Valganciclovir Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.63 Billion |

| Market Size (2031) | USD 2.12 Billion |

| Growth Rate (2026 - 2031) | 5.40% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Valganciclovir Market Analysis by Mordor Intelligence

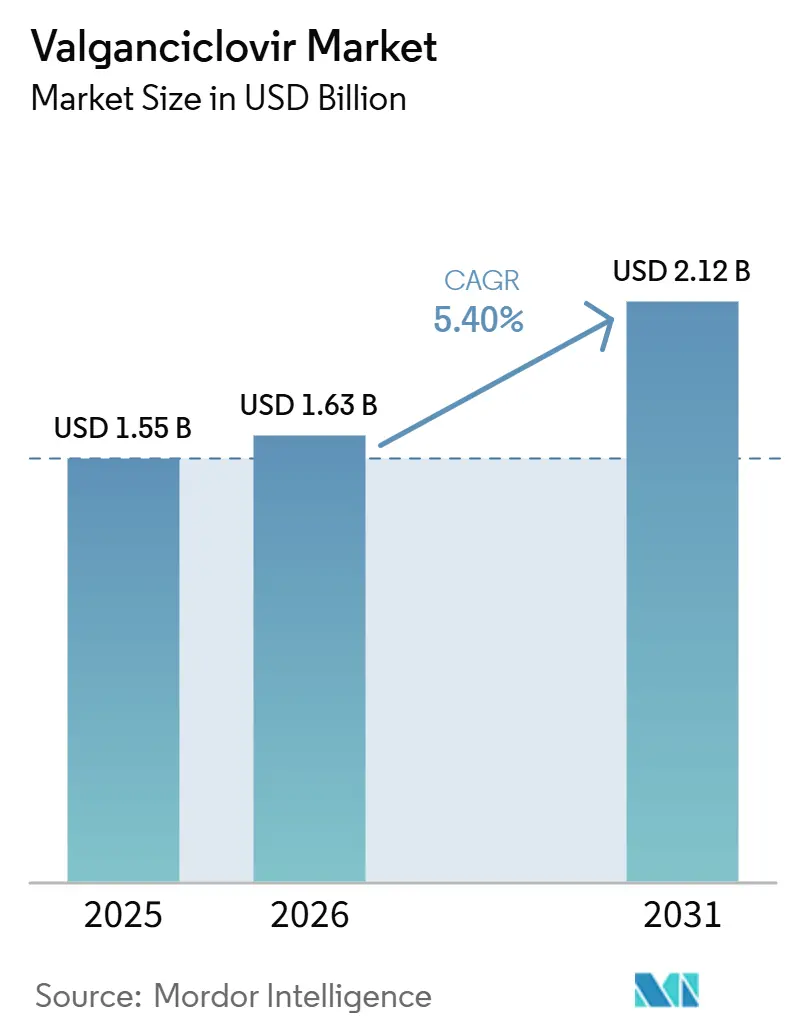

The Valganciclovir Market size was valued at USD 1.55 billion in 2025 and is estimated to grow from USD 1.63 billion in 2026 to reach USD 2.12 billion by 2031, at a CAGR of 5.40% during the forecast period (2026-2031).

The valganciclovir market is being shaped by higher global transplant volumes, a broader immunocompromised patient pool, and a firm move from inpatient intravenous treatment to outpatient oral regimens. Global solid organ transplants reached 173,727 procedures in 2024[1]F. Martin et al., “Organ Donation and Transplantation Worldwide, The Global Observatory on Donation and Transplantation 2024 Report,” Transplantation, pmc.ncbi.nlm.nih.gov, which was the highest level recorded since formal tracking began, and that lifted the core prophylaxis base for the valganciclovir market across kidney, lung, heart, and liver programs. Hematologic toxicity, renal dosing complexity, and antiviral resistance continue to limit the full volume potential of the valganciclovir market.

Key Report Takeaways

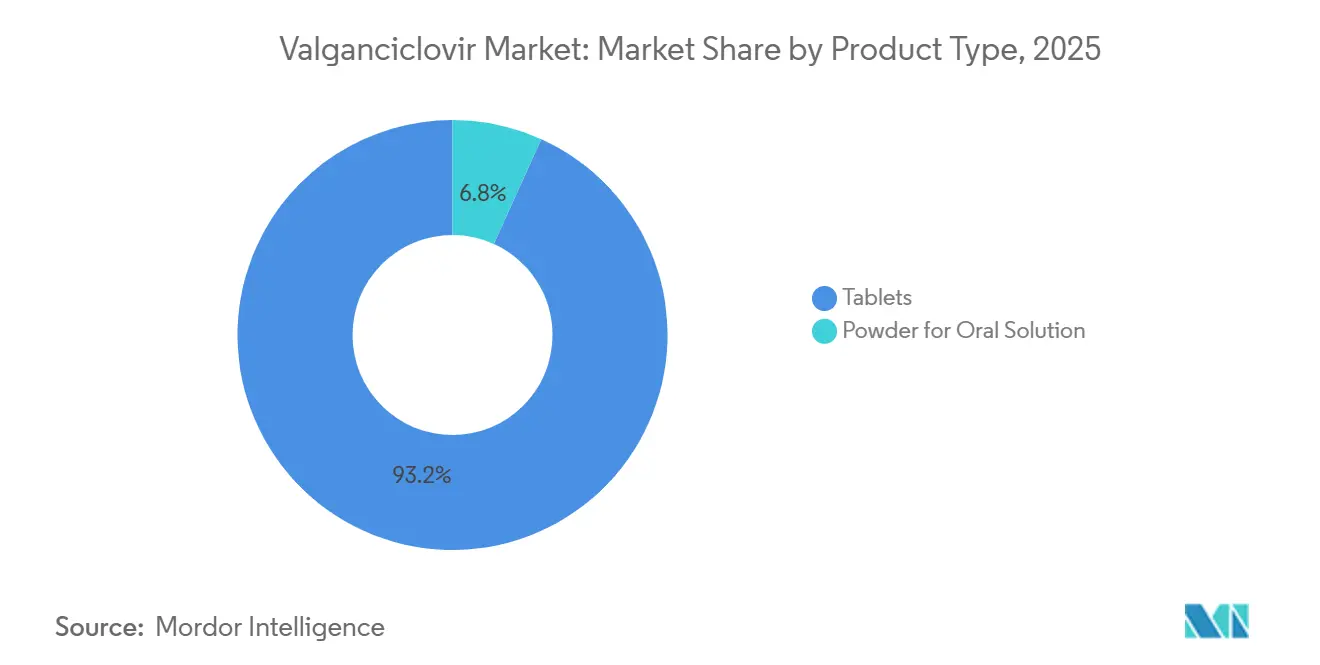

- By product type, tablets led with 93.23% revenue share in 2025, while powder for oral solution is forecast to expand at a 7.32% CAGR through 2031.

- By indication, post-transplant prophylaxis held 58.32% of global revenue in 2025 and is expected to record the highest CAGR at 7.12% through 2031.

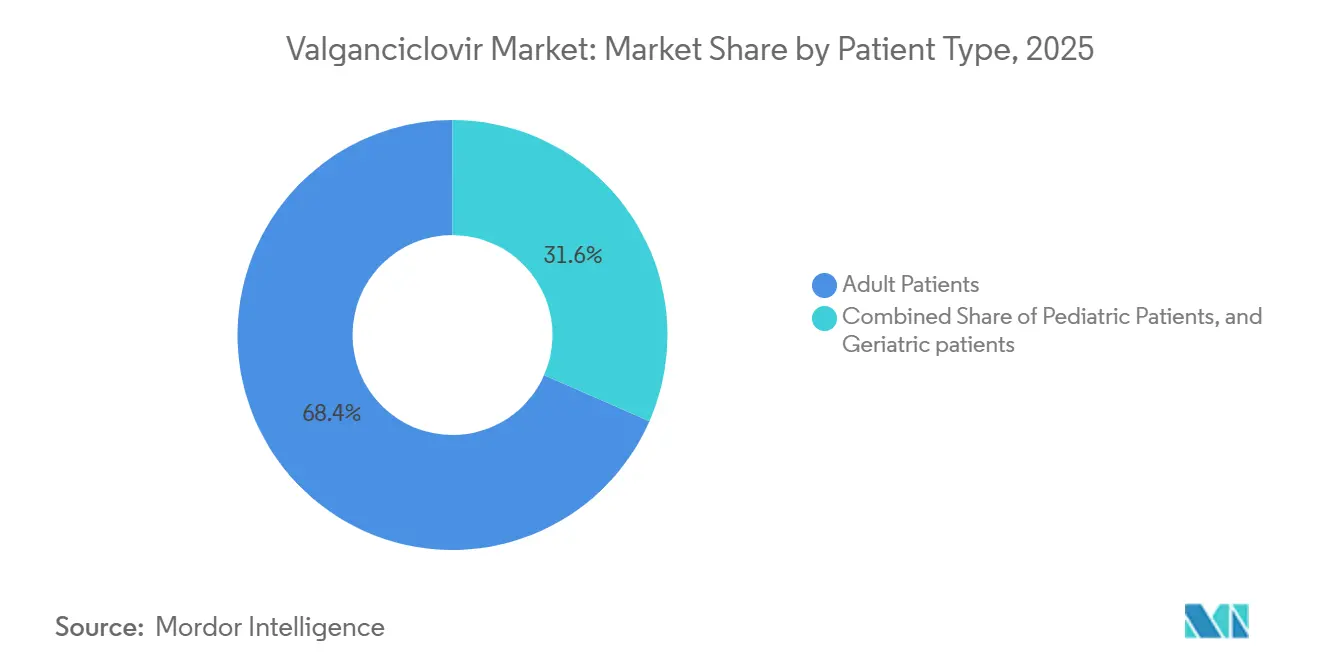

- By patient type, adults accounted for 68.43% of revenue in 2025, while geriatric patients are expected to advance at a 6.82% CAGR through 2031.

- By distribution channel, hospital pharmacies held 72.45% of revenue in 2025, while online pharmacies are projected to grow fastest at a 7.34% CAGR through 2031.

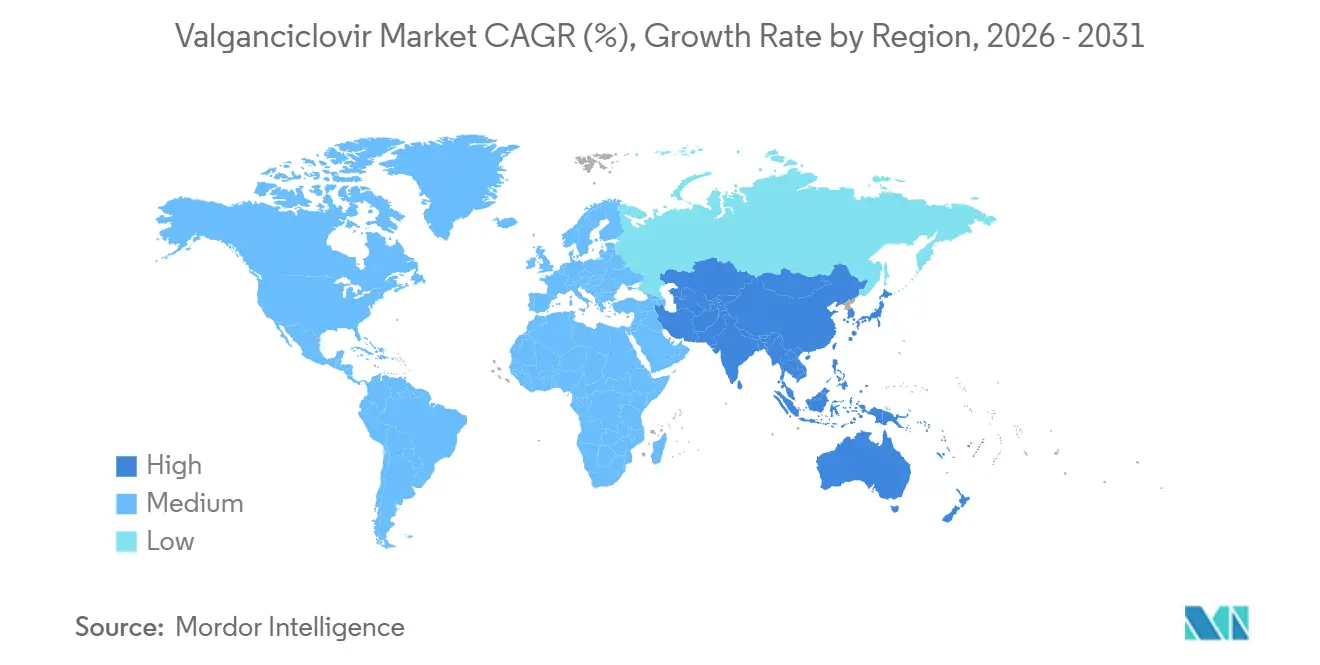

- By geography, North America commanded 43.67% of global revenue in 2025, while Asia-Pacific is projected to record the highest CAGR at 7.14% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Valganciclovir Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Solid Organ and Stem Cell Transplant Volumes | +1.2% | Global, led by North America and Europe | Medium term (2-4 years) |

| Expanding Immunocompromised Patient Pool | +0.8% | Global, highest in APAC and MEA | Long term (≥ 4 years) |

| Shift From Inpatient Intravenous Therapy to Outpatient Oral Therapy | +0.7% | North America and Europe | Short term (≤ 2 years) |

| Generic Entry and Broader Access After Patent Expiry | +0.8% | Global, accelerating in South America and APAC | Short term (≤ 2 years) |

| CMV DNA Monitoring Expands Preemptive Prophylaxis Use | +0.4% | North America, EU, APAC core | Medium term (2-4 years) |

| Pediatric-Friendly Oral Formulations Improve Adoption | +0.3% | North America, EU, spill-over to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Solid Organ And Stem Cell Transplant Volumes

The valganciclovir market is directly tied to transplant procedure growth because each new recipient adds a defined prophylaxis or treatment course. Global solid organ transplants reached 173,727 procedures in 2024, and kidney transplants alone contributed 110,467 cases, which kept the transplant setting at the center of the valganciclovir market. Updated international CMV guidelines recommend 6 months of valganciclovir prophylaxis for D+/R− kidney transplant recipients, which supports durable prescription volumes in the largest organ category.

Lung transplant volume rose 6% in 2024 to 8,236 procedures, and these patients often require 12 months or more of prophylaxis, which gives them much higher drug exposure per patient than other organ groups. Stem cell transplant also sustains demand because CMV reactivation affects 40% to 60% of allogeneic recipients in the absence of prophylaxis, which extends the relevance of the valganciclovir market beyond solid organ programs. This pattern keeps revenue weighted toward procedures with longer prophylaxis windows rather than only toward the highest procedure counts.

Expanding Immunocompromised Patient Pool

The valganciclovir market is broadening because clinically relevant CMV risk now extends well beyond traditional transplant cohorts. CMV viremia occurs in 40% to 60% of allogeneic HSCT[2]S. Kim et al., “Cytomegalovirus Infection Post-Hematopoietic Stem Cell Transplantation, A Real-World Perspective on Risk Factors and Clinical Practice,” Clinical Transplantation and Research, doi.orgrecipients without prophylaxis, which keeps antiviral demand elevated in hematology practice as well as transplant medicine. The treatment base is also widening across patients receiving JAK inhibitors, TNF-alpha inhibitors, high-dose corticosteroids, and BTK inhibitors, where CMV surveillance and preemptive therapy are becoming more common in routine practice.

Congenital CMV is adding a small but growing prescribing pool because European consensus guidance identifies valganciclovir as the drug of choice for symptomatic neonates and supports 6-month treatment courses with documented hearing and neurodevelopmental benefit. United States-level neonatal screening programs are reporting 0.3% prevalence, which means better case finding can gradually increase pediatric demand in the valganciclovir market as more infants enter treatment windows earlier. CMV retinitis also remains relevant in AIDS and non-HIV immunocompromised populations, which prevents the addressable base from narrowing to transplant recipients alone.

Shift From Inpatient Intravenous Therapy To Outpatient Oral Therapy

The valganciclovir market benefits from a clear care-delivery shift because oral dosing can replace many inpatient intravenous treatment episodes. Valganciclovir reaches plasma ganciclovir exposure comparable to intravenous ganciclovir at approved oral doses, which reduces the need for catheter placement and infusion support for many patients. The 2024 international CMV guidelines prefer oral valganciclovir for mild to moderate CMV disease and advise intravenous ganciclovir only when oral absorption is unreliable, which reinforces outpatient management as standard practice.

French procurement notices in 2026 showed active 3-year supply contracts for both oral tablets at EUR 277,104 (USD 299,000) and oral solution at EUR 49,896 (USD 54,000), which signals that hospital systems are locking in oral-formulation demand rather than preserving infusion-heavy pathways. Home monitoring models are also supporting this transition because dried blood spot CMV PCR and telemedicine follow-up are making it easier to manage stable patients away from infusion centers. As a result, the valganciclovir market is aligning more closely with ambulatory refill patterns and long-duration maintenance care.

Generic Entry And Broader Access After Patent Expiry

The valganciclovir market has moved fully into a generic access phase, and that has changed how growth is created across regions. Roche’s brand has faced generic competition in the United States since 2014, and the current US field includes at least 9 manufacturers across 11 NADAC-listed NDCs,[3]“VALGANCICLOVIR HYDROCHLORIDE for Solution Oral, NADAC Pricing,” CMS NADAC Database, ndclist.comwhich confirms a crowded supply base. CMS-linked NADAC pricing showed the generic oral solution declining from USD 3.36/mL in June 2024 to USD 2.01/mL in December 2024 and then to USD 1.29/mL by February 2026, which materially improved affordability for institutional and retail channels.

Somerset Therapeutics received FDA final approval for valganciclovir hydrochloride tablets in June 2024, adding another AB-rated generic and increasing automatic substitution capacity. Lower prices put pressure on revenue per unit in mature markets, but they also widen tender access in emerging regions, which supports higher treatment volumes in Asia-Pacific and South America. This pricing dynamic explains why the valganciclovir market can remain on a growth path even while branded economics continue to weaken.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hematologic and Renal Safety Constraints | -0.8% | Global | Short term (≤ 2 years) |

| Heavy Laboratory Monitoring Burden | -0.5% | APAC and MEA | Medium term (2-4 years) |

| Antiviral Resistance Risk in Repeated Exposure | -0.4% | Global, highest at high-volume transplant centres | Long term (≥ 4 years) |

| Reimbursement Gaps in Resource-Constrained Markets | -0.5% | South America, MEA, Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hematologic And Renal Safety Constraints

The valganciclovir market is constrained by a toxicity profile that remains clinically significant even in established transplant centers. In a real-world U.S. cohort of 15,398 kidney transplant recipients, nearly three-quarters of patients on valganciclovir or ganciclovir prophylaxis developed neutropenia or leukopenia, and those patients had more inpatient admissions, more outpatient visits, and more laboratory tests than matched patients without myelosuppression. Short-term hazard ratios for neutropenia reached 39.6 in patients exposed to valganciclovir for 1 to 90 days versus unexposed controls, which shows how quickly safety events can emerge.

The clinical problem is more serious because patients with myelosuppression still showed a 3.95-fold higher risk of CMV disease during prophylaxis, which suggests that dose changes and interruptions can weaken protection. Renal function monitoring and dose adjustment also complicate routine use, especially in older and medically complex recipients. These constraints are opening space for alternatives such as letermovir in toxicity-intolerant patients, which limits upside for the valganciclovir market in its largest indication.

Heavy Laboratory Monitoring Burden

The valganciclovir market also faces a practical access barrier because CMV management often depends on repeated laboratory surveillance. Weekly quantitative CMV PCR testing remains the standard during preemptive therapy under the 2024 international guidelines, and one 2025 randomized trial estimated the cost at USD 73.6 per PCR test. That cost burden is harder to absorb in Southeast Asia, the Middle East, and parts of Africa, where logistics and molecular testing capacity can restrict broader use. The same 2025 trial showed that absolute lymphocyte count-guided monitoring can reduce PCR testing frequency without materially worsening outcomes, which may improve access in lower-resource settings over time.

Even so, centers without reliable weekly PCR access tend to rely on standardized prophylaxis rather than nuanced preemptive therapy, which limits how flexibly the valganciclovir market can expand across care settings. The result is a market where drug availability alone does not ensure adoption because monitoring infrastructure still determines real treatment capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tablets Dominate While Powder For Oral Solution Gains Pediatric Ground

Tablets captured 93.23% share of the valganciclovir market size in 2025, which shows how strongly adult transplant protocols shape product demand. The 450 mg film-coated tablet remains the standard format for adult prophylaxis at 900 mg per day, and for CMV retinitis induction at 1,800 mg per day, so its lead in the valganciclovir market is based on routine adult use rather than short-term channel factors. Adult transplant recipients are the largest patient pool, and they usually do not need the dosing flexibility that a liquid formulation provides. The tablet format also fits stable outpatient refill behavior, which supports the broader oral-care shift across the valganciclovir market.

Powder for oral solution is projected to grow fastest at a 7.32% CAGR through 2031, and that makes it the clearest niche expansion area within the product mix. The FDA prescribing information revised in June 2025[4]“VALGANCICLOVIR HYDROCHLORIDE for Oral Solution, Prescribing Information,” DailyMed, dailymed.nlm.nih.gov identifies the 50 mg/mL oral solution as the preferred pediatric formulation for patients aged 4 months to 16 years, because body-surface-area-based dosing cannot be matched precisely with tablets.

By Indication: Post-Transplant Prophylaxis Anchors Both Scale And Growth

Post-transplant prophylaxis held 58.32% of the valganciclovir market share in 2025 and is also projected to expand at a 7.12% CAGR through 2031, which makes it both the largest and fastest-growing indication. That combination is unusual, and it shows how deeply the valganciclovir market depends on transplant prevention protocols rather than rescue treatment. The fourth international CMV guidelines continue to position valganciclovir as the most commonly used prophylaxis agent, with recommended durations ranging from 3 months in some intermediate-risk kidney recipients to 12 months or more in D+/R− lung recipients.

By Patient Type: Geriatric Growth Driven By Immunosenescence And Aging Transplant Demographics

Adults accounted for 68.43% of revenue in 2025, which makes them the clear base segment for the valganciclovir market. This pattern reflects the age profile of global solid organ transplant recipients, most of whom fall between 18 and 64 years and are concentrated in high-income care systems. Adult patients also form the most stable refill cohort because they are well represented in established transplant follow-up programs, and standard tablet dosing supports adherence. Their lead in the valganciclovir market is therefore linked to both clinical volume and practical ease of use. Adults remain the anchor population across transplant prophylaxis, CMV infection management, and retinitis treatment. This gives the segment a durable position even as pediatric and geriatric use rises.

Geriatric patients are expected to grow fastest at a 6.82% CAGR through 2031, and that reflects older transplant recipients, immunosenescence, and higher clinical vulnerability. A 2025 study in seropositive kidney transplant recipients found that older age was an independent risk factor for CMV infection, and CMV infection in that cohort was associated with higher graft loss and higher all-cause mortality.

By Distribution Channel: Hospital Pharmacies Persist As Core While Online Channels Accelerate

Hospital pharmacies held 72.45% share of the valganciclovir market size in 2025, which confirms that complex transplant care still depends most on institutional dispensing. This dominance is tied to close coordination among pharmacists, transplant teams, infectious disease specialists, and lab monitoring systems. Dose changes for renal function, cytopenia management, and CMV DNA surveillance are easier to manage inside hospital-linked workflows, so the largest share of the valganciclovir market stays in that setting. A 2025 Clinical Transplantation study found that specialty pharmacy mandates caused discharge delays in more than 60% of solid organ transplant recipients and also delayed drug therapy in a similar proportion, which highlights the operational value of hospital-based supply.

Online pharmacies are projected to grow fastest at a 7.34% CAGR through 2031, which points to a steady migration of stable maintenance patients into remote refill models. Once transplant recipients move beyond the highest-risk period, CMV monitoring tends to become less frequent and oral dosing becomes more routine, which makes digital dispensing more practical.

Geography Analysis

North America held 43.67% of global revenue in 2025, which gave the region the largest share of the valganciclovir market. The United States remains the main regional driver because it has the largest national transplant program and over 23,000 kidney transplants were recorded in 2023 through OPTN, with each patient typically entering a standard prophylaxis course. Broad generic availability also supports regional scale, and CMS-linked NADAC data showed the oral solution price falling from USD 3.36/mL in June 2024 to USD 1.29/mL by February 2026, which improved access across institutional and retail formularies.

Asia-Pacific is forecast to record the fastest CAGR at 7.14% through 2031, while Europe remains a mature but actively managed regional pillar of the valganciclovir market. Europe continues to benefit from the 2024 international CMV guideline framework, which is shaping prophylaxis practice across Germany, France, Italy, Spain, and the United Kingdom. France provided direct evidence of ongoing institutional demand in 2026 through 3-year procurement contracts for both tablets and oral solutions, which shows that transplant and neonatal centers are maintaining stable purchasing activity.

Competitive Landscape

The valganciclovir market has become a split structure with a small originator presence and a broad generic field that now competes more on supply continuity and formulation coverage than on patent protection. CHEPLAPHARM Arzneimittel GmbH remains tied to the Valcyte brand in specialty channels, and a December 2025 labeling update in the United States showed that the branded product still receives lifecycle attention even in a generic-heavy environment.

Indian manufacturers remain especially important because they supply both U.S. generic channels and emerging-market tender systems, which gives them influence far beyond one geography. Somerset Therapeutics strengthened that competitive pool in June 2024 with AB-rated FDA approval for valganciclovir hydrochloride tablets, and that strategic move added one more substitution-ready option for hospital and retail formularies.

Valganciclovir Industry Leaders

F. Hoffmann-La Roche Ltd.

Cipla Limited

CHEPLAPHARM Arzneimittel GmbH

Teva Pharmaceutical Industries Ltd.

Viatris Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Viatris Inc.'s valganciclovir tablets (450 mg) were listed and verified on Australia's Pharmaceutical Benefits Scheme (PBS), expanding subsidized access for adult patients with AIDS-related Cytomegalovirus (CMV) Retinitis and for Post-Transplant Prophylaxis in solid organ transplant recipients.

- January 2026: AvKARE's ANDA 205220 for valganciclovir HCl oral solution received an updated DailyMed label, reflecting ongoing regulatory compliance maintenance for this pediatric-use formulation in the US and confirming continued product availability.

Global Valganciclovir Market Report Scope

As per the scope of the market, valganciclovir is an antiviral medication used for the prevention and treatment of cytomegalovirus (CMV) infections, particularly in immunocompromised patients such as organ transplant recipients, individuals with HIV/AIDS, and neonates with congenital CMV infection. It contains the active ingredient valganciclovir hydrochloride, a prodrug of ganciclovir, which works by inhibiting viral DNA replication and limiting the spread of CMV within the body. The medication is administered orally in the form of tablets or powder for oral solution under the supervision of healthcare professionals.

The Valganciclovir Market Report segments the market by product type, including tablets and powder for oral solution. It also categorizes the market by indication, covering cytomegalovirus (CMV) retinitis, cytomegalovirus (CMV) infection, post-transplant prophylaxis, and congenital CMV infection. The market is further segmented by patient type, comprising pediatric patients, adult patients, and geriatric patients. Additionally, the distribution channel segment includes hospital pharmacies, retail pharmacies, online pharmacies, and others. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for key countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Tablets |

| Powder for Oral Solution |

| Cytomegalovirus (CMV) Retinitis |

| Cytomegalovirus (CMV) Infection |

| Post-Transplant Prophylaxis |

| Congenital CMV Infection |

| Pediatric Patients |

| Adult Patients |

| Geriatric Patients |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Tablets | |

| Powder for Oral Solution | ||

| By Indication | Cytomegalovirus (CMV) Retinitis | |

| Cytomegalovirus (CMV) Infection | ||

| Post-Transplant Prophylaxis | ||

| Congenital CMV Infection | ||

| By Patient Type | Pediatric Patients | |

| Adult Patients | ||

| Geriatric Patients | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and outlook for valganciclovir through 2031?

The valganciclovir market was valued at USD 1.55 billion in 2025, stands at USD 1.63 billion in 2026, and is projected to reach USD 2.12 billion by 2031 at a 5.40% CAGR.

Which indication contributes the most revenue for valganciclovir?

Post-transplant prophylaxis is the largest indication, with 58.32% of revenue in 2025, and it is also the fastest-growing indication at 7.12% CAGR through 2031.

Why do tablets still lead over oral solutions?

Tablets held 93.23% of product revenue in 2025 because adult transplant recipients remain the largest patient group, and standard tablet dosing fits routine prophylaxis and treatment use.

Which patient group is growing fastest for valganciclovir use?

Geriatric patients are expected to grow fastest at a 6.82% CAGR through 2031 because older transplant recipients face higher CMV risk and require closer prophylaxis and monitoring.

Which region leads sales and which region is expanding fastest?

North America held 43.67% of global revenue in 2025, while Asia-Pacific is expected to post the fastest growth through 2031 at a 7.14% CAGR.

What is the biggest competitive threat to valganciclovir in transplant care?

Letermovir is the main therapeutic threat because Phase 3 data showed similar CMV disease control with much lower leukopenia than valganciclovir in high-risk kidney transplant recipients.

Page last updated on: