Luxury Jewelry Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

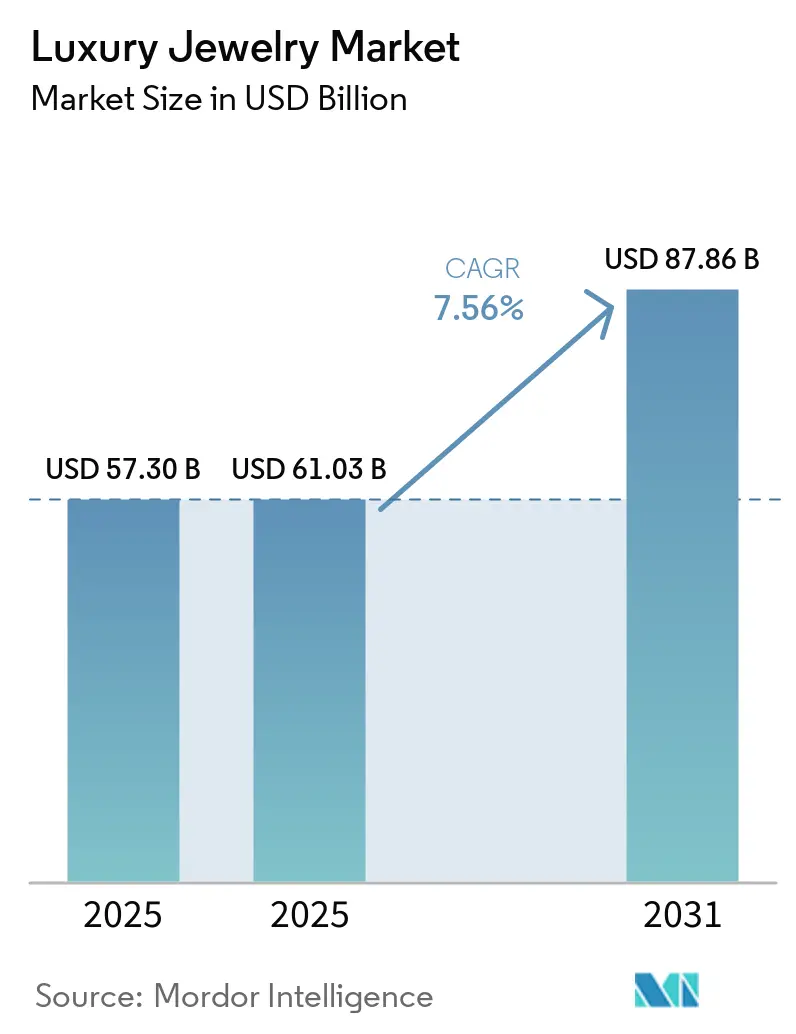

| Market Size (2025) | USD 61.03 Billion |

| Market Size (2031) | USD 87.86 Billion |

| Growth Rate (2026 - 2031) | 7.56% CAGR |

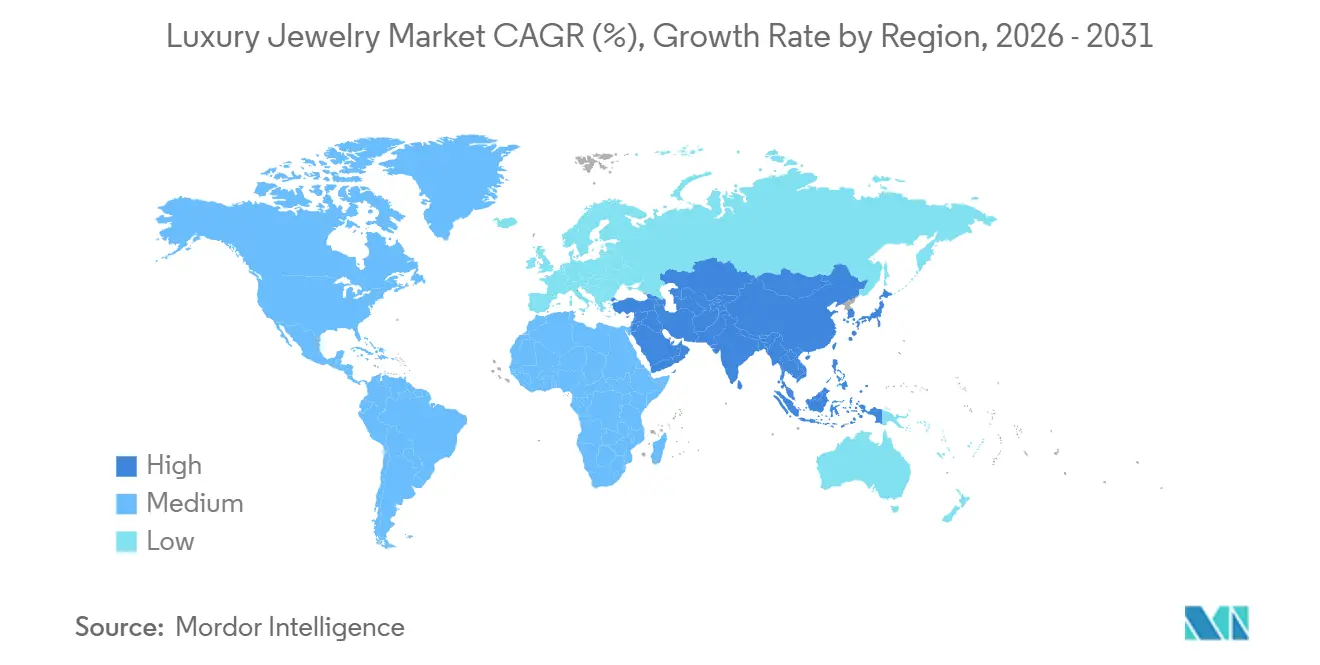

| Fastest Growing Market | South America |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Luxury Jewelry Market Analysis by Mordor Intelligence

The luxury jewelry market was valued at USD 57.30 billion in 2025 and is projected to reach USD 61.03 billion in 2026, with an anticipated growth to USD 87.86 billion by 2031, registering a CAGR of 7.56% during the forecast period. The growing demand for personalized designs, limited-edition creations, and unique jewelry pieces is driving continuous innovation in product development and enhancing consumer engagement. Additionally, the increasing significance of jewelry as a lifestyle statement and a representation of personal identity has boosted demand, with consumers favoring products that blend artistic value, heritage, and modern design aesthetics. The market is further supported by the rising adoption of sustainable practices, ethical sourcing, and material innovation within the luxury jewelry industry.

Key Report Takeaways

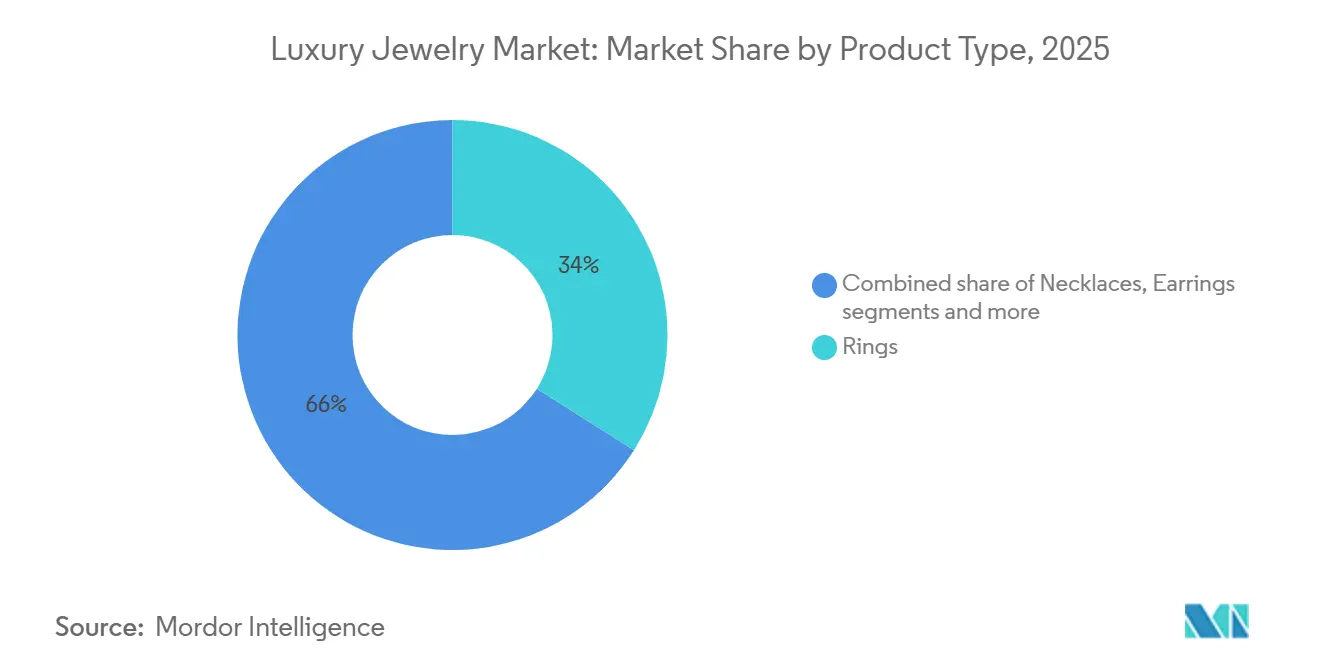

- By product type, rings led with 34.01% revenue share in 2025, while necklaces are forecast to expand at an 8.57% CAGR through 2031.

- By raw material, gold held 42.31% of the luxury jewelry market size in 2025, while diamond recorded the fastest projected CAGR at 8.65% through 2031.

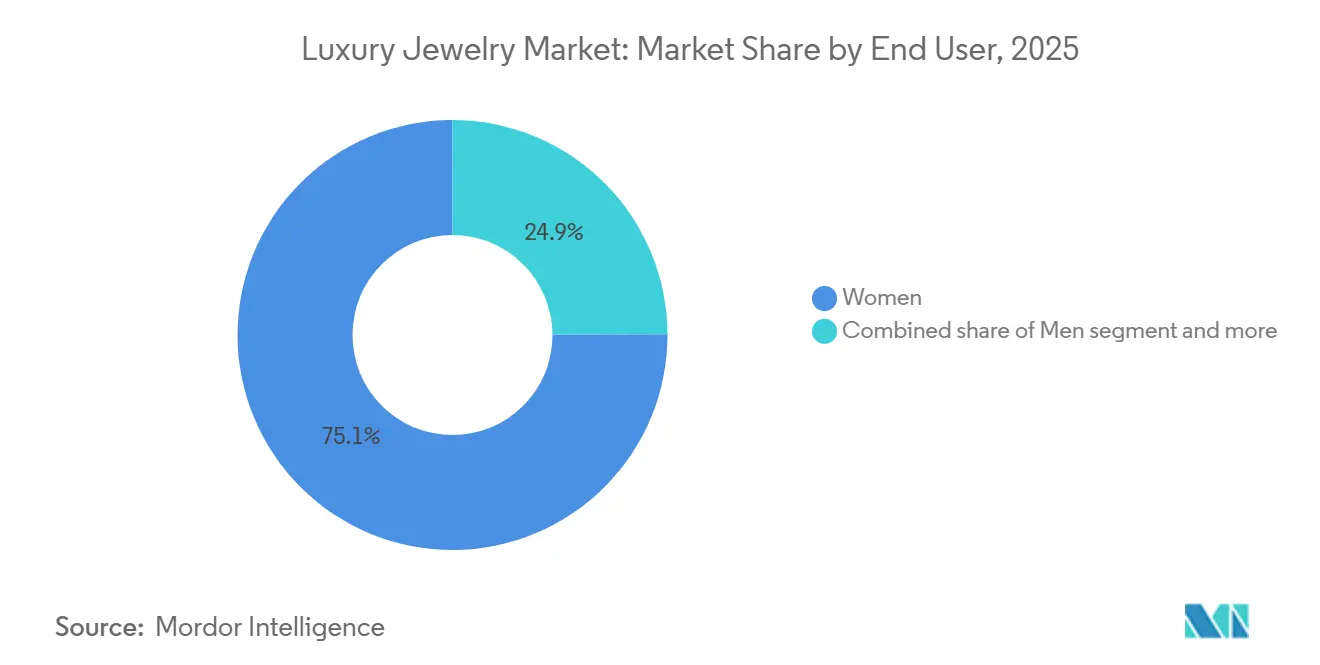

- By end user, women held 75.06% of the luxury jewelry market share in 2025, while men are projected to grow at a 7.91% CAGR through 2031.

- By distribution channel, offline retail stores accounted for 80.18% share in 2025, while online retail stores are forecast to advance at an 8.91% CAGR through 2031.

- By geography, Asia-Pacific led with 32.25% share in 2025, while South America is projected to expand at an 8.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Luxury Jewelry Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for personalized and customized jewelry | +1.2% | Global, with concentrated gains in North America, China, and United Arab Emirates | Medium term (2-4 years) |

| Impact of celebrity endorsements and social media | +1.6% | Global; highest intensity in East Asia, South America, and North America | Short term (≤ 2 years) |

| Adoption of lab-grown diamonds and innovative materials | +1.4% | Global; strongest in North America, India, and Southeast Asia | Medium term (2-4 years) |

| Rising popularity of sustainable and ethical jewelry | +0.8% | Europe and North America core; Asia-Pacific spill-over accelerating | Long term (≥ 4 years) |

| Demand for jewelry as a fashion and lifestyle statement | +0.6% | Global, with highest traction among Gen Z consumers in Asia-Pacific and South America | Short term (≤ 2 years) |

| Product innovation and contemporary design developments | +0.5% | Global, particularly in Italy (manufacturing base) and France-Switzerland luxury triangle | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demand for personalized and customized jewelry

The increasing demand for personalized and customized jewelry is a key factor driving the growth of the luxury jewelry market. Consumers are seeking exclusive pieces that reflect their personal identity, style preferences, and emotional connections. There is a growing interest in bespoke creations, including unique settings, customized engravings, personalized gemstone selections, and made-to-order designs that emphasize individuality and exclusivity. In response, luxury jewelry brands are expanding their customization services by integrating traditional craftsmanship with advanced technologies such as digital design tools, 3D modeling, and virtual visualization. These innovations enable consumers to actively participate in the design process. Furthermore, the rising preference for limited-edition and one-of-a-kind jewelry pieces has enhanced the appeal of personalization, as customized products are increasingly associated with rarity, authenticity, and superior craftsmanship.

Impact of celebrity endorsements and social media

The increasing influence of celebrity endorsements and social media is driving growth in the luxury jewelry market by enhancing brand visibility, consumer engagement, and demand for high-end products. Luxury jewelry brands are actively collaborating with celebrities, artists, and digital influencers to build emotional connections with consumers and boost brand appeal, particularly among younger demographics. Social media platforms have reshaped how consumers discover luxury jewelry, allowing brands to present new collections, craftsmanship, styling ideas, and exclusive campaigns to a broader global audience. Celebrity partnerships create strong associations between jewelry pieces and lifestyle, fashion identity, and cultural significance, fostering interest in premium collections. For example, in July 2025, Pomellato appointed Roy Wang, a Gen Z C-pop idol, as its global brand ambassador to enhance engagement with younger luxury consumers and expand its cultural reach.

Adoption of lab-grown diamonds and innovative materials

The adoption of lab-grown diamonds and innovative materials is increasing as consumers and brands prioritize sustainability, transparency, and modern luxury concepts. Luxury jewelry manufacturers are utilizing advanced materials, recycled precious metals, and technology-driven alternatives to meet evolving consumer expectations while maintaining high standards of quality and craftsmanship. Lab-grown diamonds are becoming more widely accepted due to their traceability, controlled production processes, and potential for enabling creative designs without sacrificing brilliance or durability. Furthermore, the incorporation of alternative materials and responsible sourcing practices allows luxury brands to distinguish their collections and attract environmentally conscious consumers. For example, Prada’s Eternal Gold collection features certified recycled gold and jewelry pieces with lab-grown diamonds, showcasing the integration of sustainable materials with innovative luxury design.

Rising popularity of sustainable and ethical jewelry

The increasing demand for sustainable and ethical jewelry is propelling growth in the luxury jewelry market, as consumers place greater emphasis on transparency, responsible sourcing, and environmentally conscious purchasing. Luxury jewelry brands are adapting by utilizing ethically sourced gemstones, recycled precious metals, traceable supply chains, and responsible manufacturing practices to meet evolving consumer expectations. Heightened awareness of the environmental and social impacts of traditional mining has prompted companies to adopt sustainable production methods while preserving premium craftsmanship and exclusivity. Additionally, the use of blockchain-based traceability, certification programs, and responsible sourcing standards is enhancing consumer trust by offering improved visibility into the origin and authenticity of materials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concerns regarding counterfeit luxury jewelry products | -1.1% | Global; highest exposure in online secondary markets across Asia-Pacific, Eastern Europe, and Middle East | Short term (≤ 2 years) |

| Price volatility and precious metal availability | -1.6% | Global; most acute in volume-dependent markets like India, China, and Southeast Asia | Short term (≤ 2 years) |

| Increasing cybersecurity risks in online luxury jewelry retail | -0.6% | North America, Europe, and rapidly digitalizing Asia-Pacific markets | Medium term (2-4 years) |

| Shift towards experiential luxury over material products | -0.4% | North America and Western Europe; emerging signal in urban Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Concerns regarding counterfeit luxury jewelry products

The increasing prevalence of counterfeit luxury jewelry products poses a significant challenge to the luxury jewelry market. The circulation of imitation products negatively affects brand reputation, consumer trust, and the perceived exclusivity of premium jewelry. Counterfeit items often mimic luxury designs, logos, and packaging but lack authentic materials, certified quality, and craftsmanship, creating difficulties for both consumers and established brands. The growth of digital marketplaces and unauthorized sales channels has further complicated efforts to control counterfeit products. As a result, luxury jewelry companies are investing in advanced authentication technologies, product traceability solutions, and enhanced intellectual property protection measures. For example, according to United States Customs and Border Protection (CBP), in August 2025, CBP officers in Louisville intercepted a shipment containing over 7,000 pairs of counterfeit earrings, underscoring the increasing challenge of counterfeit jewelry entering the market [1]Source: United States Customs and Border Protection (CBP), "USD30 million in counterfeit jewelry seized by Louisville CBP", cbp.gov.

Price volatility and precious metal availability

The price volatility and limited availability of precious metals pose significant challenges for the luxury jewelry market. Fluctuations in the supply and cost of essential materials, such as gold, platinum, and rare gemstones, directly affect production planning, pricing strategies, and profitability. The industry relies heavily on a stable supply of high-quality raw materials, but disruptions caused by mining limitations, supply chain issues, changing resource availability, and heightened competition for these materials create uncertainty for manufacturers. Rising material costs can lead to higher product prices, influencing consumer purchasing decisions and complicating efforts to maintain consistent collections and inventory levels. Furthermore, the scarcity of premium-grade metals and gemstones increases sourcing complexity, necessitating greater investment in responsible procurement, certification, and supplier partnerships.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rings Anchor Revenue as Necklaces Define the Next Growth Arc

The rings segment is projected to account for 34.01% of global luxury jewelry revenues in 2025, driven by growing consumer preference for premium, symbolic, and highly personalized jewelry. This growth is fueled by increasing demand for unique designs, superior craftsmanship, and exclusive collections that emphasize individuality and personal expression. The rising trend of customization, including personalized engravings, distinctive settings, and made-to-order creations, has enhanced the appeal of luxury rings among consumers seeking meaningful and differentiated products. Furthermore, advancements in jewelry design technologies and manufacturing techniques have enabled greater creativity, precision, and innovation, allowing brands to offer intricate styles, modern aesthetics, and limited-edition collections.

The necklaces segment is the fastest-growing product type in the luxury jewelry market, with a projected CAGR of 8.57% through 2031. This growth is driven by increasing consumer preference for statement pieces, evolving fashion trends, and rising demand for versatile luxury accessories. The segment is gaining traction as consumers seek distinctive designs that align with personal style and enhance self-expression. Interest in contemporary aesthetics, innovative craftsmanship, and exclusive collections has spurred the development of unique necklace designs featuring intricate patterns, rare materials, and artistic elements. Additionally, the influence of fashion movements and luxury styling trends has positioned necklaces as a key component of premium wardrobes, encouraging frequent adoption beyond traditional purchasing occasions.

By Raw Material: Gold's Cultural Primacy Intact as Diamond Assumes Fastest-Growth Position

The gold segment accounted for 42.31% of luxury jewelry revenues in 2025, driven by its enduring appeal as a premium material, strong consumer preference for timeless jewelry pieces, and its association with quality, exclusivity, and craftsmanship. Gold remains a preferred choice among luxury jewelry consumers due to its versatility in creating diverse designs, long-lasting value perception, and compatibility with both traditional and modern aesthetics. Additionally, the rising emphasis on certified purity, responsible sourcing, and high-quality craftsmanship has bolstered consumer confidence in gold-based luxury jewelry. Supporting this demand, the World Gold Council reported that global gold demand reached 5,025.2 metric tons in 2025, up from 4,606.2 metric tons in the previous year, underscoring the sustained preference and strong global demand for gold [2]Source: World Gold Council, "Gold demand worldwide", gold.org.

The diamond segment is the fastest-growing raw material segment in the luxury jewelry market, registering an 8.65% CAGR through 2031. This growth is driven by the adoption of advanced diamond processing techniques, evolving consumer interest in rare stone characteristics, and the rising popularity of distinctive diamond formats. Innovations in precision cutting, grading technologies, and stone enhancement methods are enabling the creation of more refined and intricate jewelry designs, increasing the appeal of diamond-based collections. The emergence of lab-grown diamonds has further expanded the market by offering improved traceability, design flexibility, and sustainable alternatives while maintaining a luxury positioning. Additionally, the growing demand for certified stones with detailed origin verification, coupled with the integration of digital authentication technologies, is enhancing transparency across the diamond value chain.

By End User: Women's Dominance Persists as Men's Category Accelerates in New Geographies

The women segment accounted for 75.06% of the luxury jewelry market share in 2025, driven by evolving fashion preferences, self-purchasing trends, and the increasing role of jewelry as a form of personal expression. The demand for diverse collections, ranging from classic designs to contemporary styles, has spurred continuous innovation in luxury jewelry offerings to align with changing consumer tastes. The growing trend of women purchasing premium jewelry for themselves as a symbol of achievement, individuality, and lifestyle preference has expanded demand beyond traditional gifting patterns. Additionally, greater interest in versatile jewelry suitable for various styling needs, along with a preference for exclusive designs, limited collections, and artisan craftsmanship, is further strengthening the growth of this segment.

The men’s segment is projected to grow at a 7.91% CAGR through 2031, reflecting a structural shift in masculine identity as jewelry increasingly becomes a medium of personal style, individuality, and lifestyle expression. This growth is driven by changing perceptions of men’s accessories, with luxury jewelry gaining acceptance as part of modern fashion rather than being confined to traditional or formal use. Rising interest in refined aesthetics, minimalist designs, and bold statement pieces has encouraged greater adoption of premium jewelry among male consumers. The influence of fashion trends, digital media, and evolving style culture has further normalized jewelry ownership among men, supporting demand for innovative and contemporary collections.

By Distribution Channel: Physical Retail Remains Foundational as Online Accelerates Without Substituting

Offline retail stores accounted for 80.18% of luxury jewelry revenues in 2025, highlighting the continued significance of physical retail experiences in high-value and carefully considered purchases. This segment is driven by consumers' preference for personalized interactions, expert guidance, and the ability to assess jewelry quality, craftsmanship, and detailing before making a purchase. Luxury jewelry buyers place importance on exclusive store environments, private consultations, professional styling support, and customized services that enhance confidence and create a premium purchasing experience. The opportunity to physically inspect materials, finishes, stone brilliance, and design accuracy builds consumer trust, while relationship-based services and after-sales support further emphasize the role of offline retail stores in the luxury jewelry market.

Online retail stores are projected to grow at a CAGR of 8.91% through 2031, fueled by the rapid evolution of digital luxury experiences and the increasing adoption of technology-enabled shopping platforms. This growth is supported by features such as virtual product visualization, augmented reality try-on tools, digital consultations, and advanced product authentication systems, which enhance consumer confidence in online purchases. Luxury brands are focusing on creating immersive digital experiences, secure transaction processes, and personalized recommendations to replicate premium service standards in online channels. Furthermore, advancements in logistics, transparent certification processes, and seamless omnichannel integration are contributing to the faster growth of digital platforms.

Geography Analysis

In 2025, Asia-Pacific accounted for 32.25% of global luxury jewelry revenues, driven by the region's rich jewelry traditions, growing preference for premium craftsmanship, and increasing demand for high-value branded collections. China remains the largest national contributor, supported by robust luxury consumption trends and demand for both heritage-inspired and contemporary jewelry designs. India is emerging as the fastest-growing major market, owing to its strong cultural connection with precious jewelry and a rising preference for premium products. For example, according to the Gem & Jewellery Export Promotion Council (GJEPC), the import value of gold jewelry in India exceeded USD 1.9 billion in fiscal year 2025, a significant increase from USD 1.4 billion in 2024, underscoring the growing demand for premium gold jewelry [3]Source: Gem & Jewellery Export Promotion Council (GJEPC), "Import value of gold jewelry across India", gjepc.org.

South America is the fastest-growing region in the luxury jewelry market, with a CAGR of 8.55% projected through 2031. This growth is fueled by the increasing adoption of luxury fashion trends, rising consumer interest in premium accessories, and the expanding presence of organized jewelry retail formats. Brazil and Argentina are key markets driving regional growth, as consumers increasingly favor branded jewelry, contemporary designs, and certified premium products. Additionally, the growing influence of fashion-driven purchases, a preference for unique gemstones, and the expansion of digital luxury experiences are enhancing consumer engagement and accelerating market growth across the region.

North America and Europe together represent the most mature and brand-concentrated regions in the luxury jewelry market. These regions benefit from strong demand for established luxury houses, designer collections, and high-value craftsmanship. Consumers in these markets prioritize authenticity, exclusivity, sustainable sourcing, and heritage-based jewelry offerings, creating a favorable environment for premium brands. The Middle East and Africa market is experiencing steady growth, supported by a strong affinity for luxury jewelry, demand for elaborate designs, and a preference for precious metals and gemstones. The region's luxury retail expansion, tourism-driven purchases, and appreciation for premium craftsmanship continue to contribute to long-term market development.

Competitive Landscape

The luxury jewelry market is fragmented, with numerous global luxury houses and specialized jewelry brands competing through product differentiation, craftsmanship excellence, and strong brand positioning. Key players in the market include LVMH Moët Hennessy Louis Vuitton SE, Compagnie Financière Richemont SA, Chanel S.A., Signet Jewelers Limited, and Kering S.A. These companies focus on enhancing their premium portfolios through exclusive collections, iconic designs, and superior craftsmanship to maintain consumer loyalty and strengthen their presence in the evolving luxury jewelry industry.

Competition in the market is increasingly influenced by heritage storytelling, technological integration, and geographic expansion into high-growth markets. Luxury jewelry brands are leveraging their brand legacy, artisanal expertise, and distinctive design identities to build stronger emotional connections with consumers. Simultaneously, brands are adopting digital tools such as virtual experiences, personalized shopping services, data-driven engagement strategies, and authentication technologies to enhance customer interaction and reinforce trust in premium purchases.

Additionally, companies are prioritizing strategic collaborations, boutique expansions, sustainability initiatives, and innovation in jewelry design to bolster their competitive positions. The growing focus on responsible sourcing, traceability of precious materials, and ethical craftsmanship has emerged as a key differentiator among luxury jewelry brands. Continued investments in omnichannel strategies, exclusive customer experiences, and limited-edition collections are expected to intensify competition and drive long-term growth opportunities in the global luxury jewelry market.

Luxury Jewelry Industry Leaders

-

LVMH Moet Hennessy Louis Vuitton SE

-

Compagnie Financiere Richemont SA

-

Chanel S.A.

-

Signet Jewelers Limited

-

Kering S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Chow Tai Fook Jewellery has opened a newly designed boutique in Canada at Oakridge Park, Vancouver. Featuring the brand’s signature "Timeless Red" façade, the boutique combines contemporary design with elegant oriental aesthetics.

- June 2026: Tiffany & Co. has introduced the summer segment of its high jewelry collection, Blue Book 2026: Hidden Garden. This collection draws inspiration from the hidden aspects of nature, featuring natural diamonds that resemble morning dew on flower petals and blades of grass.

- July 2025: Van Cleef & Arpels introduced two nature-inspired high jewelry collections, Flowerlace and Fleurs d'Hawaï. Drawing from the maison's floral heritage, these intricate pieces were presented during an exhibition at Scotland's historic Dumfries House.

Global Luxury Jewelry Market Report Scope

Luxury jewelry refers to high-end ornaments crafted by historic legacy maisons or elite designers using rare, high-quality materials and unparalleled master craftsmanship. The luxury jewelry market is segmented by product type, raw material, end user, distribution channel, and geography. Based on product type, the market is segmented into rings, necklaces, earrings, bracelets, chains and pendants, and other product types. Based on raw material, the market is segmented into gold, platinum, diamond, gemstone, and others. Based on end user, the market is segmented into men, women, and children. Based on distribution channel, the market is segmented into offline retail stores and online retail stores. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecast have been done based on the value (in USD million).

| Rings |

| Necklaces |

| Earrings |

| Bracelets |

| Chains and Pendants |

| Other Product Types |

| Gold |

| Platinum |

| Diamond |

| Gemstone |

| Others |

| Men |

| Women |

| Children |

| Offline Retail Stores |

| Online Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Rings | |

| Necklaces | ||

| Earrings | ||

| Bracelets | ||

| Chains and Pendants | ||

| Other Product Types | ||

| By Raw Material | Gold | |

| Platinum | ||

| Diamond | ||

| Gemstone | ||

| Others | ||

| By End User | Men | |

| Women | ||

| Children | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of luxury jewelry by 2031?

The luxury jewelry market is forecast to reach USD 87.86 billion by 2031, up from USD 61.03 billion in 2026, at a 7.6% CAGR over 2026-2031.

Which product type leads luxury jewelry sales today?

Rings led revenue in 2025 with a 34.01% share, supported by strong bridal, anniversary, and ceremonial demand.

Which raw material is growing fastest in premium jewelry collections?

Diamond is the fastest-growing raw material segment, with an 8.65% CAGR projected through 2031, helped by the widening role of lab-grown stones and premium natural diamond positioning.

Why is Asia-Pacific important for global luxury jewelry demand?

Asia-Pacific held 32.25% of revenue in 2025, with China as the largest national market in the region and India gaining ground as a major diamond jewelry buyer.

Page last updated on: