Managed Network Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

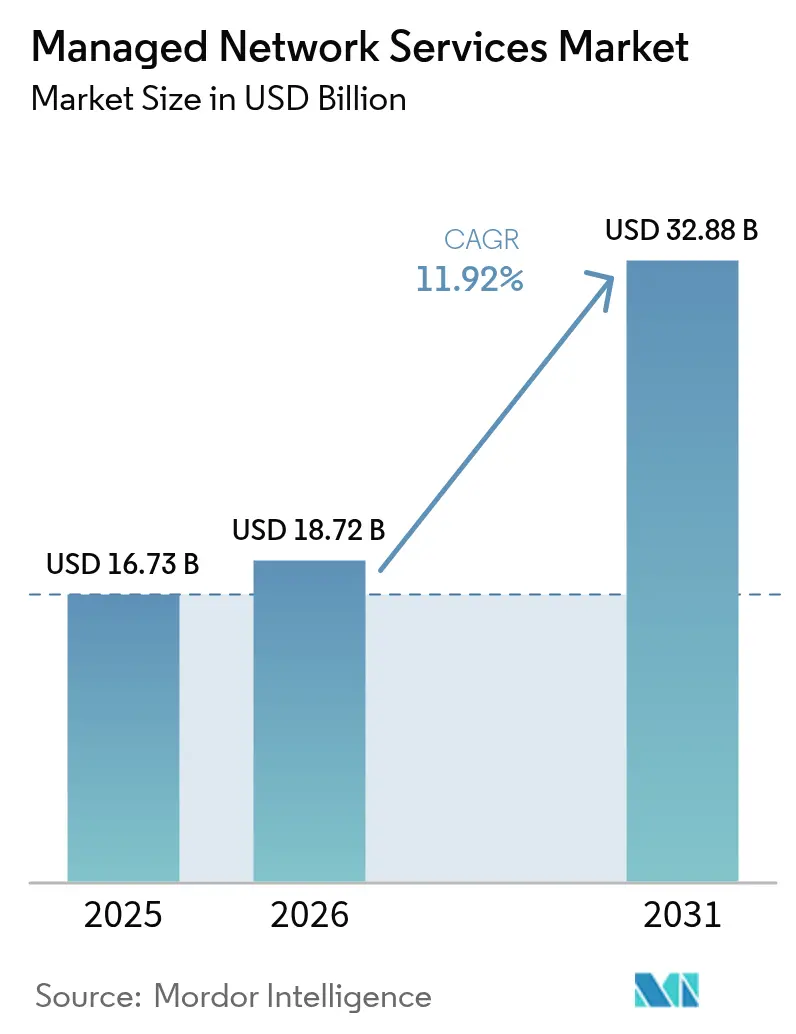

| Market Size (2026) | USD 18.72 Billion |

| Market Size (2031) | USD 32.88 Billion |

| Growth Rate (2026 - 2031) | 11.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Managed Network Services Market Analysis by Mordor Intelligence

The Network managed services market size is expected to grow from USD 16.73 billion in 2025 to USD 18.72 billion in 2026 and is forecast to reach USD 32.88 billion by 2031 at 11.92% CAGR over 2026-2031. This rapid growth stems from enterprises’ need to outsource increasingly complex network operations, turning managed services into mission-critical infrastructure that underpins corporate digital transformation strategies. Enterprises report double-digit cost reductions, faster time-to-market for new applications, and improved resiliency when moving to proactive, AI-enabled managed service models. The global shortage of qualified network engineers further accelerates demand; 95% of technology leaders cite hiring challenges while talent costs escalate, especially for emerging SD-WAN, SASE, and private 5G skill sets. [1]Robert Half, “New Research Reveals Severity of the Technology Skills Gap,” roberthalf.comConsolidation among vendors reshapes the competitive field, Hewlett Packard Enterprise’s USD 14 billion purchase of Juniper Networks exemplifies the trend toward end-to-end, software-defined, subscription-based portfolios. Finally, the Asia-Pacific investment boom in data centers and fiber backbones positions that region as the volume growth engine, even as North America remains the largest revenue contributor.

Key Report Takeaways

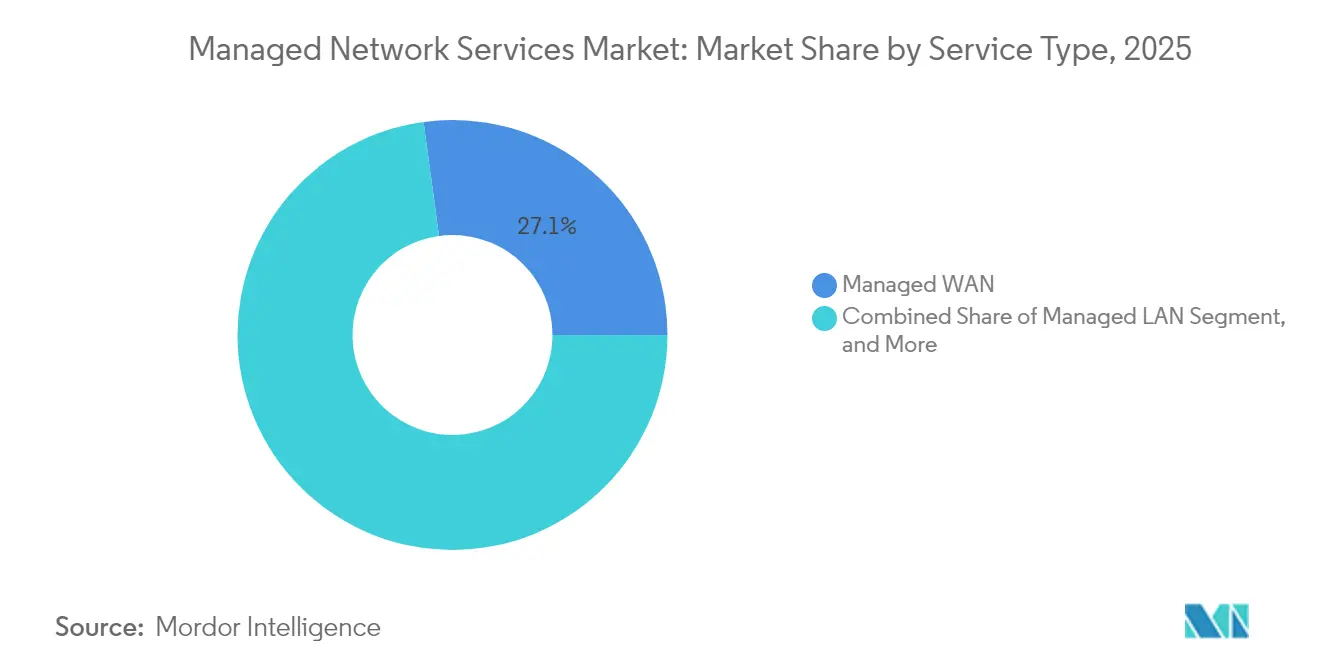

- By service type, managed WAN captured 27.15% of the Network managed services market share in 2025; Managed SD-WAN is projected to advance at a 18.4% CAGR through 2031.

- By deployment mode, on-premise solutions commanded 59.80% of the Network managed services market size in 2025, whereas cloud/NaaS models are set to grow at an 17.6% CAGR to 2031.

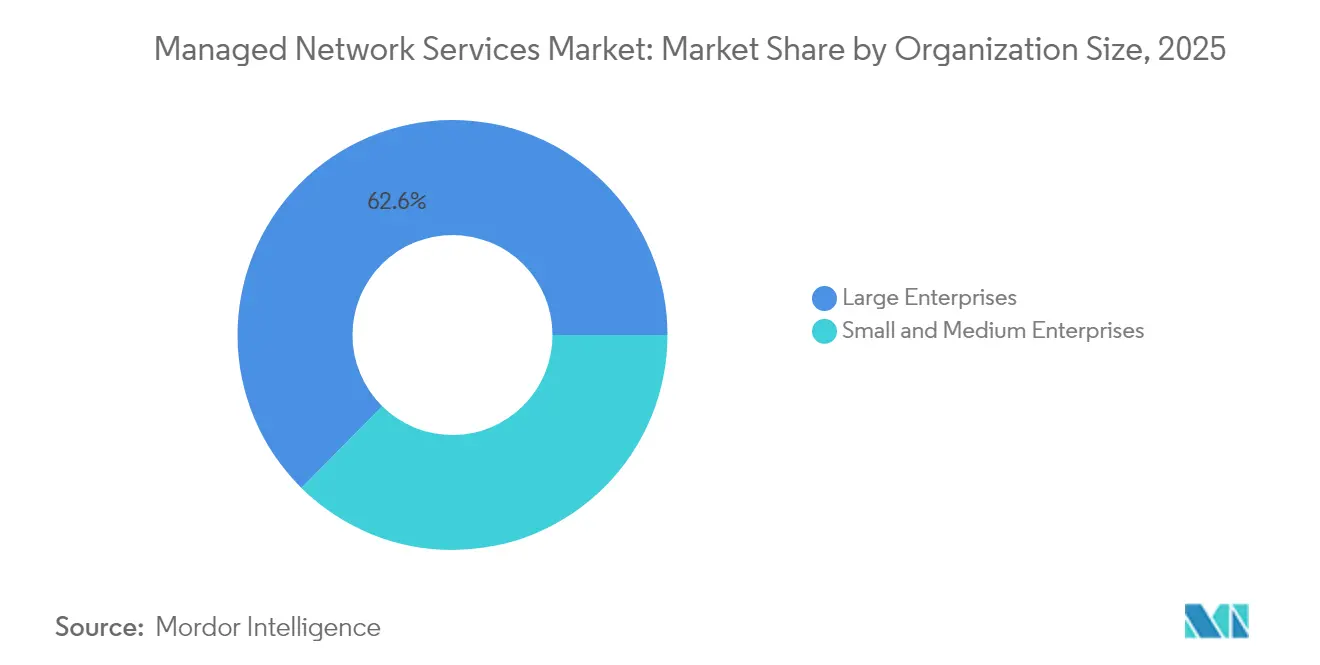

- By organization size, large enterprises held 62.60% of the Network managed services market share in 2025, while the SME segment is expected to expand at a 13.2% CAGR through 2031.

- By end-user vertical, BFSI accounted for a 21.55% share of the Network managed services market size in 2025, and healthcare is projected to grow at a 15.1% CAGR between 2026 and 2031.

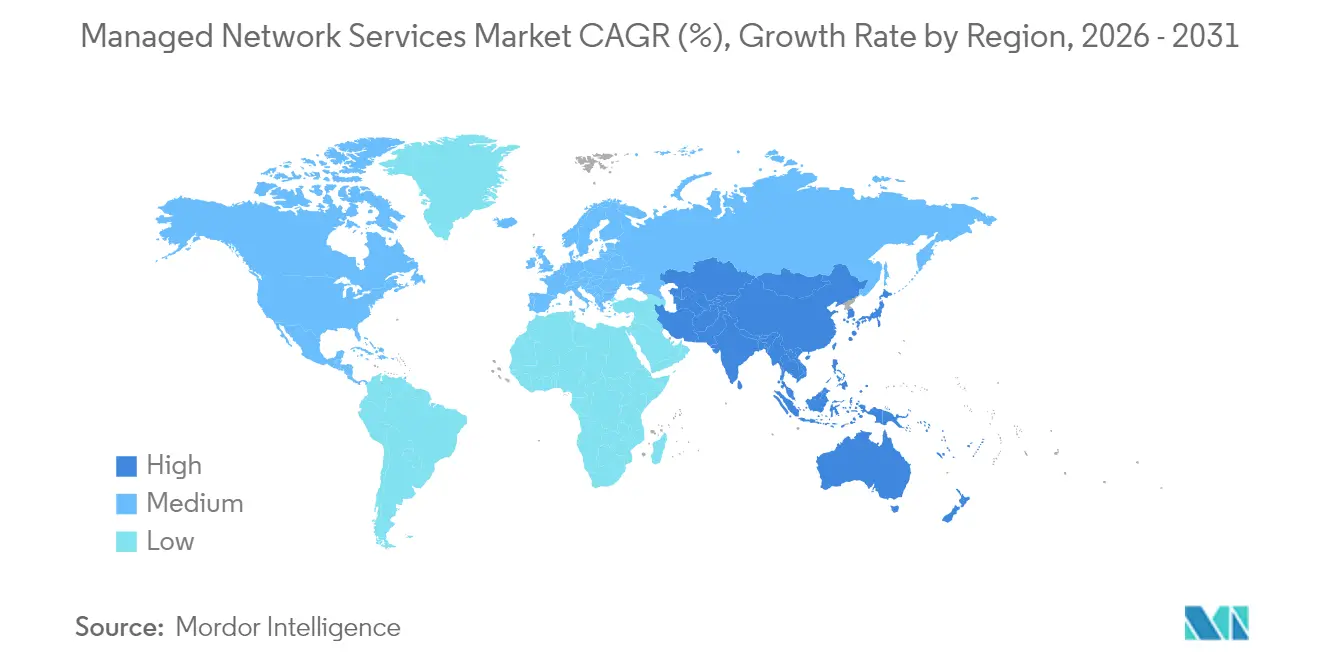

- By geography, North America accounted for 40.20% of the Network managed services market share in 2025, with the Asia-Pacific region registering the fastest growth at a 13.9% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Managed Network Services Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-saving outsourcing imperative | +1.8% | North America, Europe, global spill-over | Short term (≤ 2 years) |

| Scarcity of in-house network talent | +1.5% | North America, Western Europe | Medium term (2-4 years) |

| Surge in cloud/SaaS traffic volumes | +1.4% | Global with Asia-Pacific acceleration | Medium term (2-4 years) |

| AI-driven auto-remediation lowers SLAs | +1.2% | North America, EU core, Asia-Pacific rollout | Long term (≥ 4 years) |

| Private 5G campus rollouts | +0.8% | Manufacturing hubs worldwide | Long term (≥ 4 years) |

| EU Digital Operational Resilience Act (DORA) | +0.6% | European Union, aligned jurisdictions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cost-saving outsourcing imperative

Organizations replacing capex-intensive network ownership with opex-based managed services record 24% lower infrastructure spend and 42% higher staff productivity. [2]IBM, “The Business Value of Managed Services,” ibm.com Roughly half of adopters save at least 25% annually on IT budgets, prompting 62% of users to expand contract scope over the next 24 months. The predictable subscription model frees funds for innovation and aligns service quality to clear SLAs, making the Network managed services market a primary lever for CFO-led efficiency drives. Cloud-first SMEs amplify this trend; more than 50% already deploy AI-enabled automation that was previously unaffordable on-premise.

Scarcity of in-house network talent

The projected 75% U.S. IT labor deficit by 2034 intensifies competition for certified engineers. Enterprises struggle to maintain skills spanning SD-WAN, SASE, and zero-trust, pushing them toward providers that pool expertise across hundreds of clients. Managed service vendors invest heavily in certification programs and centralized Network Operations Centers (NOCs) to meet 24/7 coverage demands. Access to these shared resources shortens innovation cycles and reduces downtime, further enlarging the Network managed services market.

Surge in cloud and SaaS traffic volumes

AI workloads and multi-cloud architectures create unpredictable bandwidth spikes that legacy MPLS cannot accommodate. Lumen reported USD 5 billion in new AI connectivity contracts, doubling intercity backbone capacity plans. [3]Lumen Technologies, “AI Demand Drives USD 5 Billion in New Business,” lumen.com Managed service specialists leverage analytics to optimize traffic across public clouds, edge nodes, and private links, ensuring application performance without overspending on redundant circuits. As enterprise workloads migrate, managed services that dynamically scale connectivity capture a growing share of network budgets.

AI-driven auto-remediation lowers SLAs

AIOps platforms correlate millions of telemetry points to prevent incidents and slash mean-time-to-repair. Cisco’s deployments achieve sizable alert-noise reduction and downtime avoidance, underpinning SLA guarantees once deemed impossible. [4]Cisco, “Putting AI into AIOps,” cisco.com Machine learning combined with large language models delivers human-readable root-cause analyses, democratizing troubleshooting and allowing service providers to commit to “five nines” availability while trimming operational headcount.

Restraints Impact Analysis of Managed Network Services Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reluctance to outsource mission-critical nodes | −0.9% | Global, acute in regulated sectors | Medium term (2-4 years) |

| Vendor lock-in and opaque pricing models | −0.7% | EU, North America, global | Short term (≤ 2 years) |

| Energy-intensive AIOps Scope-3 emissions | −0.5% | EU, North America | Long term (≥ 4 years) |

| Edge-sovereignty mandates | −0.4% | Asia-Pacific, EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Reluctance to outsource mission-critical nodes

Financial institutions and hospitals fear third-party risk, seeing network outages as existential threats. Compliance frameworks stipulate stringent data-handling rules, leading some boards to retain in-house control over core routers. Providers counter by adopting zero-trust designs, sovereign-cloud options, and transparent incident-response playbooks, yet hesitation still trims percentage points from overall Network managed services market growth.

Vendor lock-in and opaque pricing models

Variable per-device or per-user fees ranging from USD 99 to USD 275 monthly complicate cost forecasting. Proprietary toolchains also limit portability, raising exit barriers. Regulators are now pushing for greater interoperability, and customers are increasingly demanding consumption-based, cancel-any-time contracts. Providers responding with API-rich, platform-agnostic offerings stand to regain lost momentum in the Network managed services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Managed Network Services Market Segment Analysis

By Service Type:

Software-defined momentum outpaces legacy WANManaged WAN remains the anchor at a 27.15% Network managed services market share in 2025, equating to a Network managed services market size of about USD 4.54 billion. Yet Managed SD-WAN’s 18.4% CAGR through 2031 is re-allocating budgets toward software-based overlay networks that lower costs by 30-50% compared with MPLS. Providers integrate SASE features, boosting customer stickiness through unified security and connectivity. In parallel, Managed LAN and Wi-Fi refresh cycles adopt AI-driven configuration engines that cut manual effort in half. Over the forecast window, traditional WAN revenues flatten while SD-WAN and SASE jointly exceed 40% of segment revenues, reinforcing the long-term pivot toward programmable architectures within the broader Network managed services market.

The shift also elevates managed network security demand; zero-trust mandates embed security into every service bundle, widening average contract value. Vendors such as Nile bundle secure Wi-Fi with deterministic SLAs, winning 300% revenue growth in 2024. Private 5G managed services will contribute incremental revenue late in the period as manufacturers modernize campus connectivity. Together, these trends re-draw the competitive map, favoring providers with cloud-native orchestration and multi-access edge capabilities.

By Deployment Mode:

Hybrid consumption risesOn-premise installations commanded 59.80% of the Network managed services market size in 2025, but their share erodes as cloud and NaaS models expand at an 17.6% CAGR. Consumption-based pricing aligns network spending with actual usage, resonating with CFOs who seek agility. Verizon’s NaaS subscriptions eliminate capex while delivering SLA-backed performance, prompting rapid uptake among mid-market clients.

Latency-sensitive workloads remain on-site while orchestration shifts to the cloud. Edge computing reinforces this pattern, requiring localized processing with centralized policy control. Sovereign-cloud variants address GDPR and similar mandates, removing a historical barrier to off-premise network management in Europe. Consequently, cloud-hosted control planes will oversee over 70% of enterprise ports by 2030, even as physical data paths remain diversified across branch, campus, and edge locations.

By Organization Size:

SMEs close the capability gapLarge enterprises generated 62.60% of 2025 revenues, but SMEs added the most incremental users, growing at a 13.2% CAGR and moving the Network managed services market toward democratized access to premium tooling. The average SME now runs three cloud applications, driving complexity that outstrips in-house resources. More than 60% plan to deploy generative AI within 12 months, yet only 22% retain dedicated networking staff. Managed service bundles, priced at USD 150-400 per user per month, offer enterprise-grade SLAs, security, and compliance without upfront hardware or staffing costs.

Providers craft simplified onboarding, automated ticketing, and tiered support to meet the expectations of SMEs. At the same time, large multinationals renew multi-year master service agreements to secure global coverage and unified policy enforcement, creating a dual-track market where both scalability and customer intimacy are important.

By End-User Vertical:

Healthcare outpaces BFSIBFSI institutions held 21.55% of the 2025 segment revenue because of always-on trading platforms and stringent regulatory audits under rules such as DORA. Their contracts favor redundant architectures, active-active data centers, and 15-minute recovery objectives, sustaining premium pricing. Conversely, healthcare’s 15.1% CAGR through 2031 positions it as the fastest riser, driven by telehealth, connected diagnostics, and AI-assisted care pathways that demand secure, high-capacity networks. McKinsey estimates digital health could unlock up to USD 360 billion in cost efficiencies, nudging hospital boards toward outsourced network operations.

Retail, manufacturing, and energy verticals follow suit, each embracing private 5G or edge analytics to streamline operations. Managed service providers develop vertical playbooks for pre-certified medical devices, PCI-compliant retail bundles, or IEC-62443 industrial security stacks to shorten sales cycles and ensure regulatory alignment.

Geography Analysis

North America and EMEA Managed Network Services Market

North America contributed 40.20% of 2025 revenue owing to entrenched cloud adoption, aggressive AI pilots, and a vibrant MSP ecosystem headquartered across the United States. Mature enterprises budget for proactive refresh schedules and multi-cloud optimization, funneling steady work to managed service providers. Federal sector initiatives around zero-trust also expand addressable spending. Yet growth tapers to mid-single digits as penetration reaches saturation in large accounts. Europe posts moderate expansion, buoyed by DORA-driven outsourcing among financial entities and rising sustainability mandates that favor energy-optimized managed services. Country-level data-sovereignty laws elevate demand for sovereign-cloud variants, particularly in Germany and France, adding complexity that vendors monetize through regionalized service hubs. Meanwhile, the Middle East and Africa enter an acceleration phase; national 2030 agendas and green-field smart-city projects call for turnkey network management, albeit from a lower base.

APAC Managed Network Services Market

Asia-Pacific, however, provides the standout trajectory, growing at 13.9% CAGR and accounting for an ever-larger slice of the global Network managed services market size. Hyperscale cloud players announce multi-billion-dollar data-center parks in Malaysia, Indonesia, and India, catalyzing fiber builds and managed connectivity contracts. Enterprises leapfrog legacy MPLS, deploying SD-WAN and wireless WAN from day one. Local telecom incumbents partner with global MSPs to offer unified NaaS portals, blending domestic reach with global SLA coverage. Consequently, Asia-Pacific overtakes Europe in annual new-logo count by 2027 and narrows the revenue gap by 2030.

Regulatory Landscape

Regulation affecting managed network services is tightening around resilience, third-party risk, and cybersecurity assurance, particularly where providers support critical functions. In the European Union, the Digital Operational Resilience Act (DORA) is a direct compliance driver for always-on network operations in regulated verticals, and Commission Delegated Regulation (EU) 2025/532 sets out detailed requirements for subcontracting ICT services that support critical or important functions. This affects how managed service providers structure supply chains, audit rights, and security controls in contracts.

Cybersecurity certification and common security objectives are also becoming more explicit for managed offerings. Regulation (EU) 2025/37, which amends the EU Cybersecurity Act (Regulation (EU) 2019/881), links managed security services more closely to EU-wide certification schemes, pushing providers to standardize controls and evidence for assurance. Standard-setting bodies are also shaping operational requirements for increasingly software-defined networks, including ITU-T Recommendation M.3374 (October 2025) on functional requirements for computing power network management. Together, these rules reinforce the shift toward automated, service-aware management processes in managed network operations.

Value Chain Analysis

The managed network services value chain starts with connectivity and infrastructure inputs, including enterprise LAN/WAN equipment, carrier transport and last-mile access, data center and cloud infrastructure, and security tooling. It then moves into design, integration, and lifecycle operations. Technology vendors and carriers provide the underlying platforms (SD-WAN, SASE components, observability, and automation tooling), while service providers package these capabilities into standardized service catalogs and SLAs.

Delivery is commonly anchored by centralized Network Operations Centers (NOCs) and Security Operations Centers (SOCs), supported by field services and partner ecosystems that handle site readiness, hardware logistics, and last-mile coordination. Downstream, managed service providers run ongoing monitoring, incident response, change management, and reporting, increasingly using AIOps to correlate telemetry across multi-vendor environments. Enterprises are also adopting co-managed operating models that keep policy and critical change control in-house while outsourcing 24/7 operations and complex troubleshooting. On the infrastructure side, adjacent telecom operations are developing new asset-stewardship approaches, highlighted by MD7s USD 100 million strategic equity partnership with Tikehau Star Infra announced in February 2026 to acquire and steward mobile infrastructure assets, reinforcing the value of stable, long-duration infrastructure planning and access arrangements for scalable managed services delivery.

Competitive Landscape

The competitive field sits at a moderate concentration level top five providers commanding about 45% of 2024 spend, earning a market concentration score of 6. HPE’s acquisition of Juniper exemplifies hardware-software-services convergence, enabling full-stack AI-native offerings that directly confront Cisco in both enterprise and service-provider accounts. Cisco defends its share through continuous AIOps rollouts and private 5G bundles, while also deepening MSP partnership programs for mid-market reach.

Challengers such as Nile leverage cloud-born architectures to guarantee performance “as-a-service,” targeting green-field deployments and renovation cycles alike. Kyndryl aligns with Cloudflare to pair consulting depth with globally distributed connectivity clouds, creating an enterprise on-ramp free of legacy appliance baggage. Verizon, Lumen, and AT&T are pivoting to NaaS constructs to offset legacy wireline losses, integrating SD-WAN orchestration, security, and edge computing in a single SKU.

Strategic moves continue thick and fast. Comcast Business bought Nitel to scale enterprise SD-WAN; BMC acquired Netreo to embed full-stack observability into its Helix platform. Private-equity roll-ups such as Shield Technology Partners consolidate regional MSPs, building national footprints with centralized tooling. Providers able to combine AI-assisted operations with transparent consumption pricing gain competitive headroom in an environment where vendor lock-in skepticism runs high.

Managed Network Services Industry Leaders

IBM

HCL Technologies Limited

Dell

Verizon

Accenture PLC

- *Disclaimer: Major Players sorted in no particular order

Managed Network Services Market Companies Covered in this Report

- Amazon Web Services (Amazon Connect)

- NICE Ltd.

- Genesys Telecommunications Laboratories Inc.

- Five9 Inc.

- Cisco Systems Inc.

- RingCentral Inc.

- 8x8 Inc.

- Avaya LLC

- Talkdesk Inc.

- Vonage Holdings Corp.

- Twilio Inc.

- Dialpad Inc.

- Content Guru Limited

- Mitel Networks Corporation

- Odigo SAS

- Aspect Software Group Ltd.

- Alvaria, Inc.

- Sprinklr Inc.

- SAP SE

- Zoom Video Communications Inc.

Market Opportunities and Future Outlook

Large, multi-year transformation deals and public-sector contract vehicles are expanding managed network services from device management toward full operational ownership within Network-as-a-Service constructs. In June 2026, WidePoint was selected as the single awardee for the U.S. Department of Homeland Security Cellular Wireless Managed Services (CWMS) 3.0 contract with a ceiling value of up to USD 3.1 billion over 10 years, indicating demand for managed mobility and carrier governance at scale. In July 2026, Tata Consultancy Services secured a multi-year, AI-led network operations contract with ABB using a NaaS model, reflecting enterprise demand for consolidated global operations, automation, and standardized service delivery across sites.

A second opportunity area is the convergence of networking and security into unified managed SASE offers with clearer SLAs and simplified procurement. Customers facing vendor lock-in and opaque pricing are pushing providers toward platform-agnostic operations, API-led integration, and measurable outcomes (availability, incident response, and policy compliance) that can be audited across multi-cloud and branch environments. This helps create whitespace for providers that can operationalize AI-assisted remediation while still meeting governance artifacts required by regulated verticals, including third-party risk controls for subcontractors and contract-ready reporting for resilience and security obligations.

Recent Industry Developments in Managed Network Services Market

- July 2026: Tata Consultancy Services (TCS) secured a multi-year contract with ABB to modernize and run global network operations using a Network-as-a-Service model and AI-driven automation. The deal points to a shift in buyer preference toward end-to-end operational responsibility and standardized global service delivery, with automation-led execution replacing standalone device management.

- July 2025: Hewlett Packard Enterprise closed its acquisition of Juniper Networks for about USD 14 billion, combining portfolios across networking and software. The consolidation strengthened full-stack offerings that pair infrastructure with AI-native operations, increasing competitive pressure on providers that rely on narrower, tool-led managed service propositions.

- April 2024: Accenture completed its acquisition of Fibermind to strengthen fiber and mobile 5G network services capabilities. The acquisition expanded Accenture’s engineering and deployment depth in telecom networks, supporting managed service engagements that combine build, modernization, and ongoing operations across fixed and wireless domains.

Managed Network Services Market Report Scope and Research Methodology

Market Definition and Coverage

In this methodology, the network managed services market is defined as third-party, contract-based services that monitor, manage, and optimize enterprise network environments. This includes managed LAN, WAN, Wi-Fi, and managed network security, along with the related service revenue billed to customers.

Scope exclusions: we exclude pure one-time product sales of routers, switches, and similar hardware when they are not bundled into a managed service contract.

Segments Covered in This Report

- By Service Type

- Managed LAN

- Managed WAN

- Managed Wi-Fi

- Managed Network Security

- Managed SD-WAN

- By Deployment Mode

- On-premise

- Cloud / NaaS

- By Organization Size

- Small and Medium Enterprises

- Large Enterprises

- By End-user Vertical

- BFSI

- IT and Telecom

- Healthcare and Life-Science

- Retail and eCommerce

- Manufacturing

- Education

- Energy and Utilities

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with public data that helps explain the demand pool for outsourced network operations and how it is changing by region and industry. We reviewed sources such as the FCC and national telecom regulators, ITU indicators, the World Bank, OECD broadband and enterprise digitization datasets, and NIST cybersecurity guidance to establish baseline connectivity and security needs. We also used annual reports, earnings decks, and contract announcements from service providers and large enterprise buyers to map typical contract structures and service boundaries.

To avoid building the model on one narrow dataset, we cross-checked pricing direction and deal momentum using reputable press coverage, association publications, and publicly available procurement and tender notices where relevant. In a few cases, paid subscriptions were used only for company financials and news screening, plus patent databases to track networking and security feature directions that can influence service mix. The desk research sources listed here are illustrative, and additional public and paid references were used for validation and clarification during the work.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with managed service providers, network operations leaders at end users, system integrators, and channel partners who see deal scope and renewals firsthand. We used this to confirm which services are counted as managed network services versus adjacent IT outsourcing, and to sanity check typical contract terms, renewal uplifts, and how security components are priced. For this global market, inputs were balanced across key regions so assumptions held up across different connectivity maturity levels and enterprise adoption patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 21% | APAC: 46% |

| Mid tier: 45% | Functional/Unit leaders: 29% | EMEA: 36% |

| Smaller Players: 22% | Managers: 50% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where enterprise connectivity and network operations demand was reconstructed from region-level IT and telecom spend signals. That total demand pool was then filtered by the share that is typically outsourced into managed contracts. Once that demand pool was shaped, it was split into managed LAN, WAN, Wi-Fi, and managed network security using service mix cues from interviews and publicly visible portfolio and contract language. To keep totals realistic, we corroborated the results with selective bottom-up approximations, including sampled provider revenue disclosures where available, channel checks on deal sizes, and a simple ASP x site or user-volume logic for common managed components.

Key model inputs included indicators such as enterprise broadband and IP traffic growth, the shift toward SD-WAN and cloud-connected branch architectures, security-driven scope expansion in contracts, renewal timing patterns, and region-level wage and operating cost pressure that influences outsourcing decisions. Forecasting relied mainly on scenario analysis, supported by a light multivariate regression view for directional checks. Adoption rates, contract duration trends, and pricing escalation assumptions were varied and then re-anchored to expert feedback. When bottom-up signals were incomplete, gaps were handled by using conservative mix assumptions, then re-testing totals against independent demand indicators before finalizing.

Data Validation & Update Cycle

Outputs were validated through multiple rounds of cross-checks, starting with simple variance tests across regions and service types so unusually high shares or sudden jumps were flagged early. We compared the final market totals with independent signals such as provider commentary on bookings and renewals, public contract cadence, and broad connectivity and security spending direction, then adjusted assumptions where the story did not match the data. A second analyst review was used to challenge the boundary of what is counted as managed network services, and respondents were re-contacted when major mismatches showed up.

Reports are refreshed annually, and interim updates are made when material events can shift pricing, contract scope, or demand patterns. Before delivery, a final pass is completed so the latest public information and any late-stage expert feedback are reflected in the numbers.

Mordor Intelligence's Network Managed Services Market Estimate Compared With Other Published Estimates

Published market sizes for managed network services often do not line up because the service boundary is drawn differently and the timing assumptions are not the same. Some estimates treat adjacent IT outsourcing items as part of the same bucket, while others pull hardware pass-through revenue into services, which can inflate the total.

A refresh-led gap shows up when currency conversion timing, annualized contract value treatment, and ASP uplift assumptions are handled inconsistently across updates. By re-checking renewal uplifts and FX timing during each refresh cycle, and only applying price progression when it is supported by interview validation, Mordor Intelligence keeps the 2025 value tied to what customers typically pay for managed LAN, WAN, Wi-Fi, and managed network security.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 16.73 B (2025) | |

| Global Consultancy A | USD 81.76 B (2025) | Uses a broader revenue definition that can include design, implementation, and related goods bundled with services, which expands the counted value beyond managed network operations scope. |

| Industry Research Group B | USD 82.89 B (2025) | Appears to aggregate a wider set of managed offerings, including adjacent connectivity and security items, and may annualize large multi-year contracts differently, which raises the stated 2025 total. |

The spread in the table is mainly explained by scope and timing choices rather than a true disagreement on demand direction. When service boundaries are kept tight and pricing is annualized in a consistent way, the resulting market size becomes easier to trace back to clear inputs and to replicate for planning.

Key Questions Answered in the Report

How big will the Network managed services market be by 2031?

It is projected to reach USD 32.88 billion, expanding at a 11.92% CAGR between 2026-2031.

Which service type is growing fastest?

Managed SD-WAN services are forecast to grow at 18.4% CAGR as organizations shift from MPLS to software-defined connectivity.

Why are SMEs adopting managed network services so quickly?

Cloud-first strategies and limited in-house talent push SMEs toward subscription bundles that deliver enterprise-grade security and automation at predictable costs.

What role does AI play in managed network operations?

AIOps platforms automate incident detection and remediation, enabling providers to guarantee higher SLAs while reducing operational overhead.

Page last updated on: