Flavonoid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.49 Billion |

| Market Size (2031) | USD 1.89 Billion |

| Growth Rate (2026 - 2031) | 4.85% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Flavonoid Market Analysis by Mordor Intelligence

The flavonoids market size was valued at USD 1.42 billion in 2025 and estimated to grow from USD 1.49 billion in 2026 to reach USD 1.89 billion by 2031, at a CAGR of 4.85% during the forecast period (2026-2031). The market growth is driven by regulations supporting natural colorants, improved extraction technologies, and increased consumer demand for functional nutraceuticals and cosmetics. The Food and Drug Administration's amendment to color additive regulations now permits the expanded use of butterfly pea flower extract in various food products, including ready-to-eat cereals, crackers, snack mixes, hard pretzels, plain potato chips, corn chips, tortilla chips, and multigrain chips at levels aligned with good manufacturing practice (GMP). This regulatory change, effective June 26, 2025, responds to a color additive petition (CAP) from Sensient Colors, LLC, and indicates an industry shift toward botanical pigments.[1]Source: Federal Register, "Listing of Color Additives Exempt From Certification; Butterfly Pea Flower Extract", federalregister.gov Moreover, Ohio State University's development of shelf-stable anthocyanin blues enhances functionality in acidic environments. North America dominates the market due to established FDA guidelines, while the Asia-Pacific region shows growth driven by increasing disposable income and favorable nutraceutical regulations. Supply constraints in citrus and berries affect raw material availability; however, fermentation-based production methods offer potential solutions to stabilize price fluctuations.

Key Report Takeaways

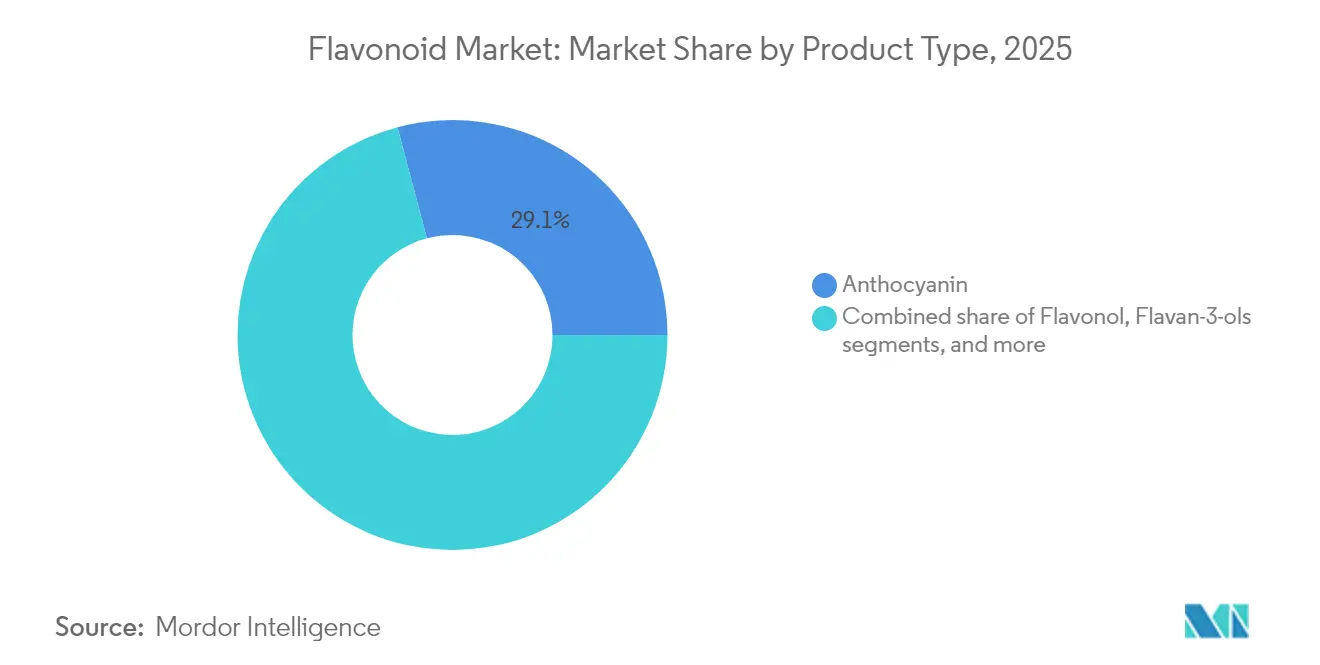

- By product type, anthocyanins led with 29.12% of the Flavonoids market share in 2025, while flavonols recorded the highest 6.12% CAGR through 2031.

- By source, berries captured 27.10% share of the Flavonoids market size in 2025; herbs and spices are projected to expand at 6.33% CAGR between 2026-2031.

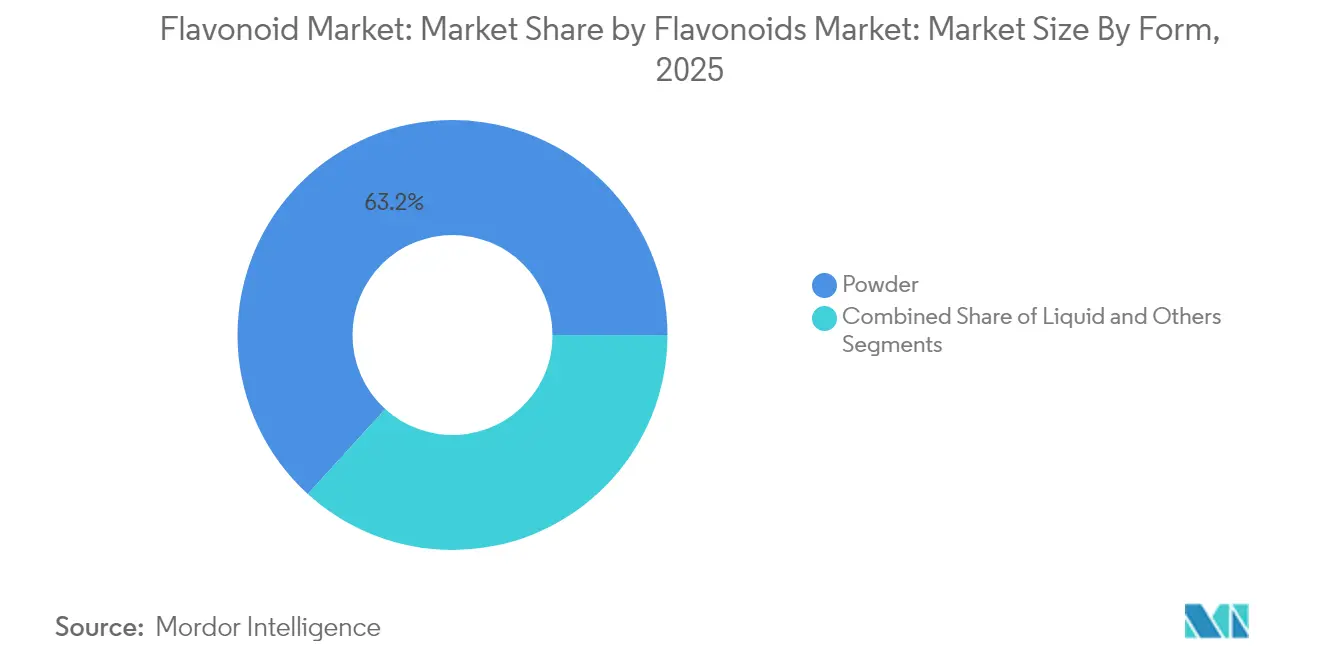

- By form, powder commanded 63.25% share of the Flavonoids market size in 2025; the innovative “other” segment advances at 6.45% CAGR through 2031.

- By application, nutraceuticals held 35.20% of the Flavonoids market share in 2025 and are advancing at 5.55% CAGR through 2031.

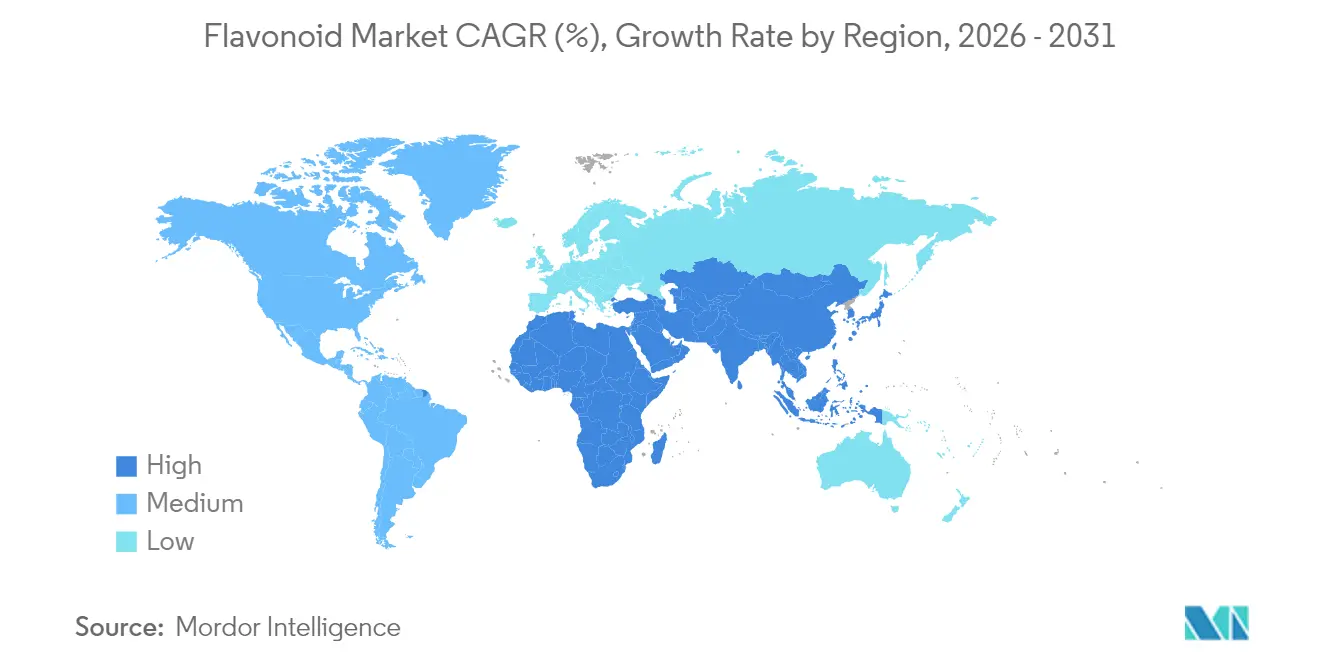

- By geography, North America dominated with 32.10% revenue share in 2025; Asia-Pacific exhibits the swiftest 6.14% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Flavonoid Market Trends and Insights

Flavonoids Market: Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for anti-inflammatory joint health supplements | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Antiviral and antimicrobial applications in natural remedies | +0.8% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Use as natural colorants in food and beverage | +1.5% | Global | Short term (≤ 2 years) |

| Increasing demand for anti-bacterial properties in skincare products | +0.9% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Expanding consumer preference for natural and functional food ingredients | +1.1% | Global | Medium term (2-4 years) |

| Technological innovations drive efficient extraction and purification methods | +0.7% | Global, with early adoption in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Anti-Inflammatory Joint Health Supplements

The increasing elderly population and growing focus on preventive healthcare drive the demand for flavonoids in joint health applications, as quercetin and other flavonoids show proven anti-inflammatory properties. In February 2025, the Food and Drug Administration's final rule updated the definition of "healthy" as an implied nutrient content claim to align with current nutrition science and Federal dietary guidance, particularly the Dietary Guidelines for Americans.[2]Source: Federal Register, "Food Labeling: Nutrient Content Claims; Definition of Term Healthy", federalregister.gov This revision establishes requirements for using "healthy" in human food product labeling, helping consumers identify nutritious foods that align with dietary recommendations and encouraging manufacturers to fortify snacks and beverages with flavonoids that meet nutrient-density criteria. The nutraceutical market continues to consume higher volumes, maintaining premium raw-material prices despite increased competition. The combination of flavonoids with conventional active ingredients reduces pill consumption and improves consumer adherence, establishing flavonoids as complementary ingredients rather than replacements. The industry's focus on joint-health claims is evidenced by investments in pilot-scale encapsulation facilities.

Antiviral and Antimicrobial Applications in Natural Remedies

Growing health awareness drives the incorporation of flavonoids in immune support products, as compounds such as baicalin and baicalein demonstrate proven antiviral and antimicrobial effects in clinical studies. The therapeutic use of flavonoids increases as regulatory bodies in Asian countries, especially China and India, recognize traditional herbal medicines containing these compounds, establishing comprehensive market entry pathways and standardized approval processes. Asian nutraceutical regulations emphasize stringent safety and efficacy standards, favoring scientifically validated flavonoid compounds through extensive research and documentation requirements. The ability of flavonoids to serve both preventive and therapeutic functions strengthens their position in the immune health market, particularly as consumers seek natural alternatives supported by robust scientific evidence and clinical validation. This dual functionality, combined with increasing regulatory acceptance and consumer demand, creates significant opportunities for manufacturers developing flavonoid-based immune support products.

Use as Natural Colorants in Food and Beverage

The flavonoid market is undergoing significant changes due to increasing consumer demand for natural and clean-label products. Food manufacturers are responding by reformulating their products with natural ingredients, which has increased flavonoid usage across multiple applications. The industry has increased investments in research and development to improve the stability and functionality of flavonoid-based ingredients, particularly for food and beverage products. The FDA's 2025 approval of three natural colors created new market opportunities and supported the food industry's transition from artificial to natural colorants.[3]Source: FDA, "FDA Approves Three Food Colors from Natural Sources", fda.gov This regulatory development coincided with improvements in colorant stability technology. The European Union's ongoing comprehensive review of food colors, including Vegetable carbon (E 153) and Iron oxides (E 172), benefits natural alternatives that meet safety standards.[4]Source: European Food Safety Authority, "Food Colors" efsa.europa.eu Food manufacturers are increasingly using anthocyanin-rich sources, particularly berries, to provide both visual appeal and health benefits. The combination of regulatory support, technological advancements, and consumer preferences is driving the adoption of flavonoid-based colorants in beverages, confectionery, and processed foods.

Increasing Demand for Anti-Bacterial Properties in Skincare Products

The cosmetics industry is incorporating functional ingredients, particularly flavonoids, into skincare formulations based on their proven anti-aging and photoprotective properties. Research shows that anthocyanins enhance collagen production and protect skin cells from UV-induced oxidative damage, making them essential components in anti-aging products. The combination of apigenin and phloretin serves as an effective alternative to hydroquinone for treating melasma, resulting in new brightening serum formulations. European regulations list 309 permitted colorants, including botanical sources, providing manufacturers with clear compliance guidelines for product development. The nutricosmetics market expansion indicates increased consumer awareness of the relationship between internal antioxidant consumption and skin health, leading to integrated supplement and topical product offerings with standardized flavonoid extracts. This development has resulted in comprehensive skincare solutions addressing both internal and external skin health factors. Product communication now emphasizes scientific evidence over traditional natural ingredient messaging, highlighting the documented effectiveness of flavonoid-based formulations for specific skin concerns.

Flavonoids Market: Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited shelf life | -0.8% | Global | Short term (≤ 2 years) |

| Regulatory restriction on health claims | -0.6% | North America and Europe primarily | Medium term (2-4 years) |

| Potential allergic reaction and drug interactions | -0.4% | Global | Long term (≥ 4 years) |

| Dependency on seasonal and regional crop supply | -1.2% | Global, acute in citrus-dependent regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Shelf Life

The degradation of flavonoids during storage and processing creates significant technical and economic challenges for market growth, particularly in applications requiring long shelf life. The stability of anthocyanins heavily depends on environmental factors such as pH levels, temperature conditions, and light exposure, which directly affect their biological effectiveness and commercial viability in various applications. Advanced encapsulation technologies and co-pigmentation methods, while effective in improving stability, significantly increase production costs and add complexity to manufacturing processes. Anthocyanin-based intelligent packaging systems function as comprehensive pH indicators, providing sophisticated color-change capabilities for continuous product monitoring throughout the supply chain. Ongoing research on flavonoid-based nanogels demonstrates considerable potential for improved stability and bioavailability, though scaling these solutions for commercial production remains technically challenging. These stability concerns primarily impact the food and beverage industry, where natural colorants must consistently maintain their visual and functional properties throughout extended distribution and storage periods, often lasting several months.

Dependency on Seasonal and Regional Crop Supply

Climate-related supply disruptions significantly affect the pricing and availability of flavonoids, particularly those derived from citrus fruits and berries. The impact extends across the entire supply chain, from agricultural production to final product manufacturing. According to the European Commission, the European Union's citrus production (excluding grapefruit) decreased from 10.3 million tons in 2022 to 7.4 million tons in 2023, primarily due to drought, restricted irrigation, and high temperatures.[5]Source: European Commission, "Citrus fruit statistics", agriculture.ec.europa.eu Environmental stresses, such as temperature fluctuations and increased pest pressures in kiwifruit production, demonstrate the vulnerability of flavonoid source crops to changing climate patterns. The geographic concentration of flavonoid sources creates substantial systemic risks for global pricing and availability, especially as demand growth exceeds supply expansion in key agricultural regions. In response to these challenges, companies implement comprehensive supply chain resilience strategies, including geographic diversification, alternative source development, and improved storage solutions to maintain market stability and ensure consistent supply to meet growing market demands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Anthocyanins Retain Lead While Flavonols Accelerate

Anthocyanins dominated the Flavonoids market with a 29.12% share in 2025, driven by their applications as natural colorants and antioxidants. Recent regulatory approvals for butterfly pea and increased demand for natural blue colors in beverage reformulations support this segment's growth. Flavonols, particularly quercetin, demonstrate a 6.12% CAGR, supported by expanding applications in cardiovascular and metabolic health. Recent developments in water-soluble 3-hydroxyflavonol technology enhance bioavailability, increasing clinical applications. Flavan-3-ols maintain stable growth due to FDA cardiovascular qualified health claims for cocoa powders, while flavones and isoflavones serve specific hormonal health applications. During the forecast period, increased therapeutic validation and pharmaceutical trials position flavonols to reduce the market share gap.

The market for flavonols continues to expand through ongoing research and development, while anthocyanins maintain their market position through color innovation. Manufacturers gain competitive advantages through improved stability technologies, securing premium contracts with major beverage and beauty companies. Growing clinical evidence for flavonol efficacy is expected to increase healthcare provider acceptance and expand over-the-counter availability, facilitating broader market penetration in mainstream health channels.

By Source: Berries Dominate but Herbs and Spices Gain Ground

Berries contributed 27.10% of the Flavonoids market size in 2025, supported by established supply chains and widespread use of blueberry and blackcurrant extracts. However, climate-related yield variations create price volatility that affects processor margins. The herbs and spices segment grows at 6.33% CAGR, supported by the continuous cultivation of Scutellaria and rosemary, which provide concentrated active compounds at lower doses. Citrus maintains its market position through efficient hesperidin production, though disease and drought concerns lead to geographic diversification of sources. Soybean isoflavones serve the menopause support segment, while tea and cocoa maintain stable demand due to traditional consumption patterns.

Manufacturers distribute sourcing across hemispheres to minimize weather-related disruptions and maintain market stability. Fermentation facilities test baicalin production using stainless-steel bioreactors, reducing dependence on crop cycles and minimizing pesticide exposure. This approach ensures consistent quality and meets environmental, social, and governance (ESG) requirements, positioning herb-derived and fermentation-derived flavonoids as risk management tools. As regulatory requirements for product disclosure increase, supply chain traceability becomes crucial in supplier selection, benefiting sources with comprehensive audit systems.

By Form: Powder Remains Pre-Eminent While Novel Systems Emerge

Powder formats maintained a 63.25% market share in 2025, primarily due to their shelf stability, ease of blending, and compatibility with existing dry-mix infrastructure. Liquid variants are essential for beverage and cosmetic emulsions requiring rapid dispersion but face challenges with oxidation and microbial contamination, which reduce shelf life. The "others" category, experiencing a 6.45% CAGR, includes nanogels, beadlets, and co-extruded cylinders that improve bioavailability and enable pH-triggered release. Aqueous two-phase extraction technology produces high-purity concentrates suitable for injectable pharmaceuticals.

End-users prioritize cost per effective dose over raw material costs, making high-loading beadlets economically viable despite higher unit prices. Advanced moisture-barrier film packaging helps maintain product potency and reduces waste. The industry's shift toward clean labels has increased the adoption of solvent-free granulation methods. While powder formats continue to dominate the Flavonoids market, the industry is gradually moving toward specialized delivery systems that influence product development strategies.

By Application: Nutraceuticals Drive Multi-Sector Expansion

Nutraceuticals hold 35.20% of the Flavonoids market share in 2025 and maintain a 5.55% CAGR, driven by physician-supported claims for joint health, liver function, and immune system support. Food and beverage manufacturers are reformulating products with plant-based colors, supported by the 2025 GRAS regulatory reforms emphasizing transparency. The pharmaceutical industry is conducting Phase 1 and Phase 2 clinical trials of chrysin and quercetin for metabolic disorders, suggesting potential prescription drug development. The cosmetics industry incorporates anthocyanin complexes for UV protection, with increasing adoption of combined topical and oral treatment approaches.

The animal feed industry is evaluating Scutellaria flavonoids as natural growth promotants, in response to regulations limiting antimicrobial use in livestock. Multi-purpose applications, such as packaging films that function as pH indicators, demonstrate how single extracts can benefit multiple industrial segments. This diversification protects the Flavonoids market from demand fluctuations in individual sectors while encouraging innovation that extends intellectual property across multiple categories.

Geography Analysis

North America accounted for 32.10% of 2025 revenue, supported by FDA health-claim clarity and established supplement distribution channels. The region faces challenges from citrus greening disease and extreme weather conditions, driving companies to source ingredients from Latin America or through fermentation processes. IFF's USD 70 million investment in February 2025 to expand its Cedar Rapids, Iowa, facility by 47,000 square feet demonstrates a commitment to domestic production. The expansion, scheduled for completion in 2026, will increase Taura by IFF fruit ingredients production to serve the healthy snacks market. While retailers value U.S.-grown ingredients, buyers accept imported alternatives during domestic supply shortages and price increases.

Asia-Pacific shows the highest growth rate at 6.14% CAGR, driven by expanding middle-class consumption, acceptance of traditional medicine, and emerging manufacturing centers. China's incorporation of validated flavonoids in its functional-food catalogue and India's Ayurvedic standards create efficient approval processes, reducing time-to-market. The expansion of e-commerce beyond urban areas increases market penetration and sales volume.

Europe maintains consistent growth, supported by strict additive regulations and environmentally conscious consumers. EFSA's reassessment of existing colorants creates opportunities for flavonoid alternatives that avoid extensive toxicological reviews. Ongoing drought conditions reduce EU citrus production, limiting regional hesperidin availability and increasing interest in Blackcurrant and Elderberry alternatives. The cosmetics industry in France and Italy benefits from comprehensive regulations covering 309 approved colorants, facilitating faster development of skincare products containing flavonoids.

Regulatory Landscape

In the United States, flavonoid-based ingredients used as colors, extracts, or functional components generally sit under FDA food additive and GRAS pathways, with labeling and implied nutrient content claims shaping go-to-market approaches for nutraceuticals and fortified foods. A near-term compliance inflection point is the FDA agenda item (RIN 0910-AJ02), which targets amendments to 21 CFR parts 170 and 570 to introduce mandatory GRAS notice submissions for certain human and animal food uses. The agenda lists a proposed rule timing aligned to December 2026, which raises the bar for documentation and early regulatory engagement for novel or high-use botanical flavonoid preparations.

In Europe, flavonoid concentrates and certain botanical extracts are governed by the Novel Food Regulation (EU) 2015/2283, with EFSA risk assessment underpinning authorization and, in some cases, time-limited data protection. Recent EU actions illustrate this pathway: in February 2025, the European Commission authorized glucosyl hesperidin for placing on the market as a novel food for a five-year period (for Nagase Viita Co., Ltd.). In parallel, the Novel Food Catalogue update (January 2026) reinforced that while some plant parts used in supplements may be non-novel, purified bioflavonoids such as quercetin and rutin can still trigger pre-market authorization when supplied at specific high-concentration criteria. This influences ingredient standardization decisions for supplement and functional food launches.

Value Chain Analysis

The flavonoid value chain starts with agricultural feedstocks (citrus fruits, berries, tea, cocoa, and herbs and spices) and extends through primary processing, extraction and purification, formulation (powders, liquids, and delivery systems such as beadlets or liposomal formats), and distribution to food and beverage, nutraceutical, pharmaceutical, and cosmetic manufacturers. Crop seasonality and climate variability in key sources, notably citrus and berries, remain upstream risks that affect availability, quality consistency, and pricing. As a result, buyers tend to tighten specifications, increase traceability expectations, and diversify origins.

Value addition is concentrated in extraction, purification, and stabilization. Suppliers use technologies such as supercritical fluid extraction, ultrasound-assisted extraction, and microwave-assisted extraction to improve yield and reduce solvent and energy intensity. Downstream, regulatory compliance, including FDA GRAS/food additive status in the United States and EFSA-led evaluations, E-number additive rules, and EU Novel Food procedures, increases documentation and quality system requirements. This tends to favor integrated operators and audited suppliers. To reduce dependence on harvest cycles and meet clean-label and sustainability requirements, the chain is also incorporating precision fermentation and advanced encapsulation platforms to convert commodity feedstocks into standardized, application-ready flavonoid ingredients.

Competitive Landscape

The global flavonoid market is moderately fragmented. The market features prominent players like The Merck Group, Indena S.p.A., Cayman Chemical Company, and Layn Natural Ingredients, among others, leading the industry through various strategic initiatives. Companies are heavily investing in research and development to discover novel flavonoid compounds and enhance existing product portfolios, particularly focusing on improving bioavailability and efficacy.

Moreover, companies have developed solvent-free fermentation technology that reduces solvent disposal costs and increases product purity to pharmaceutical standards. The increase in patent filings for microfluidic and high-pressure homogenization techniques indicates growing competition for intellectual property rights and associated royalty revenues. New market participants are utilizing contract manufacturing partnerships to accelerate commercialization without significant capital expenditure.

Givaudan's expansion in the Asia-Pacific region demonstrates strategic positioning to minimize supply chain risks and gain geographical advantages. Companies now achieve competitive advantages through regulatory compliance, supply chain optimization, and comprehensive efficacy documentation rather than production capacity increases. This market environment favors organizations with operational flexibility and specialized industry knowledge.

Flavonoid Industry Leaders

-

Cayman Chemical Company

-

The Merck Group

-

Indena S.p.A

-

Layn Natural Ingredients

-

The Archer-Daniels-Midland Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Sugar reduction and sensory performance in beverages and plant-forward formulations are broadening how manufacturers use flavonoids. Beyond antioxidant positioning, the ingredients are being positioned for taste modulation, bitterness management, and sweetening systems. A specific example is HealthTech Bioactives' July 2026 launch of Citrose, a patented citrus-based high-intensity sweetener sourced from immature bitter orange (Citrus aurantium) and aimed at reduced-sugar beverages and dairy alternatives. This introduces whitespace for citrus-derived bioflavonoid solutions that target both functionality and formulation performance.

Delivery technologies that address solubility and bioavailability constraints are creating opportunities across nutraceuticals, functional foods, and beauty-from-within positioning, where hydrophobic flavonoids can face absorption limits in conventional formats. Ceres Biotech introduced a liposomal apigenin powder (July 2026) in 50% and 70% concentrations, reinforcing continued productization of advanced delivery systems as suppliers compete on efficacy-per-dose, dispersion behavior, and stability in real-world matrices. On the regulatory front, EU Novel Food authorizations and EFSA safety work, together with ongoing EU additive re-evaluation activity with status updates published through February 2026, keep high-concentration extracts and new processing routes focused on data quality, standardized specifications, and compliant claims substantiation. This favors manufacturers able to pair clinical and safety dossiers with scalable, traceable supply.

Recent Industry Developments

- May 2026: Indena S.p.A. unveiled advanced botanical solutions for healthy aging and skin health at Vitafoods 2026 in Geneva. The updates reinforced the company focus on standardized botanical actives and application-led innovation in nutraceutical and beauty positioning, supporting premiumization strategies for flavonoid-containing ingredients and systems.

- March 2026: Cayman Chemical completed a pilot-scale run validating eXoZymes technology to improve scalability for biochemical production. The milestone supports a broader shift toward more predictable, scalable production routes that can complement crop-derived supply and help meet tighter reproducibility requirements for high-specification flavonoid-related products.

- November 2025: Indena S.p.A. announced a sustainability program that includes investment in renewable energy, targeting 4 MW of photovoltaic power by 2026 and 80% renewable electricity by 2030. The program aligns botanical ingredient manufacturing with customer procurement requirements around footprint and traceability, strengthening competitiveness with multinational food, supplement, and personal care buyers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the flavonoid market covers the sales value of flavonoid ingredients that are produced, processed, and sold for use in food and beverages, nutraceuticals, pharmaceuticals, cosmetics, and similar end uses, across major regions.

Scope exclusions: We exclude finished consumer products where flavonoids are only an embedded minor component and the product is primarily priced as a branded formulation.

Segmentation Overview

-

By Type

- Anthocyanin

- Flavones

- Flavan-3-ols

- Flavonol

- Anthoxanthin

- Isoflavones

- Other Product Types

-

By Source

- Citrus Fruits

- Berries

- Soybeans

- Tea

- Cocoa

- Herbs and Spices

- Others

-

By Form

- Powder

- Liquid

- Others

-

By Application

- Food and Beverages

- Nutraceutical

- Pharmaceutical

- Cosmetic and Personal Care

- Animal Feed

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the industry chain and set realistic input ranges before interviews. We leaned on public, non-paywalled sources such as USDA and other national agriculture statistics, US FDA and EFSA publications for ingredient and claims-related context, FAO datasets for crop supply signals, UN Comtrade for trade flows of relevant botanical extracts, and peer-reviewed journal articles for application and stability trends.

In addition, we reviewed company annual reports, investor presentations, press releases, and association websites to understand capacity additions, product positioning, and application mix shifts. For cross-checking financial direction, a paid subscription covering company financials and news helped track revenue movement and corporate actions at a high level. The source list above is illustrative, and many other references were also used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with ingredient manufacturers, extract processors, distributors, and downstream users across food, supplements, pharma, and personal care, so that desk assumptions could be corrected where needed. Since this is a global market, we ensured coverage across APAC, EMEA, and the Americas to reflect differences in sourcing, regulations, and application demand, and then we revisited a few respondents when large variances showed up in price or volume assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 13% | APAC: 48% |

| Mid tier: 46% | Functional/Unit leaders: 32% | EMEA: 31% |

| Smaller Players: 16% | Managers: 55% | Americas: 21% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up structure, where the main total was constructed by rebuilding demand pools from application consumption and ingredient inclusion rates, then stress tested using supplier and channel signals. In practice, the top-down layer connects food and beverage and supplement output indicators to typical flavonoid use levels, while pharma and cosmetics demand is translated through form adoption and formulation intensity.

To keep the model grounded, a few inputs were treated as key levers, such as average selling price ranges by flavonoid type and form, the split of demand by application, regional sourcing and trade dependency, and the pace of substitution toward natural functional ingredients. Where direct volume datapoints were missing, gaps were handled using bounded ranges informed by interviews and trade proxies, which were then narrowed through consistency checks across regions. Forecasts were run using scenario analysis, where drivers like health positioning in supplements, clean label food launches, and price movement for botanical raw materials were varied within expert validated limits, and the final outlook reflects the most consistent scenario across checks.

Data Validation & Update Cycle

Outputs were validated through cross checks against independent signals, including trade movement direction, reported capacity expansions, and application demand momentum discussed by respondents. When a region or application showed an unusual jump, it was reviewed again, assumptions were re-tested, and follow-up calls were triggered to confirm whether the change was structural or a timing issue.

Before sign-off, the full model is reviewed in steps, starting with input logic checks and then moving to market total reasonableness and regional share alignment. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory changes or supply disruptions that can shift pricing or availability. Right before delivery, we run a fresh review pass so the numbers reflect the latest available developments.

Mordor Intelligence's Flavonoid Market Size Compared Against Other Published Estimates

Published market values for flavonoids can look far apart because studies do not always count the same ingredient boundaries, years, and pricing assumptions. Differences also come from how quickly price decks are refreshed and whether application demand is reconstructed from consumption indicators or taken from broad category ratios.

The benchmark table shows a tighter 2026 sized market versus some sources that report larger 2024 totals, and in Mordor Intelligence's model the value is counted at the ingredient level across defined flavonoid types and forms, rather than mixing finished product revenue or broad polyphenol style adjacencies into the same number.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.49 B (2026) | |

| Industry Research Group A | USD 1.10 B (2024) | Uses an earlier base year and applies a faster growth path, and the scope description is less specific on ingredient versus finished product revenue, which can shift the starting value. |

| Global Research Publisher B | USD 1.28 B (2024) | Starts from 2024 pricing and demand assumptions and may include broader application revenue mapping, while the year difference and price progression method can widen the gap versus a 2026 based estimate. |

Overall, the spread is mainly explained by year selection, what gets counted as an ingredient market versus downstream product value, and how prices are rolled forward. By anchoring the size to clear application demand linkages and checkable price ranges, the estimate stays easier to trace and repeat when inputs change.

Key Questions Answered in the Report

What is the current Flavonoids market size and how fast is it growing?

The flavonoids market is estimated at USD 1.49 billion in 2026 and is anticipated to reach USD 1.89 billion by 2031, registering a 4.85% CAGR.

Which product type leads the Flavonoids market?

Anthocyanins lead with 29.12% 2025 share, though flavonols post the fastest 6.12% CAGR.

Why is Asia-Pacific the fastest-growing region?

Supportive nutraceutical rules, rising disposable income, and local manufacturing investments such as Givaudan’s new Indonesian plant fuel a 6.14% CAGR.

Which application segment shows the strongest momentum?

Nutraceuticals dominate with 35.20% share and remain the fastest growing at 5.55% CAGR, supported by clinical validation and updated FDA labeling rules.

Page last updated on: