R-142b Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

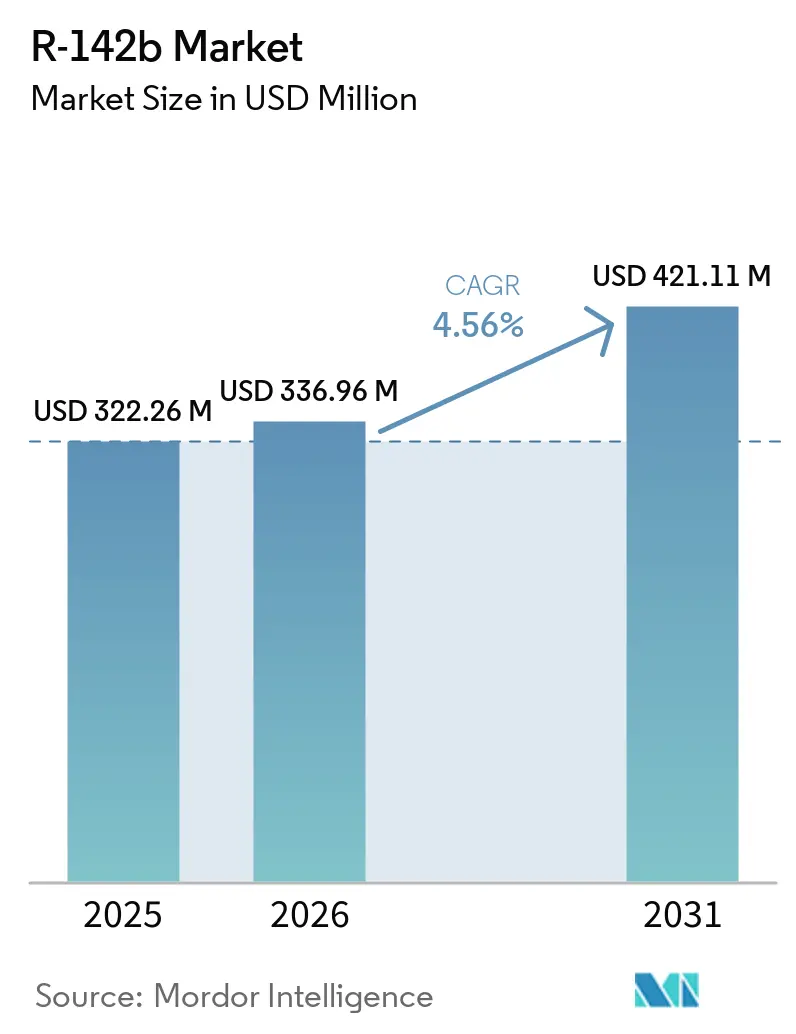

| Market Size (2026) | USD 336.96 Million |

| Market Size (2031) | USD 421.11 Million |

| Growth Rate (2026 - 2031) | 4.56% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

R-142b Market Analysis by Mordor Intelligence

The R-142b Market size was valued at USD 322.26 million in 2025 and is estimated to grow from USD 336.96 million in 2026 to reach USD 421.11 million by 2031, at a CAGR of 4.56% during the forecast period (2026-2031). The R-142b market is witnessing distinct trends: demand for its use in refrigerants and foam-blowing applications is decreasing due to Montreal Protocol regulations, while its role as a feedstock for polyvinylidene fluoride (PVDF) and polyvinyl fluoride (PVF) is increasing, supported by investments in battery-cell and semiconductor industries. Producers with integrated hydrofluoric acid and chloroform operations are better equipped to manage margin fluctuations compared to stand-alone formulators, particularly during hydrogen fluoride price increases. Quota systems in China and the United States now prioritize feedstock exemptions, creating a segmented R-142b market. This structure allocates virgin R-142b molecules to PVDF production, while refrigerant users increasingly depend on reclaimed supplies. Furthermore, the European Union's carbon dioxide (CO₂)-equivalent fee, effective January 2026, is expected to raise the landed costs of high-global warming potential (GWP) fluorocarbons, accelerating the shift to hydrofluoroolefins (HFOs) and natural refrigerants in equipment conversions.

Key Report Takeaways

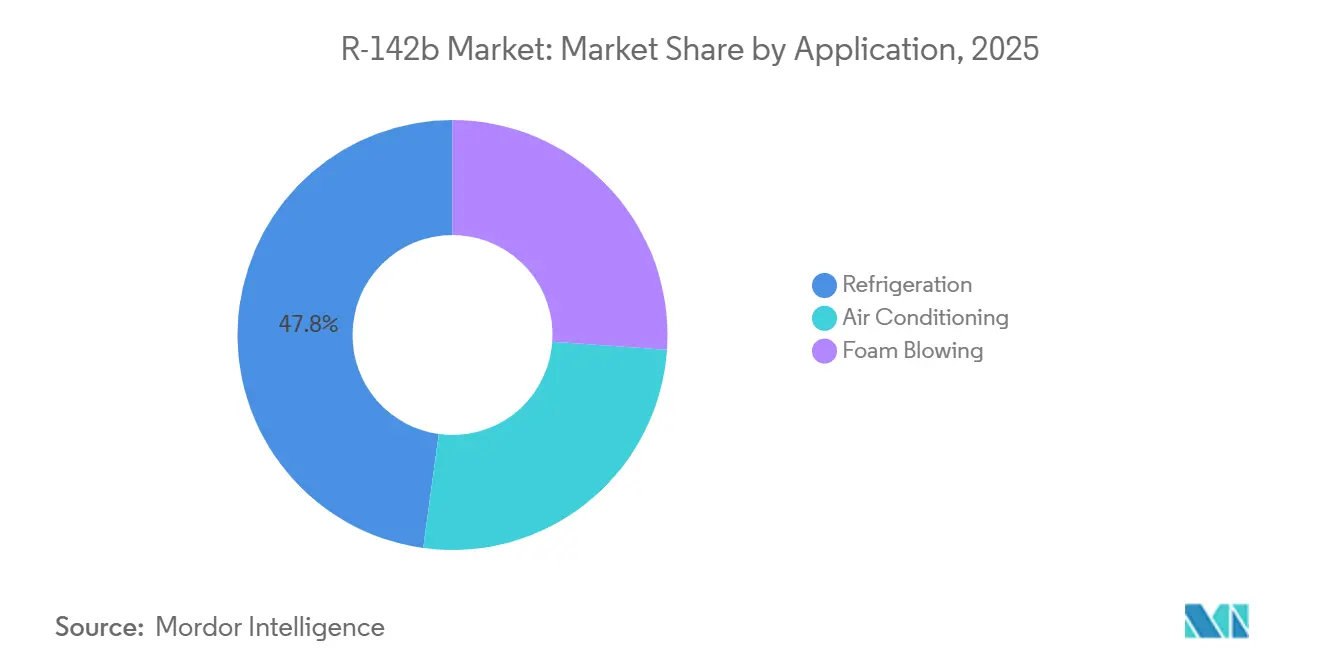

- By application, refrigeration held 47.82% of the R-142b market share in 2025, while foam blowing is projected to expand at a 4.78% CAGR through 2031.

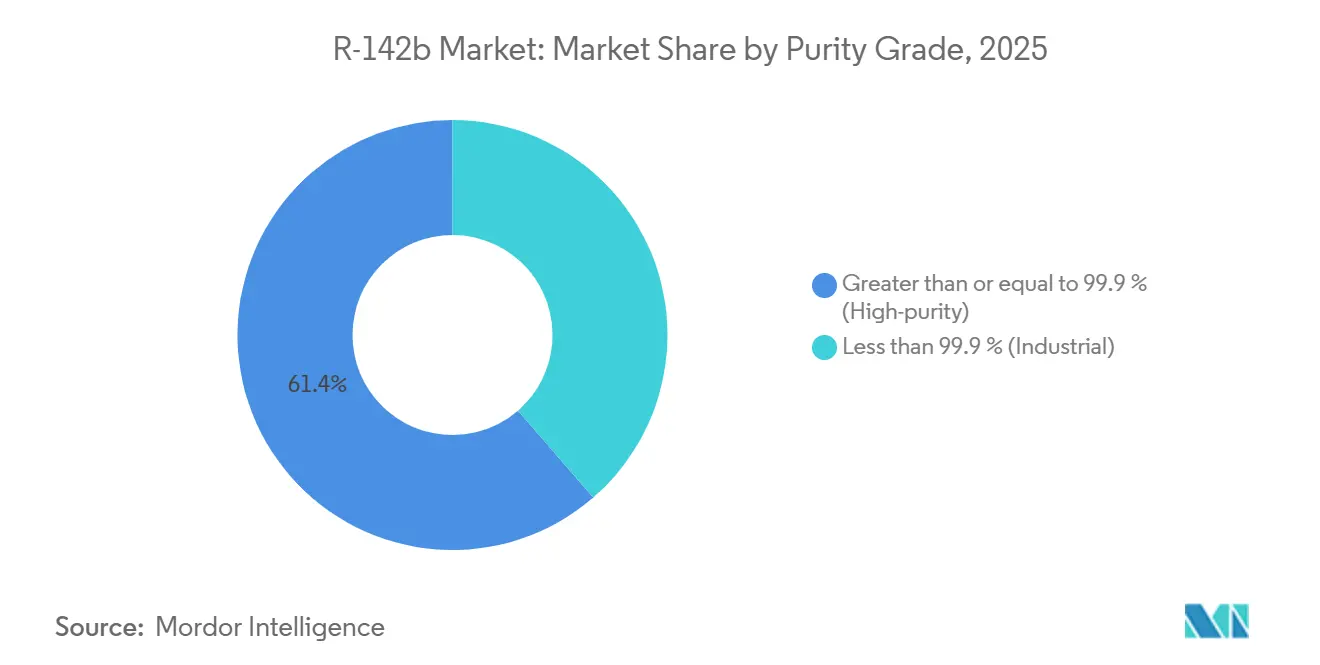

- By purity grade, high-purity material accounted for 61.35% of the R-142b market size in 2025 and is set to grow at a 4.81% CAGR to 2031.

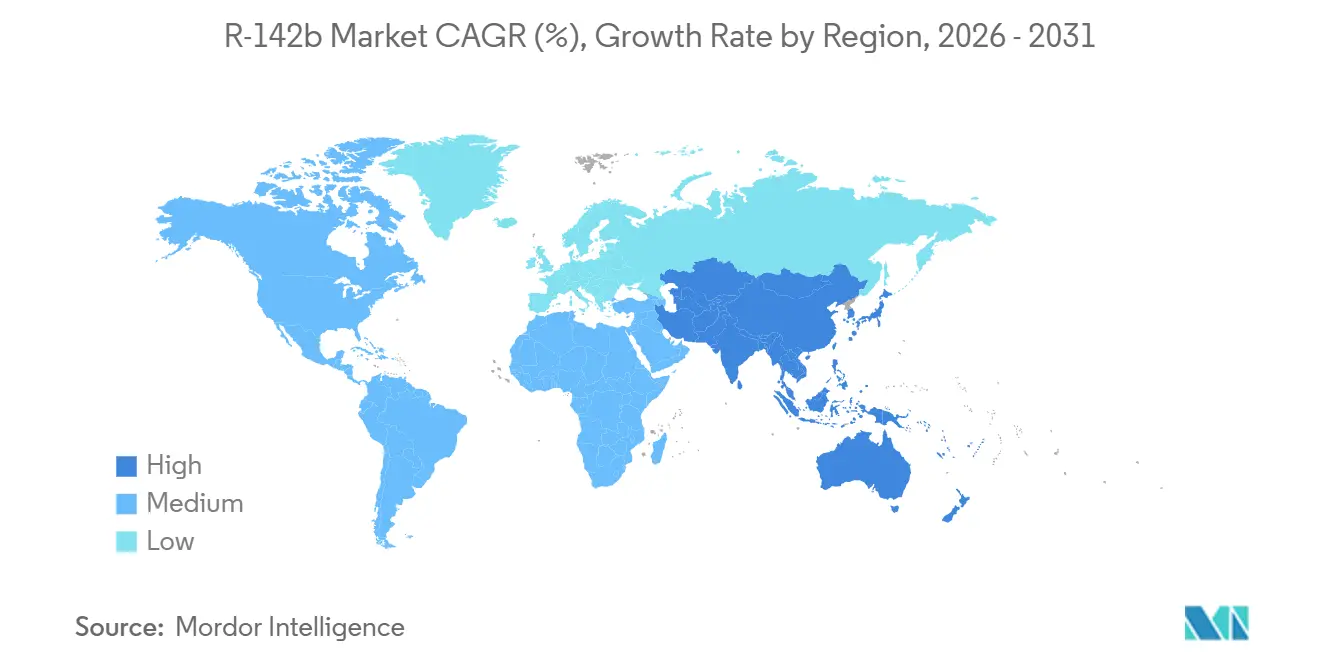

- By geography, Asia-Pacific commanded 45.76% of 2025 revenue and is expected to record the fastest regional CAGR at 4.66% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global R-142b Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising PVDF-binder demand from Li-ion battery gigafactories | +1.2% | Global, concentrated in China, South Korea, the U.S., and Europe | Medium term (2-4 years) |

| Expanding fluorochemical capacity integration in China and India | +0.9% | Asia-Pacific core, spill-over to the Middle East & Africa | Short term (≤ 2 years) |

| Increasing use as feedstock for fluoropolymers (PVDF, PVF) | +1.0% | Global, led by Asia-Pacific and North America | Long term (≥ 4 years) |

| Growing demand from refrigeration and blowing-agent blends | +0.6% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Kigali allowance for feedstock exemptions sustaining supply | +0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising PVDF-Binder Demand from Li-Ion Battery Gigafactories

The construction of battery gigafactories is a significant driver for the R-142b market. Lithium iron phosphate battery chemistries require 1.5-2 kilograms of polyvinylidene fluoride (PVDF) binder per megawatt-hour, resulting in an additional demand of 850-1,130 tons of R-142b feedstock annually[1]Arkema, “Kynar PVDF Product Range,” arkema.com. Arkema’s expansion in Calvert City and Kureha’s new Iwaki production line will collectively add over 23,000 tons of PVDF nameplate capacity by mid-2026. Furthermore, the International Finance Corporation’s (IFC) December 2025 investment in Gujarat Fluorochemicals Limited (GFCL) EV Products marks India’s entry into the battery-grade PVDF supply chain. Binder specifications are increasingly shifting toward fluorosurfactant-free grades, such as Kynar HSV 900, which enable higher energy density and command premium pricing. Consequently, a growing portion of the R-142b market is now tied to long-term battery offtake agreements rather than spot refrigerant sales.

Expanding Fluorochemical Capacity Integration in China and India

Between 2024 and 2026, over 120,000 tons of annual fluorochemical capacity became operational in China and India, reducing conversion costs by up to 22% compared to merchant-feedstock models[2]SRF Limited, “Corporate Presentation,” srf.com. Projects like SRF Limited’s USD 894 million Dahej complex and Gujarat Fluorochemicals Limited’s plan for approximately 30,000 tons of captive R-142b capacity highlight a shift toward backward integration in the R-142b market. Chinese producers benefit from subsidized fluorspar mining and low-cost energy, providing them with a competitive export advantage even after accounting for logistics and tariff costs. Additionally, Daikin’s January 2026 launch of Daikin Chemical India Private Limited aims to support India’s growing semiconductor and battery industries, potentially driving future local demand for R-142b. These integrated capacity expansions are reshaping the global cost structure and intensifying market competition.

Growing Demand from Refrigeration and Blowing-Agent Blends

Despite regulatory challenges limiting incremental growth, legacy refrigeration applications continue to account for nearly half of the R-142b market. Existing supermarket, industrial process, and transport cold-chain equipment rely on blends containing R-142b, ensuring baseline demand as these systems are maintained, even as new installations adopt alternative solutions. In the foam-blowing segment, China’s 2026 hydrochlorofluorocarbon (HCFC)-141b ban is temporarily boosting demand, as polyurethane manufacturers transition to R-142b before eventually shifting to hydrofluoroolefin (HFO)-1233zd or hydrocarbon-based alternatives. This will result in a short-term increase in insulation-related demand for R-142b through 2028, after which virgin molecules will primarily be allocated to feedstock customers.

Kigali Allowance for Feedstock Exemptions Sustaining Supply

The Kigali Amendment provides exemptions for feedstock uses, allowing substances to be transformed or destroyed without being subject to phase-down schedules. This provision is now incorporated into the quota systems of the United States, the European Union (EU), and China. For 2026, the United States allocated 229.5 million metric tons of carbon dioxide equivalent (MTEVe) of production allowances, while China maintained a production quota of 3,360 tons and a domestic-use ceiling of 1,240 tons. These regulatory carve-outs establish a baseline level of support for the R-142b market as a chemical intermediate, even as refrigerant demand continues to decline.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Montreal Protocol phase-out for non-feedstock uses | -0.8% | Global, accelerated enforcement in the EU and North America | Short term (≤ 2 years) |

| Commercial availability of ultra-low-GWP substitutes (HFO-1234yf, CO₂) | -0.6% | North America, Europe, Japan | Medium term (2-4 years) |

| Volatile HF and chloroform input costs squeezing margins | -0.4% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Montreal Protocol Phase-Out for Non-Feedstock Uses

Developed countries are required to eliminate HCFC production by 2030, while Article 5 countries must follow by 2040. This will reduce legacy refrigerant and foam-blowing demand by 35-40% during the forecast period. China plans to cut its national HCFC quota by 12,200 tons for 2026 and will phase out HCFC-22 in VRF systems by January 2027, removing a key blend component that previously absorbed R-142b. In the United States, new VRF equipment using high-GWP HFCs will be banned starting in 2027, further limiting end-market volumes. The European Union’s 2024/573 Regulation prohibits servicing equipment with GWP greater than or equal to 150 from 2030, leaving inventories stranded in systems dependent on R-142b-rich blends. Additionally, stricter leak-repair thresholds are expected to reduce make-up volumes, weakening refrigerant demand.

Commercial Availability of Ultra-Low-GWP Substitutes

HFO-1234yf has achieved 90% penetration in new light-duty vehicles across Europe and North America, eliminating R-134a retrofit opportunities that could have absorbed R-142b. Transcritical CO₂ systems now account for approximately 30% of European supermarket refrigeration, while R-32 and hydrocarbon alternatives are increasingly used in small air-conditioning units. Honeywell’s Solstice LBA and Chemours’ Opteon blowing agents are scaling production and supporting customer transitions, replacing R-142b in polyurethane foam production. Natural refrigerants, such as propane and ammonia, are also being adopted in commercial heat pumps and chillers, significantly reducing the addressable market for R-142b in new HVAC equipment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Feedstock Pivot Redefines Growth Hierarchy

In 2025, refrigeration accounted for 47.82% of the R-142b market share. However, its growth is limited due to Environmental Protection Agency (EPA) regulations mandating reclaimed-only servicing for supermarket systems starting January 2029. Air-conditioning, which represents approximately one-fifth of the total demand, is declining as original equipment manufacturers (OEMs) transition to alternatives like R-32 or R-454B to meet efficiency and global warming potential (GWP) requirements. Foam blowing, while a smaller segment, is projected to grow at the fastest rate with a compound annual growth rate (CAGR) of 4.78%, driven by Chinese polyurethane manufacturers phasing out hydrochlorofluorocarbon-141b (HCFC-141b) by 2028. Additionally, demand for polyvinylidene fluoride (PVDF) and polyvinyl fluoride (PVF) feedstock is increasing at a faster pace, diverting high-purity R-142b molecules from commodity applications. Incremental PVDF capacity expected through 2028 will require an additional 12,000-15,000 tons of R-142b feedstock, further shifting the market focus toward specialty polymers.

As feedstock applications expand, producers are prioritizing long-term supply agreements with battery and semiconductor manufacturers. These agreements often include bundling R-142b with downstream polymer tolling to maximize value. This strategic shift is evident in collaborations such as the Chemours-SRF joint venture, which consolidates procurement volumes to secure allocations under tightening quotas. By 2031, the R-142b market share attributed to feedstock applications is expected to surpass refrigerant and foam-blowing uses, redefining demand patterns and pricing structures.

By Purity Grade: Semiconductor and Battery Specs Drive Premium Segment

High-purity R-142b (Greater than or equal to 99.9%) accounted for 61.35% of revenue in 2025 and is projected to grow at a CAGR of 4.81% through 2031. This growth reflects the stringent impurity requirements in PVDF polymerization and semiconductor etching processes. The high-purity segment commands a premium price of USD 700-1,200 per ton over industrial-grade supply, supported by the limited availability of electronic-grade hydrogen fluoride (HF) and fluorination capacity. Industrial-grade R-142b, primarily used in blend manufacturing, faces a structural decline as reclaimed refrigerants and ultra-low-GWP substitutes gain market share. Zhejiang Juhua’s 50,000-ton electronic-grade HF plant strengthens its leadership in the high-purity segment, while companies like Kureha and Arkema have secured multi-year offtake agreements to mitigate supply risks.

Manufacturers are also innovating to enhance performance, such as developing PVDF/polytetrafluoroethylene (PTFE) composite binders for greater than or equal to 4.5-volt cathodes, which could double binder loadings and increase R-142b usage per battery cell. Consequently, the R-142b market is diverging into a premium, price-insulated segment driven by technological advancements and a shrinking commodity segment constrained by regulatory pressures.

Geography Analysis

Asia-Pacific accounted for 45.76% of the 2025 market value and is expected to grow at a compound annual growth rate (CAGR) of 4.66% through 2031. This growth is driven by major Chinese companies such as Dongyue, Zhejiang Juhua, and Sinochem Lantian, which collectively control approximately 50% of global nameplate capacity. India is the fastest-growing sub-region, supported by SRF’s USD 894 million fluoropolymer complex and Gujarat Fluorochemicals’ planned 30,000-ton R-142b unit designed for captive polyvinylidene fluoride (PVDF) production. Japan continues to play a significant role in the high-purity segment, with companies like Kureha and Daikin supplying Korean and domestic battery plants transitioning to next-generation chemistries.

The Environmental Protection Agency’s (EPA) allowance system limits production to 229.5 million metric tons of carbon dioxide equivalent (MTEVe) for 2026. Despite this, PVDF capacity expansions at Arkema’s Calvert City facility and the Chemours-SRF partnership are expected to support feedstock demand. The implementation of reclaimed-only servicing rules in 2029 will redirect virgin supply from refrigeration applications to polymers, tightening the local commodity pool and emphasizing the strategic importance of integrated production capacity.

The European Union (EU) Regulation 2024/573 mandates a reduction in quotas to 10% of baseline levels by 2027-2029 and introduces a EUR 3 (USD 3.53) per ton carbon dioxide (CO₂)-equivalent fee starting January 2026, increasing costs for high-global warming potential (GWP) imports. In response, European original equipment manufacturers (OEMs) are accelerating the adoption of CO₂, hydrocarbons, and hydrofluoroolefins (HFOs). Additionally, PVDF demand is increasingly being met by Asian manufacturers exporting high-purity pellets outside the quota system. South America and the Middle East & Africa collectively contribute less than 10% of global revenue. However, these regions present growth opportunities in hot-climate heating, ventilation, and air conditioning (HVAC) systems and emerging battery industries, supported by investments aligned with the Belt and Road Initiative.

Competitive Landscape

The R-142b market is moderately consolidated. The five largest producers control approximately two-thirds of the total production capacity. Vertical integration is a key factor, as companies with ownership of fluorspar mines and hydrogen fluoride (HF) plants can produce R-142b at a cost of USD 800-1,000 per ton lower than merchant blenders, thereby maintaining margins against raw material price fluctuations. Arkema’s Kynar HSV 900, recognized with the 2025 American Chemical Society (ACS) Heroes of Chemistry Award, demonstrates how advancements in downstream applications can support upstream feedstock economics. Similarly, Daikin’s earlier equity investment in OCSiAl expands its presence in advanced composites and battery materials, providing a strategic approach to address commoditization in the traditional refrigerant market.

New market entrants include Indian companies such as Navin Fluorine and Tanfac, which benefit from Special Economic Zone (SEZ) incentives that reduce effective capital expenditure by nearly one-third and shorten the payback period to approximately five years. Private equity interest has also emerged, as demonstrated by Element Solutions’ USD 400 million acquisition of Electronic Fluorocarbons in January 2026, indicating growing interest in specialty gas niches within semiconductor supply chains. Concurrently, service-oriented companies like Linde are expanding refrigerant recovery and destruction networks, positioning themselves for a future dominated by reclaimed refrigerants, as mandated by United States (U.S.) and European Union (EU) regulations.

R-142b Industry Leaders

Zhejiang Juhua Co., Ltd.

DONGYUE GROUP

Arkema

SINOCHEM LANTIAN CO., LTD.

Zhejiang Sanmei Chemical Incorporated Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Element Solutions acquired Electronic Fluorocarbons to expand its specialty fluorochemical portfolio, including R-142b (1-Chloro-1,1-difluoroethane), a key compound used in semiconductor etching processes. This acquisition aligns with the company's strategy to address the increasing demand for high-purity fluorochemicals in the semiconductor industry.

- August 2025: Chemours and SRF established a strategic partnership to ensure the procurement of R-142b (Chlorodifluoromethane) and fluoropolymer tolling volumes. This collaboration aims to address the challenges posed by tightening quotas in the U.S. and EU, which regulate the production and supply of R-142b, a critical raw material used in the manufacturing of fluoropolymers. The agreement is expected to enhance supply chain stability and support compliance with regulatory requirements.

Global R-142b Market Report Scope

R-142b is a hydrochlorofluorocarbon (HCFC) used as a refrigerant, blowing agent, and chemical intermediate. Its stability at high temperatures makes it applicable for high-temperature heat pumps, air conditioning systems, and as a raw material in the production of vinylidene fluoride (VDF).

The R-142b market is segmented by application, purity grade, and geography. By application, the market is segmented into air conditioning, refrigeration, and foam blowing. By purity grade, the market is segmented into greater than or equal to 99.9 % (high-purity) and less than 99.9 % (industrial). The report also covers the market size and forecasts for R-142b in 16 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Air Conditioning |

| Refrigeration |

| Foam Blowing |

| Greater than or equal to 99.9% (High-purity) |

| Less than 99.9% (Industrial) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Spain | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Air Conditioning | |

| Refrigeration | ||

| Foam Blowing | ||

| By Purity Grade | Greater than or equal to 99.9% (High-purity) | |

| Less than 99.9% (Industrial) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Spain | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of R-142b Market?

The R-142b Market size was valued at USD 322.26 million in 2025 and is estimated to grow from USD 336.96 million in 2026 to reach USD 421.11 million by 2031, at a CAGR of 4.56% during the forecast period (2026-2031).

Which application currently dominates R-142b demand?

Refrigeration leads with 47.82% revenue share in 2025, though feedstock use is rising fast.

Why is PVDF growth so important for R-142b suppliers?

Each ton of PVDF requires almost one ton of R-142b feedstock, tying future demand to battery-cell and semiconductor expansion.

How will EU regulations affect R-142b imports?

Regulation 2024/573 introduces a EUR 3 (USD 3.53) per ton CO₂-equivalent fee from 2026 and steep quota cuts, lifting costs for high-GWP shipments.

Page last updated on: