Inulin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1 Billion |

| Market Size (2031) | USD 1.34 Billion |

| Growth Rate (2026 - 2031) | 6.08% CAGR |

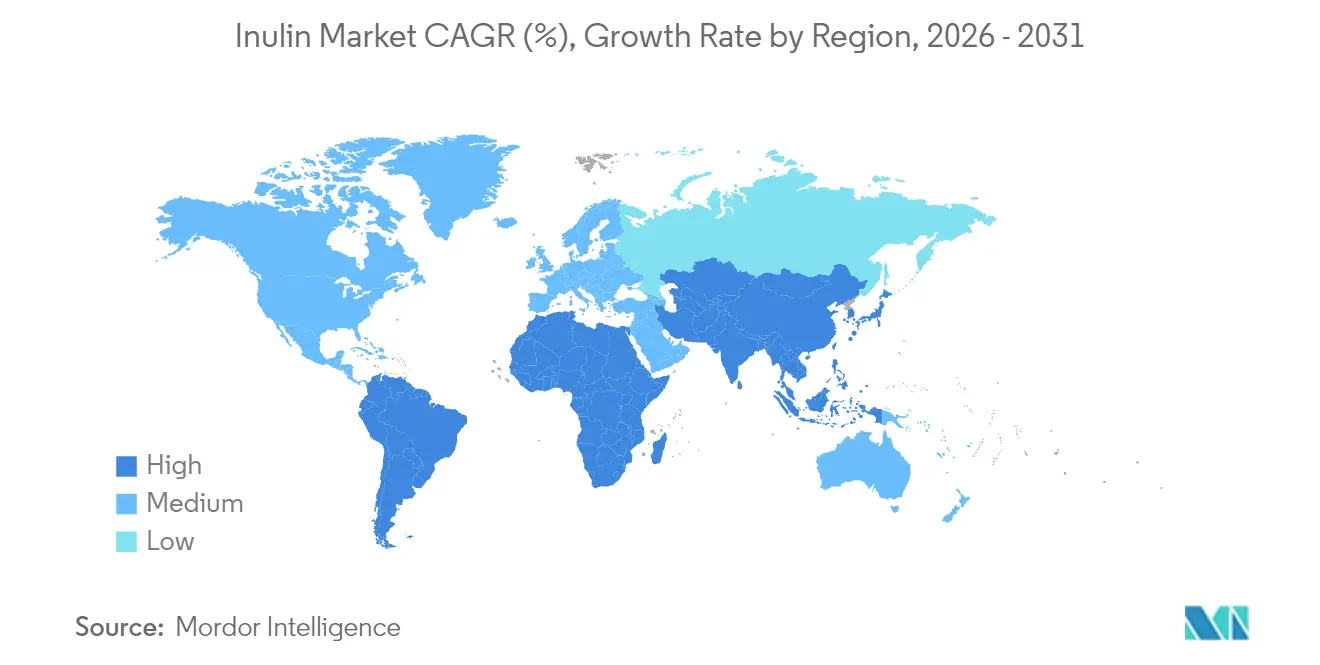

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

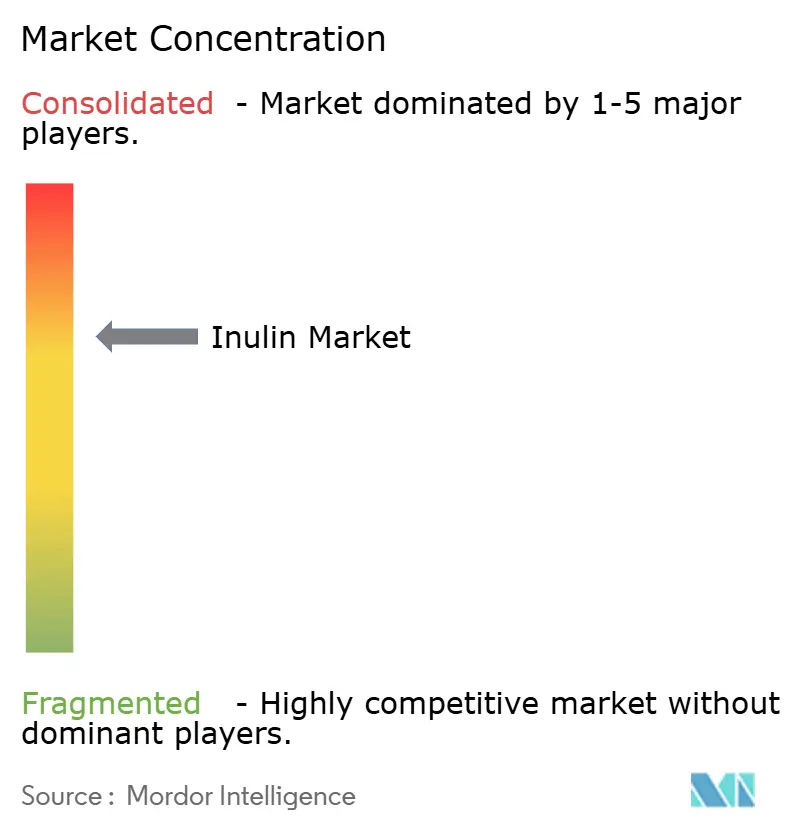

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Inulin Market Analysis by Mordor Intelligence

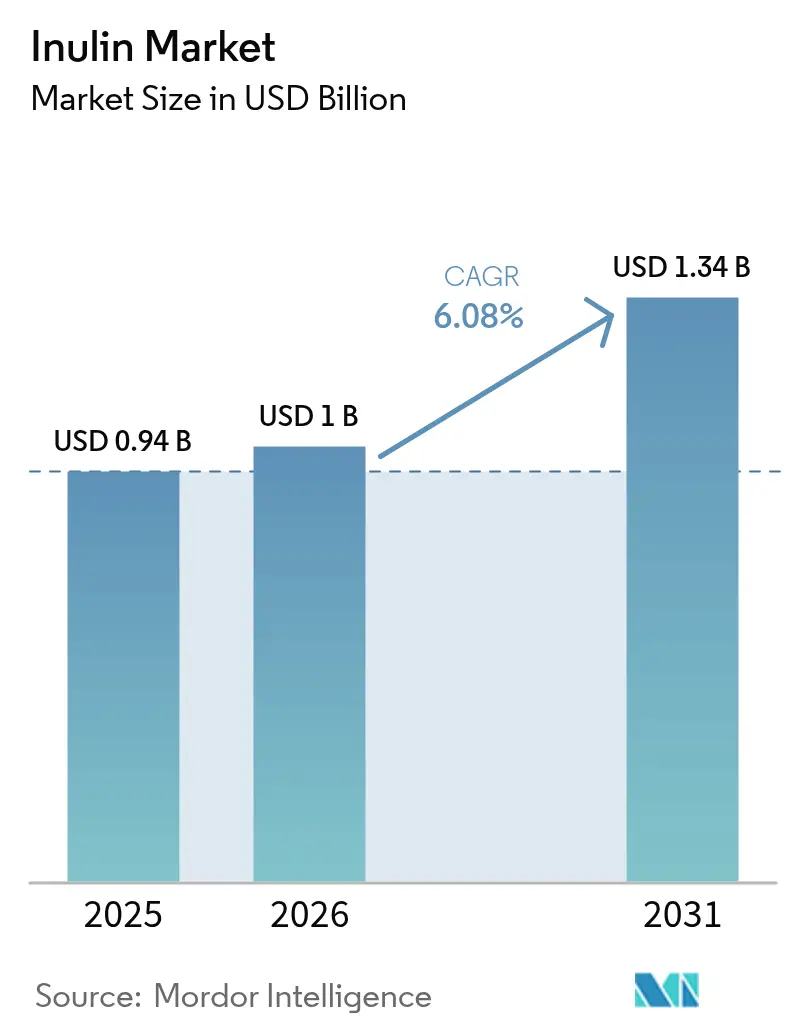

Inulin market size in 2026 is estimated at USD 1.0 billion, growing from 2025 value of USD 0.94 billion with 2031 projections showing USD 1.34 billion, growing at 6.08% CAGR over 2026-2031. This growth is fueled by a rising consumer emphasis on digestive health and the U.S. FDA's GRAS affirmations for various botanical sources. Moreover, advancements in extraction technologies are bolstering production efficiency, further fueling demand. European processors leverage established chicory supply chains, while North America's scalable Jerusalem artichoke projects and Mexico's agave integration diversify sourcing strategies. This diversification mitigates raw-material risks and fortifies supply chain resilience. Clinical research underscores inulin's health benefits, from improving lipid profiles and enhancing calcium absorption to enriching the microbiome. Such validations not only bolster health claims but also spur innovation in product development. Liquid inulin is becoming a favored choice in ready-to-drink beverages, thanks to its rapid solubilization that boosts factory throughput and refines product texture. On the other hand, powdered inulin continues to play a pivotal role in bakery and dairy applications. Yet, challenges loom: price sensitivity in developing markets and stability concerns in acidic, heat-treated foods. Nevertheless, strides in processing techniques and encapsulation technologies are enhancing cost efficiency and functional stability, setting the stage for the market's sustained growth.

Key Report Takeaways

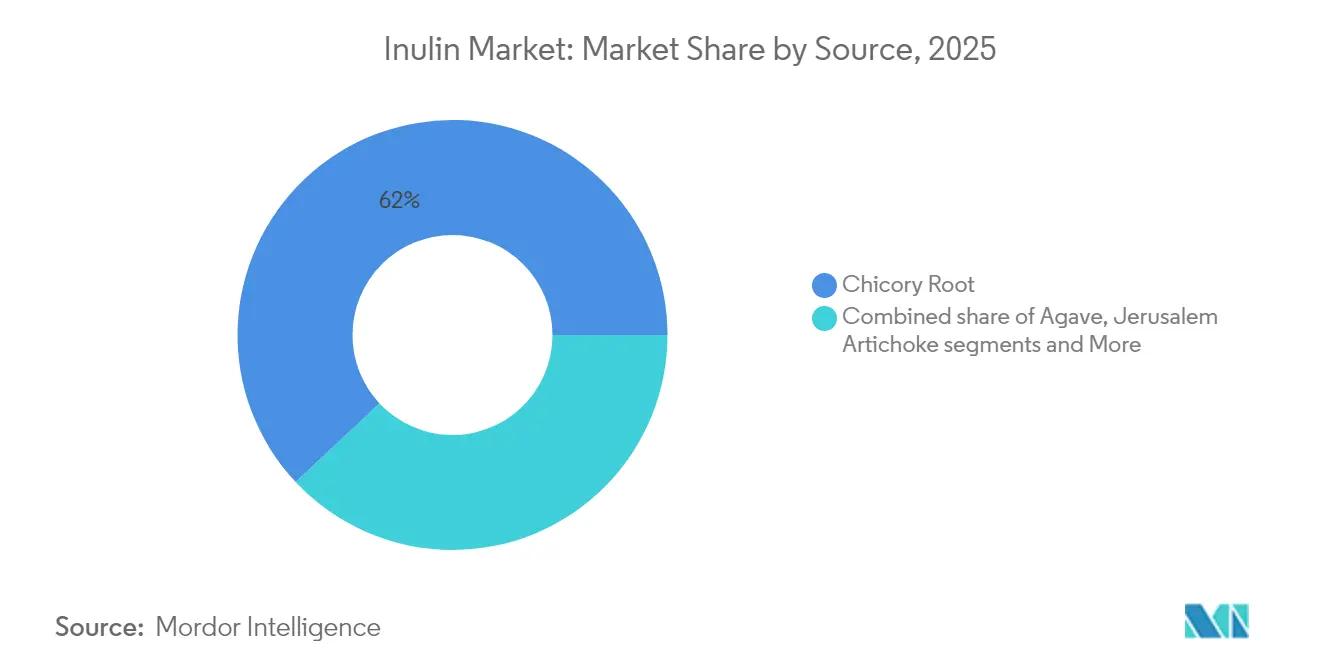

- By source, chicory root led with 61.99% of the inulin market share in 2025; Jerusalem artichoke is projected to expand at a 7.26% CAGR through 2031.

- By form, powder accounted for 70.62% share of the inulin market size in 2025, while liquid is advancing at a 7.30% CAGR through 2031.

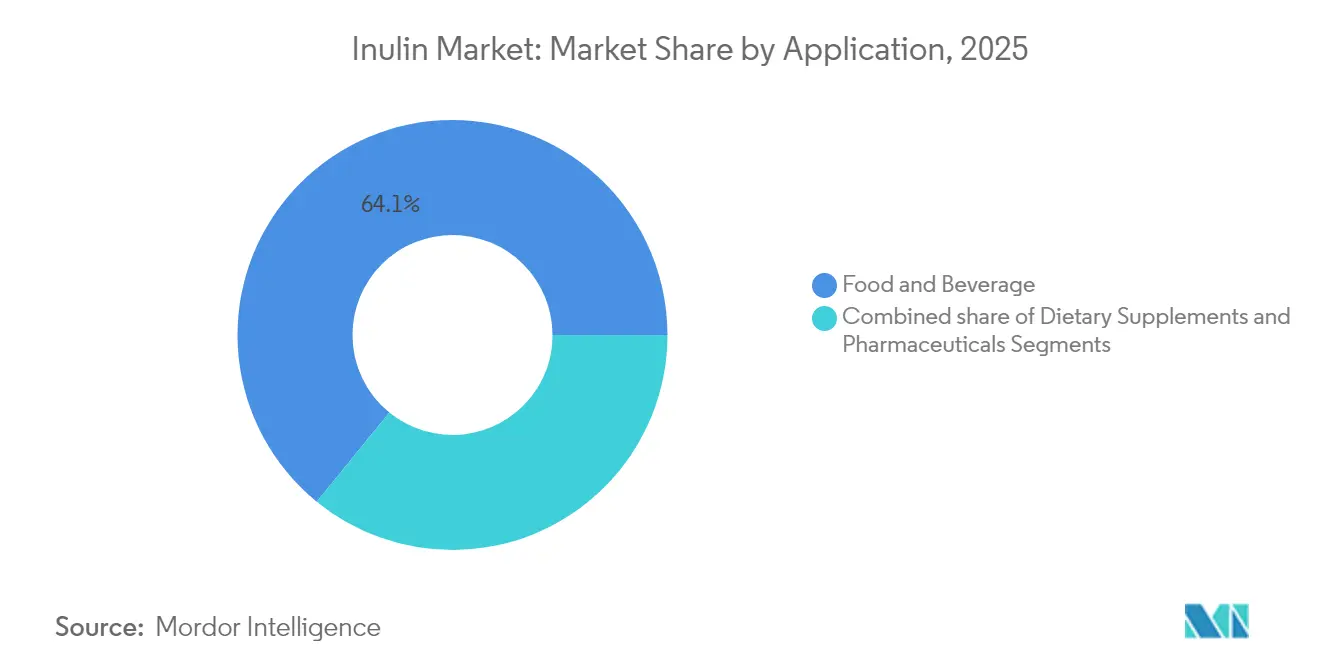

- By application, food and beverage held 64.12% revenue share in 2025; dietary supplements are growing at a 7.16% CAGR to 2031.

- By geography, Europe dominated with 47.42% revenue share in 2025, whereas Asia-Pacific is set to register a 7.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Inulin Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing demand for prebiotics ingredients | +1.8% | Global, with Asia-Pacific leading adoption | Medium term (2-4 years) |

| Increase consumer focus on clean label ingredients | +1.2% | North America and Europe primary, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Rising geriatric population seeking digestive health products | +0.9% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Demand form gluten-free products manufacturers for texture improvement | +0.7% | North America and Europe core markets | Medium term (2-4 years) |

| Increased consumer emphasis on low calorie food products | +0.6% | Global, led by urban demographics | Short term (≤ 2 years) |

| Expanding demand for fortified food industry | +0.5% | Asia-Pacific growth markets, established in developed regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing demand for prebiotics ingredients

Inulin has emerged as a pivotal ingredient in the growing prebiotics market, which is evolving beyond traditional probiotic supplementation. Its selective fermentation by beneficial gut bacteria positions it as a key driver of gut health. The U.S. FDA's recognition of inulin as a soluble fiber that contributes to dietary fiber intake has validated its health claims, allowing manufacturers to confidently market its prebiotic benefits to consumers[1]Cereals and Grains Association, "The Science of Prebiotics", www.cerealsgrains.org. This regulatory clarity provides inulin with a competitive edge over other prebiotics that face challenges in obtaining health claim approvals. Additionally, inulin's dual functionality as a prebiotic and as a fat and sugar replacer enhances its appeal to food manufacturers aiming to develop clean-label products. Short-chain inulin, in particular, has demonstrated greater efficacy in preventing atherosclerosis compared to long-chain variants, presenting opportunities for product differentiation based on molecular structure. This combination of regulatory support, functional versatility, and health benefits underscores inulin's growing importance in the prebiotics market.

Increase consumer focus on clean label ingredients

Clean label positioning has transitioned from being a marketing strategy to an essential operational focus for manufacturers. Inulin, derived from plant-based sources and requiring minimal processing, aligns seamlessly with the increasing consumer demand for transparency and natural ingredients. Its Generally Recognized As Safe (GRAS) status and well-established safety profile allow manufacturers to replace synthetic additives without compromising critical aspects such as product functionality or shelf life. In the European Union, stringent regulations mandating clear ingredient labeling provide a competitive advantage to products containing recognizable components like chicory root-derived inulin, as opposed to synthetic alternatives[2]European Union, "Regulation (EU) No 1169/2011 Of The European Parliament And Of The Council", www.eur-lex.europa.eu. This regulatory framework particularly benefits liquid inulin applications, where the simplicity of processing and the familiarity of ingredients significantly influence consumer preferences. The adoption of inulin is no longer limited to premium products; mass-market manufacturers are increasingly incorporating it to meet clean label expectations while maintaining cost efficiency.

Rising geriatric population seeking digestive health products

The United Nations World Population Prospects highlights the accelerating trend of global population aging, with individuals aged 65 and older projected to account for 16% of the global population by 2050. This demographic shift is driving sustained demand for digestive health solutions tailored to the needs of older adults[3]United Nations, "Department of Economic and Social Affairs Population Division", www.population.un.org. Research from the National Institute on Aging has emphasized the critical connection between gut health and cognitive function in elderly populations, expanding the potential applications of inulin beyond its traditional role in digestive health. Age-related changes in gastrointestinal function, such as reduced stomach acid production and alterations in gut microbiome composition, create unique nutritional requirements. Inulin's gentle prebiotic properties make it an effective solution, addressing these needs without causing the digestive discomfort often associated with more aggressive interventions. Furthermore, the Centers for Disease Control and Prevention's Healthy Aging Program underscores the importance of preventive nutrition strategies, positioning functional ingredients like inulin as vital tools for supporting health and independence among aging populations.

Demand form gluten-free products manufacturers for texture improvement

The U.S. Food and Drug Administration has standardized the definition of gluten-free labeling under 21 CFR 101.91, providing clarity to market definitions while creating significant opportunities for functional ingredients that address texture-related challenges in gluten-free formulations. The Celiac Disease Foundation reports that celiac disease affects approximately 1% of the global population. Additionally, a growing number of consumers are adopting gluten-free diets due to perceived health benefits, thereby expanding the potential market for texture-enhancing ingredients. Inulin, a versatile ingredient with gel-forming properties under specific temperature and concentration conditions, plays a crucial role in improving texture across various gluten-free product categories, including baked goods and processed foods requiring structural stability. Its ability to enhance water retention and extend shelf life effectively addresses critical formulation challenges, such as maintaining moisture and preventing staleness, which are prevalent in gluten-free product development.

Restraint Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High processing cost of inulin | -1.1% | Global, particularly impacting price-sensitive markets | Short term (≤ 2 years) |

| Stability issues of inulin under high temperature and low ph | -0.8% | Global, affecting processed food applications | Medium term (2-4 years) |

| Inconsistent clinical evidence for claimed benefits | -0.6% | Developed markets with stringent regulatory oversight | Long term (≥ 4 years) |

| Stringent labeling requirements in developed countries | -0.4% | North America and Europe primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High processing cost of inulin

According to data from the U.S. Department of Agriculture's Economic Research Service, specialty crop processing requires significantly higher capital investment per unit of output compared to commodity crops. This high capital requirement creates substantial entry barriers for new inulin production facilities. The inulin extraction process is complex, involving multiple stages such as hot water diffusion, concentration under reduced pressure, and precision drying. These processes demand advanced equipment and technical expertise, which restrict supply chain flexibility and increase operational challenges. Additionally, the International Energy Agency reports that rising energy costs are impacting food processing operations, particularly energy-intensive processes like spray drying and concentration, both of which are critical for inulin production. These technical and financial requirements result in considerable capital investments for production facilities, favoring established players with existing infrastructure. This dynamic makes it challenging for new entrants to compete effectively, despite the growing opportunities in the market.

Inconsistent clinical evidence for claimed benefits

The European Food Safety Authority (EFSA) has established rigorous evidence standards for health claims related to dietary fibers, including inulin. Many claimed benefits fail to meet these standards, creating significant regulatory uncertainty for manufacturers aiming to make specific health claims. Similarly, the U.S. Federal Trade Commission (FTC) has intensified its enforcement actions against unsubstantiated health claims, requiring manufacturers to provide robust clinical evidence to substantiate their promotional messages. This heightened scrutiny has placed additional pressure on the functional ingredient market. However, variability in clinical trial methodologies, participant demographics, and outcome measures poses a major challenge in building a consistent evidence base for inulin's specific health benefits. These inconsistencies limit manufacturers' ability to make definitive therapeutic claims. Data from the National Institutes of Health's clinical trial database further reflects this complexity, showing mixed results across studies examining inulin's health effects. This variability highlights the difficulty of establishing clear causal relationships between inulin consumption and health outcomes, particularly in diverse population groups. As a result, manufacturers face significant hurdles in navigating regulatory requirements and substantiating health claims for inulin.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Chicory Root Market Leadership

Chicory root retains its dominant 61.99% market share in 2025, a result of decades of advancements in cultivation techniques and the development of a well-established processing infrastructure across European growing regions. The European Union's Common Agricultural Policy continues to provide critical agricultural support for chicory cultivation, ensuring stable supply chains and predictable pricing structures that underpin large-scale inulin production. Belgium and the Netherlands remain global leaders in chicory production, supported by long-standing agricultural cooperatives and state-of-the-art processing facilities. These facilities have consistently optimized extraction yields and maintained high-quality standards over decades of commercial operations. The processing infrastructure for chicory mirrors that of sugar beet operations, enabling significant economies of scale while leveraging existing expertise in root crop handling and processing, further solidifying its competitive edge in the market.

Jerusalem artichoke is emerging as the fastest-growing source segment, with a projected CAGR of 7.26% through 2031. This growth is driven by its superior inulin concentration and sustainable cultivation attributes, which address both environmental and economic challenges. According to the U.S. Department of Agriculture's Agricultural Research Service, Jerusalem artichoke contains an exceptional inulin concentration of 75-80% by dry weight, far surpassing chicory's approximate 20% concentration. This higher inulin content translates to reduced processing volumes and potentially lower extraction costs, making it an economically attractive option. Research from Ohio State University Extension highlights Jerusalem artichoke's adaptability to diverse growing conditions and its alignment with sustainable agricultural practices.

By Form: Powder Segment Dominance

In 2025, powder inulin commands a dominant 70.62% share of the market, thanks to its advantages in handling, storage, and formulation. These benefits seamlessly integrate with the current food processing infrastructure and ingredient management systems utilized by manufacturers worldwide. The International Organization for Standardization (ISO) has set forth guidelines for the handling of powdered ingredients, covering aspects from storage to transportation and processing. These standards bolster the market position of powder inulin, aligning it with established industry practices and ensuring compatibility with existing equipment. The powdered form of inulin allows for precise dosing and consistent blending, both of which are paramount in industrial food production. Such consistency is vital for quality control systems that depend on predictable ingredient behavior.

Liquid inulin is on a growth trajectory, projected to expand at a 7.30% CAGR through 2031. This surge is attributed to its superior processing characteristics in beverage and liquid food applications. Here, the challenges of powder dissolution can impact texture and clarity. The Food and Agriculture Organization (FAO) recognizes these advantages, emphasizing the benefits of pre-dissolved functional ingredients in continuous production systems. Liquid inulin stands out in automated processing settings, streamlining the mixing process and sidestepping the challenges of powder handling. This not only boosts production efficiency but also mitigates contamination risks, especially in sensitive manufacturing environments.

By Application: Food and Beverage Segment Leadership

Food and beverage applications dominate the market, holding a 64.12% share in 2025. This underscores inulin's versatility, adeptly addressing fat reduction, sugar replacement, and fiber enhancement across a myriad of product categories. The U.S. Food and Drug Administration's guidelines on nutrient content claims empower manufacturers to spotlight inulin's fiber benefits. This not only bolsters fat and sugar reduction efforts but also paves the way for comprehensive product reformulations. The Codex Alimentarius Commission acknowledges the pivotal role of functional ingredients in enhancing nutritional profiles without compromising sensory attributes. This endorsement further cements inulin's presence in bakery, dairy, and processed food sectors.

Dietary supplements are set to be the fastest-growing sector, boasting a 7.16% CAGR through 2031. This surge is fueled by an aging population and a preventive healthcare movement emphasizing digestive health and metabolic support. The U.S. Dietary Supplement Health and Education Act lays down the regulatory groundwork for inulin-infused supplements, allowing for structure-function claims that resonate with health-savvy consumers. Similarly, Health Canada's Natural Health Products Regulations endorse inulin as a medicinal component for digestive health, unlocking further avenues in the regulated supplement market.

Geography Analysis

In 2025, Europe commands a dominant 47.42% share of the market, a testament to decades of regulatory evolution and consumer education in functional foods. This leadership is bolstered by a well-established infrastructure for chicory cultivation and processing. Starting February 2025, the European Food Safety Authority's revamped guidance on novel food assessments is set to streamline approval processes. While ensuring stringent safety standards, this move could hasten the introduction of new inulin products. Germany and France, with their rich health food traditions and robust domestic production, spearhead regional consumption. Meanwhile, the UK's regulatory alignment post-Brexit ensures continued market access for European suppliers. Europe's stringent labeling mandates, particularly under Regulation 1169/2011, bolster inulin's appeal as a 'clean label' choice, giving it an edge over synthetic counterparts.

Asia-Pacific, with a projected CAGR of 7.27% through 2031, is witnessing a surge in functional food adoption, driven by urbanization and increasing disposable incomes. China's regulatory landscape, notably its proposal to broaden health food categories to encompass candies and beverages, stands in stark contrast to the West's more stringent approach, potentially giving China a market development edge. Japan's aging demographic fuels a consistent demand for digestive health products. Coupled with the nation's advanced food processing capabilities, this creates a fertile ground for both traditional and contemporary applications of inulin. In India, a burgeoning processed food sector meets a rising health-conscious urban populace, presenting vast opportunities.

North America, while a mature market with clear regulatory landscapes and consumer awareness, still harbors growth potential in emerging applications and demographics. A case in point in 2024 is Canada's investment landscape, highlighted by Jungbunzlauer's USD 200 million biogum facility in Port Colborne. While this investment zeroes in on xanthan gum, it underscores the region's commitment to functional ingredient production. Clean label trends and a premiumization wave in health foods further bolster inulin's market presence. Additionally, with Jerusalem artichoke cultivation thriving in the northeastern and northcentral states, the region finds an alternative sourcing avenue, lessening its reliance on European chicory imports.

Competitive Landscape

The global inulin market is moderately consolidated in nature, characterized by the dominance of a limited number of major players who hold significant market shares across regions. Leading the charge are companies like Suedzucker AG, Cooperative Royal Cosun UA, Cosucra Groupe Warcoing SA, Cargill, Incorporated, and Ingredion Incorporated. These firms boast robust distribution networks, vertically integrated operations, and a steady stream of product innovations. Their strong presence in both developed and emerging markets not only gives them a competitive advantage but also empowers them to set pricing benchmarks and shape supply chain dynamics.

This consolidation has birthed a fiercely competitive landscape, where differentiation hinges on quality certifications, unique extraction methods, and the provision of value-added functional ingredients. These industry leaders pour significant resources into R&D, crafting inulin formulations that boast improved solubility, taste-masking features, and gut-health benefits. This aligns seamlessly with the rising consumer demand for clean-label and prebiotic-rich products. Furthermore, strategic partnerships with food and beverage manufacturers solidify their market stance, creating hurdles for smaller or nascent entrants.

Untapped potential lies in pharmaceutical realms, where inulin's capabilities in drug delivery remain largely commercialized. There's also promise in sustainable processing methods that not only address environmental challenges but also cut production costs. The FDA's GRAS nod for agave-derived inulin opens doors for new source materials, hinting at potential upheavals in the traditionally chicory-focused supply chains. On the horizon, biotechnology firms are pioneering fermentation-based inulin production, while agricultural tech companies are fine-tuning Jerusalem artichoke farming for large-scale inulin extraction.

Inulin Industry Leaders

-

Suedzucker AG

-

Royal Cosun (Coöperatie Koninklijke Cosun U.A.)

-

Cosucra Groupe Warcoing SA

-

Cargill, Incorporated

-

Ingredion Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Univar Solutions Belgium N.V. ("Univar Solutions"), a global leader in specialty ingredients and chemicals, has bolstered its collaboration with Ingredion Incorporated. Ingredion, renowned globally for its food and beverage ingredients, will see their partnership with Univar's Foodology division extend its reach into the Benelux region.

- April 2025: Prinova has acquired Brazilian specialty ingredients distributor Aplinova, expanding its presence in Latin America and gaining access to Aplinova’s expertise in functional ingredients, including inulin for food, beverage, supplement, and personal care markets. Aplinova, recognized as a key player in Brazil’s ingredients sector, recently opened an Innovation Centre in Jundiaí focused on research and development for health and wellness, sugar reduction, and natural flavors—areas where inulin is commonly utilized as a fiber and sugar substitute.

- November 2024: Cargill, a titan in the food and agriculture sector, has unveiled plans to inject a substantial US$240 million (around Rs. 1500 crores) into India over the coming five years. This infusion aims to bolster the nation's food safety and economic landscape, providing a significant boost to both the food processing and agriculture sectors.

- August 2024: In a strategic move, DKSH has broadened its exclusive distribution pact with Cosucra, a frontrunner in natural and health-centric food ingredients. This expansion, covering Australia and New Zealand, sees DKSH distributing Cosucra’s dietary fibers and plant-based proteins, amplifying market opportunities for both entities.

Global Inulin Market Report Scope

Inulin is a naturally occurring, non-absorbable, and indigestible oligosaccharide found in the roots or tubers of various plants such as Jerusalem artichoke or chicory. It stimulates the growth of beneficial bacteria in the gut, including Lactobacilli and Bifidobacteria, thereby modulating the microflora composition.

The inulin market is segmented by application and geography. By application, the market is segmented into food and beverage, dietary supplements, and pharmaceuticals. Food and beverage are further segmented into bakery and confectionery, dairy products, meat products, beverages, and other foods and beverages. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa.

For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| Agave |

| Jerusalem Artichoke |

| Chicory Root |

| Others |

| Powder |

| Liquid |

| Food and Beverages | Bakery and Confectinery |

| Dairy Products | |

| Meat Products | |

| Beverages | |

| Other Food and Beverages | |

| Dietary Supplements | |

| Pharmaceuticals |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Poland | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Egypt | |

| Morocco | |

| Turkey | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Source | Agave | |

| Jerusalem Artichoke | ||

| Chicory Root | ||

| Others | ||

| By Form | Powder | |

| Liquid | ||

| By Application | Food and Beverages | Bakery and Confectinery |

| Dairy Products | ||

| Meat Products | ||

| Beverages | ||

| Other Food and Beverages | ||

| Dietary Supplements | ||

| Pharmaceuticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Poland | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving the current growth of the inulin market?

Digestive-health awareness, clean-label reformulation, and FDA-backed fiber status are the primary catalysts supporting the 6.08% CAGR projected through 2031.

Which source dominates the inulin market and why?

Chicory root leads with 61.99% share because of entrenched European cultivation networks and mature extraction infrastructure that deliver consistent quality.

Why is liquid inulin gaining popularity in beverages?

Liquid forms dissolve rapidly, enable precise in-line dosing, and remove dust-control steps, translating to faster throughput and improved clarity in ready-to-drink products.

Which region is growing fastest for inulin consumption?

Asia-Pacific is expanding at a 7.27% CAGR as rising incomes and regulatory openness in China and Southeast Asia unlock new functional-food formats.

Page last updated on: