Extended Detection And Response Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

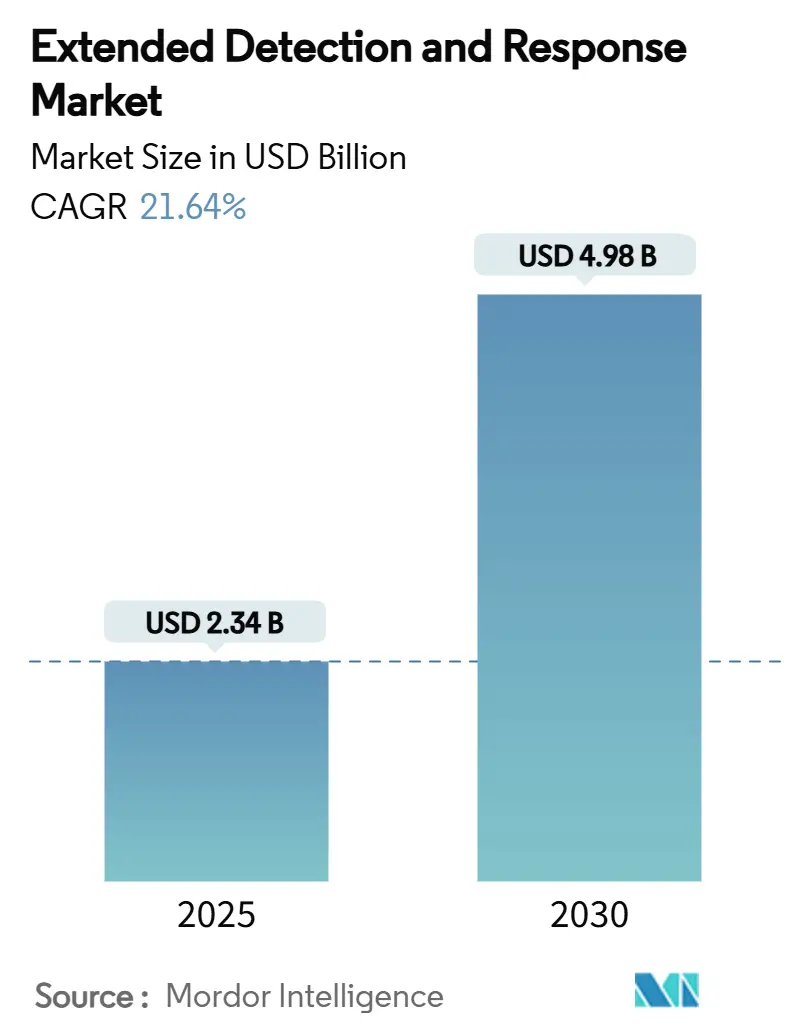

| Market Size (2025) | USD 2.34 Billion |

| Market Size (2030) | USD 4.98 Billion |

| Growth Rate (2025 - 2030) | 21.64% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Extended Detection And Response Market Analysis by Mordor Intelligence

The Extended Detection and Response market size is valued at USD 2.34 billion in 2025 and is projected to reach USD 4.98 billion by 2030, expanding at a 21.64% CAGR during the forecast period. This fast-rising trajectory reflects mounting pressure on enterprises to consolidate threat detection across endpoints, networks, cloud workloads, and identities into a single analytics layer that can keep pace with multi-vector attacks. AI-powered analytics, tighter breach-disclosure regulations, and steep cyber-insurance premiums are accelerating platform uptake, while the collapse of traditional Security Operations Center and Network Operations Center silos is reshaping operating models. Cloud-first deployment remains dominant, yet hybrid models gain momentum as organizations strive to reconcile data-sovereignty mandates with the need for global telemetry correlation. Competitive intensity is building as leading vendors pursue acquisitions and platform unification strategies to curb tool sprawl and deliver end-to-end response orchestration.

Key Report Takeaways

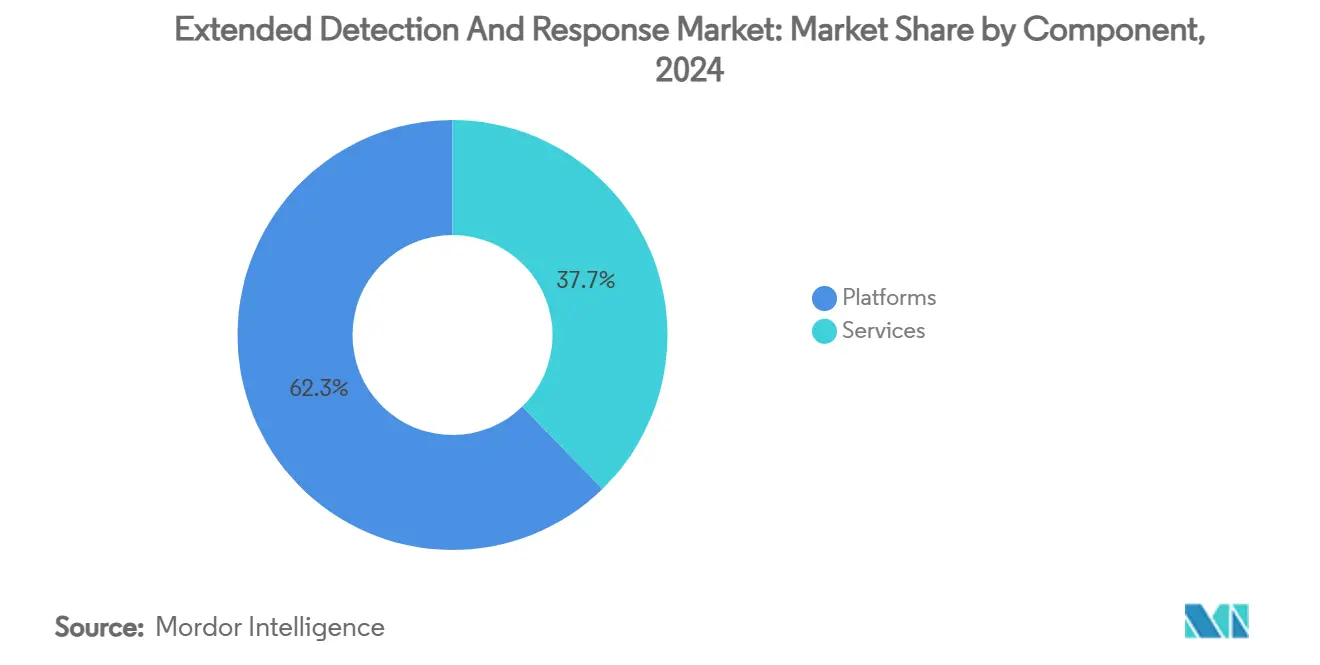

- By component, Platforms held 62.3% revenue share of the Extended Detection and Response market in 2024, whereas Services are forecast to advance at a 25.1% CAGR to 2030, underscoring demand for managed offerings.

- By deployment mode, Cloud-based solutions commanded 71.4% share in 2024; Hybrid deployments are the fastest-growing at 26.1% CAGR through 2030 as firms balance visibility with data-residency obligations.

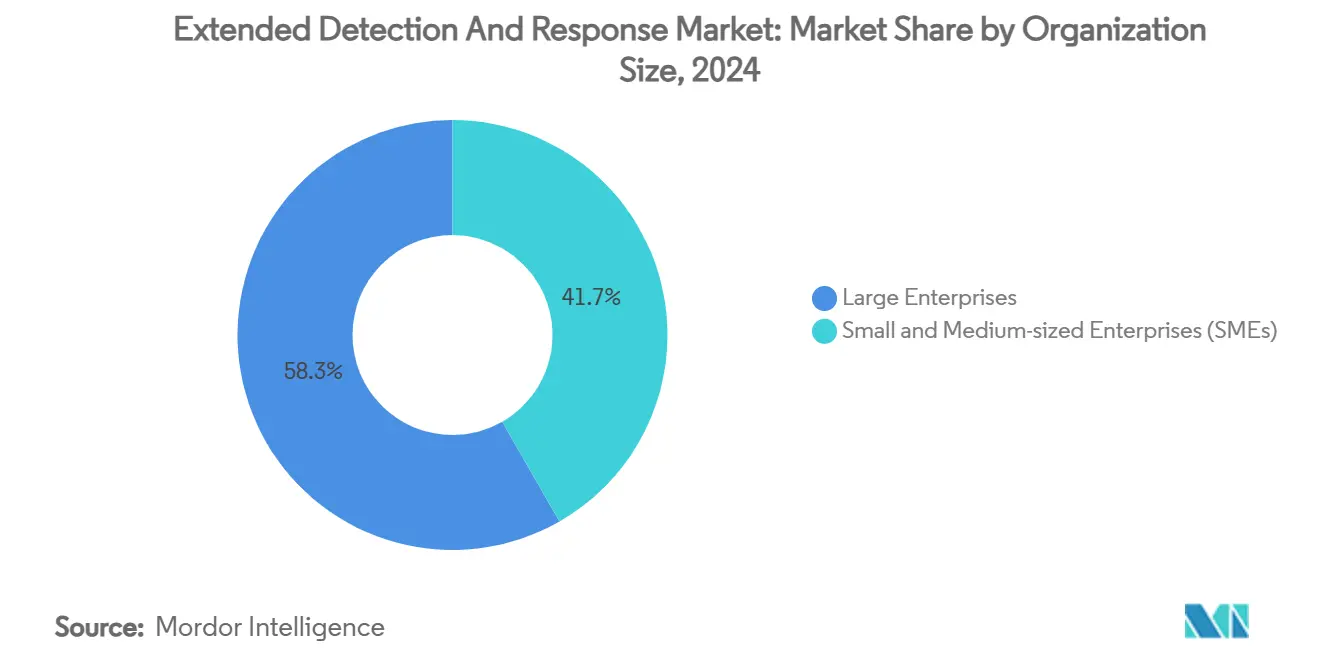

- By organization size, Large Enterprises accounted for 58.3% adoption in 2024, while SMEs are set to grow at a 27.1% CAGR on the back of cloud-native ease of use.

- By end-user industry, BFSI led with 24.1% share of the Extended Detection and Response market size in 2024; Healthcare and Life Sciences is poised for a 23.1% CAGR to 2030.

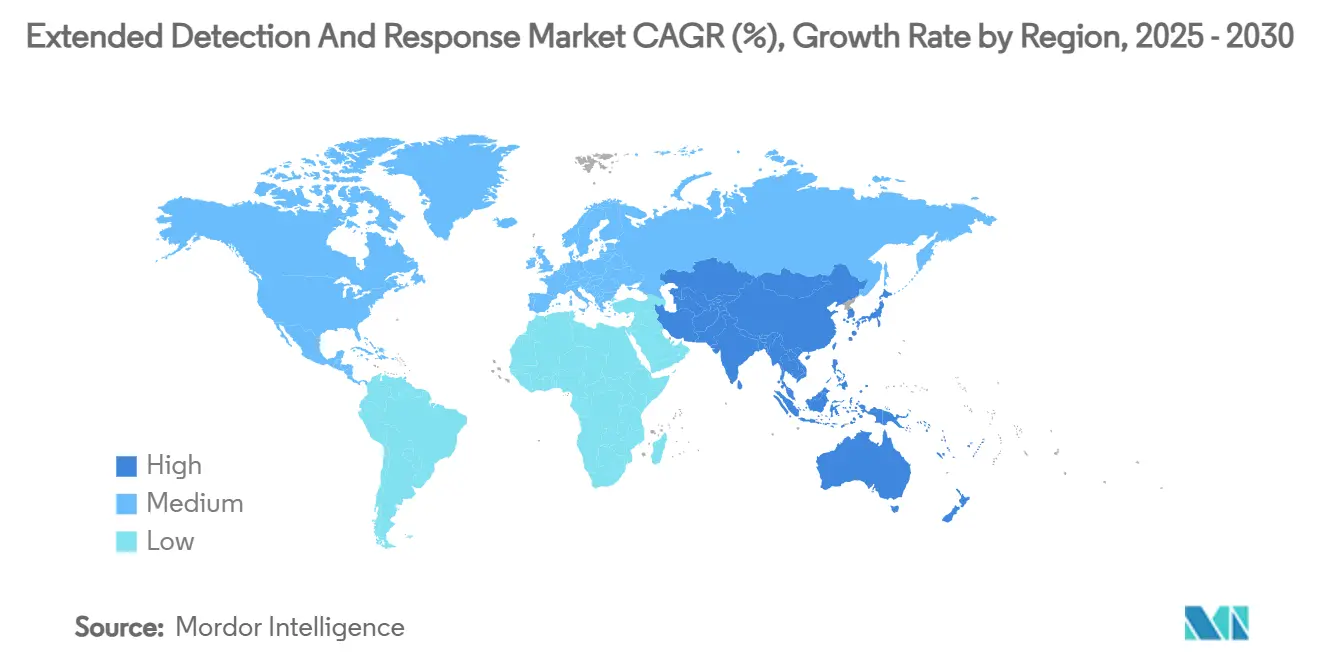

- By geography, North America dominated with a 42.2% share in 2024, whereas Asia-Pacific is projected to accelerate at a 19.1% CAGR over the same horizon.

Global Extended Detection And Response Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-driven threat analytics demand | +4.2% | Global, led by North America and Europe | Medium term (2-4 years) |

| Surge in complex multi-vector cyber-attacks | +3.8% | Global, highest in BFSI, and critical infrastructure | Short term (≤ 2 years) |

| Convergence of SOC and NOC operations | +2.9% | North America and the EU, expanding to the Asia-Pacific | Medium term (2-4 years) |

| Regulatory mandates for breach disclosure | +3.1% | North America and the EU, spillover to the Asia-Pacific | Short term (≤ 2 years) |

| Need for unified telemetry across hybrid estates | +2.7% | Global, multi-cloud enterprises | Medium term (2-4 years) |

| Cyber-insurance premium optimization | +1.8% | North America and the EU, emerging in the Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-driven Threat Analytics Demand

Organizations are adopting Extended Detection and Response platforms to convert billions of daily signals into prioritized incidents through machine learning that short-circuits analyst overload. Microsoft’s security operations environment processes 78 trillion signals every day, using generative AI to filter noise and surface high-fidelity threats.[1]Microsoft, “Cybersecurity Incident Correlation in the Unified Security Operations Platform,” techcommunity.microsoft.com The vendor’s Phishing Triage Agent illustrates the shift toward autonomous investigations that compress dwell time from hours to minutes. Banking executives rank fraud detection as their top generative-AI use case, driving strong Extended Detection and Response market uptake in financial services. Agentic AI, which enables self-learning response playbooks, is now a key R&D focus as vendors rush to neutralize AI-enabled adversaries in real time. The momentum underscores an industry consensus that only AI-native telemetry correlation can keep pace with evolving attacker tradecraft.

Surge in Complex Multi-vector Cyber-attacks

Attackers increasingly chain endpoints, email, cloud workloads, and operational technology into synchronized campaigns designed to slip past point solutions. ENISA recorded ransomware and DDoS as the two most reported incident types in 2024, noting a sharp rise in Cybercrime-as-a-Service toolkits that coordinate simultaneous vectors. Manufacturing suffered a 33% jump in cybercrime losses as threat actors exploited IT-OT convergence points to magnify disruption. Reserve Bank of India monitoring detected 400 million malware instances during 2023, highlighting the scale of multi-vector targeting of financial systems. Recorded Future found AI-generated phishing volumes surging 1,265%, evidencing adversaries’ embrace of generative content to stage convincing, multi-stage attacks. These trends raise the bar for correlation depth and speed, pushing Extended Detection and Response market adoption toward platforms able to resolve disparate security events into a single incident narrative.

Convergence of SOC and NOC Operations

The traditional firewall between Security Operations Centers and Network Operations Centers is dissolving as organizations recognize that performance anomalies can signal security threats. Cisco’s demonstration at Black Hat 2024 showed how embedding XDR telemetry in NOC workflows revealed malware activity that would have remained invisible to isolated SOC tooling. Early adopters are building Security Network Operations Centers to pool budgets, slash mean-time-to-detect, and align incident response with business-service availability. Industrial operators such as energy utilities are extending convergence into operational technology networks, enabling zero-trust policy enforcement across plant-floor assets. The resulting unified telemetry fabric is emerging as a core architectural principle for Extended Detection and Response market deployments.

Regulatory Mandates for Breach Disclosure

Faster breach-notification laws are forcing boards to verify they can detect, scope, and disclose material incidents within days. The United States Securities and Exchange Commission now requires public companies to file an incident 8-K within four business days, a timeline that manual investigation cannot meet. Europe’s NIS2 Directive and sector-specific rules in finance, healthcare, and energy likewise demand near-real-time situational awareness. Critical-infrastructure operators must also adhere to the Cyber Incident Reporting for Critical Infrastructure Act, intensifying pressure to deploy automated threat-correlation engines. These mandates are expanding the addressable Extended Detection and Response market because only integrated platforms can supply the audit-ready forensics that regulators expect.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of XDR-skilled cybersecurity workforce | -2.8% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Data sovereignty and residency concerns | -1.9% | EU and Asia-Pacific with strict localization | Long term (≥ 4 years) |

| Tool sprawl and integration complexity | -1.6% | Global, large enterprises | Short term (≤ 2 years) |

| Adversary use of GenAI to evade detection | -1.3% | Global, advanced economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of XDR-skilled Cybersecurity Workforce

A global shortfall of 4.8 million cybersecurity professionals leaves many organizations unable to staff Extended Detection and Response programs adequately.[2]ISC2, “The State of the Cybersecurity Workforce 2024,” isc2.org ISC2 data show the skills gap widened 19% during 2024, while workforce growth was virtually flat. XDR expertise is even rarer because analysts must combine threat hunting, correlation logic, and response automation skills seldom taught in traditional security curricula. Boston Consulting Group notes that only 72% of advertised cyber roles are filled, compelling enterprises to outsource to managed XDR providers or rely on AI assistants to lighten analyst workloads. Cisco research finds that AI chat interfaces within XDR consoles reduce triage time and analyst burnout, yet high-severity incidents still require human oversight. This talent bottleneck slows adoption and constrains the Extended Detection and Response market growth outlook.

Data Sovereignty and Residency Concerns

Regulators are asserting digital sovereignty, insisting that sensitive telemetry remain inside national borders. The European Union’s stance pushes enterprises toward hybrid Extended Detection and Response deployments that maintain local storage while selectively sharing indicators of compromise. Thales reports that encryption-key ownership and location have become board-level priorities, forcing platform vendors to support Bring-Your-Own-Key models and granular retention policies. Security teams worry that restricting data movement will blind correlation engines that rely on global context, potentially degrading detection efficacy. Wallarm underscores the tension between GDPR compliance and advanced threat hunting that demands cross-border log analysis. These constraints spur innovation in federated analytics but temper near-term Extended Detection and Response market expansion, especially in highly regulated sectors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platforms Remain Foundational, Services Accelerate

Platforms anchored 62.3% of 2024 revenue as organizations prioritized unified telemetry correlation to replace siloed toolsets. The Extended Detection and Response market share dominance stems from Microsoft, Palo Alto Networks, and CrowdStrike bundling endpoint, network, and cloud analytics into single consoles that achieve 99% correlation accuracy while cutting storage needs by 7.4×. Simultaneously, Services are slated for a 25.1% CAGR through 2030, propelled by Managed XDR offerings that address the acute workforce gap. Professional-services teams support data migration from legacy SIEM deployments, develop custom detection logic, and provide 24 × 7 response orchestration—capabilities most enterprises cannot staff internally. As vendor roadmaps emphasize out-of-the-box automation, services partners will shift toward continuous tuning and specialized threat hunting rather than basic platform operation.

The Services upsurge aligns with growing preference for outcome-based contracting, allowing security leaders to benchmark providers on incident-containment metrics instead of technology stacks. Red Canary’s collaboration with Palo Alto Networks to deliver Managed XSIAM exemplifies service-led value creation tailored to mid-market budgets. Platform suppliers respond by embedding low-code playbook builders and AI copilots, lowering entry barriers for in-house teams and further broadening the Extended Detection and Response market.

By Deployment Mode: Hybrid Models Gain Strategic Relevance

Cloud-based solutions dominated 71.4% of 2024 spend thanks to elastic scaling, centralized updates, and quick time-to-value. However, Hybrid configurations are projected to grow 26.1% annually as enterprises confront residency rules and sensitive-data controls. Microsoft’s multi-tenant management update illustrates how cloud-native consoles can federate incident oversight while enabling local log retention where policy demands. On-premises remains essential for critical-infrastructure operators that maintain air-gapped networks or require deterministic latency.

Hybrid architectures typically split telemetry storage—retaining high-sensitivity logs on-premises while forwarding metadata to cloud analytics engines. This design lets organizations satisfy compliance without sacrificing global threat-intel enrichment, steering extended Detection and Response market evolution toward flexible data-fabric capabilities. Vendors able to demonstrate sovereign-cloud zones and customer-managed encryption keys will command a competitive edge among regulated buyers.

By Organization Size: Democratization Drives SME Uptake

Large Enterprises accounted for 58.3% of 2024 adoption, leveraging the Extended Detection and Response market size advantages to integrate multiple clouds, data centers, and OT environments. Yet SMEs now register a 27.1% CAGR because cloud-native licensing tiers remove heavy infrastructure prerequisites and bundle best-practice detections. Stellar Cyber and Judy Security’s partnership packages enterprise-grade open XDR for managed-service providers, delivering fixed-fee SOC capabilities that align with small-business budgets.

SMEs increasingly recognize that sophisticated threat actors target supply-chain partners irrespective of scale. Cloud subscriptions with automated playbooks, curated detections, and embedded AI assistants pare analyst hours to levels sustainable for lean teams. As vendors refine multi-tenant dashboards and usage-based pricing, the Extended Detection and Response industry is set to mirror SaaS adoption curves observed in CRM and collaboration tooling.

By End-User Industry: Healthcare Surges, BFSI Retains Lead

BFSI held 24.1% revenue share in 2024 as banks pursue fraud analytics, regulatory compliance, and cyber-insurance qualification. The sector relies on Extended Detection and Response market capabilities to reconcile transaction monitoring with behavioral analytics, delivering early payment-fraud detection across account, device, and network layers. Healthcare and Life Sciences, meanwhile, posts a 23.1% CAGR through 2030, fuelled by electronic-medical-record digitization and ransomware targeting. Deloitte notes Indian hospitals now allocate up to 10% of IT budgets to cybersecurity, with forecasts reaching 15% by 2027.

Manufacturing uptake accelerates as IT-OT convergence exposes legacy industrial control systems. Energy utilities prioritize zero-trust segmentation across grid assets, relying on XDR to fuse operational-technology logs with corporate IT events. Retail and eCommerce platforms adopt XDR to secure peak-season transactions and protect loyalty data. This sectoral diversity broadens addressable demand, anchoring long-term Extended Detection and Response market resilience.

Geography Analysis

North America retained a 42.2% share in 2024 owing to stringent disclosure mandates and early vendor presence. SEC four-day reporting rules drive rapid investment in incident-materiality assessment engines built into XDR consoles. Financial institutions such as Capital One apply AI-native threat analytics to shorten dwell times, reinforcing regional leadership.[3]Everest Group, “The BFS Sector in 2025,” everestgrp.com Workforce scarcity remains acute, yet managed XDR adoption offsets staffing gaps and sustains Extended Detection and Response market momentum.

Asia-Pacific is forecast to grow at a 19.1% CAGR to 2030, powered by accelerated cloud adoption, cyber-insurance clauses, and digital-infrastructure spending. NTT DATA reports 58% of regional banks exploring generative-AI security use cases, catalyzing XDR deployments. Indian hospitals face some of the world’s highest cyber-attack volumes, prompting security budgets to scale rapidly. Manufacturing exporters adopt hybrid XDR to secure globally dispersed plants while meeting local data-sovereignty laws. Government-funded critical-infrastructure programs further enlarge the Extended Detection and Response market base.

Europe grows steadily under the NIS2 Directive and GDPR. Data-residency imperatives nurture hybrid architectures and domestic cloud zones. Vendors providing customer-controlled encryption keys win share, while managed-service providers bridge skills shortages in smaller markets. South America and the Middle East, and Africa trail in absolute numbers but register rising adoption through subscription-based managed XDR that bypasses up-front capital outlays. Cross-regional threat-intelligence sharing remains a constraint, yet the appeal of unified detection continues to lift overall Extended Detection and Response market demand.

Competitive Landscape

The market is moderately fragmented yet consolidating as leaders expand portfolios through acquisition. Microsoft, Palo Alto Networks, and CrowdStrike enhance economies of scale by integrating endpoint, network, identity, and cloud telemetry on unified data fabrics. Sophos closed its USD 859 million Secureworks purchase in February 2025 to bolster mid-market offerings.[4]CRN, “Sophos Closes $859M Acquisition of Secureworks,” crn.com Cisco’s USD 28 billion Splunk buy signals a broader trend toward merging SIEM and XDR stacks for end-to-end visibility.

Strategic alliances deepen channel reach: CrowdStrike collaborates with Google Cloud, Dell, and HCLTech to deliver managed detection and response bundles. Vendors emphasize AI-native engines that automate 80-90% of triage tasks, positioning human analysts for strategic hunting. Disruptors push open-architecture models to differentiate against vertically integrated incumbents. Industry-specific variants focusing on operational technology and mid-market simplicity create white-space growth vectors.

Platform vendors compete on data-ingestion cost, playbook catalog breadth, and multitenant role-based access suited for service-provider environments. Partner ecosystems and marketplace integrations increasingly influence buyer decisions as tool-consolidation initiatives aim to cut license overhead. The Extended Detection and Response market trajectory thus hinges on balancing consolidation with the flexibility needed to ingest diverse telemetry and adapt to evolving compliance regimes.

Extended Detection And Response Industry Leaders

Palo Alto Networks Inc.

Microsoft Corporation

CrowdStrike Holdings Inc.

Cisco Systems Inc.

Trend Micro Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Sophos completed its USD 859 million acquisition of Secureworks, integrating the Taegis XDR platform to extend mid-market coverage, combining vulnerability and identity threat detection with existing controls.

- February 2025: Kaspersky launched “Kaspersky Next,” a three-tier suite blending endpoint protection, EDR, and XDR capabilities for cloud and on-premise deployments to counter ransomware and data-breach pressures.

- January 2025: Darktrace and Xage Security partnered to merge AI-driven anomaly detection with zero-trust access, strengthening critical-infrastructure defenses across OT and IT estates.

- November 2024: N-able bought Adlumin for USD 250 million, adding cloud-native XDR and managed detection to unify security services for IT providers.

Global Extended Detection And Response Market Report Scope

| Platforms |

| Services |

| Cloud-based |

| On-Premises |

| Hybrid |

| Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| IT and Telecom |

| Government and Defense |

| Retail and eCommerce |

| Manufacturing |

| Energy and Utilities |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Platforms | ||

| Services | |||

| By Deployment Mode | Cloud-based | ||

| On-Premises | |||

| Hybrid | |||

| By Organization Size | Small and Medium-sized Enterprises (SMEs) | ||

| Large Enterprises | |||

| By End-User Industry | Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | |||

| IT and Telecom | |||

| Government and Defense | |||

| Retail and eCommerce | |||

| Manufacturing | |||

| Energy and Utilities | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the Extended Detection and Response market?

The Extended Detection and Response market size stands at USD 2.34 billion in 2025, with a forecast to reach USD 4.98 billion by 2030.

What is the projected CAGR for the Extended Detection and Response market between 2025 and 2030?

The market is expected to grow at a 21.64% CAGR over the forecast period.

Which deployment model is growing fastest in the Extended Detection and Response market?

Hybrid deployments are expanding at a 26.1% CAGR as organizations balance cloud efficiency with data-sovereignty requirements.

Which industry segment leads the Extended Detection and Response market?

BFSI currently holds the largest share at 24.1%, driven by fraud-detection priorities and regulatory compliance needs.

Why are SMEs increasingly adopting Extended Detection and Response solutions?

Cloud-native platforms and XDR-as-a-Service models lower cost and skills barriers, enabling SMEs to access enterprise-grade threat detection and response.

Which region is expected to see the fastest growth in the Extended Detection and Response market?

Asia-Pacific is projected to advance at a 19.1% CAGR through 2030, led by digital-transformation spending and emerging regulatory mandates.

Page last updated on: