Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

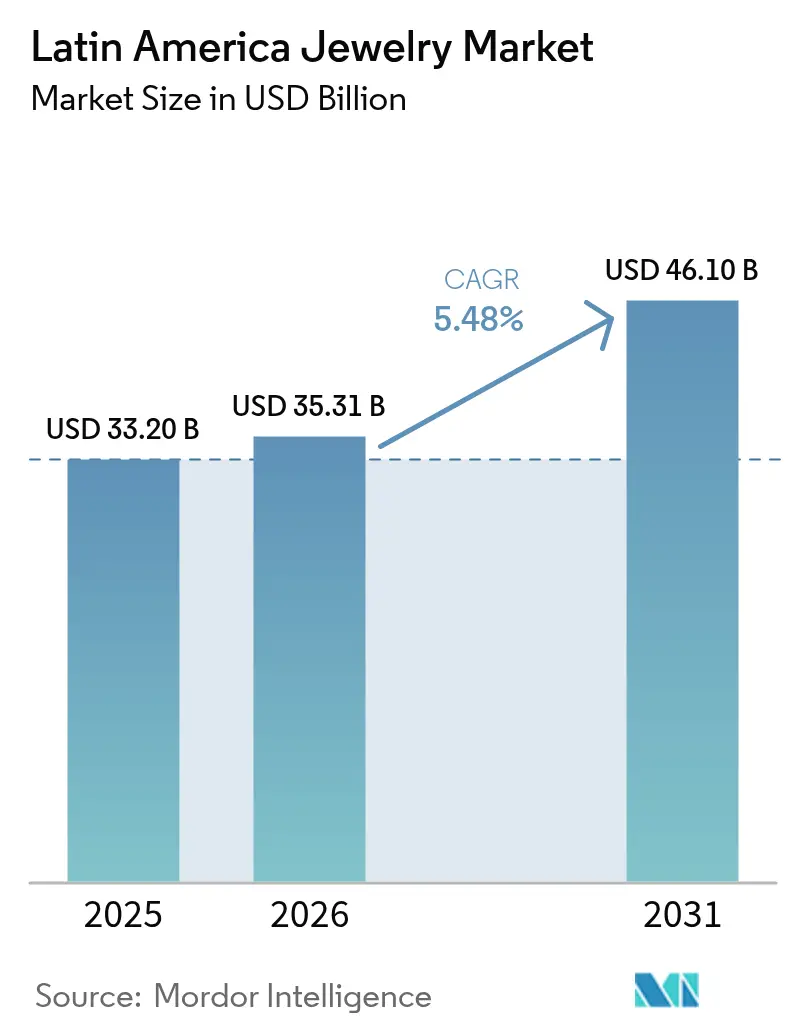

| Base Year Market Size (2025) | USD 33.20 Billion |

| Market Size (2026) | USD 35.31 Billion |

| Market Size (2031) | USD 46.10 Billion |

| Growth Rate (2026 - 2031) | 5.48% CAGR |

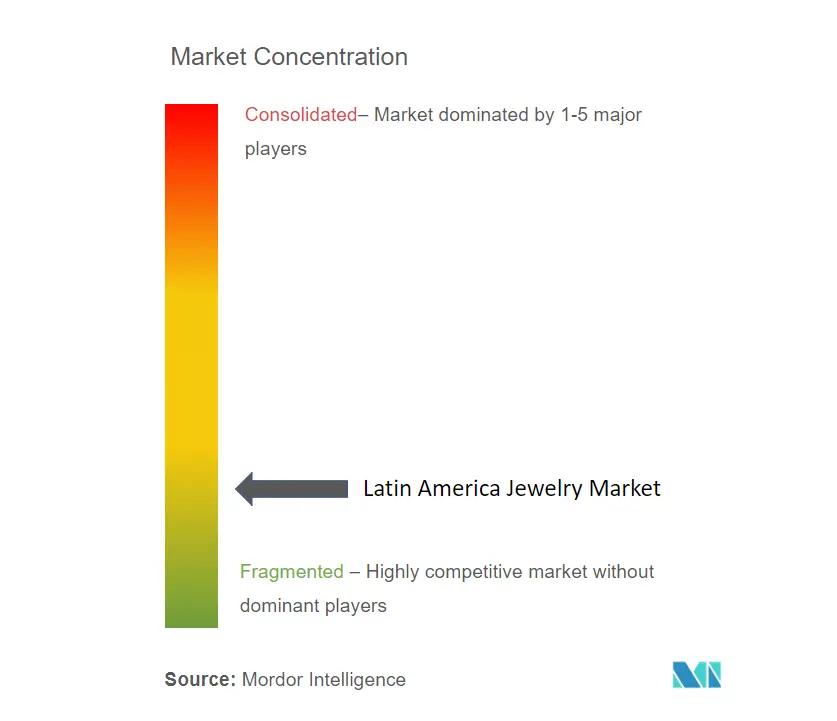

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Latin America Jewelry Market Analysis by Mordor Intelligence

The Latin America jewelry market size is projected to be USD 33.20 billion in 2025, USD 35.31 billion in 2026, and reach USD 46.10 billion by 2031, growing at a CAGR of 5.48% from 2026 to 2031. Rising disposable incomes in Brazil and Mexico, modernization of the retail channel, and the turn toward branded luxury underpin this trajectory. Brazil’s luxury segment expanded 11.7% in 2024 and is forecast to advance 15% in 2025, reinforcing the country’s pivotal role within the Latin America jewelry market. Inflationary headwinds in Argentina temper spending power, yet tariff reductions on capital goods and a firmer reserve position are restoring confidence. Meanwhile, accelerating e-commerce adoption and the launch of lab-grown diamonds are widening access to affordable luxury across the region. Counterfeit risks, raw-material volatility, and complex import duties remain structural challenges, but firms that localize design, authenticate products, and leverage digital channels appear well positioned to capture growth in the Latin American jewelry market.

Key Report Takeaways

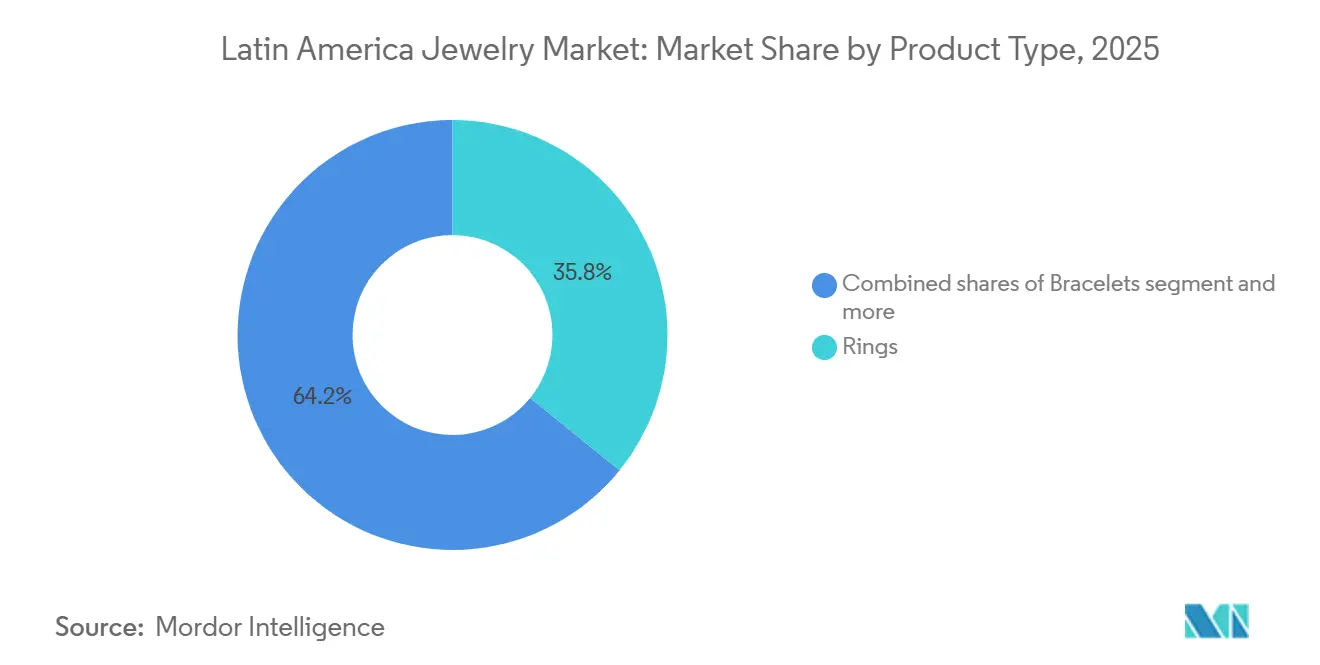

- By product type, rings led with 35.84% of the Latin America jewelry market share in 2025, while bracelets posted the fastest growth at a 6.93% CAGR through 2031.

- By material, precious metals captured 63.72% of 2025 sales; mixed-material pieces are advancing at a 6.34% CAGR to 2031.

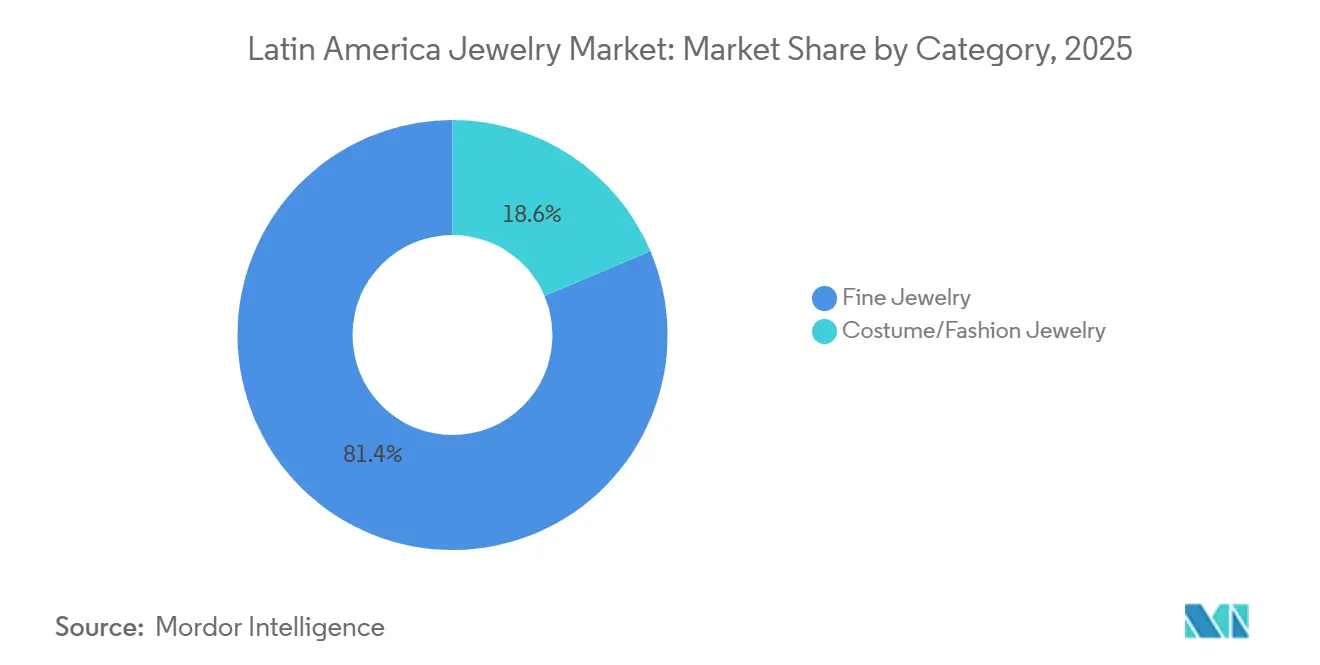

- By category, fine jewelry maintained an 81.38% share in 2025, whereas costume and fashion jewelry are set to rise at a 6.28% CAGR through 2031.

- By end user, women accounted for 73.65% of 2025 purchases; men’s jewelry registers the highest 7.53% CAGR over 2026-2031.

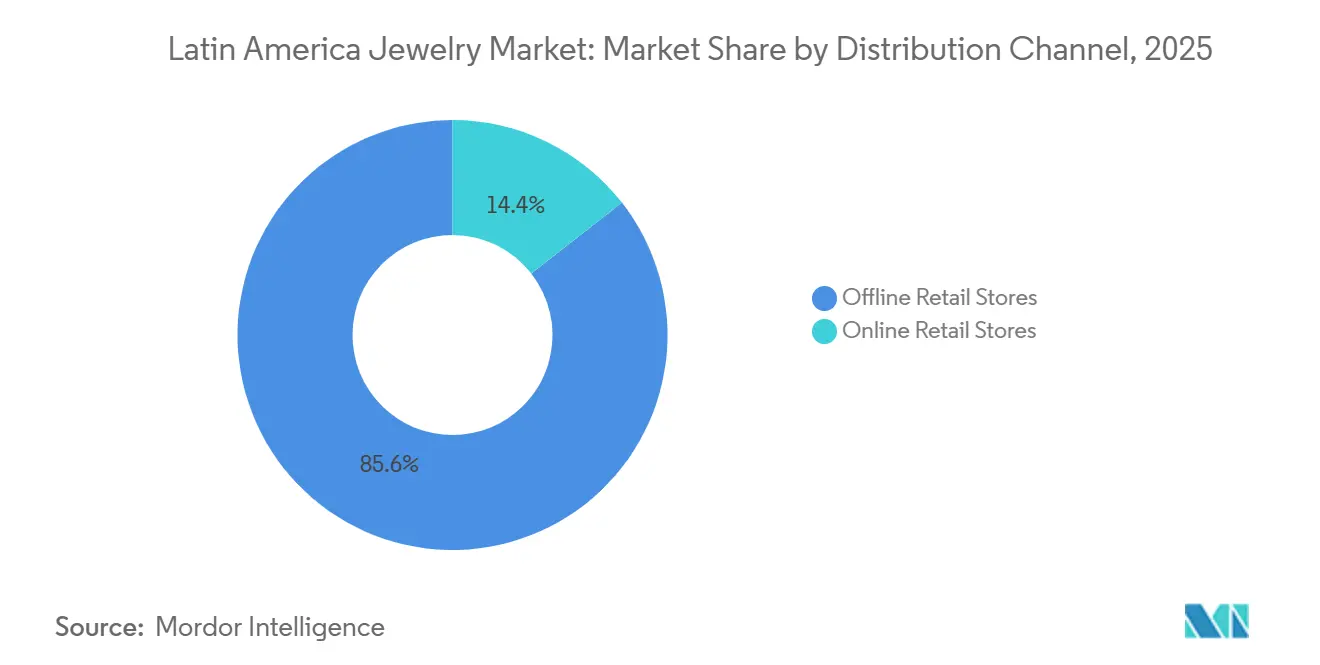

- By distribution channel, offline stores accounted for 85.56% of 2025 turnover, while online sales are growing at 5.82% annually through 2031.

- By geography, Brazil dominated with 44.53% of 2025 revenue, and Argentina represents the quickest-expanding market at a 6.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Latin America Jewelry Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising popularity of customized and personalized jewelry pieces | +0.8% | Brazil, Mexico, Chile; spillover to Argentina and Colombia | Medium term (2-4 years) |

| Tourism-driven jewelry purchases | +0.7% | Brazil, Colombia, Peru; Caribbean coastal zones | Short term (≤ 2 years) |

| Strong cultural significance of jewelry in celebrations | +0.9% | Region-wide with peak intensity in Mexico, Brazil, Colombia | Long term (≥ 4 years) |

| Expansion of branded retail chains and shopping malls | +1.0% | Brazil, Mexico, Chile, Colombia | Medium term (2-4 years) |

| Rising demand for affordable luxury and demi-fine jewelry | +0.8% | Brazil, Argentina, Chile | Medium term (2-4 years) |

| Growth of lab-grown diamonds and synthetic gemstones | +0.6% | Brazil, Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Popularity of Customized and Personalized Jewelry Pieces

Customization has shifted from a niche service to a core revenue stream, particularly in Brazil and Chile, where consumers increasingly demand pieces that reflect personal narratives rather than mass-market designs. Vivara's Life brand, a silver-jewelry line positioned as "democratic luxury", expanded rapidly in 2025, with the company targeting a doubling of Life stores to capture middle-income buyers seeking affordable personalization. Tiffany's limited-edition Lock bracelet, released in São Paulo in December 2024 with only 10 pieces featuring Brazilian-flag-inspired sapphires and tsavorite, sold out within days, demonstrating that scarcity and local symbolism drive premiums even in a price-sensitive market. This trend is underpinned by the rise of digital configurators and in-store engraving services, which lower the cost of bespoke production while maintaining the perception of exclusivity. Regional artisans in Chile and Peru are leveraging heritage techniques, such as filigree and pre-Columbian motifs, to differentiate themselves from global brands, creating a bifurcated market where both high-tech personalization platforms and handcrafted customization coexist. The shift toward personalization also reflects a broader generational change; younger buyers view jewelry as an extension of identity rather than a status symbol, a behavioral pivot that favors brands capable of rapid design iteration and direct-to-consumer engagement.

Tourism-Driven Jewelry Purchases

Tourism recovery across Latin America has reignited jewelry sales in gateway cities, with the Americas reaching approximately 97% of 2019 visitor levels by 2024, according to UN Tourism data[1]Source: UN Tourism, “World Tourism Barometer,” unwto.org. Colombia's visitor exports totaled COP 42.1 billion in 2024, a figure that includes significant jewelry purchases by international tourists drawn to Bogotá's emerald district and Cartagena's artisan markets, according to the World Travel and Tourism Council. Airport retail has emerged as a strategic channel; Panama's Tocumen International Airport, a regional hub, saw luxury jewelry concessions expand in 2024-2025, capturing transit passengers traveling between North and South America. Tiffany's opening of its first Blue Box Café in Latin America, located within the Mexico City flagship in February 2025, signals that experiential retail tied to tourism can drive both immediate sales and long-term brand affinity. Brazil's luxury market benefits from domestic tourism as well; São Paulo's Iguatemi mall, which attracts approximately 50,000 visitors daily, hosts flagship stores from Tiffany, Cartier, and Chanel, effectively functioning as a jewelry destination for affluent Brazilians and regional tourists. The tourism-jewelry nexus is further amplified by duty-free shopping incentives in Chile and Argentina, where foreign visitors can reclaim value-added taxes on high-ticket purchases, making fine jewelry comparatively more attractive than in domestic markets with cumulative taxation.

Strong Cultural Significance of Jewelry in Celebrations

Jewelry remains deeply embedded in Latin American life-cycle events, quinceañeras, weddings, and religious confirmations, where gold and gemstone pieces serve as both adornment and intergenerational wealth transfer. In Mexico and Colombia, quinceañera ceremonies often involve the gifting of gold jewelry sets, a tradition that sustains demand for rings, necklaces, and earrings even during economic downturns. Brazil's wedding market, which rebounded strongly in 2024-2025 after pandemic delays, drives engagement ring and wedding band sales, with Vivara reporting record margins in the third quarter of 2025, partly attributable to bridal demand. Religious festivals, such as Brazil's Festa de Nossa Senhora Aparecida and Colombia's Semana Santa, spur purchases of devotional jewelry, including crosses and medallions, often crafted from precious metals to ensure longevity and heirloom status. This cultural embeddedness creates a demand floor that is relatively insulated from discretionary spending cuts; families prioritize jewelry for milestone events even as they reduce expenditures in other categories. The trend also favors local and regional brands that understand ceremonial nuances; for instance, Tous's 20-year presence in Chile and its June 2025 opening of a concept store in Bogotá's Nuestro Bogotá mall reflect a strategy of embedding the brand within local celebration ecosystems. Cultural significance also extends to inheritance practices, where jewelry functions as portable, divisible wealth, particularly relevant in Argentina's volatile economic environment where tangible assets hedge against currency devaluation.

Rising Demand for Affordable Luxury and Demi-Fine Jewelry

Affordable luxury, defined as jewelry priced between mass-market costume pieces and traditional fine jewelry, is capturing share as middle-income consumers seek brand prestige without the price tags of solid gold or natural diamonds. Vivara's Life brand, which focuses on silver jewelry with gemstone accents, generated strong sales growth in 2025, enabling the company to post a 33% profit increase in the third quarter despite a strategic pause on new gold purchases until mid-2026. Pandora's lab-grown diamond collections, launched in Mexico and Brazil in the second half of 2023, have gained traction among younger buyers who prioritize sustainability and value; lab-grown diamonds typically cost 60-80% less than natural equivalents, making them accessible to consumers priced out of traditional fine jewelry. The 23% increase in gold prices during 2024, which pushed the average price to USD 2,386 per ounce, accelerated the shift toward mixed-material designs that combine base metals with plated finishes or synthetic gemstones, according to the World Gold Council[2]Source: World Gold Council, “Gold Demand Trends Full Year 2024,” gold.org . This segment is also benefiting from e-commerce penetration; Brazil's online retail market will grow from USD 52.87 billion in 2024 to USD 125.68 billion by 2029, with jewelry a top-performing category as digital channels reduce distribution costs and enable direct-to-consumer pricing, according to the U.S. International Trade Administration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High risk of jewelry counterfeiting and imitation products | -0.5% | Brazil, Chile, Argentina; e-commerce channels across region | Short term (≤ 2 years) |

| Economic volatility and inflationary pressures | -0.7% | Argentina (acute), Brazil, Colombia; spillover to Peru and Chile | Medium term (2-4 years) |

| Complex import/export duties and taxation | -0.6% | Brazil (cumulative tax regime), Argentina, Colombia; intra-Mercosur trade | Long term (≥ 4 years) |

| Fluctuating prices of gold, silver, and gemstones | -0.5% | Global, with acute impact on Brazil and Mexico producers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Risk of Jewelry Counterfeiting and Imitation Products

Counterfeiting erodes brand equity and consumer trust, with Latin America particularly vulnerable due to porous borders, limited enforcement resources, and the proliferation of e-commerce platforms that facilitate cross-border sales of fake goods. INTERPOL's Operation Crete II, conducted in 2024, seized 2,478 counterfeit jewelry items valued at USD 523,000 in Chile alone, underscoring the scale of illicit trade in a relatively small market[3]Source: INTERPOL, “Operation Crete II Targets Counterfeit Goods,” interpol.int . The OECD and EUIPO jointly calculated a global jewelry counterfeiting propensity index (GTRIC-p) of 0.8661, indicating that nearly 87% of jewelry trade flows face a high risk of imitation; the European Union scored 0.998, indicating near-universal exposure. In Brazil, the rise of Chinese e-commerce platforms, such as AliExpress, Shein, and Temu, has flooded the market with low-cost jewelry that often mimics branded designs, compressing margins for legitimate players and confusing consumers about authenticity. Mexico's anti-counterfeiting framework includes holographic seals and digital registries, yet enforcement remains inconsistent, particularly in informal markets where counterfeit jewelry circulates alongside genuine pieces. The reputational damage is compounded by social media; a single viral post exposing a fake Pandora charm or Tous bracelet can deter thousands of potential buyers. Blockchain-based authentication systems are emerging as a countermeasure, brands are piloting digital certificates tied to individual pieces, but adoption is slow and costly, limiting deployment to high-value items rather than mass-market jewelry.

Fluctuating Prices of Gold, Silver, and Gemstones

Raw material price volatility directly impacts jewelry margins and consumer affordability, with gold prices averaging USD 2,386 per ounce in 2024, a 23% year-over-year increase, and the World Bank forecasting further rises to USD 3,400 in 2025 and USD 3,575 in 2026, according to the World Gold Council. J.P. Morgan's more aggressive projection, estimating a move toward USD 5,000 per ounce by the fourth quarter of 2026, introduces uncertainty for producers who must decide whether to hedge, pass costs through to consumers, or absorb margin compression. Vivara's decision to pause new gold purchases until mid-2026 and instead recycle existing inventory reflects a strategic bet that prices will moderate, but this approach limits the company's ability to introduce new designs and respond to demand shifts. Silver prices are also climbing, with the World Bank forecasting USD 38 per ounce in 2025 and USD 41 in 2026, pressuring affordable luxury brands that rely on silver as a lower-cost alternative to gold. Gemstone prices exhibit similar volatility; Peru's illicit gold supply chains, documented in multiple reports, introduce provenance risks that can disrupt legitimate sourcing and inflate compliance costs for brands seeking conflict-free certification. The price surge in 2024 caused global gold jewelry consumption to fall 11% year-over-year to 1,877.1 tonnes, even as consumer spending rose 9% to USD 144 billion, a divergence that signals buyers are purchasing smaller, lighter pieces to stay within budget, according to the World Gold Council. This dynamic favors hollow designs, plated finishes, and mixed-material constructions, but it also risks alienating traditional buyers who equate jewelry value with gold weight and purity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Stackable Bracelets Drive Volume Growth

Rings commanded 35.84% of Latin America's jewelry market in 2025, anchored by bridal demand and cultural traditions that prioritize engagement and wedding bands, yet bracelets will expand at 6.93% annually through 2031, the fastest rate among product types. Tiffany's Lock bracelet, launched in August 2022 and rolled out across Latin America in 2024-2025, exemplifies the shift toward icon-driven, stackable designs that encourage repeat purchases; the limited-edition Brazilian-flag-inspired version sold out in São Paulo within days, demonstrating that scarcity and localization drive premiums. Pandora's charm bracelet platform, which allows consumers to add individual charms over time, converts jewelry from a one-time purchase into an ongoing relationship, a model that resonates in Latin America, where gifting culture and milestone celebrations sustain demand. Necklaces and chains with pendants together represent a significant share, driven by religious devotion and the popularity of layered looks among younger consumers; Vivara's Life brand offers silver necklaces with interchangeable pendants, targeting middle-income buyers who seek versatility.

Earrings remain a staple category, particularly in Brazil and Colombia, where piercing is nearly universal among women, but growth is constrained by saturation; most consumers already own multiple pairs, limiting incremental demand to fashion-driven replacements. Chains and pendants benefit from the trend toward personalization, with brands offering engraving services and customizable lengths that appeal to both men and women. Other product types, including brooches, cufflinks, and body jewelry, occupy niche segments but are experiencing renewed interest as fashion cycles revive vintage aesthetics and gender-neutral designs. The product mix is also shifting toward lighter, hollow constructions in response to gold price increases; consumers are prioritizing design and brand over gold weight, a behavioral change that favors skilled designers and penalizes commodity-focused producers. Regulatory frameworks such as Brazil's hallmarking requirements ensure that gold purity claims are verifiable, reducing fraud risk but adding compliance costs for smaller manufacturers.

By Material: Mixed Materials Challenge Precious Metals

Precious metals, gold, platinum, and silver, accounted for 63.72% of market value in 2025, but mixed materials will grow at 6.34% through 2031 as consumers seek affordable luxury and brands experiment with innovative alloys and finishes. The 23% surge in gold prices during 2024 accelerated the shift toward mixed-material designs that combine base metals with gold plating, synthetic gemstones, or enamel accents, enabling brands to maintain visual appeal while controlling costs. Vivara's Life brand, which focuses on silver jewelry with gemstone embellishments, posted strong sales growth in 2025, demonstrating that middle-income consumers will trade down in material composition if design and brand remain compelling. Pandora's lab-grown diamond collections, launched in Mexico and Brazil in late 2023, pair lab-created stones with sterling silver or gold-plated settings, offering the look of fine jewelry at a fraction of the price.

Base metals, primarily brass, copper, and stainless steel, are gaining traction in fashion jewelry, particularly among younger consumers who prioritize trend responsiveness over longevity. Brands such as Tous and Swarovski use proprietary alloys and surface treatments to mimic the appearance of precious metals while achieving price points accessible to mass-market buyers. Mixed materials also enable experimentation with color and texture; enamel, resin, and ceramic inserts allow designers to create bold, contemporary pieces that differentiate from traditional gold and diamond jewelry. The regulatory environment is tightening; Brazil's legislation banning the import and production of jewelry containing lead and nickel, enacted in the mid-2010s and enforced more rigorously since 2024, has forced costume jewelry manufacturers to reformulate alloys, increasing production costs but improving consumer safety. Precious metals retain their dominance in bridal and heirloom categories, where consumers view jewelry as an investment and store of value, but the erosion of market share to mixed materials signals a structural shift toward fashion-driven consumption and away from commodity-based valuation.

By Category: Costume Jewelry Narrows the Gap

Fine jewelry accounted for 81.38% of market value in 2025, reflecting Latin America's cultural preference for gold and gemstone pieces that serve as both adornment and wealth storage. Yet costume and fashion jewelry will grow at 6.28% annually through 2031, narrowing the gap as e-commerce and fast fashion reshape buying behavior. Brazil's e-commerce boom, projected to grow from USD 52.87 billion in 2024 to USD 125.68 billion by 2029 at an 18.91% compound rate, has lowered distribution costs for costume jewelry brands, enabling them to reach consumers in secondary cities and rural areas previously dominated by local jewelers U.S. International Trade Administration. Chinese platforms Shein and Temu, which entered Brazil in 2024, offer jewelry at price points 50-70% below domestic brands, compressing margins across the costume segment and forcing established players to compete on speed and design rather than price. Vivara's strategic pause on new gold purchases until mid-2026, coupled with its expansion of the silver-focused Life brand, illustrates how even fine jewelry specialists are hedging against raw material inflation by diversifying into lower-cost categories.

Fine jewelry's enduring dominance is rooted in Latin America's gifting culture and the role of jewelry in life-cycle events; engagement rings, wedding bands, and quinceañera sets are almost exclusively fine jewelry, creating a demand floor that insulates the category from economic downturns. Costume jewelry, by contrast, is driven by fashion cycles and impulse purchases; the average transaction value is lower, but purchase frequency is higher, creating opportunities for brands that can iterate designs quickly and leverage social media for discovery. The category boundary is blurring as demi-fine jewelry, pieces that combine precious metals with lower-cost materials, emerges as a hybrid segment; Pandora's lab-grown diamond collections and Tous's silver-and-gemstone lines straddle the fine/costume divide, appealing to consumers who want brand prestige without fine jewelry price tags. Regulatory oversight is lighter for costume jewelry, reducing compliance costs but also increasing counterfeiting risk, a trade-off that brands must manage through authentication technologies and consumer education.

By End User: Men's Jewelry Surges

Women accounted for 73.65% of jewelry purchases in 2025, a share that reflects both cultural norms and product availability, but men's jewelry will grow at 7.53% annually through 2031, the fastest rate across all end-user segments, driven by changing attitudes toward male self-expression and the introduction of unisex designs. Tiffany's Lock collection, launched in August 2022 with eight unisex bangles featuring an innovative clasp, was described as "off to a solid start" in North America and has since expanded to Latin America, where younger male consumers in Brazil and Mexico are adopting minimalist jewelry as a form of personal branding. Pandora's charm bracelets, traditionally marketed to women, are being repositioned as gender-neutral through campaigns featuring male influencers and athletes, a strategy that resonates in Latin America's football-obsessed culture. Montblanc reported that Brazil and Mexico are performing on par with, or even above, the United States in high-value watch categories, signaling that male consumers in the region are willing to invest in luxury accessories.

Children's jewelry represents a smaller but stable segment, driven by baptism, first communion, and birthday gifting traditions; gold bracelets and necklaces are common gifts for newborns in Brazil and Colombia, creating early brand loyalty that can extend into adulthood. Women's jewelry remains the core category, with rings, earrings, and necklaces dominating sales, but the segment is maturing; growth is increasingly dependent on trade-up behavior, consumers replacing costume jewelry with fine pieces or upgrading to branded luxury, rather than new customer acquisition. The rise of men's jewelry is also visible in product innovation; brands are introducing larger, bolder designs that appeal to male aesthetics, such as chunky chains, signet rings, and leather-and-metal bracelets. Cultural shifts are accelerating adoption; social media platforms, particularly Instagram and TikTok, showcase male celebrities and influencers wearing jewelry, normalizing the category and reducing the stigma that historically limited male participation. The end-user segmentation is further complicated by gifting dynamics; a significant share of women's jewelry is purchased by men (and vice versa), meaning that marketing must address both the buyer and the wearer, a dual-audience challenge that requires nuanced messaging and channel strategies.

By Distribution Channel: Offline Dominance Erodes Slowly

Offline retail stores captured 85.56% of jewelry sales in 2025, reflecting consumer preference for tactile evaluation, immediate gratification, and the perceived security of purchasing high-value items in physical locations, yet online retail will grow at 5.82% annually through 2031 as brands invest in e-commerce infrastructure and younger consumers embrace digital channels. Vivara's integration with Mercado Libre and TikTok in 2025 represents a strategic pivot toward digital-first distribution; the company aims to capture consumers who discover products on social media and complete purchases on e-commerce platforms without visiting a store. Pandora's decision to re-route Latin American supply chains to serve the region directly, bypassing U.S. distribution hubs, reduces delivery times and tariff exposure, making online fulfillment more competitive with offline retail. Brazil's e-commerce market will grow from USD 52.87 billion in 2024 to USD 125.68 billion by 2029, with jewelry benefiting from improved payment infrastructure, including installment plans and digital wallets that lower the barrier to high-ticket purchases, according to the U.S. International Trade Administration.

Offline retail's enduring dominance is rooted in the experiential nature of jewelry shopping; consumers want to see how pieces look on their skin, assess weight and craftsmanship, and receive personalized service from sales associates. Tiffany's São Paulo flagship, which opened in January 2025 with a dedicated high jewelry salon and private consultation rooms, exemplifies the shift toward experiential retail that justifies physical stores even as e-commerce grows. Mall-based stores benefit from foot traffic and co-location with complementary luxury brands, creating a halo effect that elevates the entire category. Security concerns also favor offline retail; consumers in Latin America are wary of online fraud and prefer the legal recourse and brand accountability that come with in-store purchases. Online channels are gaining share in costume and fashion jewelry, where lower price points reduce purchase risk and design variety encourages browsing and impulse buying. The distribution landscape is also being reshaped by social commerce; TikTok and Instagram enable brands to sell directly through video content, collapsing the discovery-to-purchase funnel and reducing reliance on traditional retail intermediaries.

Geography Analysis

Brazil commands 44.53% of Latin America's jewelry market in 2025, anchored by a luxury sector that expanded 11.7% in 2024 and is forecast to grow 15% in 2025, with jewelry and watches posting a 15% compound annual growth rate over the past 2 years, according to MCF Consultoria and Abrael. The country's approximately 1.3 million high-net-worth individuals, projected to reach 1.5 million by 2030, provide a stable base of affluent consumers who prioritize branded luxury and are relatively insulated from macroeconomic volatility. Vivara's third-quarter 2025 profit surged 33% to R$175.8 million (approximately USD 32 million), driven by record margins and the expansion of its Life brand, which targets middle-income buyers with silver jewelry positioned as "democratic luxury". Tiffany's January 2025 opening of a 408-square-meter flagship at Iguatemi São Paulo, featuring works by Brazilian artists João Carlos Galvão and Humberto Campana, signals that global jewelers view Brazil as a long-term growth market despite currency volatility that forces local prices 20-25% above U.S. and European levels. Brazil's cumulative import taxation regime, which can inflate landed costs by approximately 69% through layered duties (Import Duty, IPI, PIS/COFINS, ICMS), favors domestic producers such as Vivara and HStern, who avoid import tariffs and benefit from local sourcing of gold and gemstones.

Argentina will grow at 6.65% annually through 2031, the fastest rate among major geographies, a paradox explained by tariff reductions from 35% to 12.6% on capital goods, fiscal consolidation that stabilized foreign-exchange reserves at USD 41.7 billion by October 2025, and a mining discovery in San Juan province with potential reserves of 32 million ounces of gold and 659 million ounces of silver, according to the Global Trade Alert. The country's economic volatility has historically driven demand for jewelry as a store of value; gold and silver pieces function as portable, divisible wealth that hedges against currency devaluation, a dynamic that sustains demand even when discretionary spending collapses. Argentina's jewelry market is also benefiting from the normalization of trade relations with the United States and the European Union, which has reduced tariff uncertainty and encouraged international brands to re-enter the market after years of retreat. Colombia, Chile, and Peru collectively represent a significant share of regional demand, with Colombia's visitor exports totaling COP 42.1 billion in 2024, a figure that includes substantial jewelry purchases by international tourists drawn to Bogotá's emerald district, according to the World Travel and Tourism Council[4]Source: World Travel & Tourism Council, “Economic Impact Reports,” wttc.org. Peru's GDP growth of 3.1% in 2024, driven by high gold and copper prices, has boosted disposable incomes in urban centers, yet political uncertainty ahead of 2026 elections is dampening consumer confidence and deferring high-ticket purchases.

Rest of South America, including Uruguay, Paraguay, Bolivia, Ecuador, and the Guianas, accounts for a smaller share of regional demand but exhibits pockets of opportunity in border trade and tourism-driven sales. Uruguay's status as a regional financial hub attracts affluent consumers from Argentina and Brazil who purchase jewelry to circumvent capital controls and currency restrictions in their home countries. Paraguay's Ciudad del Este, a major cross-border retail zone, generates significant jewelry sales to Brazilian and Argentine visitors seeking lower prices and tax-free shopping. The geographic segmentation is further complicated by intra-regional migration; Venezuelan and Colombian migrants in Ecuador, Peru, and Chile represent a growing consumer base with distinct preferences and purchasing power. Regulatory harmonization under Mercosur has reduced some trade barriers, but divergent tax regimes and customs procedures continue to fragment the market, limiting the ability of regional brands to achieve scale economies. The geography analysis underscores that Brazil's dominance is structural, rooted in population size, wealth concentration, and domestic production capacity, while Argentina's rapid growth reflects a low base and policy normalization rather than a fundamental shift in competitive dynamics.

Regulatory Landscape

Regulation across Latin America continues to tighten around traceability, product integrity, and trade compliance, with Brazil and Mexico acting as key reference points for regional operators. In Brazil, the National Mining Agency (ANM) issued Resolution No. 232/2026 on March 27, 2026, requiring Kimberley Process Certificate (KPC) procedures for rough diamonds to be integrated into the federal Siscomex environment. This strengthens customs-level traceability and increases scrutiny around import and export declarations.

Mexico also reinforces compliance expectations for precious metal and jewelry trade through anti-money laundering controls under LFPIORPI, with 2026 thresholds referenced at 805 UMAs for customer identification and 1,605 UMAs for reporting. Trade rules further affect sourcing economics, as a Presidential Decree published April 23, 2026 updated import tariffs across 185 tariff lines (5% to 35%). Importers and brand owners will need to monitor how tariff classifications affect costs for finished jewelry, components, and other luxury goods moving into the country.

Competitive Landscape

The Latin America jewelry market exhibits moderate concentration, indicating that the top 5 players, Vivara, HStern, Pandora, Richemont, and LVMH, hold significant but not dominant positions, leaving ample room for regional specialists and digital-first disruptors to capture share. Vivara's third-quarter 2025 profit increase of 33% to R$175.8 million, driven by its Life brand expansion and strategic pause on new gold purchases until mid-2026, exemplifies a margin-over-volume strategy that prioritizes profitability and inventory efficiency over aggressive store rollouts. Pandora's opening of 70 stores in Brazil over 18 months and its re-routing of Latin American supply chains to bypass U.S. hubs demonstrate a localization strategy that reduces tariff exposure and delivery times, enabling the brand to compete on price and speed with domestic players.

LVMH's Tiffany brand has invested heavily in flagship retail, opening a 408-square-meter store in São Paulo in January 2025 and an 878-square-meter flagship in Mexico City in February 2025, complete with the first Blue Box Café in Latin America, signaling a long-term commitment to experiential retail that justifies premium pricing. White-space opportunities exist in affordable luxury and men's jewelry, segments where incumbents have limited presence and where digital-native brands can leverage social commerce to acquire customers at lower cost than traditional retail. Emerging disruptors include Chinese e-commerce platforms, Shein, Temu, Aliexpress, which entered Brazil and Chile in 2024 and offer jewelry at price points 50-70% below domestic brands, compressing margins and forcing established players to compete on design differentiation and brand authenticity rather than price.

Technology adoption is accelerating; Vivara's integration with Mercado Libre and TikTok in 2025, and Pandora's use of digital configurators for charm bracelets, illustrate how brands are collapsing the discovery-to-purchase funnel and reducing reliance on physical retail. Blockchain-based authentication systems are being piloted to combat counterfeiting, a critical issue given that INTERPOL's Operation Crete II seized 2,478 counterfeit jewelry items worth USD 523,000 in Chile alone in 2024. Strategy patterns reveal a bifurcation: global luxury houses (Tiffany, Cartier, Bulgari) are investing in flagship stores and high-touch service to justify premium pricing, while mass-market brands (Pandora, Tous) are scaling franchise networks and e-commerce to achieve volume. Regional players such as Vivara and HStern occupy a middle ground, leveraging local sourcing and cultural insights to compete on authenticity and value, a positioning that becomes more defensible as import tariffs and currency volatility penalize international competitors.

Latin America Jewelry Industry Leaders

Vivara Participações S.A.

HStern Indústria e Comércio SA

Pandora A/S

Compagnie Financière Richemont SA

LVMH Moët Hennessy Louis Vuitton SE

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Industrialization of personalization, and shorter design-to-shelf cycles, stands out as a near-term opportunity for brands targeting Brazil, Mexico, and Chile. As consumers shift from mass-market designs toward customized pieces and branded narratives, investments in CAD/CAM, additive manufacturing (3D printing), and laser welding can support small-batch complexity and faster refresh rates. Virtual try-on tools also provide differentiation for online jewelry where tactile evaluation remains a buying friction. Vivara scaling its Life concept in Brazil, alongside global brands investing in experiential flagships in Sao Paulo and Mexico City, underlines how personalization paired with high-service retail can strengthen conversion.

Transparency and authentication present another area for differentiation, particularly as counterfeit exposure and provenance expectations rise alongside compliance focus. Brazil has moved to digitize and tighten rough diamond traceability through ANM Resolution No. 232/2026 and Siscomex integration, while brands are piloting blockchain-style digital certificates for high-value pieces to back authenticity claims. Execution also appears to offer room for platform-led and social commerce in the region, with Vivara integrating with Mercado Libre and TikTok in 2025. Adjustments to fulfillment and pricing models to serve Latin America more directly (as referenced in Pandora disclosures) can support shorter lead times and clearer regional pricing, which becomes more relevant as import duties and tariff changes add friction to cross-border sourcing.

Recent Industry Developments

- May 2026: Vivara Participacoes S.A. executed a Third Amendment to its Shareholders Agreement on May 28, 2026. The update reinforces governance and shareholder alignment while the company continues to balance profitability, inventory discipline, and the expansion of its Life brand footprint in Brazil.

- January 2026: Pandora rolled out a new go-to-market pricing model across Latin America, as communicated in its 2026 investor materials. The shift standardizes regional pricing execution and supports store network performance, strengthening competitiveness versus local players and cross-border online sellers.

- December 2024: Tiffany and Co. opened a flagship at Iguatemi Sao Paulo, bringing a high jewelry salon and brand-led experiential zones into one of Brazil's most important luxury retail destinations. The investment deepened local engagement for high-ticket categories and raised the bar for experiential offline jewelry retail in the region.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the retail value of jewelry sold across Latin America, including fine and costume pieces made from precious metals, base metals, and mixed materials. The sizing reflects what end users purchase through offline and online channels, converted and reported in USD.

Scope exclusions: services such as jewelry repair, resizing, cleaning, and appraisal fees are excluded from the market value.

Segmentation Overview

- By Product Type

- Necklaces

- Rings

- Earrings

- Bracelets

- Chains and Pendants

- Other Product Types

- By Material

- Precious Metals

- Base Metals

- Mixed Materials

- By Category

- Fine Jewelry

- Costume/Fashion Jewelry

- By End User

- Women

- Men

- Children

- By Distribution Channel

- Offline Retail Stores

- Online Retail Stores

- By Geography

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to build the starting structure for the model, and then to sanity check the output against reliable public signals. We mainly refer to non-paywalled sources such as national statistics offices for CPI and retail trade trends, central banks for FX and macro indicators, UN Comtrade for jewelry and precious metal trade flows, and customs and tax authority publications where they disclose import duties and category notes.

Alongside this, we review company annual reports, investor presentations, store expansion announcements, and reputable press coverage to understand channel shifts and the likely pricing direction. For fact checks that are hard to observe in open sources, we also use paid subscriptions for company financials and intelligence, plus shipment-level import and export databases to see how trade mixes move over time. These desk sources are illustrative and not exhaustive, and many other public documents were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test assumptions that desk sources do not fully explain, especially around category splits, channel margins, and how consumers trade up or down under different income conditions. We interview manufacturers, wholesalers, retailers, and material-focused experts across key Latin American markets, then align views on volumes, pricing, and promotional intensity before the model is finalized.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 12% | |

| Mid tier: 52% | Functional/Unit leaders: 34% | |

| Smaller Players: 20% | Managers: 54% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand pool build that links jewelry spending to country-level consumer and retail signals, and then rolls it up to the Latin America total. When the model is being built, we use practical inputs such as real retail sales growth, inflation and FX movements, import trends for jewelry categories, online share shifts, and observed pricing changes for key materials and finished goods.

To keep the totals realistic, the output is cross-checked with selective bottom-up approximations, such as sampled average selling price bands multiplied by estimated unit volumes for major product groups, followed by channel checks on typical markups. Where direct volume hints are missing in smaller countries, we fill gaps using proxy indicators like urban population, income distribution changes, and category penetration ranges shared by interviewees. We then test sensitivity so no single assumption overdrives the result.

For forecasting, scenario analysis is used because the region can swing with currency moves and inflation. Growth paths are set using base case macro expectations, then adjusted using what primary respondents expect for store expansion, e-commerce adoption, and consumer preference changes, including the pace of fine versus costume purchases.

Data Validation & Update Cycle

Validation is done through repeated triangulation across independent signals so the final number is not dependent on one data line. We run variance checks by country, channel, and broad category, then look for outliers that conflict with trade direction, retail growth, or price movement logic.

Before sign-off, the model and assumptions are reviewed in more than one analyst pass, and any material mismatch triggers a re-check of the source notes, and when needed, a re-contact with relevant experts. The report is refreshed each year, and we also make interim updates if a major event changes demand patterns, regulations, or pricing. Right before delivery, a final review pass is completed so clients receive the latest updated view.

Mordor Intelligence's Latin America Jewelry Market Size Versus Other Published Estimates

Published market sizes for Latin America jewelry do not always match because researchers can use different definitions, pricing assumptions, and year selection, and the gaps get wider when currency conversion choices are not aligned. Differences also show up when one study mixes retail value with trade value, or when informal and unbranded sales are treated differently.

Repair, cleaning, and appraisal services sit outside Mordor Intelligence's scope, and that alone can pull totals away from estimates that treat the broader jewelry services ecosystem as part of the same spending pool. Another common driver is geography and channel handling, where some estimates use a narrow country set, apply a single FX rate across the year, or project faster price escalation for precious materials without cross-checking the implied unit demand against retail traffic and import trends.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 33.20 B (2025) | |

| Global Consultancy A | USD 8.58 B (2024) | Uses a different base year and a much smaller value that likely reflects a narrower country basket or a tighter product definition. The published snapshot does not clearly explain whether the figure is retail value, trade value, or manufacturer level revenue, which can materially change the total. |

| Industry Publisher B | USD 9.13 B (2025) | Appears to follow a category structure that can undercount broad costume jewelry and mixed-material pieces if the focus is weighted toward fine jewelry materials and branded reporting. Country coverage and FX timing are not fully transparent in the public summary, so regional roll-ups can end up conservative. |

Looking across the three figures, the spread is mainly explained by what gets counted as jewelry spend, how wide the country and channel coverage is, and whether pricing is treated as a simple uplift or tied back to demand signals. Our checks on retail direction, trade movement, and interview-led pricing bands help keep the final value traceable to clear inputs that can be repeated and reviewed.

Key Questions Answered in the Report

How large will the Latin America jewelry market be by 2031?

It is forecast to reach USD 46.10 billion, expanding at a 5.48% CAGR from 2026 through 2031.

Which product category is growing fastest in the region?

Bracelets are projected to post the quickest 6.93% CAGR, outpacing rings, earrings, and necklaces.

Why is men’s jewelry gaining momentum?

Unisex designs, social-media influence, and changing attitudes toward male self-expression are lifting men’s jewelry at a 7.53% CAGR.

How are high gold prices affecting consumer choices?

Elevated bullion costs are steering buyers toward mixed-material and lab-grown stone pieces that deliver luxury aesthetics at lower price points.

What role does e-commerce play in future sales?

Online channels, fueled by platforms like Mercado Libre and TikTok, are projected to nearly double their share to about 20% of total regional sales by 2031.

Page last updated on: