Managed Detection And Response Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

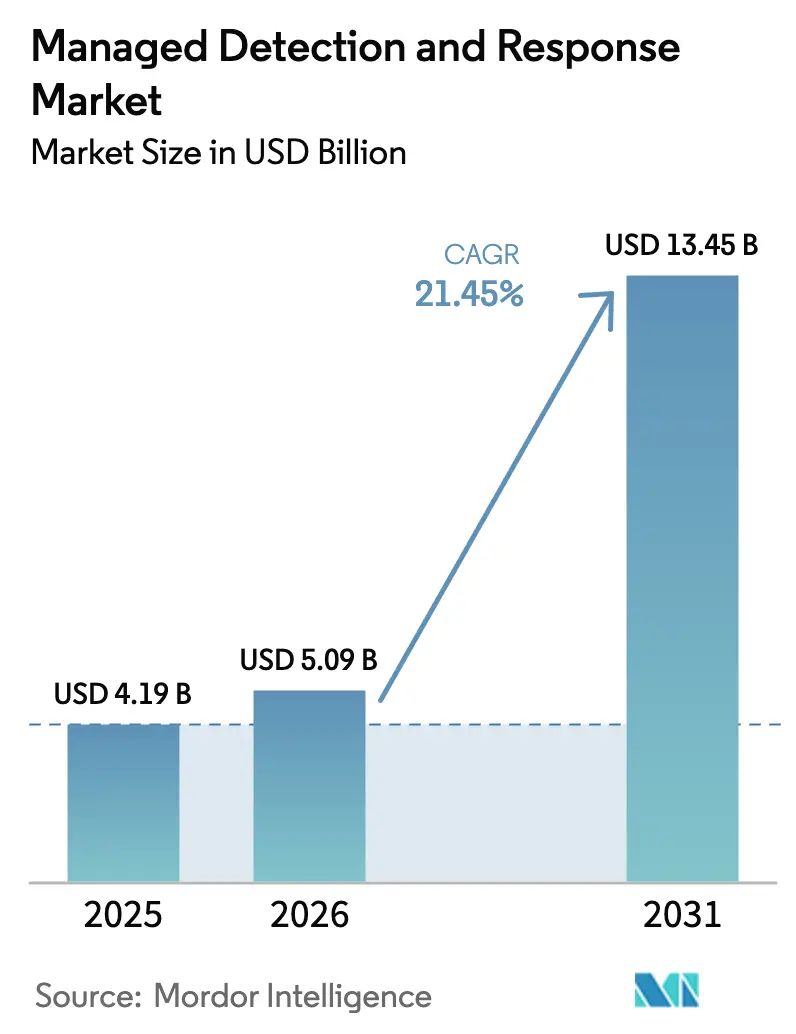

| Market Size (2026) | USD 5.09 Billion |

| Market Size (2031) | USD 13.45 Billion |

| Growth Rate (2026 - 2031) | 21.45% CAGR |

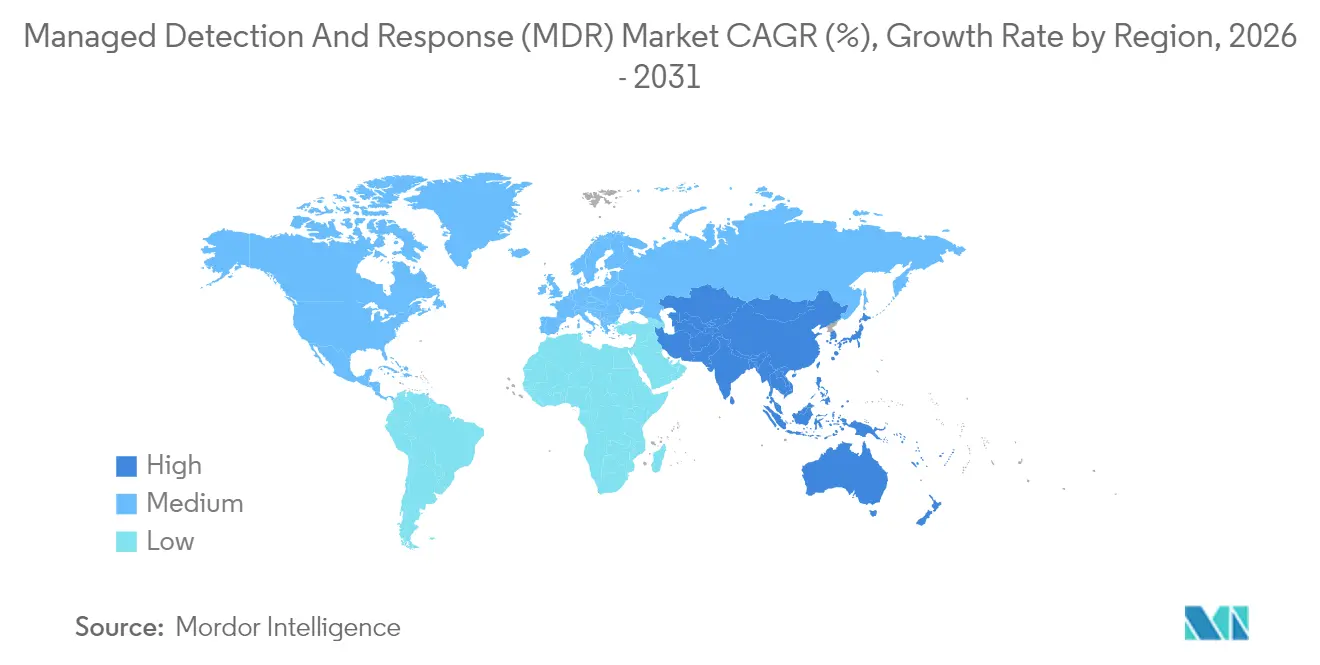

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Managed Detection And Response Market Analysis by Mordor Intelligence

The Managed Detection And Response Market size market is expected to grow from USD 4.19 billion in 2025 to USD 5.09 billion in 2026 and is forecast to reach USD 13.45 billion by 2031 at 21.45% CAGR over 2026-2031.

This sustained expansion signals an enterprise migration from reactive security toward always-on threat hunting, real-time incident response, and outcome-based cyber-risk reduction. Intensifying adversary sophistication, widening talent shortages, and new cross-sector regulations are converting managed detection and response services into foundational security infrastructure for organizations of every scale. Competitive differentiation now pivots on AI-driven automation that trims dwell time, boosts analyst productivity, and delivers sub-minute containment across hybrid estates. Commercial momentum also benefits from cyber-insurance premium incentives, which increasingly require verifiable managed detection and response controls before underwriting coverage.

Key Report Takeaways

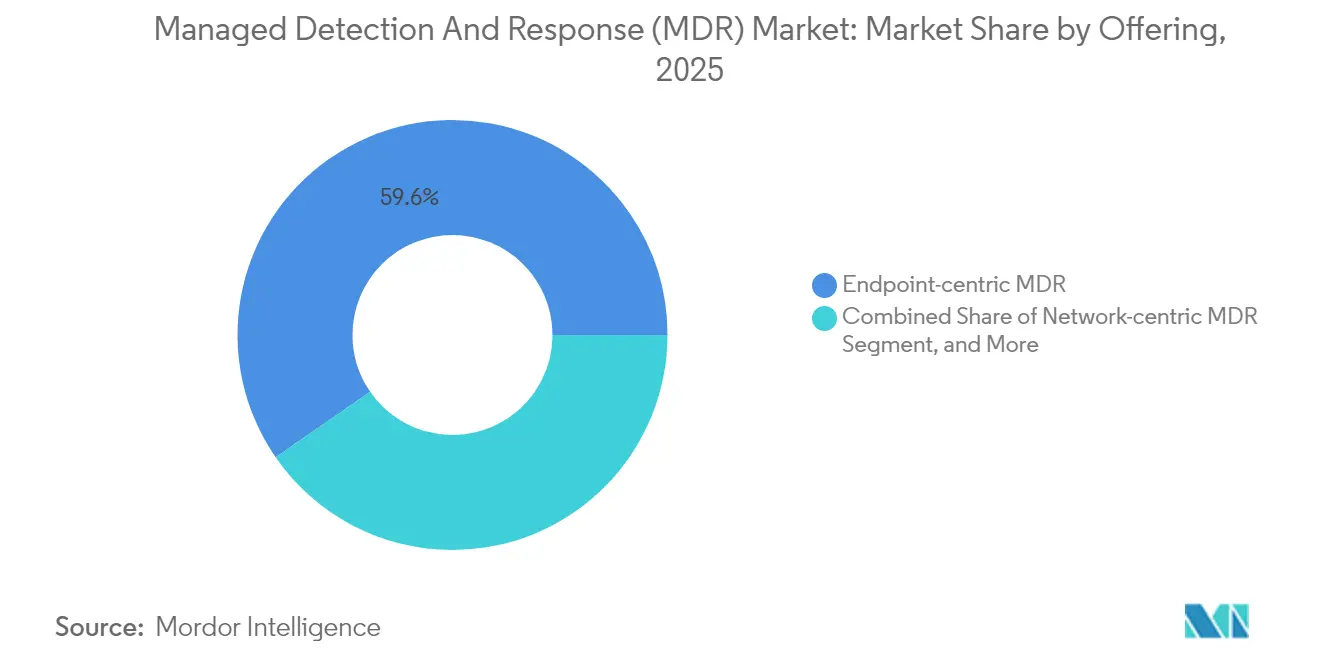

- By offering endpoint-centric services led with 59.62% revenue share in 2025, while managed extended detection and response is projected to compound at 27.61% CAGR through 2031.

- By deployment mode, cloud-delivered solutions held 69.85% share of the MDR market size in 2025, and hybrid architecture is advancing at 23.78% CAGR to 2031.

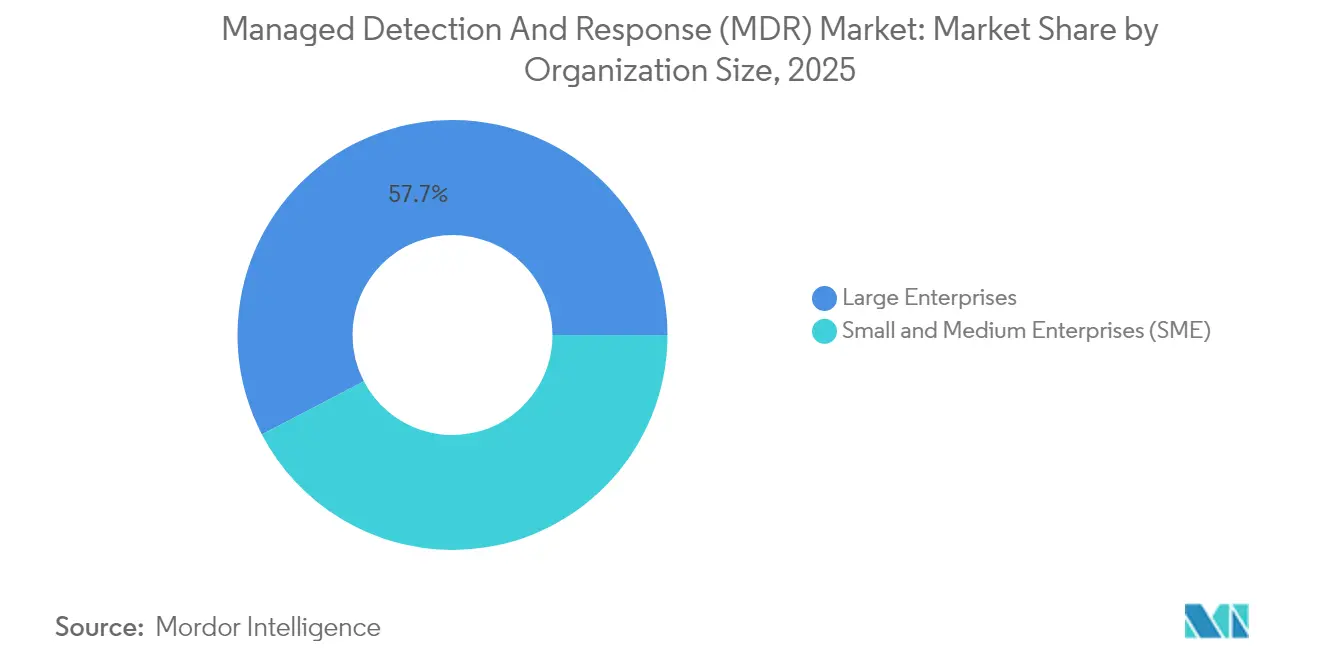

- By organization size, large enterprises accounted for 57.65% of 2025 spending, whereas small and medium enterprises are expanding at a 27.02% CAGR through 2031.

- By vertical, banking, financial services, and insurance captured 28.74% of the MDR industry share in 2025; healthcare and life sciences are forecast to expand at a 23.60% CAGR to 2031.

- By geography, North America represented 45.78% revenue share in 2025, while Asia-Pacific is the fastest-growing region with a 25.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Managed Detection And Response Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating sophistication of cyber-attacks | +4.2% | Global | Short term (≤ 2 years) |

| Cybersecurity talent shortage | +3.8% | North America and the EU spill over to the Asia-Pacific | Medium term (2-4 years) |

| Expanding regulatory compliance mandates | +3.1% | EU core, expanding to Asia-Pacific and the Americas | Medium term (2-4 years) |

| Cyber-insurance premium credits tied to MDR adoption | +2.4% | North America and the EU | Short term (≤ 2 years) |

| OT / IoT convergence is creating a new attack surface | +2.9% | Global, concentrated in manufacturing regions | Long term (≥ 4 years) |

| AI-driven autonomous SOC-as-code lowers the entry barrier | +2.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Sophistication of Cyber-Attacks

Threat actors now weaponize artificial-intelligence tooling such as EDRKillShifter to sidestep endpoint defenses and employ extortion tactics that emphasize stealthy data theft across hybrid clouds.[1]ExtraHop, “2025 Security Predictions: Top Ransomware Groups to Watch,” extrahop.com Operational-technology breaches climbed 73% in the last reporting cycle, exposing manufacturing and energy assets where IT-OT convergence widens attack surfaces. Nation-state campaigns increasingly compromise software supply chains, compelling enterprises to seek managed detection and response market leaders with end-to-end visibility. These developments accelerate demand for AI-enabled threat hunting that correlates endpoint, network, and identity telemetry at scale.

Cyber-Security Talent Shortage

The global deficit of 4.8 million practitioners leaves 90% of organizations with critical skills gaps in AI, cloud, and zero-trust disciplines. Seventy-one percent of security operations center analysts report burnout from unmanageable alert volumes, precipitating double-digit attrition that weakens in-house defenses. Managed detection and response market providers close this gap with 24/7 monitoring and specialized expertise unavailable to many firms. AI-powered triage now routes benign events away from human review, allowing limited headcount to focus on proactive hunting.

Expanding Regulatory Compliance Mandates

The European Union’s NIS2 Directive, effective October 2024, obliges essential-service operators to implement rigorous risk management and incident reporting that many can satisfy only through third-party services.[2]Cloud Security Alliance, “Cybersecurity Laws Ahead of 2025,” cloudsecurityalliance.org Financial institutions face added obligations under the Digital Operational Resilience Act from January 2025, extending oversight to technology vendors. In the United States, forthcoming critical-infrastructure reporting rules reinforce this compliance tide. Collectively, these statutes reposition the managed detection and response market from an optional safeguard to a mandatory control for cross-border enterprises.

AI-Driven Autonomous SOC-as-Code Lowers Entry Barrier

Agentic platforms automate investigation, containment, and regulatory notification, enabling smaller providers to match tier-one service levels without proportionate headcount. IBM’s autonomous threat-operations engine illustrates how code-driven playbooks can resolve routine incidents end-to-end. Microsoft’s 11 dedicated AI agents for Security Copilot further normalize machine-executed response workflows. The result is a bifurcated MDR market in which AI-first vendors outpace conventional MSSPs on speed, accuracy, and cost efficiency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total cost of ownership for SMEs | -2.1% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Cross-border data-sovereignty concerns | -1.8% | EU, Asia-Pacific, with data localization laws | Medium term (2-4 years) |

| Alert fatigue and SOC complacency risk | -1.3% | Global | Medium term (2-4 years) |

| Unmanaged IoT/medical device blind-spots | -1.6% | Healthcare, manufacturing sectors globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership for SMEs

Comprehensive managed detection and response subscriptions can consume 7-12% of small-business IT budgets, with average per-employee outlays reaching USD 2,800.[3]Coalition, “Premium Credits for MDR,” coalitioninc.com Specialized compliance overlays for HIPAA or PCI-DSS add further premiums. While cyber-insurance discounts of up to 12.5% offset the expense, affordability remains a gating factor in emerging economies. Tiered service blends and channel-focused offerings such as Field Effect’s MDR Core illustrate pricing innovations aimed at expanding SME uptake.

Cross-Border Data-Sovereignty Concerns

Localization statutes—including China’s Personal Information Protection Law and India’s prospective rules—require that personal data remain within national borders, forcing providers to build regional data centers and sovereign-cloud architectures. These mandates raise infrastructure costs and can fragment global threat-intelligence correlation, diminishing detection efficacy. Scholarly work on data-residency trade-offs warns that such fragmentation complicates unified visibility across jurisdictions. Consequently, multinational organizations weigh regulatory exposure against the operational benefits of centralized security analytics when selecting managed detection and response vendors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Platform Convergence Favors MXDR

The segment led by endpoint-centric solutions recorded 59.62% revenue in 2025 as ransomware and credential-theft attacks continue to pivot on user devices. Managed eXtended detection and response is projected to grow at a 27.61% CAGR, underscoring enterprise appetite for consolidated telemetry across endpoints, networks, identities, and cloud workloads. MXDR’s ability to normalise diverse data feeds into a unified analytics layer reduces investigative latency and boosts containment accuracy. OT-focused services are attracting heavy-industry adopters where operational downtime translates into direct revenue loss, and where the MDR market size for those services is projected to expand rapidly through 2031. Increasing rollout of secure-by-design firmware on smart-factory devices further accelerates demand for deep-packet-inspection-capable MDR.

A parallel driver is the rising cost of siloed tooling; large firms routinely run more than 40 point products. MXDR’s consolidation value proposition appeals to finance and healthcare organizations juggling overlapping compliance regimes. The managed detection and response market share of MXDR is therefore expected to climb steadily as platforms mature their native SOAR, sandboxing, and threat-intelligence orchestration.

By Deployment Mode: Hybrid Architectures Gain Momentum

Cloud-native delivery dominated 69.85% of 2025 revenue owing to subscription flexibility, instant feature upgrades, and global telemetry enrichment through multi-tenant analytics. This architecture lets providers roll out AI models without customer infrastructure changes, keeping time-to-value low. Nevertheless, regulatory commitments and national-security considerations sustain an on-premises cohort within public-sector and critical-infrastructure operators.

Hybrid deployment bridges these poles by retaining sensitive logging locally while forwarding enriched metadata to cloud analytics engines. With a projected 23.78% CAGR to 2031, hybrid represents the sweet spot for firms balancing sovereignty, latency, and scale. For providers, it widens addressable demand without relinquishing SaaS efficiencies, reinforcing the managed detection and response market’s pivot to platform-agnostic service delivery.

By Organization Size: SME Uptake Reshapes Demand Curves

Large enterprises drove 57.65% of 2025 revenue as complex security stacks, multi-cloud estates, and stringent audit requirements necessitated outsourced monitoring. These organizations typically run dedicated engagement models featuring custom playbooks and embedded threat-intel feeds. As a result, the managed detection and response market size derived from this cohort remains substantial even as growth moderates.

Conversely, SMEs are poised for a 27.02% CAGR through 2031. Drivers include insurer mandates, supply-chain security clauses, and cost-effective “SOC-in-a-box” packaging that eliminates the need for around-the-clock staffing. Niche vendors targeting MSP ecosystems with white-label MDR broaden market accessibility, signaling a democratisation trend that will shift total addressable volumes toward the mid-market.

By Vertical: BFSI Retains Scale While Healthcare Leads Growth

Banking, financial services, and insurance commanded a 28.74% share in 2025 as regulators enforced rapid breach-notification standards and third-party risk audits. High-frequency transaction environments require millisecond-level detection of lateral movement, reinforcing spending on MDR industry leaders that integrate network, application, and identity analytics. The vertical’s maturity fosters multi-year contracts with tier-one providers, stabilising recurring revenue flow.

Healthcare and life sciences are forecast at a 23.60% CAGR to 2031, propelled by surging adoption of connected diagnostic devices and ransomware campaigns that jeopardise patient safety. The managed detection and response market share of OT/IoT monitoring within hospitals climbs as legacy medical equipment remains unpatchable yet mission-critical. Providers with clinical-context capabilities and FDA-aligned reporting workflows are best positioned to capture this opportunity.

Geography Analysis

North America retained 45.78% revenue share in 2025, buoyed by mature cyber-insurance ecosystems that grant premium deductions once verified MDR controls are in place. Large public companies view managed detection and response market engagement as essential infrastructure following cascading supply-chain attacks such as SolarWinds. The United States remains the primary revenue engine, but Canadian banks and energy operators also account for notable multi-year contracts.

Asia-Pacific registers the highest trajectory at 25.48% CAGR through 2031, supported by rapid digitisation, a growing middle class, and high ransomware exposure. Regional cybersecurity budgets are projected at USD 52 billion by 2027 with 12.8% annual growth, framing a sizeable managed detection and response market opportunity. Governments in Singapore, Japan, and India actively promote shared-services security models and sovereign cloud zones, catalysing adoption among medium-sized firms that previously relied on ad hoc controls.

Europe advances on the strength of NIS2 and sectoral regulation. German automotive suppliers and French aerospace primes extend managed detection and response engagements to cover supply-chain partners. Sovereign-cloud partnerships between local telcos and hyperscalers provide the compliance backbone for cross-border telemetry exchange. Meanwhile, Middle East and Africa adoption levels grow from a small base as energy diversification and smart-city programs create fresh demand for outsourced cyber-skills.

Competitive Landscape

Market consolidation accelerated in early 2025 when Sophos absorbed Secureworks for USD 859 million, creating the largest pure-play provider serving more than 28,000 customers worldwide. CrowdStrike continues to lead revenue share, deepening alliances with cloud and firewall vendors to extend coverage across workloads and industrial protocols. Strategic differentiation increasingly hinges on machine-executed response; SentinelOne highlighted its first positive non-GAAP operating margin while attributing gains to automated containment modules.[4]SentinelOne, “FY 2025 Results,” sentinelone.com

Disruptors leverage agentic AI to compress mean-time-to-respond. Ontinue unveiled autonomous investigation for Microsoft cloud estates, showcasing sub-60-second containment without analyst intervention. Arctic Wolf expanded its platform via the acquisition of BlackBerry’s Cylance assets for USD 160 million plus shares, bolstering native endpoint telemetry. White-space remains in OT security, medical-device monitoring, and compliance-grade sovereign-cloud MDR. Cyber-insurers now co-design controls with providers, elevating those vendors whose playbooks demonstrably reduce claims frequency.

Managed Detection And Response Industry Leaders

CrowdStrike Holdings, Inc.

Arctic Wolf Networks, Inc.

Rapid7, Inc.

eSentire Inc.

SentinelOne, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Contrast Security launched Application Detection and Response to secure custom applications and APIs.

- June 2025: Fortinet posted USD 1.54 billion Q1 2025 revenue, up 14% year-on-year, and reaffirmed investment in unified SASE plus SOC services.

- May 2025: Securonix released GenAI agents automating level-1-to-3 SOC workflows.

- April 2025: Blackpoint Cyber debuted the CompassOne unified posture platform for MSPs.

Global Managed Detection And Response Market Report Scope

| Endpoint-centric MDR |

| Network-centric MDR |

| Cloud-centric MDR |

| OT / IoT MDR |

| Managed eXtended Detection and Response (MXDR) |

| On-premises |

| Cloud |

| Hybrid |

| Small and Medium Enterprises (SME) |

| Large Enterprises |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Government and Public Sector |

| Manufacturing |

| Retail and E-Commerce |

| Energy and Utilities |

| Education |

| Telecommunications and IT |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Offering | Endpoint-centric MDR | ||

| Network-centric MDR | |||

| Cloud-centric MDR | |||

| OT / IoT MDR | |||

| Managed eXtended Detection and Response (MXDR) | |||

| By Deployment Mode | On-premises | ||

| Cloud | |||

| Hybrid | |||

| By Organization Size | Small and Medium Enterprises (SME) | ||

| Large Enterprises | |||

| By Vertical | Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | |||

| Government and Public Sector | |||

| Manufacturing | |||

| Retail and E-Commerce | |||

| Energy and Utilities | |||

| Education | |||

| Telecommunications and IT | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the managed detection and response (MDR) market?

The managed detection and response market size reached USD 5.09 billion in 2026 and is projected to reach USD 13.45 billion by 2031.

How fast is the MDR industry expected to grow?

It is forecast to post a 21.45% CAGR between 2026 and 2031, reflecting persistent demand for outsourced security expertise.

Which region will see the fastest uptake of managed detection and response services?

Asia-Pacific is projected to expand at a 25.48% CAGR through 2031 on the back of rapid digitisation and escalating cyber-threat activity.

Why are small and medium enterprises increasingly adopting managed detection and response?

SMEs benefit from cyber-insurance premium credits and turnkey 24/7 monitoring that overcomes internal skills shortages while remaining cost-predictable.

What technological shift is reshaping competitive dynamics among MDR vendors?

AI-driven autonomous SOC-as-code now automates investigation and response, enabling faster containment and lowering provider entry barriers.

Which industry vertical is forecast to exhibit the highest growth in MDR spending?

Healthcare and life sciences are expected to grow at a 23.60% CAGR due to the expansion of connected medical devices and rising ransomware exposure.

Page last updated on: