Gems And Jewelry Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 394.74 Billion |

| Market Size (2031) | USD 493.68 Billion |

| Growth Rate (2026 - 2031) | 4.58% CAGR |

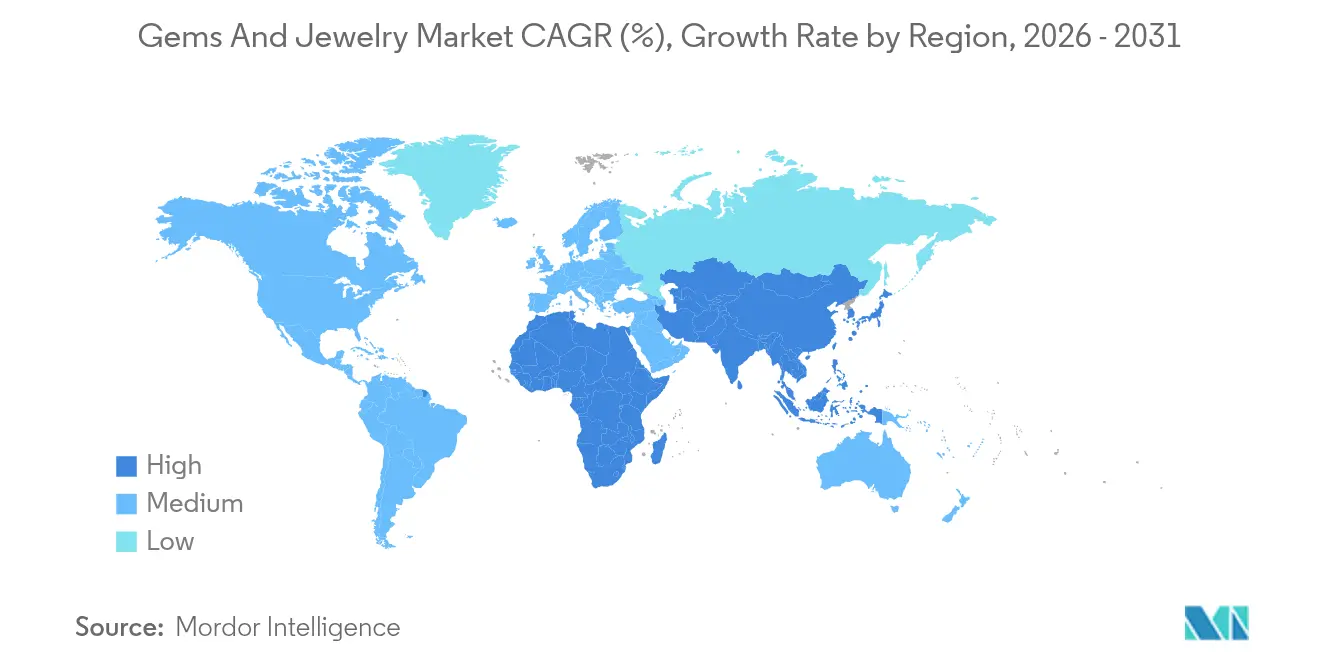

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

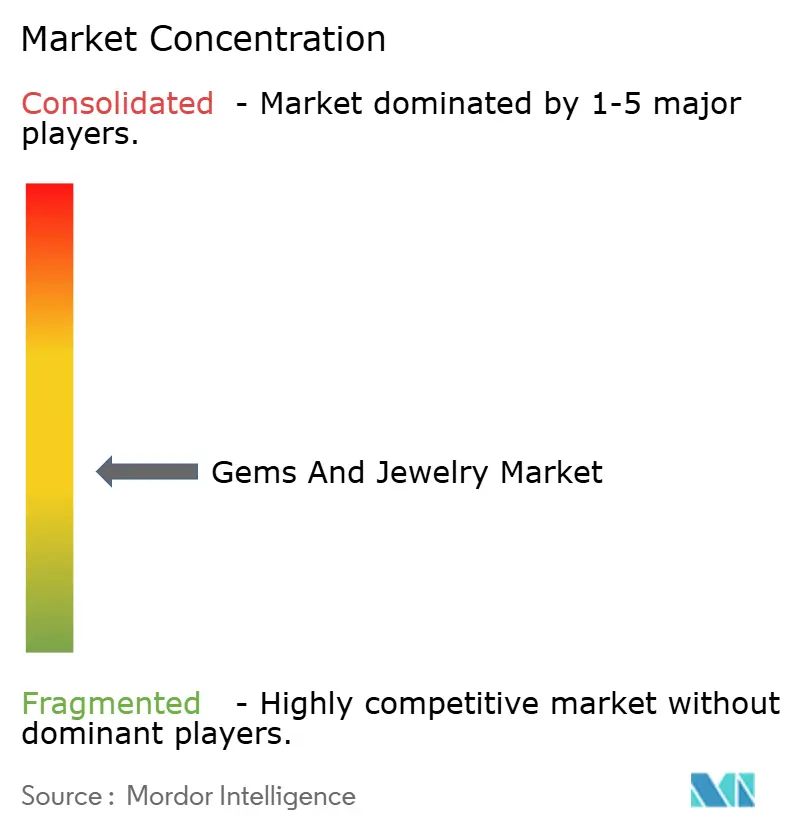

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gems And Jewelry Market Analysis by Mordor Intelligence

The gems and jewelry market size was valued at USD 377.45 billion in 2025 and estimated to grow from USD 394.74 billion in 2026 to reach USD 493.68 billion by 2031, at a CAGR of 4.58% during the forecast period (2026-2031). The increasing adoption of lab-grown diamonds, the rapid shift toward digital retail platforms, and changing consumer demographics are driving market growth. These factors are broadening the customer base, while sustainability concerns are prompting significant changes in supply chains. Regional demand patterns vary significantly. The Asia-Pacific region continues to dominate in terms of revenue, while the Middle East and Africa are witnessing the fastest growth in sales volume due to a combination of cultural preferences and rising wealth. Consumer preferences are also shifting, with a growing interest in jewelry for everyday fashion rather than just traditional bridal categories. The men’s jewelry segment is emerging as a key area of demand. In terms of competition, the market is moderately competitive, with companies focusing on technology investments, ethical sourcing practices, and creating engaging omnichannel experiences to differentiate themselves and attract customers.

Key Report Takeaways

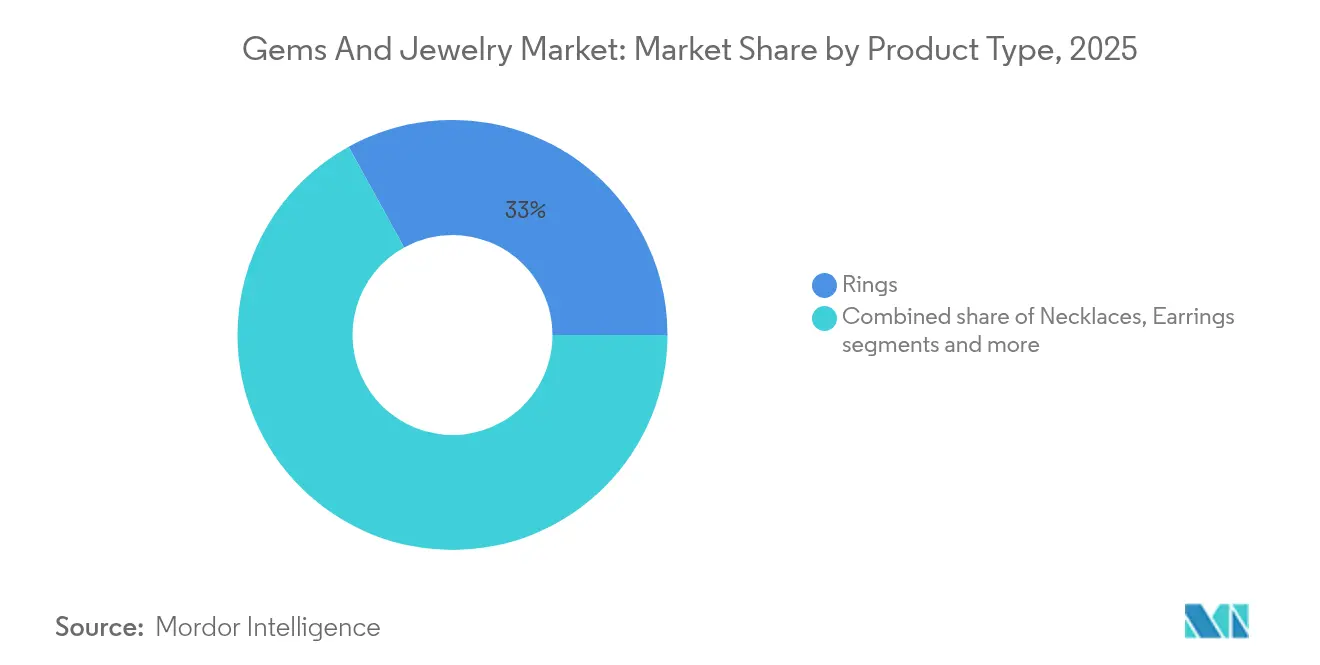

- By product type, rings held 33.02% revenue share in 2025; necklaces are forecast to advance at a 6.19% CAGR through 2031.

- By material type, precious metals dominated with a 62.10% share in 2025, while base metals are projected to grow at a 6.85% CAGR to 2031.

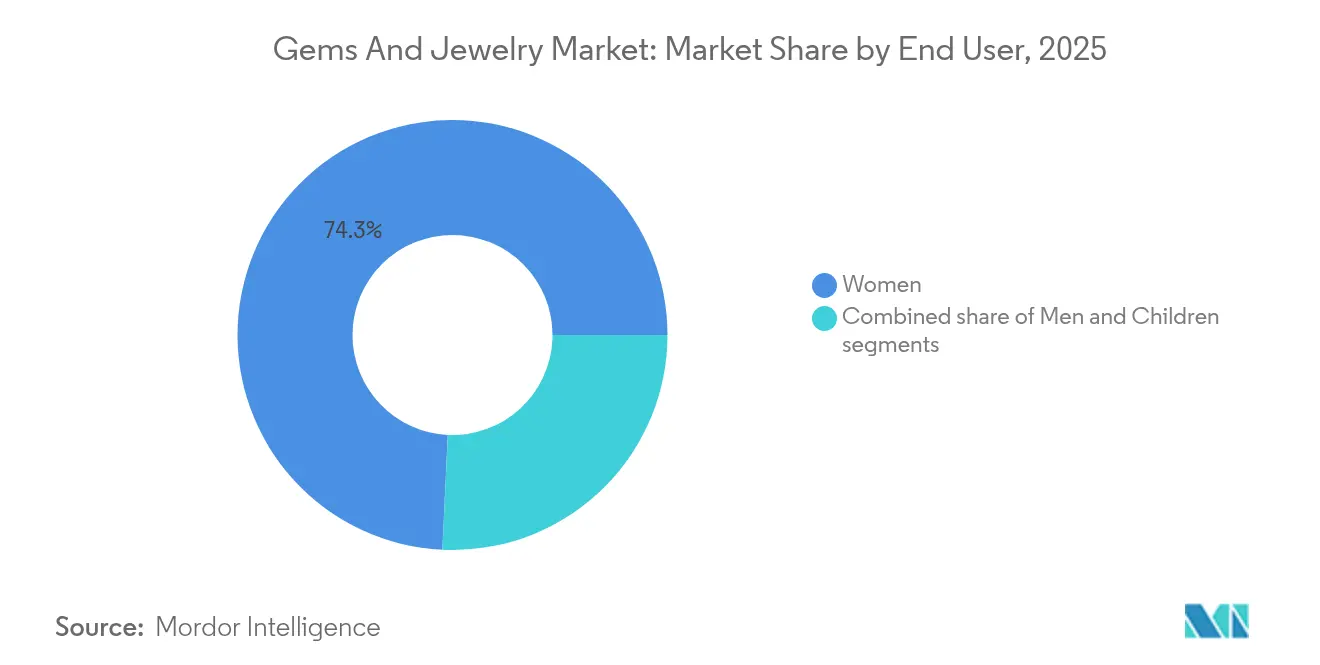

- By end user, women accounted for 74.25% of spending in 2025; the men’s segment is set to expand at a 6.03% CAGR to 2031.

- By category, fine jewelry captured 83.60% revenue in 2025; costume jewelry is poised for a 6.62% CAGR through 2031.

- By distribution channel, offline retail controlled 81.55% sales in 2025; online retail is expected to rise at a 7.05% CAGR to 2031.

- By geography, Asia-Pacific commanded a 38.74% share in 2025; the Middle East and Africa are projected to register a 6.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gems And Jewelry Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing fashion and lifestyle trends | +0.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Rising customization and personalization | +0.6% | North America and Asia-Pacific core markets | Medium term (2-4 years) |

| Adoption of lab-grown diamonds for sustainability and cost | +1.2% | Global, led by United States and India | Short term (≤ 2 years) |

| Jewelry as an investment and wealth-preservation hedge | +0.9% | Global, concentrated in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Cultural and traditional significance | +0.7% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Emergence of AR/VR virtual try-on tools | +0.4% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Jewelry as an investment and wealth-preservation hedge

Jewelry is increasingly seen as a reliable way to preserve wealth, especially during times of global economic uncertainty and rising inflation. In India, gold continues to dominate as the preferred investment option, as per the Gem and Jewellery Export Promotion Council, with gold demand in 2024 reaching 802.8 tonnes, a 5% rise compared to the previous year. Investment demand alone increased by 14% year-on-year in Q4 2024, reaching 76 tonnes[1]Source: Gem and Jewellery Export Promotion Council, "India’s Gold Jewellery Demand in 2024 Drops 2% To 563.4 Tonnes; +22% in Value to ₹3,61,690 Crore", gjepc.org. This growing confidence among institutions is boosting retail demand for high-purity and certified jewelry, including rare gemstones and vintage items. Platforms offering secure storage and verification of authenticity are becoming popular among wealthy individuals looking to diversify their investments. The Reserve Bank of India (RBI) significantly increased its gold reserves from 16 tonnes in 2023 to 72.6 tonnes in 2024, reflecting a strategic effort to protect against economic instability and inflation, as per the World Gold Council[2]Source: World Gold Council, "India gold market update: Investment demand shines", gold.org. This move shows strong institutional trust in gold as a stable asset, which further strengthens retail investor confidence and drives demand for high-quality investment jewelry.

Growing fashion and lifestyle trends

Jewelry has evolved from being an occasional luxury to becoming a part of everyday self-expression, supported by rising consumer purchasing power. The International Monetary Fund (IMF) reports that the global GDP per capita has reached USD 14,210 in 2025, reflecting stronger financial capacity among consumers[3]Source: International Monetary Fund (IMF), "World Datasets", imf.org. Social media has become a factor in spreading trends rapidly, with influencers creating viral "must-have" moments that make affordable luxury more popular. To keep up with these fast-changing trends, brands are adopting quicker design-to-market strategies and utilizing digital fashion weeks to stay relevant. For instance, Kendra Scott’s 2024 LoveShackFancy collection, which featured bow necklaces and heart-shaped lockets, demonstrated how limited-edition releases, combined with compelling storytelling and personalization, appeal to younger, style-conscious consumers. These approaches foster long-term brand loyalty, and as a result, the jewelry market is increasingly shifting toward fashion-focused designs and creating unique, experience-driven offerings for consumers.

Adoption of lab-grown diamonds for sustainability and cost

The growing popularity of lab-grown diamonds is transforming the gems and jewelry market by offering a cost-effective and sustainable alternative to mined diamonds. These diamonds, which are nearly identical to natural ones in quality, provide consumers with access to larger and higher-value stones at more affordable prices. Expanding production capabilities in countries like India and China are further driving down costs, making lab-grown diamonds more accessible. This shift is particularly appealing to millennials and Gen Z, who are increasingly prioritizing sustainability in their purchasing decisions. For instance, a survey performed by Grown Diamond Corporation revealed that 83% of consumers were open to buying fashion jewelry made with lab-grown diamonds, and 65% would consider man-made diamonds for engagement rings. These preferences indicate a significant change in consumer behavior, with synthetic diamonds gaining traction in jewelry segments. This trend is making diamonds more accessible to a broader audience, reshaping the market landscape.

Emergence of AR/VR virtual try-on tools

The use of Augmented Reality/Virtual Reality try-on tools is revolutionizing online jewelry shopping by addressing the challenge of not being able to physically try on items. These tools help customers feel more confident in their purchases, leading to higher sales and fewer returns. With AI-powered simulations, shoppers can see how rings, gemstones, and metals look on their skin tone and under different lighting conditions. Companies that have adopted these technologies are seeing increased average order values, while smaller brands are using them to reach global markets without needing physical stores. For example, Brilliant Earth introduced a virtual try-on feature in October 2024, allowing customers to see how jewelry looks on them before buying. Similarly, Christian Dior Couture launched a virtual try-on for its "Rose des Vents" campaign in April 2024, enabling users to try on earrings using their smartphones. As the cost of this technology decreases, virtual try-on is becoming a standard feature in the gems and jewelry market, rather than just a unique selling point.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Volatility in precious metal and gem prices | -1.1% | Global, acute in manufacturing hubs | Short term (≤ 2 years) |

| High import duties and taxes | -0.7% | Cross-border trade routes, India-United States corridor | Medium term (2-4 years) |

| Proliferation of counterfeit products | -0.5% | Global, concentrated in Asia-Pacific | Medium term (2-4 years) |

| Ethical and sustainability concerns | -0.3% | North America and Europe, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of counterfeit products

The growing issue of counterfeit products is a major challenge for the gems and jewelry market, as it weakens consumer confidence and harms the reputation of trusted brands. For instance, in August 2025, a case in Chennai exposed how two individuals deceived a bank out of over INR 2 crore by using fake gold jewelry. Similarly, United States Customs and Border Protection intercepted counterfeit jewelry valued at USD 30 million in Louisville in August 2025, showcasing the widespread nature of this problem[4]Source: United States Customs and Border Protection, "USD 30 Million in counterfiet jewelry seized", cbp.gov. To address this, manufacturers are increasingly using advanced technologies such as laser inscriptions, blockchain-based tracking systems, and QR-coded certifications to ensure product authenticity. Regulatory authorities are intensifying their enforcement efforts and launching awareness campaigns to educate consumers about identifying genuine products. These combined efforts not only protect buyers and uphold brand integrity but also play a crucial role in fostering trust in authentic products, which is vital for the market's sustained growth.

High import duties and taxes

High import duties and taxes continue to be a major challenge for the gems and jewelry market, as they increase costs and reduce global price competitiveness. For instance, in August 2025, the United States raised tariffs on Indian jewelry imports from 10% to 25%. This created additional cost pressures for Indian exporters, forcing many manufacturers to explore solutions such as relocating production facilities, utilizing duty-drawback schemes, or finding alternative sourcing options to maintain profitability. On the other hand, India’s decision to lower gold import duties from 15% to 6% in 2024 significantly improved the competitiveness of domestic manufacturers. This policy change reshaped trade patterns, allowing Indian manufacturers to compete more effectively in both local and international markets. The market still faces challenges from complex regulatory requirements and unclear compliance processes, which further increase operational costs. Larger, vertically integrated companies with strong supply chains and in-house logistics are better equipped to handle these challenges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rings Drive Market Leadership

Rings remain the leading category in the gems and jewelry market, capturing a substantial 33.02% share in 2025. Their strong demand is primarily due to their significance in engagements, weddings, and other special occasions, making them a timeless choice for consumers. The availability of classic, modern, and personalized designs further enhances their appeal. The growing popularity of online shopping has made it easier for customers to explore a wide range of options, with many seeking unique, high-quality craftsmanship to suit their preferences.

The necklace segment is expected to experience the fastest growth among jewelry categories, with a projected CAGR of 6.19% from 2026 to 2031. This growth is driven by changing fashion trends, such as layering and mixing styles, which encourage consumers to purchase multiple necklaces. Social media platforms and influencer campaigns are significantly influencing younger buyers, promoting innovative and trendy designs. Moreover, necklaces are increasingly being used as versatile accessories for both everyday wear and formal events, further boosting their demand across global markets.

By Material Type: Precious Metals Maintain Dominance

Precious metals led the gems and jewelry market in 2025, contributing 62.10% of the total market share. Gold remains a popular choice due to its value as an investment and its cultural significance, while silver attracts consumers with its affordability and versatility. Buyers are increasingly interested in both traditional and modern designs, with customization options and high-quality craftsmanship adding to their appeal. The segment also benefits from a strong presence in retail stores and the growing popularity of online shopping, making it accessible to a wide range of customers.

Base-metal jewelry is expected to grow the fastest among material categories, with a projected CAGR of 6.85% through 2031. This growth is supported by advancements in technology, such as anti-tarnish coatings and hypoallergenic materials, which make these pieces more durable and suitable for everyday use. Social media trends and influencer promotions are driving interest in affordable and stylish base-metal jewelry, especially among younger consumers. Innovative designs and finishes are helping this category gain popularity in global markets, offering a cost-effective yet fashionable option for buyers.

By End User: Women Lead, Men Accelerate

Women are the largest consumers in the gems and jewelry market, contributing to 74.25% of total spending in 2025. This is mainly driven by purchases for weddings, personal use, and gifting occasions. Both traditional and modern jewelry designs continue to attract female buyers, supported by effective marketing campaigns and social media promotions. The growing availability of affordable luxury options has further solidified women’s role as the primary consumers in this market.

The men’s jewelry segment, while smaller, is expected to grow significantly at a CAGR of 6.03% through 2031. Changing fashion trends and the increasing acceptance of gender-neutral styles are key factors driving this growth, especially in regions like Asia-Pacific and North America. Men are showing more interest in jewelry items such as rings, bracelets, and cufflinks, which are becoming popular as fashion statements. Targeted marketing efforts and innovative designs are helping to expand the appeal of men’s jewelry, gradually diversifying the market’s consumer base.

By Category: Fine Jewelry Dominance Faces Disruption

Fine jewelry continues to lead the gems and jewelry market, contributing 83.60% of total revenue in 2025. This segment's popularity stems from the enduring appeal of precious metals and gemstones, along with the trust consumers place in certified and authentic products. Traditional designs and expert craftsmanship remain key drivers of demand, while premium branding enhances its value. The availability of fine jewelry through both physical retail stores and online platforms has further expanded its reach to a broader customer base.

Meanwhile, costume jewelry is projected to grow at the fastest rate, with a CAGR of 6.62% from 2026 to 2031. This growth is fueled by the increasing use of lab-grown diamonds, recycled materials, and affordable designs that cater to cost-conscious buyers. Costume jewelry is also gaining traction due to its trendy and versatile collections, often promoted by influencers and social media campaigns. These factors are helping costume jewelry attract a growing audience and gradually close the gap with fine jewelry in terms of consumer interest and market relevance.

By Distribution Channel: Digital Transformation Accelerates

Offline retail remains the leading channel in the gems and jewelry market, contributing 81.55% of the total market share in 2025. Physical stores continue to attract customers due to the ability to see and feel the products in person, which builds trust and confidence in high-value purchases. Flagship stores, specialty retailers, and multi-brand outlets are preferred for their personalized services, expert guidance, and the opportunity to inspect jewelry before buying. These factors make offline retail a dominant force in the market.

On the other hand, online sales are growing at a fast pace, with an expected CAGR of 7.05% through 2031. This growth is driven by technological advancements like augmented reality (AR) and virtual reality (VR), which allow customers to visualize jewelry online. Features such as insured shipping, easy returns, and loyalty programs that connect online and offline shopping experiences are also boosting e-commerce adoption. Online platforms offer convenience, a wide variety of designs, and customization options, making them an increasingly important part of the market's growth trajectory.

Geography Analysis

Asia-Pacific accounted for 38.74% of the revenue in 2025, driven by a strong cultural preference for gold, increasing disposable incomes, and its leading role in cutting and polishing gemstones. Countries like China are utilizing heritage-inspired designs to attract domestic consumers, while India benefits from reduced duties that enhance its export competitiveness. Surat’s lab-grown diamond production is helping the region by lowering costs and improving supply chain efficiency. Urbanization is also boosting bridal jewelry spending, as consumers aspire to replicate celebrity wedding trends.

The Middle East and Africa are expected to grow at a CAGR of 6.88%, combining high spending from oil wealth with the cultural significance of jewelry in traditional ceremonies. Gold jewelry in this region serves both as a decorative item and a form of savings, ensuring steady demand even during economic downturns. Dubai’s tax-free shopping hubs act as key re-export centers for Africa and Europe, while local mining activities in countries like Kenya and Ghana strengthen the upstream supply chain. The growing youth population and increasing e-commerce adoption are expanding the customer base in this region.

North America and Europe represent mature markets that are now focusing on innovation to sustain growth. Consumers in these regions are increasingly drawn to sustainable practices, lab-grown diamonds, and personalized shopping experiences. In the United States, tariffs are encouraging near-shoring and vertical integration, while the European Union’s conflict-minerals regulations are driving the adoption of blockchain technology for tracking product origins. Millennials and Gen Z are reshaping the market with their preference for online shopping and self-purchasing, challenging traditional retail formats. Ethical sourcing and digital convenience are becoming key factors for success in these established but competitive markets.

Competitive Landscape

The gems and jewelry market is moderately fragmented with leading players such as LVMH Moët Hennessy Louis Vuitton SE, Compagnie Financière Richemont SA and Chow Tai Fook (Holding) Limited, with opportunities for consolidation and growth for smaller, innovative players. Large luxury companies benefit from controlling the entire supply chain, from mining to retail, which helps them manage costs effectively. Meanwhile, newer digital-first brands are growing quickly by using influencer marketing and limited-edition product drops to attract younger consumers. Companies are focusing on creating seamless shopping experiences across online and offline channels, offering personalized products, and ensuring transparency in their supply chains.

Sustainability has become a key factor in building brand reputation. For example, Pandora has committed to using only recycled metals, and Signet is conducting responsible sourcing audits to gain a competitive edge. Mergers and acquisitions are increasing as companies aim to expand their capabilities in lab-grown diamonds and strengthen their regional presence. Retailers are also adopting advanced technologies like augmented reality for virtual fittings, artificial intelligence for custom designs, and dynamic pricing to enhance customer experiences. Businesses that invest in understanding customer preferences through data platforms are better positioned to optimize their product offerings and marketing strategies.

Regulations and compliance requirements, such as traceability and environmental, social, and governance (ESG) reporting, are becoming more stringent. These demands often favor larger companies with the resources to meet these standards, potentially leading to greater market concentration. Blockchain technology is being tested to prevent counterfeit products, but industry-wide adoption is still in its early stages. At the same time, companies that prioritize ethical sourcing and sustainability are gaining consumer trust and loyalty. As the market evolves, businesses that combine innovation, transparency, and customer-centric strategies are likely to maintain a competitive edge in this dynamic industry.

Gems And Jewelry Industry Leaders

-

LVMH Moët Hennessy Louis Vuitton SE

-

Compagnie Financière Richemont SA

-

Chow Tai Fook (Holding) Limited

-

Pandora A/S

-

Swarovski AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: India's P N Gadgil Jewellers (PNGD.NS) introduced Litestyle, a sub-brand focused on lightweight and lower-carat jewelry. This launch aimed to cater to budget-conscious consumers as record gold prices drove demand for more affordable options.

- April 2025: US-based fine jewelry label Angara expanded its operations to India, adopting a digital-first strategy to cater to the local market. The brand also announced plans to establish a physical retail presence, aiming to strengthen its connection with Indian consumers.

- August 2024: Reliance Jewels marked its 17th anniversary in the jewelry industry by unveiling the Aabhar collection. The collection showcased an array of earrings, including jhumkis, studs, and J-balls, designed to appeal to diverse age groups, styles, and occasions.

- August 2022: Pandora launched a new line of jewelry known as the 'Pandora Brilliance' in the United States and Canada. This line features diamonds produced from 100 percent renewable energy, grown in the United States.

Global Gems And Jewelry Market Report Scope

Gems and jewelry are decorative objects worn on clothes or the body that are usually made from valuable metals, such as gold, silver, and precious stones. The market report is segmented by product type, distribution channel, and geography. Based on product type, the market has been segmented into Rings, Necklaces, Earrings, Bracelets, Chains & Pendants, and Other Product Types. Based on the distribution channel, the market has been segmented into Offline Retail Stores and Online Retail Stores. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle-East & Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD billion).

| Rings |

| Necklaces |

| Earrings |

| Bracelets |

| Chains and Pendants |

| Other Product Types |

| Precious Metals |

| Base Metals |

| Mixed Materials |

| Men |

| Women |

| Children |

| Fine |

| Costume |

| Offline Retail Stores |

| Online Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Colombia | |

| Chile | |

| Peru | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Rings | |

| Necklaces | ||

| Earrings | ||

| Bracelets | ||

| Chains and Pendants | ||

| Other Product Types | ||

| By Material Type | Precious Metals | |

| Base Metals | ||

| Mixed Materials | ||

| By End User | Men | |

| Women | ||

| Children | ||

| By Category | Fine | |

| Costume | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Colombia | ||

| Chile | ||

| Peru | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the global gems and jewelry market in 2026?

The gems and jewelry market size is USD 394.74 billion in 2026 and is projected to reach USD 493.68 billion by 2031 at a 4.58% CAGR.

Which product category leads sales?

Rings hold the top position, accounting for 33.02% of 2025 revenue due to engagement and wedding demand.

Which region will grow fastest through 2031?

The Middle East and Africa gems and jewelry market is forecast to grow at 6.88% CAGR, outpacing all other regions.

How are online channels changing jewelry retail?

Online platforms are expected to expand at 7.05% CAGR, aided by AR/VR try-on, insured shipping, and omnichannel loyalty programs.

Page last updated on: