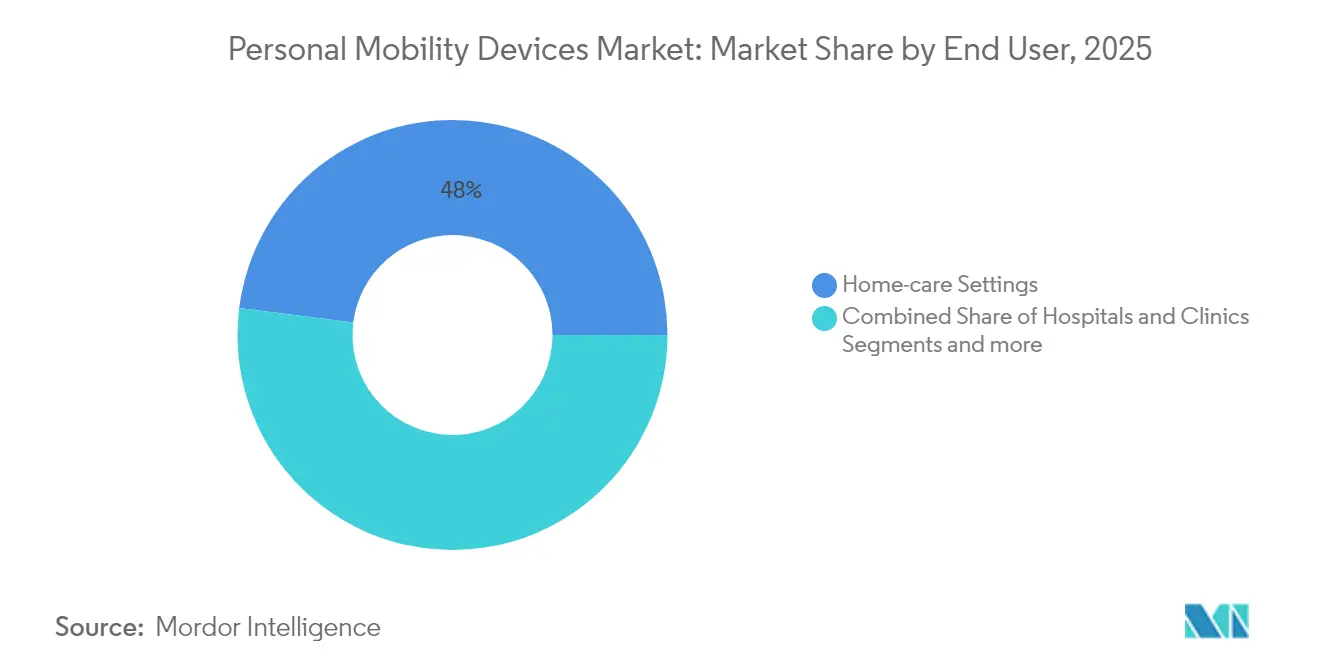

- By end user, home-care settings accounted for 48.00% of the personal mobility devices market size in 2025 and remain dominant, whereas rehabilitation and long-term care centers are advancing at a 6.45% CAGR to 2031.

- By geography, North America commanded 38.40% share of the personal mobility devices market in 2025; Asia-Pacific records the strongest CAGR at 6.66% to 2031.

- By distribution channel, offline retail captured 70.60% share in 2025, while the e-commerce segment is set to grow at 6.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Personal Mobility Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging-in-place preference & home-care reimbursement expansion | +1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Surge in robotic & AI-driven wheelchairs reaching commercial price points | +0.8% | Global, with early adoption in North America & Japan | Long term (≥ 4 years) |

| Mini-mobility regulation easing for scooters & e-kick devices in OECD cities | +0.6% | OECD countries, spillover to emerging markets | Short term (≤ 2 years) |

| Growing geriatric population & chronic disease prevalence | +1.4% | Global, concentrated in APAC & North America | Long term (≥ 4 years) |

| Battery density breakthroughs lifting range & payload of powered devices | +0.7% | Global, manufacturing concentrated in APAC | Medium term (2-4 years) |

| Rapid e-commerce penetration in DME retail | +0.5% | Global, led by North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging-in-Place Preference & Home-Care Reimbursement Expansion

Medicare’s 2025 Home Health Prospective Payment System now reimburses 80% of approved mobility device costs, aligning coverage with community-based care goals. U.S. private insurers mirror this structure, guaranteeing continuity across commercial plans. Streamlined telehealth evaluations further reduce administrative friction, which brings purchasing decisions earlier in the disability journey. European payers adjust in parallel, adding personal mobility devices to home-adaptation budgets. As reimbursement spreads across Asia-Pacific, independent living purchases become integral to retirement planning.

Surge in Robotic & AI-Driven Wheelchairs Reaching Commercial Price Points

WHILL’s autonomous chairs already ferry travelers across major U.S. airports, proving that lidar, depth cameras, and drive-by-wire systems meet safety and cost targets. Japanese nursing homes deploy similar fleets to ease staff workloads. Component price declines invite midsize manufacturers to license navigation stacks rather than build them from scratch. Insurers have begun covering autonomous options when they remove the need for human attendants, suggesting a virtuous cycle of data collection and actuarial validation.

Mini-Mobility Regulation Easing for Scooters & E-Kick Devices in OECD Cities

Regulatory modernization accelerates device uptake. Australia permits personal mobility devices on shared paths under updated Road Rules. Quebec authorizes motorized mobility aids on public roads once they meet specific lighting and brake standards. Japan’s transport ministry sets dimensional ceilings that guarantee train access for scooters. These moves legitimize powered devices in dense urban areas, expanding total addressable riders within the personal mobility devices market.

Growing Geriatric Population & Chronic Disease Prevalence

Asia’s elderly headcount is expected to reach 923 million by mid-century, raising demand for supportive technologies. Chronic conditions such as diabetes and osteoarthritis often restrict movement long before retirement age, extending product lifecycles. Rising disposable income in China and Thailand prompts families to purchase premium chairs rather than rely on hospital-supplied loaners. Western markets still grow, but sheer demographic momentum in Asia-Pacific defines future volume.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High out-of-pocket cost amid limited insurance coverage outside Tier-1 markets | -0.9% | Emerging markets, rural areas in developed countries | Medium term (2-4 years) |

| Safety recalls & rising litigation on lithium-ion fire risk | -0.6% | Global, concentrated in North America & EU | Short term (≤ 2 years) |

| Re-use / refurbished equipment suppressing new unit sales in OECD | -0.4% | OECD countries, particularly North America & EU | Long term (≥ 4 years) |

| Supply-chain exposure to rare-earth motor magnets | -0.3% | Global, manufacturing concentrated in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Cost Amid Limited Insurance Coverage Outside Tier-1 Markets

In the United States a beneficiary still pays 20% of an approved device, which may equate to several months of Social Security income. Coverage gaps are wider in Latin America and parts of Southeast Asia where national plans exclude durable medical equipment. Private insurers demand clinical validation, adding evaluation charges that push total expense beyond household budgets. Rural patients face added travel costs for fitting sessions, reinforcing inequity between urban and remote populations.

Safety Recalls & Rising Litigation on Lithium-Ion Fire Risk

The U.S. Consumer Product Safety Commission recalled 7,250 RELiON batteries after overheating incidents. Permobil removed SmartDrive speed dials following hundreds of complaints that linked malfunctions to injuries. Plaintiffs now target both manufacturers and cell suppliers, driving up insurance premiums and slowing market introductions of next-generation chemistries. Regulators consider broader certification regimes that may extend product cycles and raise compliance costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Wheelchairs Anchor Demand While Scooters Accelerate

Wheelchairs captured 44.85% of 2025 revenue, underscoring their foundational role in the personal mobility devices market. Manual variants remain the first choice for hospitals and budget-constrained buyers, while powered models appeal to users seeking independence over longer distances. WHILL’s joystick-free mid-wheel platform exemplifies a design pivot toward intuitive control. Mobility scooters follow with a 6.48% CAGR forecast to 2031, fueled by retirees who need a stable outdoor solution for shopping and leisure. Stair and platform lifts create household vertical access, gaining share as multi-story homes retrofit for aging residents. Competition now centers on out-of-box connectivity, seat ergonomics, and transportability rather than simple speed specifications.

Growth drivers vary by sub-segment. Manual chair sales rely on consistent reimbursement and refurbishment programs that place second-life units in emerging economies. Powered chair demand tracks battery breakthroughs that reduce weight without sacrificing torque. Scooters benefit from liberalized sidewalk rules in many OECD cities. Lift installations correlate with real-estate trends toward multi-level living spaces. Manufacturers that serve each niche through modular platforms can cross-sell accessories and lock in service revenue.

By Technology: Manual Dominates but Power-Assist Narrows the Gap

Manual designs held 50.10% market share in 2025 due to low price, simple maintenance, and universal insurance recognition. Lightweight aluminum frames and quick-release wheels keep the category competitive for active users. Powered systems, however, should grow at 6.4% CAGR on the back of denser batteries and falling electronics costs. Power-assist kits such as Sunrise Medical’s Empulse line transform a standard chair into a hybrid, providing a bridge for consumers hesitant about full electrification. Research into cobalt-free lithium-ion chemistries promises lower materials risk and extended cycle life.

Future design language blends energy-harvesting hubs, smartphone-based controls, and over-the-air diagnostics. As weight and price converge, insurers may eventually grade benefit levels on functionality rather than drive system. Suppliers who integrate open APIs for remote monitoring position themselves for value-based care contracts that reimburse on mobility outcomes rather than device acquisition alone.

By End User: Home-Care Prevails but Institutional Demand Gains Speed

Home-care environments accounted for 48.00% of the personal mobility devices market size in 2025. Households value equipment that folds for storage, negotiates tight hallways, and links to telehealth portals. Medicare’s 80% reimbursement ceiling underpins U.S. consumption, while analogous programs in the EU support a thriving repair ecosystem. Rehabilitation and long-term care centers are projected to grow at 6.45% CAGR as population aging increases post-acute residency periods. Facilities adopt fleet management dashboards to track utilization and preventive maintenance, cutting downtime for high-end powered chairs.

Hospitals and clinics remain steady buyers of rugged, infection-control-compliant devices. Procurement teams favor standardized platforms that share parts across multiple wards. Autonomous wheelchairs inside Japanese nursing homes already reduce staff transfers and collect route analytics for facility planners. As service models mature, manufacturers may sell uptime guarantees rather than units, aligning incentives with institutional cost-containment objectives.

By Distribution Channel: Physical Stores Retain Primacy but Digital Gains Trust

Offline suppliers controlled 70.60% of 2025 revenue because fitting accuracy still governs clinical outcomes. Certified dealers measure seat width, back-angle, and footrest length, then submit documentation to payers. They also install stair lifts and train users on safe transfers. Even so, e-commerce is forecast to log a 6.78% CAGR to 2031. Digital storefronts compress search costs, showcase video tutorials, and bundle financing plans. Remote approval portals match CMS prior-authorization workflows, removing paper bottlenecks.

Hybrid models blur lines between channels. Many retailers now schedule virtual show-and-tell sessions before an in-home fitting. Some manufacturers operate direct-to-consumer websites for standardized products like rollators but route complex powered chairs through brick-and-mortar partners. Marketplace differentiation therefore hinges on omnichannel execution rather than a strict online-versus-offline dichotomy within the personal mobility devices market.

Geography Analysis

North America led with 38.40% share in 2025 as Medicare coverage and ADA regulations created predictable volumes for suppliers. The personal mobility devices market benefits from an aging Baby Boomer cohort that prioritizes active lifestyles. Autonomous chair pilots at Los Angeles International Airport and Miami International Airport highlight early adoption appetite. Canada supports growth via provincial equipment loan programs, and Mexico expands public-insurance formularies, though price sensitivity is greater south of the border.

Asia-Pacific delivers the fastest CAGR at 6.66% through 2031. China’s middle class purchases powered scooters for suburban travel, while Japan pioneers robotic chairs to cope with caregiver shortages. India’s public-private partnerships scale low-cost manual chairs nationwide, yet premium demand rises in metro hospitals. Government initiatives fund domestic battery cell factories, aiming to cut import dependency and stabilize the personal mobility devices market supply chain. Southeast Asian nations revise import tariffs on medical devices, broadening market access for global brands.

Europe holds a sizeable yet slower-growing base. Universal healthcare plans reimburse most mobility aids, but refurbished equipment prolongs replacement cycles. The European Commission’s 2024 guidance on light electric vehicle standards harmonizes cross-border product certification, easing pan-EU distribution. Middle East and Africa show early-stage adoption tied to hospital construction booms and newly introduced mandatory health insurance in Gulf Cooperation Council states. South America progresses steadily as Brazil expands long-term care benefits and Argentina subsidizes domestic wheelchair production.

Competitive Landscape

The personal mobility devices market remains moderately fragmented. Permobil, Invacare, and Sunrise Medical together account for a large slice of wheelchair revenue, yet numerous regional firms populate scooter and rollator niches. MIGA Holdings acquired Invacare’s North American operations in 2024, allowing Invacare to refocus on Europe and Asia-Pacific. Sunrise Medical bought Nuprodx and Ride Designs to control the high-margin seating segment[1]Sunrise Medical, “Ride Designs Acquisition Press Release,” sunrisemedical.com.

Technology investment differentiates leaders. Permobil’s 14,000-square-meter innovation center unites R&D with automated production lines to compress design-to-market cycles[2]Permobil, “SmartDrive Recall Statement,” permobil.com. WHILL leverages edge computing to run obstacle-avoidance algorithms locally, reducing latency in crowded terminals. Competitors explore rare-earth-free motors to mitigate supply shock risks flagged by the U.S. Department of Energy[3]U.S. Department of Energy, “Critical Materials Assessment,” energy.gov. Firms with in-house electronics and battery packs shield themselves from component shortages, while those reliant on contract assemblers face cost volatility.

Service strategies evolve. Subscription models bundle devices, software updates, and maintenance into monthly fees, smoothing revenue. Extended warranties, cloud-based diagnostics, and remote firmware pushes strengthen brand stickiness. As autonomous functionality expands, intellectual-property portfolios around localization algorithms and sensor fusion rise in strategic value. Consolidation is expected to continue, especially if mid-tier brands struggle to fund required software talent.

Global Personal Mobility Devices Industry Leaders

Invacare Corporation

Ottobock

Drive DeVilbiss Healthcare

Stryker Corporation

GF Health Products Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Permobil inaugurated a 14,000 m² innovation center in Sundsvall, Sweden, combining production and R&D and installing rooftop solar panels to meet LEED Gold standards.

- November 2024: MIGA Holdings closed its purchase of Invacare’s North American business, enabling cost realignment and sharper geographic focus.

- October 2024: WHILL and Envoy Air launched self-driving wheelchairs at American Airlines terminals in Los Angeles and Miami, the first such service in U.S. airports.

- October 2023: Sunrise Medical completed the takeover of Ride Designs, adding custom seating systems to its portfolio.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the personal mobility devices market as all newly manufactured wheelchairs, walkers, rollators, canes, crutches, mobility scooters, stair lifts, and platform lifts sold through medical or specialized retail channels to individuals with temporary or permanent mobility impairment. We capture factory-gate revenue and distributor margin across 17 countries, expressing every value in constant 2024 USD.

Scope Exclusions: Recreational e-scooters, exoskeletons, rentals, and after-sales service revenues are excluded.

Segmentation Overview

- By Product

- Wheelchairs

- Manual Wheelchairs

- Powered Wheelchairs

- Robotic/Autonomous Wheelchairs

- Walking Aids

- Canes & Crutches

- Walkers & Rollators

- Mobility Scooters

- 3-Wheel

- 4-Wheel

- Stair Lifts & Platform Lifts

- Wheelchairs

- By Technology

- Manual

- Powered

- Hybrid / Power-assist

- By End User

- Hospitals & Clinics

- Home-care Settings

- Rehabilitation & Long-term Care Centers

- By Distribution Channel

- Offline

- E-commerce

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with rehabilitation physicians, mobility dealers, reimbursement administrators, and product engineers across North America, Europe, and Asia clarify mix shifts, channel mark-ups, and replacement cycles, filling gaps left by secondary data and anchoring our scenario assumptions.

Desk Research

We start with demographic baselines from the United Nations Population Division, disability prevalence from WHO Global Health Estimates, and injury statistics from the Global Burden of Disease study. Trade volumes and average unit prices are extracted from UN Comtrade HS codes 8713 and 9021, which are then matched with national tariff notes to distinguish wheelchairs, scooters, and walking aids. Device adoption trends are cross-checked against hospital procurement data in OECD Health Data, quarterly Medicare Durable Medical Equipment claims, and patent families mined through Questel that flag technology inflection points. Company revenue splits are obtained from D&B Hoovers, while Dow Jones Factiva provides real-time news for growth sense checks. The sources named are illustrative only; many further public and proprietary references underpin our evidence base.

Market-Sizing & Forecasting

A top-down demand pool is built from age-adjusted disabled population counts multiplied by device penetration and replacement rates, and then supplier roll-ups from ten leading manufacturers offer a selective bottom-up check. Key model inputs include median reimbursement caps, lithium-ion battery cost curves, hospital discharge-to-home ratios, rising e-commerce shares, and regulatory milestones such as EU MDR deadlines. Multivariate regression projects 2026-2030 growth, while scenario analysis flexes outcomes for policy shocks.

Data Validation & Update Cycle

Outputs pass variance thresholds, senior-analyst peer review, and client-side sense checks before sign-off. The market model refreshes each year, with interim updates triggered by major recalls, reimbursement code shifts, or landmark M&A events.

Why Mordor's Personal Mobility Devices Baseline Stands Credible and Reliable

Published estimates often differ because firms adopt dissimilar device baskets, apply varied ASP escalation rules, and lock forecasts to outdated claim files. Our clear scope and annual refresh ensure users receive figures that mirror current demand rather than last year's paperwork.

Key gap drivers include narrower country coverage in some studies, omission of lift platforms, reliance on claims data without retail channels, or inclusion of leisure scooters that inflate totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 14.81 B (2025) | Mordor Intelligence | |

| USD 12.12 B (2024) | Regional Consultancy A | Covers ten nations only and excludes stair lifts and e-commerce sales |

| USD 12.57 B (2025) | Global Consultancy B | Values drawn solely from insurance claims, omitting hospital and cash retail purchases |

| USD 15.30 B (2024) | Trade Journal C | Blends disability aids with consumer leisure scooters, inflating segment volumes |

These contrasts show that Mordor's iterative, evidence-rich approach provides a balanced, transparent baseline that decision-makers can readily trace and replicate.

Key Questions Answered in the Report

What is the current size of the personal mobility devices market?

The personal mobility devices market size stands at USD 15.71 billion in 2026 and is projected to reach USD 21.11 billion by 2031 at a 6.09% CAGR.

Which product category generates the most revenue?

Wheelchairs lead the product mix with 44.85% revenue share in 2025, underscoring their foundational role across care settings.

What region is growing the fastest?

Asia-Pacific posts the highest regional CAGR at 6.66% through 2031, driven by rapid population aging and rising household incomes.

How are reimbursement policies affecting demand?

Expanded home-care reimbursement in markets such as the United States now covers 80% of approved device costs, boosting uptake among seniors.

What technology trends are reshaping the industry?

Autonomous navigation, power-assist systems, and rare-earth-free motors are ushering in lighter, smarter devices that demand less caregiver intervention.

Are online channels overtaking traditional suppliers?

E-commerce grows at 6.78% CAGR as buyers appreciate home delivery and transparent pricing, yet physical dealers remain vital for fitting and after-sales service.

Page last updated on: