Organic Spices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 24.57 Billion |

| Market Size (2031) | USD 33.34 Billion |

| Growth Rate (2026 - 2031) | 6.29% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Organic Spices Market Analysis by Mordor Intelligence

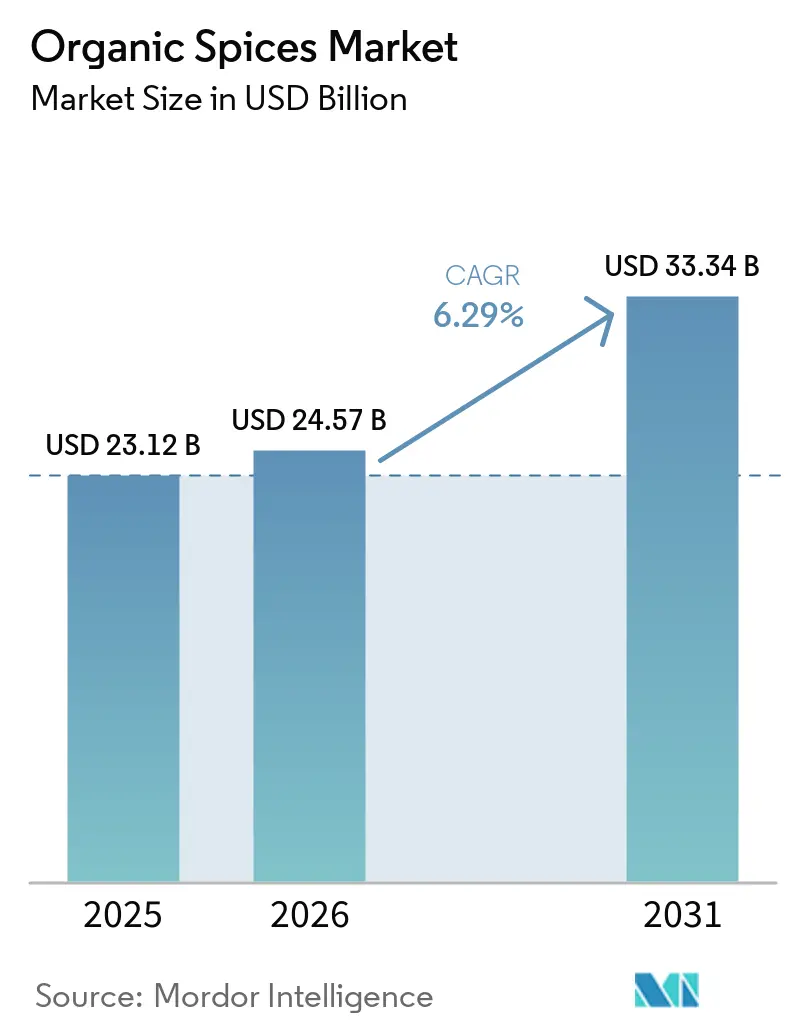

The organic spices market size is expected to grow from USD 23.12 billion in 2025 to USD 24.57 billion in 2026 and is forecast to reach USD 33.34 billion by 2031 at 6.29% CAGR over 2026-2031. The global organic spices market is transitioning into a compliance-focused industry, where certification-backed traceability now outweighs price competitiveness in determining market access. Regulatory tightening in the United States and European Union is driving up costs for smallholder supply chains, while vertically integrated players with robust documentation systems are gaining a competitive edge. Simultaneously, challenges such as climate volatility, logistics disruptions, and contamination risks are intensifying supply chain vulnerabilities, making investments in advanced testing and blockchain-enabled traceability critical. Growing consumer demand in the organic spices market for clean-label and ethically sourced products continues to bolster premium positioning, emphasizing the importance of sustainability, compliance, and innovation in supply chain management for long-term competitiveness. This evolving landscape is fostering stronger multinational partnerships with local processors and encouraging niche differentiation.

Key Report Takeaways

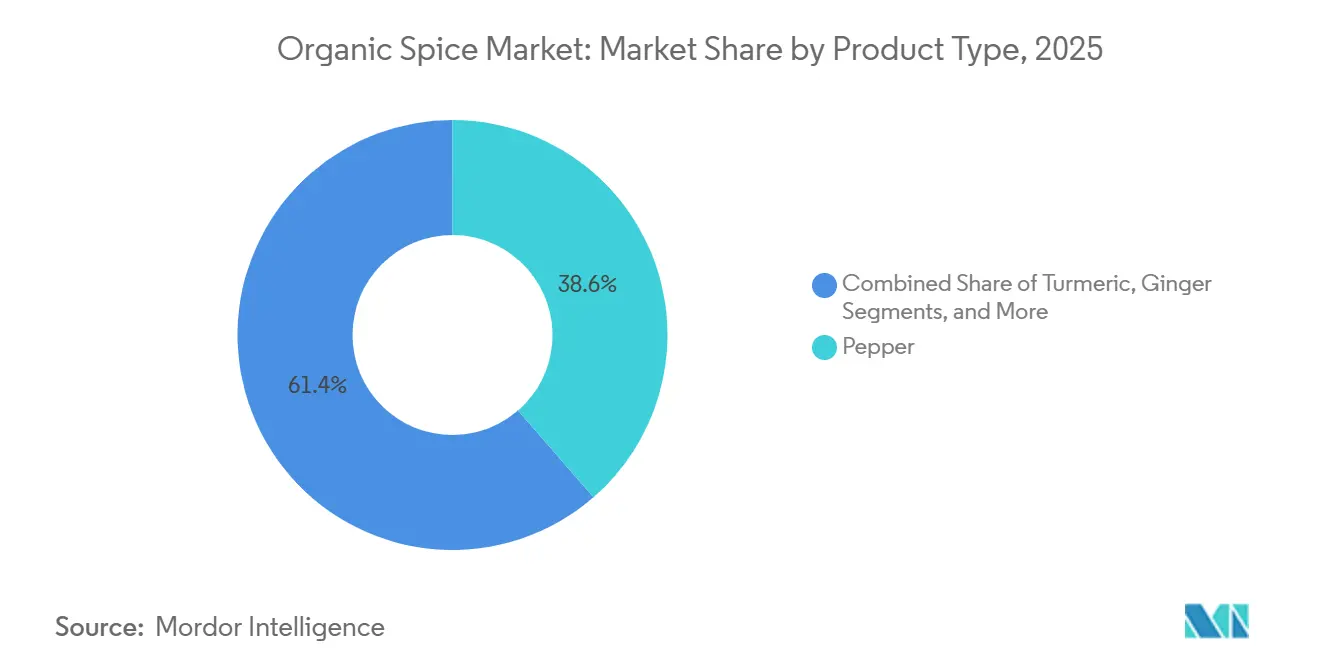

- In 2025, pepper accounted for 38.62% of the organic spices market share, while turmeric is expected to grow at a CAGR of 8.40% through 2031.

- In 2025, powdered variants represented 45.50% of the market share, and they are projected to expand at a CAGR of 7.30% during the forecast period ending in 2031.

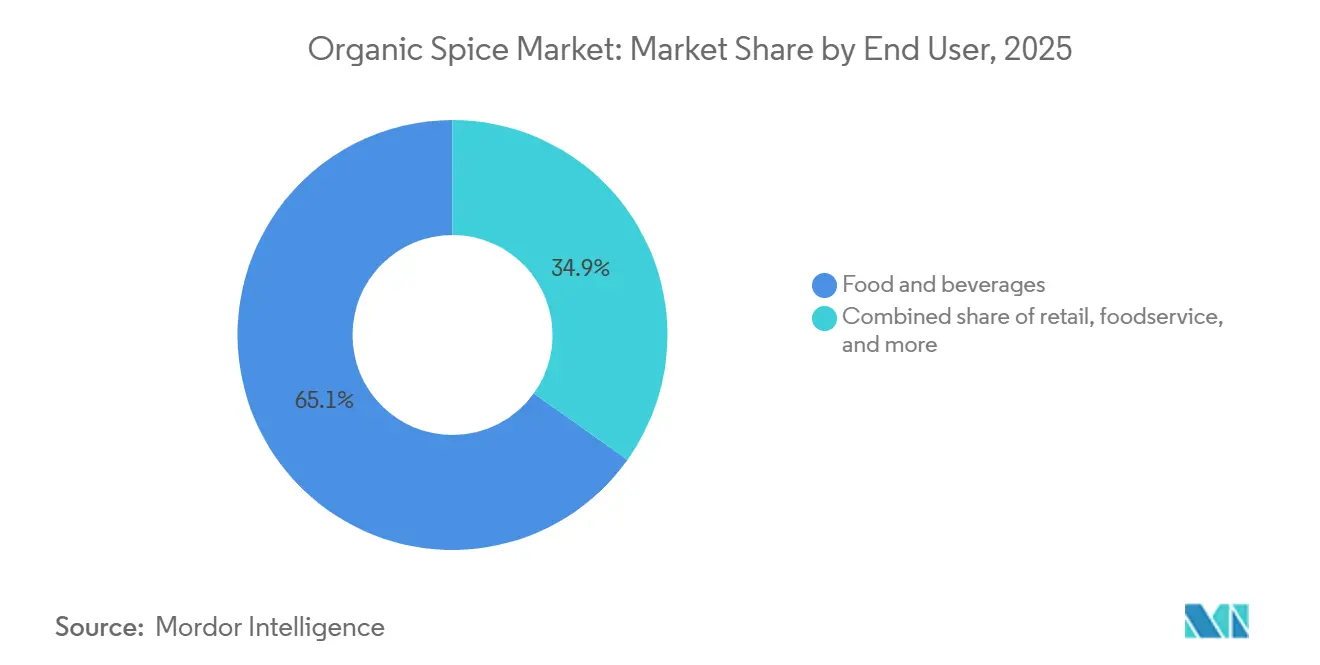

- In 2025, the food and beverages sector captured 65.12% of the market share, whereas retail demand is anticipated to grow at a CAGR of 7.68% through 2031.

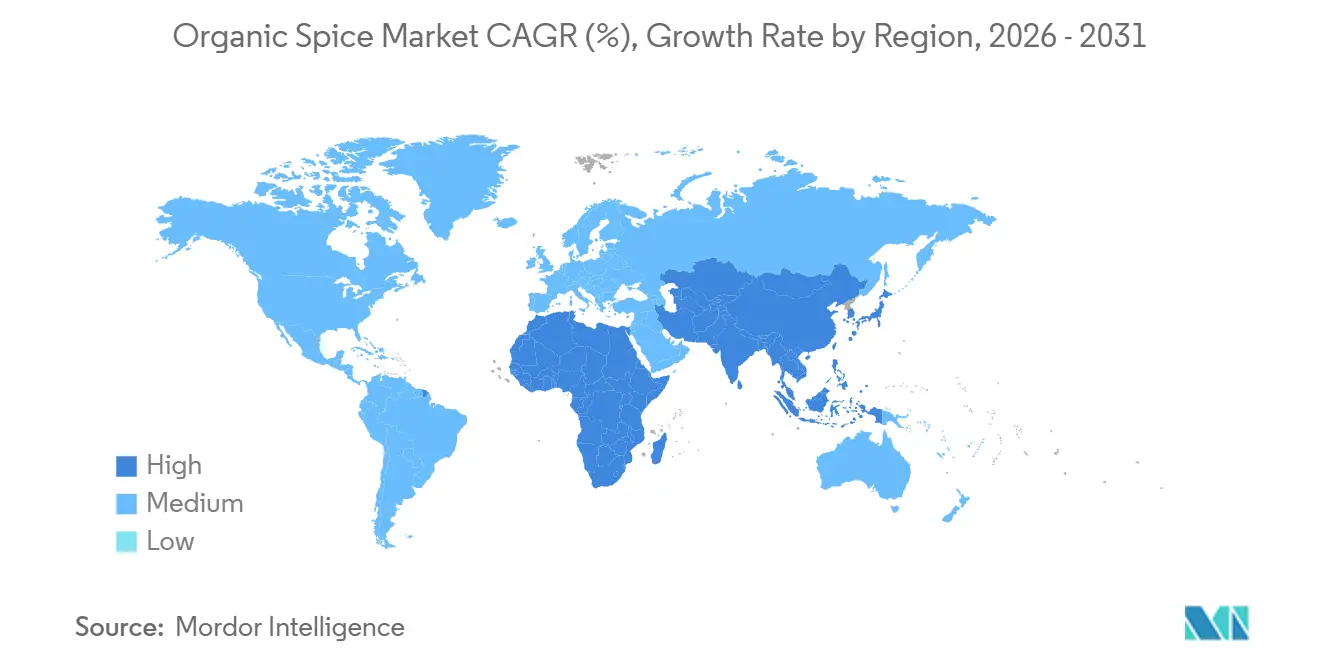

- In 2025, the Asia-Pacific region held a 41.34% revenue share and is forecast to register a CAGR of 7.80% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Organic Spices Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for natural, chemical-free, and clean-label food products | +1.2% | Global (notably North America and Europe) | Medium term (2-4 years) |

| Stringent government regulations and certifications promoting organic farming | +0.8% | Global (Europe Union and North America) | Long term (≥ 4 years) |

| Surge in ethnic and convenience cuisine consumption | +0.6% | North America, Europe, Asia-Pacific cities | Short term (≤ 2 years) |

| Rapid expansion of organised retail and e-commerce | +0.4% | Global, fastest in Asia-Pacific | Medium term (2-4 years) |

| Growth in international trade and export opportunities | +0.3% | Asia-Pacific origins (India, Vietnam, Indonesia) to North America and Europe Union destinations | Long term (≥ 4 years) |

| Increasing demand from food processing and packaged food industries | +0.2% | North America, Europe, Asia-Pacific hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for natural, chemical-free, and clean-label food products

The global organic spices market is experiencing significant growth, driven by a strong consumer shift toward natural, chemical-free, and clean-label food products. Ingredient transparency has become a standard expectation. In Europe, this trend has reached maturity, with organic food retail sales accounting for 12% in Denmark and 11% in Switzerland. This growth is fueled by consumers' willingness to pay a premium for certified organic ingredients, as reported by the IFOAM Organization[1]IFOAM, "Share of retail sales of organic products in selected countries in Europe in 2023", www.ifoam.bio. To meet this demand, food manufacturers are reformulating their offerings with certified organic spices, avoiding synthetic residues. Buyers are increasingly prepared to pay higher prices for verified compliance. Vertically integrated players are well-positioned to capitalize on this trend by securing certified acreage and ensuring a stable long-term supply. Conversely, smaller exporters face challenges due to the financial and administrative burdens of certification. Initiatives aimed at training farmers in sustainable practices and developing certified supply pipelines are enhancing market resilience. However, the market is also consolidating, as only well-capitalized processors can manage the multi-year conversion periods and rigorous audit requirements. Ultimately, the growing preference for clean-label products in the organic spices market is not only influencing consumer behavior but also redefining competitive dynamics, driving the industry toward sustainability, transparency, and long-term supply security.

Stringent government regulations and certifications promoting organic farming

Stringent government regulations and certification frameworks, emphasizing documentation, traceability, and fraud prevention, are increasingly shaping the global organic spices market. In the United States, the European Union, and India, updated rules are elevating compliance demands. This shift in the organic spices market poses challenges for smallholder farmers and under-capitalized exporters, while larger, vertically integrated players, adept at absorbing certification costs and navigating intricate audits, find themselves at an advantage. Beginning March 2024, the USDA's Strengthening Organic Enforcement (SOE) rule is set to redefine compliance within the organic spice supply chain. As underscored by SCS Global Services, the new regulation requires NOP Import Certificates for all imported organic products and extends certification mandates to include brokers and traders. Rather than mere obstacles, these intertwined regulatory layers serve as competitive moats, granting disciplined suppliers assured market access and premium positioning. Consequently, the industry is gravitating towards well-capitalized processors and multinational collaborations, with sustainability and compliance emerging as cornerstones for enduring growth.

Surge in ethnic and convenience cuisine consumption

The global organic spices market is experiencing significant growth, driven by increasing demand for ethnic and convenience cuisines. Factors such as globalization of tastes, migration, and digital recipe sharing are expanding the market beyond traditional boundaries. Consumers are prioritizing authentic flavors in convenient formats, fueling the demand for ready-to-use blends, single-origin products, and innovative packaging solutions like resealable pouches and QR-code traceability. E-commerce platforms are accelerating this trend by enabling direct-to-consumer brands to bypass traditional retail constraints, communicate provenance effectively, and justify premium pricing. Additionally, spice processors are leveraging co-packing and private-label opportunities to capture value through formulation expertise and small-batch production capabilities, which larger competitors often find difficult to replicate. However, the increasing variety of SKUs and distribution channels introduces operational complexities, necessitating robust certification management and lot-tracking systems to maintain organic integrity and prevent commingling. These developments highlight how authenticity, convenience, and regulatory compliance are reshaping competitiveness in the organic spices market.

Rapid expansion of organized retail and e-commerce

Organized retail and e-commerce are rapidly reshaping the global organic spices market, steering purchases away from traditional open-air markets and towards supermarkets, hypermarkets, and online platforms. This shift within the organic spices market centralizes buying power and elevates expectations for consistent quality, tamper-proof packaging, and traceable supply chains, benefiting suppliers who can meet these stringent retailer demands. Concurrently, online platforms are favoring brands that invest in digital marketing and provenance storytelling, allowing them to forge direct connections with health-conscious consumers and validate their premium pricing. While larger chains leverage slotting fees and price concessions, squeezing processor margins, smaller exporters and regional brands are seizing opportunities with specialty retailers, natural-food co-ops, and direct-to-consumer models. Here, their emphasis on sustainability and authenticity fosters a loyal customer base, largely shielded from price-driven competition.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher production costs compared to conventional spices | -0.9% | Global, with acute impact in developed markets | Medium term (2-4 years) |

| Risk of contamination or adulteration in the supply chain | -0.7% | Global, particularly India-export dependent regions | Short term (≤ 2 years) |

| Climate-induced yield volatility in key origins | -0.5% | Asia-Pacific, Latin America, Africa | Long term (≥ 4 years) |

| Competition from conventional and non-certified "natural" spice products | -0.3% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher production costs compared to conventional spices

The global organic spices market is constrained by higher production costs compared to conventional spices. Organic farming involves labor-intensive practices, lower yields, and reliance on expensive inputs such as biofertilizers and biopesticides. Furthermore, the certification process adds financial and administrative challenges. Smallholder farmers, in particular, face difficulties due to lengthy conversion periods and audit expenses, often lacking the scale to absorb these costs. This has resulted in a fragmented supply base, where well-capitalized grower groups and multinational-linked contract farmers gain a competitive edge, while smaller producers struggle to remain viable or exit the market. The high cost structure limits market penetration into price-sensitive segments, concentrating demand in affluent markets where consumers prioritize health and sustainability. Processors can address some of these challenges by offering value-added services such as sterilization, private labeling, and advanced packaging. However, these services require significant scale and investment capacity, which many regional players lack, further strengthening the competitive position of larger, integrated suppliers.

Risk of contamination or adulteration in the supply chain

The global organic spices market is challenged by contamination and adulteration risks across its supply chain, which undermine consumer confidence and escalate compliance expenses. In 2024, the European Commission identified 277 safety concerns related to spices and herbs, as reported by the Central Bureau of Investigation[2]CBI, “European Market for Spices and Herbs,” cbi.eu. The global organic spices market is challenged by contamination and adulteration risks across its supply chain, which undermine consumer confidence and escalate compliance expenses. Exporters, particularly those handling high-risk crops such as turmeric and ginger, face increased rejection rates and costly recalls due to issues like pesticide drift, commingling during transportation, and intentional substitution with non-organic products. To address these challenges, major import markets have implemented stricter residue-testing protocols and traceability audits. Suppliers in the organic spices market are now required to invest in accredited laboratory testing, lot-tracking systems, and segregated storage facilities to maintain organic certification. This regulatory landscape benefits vertically integrated companies that oversee the entire value chain, enabling them to mitigate contamination risks and secure premium pricing. Conversely, smaller exporters without comprehensive oversight are under growing pressure to collaborate with organized grower groups or risk being excluded from the organic spices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pepper Dominance Drives Premium Positioning

In 2025, pepper will hold a commanding 38.62% share of the global organic spices market, driven by its extensive culinary applications and versatility. However, turmeric is set to redefine the organic spices market dynamics, achieving a strong CAGR of 8.40% through 2031 as it transitions toward functional-wellness applications. Valued for its anti-inflammatory and antioxidant properties, turmeric is experiencing increased demand from nutraceutical manufacturers and health-focused food processors. Nonetheless, climate variability and yield-related risks pose challenges to scaling production. Concurrently, spices such as ginger, chili, and cinnamon continue to witness stable demand across culinary and medicinal segments but face supply chain disruptions and competitive pressures from lower-cost producers. On the other hand, cardamom, cloves, and cumin are gaining traction, supported by the growing popularity of ethnic cuisines and premium single-origin offerings.

Turmeric's functional shift underscores a broader market trend where product growth is diverging from traditional culinary demand and aligning with health and wellness priorities. Buyers are increasingly seeking high-curcumin varieties and comprehensive certificates of analysis, incentivizing suppliers to invest in varietal optimization, controlled drying techniques, and advanced quality testing. Additionally, industry-led initiatives focused on enhancing farmer capabilities, sustainability, and transparency are emerging as critical competitive advantages. This evolution indicates that future growth in the organic spices market will favor spices with documented bioactive properties and certified-organic traceability. These developments are reshaping the competitive landscape, positioning wellness-driven applications as the primary growth driver for the organic spices market.

By Form: Powder Segment Leads Through Convenience Innovation

By 2025, powdered spices are projected to dominate the global organic spices market, securing a 45.50% share and achieving a CAGR of 7.30% through 2031. This growth is primarily driven by their alignment with the operational requirements of industrial food processors, who prioritize consistency, safety, and efficiency. Pre-ground powders streamline formulation processes, minimize contamination risks, and facilitate compliance with stringent food-safety standards, offering a clear advantage over whole or crushed spices. While whole spices maintain a niche appeal among culinary purists, their additional handling and infrastructure requirements make them less viable for large-scale operations. Crushed and flaked spices address specific needs where texture and visual appeal are critical, but the broader trend of food production industrialization continues to reinforce the dominance of powdered forms.

Advancements in processing technologies are further solidifying the leadership of powdered spices. Innovations such as steam sterilization and optical sorting ensure compliance with organic standards while maintaining product purity and safety. These capital-intensive processes create entry barriers for smaller processors, favoring mid-sized and large-scale players who can distribute costs across multiple spice varieties and customer segments. As a result, competition within this segment is shifting from price-based strategies to a focus on quality assurance. Suppliers investing in advanced testing and traceability systems are capturing increased demand from both industrial buyers and retail consumers. This organic spices market dynamic positions powdered organic spices as a critical component of modern supply chains, where safety, consistency, and certification integrity are non-negotiable.

By End User: Retail Channels Accelerate as Direct-to-Consumer Brands Proliferate

In 2025, the food and beverage sector is set to dominate, holding a 65.12% share, underscoring the vastness of industrial food production and the growing incorporation of spices in packaged foods, condiments, snacks, and drinks. Yet, retail channels are on the rise, projected to grow at 7.68% through 2031. This surge is largely attributed to direct-to-consumer brands harnessing e-commerce, allowing them to sidestep traditional distribution. These brands are effectively reaching out to health-conscious consumers, emphasizing their stories of provenance and commitment to clean-label products. Meanwhile, the foodservice sector is also witnessing growth. Restaurants and catering services are increasingly opting for certified-organic ingredients, aiming to elevate their menu offerings and attract diners who prioritize sustainability. Beyond these primary uses, there's a burgeoning niche in nutraceuticals, supplements, and personal care. Here, organic spice extracts are highly valued for their bioactive compounds, which are beneficial for wellness and skincare.

This evolving landscape is not just about products but is reshaping the very economics of distribution and the competitive landscape. Organized retail, while offering visibility and scale, comes with its challenges. It exerts margin pressures through slotting fees and promotional allowances, making it tough for brands without distinct differentiation. On the other hand, e-commerce stands out with its advantages: it provides flexibility, incurs lower fixed costs, and fosters direct engagement with customers. This direct connection paves the way for innovative approaches like subscription models and swift testing of stock-keeping units (SKUs). The significance of integrated supply chains is underscored by strategic moves in the industry, such as produce distributors merging with spice blenders, all in a bid to tap into the burgeoning foodservice market. In essence, while the end-user landscape becomes more fragmented, there's a clear shift towards channels that prioritize authenticity, traceability, and compelling brand narratives. These elements are not just buzzwords; they are becoming the cornerstone of consumer engagement and sustainability, driving long-term competitiveness in the organic spices market.

Geography Analysis

Asia-Pacific, accounting for a 41.34% share in 2025, stands as the dominant force in the global organic spices market, with projections of a 7.80% growth rate extending through 2031. Central to this growth is India, bolstered by its robust certification frameworks and export infrastructure. The region's significance is underscored by rising demands in China and Japan, alongside premium niches in Australia and New Zealand. However, challenges persist: fragmented smallholder farming and contamination risks threaten credibility, underscoring the critical need for traceability and compliance to ensure sustained growth.

North America and Europe lead as the primary import markets, imposing stringent certification and traceability standards. While these standards elevate barriers to entry, they also reward those suppliers who maintain discipline. In the United States, organized retail chains emphasize consistency and packaging integrity. Conversely, Europe's fragmented market landscape provides opportunities for artisanal and single-origin brands. Both continents are witnessing a surge in e-commerce, facilitating direct-to-consumer models. This shift amplifies the influence of brands adept at cultivating loyalty through narratives of provenance and sustainability.

Regions like South America, the Middle East, and Africa are emerging as new frontiers of opportunity. Brazil and Argentina are ramping up cultivation efforts, aiming to rival traditional Asian sources. Meanwhile, the Middle East is not only consuming but also re-exporting, aligning its offerings with Halal and clean-label trends. Africa, with its wild collection areas, harbors immense potential in the organic spices market, though it grapples with certification and infrastructure hurdles. These developments illustrate a clear divide: established markets prioritize stringent compliance, while emerging regions boast cost advantages and untapped supply opportunities.

Competitive Landscape

The global organic spices market is characterized by fragmentation, with multinational processors, regional exporters, and smallholder cooperatives competing for market share. Leading players such as McCormick, Olam, and Frontier Co-op capitalize on brand equity, extensive certifications, and integrated supply chains. In contrast, smaller firms differentiate themselves through single-origin products and sustainability-focused narratives that appeal to environmentally conscious consumers. Strategic initiatives in the organic spices market often center on vertical integration, acquisitions, and diversification into adjacent categories, including nutraceuticals and botanical extracts.

Technological advancements are becoming a critical differentiator. Premium suppliers are leveraging advanced residue testing, steam sterilization, and blockchain-enabled traceability to distinguish themselves from commodity exporters. Additionally, direct-to-consumer brands are disrupting traditional distribution models by utilizing e-commerce platforms to bypass intermediaries and communicate product provenance through digital storytelling and QR codes. Regulatory tightening, particularly in the United States and European Union, is raising compliance standards, favoring companies with robust internal controls and traceability systems.

The competitive outlook indicates that while the organic spices market is currently fragmented, consolidation is likely to accelerate. Larger, well-capitalized firms with advanced compliance frameworks and technological capabilities are positioned to capture a greater share of the market. Conversely, smaller exporters must align with organized grower groups to remain competitive or risk exclusion. In this evolving landscape, scale, certification integrity, and transparency are becoming critical drivers of competitiveness.

Organic Spices Industry Leaders

-

McCormick & Company

-

Olam Food Ingredients (ofi)

-

Frontier Co-op (Simply Organic)

-

Organic Spices Inc.

-

Mountain Rose Herbs

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: McCormick completed a comprehensive redesign of its Gourmet Collection, introducing 54 certified organic varieties, with a full retail rollout in January 2026. The updated portfolio emphasized key organic products, including garlic powder, smoked paprika, cardamom, oregano, thyme, and ground cardamom.

- February 2025: Newman's Own launched a new organic seasoning line. The company launched 9 new products that are non-GMO, organic, gluten-free and USDA-certified. The products are available on Amazon and Walmart stores.

- January 2025: Olde Thompson acquired Gel Spice through Kainos Capital, expanding its position as the largest private label spice company with enhanced distribution capabilities across retail, foodservice, and industrial channels, including organic spice offerings.

Global Organic Spices Market Report Scope

Organic spices are spices grown and processed without synthetic pesticides, herbicides, fertilizers, or chemical fumigation, and must meet strict certification standards to ensure purity, ecological balance, and traceability. Rising consumer demand for premium organic ingredients, including Cardamom, is further supporting growth across the global organic spices market. They are valued for being chemical-free, environmentally sustainable, and aligned with clean-label consumer preferences.

| Pepper |

| Turmeric |

| Ginger |

| Chili |

| Cinnamon |

| Coriander |

| Cumin |

| Mustard |

| Cardamom |

| Cloves |

| Others |

| Whole |

| Powder |

| Crushed/Flakes |

| Others |

| Food and Beverages |

| Retail |

| Foodservice |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Pepper | |

| Turmeric | ||

| Ginger | ||

| Chili | ||

| Cinnamon | ||

| Coriander | ||

| Cumin | ||

| Mustard | ||

| Cardamom | ||

| Cloves | ||

| Others | ||

| Form | Whole | |

| Powder | ||

| Crushed/Flakes | ||

| Others | ||

| End User | Food and Beverages | |

| Retail | ||

| Foodservice | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the organic spices market?

The organic spices market size is USD 24.57 billion in 2026 and is projected to reach USD 33.34 billion by 2031 at a 6.29% CAGR.

Which product type holds the largest share?

Pepper leads with 38.62% of 2025 revenue, reflecting ubiquitous culinary use and robust supply chains.

Which region drives the most demand?

Asia-Pacific contributes 41.34% of global turnover and is set for a 7.80% CAGR to 2031, powered by production strength in India and expanding middle-class consumption.

Why are powdered organic spices growing so quickly?

Powdered formats captured 45.50% share in 2025 and will grow at 7.30% CAGR because they deliver convenience, uniformity, and longer shelf life demanded by home cooks and food processors.

Page last updated on: