Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

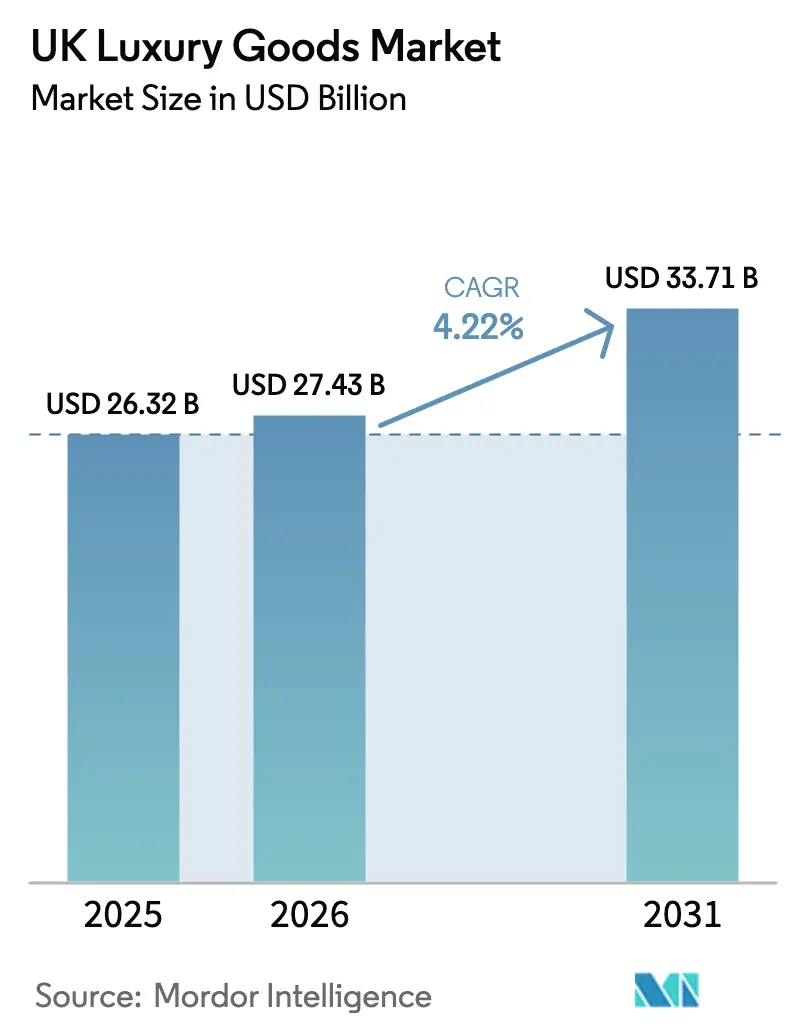

| Base Year Market Size (2025) | USD 26.32 Billion |

| Market Size (2026) | USD 27.43 Billion |

| Market Size (2031) | USD 33.71 Billion |

| Growth Rate (2026 - 2031) | 4.22% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

UK Luxury Goods Market Analysis by Mordor Intelligence

UK luxury goods market size in 2026 is estimated at USD 27.43 billion, growing from 2025 value of USD 26.32 billion with 2031 projections showing USD 33.71 billion, growing at 4.22% CAGR over 2026-2031. The UK luxury fashion market is evolving through innovation in materials and design, with sustainability and ethical sourcing becoming central priorities. This evolution is further reinforced by social media and celebrity influence, which continue to shape consumer perceptions and amplify brand visibility through curated digital storytelling. Clothing and apparel, central to luxury identity and seasonal trends, continue to dominate. Women continue to anchor the luxury segment, but men are emerging as a fast-growing demographic, driven by rising interest in high-end streetwear, grooming, and premium accessories. This shift presents brands with opportunities to diversify their offerings and refine their marketing strategies. Distribution strategies are evolving as well. Single-brand boutiques remain vital for reinforcing brand identity and offering curated in-store experiences that deepen customer loyalty.

Key Report Takeaways

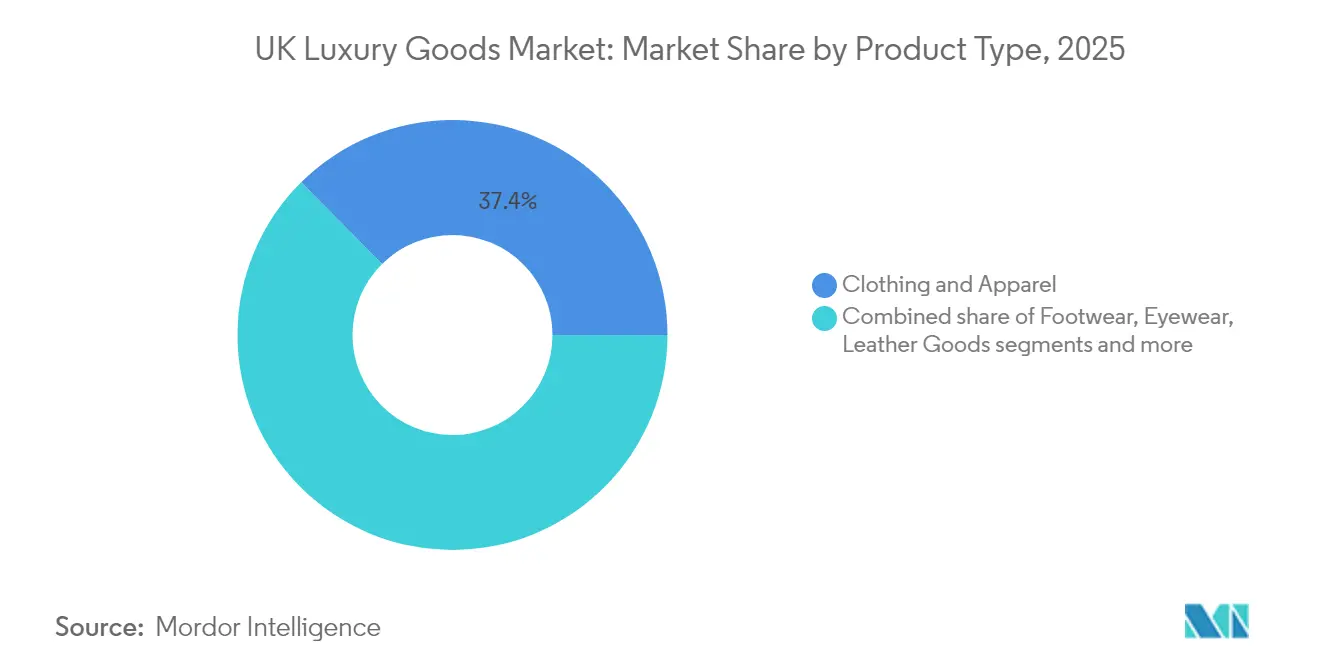

- By product type, clothing and apparel held the largest market share in 2025 at 37.43%, while leather goods are projected to be the fastest-growing segment from 2026 to 2031 at a CAGR of 4.56%.

- By end user, women dominated the market with 54.35% of the share in 2025, although the men’s segment is expected to grow faster at a CAGR of 4.92%.

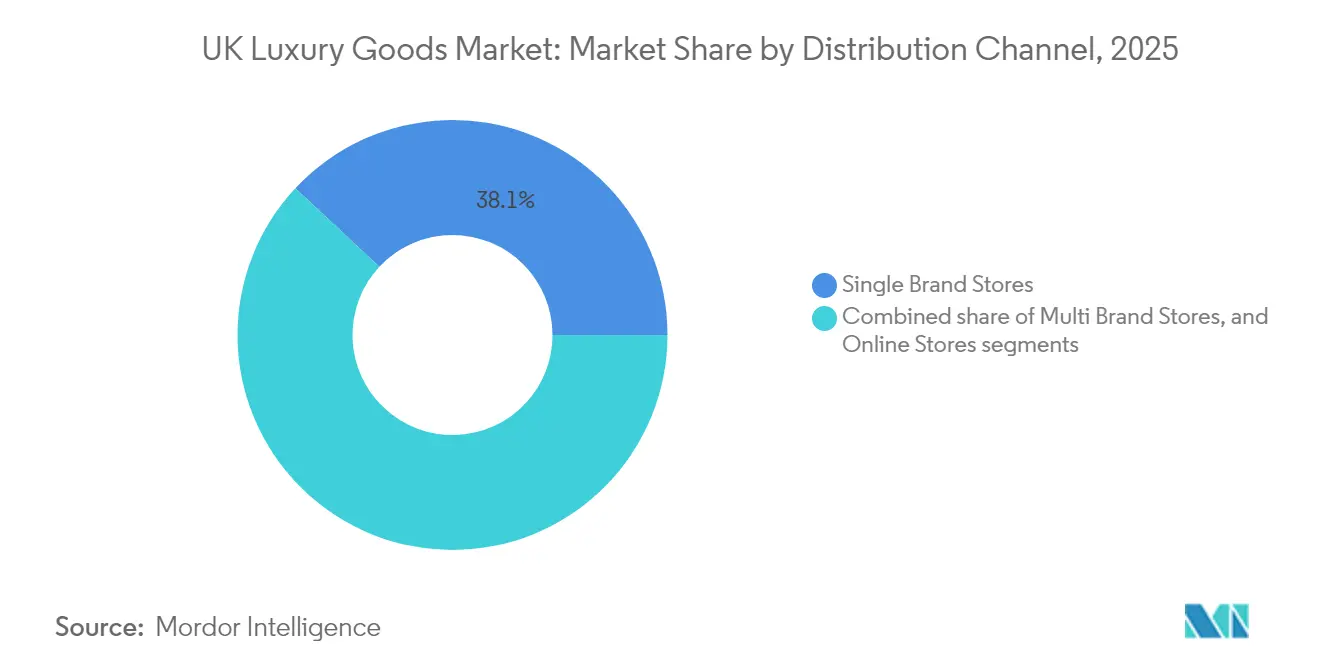

- By distribution channel, single brand stores led with 38.05% share in 2025; however, online stores are forecasted to grow the fastest at 5.32% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UK Luxury Goods Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Product innovation in terms of raw material and design | +1.2% | United Kingdom, with influence across European luxury markets | Medium term (2-4 years) |

| Influence of social media and celebrity endorsement | +0.9% | United Kingdom-wide, with concentration in urban centers | Short term (≤ 2 years) |

| Increasing strategic investment and initiatives propelling the market | +0.8% | United Kingdom-wide, with focus on London and other major cities | Medium term (2-4 years) |

| Consumer emphasis on sustainability | +0.6% | United Kingdom-wide, with stronger impact in affluent urban areas | Long term (≥ 4 years) |

| Digital transformation and e-commerce adoption enhance accessibility for affluent consumers. | +0.5% | United Kingdom-wide, with stronger penetration in metropolitan areas | Short term (≤ 2 years) |

| Technology integration in luxury retail improves shopping experiences. | +0.4% | United Kingdom-wide, with concentration in flagship stores and premium locations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Product innovation in terms of raw material and design

In the UK, luxury brands are merging time-honored craftsmanship with a commitment to sustainability, reshaping the landscape of high-end goods. Brands are adopting innovative materials that balance design excellence with environmental responsibility. A notable instance is Uncaged Innovations, which unveiled 'Elevate' in November 2024. This bio-based leather alternative boasts a remarkable 95% reduction in greenhouse gas emissions, 93% less water consumption, and 72% lower energy use compared to its traditional counterpart. Furthermore, Uncaged’s collaboration with ten independent fashion labels, including the UK-based Stow, reflects a growing shift in the industry. Sustainability-led innovation is no longer confined to major luxury houses. Independent, design-driven labels are also finding creative ways to merge aesthetics with accountability. As the EU gears up to enforce its Ecodesign for Sustainable Products Regulation, mandating Digital Product Passports for textiles by mid-2027, UK luxury houses are taking proactive steps [1]Source: CBI Ministry of Foreign Affairs, "The European market potential for leather bags,"cbi.eu . Many of these efforts also reflect strategic foresight, ensuring continued access to European markets post-Brexit.

Influence of social media and celebrity endorsement

In the UK luxury market, brand perception and purchase intent are increasingly swayed by celebrity endorsements, especially among the digitally-savvy younger audience. Short-form celebrity-led content on platforms such as Instagram and TikTok now plays a pivotal role in shaping brand image and influencing purchase intent. A 2024 University of Portsmouth survey indicated that 60% of consumers trusted influencer recommendations, while nearly half of all purchasing decisions were influenced by these endorsements [2]Source: University of Portsmouth, “New research unveils the ‘dark side’ of social media influencers and their impact on marketing and consumer behaviour,”port.ac.uk . Campaigns like Burberry's "Art of the Trench" underscore the potency of digital engagement in bolstering brand equity and nurturing customer loyalty. These campaigns highlight the growing importance of social media integration in luxury marketing, translating digital engagement into measurable business outcomes.

Increasing strategic investment and initiatives propelling the market

Luxury brands in the UK are embedding sustainability into their core operations, transitioning from marketing-driven claims to measurable action. The UK's fashion industry is a significant contributor and is increasingly turning to circular economy models. These include garment recycling, resale platforms, and the use of regenerative materials, all aimed at minimizing environmental impact. British luxury brand Stella McCartney stands out, leading the charge with innovations like bio-based textiles and collaborations with entities such as the Ellen MacArthur Foundation. Meanwhile, a new wave of affluent, digitally savvy luxury buyers is emerging in the UK. These "new luxury consumers" are younger, prioritize authenticity and craftsmanship, and seek brands that resonate with their values. For these consumers, luxury extends beyond status, it represents individuality, craftsmanship, and purpose. Millennials, in particular, are championing this movement, gravitating towards brands with genuine commitments to environmental and social causes.

Consumer emphasis on sustainability

Sustainability has evolved from a marketing theme into a fundamental business strategy across the UK luxury segment. Brands now weave environmental considerations into their design, sourcing, and production processes. Consumers are responding: affluent UK households increasingly seek luxury goods that resonate with ethical and environmental values. This emerging generation of luxury consumers is younger, digitally connected, and values authenticity, craftsmanship, and social responsibility over traditional notions of prestige. Millennials, in particular, are at the forefront of this shift, showcasing heightened eco-awareness and a preference for brands that mirror their values. For example, Stella McCartney redefined sustainable luxury with innovations like mushroom-based leather (Mylo™) and a commitment to cruelty-free collections. Meanwhile, Burberry aims for net-zero emissions across its supply chain by 2040 and has already phased out plastic packaging

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availablity of counterfeit products | -0.7% | United Kingdom-wide, with concentration in urban centers and online channels | Medium term (2-4 years) |

| Lesser demand from price sensitive consumers | -0.5% | United Kingdom-wide, with stronger impact in regions with lower disposable income | Short term (≤ 2 years) |

| Brexit-related trade barriers increase operational costs and retail prices. | -0.4% | United Kingdom-wide, with particular impact on import-dependent luxury categories | Long term (≥ 4 years) |

| Labor shortages in specialized craftsmanship | -0.3% | United Kingdom-wide, with concentration in traditional manufacturing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Availablity of counterfeit products

Counterfeit products are posing a growing challenge to brand integrity and revenues in the UK. Improved imitation quality has made them harder to detect, heightening risks for both brands and consumers, posing a significant threat to the luxury market. Social media platforms further amplify the issue by providing a space for counterfeit promotion. According to research from the Intellectual Property Office, as of February 2024, 24% of male consumers, influenced by social media endorsements, are inclined to purchase counterfeit goods, compared to only 10% of female consumers [3] Source: Intellectual Property Office, "The impact of complicit social media influencers on counterfeit purchasing among male consumers in the UK," gov.uk. The study highlights four main reasons why people buy counterfeit products which includes influence from trusted figures like influencers, personal justifications for the purchase, lack of awareness about the risks involved, and a higher willingness to take risks. Younger males aged 16-33 are particularly vulnerable to these influences. Moreover, the widening income inequality has led some consumers to attribute an 'egalitarian value' to counterfeit goods.

Lesser demand from price sensitive consumers

In the UK, the luxury market is witnessing a significant transformation. Price-sensitive consumers, once pivotal to the growth of entry-level luxury, are now reevaluating their priorities. With inflation and economic uncertainties weighing heavily, these consumers are shifting their focus from status-driven purchases to value, durability, and practicality. Consequently, sales of accessible luxury items like affordable handbags, small leather goods, and beauty products have seen a downturn. These items, once favorites among aspirational buyers, are now facing reduced demand. This trend has created a market divide high-net-worth consumers continue to drive ultra-premium sales, while mid-tier segments face slower growth amid changing spending priorities. such as fine jewelry, watches, and bespoke fashion, the mid-tier luxury segments find it challenging to sustain their momentum

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Clothing and Apparel Dominates

In 2025, clothing and apparel took center stage in the UK's luxury goods market, seizing a dominant 37.43% share. This dominance reflects apparel’s central role in personal luxury, serving as both a symbol of status and a means of self-expression. British consumers are increasingly linking luxury apparel with top-notch quality and artisanal craftsmanship. Moreover, the sector is undergoing a digital metamorphosis, with e-commerce now commanding major segment in the market. Augmented reality and virtual try-on tools are enriching the digital shopping experience, driving engagement, and reshaping how consumers purchase luxury products.

Leather goods are carving out a significant niche in the UK luxury scene, with projections indicating a CAGR of 4.56% from 2026 to 2031. This growth trajectory is largely attributed to innovations in sustainable materials, especially bio-based leather alternatives. These alternatives boast a staggering reduction in greenhouse gas emissions, less water consumption, and decreased energy use compared to their conventional counterparts. Responding to this trend, traditional players are pivoting. Gruppo Mastrotto, for instance, launched its FW25/26 line themed “Leather Forward,” emphasizing sustainability, nature-centric design, and ethical principles.

By End User: Men's Segment Accelerates Growth Trajectory

In 2025, women dominated the UK's luxury goods market, holding a commanding 54.35% share. Their strong affinity for fashion, accessories, and beauty drives this trend. The market thrives on a diverse range of offerings tailored for women, from apparel and fine jewelry to handbags and cosmetics. Historically, these offerings have been central to luxury brand strategies, attracting hefty investments in product innovation and marketing. This shift is evident in the rising demand for timeless, high-quality items, especially in fine jewelry and leather goods, which promise both durability and investment potential.

On the other hand, the men's segment is swiftly becoming the growth engine of the UK's luxury market, with projections indicating a CAGR of 4.92% from 2026 to 2031. This growth is driven by evolving perceptions of masculinity and the increasing significance of fashion in male identity. For example, the European market has witnessed a surge in demand for men's leather bags, highlighting a diversification in male product categories. In response, luxury brands are broadening their menswear collections and tailoring campaigns to resonate with this changing demographic.

By Distribution Channel: Digital Acceleration Reshapes Retail Landscape

In 2025, single-brand stores command a dominant 38.05% share of the country's luxury market, solidifying their status as the favored distribution channel. These exclusive outlets empower brands with total control over customer interactions, merchandising, and narrative crafting. More than just product showcases, these physical venues immerse customers in the brand's identity, heritage, and values. Brands are intensifying their presence in iconic locales such as Bond Street and Regent Street. For instance, Perry Ellis Europe is set to debut five standalone stores for its menswear labels, Farah and Original Penguin, by 2025, eyeing prime spots in London and Manchester.

Online stores are emerging as the swiftest-growing channel for luxury distribution, with projections indicating a CAGR of 5.32% from 2026 to 2031. This rapid growth underscores a significant digital evolution in the luxury sector, driven by shifting consumer demands for convenience, accessibility, and tailored experiences. The ascent of luxury e-commerce is bolstered by tools like data analytics and artificial intelligence, crafting personalized shopping journeys. Major brands are amplifying their digital investments, aiming to refine customer experiences, optimize logistics, and diversify product lines.

Geography Analysis

London remains the center of the UK’s luxury goods market, supported by its high concentration of wealth, global visitors, and strong fashion heritage. The city attracts affluent shoppers with its mix of flagship stores, premium services, and well-known areas like Bond Street, Mayfair, and Knightsbridge. For most luxury brands, having a strong physical presence in London is still essential. Many are investing in more personalized experiences, such as private shopping, exclusive events, and creative brand showcases, to strengthen customer relationships and keep physical retail relevant alongside digital platforms.

Cities like Manchester, Birmingham, Edinburgh, and Glasgow are becoming key regional markets. Manchester’s redevelopment and growing professional base have drawn global names like Selfridges and Burberry. Birmingham’s Bullring & Grand Central and Mailbox areas are seeing more luxury retailers, catering to high-end consumers across the Midlands. In Scotland, Edinburgh’s heritage appeal and Glasgow’s vibrant shopping culture continue to attract both domestic and international shoppers.

These cities benefit from lower operating costs and a growing number of affluent and younger consumers who value modern, accessible luxury. E-commerce has also helped expand luxury shopping beyond London, giving consumers in cities such as Leeds and Bristol easier access to high-end products. These developments highlight how the UK’s luxury market is evolving into a more regionally balanced and digitally connected landscape.

Competitive Landscape

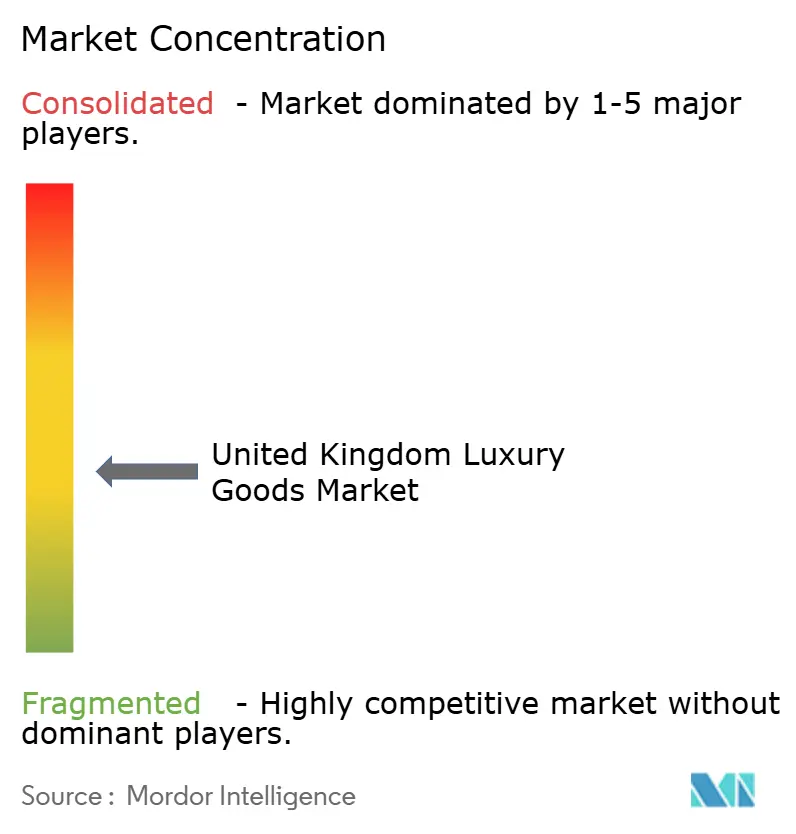

The UK luxury goods market is moderately fragmented, characterized by a diverse range of international and domestic players operating across key segments such as apparel, watches, jewelry, beauty, and accessories. Leading global brands, including LVMH (which encompasses Louis Vuitton and Dior), Kering (parent company of Gucci), and Richemont (owner of Cartier), dominate with strong brand recognition and significant market shares. This mix of international and domestic players, alongside the rising demand for bespoke and sustainable products, reflects the market’s diverse and competitive character.

Consumer behavior in the UK is undergoing a significant transformation, driven by a growing preference for digital channels and ethical consumption. Luxury brands are adapting by implementing robust omnichannel strategies that seamlessly integrate immersive in-store experiences with advanced digital platforms. Luxury brands are using these platforms to deliver greater personalization, virtual experiences, and on-demand customer service enhancing the overall buying journey. Furthermore, the demand for limited-edition collections, influencer-led marketing campaigns, and direct-to-consumer business models is gaining traction, particularly among Gen Z and millennial shoppers who value exclusivity, authenticity, and convenience.

Technology adoption is playing an increasingly pivotal role in shaping the competitive landscape of the luxury goods market. Innovations such as digital product passports are not only addressing regulatory compliance but also enhancing transparency and fostering deeper customer engagement. For example, the EU's Ecodesign for Sustainable Products Regulation, which will require Digital Product Passports for textile products by mid-2027, highlights the growing emphasis on sustainability and the role of technology in meeting these evolving consumer and regulatory demands. This shift is likely to shape strategic priorities for luxury brands over the next several years.

UK Luxury Goods Industry Leaders

-

LVMH Moet Hennessy Louis Vuitton

-

Compagnie Financière Richemont S.A.

-

Burberry Group plc

-

Kering SA

-

Chanel Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Von Baer launched a dedicated UK website, vonbaer.co.uk, offering premium full-grain vegetable-tanned Italian leather bags and accessories, including briefcases, wallets, backpacks, and travel bags. The brand emphasizes timeless European craftsmanship, sustainability through natural tanning processes, and luxury tailored for the UK market with local delivery and support.

- March 2025: Rolex, in partnership with Watches of Switzerland Group, opened its largest European flagship boutique at 34 Old Bond Street, London, spanning over 7,200 square feet across four floors in the heart of Mayfair.

- February 2025: At Watches & Wonders 2025, Rolex unveiled several exciting new models, most notably the entirely new Oyster Perpetual Land-Dweller series, its first new collection in 13 years, featuring a sleek, thinner case design inspired by vintage Oysterquartz models and powered by the innovative in-house Caliber 7135 with the patented Dynapulse escapement.

- December 2024: French leather goods brand Polène opened its first London store at 74-76 Regent Street, marking its entry into the UK market alongside existing boutiques in Paris, New York, Tokyo, and Seoul.

UK Luxury Goods Market Report Scope

Luxury goods refer to high-priced personal accessories that are often handcrafted with painstaking detail and discipline, featuring extraordinary craftsmanship, and are built with the highest quality materials.

The United Kingdom's luxury goods market is segmented by type, end user, and distribution channels. By type, the market is segmented into clothing and apparel, footwear, eyewear, leather goods, jewelry, watches, and beauty and personal care. By end user, the market is segmented into men, women, and unisex. By distribution channel, the market is divided into single-brand stores, multi-brand stores, online stores, and other distribution channels. The report offers market size and forecasts in value terms (USD million) for all the above segments.

By Product Type

| Clothing and Apparel |

| Footwear |

| Eyewear |

| Leather Goods |

| Jewelry |

| Watches |

| Beauty and Personal Care |

By End User

| Men |

| Women |

| Unisex |

By Distribution Channel

| Single Brand Stores |

| Multi Brand Stores |

| Online Stores |

| By Product Type | Clothing and Apparel |

| Footwear | |

| Eyewear | |

| Leather Goods | |

| Jewelry | |

| Watches | |

| Beauty and Personal Care | |

| By End User | Men |

| Women | |

| Unisex | |

| By Distribution Channel | Single Brand Stores |

| Multi Brand Stores | |

| Online Stores |

Key Questions Answered in the Report

What is the current size of the UK luxury goods market?

The market stands at USD 27.43 billion in 2026 and is projected to reach USD 33.71 billion by 2031.

Which product type leads sales in the UK luxury goods market?

Clothing and apparel leads with a 37.43% share, followed by rapidly expanding leather goods.

How fast is the online channel growing for luxury goods in the UK?

Online stores are forecast to post a 5.32% CAGR between 2026 and 2031, the fastest among all retail formats.

Which end-user segment is projected to grow fastest?

The men’s segment is expected to expand at a 4.92% CAGR through 2031, driven by younger male shoppers embracing premium fashion and accessories.

Page last updated on: