Lutein Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

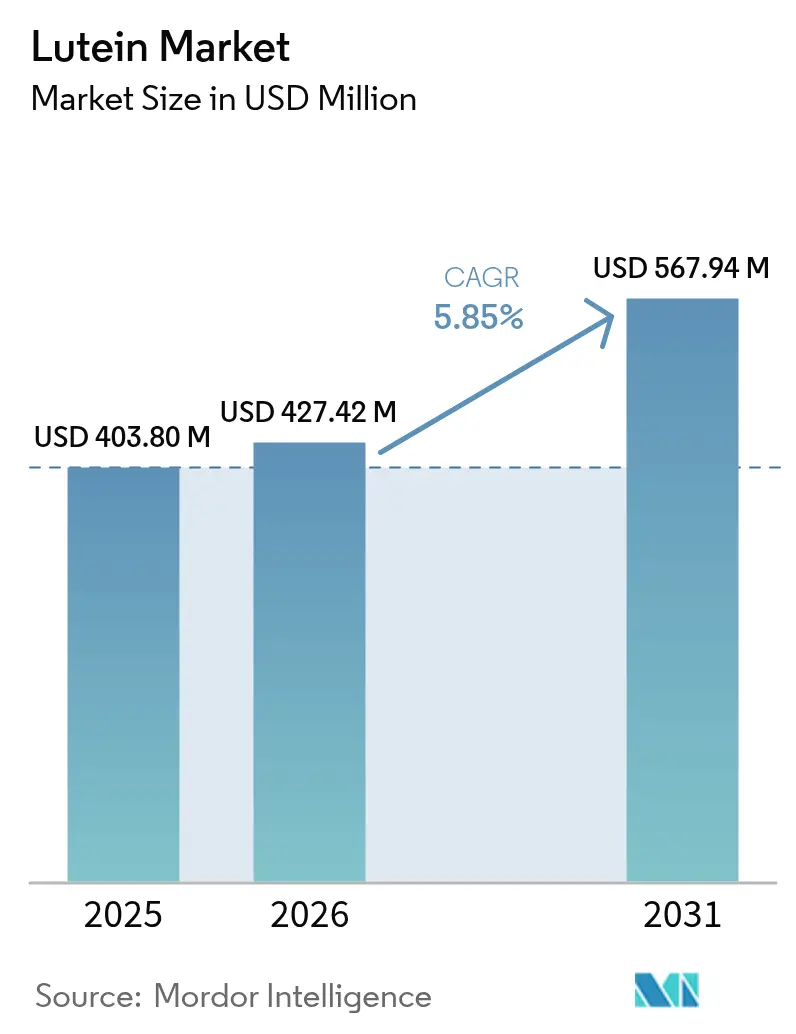

| Market Size (2026) | USD 427.42 Million |

| Market Size (2031) | USD 567.94 Million |

| Growth Rate (2026 - 2031) | 5.85% CAGR |

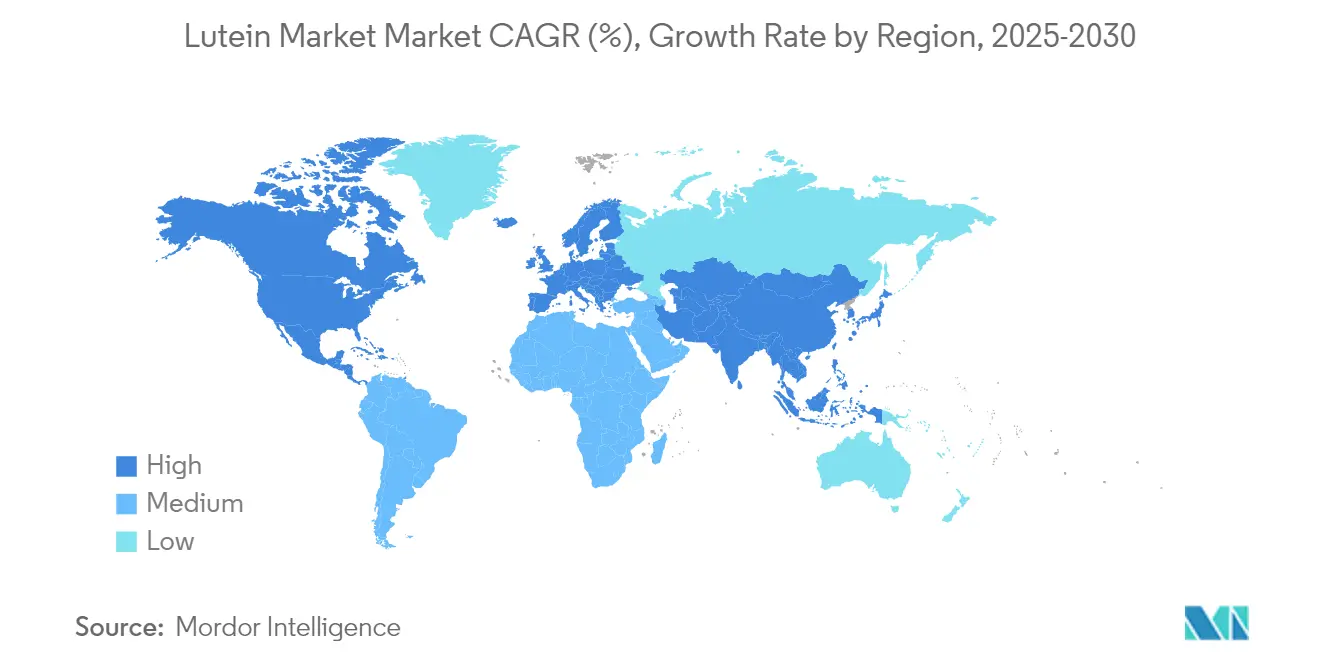

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

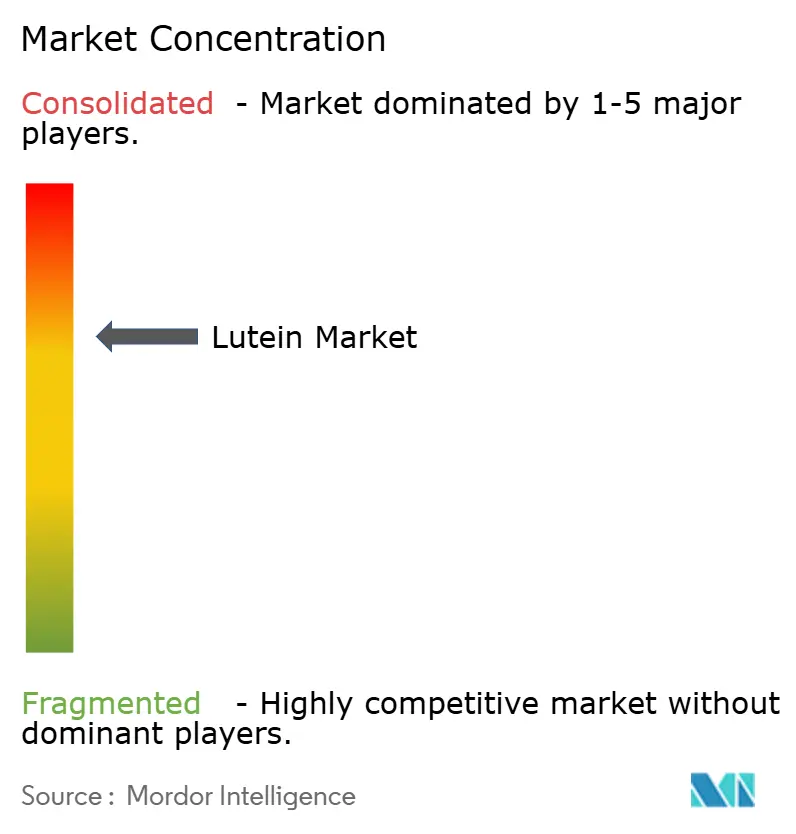

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Lutein Market Analysis by Mordor Intelligence

The global lutein market size was valued at USD 403.80 million in 2025 and estimated to grow from USD 427.42 million in 2026 to reach USD 567.94 million by 2031, at a CAGR of 5.85% during the forecast period (2026-2031). Driven by its recognized benefits for eye health, cognitive function, and preventive wellness, the lutein market is on a steady rise. As consumers increasingly gravitate towards natural, functional ingredients, lutein's presence is expanding in dietary supplements, fortified foods, and beverages. Preference for clean labels has made naturally sourced lutein the dominant choice, while there's a notable uptick in demand for nutraceutical-grade products. While powdered and crystalline forms of lutein are widely used, oil-based formats are carving a niche, especially in emulsified applications. Dietary supplements lead in usage, but cosmetics and personal care are emerging as rapidly growing segments. North America stands out as a major revenue contributor, yet the Asia-Pacific region is witnessing the swiftest growth, spurred by innovation and heightened health awareness. Key players are bolstering market confidence and diversifying products through strategic collaborations and increasing clinical validations of lutein's benefits. Moreover, advancements in extraction technologies and the growth of marigold cultivation are streamlining the supply chain and enhancing scalability. In developing regions, regulatory backing for natural antioxidants in functional foods is further propelling market penetration.

Key Report Takeaways

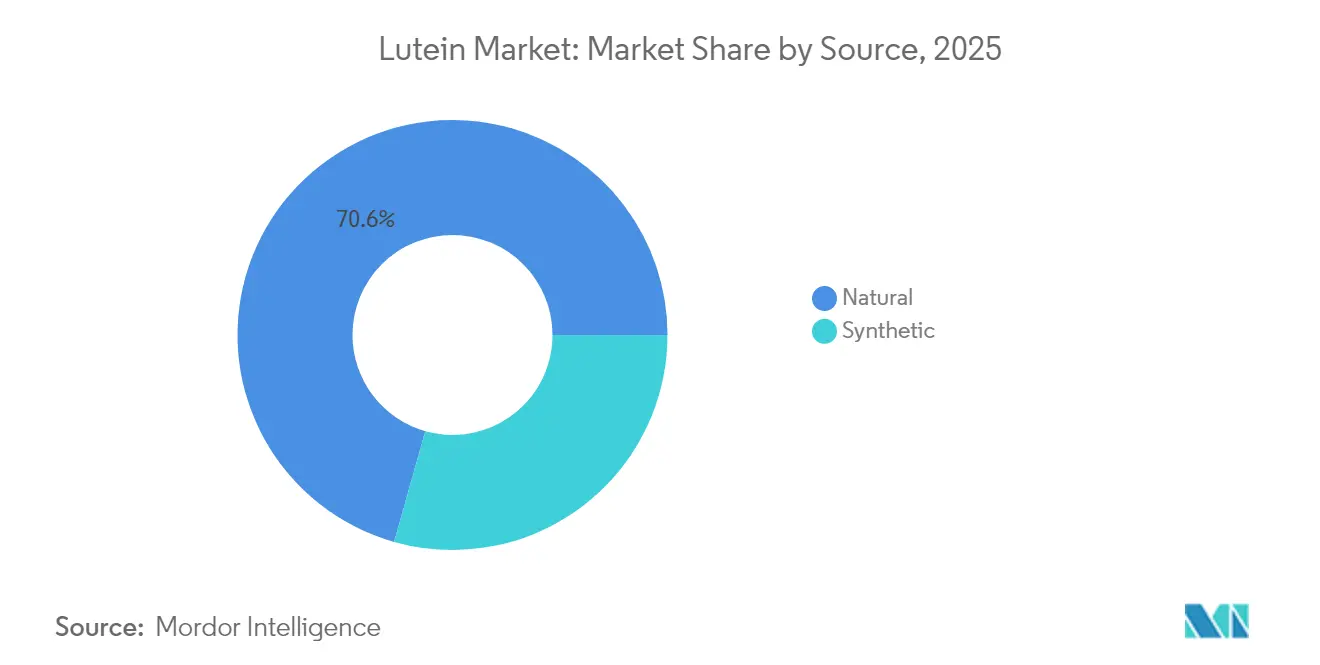

- By source, natural lutein led with 70.62% of the 2025 lutein market share and is set to expand at a 7.62% CAGR to 2031.

- By grade, the food grade captured 34.72% of the revenue in 2025, whereas the nutraceutical grade is projected to grow at a 7.39% CAGR during 2026-2031.

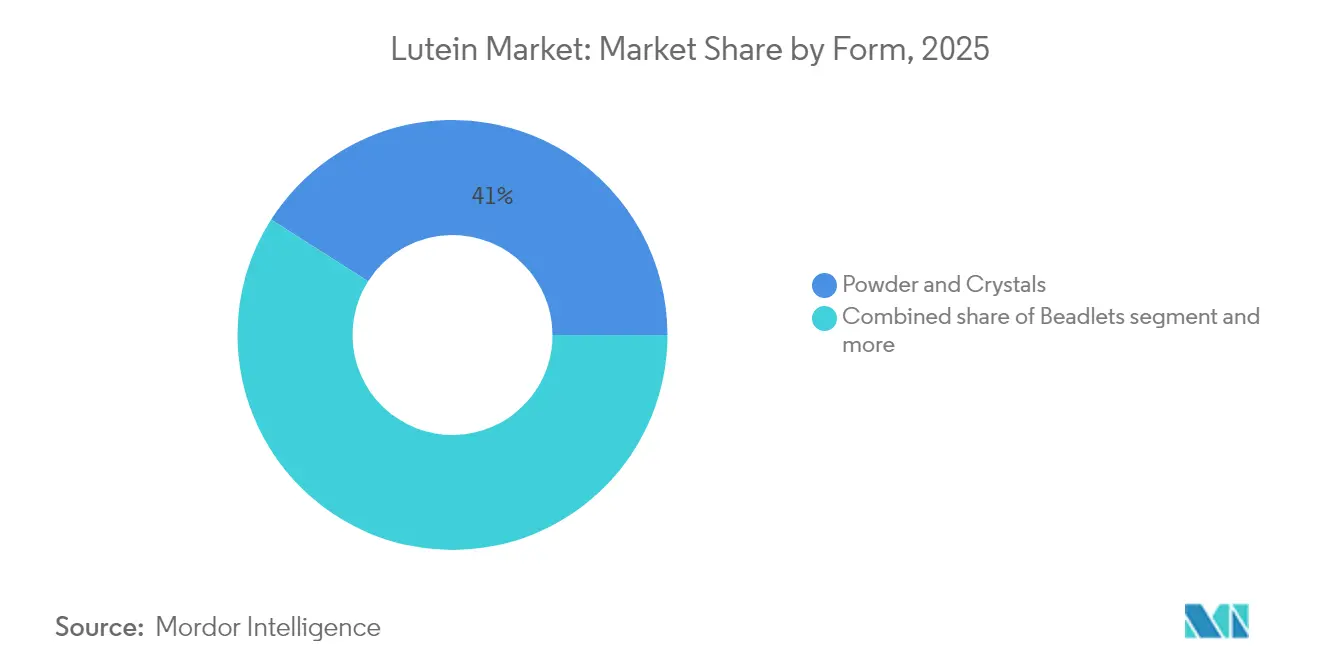

- By form, powder and crystals held 40.98% share of the lutein market size in 2025, while oil suspensions/ emulsions are forecast to rise at 6.78% CAGR through 2031.

- By application, dietary supplements accounted for 46.25% of 2025 revenue; cosmetics and personal care are advancing at an 7.74% CAGR over the same horizon.

- By geography, North America commanded 35.42% revenue in 2025; Asia-Pacific is the fastest region with a 7.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lutein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for eye health supplements and products | +1.8% | North America, Europe | Medium term (2-4 years) |

| Increasing focus on cognitive health solutions | +1.2% | Developed markets | Long term (≥ 4 years) |

| Growing adoption of functional foods and beverages with health-promoting ingredients | +1.5% | Asia-Pacific with spill-over to Western markets | Medium term (2-4 years) |

| Wide availability of raw materials, particularly marigold flowers | +0.9% | India, Mexico, Peru | Short term (≤ 2 years) |

| Expanding market for anti-aging skincare products | +1.1% | Global premium segments | Medium term (2-4 years) |

| Advancement in micro-algae fermentation reducing environmental impact | +0.8% | Technology hubs in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Eye Health Supplements and Products

The increased use of digital devices has led to higher demand for eye health supplements, particularly those containing lutein as a key ingredient. Research shows that lutein supplements improve macular pigment density and reduce eye strain in frequent screen users, with studies documenting better tear production and faster photo-stress recovery. The growing awareness of lutein's benefits has created a significant market opportunity in the eye health supplement sector. According to the Consumer Healthcare Products Association (CHPA), over-the-counter (OTC) eye care product sales in the United States reached 146 million units in 2024, indicating consistent consumer interest in eye health self-care [1]Source: Consumer Healthcare Products Association, “OTC Sales Statistics", chpa.org . This substantial market performance reflects the increasing consumer focus on preventive eye care measures and self-directed health management solutions. Companies are seeking regulatory approvals and developing new products to strengthen their position in the eye health market. The FDA granted GRAS (Generally Recognized As Safe) status to OmniActive's Lutemax Free Lutein for infant formula use in 2025 [2]Source: OmniActive Health Technologies, “FDA Acknowledges OmniActive’s Lutemax Free Lutein for Use in Infant Formula”,omniactives.com. This approval extends lutein's applications from adult supplements to infant nutrition, confirming its safety for visual and cognitive development in infants. The growing body of scientific evidence supporting lutein's efficacy in eye health maintenance has strengthened its position as a crucial ingredient in the eye health supplement market.

Increasing Focus on Cognitive Health Solutions

Lutein exhibits neuroprotective properties that extend beyond its known benefits for eye health. Research indicates lutein supports cognitive performance and brain health across different age groups. Its capacity to cross the blood-brain barrier and concentrate in neural tissues makes it significant for addressing neurodegenerative conditions and preventing cognitive decline. Clinical studies show that lutein and zeaxanthin supplementation enhances dynamic visual and cognitive performance in children, including increased brain-derived neurotrophic factor (BDNF) levels. Research demonstrates improvements in attention, episodic memory, and visuospatial processing, indicating lutein's impact on brain structure and function. Lutein has been shown to reduce neuroinflammation and oxidative stress in brain tissue. This evidence supports increased investment in cognitive health formulations that address the needs of aging and health-conscious populations. According to the Centers for Disease Control and Prevention (CDC), as of 2024, approximately 1 in 10 adults aged 45 and older report experiencing worsening memory loss or cognitive decline, while 1 in 4 report providing care for individuals with cognitive impairment [3]Source: Centers for Disease Control and Prevention, “Cognitive Health and Caregiving”, cdc.gov . These statistics underscore the need for evidence-based interventions, positioning lutein as a key component in cognitive health applications.

Growing Adoption of Functional Foods and Beverages with Health-Promoting Ingredients

Driven by a surge in consumer demand for nutritionally enriched products, the functional food and beverage sector is increasingly embracing lutein. For instance, beverages now commonly feature whey protein and lutein, showcasing the carotenoid's seamless integration into daily consumables. While natural sources of lutein are pricier than their synthetic counterparts, a growing preference for clean labels is steering the market towards the former, underscoring consumers' heightened emphasis on transparency and traceability. Owing to technological strides like microencapsulation and stabilization, earlier challenges in formulation have been surmounted. This progress allows for the stable and bioavailable incorporation of lutein into dairy, beverages, and baked goods. Leading the charge in this domain are manufacturers such as Kemin Industries, OmniActive Health Technologies, Chenguang Biotech Group, and Allied Biotech Corp., all of whom are pivotal in supplying lutein for food and beverage uses. As global interest surges in fortified products promoting eye health, cognitive function, and healthy aging, lutein is carving out a prominent role in worldwide functional product innovations.

Wide Availability of Raw Materials, Particularly Marigold Flowers

The cultivation of marigolds across India, Mexico, and Peru creates supply chain resilience, despite regional variations in cultivation practices and yield optimization. The global lutein market benefits from the consistent availability of raw materials, particularly marigold flowers, which serve as the primary natural source of lutein. The established marigold cultivation in India, China, and Latin American regions ensures a stable and cost-effective supply chain for lutein extraction. These regions provide suitable climatic conditions and reduced production costs, enabling efficient large-scale marigold farming. The ability to scale marigold cultivation maintains a consistent raw material supply for industrial extraction processes, meeting the increasing global demand across supplements, food, and pharmaceutical sectors. Improvements in farming practices and extraction technologies have enhanced lutein yield per hectare, increasing production efficiency and manufacturer profitability. The market's preference for natural lutein sources over synthetic alternatives reinforces the significance of marigold-derived lutein. The dual benefits of marigolds as a lutein source and income generator for farmers encourage sustained cultivation, strengthening supply chain stability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Significant fluctuations in raw material prices | -1.4% | Global, with acute impact in primary cultivation regions | Short term (≤ 2 years) |

| Strong competition from alternative ingredients | -1.1% | Global, with intensified competition in cost-sensitive markets | Medium term (2-4 years) |

| Consumer hesitation regarding synthetic lutein products | -0.8% | Developed markets with high clean-label awareness | Medium term (2-4 years) |

| Intricate extraction and purification procedures | -0.6% | Global, with higher impact on smaller manufacturers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Significant Fluctuations in Raw Material Prices

The lutein market faces a major constraint due to substantial fluctuations in raw material prices, primarily related to marigold flower cultivation. Marigold flowers, being the main natural source of lutein, are subject to agricultural output variations caused by climatic conditions, pest infestations, and seasonal supply-demand imbalances, which directly impact raw material availability and pricing. These price variations increase the overall costs of lutein extraction and production, reducing manufacturer margins and complicating price forecasting. Small-scale manufacturers are particularly vulnerable to these cost increases, which may result in market consolidation or diminished competitive positions. The pricing volatility is further intensified by geopolitical factors, trade restrictions, and changes in agricultural policies in key producing nations such as India and China. The unstable raw material prices also create difficulties in establishing long-term contracts and maintaining pricing stability for downstream applications across food, nutraceuticals, and pharmaceutical sectors. This instability can discourage substantial investments in new product development. Consequently, the fluctuating input costs continue to present a significant challenge for maintaining reliable supply chains and sustainable growth in the global lutein market.

Strong Competition from Alternative Ingredients

The lutein carotenoid market faces mounting competitive pressure from established and emerging alternatives such as beta-carotene, astaxanthin, lycopene, and zeaxanthin, which offer overlapping health benefits in areas like eye health, antioxidant support, and cognitive function. These alternatives often come with distinct cost-benefit profiles, allowing manufacturers to tailor formulations based on target demographics, regional preferences, and price sensitivity. Multi-carotenoid formulations that combine lutein with other carotenoids present significant market challenges, as such combinations may be perceived as more efficacious than single-ingredient products. This trend continues to divert demand away from pure lutein supplements, particularly in the nutraceutical and functional food sectors, where product differentiation remains crucial for market success. Synthetic carotenoids continue to compete aggressively in cost-sensitive markets, such as mass-market supplements and animal feed, where price often outweighs origin. Although consumer preference for natural and plant-derived ingredients restricts synthetic lutein's penetration in premium segments, ongoing advancements in synthetic biology and fermentation-based production methods may erode this gap over time, making synthetics more competitive both in price and perceived quality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Natural Dominance Drives Premium Positioning

Natural lutein sources accounted for 70.62% of the market share in 2025, driven by consumer preference for clean-label products and regulatory support for marigold-derived ingredients. The natural segment is growing at 7.62% CAGR (2026-2031), supported by increased applications in infant formula and functional foods where natural ingredients command premium pricing. Synthetic lutein alternatives, despite their cost advantages, face resistance from consumers, particularly in developed markets with high clean-label awareness.

The natural segment benefits from established extraction technologies and regulatory approvals, with JECFA's acceptable daily intake levels supporting broad food applications. Microalgae-based production has emerged as a natural alternative to traditional marigold sources, with research showing lutein productivity rates 3-6 times higher than conventional cultivation methods. While the synthetic segment maintains its position in cost-sensitive applications and industrial uses, regulatory scrutiny and consumer preferences favor natural alternatives. Biotechnological production methods using engineered microorganisms are creating a middle ground between natural and synthetic categories, offering scalable production with natural positioning.

By Grade: Food Applications Lead Market Expansion

In 2025, food-grade lutein commands a 34.72% market share, buoyed by extensive regulatory endorsements and a robust safety profile spanning diverse food categories. This surge in market share is largely attributed to the escalating appetite for fortified foods and beverages, as consumers increasingly seek preventive health benefits, especially for vision and cognitive enhancement, from their daily consumables. The nutraceutical-grade segment is on a rapid ascent, with projections indicating a 7.39% CAGR growth from 2026 to 2031. This momentum is fueled by a rising demand for dietary supplements and strong clinical validation of lutein's health advantages. Meanwhile, pharmaceutical-grade lutein is carving out a niche, thanks to its stringent quality benchmarks and its promising roles in ophthalmology and neurology.

Cosmetic-grade lutein is also on the rise, driven by advanced delivery mechanisms and a growing consumer inclination towards natural anti-aging remedies. Innovations like microencapsulation technologies are enhancing the stability and bioavailability of specialized formulations across these grades. Leading the charge in crafting versatile lutein formulations, which adhere to regulatory standards across food, supplements, pharmaceuticals, and personal care, are industry giants such as DSM-Firmenich, Divi’s Laboratories Ltd, and Flora Extracts Pvt. Ltd.

By Form: Powder Dominance Faces Innovation Challenge

In 2025, powder and crystal forms command the market with a 40.98% share. Their dominance stems from mature, scalable manufacturing technologies and cost-effective production, ensuring widespread accessibility for bulk formulation in the food, supplement, and feed industries. Long-standing regulatory acceptance and the ease of blending with dry formulations further bolster their position. These forms seamlessly integrate with globally popular delivery formats, including tablets, capsules, and powdered drink mixes.

Conversely, oil suspensions/emulsions are the fastest-growing segment, boasting a 6.78% CAGR. Their surge is attributed to enhanced bioavailability, particularly in fat-rich matrices such as dairy, functional beverages, and soft gels. These formats effectively overcome lutein’s traditional challenges of poor solubility and sensitivity to oxidation. The burgeoning popularity of ready-to-drink functional beverages and health shots has spurred demand for oil-based lutein forms, prized for their superior absorption and cleaner sensory profile. Beadlets are becoming increasingly popular for their controlled-release properties and stability during high-heat processing, making them a preferred choice for multivitamin formulations and gummy applications. Meanwhile, advanced systems like liposomes and nanoparticles are carving a niche in the “Others” category, delivering targeted solutions and enhanced bioefficacy, particularly in clinical nutrition and cosmeceuticals.

By Application: Supplements Drive Growth Across Health Sectors

In 2025, dietary supplements command a dominant 46.25% market share, largely attributed to robust clinical evidence underscoring lutein's efficacy in warding off age-related macular degeneration (AMD), boosting visual performance, and bolstering cognitive function. This segment enjoys widespread consumer acceptance of delivery formats like capsules, tablets, and softgels, which are particularly suited for lutein. Furthermore, heightened health awareness, especially among the elderly and those frequently exposed to screens, has spurred demand for eye health supplements, cementing lutein's status as a pivotal ingredient in vision care. Regulatory endorsements and health claims across various regions further bolster the segment's supremacy.

On the other hand, the cosmetics and personal care sector is witnessing the swiftest growth, with an 7.74% CAGR. This surge is driven by a burgeoning appetite for ingestible beauty products, or nutricosmetics, and skincare lines prioritizing natural antioxidants. Given lutein's established prowess in shielding skin from oxidative stress and blue light harm, it's become a sought-after ingredient in both topical and ingestible beauty solutions. The momentum is further fueled by cutting-edge delivery methods like microencapsulation and nanoemulsions, which boost skin absorption, coupled with a rising consumer inclination towards natural, plant-based actives in anti-aging and UV-defense products.

Geography Analysis

In 2025, North America commands a significant 35.42% share of the market, a position bolstered by its established regulatory framework. This framework not only includes FDA GRAS approvals for lutein in foods and infant formulas but also boasts extensive clinical validation from leading research institutions. The region's advanced dietary supplement industry thrives on a consumer base that prioritizes natural, scientifically validated ingredients like lutein. Retail infrastructures support premium product positioning, and consumers are increasingly willing to invest in clean-label and functional health products. Furthermore, with Health Canada recognizing lutein as a natural health product under Schedule 1, there's a boost in regulatory confidence, paving the way for cross-border product expansions.

Asia-Pacific is on a rapid ascent, forecasting a CAGR of 7.29% from 2026 to 2031. Rising disposable incomes, an aging populace, and a heightened urban focus on health fuel this growth. As Western dietary habits and wellness trends permeate, nations like China and India are experiencing a surge in the consumption of functional foods and dietary supplements. The region is also reaping the benefits of favorable regulatory endorsements, such as the European Union's nod to lutein esters (E 161b), which aids in regional adoption and aligns safety standards. Investments in domestic production and innovations in fortified food formats are propelling local manufacturing and boosting exports.

South America, along with the Middle East and Africa, holds significant untapped potential, especially in marigold-rich nations like Mexico and Peru. These areas are bolstering their extraction and processing capabilities, capitalizing on the availability of cost-effective raw materials and a surge in domestic demand. With regulatory harmonization and an influx of foreign investments in food processing, these regions are poised for accelerated market development in the coming years.

Regulatory Landscape

Regulation for lutein spans food additive, dietary supplement/novel food, and (in some markets) color additive frameworks, which creates region-specific compliance pathways for the same carotenoid ingredient. In the United States, market access commonly relies on FDA GRAS notices for defined uses and specifications, and in 2025 the FDA acknowledged OmniActive Health Technologies' Lutemax Free Lutein for use in infant formula, which broadens early-life nutrition applications under a high-scrutiny category.

In China, the National Health Commission and the State Administration for Market Regulation issued GB 1886.382-2025 (National Food Safety Standard for Food Additive Lutein) in March 2025, replacing GB 26405-2011, with mandatory compliance taking effect in September 2025. In Europe and the United Kingdom, lutein is regulated as a permitted food additive (E 161b) under the assimilated Regulation (EU) No 231/2012, and suppliers typically align technical specifications and labeling to these additive listings alongside safety evaluations such as JECFA guidance used as global reference points.

Value Chain Analysis

The lutein value chain starts with feedstock sourcing, dominated by marigold (Tagetes erecta) cultivation and harvest, followed by primary processing into oleoresin and downstream conversion into standardized lutein ingredients. Core steps include drying/pelletization (marigold) or dewatering (algae), solvent extraction of oleoresin, saponification to produce free lutein, purification and crystallization, and stabilization into commercial formats such as powders and crystals, beadlets, and oil suspensions/emulsions for B2B supply to supplement, food and beverage, pharmaceutical, animal feed, and cosmetics formulators.

Upstream supply is concentrated in key cultivation regions such as India and China, while secondary processing and formulation capacity are more distributed. Ingredient participants across these stages include Kemin Industries (FloraGLO), OmniActive Health Technologies (Lutemax), DSM-Firmenich, BASF SE, and Chenguang Biotech Group. The main value-chain risks center on agricultural seasonality and price volatility for marigold, along with product instability (oxidation and heat sensitivity), which raises the importance of encapsulation and controlled manufacturing. Regulatory requirements, including EU E 161b specifications and US FDA GRAS dossiers for defined applications, affect solvent choices, impurity controls, and traceability practices across suppliers and contract manufacturers.

Competitive Landscape

The lutein market is witnessing medium consolidation, with major players tightening their grip. DSM-Firmenich is rolling out a vitamin transformation initiative, focusing on boosting margins and weaving precision fermentation technologies into its production. This approach not only enhances production efficiency but also aligns with the growing demand for sustainable and innovative manufacturing practices. Kemin Industries, tapping into U.S.-grown marigold production and vertical farming, ensures consistent pigment content and a reliable year-round supply. By leveraging vertical farming, the company minimizes environmental impact while maintaining high-quality raw materials. BASF is teaming up with biotech firms to refine supercritical CO₂ extraction, aiming for enhanced yields and sustainability. This collaboration underscores BASF's commitment to adopting advanced technologies that improve extraction efficiency and reduce carbon footprints.

Meanwhile, Divi’s Laboratories Ltd. is pioneering microencapsulation delivery systems, boosting lutein's bioavailability and stability. These systems not only improve the functional properties of lutein but also expand its application potential across various industries. Such innovations facilitate effective segmentation across varied end uses, from cosmetics and functional foods to animal feed, enabling companies to implement premium pricing strategies and cater to niche markets.

Industry-wide research and development is honing in on sustainability, heightened bioefficacy, and clinically backed health benefits. Numerous manufacturers are joining forces with academic and clinical research entities, conducting randomized controlled trials to spotlight lutein’s benefits for both eye and cognitive health, with an eye on broader label claims. These trials provide robust scientific evidence, helping manufacturers differentiate their products in a competitive market. The race for nanoparticle-based delivery system patents is heating up, with top patent holders eyeing intellectual property licensing as a strategy to amplify their market presence.

Lutein Industry Leaders

-

Kemin Industries, Inc.

-

Allied Biotech Corporation

-

OmniActive Health Technologies

-

DSM-Firmenich N.V.

-

BASF SE

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory clearance in sensitive nutrition categories and tighter product specifications are expanding higher-value formulation space for lutein suppliers that can provide robust documentation, stability data, and traceability. A concrete proof point is the 2025 FDA acknowledgement of OmniActive Health Technologies' Lutemax Free Lutein for infant formula, which extends lutein's addressable uses beyond adult supplements into early-life nutrition. In that segment, ingredient qualification and consistency requirements are stringent and tend to favor established producers with validated supply chains.

Technology-led supply diversification is also creating room beyond marigold extraction, particularly to reduce exposure to agricultural volatility and to support nutraceutical-grade demand. In July 2025, KAIST researchers reported engineered Corynebacterium glutamicum producing 1.78 g/L lutein, pointing to ongoing progress in microbial platforms for fermentation-based supply options. On the demand side, EU authorization of lutein as a food color additive (E 161b) supports multi-function positioning (color plus antioxidant or health benefits) in fortified foods and beverages, and delivery-system innovation, including microencapsulation, beadlets, and oil dispersions, addresses formulation constraints that have limited lutein uptake in heat-processed and ready-to-drink formats.

Recent Industry Developments

- March 2026: OmniActive Health Technologies and Sirio Pharma announced a major collaboration to expand the lutein finished-format portfolio and accelerate commercialization across key markets. The partnership emphasizes consumer-friendly dosage forms and multi-market distribution, indicating a broader approach beyond single product releases.

- June 2025: OmniActive Health Technologies received US FDA acknowledgement for the use of Lutemax Free Lutein in infant formula under the GRAS pathway. The milestone expands lutein's permitted use into early-life nutrition, a highly regulated application with stringent safety and specification expectations. It strengthens OmniActive's positioning with infant formula manufacturers and raises the bar for documentation among competing suppliers.

- February 2024: Divi's Laboratories began Phase I operations at its Kakinada Unit-III manufacturing facility. The site supports backward integration by producing starting materials for Divi's core manufacturing units and extends capabilities relevant to nutraceutical API manufacturing. Greater internalization of upstream inputs can improve supply reliability and cost control for ingredient-grade offerings.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as the value of lutein ingredient sold into commercial use, where lutein is supplied as an identifiable ingredient grade across common forms such as powder, beadlet, oil dispersion, or crystalline material.

Scope exclusions: finished consumer products (for example eye health capsules or fortified foods) and broad carotenoid blends that are not clearly sold as lutein are excluded.

Segmentation Overview

-

By Source

- Natural

- Synthetic

-

By Grade

- Feed Grade

- Food Grade

- Pharmaceutical Grade

- Cosmetic Grade

- Nutraceutical Grade

-

By Form

- Powder and Crystals

- Beadlets

- Oil Suspensions/Emulsions

- Others

-

By Application

- Dietary Supplements

- Food and Beverage

- Pharmaceuticals

- Animal Feed

- Cosmetics and Personal Care

- Other Applications

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- France

- United Kingdom

- Spain

- Netherlands

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Rest of South America

-

Middle East and Africa

- United Arab Emirates

- South Africa

- Saudi Arabia

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the starting boundaries and to keep assumptions anchored to public signals that can be rechecked. We mainly referenced official agriculture and trade data for marigold and botanical inputs, import and export statistics, and food additive and supplement related references from regulators (where lutein permissions and use levels are discussed).

To support this work, we also reviewed sources such as customs and tariff line trade portals, government agriculture agencies, peer reviewed nutrition and ophthalmology journals, and trade association publications connected to pigments and nutraceutical ingredients. Company filings, investor presentations, and reputable press releases were used to confirm capacity additions, product positioning, and general pricing direction. In a few cases, paid subscriptions for company financials and patent databases were used to validate ownership changes and innovation activity. The sources listed above are illustrative only, since many other references were also checked during validation and clarification.

Primary Interviews and Surveys

Primary work was used to pressure test what we saw in public sources, especially realized pricing, grade splits, and how demand is changing by application. We spoke with a mix of ingredient suppliers, downstream formulators, distributors, and technical experts across APAC, EMEA, and the Americas, then used those inputs to confirm the key assumptions that drive the model outputs.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 13% | APAC: 43% |

| Mid tier: 61% | Functional/Unit leaders: 32% | EMEA: 35% |

| Smaller Players: 14% | Managers: 55% | Americas: 22% |

Market-Sizing & Forecasting

Market sizing is built using a top-down approach where production and trade signals for key botanical and ingredient supply routes are translated into an addressable ingredient demand pool, then converted into value using market-consistent pricing. Since reporting labels can vary by country and grade, we focus on the portion that is commercially sold as lutein ingredient and then allocate it across major consuming uses.

To keep totals realistic, we corroborate them with selective bottom-up approximations, such as sampled supplier revenue checks, channel feedback on volume movement, and a simple ASP multiplied by volume build for the most visible use cases. Inputs that materially move the model include lutein ingredient pricing by grade and form, marigold cultivation and extraction availability, demand pull from eye health and nutrition positioning, animal feed usage for pigmentation, and regional import reliance that affects delivered costs. Forecasts are mainly shaped through scenario analysis, where demand and pricing paths are adjusted based on expert consensus and then stress tested against what distributors and formulators expect to change over the next few years. When gaps appear in company level data, values are bridged using peer averages and capacity based indicators, then reviewed again during interviews.

Data Validation & Update Cycle

Validation is done through structured cross checks across at least three angles: supply indicators, pricing logic, and end use demand signals. We compare model outputs against independent metrics such as trade flows, reported capacity changes, and observed price ranges, and then drill into any variance that looks too large for a given region or application.

Before sign off, the model is reviewed in multiple steps so assumptions and calculations are checked for consistency and arithmetic integrity. If an unexpected shift is noticed, such as a raw material swing or a large pricing reset, relevant experts are recontacted to confirm whether it is temporary or structural. Reports are refreshed annually, and interim updates are made when material events can change demand or supply, followed by a final pre delivery pass so the latest updates are reflected.

Mordor Intelligence's Lutein Market Size Measured Against Other Published Estimates

Published estimates for lutein can look different even when the topic name is the same, since the counted scope and the pricing logic behind the totals are not always aligned. Differences also come from the selected starting year, the way inflation and currency timing are handled, and whether the number is built as an ingredient market or a finished product market.

By tracking realized ingredient grade pricing and checking import reliance by region, Mordor Intelligence keeps the lutein market total tied to pure lutein ingredient sales rather than broad carotenoid mixes or consumer product revenues, which is one practical reason the published values do not match. In addition, some estimates apply more aggressive demand growth in supplements without matching it to supply availability and delivered cost changes, which can widen the spread over time.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 427.42 M (2026) | |

| Global Consultancy A | USD 387.69 M (2025) | Uses a different base year and does not clearly separate pure lutein ingredient revenue from adjacent carotenoid category reporting, which can shift the starting total before forecasting is applied. |

| Industry Publisher B | USD 283.13 M (2025) | Appears to run a narrower revenue boundary and a more conservative pricing baseline, which can occur when lower-grade mixes and application-specific demand are excluded or valued at lower assumed ASPs. |

The comparison shows that most of the variance is explained by what is counted as lutein and how pricing is set in the base year, followed by how demand growth is layered into supplements and feed use. When scope is kept consistent to pure ingredient sales and the price and volume assumptions are checked against trade and channel signals, the resulting market size is easier to trace and repeat.

Key Questions Answered in the Report

What is the current value of the lutein market and how fast is it growing?

The lutein market was worth USD 427.42 million in 2026 and is projected to reach USD 567.94 million by 2031, reflecting a 5.85% CAGR.

Which source dominates supply?

Natural lutein from marigold commands 70.62% share, with an 7.62% CAGR forecast due to strong clean-label demand.

Why is lutein increasingly added to infant formula?

FDA GRAS clearance confirmed safety in 2025, enabling manufacturers to target early-life vision and cognitive development.

Which application is expanding the fastest?

Cosmetics and personal care show the highest 7.74% CAGR, leveraging lutein’s antioxidant and blue-light filtering properties.

Page last updated on: