Lycopene Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 168.5 Million |

| Market Size (2031) | USD 217.73 Million |

| Growth Rate (2026 - 2031) | 5.26% CAGR |

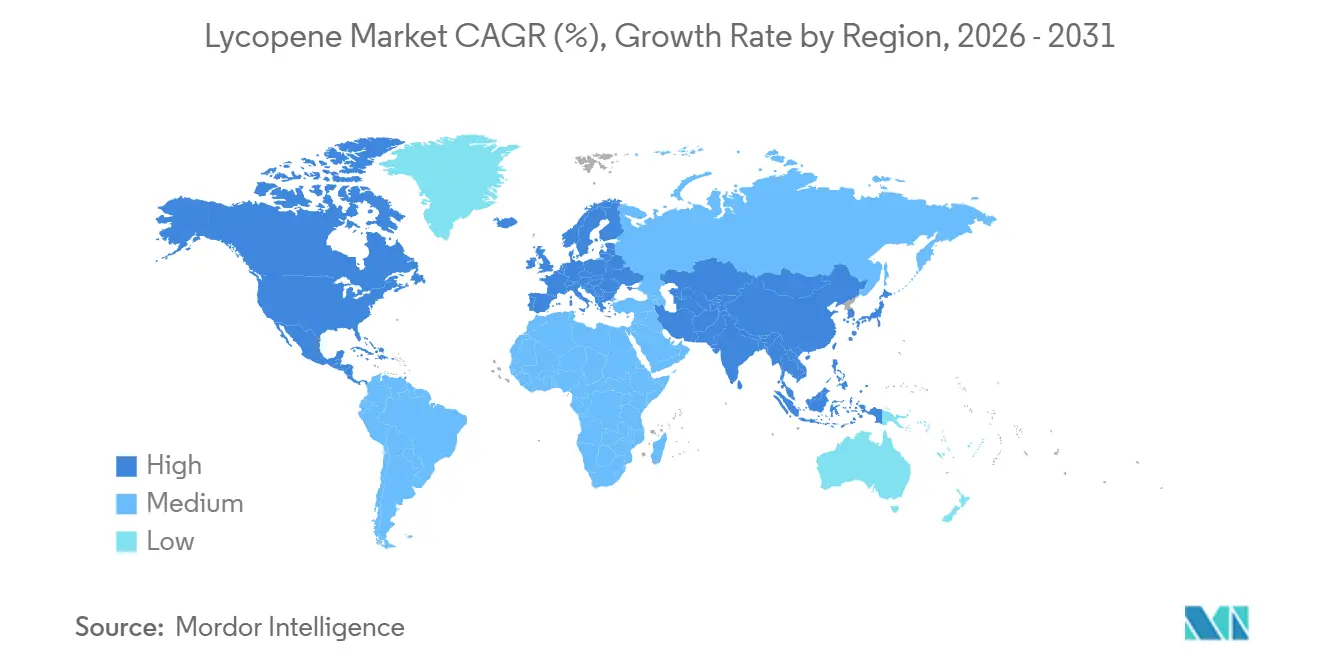

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Lycopene Market Analysis by Mordor Intelligence

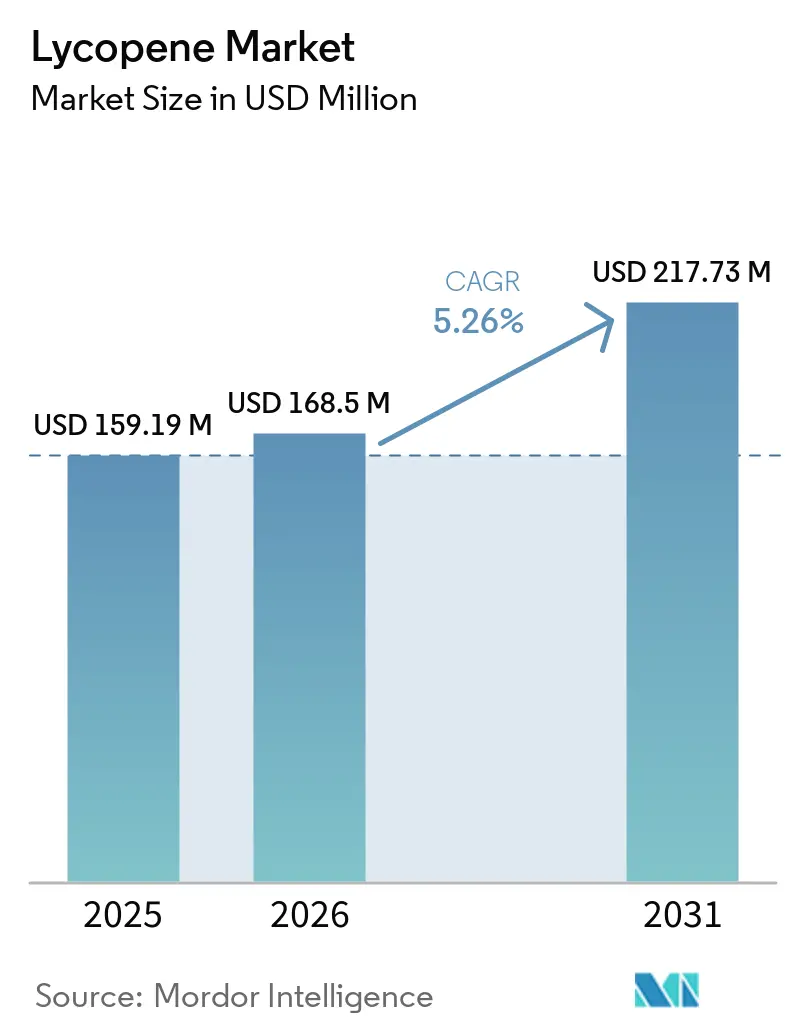

The lycopene market was valued at USD 159.19 million in 2025 and reached USD 168.50 million in 2026. It is projected to grow to USD 217.73 million by 2031, registering a CAGR of 5.26% during the forecast period of 2026-2031. The market's growth is driven by three key factors: the increasing replacement of petroleum-based dyes with natural colorants due to regulatory pressures, the premiumization of ingredients in the dietary supplement segment, and the expanding cross-application use of lycopene in nutricosmetics. Regulatory bodies are increasingly imposing restrictions on synthetic dyes, prompting manufacturers to adopt natural alternatives like lycopene. Additionally, the rising consumer preference for high-quality, natural, and functional ingredients in dietary supplements is further boosting demand. The growing popularity of nutricosmetics, which combine nutrition and cosmetics, has also opened new avenues for lycopene applications.

Key Report Takeaways

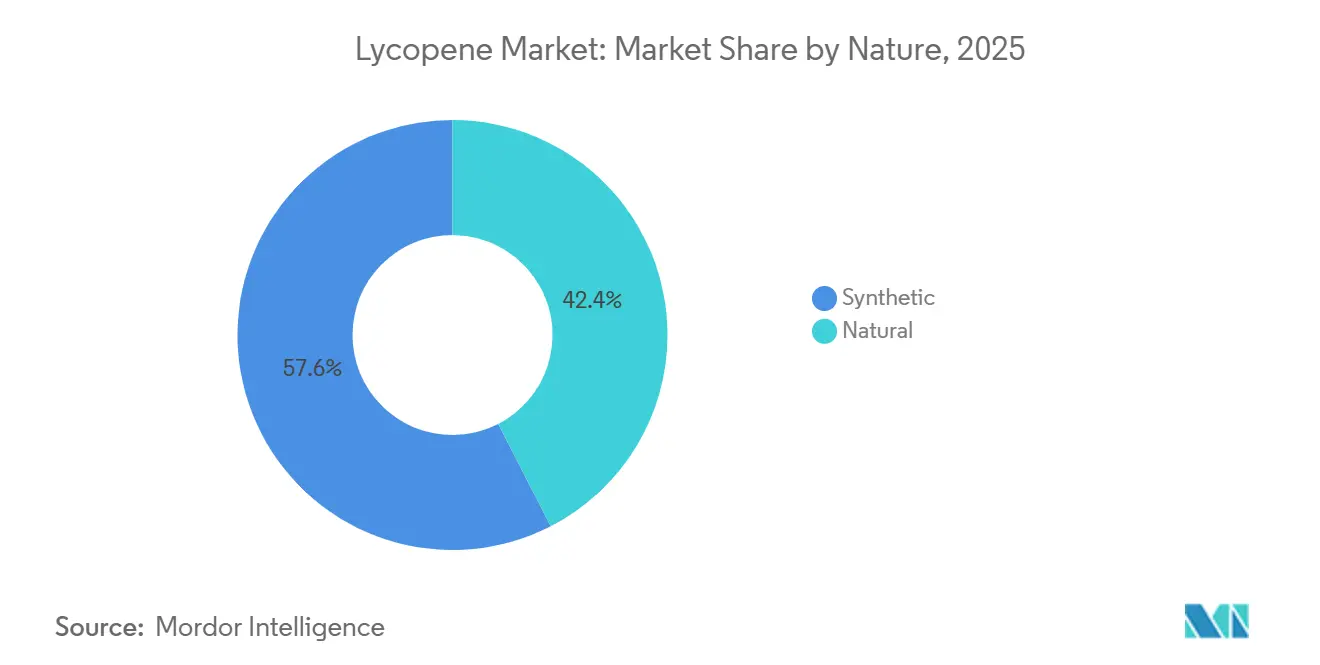

- By nature, the synthetic segment accounted for 57.56% of 2025 revenue, while natural will post a 6.94% CAGR through 2031.

- By form, the powder segment accounted for 46.81% of 2025 revenue, while liquid will post a 6.53% CAGR through 2031.

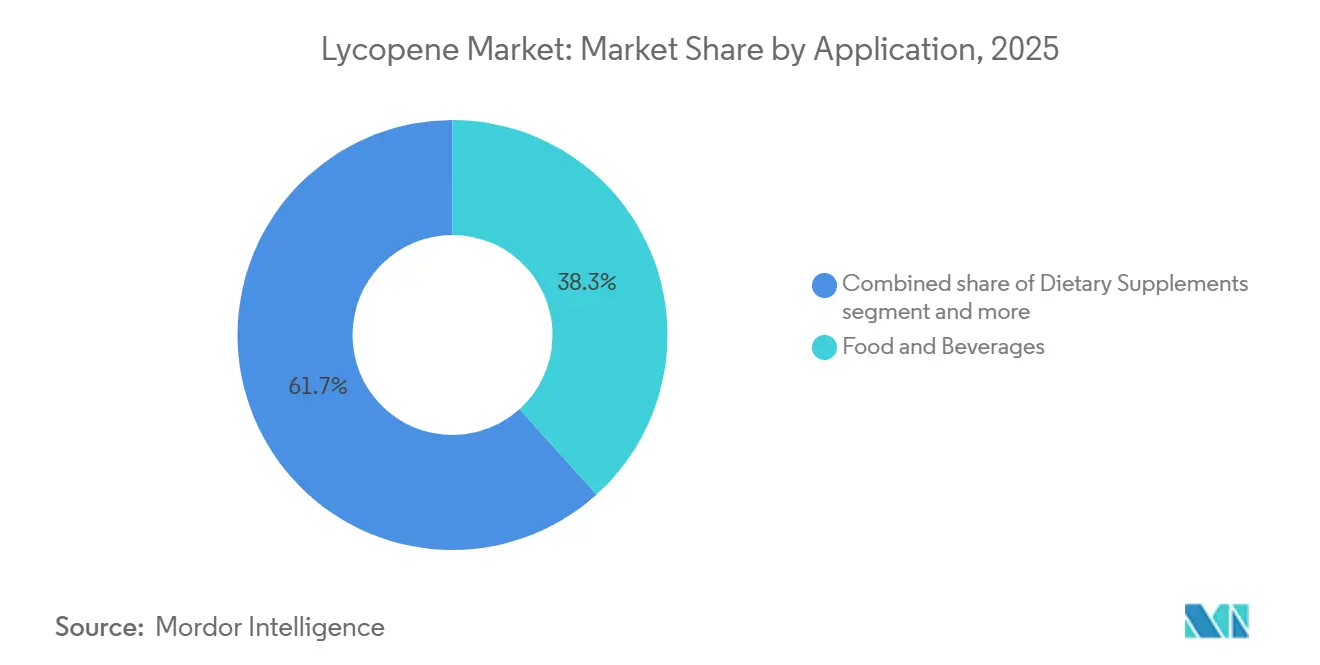

- By application, food and beverages accounted for 38.31% of 2025 demand, whereas dietary supplements are forecast to grow at a 7.76% CAGR through 2031.

- By geography, North America accounted for 40.75% of 2025 sales, while Asia-Pacific will expand at a 7.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lycopene Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for clean-label antioxidant ingredients | +1.0% | North America and European Union, with spillover to Asia-Pacific | Short term (≤ 2 years) |

| Broader use in skin health, beauty-from-within, and preventive wellness formulations | +0.8% | North America, European Union, and expanding Asia-Pacific | Medium term (2-4 years) |

| Shift toward plant-derived food colorants | +0.8% | European Union, North America, East Asia | Medium term (2-4 years) |

| Rising incorporation in functional beverages and fortified foods | +0.9% | Global | Short term (≤ 2 years) |

| Growing use of lycopene in dietary supplements for cardiovascular health support | +0.6% | Asia-Pacific core, spill-over to North America and Middle East and Africa | Medium term (2-4 years) |

| Technological advancements in microencapsulation | +0.5% | Global, early gains in North America, European Union, and China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for clean-label antioxidant ingredients

The increasing demand for clean-label antioxidant ingredients has significantly contributed to the growth of the lycopene market. Manufacturers are aligning product development with consumer preferences for simple, natural, and minimally processed formulations. Lycopene, a well-known natural antioxidant, has gained prominence in clean-label food, beverage, and nutraceutical applications, where transparency and ingredient familiarity are key factors influencing purchasing decisions. This trend has driven the broader adoption of lycopene as both a functional ingredient and a natural colorant in health-oriented product innovations. By 2025, approximately 13% of the U.S. population preferred clean eating, highlighting a shift toward health-conscious consumption and the avoidance of artificial additives[1]Source: International Food Information Council (IFIC), "2025 IFIC Food & Health Survey", ific.org. This preference has bolstered demand for antioxidant-rich ingredients like lycopene, particularly in fortified foods and dietary supplements. As brands adapt to these changing consumer behaviors, clean-label positioning has become a crucial factor for product differentiation, further accelerating the use of lycopene in mainstream food and wellness products.

Shift toward plant-derived food colorants

The increasing preference for plant-based food colorants has significantly contributed to the growth of the lycopene market. Manufacturers are progressively replacing synthetic colorants with natural alternatives to meet evolving clean-label demands. Lycopene, sourced from tomatoes and other plants, has gained importance as a natural red-orange pigment, particularly in food and beverage applications where visual appeal and ingredient transparency are essential. This shift has been further driven by heightened regulatory and consumer scrutiny of artificial additives, prompting brands to reformulate products with plant-based coloring solutions. In 2024, consumer willingness to pay a premium for specific food and beverage claims further reinforced this trend. Claims such as “natural / all-natural” emerged as the most valued by consumers, with “made with plant-based ingredients” also ranking among the top ten premium-value claims [2]Source: Ingredion, "Maximize brand value by formulating to 2024 consumer food preferences", ingredion.com. This highlighted a strong preference for plant-derived and minimally processed ingredients, motivating manufacturers to incorporate natural colorants like lycopene in functional foods, beverages, and nutraceuticals. Consequently, the move toward plant-based positioning has become a significant driver for the increased use of lycopene across mainstream product categories.

Rising incorporation in functional beverages and fortified foods

The growing use of lycopene in functional beverages and fortified foods has been a significant factor in market growth. Manufacturers have increasingly incorporated lycopene into products such as juices, dairy-based drinks, energy beverages, sauces, and nutritionally enhanced packaged foods. This trend is supported by rising consumer demand for products that offer both taste and health benefits, particularly those with antioxidant-rich formulations that promote preventive health and wellness. By 2025, nearly three-quarters of global consumers were aware of functional foods and beverages, indicating a notable shift toward health-conscious consumption and greater acceptance of fortified products in daily diets [3]Source: Institute of Food Technologists, "The Top 10 Functional Food Trends", ift.org. This heightened awareness has driven manufacturers to focus on product development, positioning lycopene as a value-added ingredient to improve nutritional profiles and achieve product differentiation. Consequently, the increasing adoption of functional beverages and fortified foods has become a key driver of demand, highlighting lycopene's expanding role in mainstream food and beverage applications.

Growing use of lycopene in dietary supplements for cardiovascular health support

The increasing use of lycopene in dietary supplements for cardiovascular health has been a significant driver of market growth, as consumers place greater emphasis on preventive healthcare and long-term heart health management. Lycopene has gained widespread acceptance in the nutraceutical industry due to its recognized antioxidant properties, which support lipid profile regulation, reduce oxidative stress, and contribute to overall cardiovascular wellness. This has established lycopene as a preferred ingredient in heart health-focused formulations, particularly in capsules, softgels, and tablets aimed at aging and health-conscious consumers. Manufacturers have increasingly incorporated lycopene into cardiovascular supplement portfolios as part of broader "heart health" strategies, often combining it with other functional ingredients such as omega-3 fatty acids, vitamins, and plant sterols. This trend has been further driven by growing consumer awareness of preventive nutrition and the shift from treatment-based healthcare to daily wellness supplementation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited natural raw material availability | -0.7% | Global, most acute in China and Southern Europe | Short term (≤ 2 years) |

| Cost pressure from crop-dependent extraction and multi-step purification | -0.5% | Global, amplified in markets dependent on natural lycopene | Medium term (2-4 years) |

| Claim substantiation and labeling friction across regions | -0.4% | European Union, North America, Asia-Pacific regulated markets | Medium term (2-4 years) |

| Formulation instability in liquid and high-heat processed applications | -0.5% | Global, most acute in beverage and processed food segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited natural raw material availability

Limited availability of natural raw materials remains a significant restraint on the lycopene market. The extraction of natural lycopene relies heavily on tomato-based and other plant sources, which are affected by seasonal fluctuations, variability in agricultural yields, and climate sensitivity. This constrained supply base hampers the scalability of natural lycopene production, making it challenging to consistently meet the increasing demand from food, beverage, and nutraceutical manufacturers. Consequently, producers often encounter supply instability, which affects pricing consistency and complicates long-term procurement planning. Furthermore, the scarcity of high-yield raw materials raises production costs and lowers extraction efficiency, reducing the competitiveness of natural lycopene compared to synthetic alternatives. This supply limitation also creates reliance on specific geographic regions for raw material sourcing, heightening vulnerability to disruptions caused by agricultural, logistical, or weather-related factors. Together, these challenges form a structural barrier that restricts the growth of natural lycopene, despite the rising consumer preference for clean-label and plant-based ingredients.

Cost pressure from crop-dependent extraction and multi-step purification

The cost pressures associated with crop-dependent extraction and multi-step purification processes have significantly restrained the growth of the lycopene market. Natural lycopene production is heavily reliant on agricultural raw materials, particularly tomatoes, which are affected by seasonal availability, climatic variations, and yield fluctuations. This reliance introduces cost instability, as raw material procurement is influenced by weather and agricultural productivity cycles, leading to inconsistent input costs for manufacturers. Furthermore, the extraction and purification of lycopene require multiple complex processing steps, including solvent extraction, concentration, and refinement, to achieve the desired purity levels. These processes increase operational costs, energy consumption, and production time, reducing overall cost efficiency. Consequently, natural lycopene faces higher pricing pressures than synthetic alternatives, limiting its competitiveness in price-sensitive applications and restricting broader market penetration, despite growing demand for clean-label ingredients.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Nature: Natural Lycopene Gains Ground on Clean-Label Demand

In 2025, synthetic sources represented the largest share of the lycopene market, accounting for 57.56%. This dominance was attributed to their cost efficiency, scalability, and consistent product quality. Synthetic or fermentation-derived lycopene is extensively utilized in dietary supplements, functional foods, and beverages due to its reliable availability and stable physicochemical properties. Manufacturers favor this segment as it enables standardized formulations, enhanced shelf-life performance, and reduced reliance on agricultural variability, making it the most commercially viable and scalable option in the global lycopene market.

Conversely, natural lycopene held a market share of 6.94% in 2025, despite growing consumer preference for clean-label and plant-based ingredients. Primarily sourced from tomatoes and other red fruits, natural lycopene is marketed as a premium ingredient in nutraceuticals and health-oriented food products. Its demand is driven by increasing awareness of natural antioxidants and their preventive health benefits. However, its market share remains constrained by higher production costs, lower extraction yields, and supply limitations, which hinder its competitiveness compared to synthetic alternatives in mass-market and cost-sensitive applications.

By Form: Powder Format Leads; Liquid Gains from Beverage Integration

In 2025, the powder form held the largest share of the lycopene market at 46.81%, driven by its stability, ease of handling, and broad applicability across various end-use industries. Powdered lycopene is commonly used in dietary supplements, functional foods, and nutraceutical formulations due to its longer shelf life, simplified storage and transportation, and compatibility with encapsulation and tablet production processes. Its solid form also facilitates controlled dosing and enhances formulation flexibility, making it the most widely utilized format in commercial applications.

Conversely, liquid lycopene represented a smaller market share of 6.53% in 2025, primarily utilized in specialized applications such as beverages, emulsions, and certain fortified food products. While the liquid form offers benefits like easier dispersion and faster absorption in specific formulations, its adoption is constrained by stability issues, higher packaging requirements, and a shorter shelf life compared to powder forms. These limitations confine its use to niche applications, whereas the powder form remains the dominant and more versatile option in the global lycopene market.

By Application: Supplements Outpace Food and Beverages in CAGR

In 2025, the food and beverages segment held the largest share of the lycopene market at 38.31%. This dominance was driven by the increasing use of lycopene as a natural colorant and functional ingredient in various products, including juices, dairy items, sauces, and fortified foods. Its antioxidant properties, combined with its ability to enhance nutritional value and visual appeal, make it a preferred choice for manufacturers addressing the growing consumer demand for healthier and clean-label food products. The segment benefits from extensive product penetration and the rising trend of fortification across global processed food categories.

In comparison, dietary supplements represented 7.76% of the lycopene market in 2025. This segment's growth was supported by increasing awareness of preventive healthcare and the role of antioxidants in promoting cardiovascular, skin, and prostate health. Lycopene is commonly incorporated into capsule, tablet, and softgel formulations aimed at health-conscious consumers. However, its market share remains smaller than that of the food and beverages segment due to the broader consumption base and higher volume demand in the food and beverages industry, while dietary supplements cater to a more niche audience with specific health-focused applications.

Geography Analysis

In 2025, North America held the largest share of the lycopene market at 40.75%. This dominance was supported by high consumer awareness of functional ingredients and the strong presence of dietary supplements and fortified food products. The region benefits from a well-established nutraceutical industry, advanced food processing capabilities, and significant demand for antioxidant-rich products aimed at preventive healthcare. Additionally, high disposable income levels and a mature retail and e-commerce ecosystem contribute to the consistent consumption of lycopene-based formulations across food and supplement applications.

Asia-Pacific emerged as the fastest-growing region in 2025, with a market share of 7.08%. This growth was driven by increasing health consciousness, an expanding middle-class population, and the rising adoption of dietary supplements and functional foods. Factors such as rapid urbanization, changing dietary habits, and a growing focus on preventive wellness have accelerated demand, particularly in countries like China, India, and Japan. Furthermore, the expansion of food processing industries and increased investments by global ingredient companies are enhancing market penetration in the region.

Regions such as Europe, Latin America, and the Middle East and Africa collectively accounted for a moderate but steadily growing share of the lycopene market in 2025. In Europe, strong regulatory emphasis on natural and clean-label ingredients has driven demand for natural lycopene in food and nutraceutical applications. Latin America is showing potential due to increasing health awareness and trends in food fortification. Meanwhile, the Middle East and Africa are gradually expanding their market presence, supported by urbanization and improved access to functional food products. However, these regions remain smaller in overall market share compared to North America and Asia-Pacific.

Competitive Landscape

The lycopene market exhibits moderate concentration, with 3–4 major integrated suppliers, BASF, DSM-Firmenich, and Lycored, dominating the specialty and premium-grade lycopene segment. In contrast, a larger, fragmented group of Chinese and Indian manufacturers, including Zhejiang NHU, Wellgreen Technology, Xi'an Lyphar, Xi'an Natural Field, Divi's Nutraceuticals, and Allied Biotech, primarily competes on commodity-grade pricing. Among the top-tier suppliers, competitive strategies are increasingly focused on encapsulation capabilities, bioavailability data packages, and regulatory dossier support, rather than solely on raw ingredient supply.

Lycored has achieved a significant competitive advantage by securing EFSA novel food approvals for its Lumenato and Lycoderm tomato-derived complexes. This regulatory approval creates a strong position in the EU nutricosmetics market, which smaller competitors are unlikely to replicate in the near term. Within the fragmented mid-tier, opportunities exist for fermentation-derived lycopene from Blakeslea trispora, which is regulated under JECFA INS 160d(ii). This approach provides a non-tomato supply chain for natural lycopene but requires careful navigation of regulatory requirements in different jurisdictions.

Technological advancements, such as protein-polysaccharide encapsulation, high-internal-phase emulsions, and supercritical CO₂ extraction, the latter now a standard practice in leading Chinese facilities, are distinguishing capable ingredient manufacturers from commodity extract suppliers. These technologies are expected to become essential qualifications as beverage and cosmetic customers increasingly tighten supplier requirements.

Lycopene Industry Leaders

-

BASF SE

-

DSM-Firmenich AG

-

Lycored Ltd.

-

Archer Daniels Midland Company

-

Allied Biotech Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Sensient Technologies Corporation revealed a USD 250 million investment to expand its natural food dye production capacity, aligning with its strategy to meet the growing global demand for clean-label and naturally derived color solutions. The investment focuses on enlarging its largest natural color manufacturing site in St. Louis by approximately 28,800 square feet. This expansion aims to improve supply chain reliability, consistency, and scalability for natural colorants used in food and beverage applications.

- January 2026: ADM announced a USD 26 million investment in its Erlanger facility to strengthen its position in providing innovative food and beverage solutions derived from natural sources. The expansion aims to enhance the capacity, delivery efficiency, and supply reliability of the company’s flagship U.S. flavors site, focusing on naturally derived color and flavor solutions.

- October 2025: Lycored unveiled its Versatile Application Solution (VAS) technology at SupplySide Global 2025, signifying a significant advancement in its ingredient delivery capabilities. This innovation utilizes microencapsulated starch beadlets to enhance the performance of active ingredients, such as lycopene, across various formats, including tablets, gummies, capsules, and powdered beverages. The system improves critical functional properties, including stability, solubility, flowability, compressibility, and homogeneity, facilitating easier and more consistent formulation for nutraceutical and functional food applications.

Global Lycopene Market Report Scope

| Synthetic |

| Natural |

| Powder |

| Liquid |

| Others |

| Dietary Supplements |

| Food and Beverages |

| Pharmaceuticals |

| Cosmetics and Personal Care |

| Others |

| North America |

| Europe |

| Asia-Pacific |

| South America |

| Middle East and Africa |

| By Nature | Synthetic |

| Natural | |

| By Form | Powder |

| Liquid | |

| Others | |

| By Application | Dietary Supplements |

| Food and Beverages | |

| Pharmaceuticals | |

| Cosmetics and Personal Care | |

| Others | |

| By Geography | North America |

| Europe | |

| Asia-Pacific | |

| South America | |

| Middle East and Africa |

Key Questions Answered in the Report

Which form dominated the lycopene market in 2025?

Powder form led the market with a 46.81% share driven by stability and wide application use.

Which segment held the largest share in 2025 in terms of nature?

Synthetic sources accounted for the largest share at 57.56% due to cost efficiency and scalability.

Which application segment was the largest in 2025?

Food and beverages held the leading share at 38.31% owing to strong demand for functional and fortified products.

Which region was the fastest-growing from 2026–2031?

Asia-Pacific recorded the highest growth with a 7.08% CAGR driven by rising health awareness and supplement demand.

Page last updated on: