Luxury Goods Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

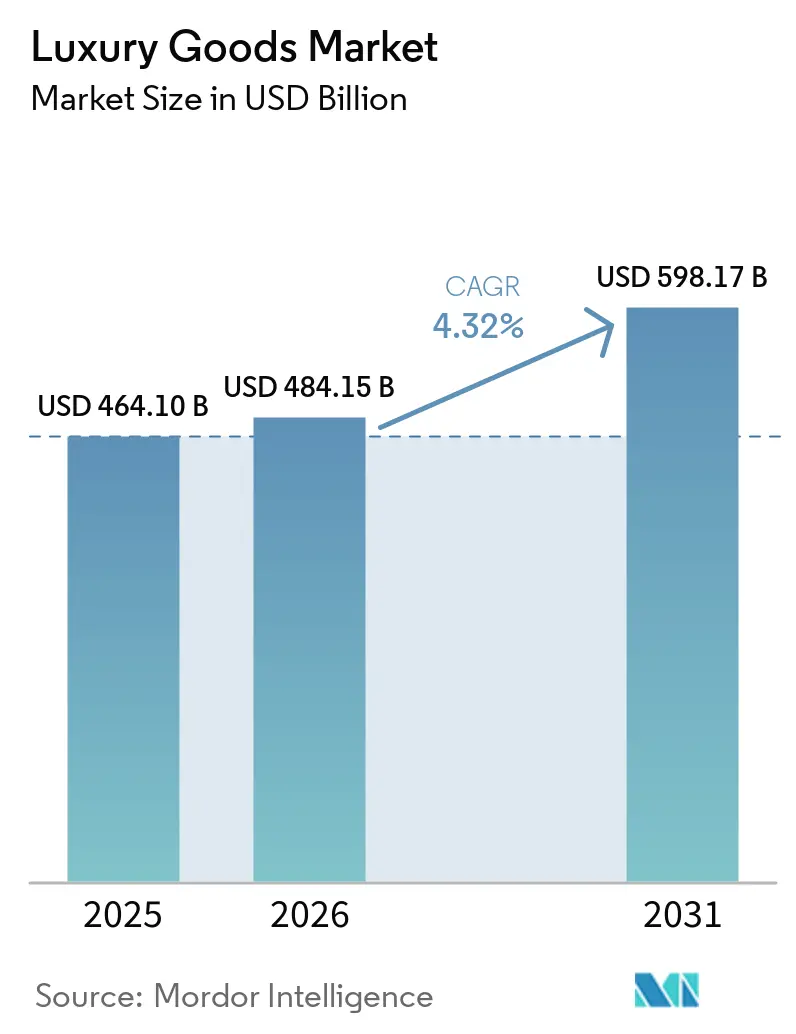

| Market Size (2026) | USD 484.15 Billion |

| Market Size (2031) | USD 598.17 Billion |

| Growth Rate (2026 - 2031) | 4.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Luxury Goods Market Analysis by Mordor Intelligence

The global luxury goods market size is expected to grow from USD 464.1 billion in 2025 to USD 484.15 billion in 2026 and is forecast to reach USD 598.17 billion by 2031 at 4.32% CAGR over 2026-2031. The global luxury goods market is witnessing resilient growth, digital connectivity is expanding, and there's a robust demand for iconic heritage brands, all contributing to the resilient growth of the global luxury goods market. While clothing and apparel lead the product categories, watches are emerging as the fastest-growing segment, signaling a shift towards investment-driven purchases. Women have traditionally driven the bulk of sales, but male consumers are now accelerating market expansion. Europe, with its entrenched luxury culture and allure for tourists, remains the largest regional luxury goods market. However, the Asia-Pacific region is swiftly gaining ground, buoyed by a burgeoning affluent population and a surge in aspirational consumption. While single-brand boutiques currently rake in the most revenue, online channels are witnessing the swiftest growth. Brands within the luxury goods market are increasingly turning to data-driven omnichannel strategies to align with shifting consumer expectations. Amid these transformations, sustainability and ESG transparency have taken center stage. Younger consumers, in particular, are emphasizing ethical practices, authenticity, and traceable supply chains in their buying choices.

Key Report Takeaways

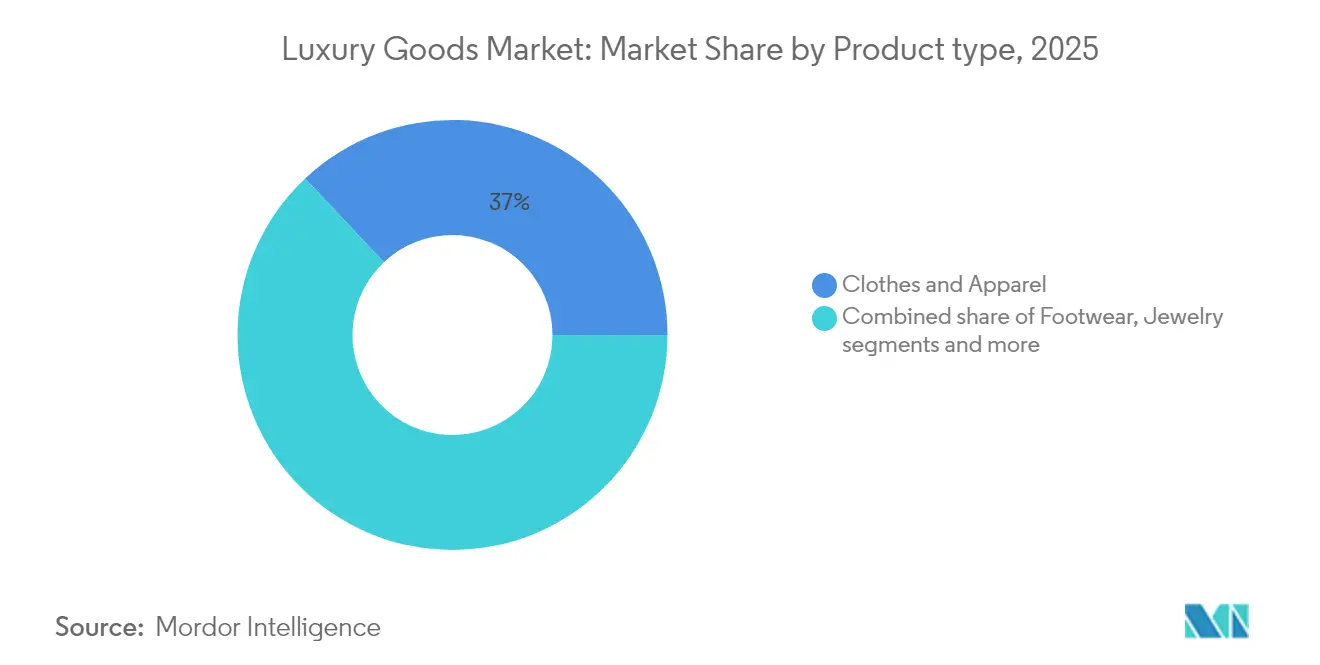

- By product type, clothing and apparel held 37.02% of the global luxury goods market share in 2025, while watches are forecast to grow fastest at a 4.38% CAGR through 2031.

- By end user, women represented 56.08% of purchases in 2025; men are projected to advance at a 4.69% CAGR over the forecast period.

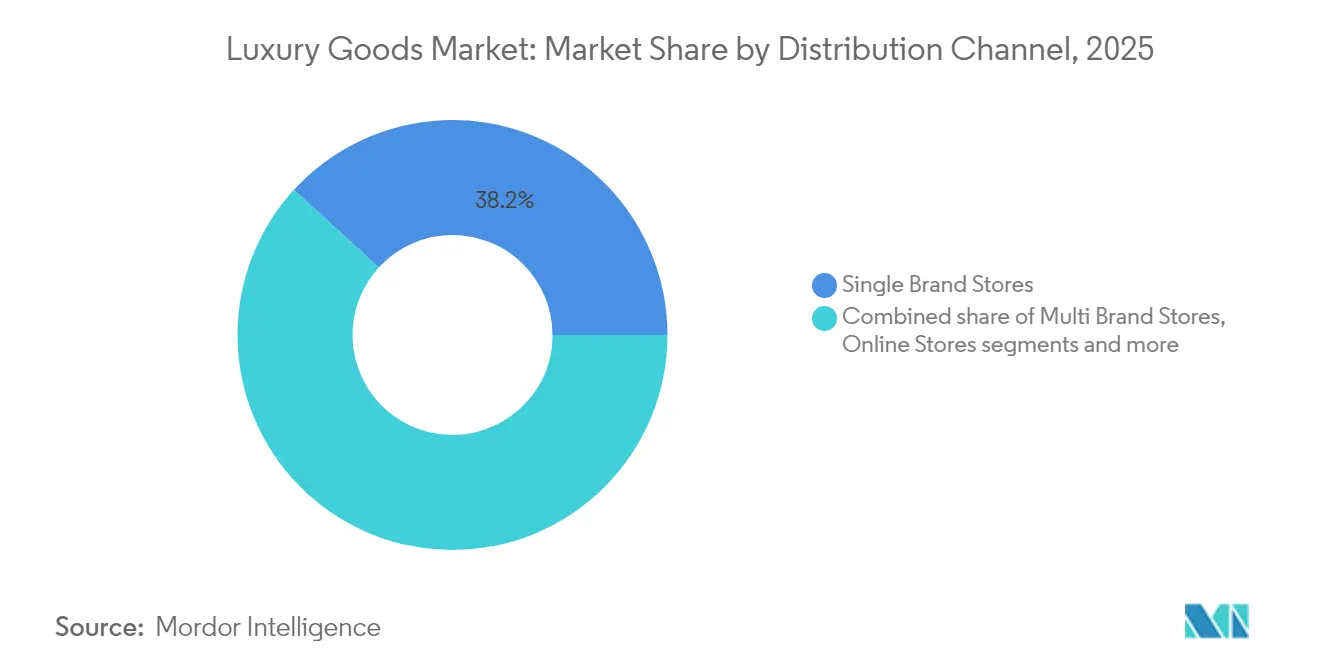

- By distribution channel, single-brand stores controlled 38.20% of 2025 revenue; online stores record the highest projected CAGR of 5.05% to 2031.

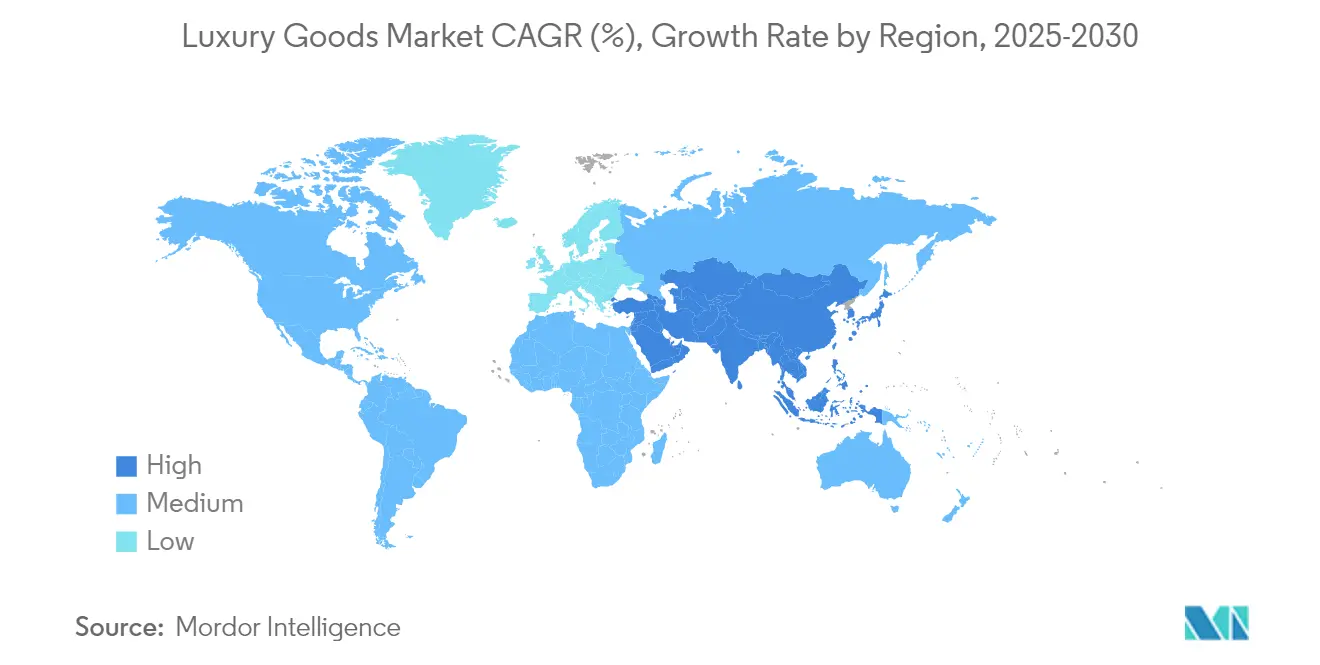

- By geography, Europe accounted for 52.10% of 2025 sales, whereas Asia-Pacific is poised to accelerate at a 5.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Luxury Goods Market Trends and Insights

Drivers Impact Table*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Consumer shift toward sustainable and eco-certified luxury products | +1.2% | Global, with EU leading regulatory framework | Medium term (2-4 years) |

| Influence of social media and celebrity endorsement | +0.8% | Global, with Asia-Pacific showing highest engagement | Short term (≤ 2 years) |

| Rising disposable income and wealth accumulation | +0.9% | Asia-Pacific core, spill-over to Middle East | Long term (≥ 4 years) |

| Product innovation in terms of raw material and design | +0.7% | Global, with Europe and North America leading Research and Development | Medium term (2-4 years) |

| Consumers inclination towards limited edition products | +0.6% | Global, with strongest impact in North America and Europe | Short term (≤ 2 years) |

| Growth of experience-based luxury and personalization services | +0.5% | Global, with premium markets leading adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Consumer shift toward sustainable and eco-certified luxury products

Sustainability is now a major factor driving the growth of the global luxury goods market. Luxury brands are increasingly adopting eco-friendly practices, such as offering buy-back programs, lifetime repair services, and creating collections from recycled materials in the luxury goods market. These efforts are further encouraged by regulatory requirements like the EU’s Corporate Sustainability Reporting Directive and the upcoming digital product passports, which were implemented in September 2024 [1]Source: European Commission, “EU's Digital Product Passport: Advancing Transparency and Sustainability,”europa.eu. This initiative, part of the Ecodesign for Sustainable Products Regulation, aims to enhance transparency across product value chains by providing comprehensive information about each product’s origin, materials, environmental impact, and disposal recommendations. For instance, Chanel has announced its Nevold initiative, set to launch in 2025, which will transform unsold stock into premium recycled materials. Similarly, Bottega Veneta has introduced its “Certificate of Craft” program, which provides lifetime repair services and uses surplus leather to create new products. These sustainability-focused initiatives not only help luxury brands reduce their environmental impact but also enhance the exclusivity and value of their products.

Influence of social media and celebrity endorsement

Social media platforms like Instagram and TikTok have become vital tools for promoting and selling luxury goods, especially in rapidly growing markets. These platforms simplify the process for consumers, allowing them to easily discover products and make purchases. In the luxury goods market, widespread usage has made social media a key channel for luxury brands to connect with their audience. Influencer marketing has evolved from short-term promotions to long-term collaborations that build stronger brand associations. For instance, the long-term collaboration with David Beckham started in Q3 2024 with the Fall/Winter campaign, while the Spring/Summer 2024 collection featured Gisele Bündchen. These celebrity campaigns doubled social media engagement and reached 40 million livestream views. Similarly, Zendaya’s role as an ambassador for Louis Vuitton continues to enhance the brand’s appeal across both Western and Asian markets by creating aspirational connections with consumers. In 2024, Dior collaborated with Jisoo from BLACKPINK for a special campaign that combined the global influence of K-pop with the sophistication of Parisian high fashion.

Rising disposable income and wealth accumulation

Luxury spending has remained strong despite challenges in the global economy, mainly due to the consistent wealth of ultra-high-net-worth individuals (UHNWIs). These wealthy individuals continue to drive demand for premium products in the luxury goods market,, even as overall consumer confidence varies. Additionally, disposable income is increasing, as reported by the International Monetary Fund. As of April 2025, it stands at USD 206.88 thousand per capita globally [2]Source: International Monetary Fund, “GDP, Current Prices Purchasing Power Parity; Billions of International Dollars,”imf.org. Strong holiday sales, especially during events like China's Singles' Day and Western Christmas shopping, bolstered this growth. Additionally, high-spending tourists are increasingly opting for domestic shopping. These consumers, who previously indulged in international shopping sprees, are now buying luxury goods locally. India, urbanization, rising disposable incomes, and heightened brand awareness are driving the rapid expansion of the luxury beauty market. Responding to this surge, global giants like Estée Lauder and LVMH are inaugurating new stores in major cities such as Mumbai, Delhi, and Bengaluru, as well as in emerging centers like Hyderabad and Pune. The Middle East is solidifying its status in the luxury goods market as a pivotal luxury region. Saudi Arabia's Vision 2030 reforms have birthed upscale shopping venues like VIA Riyadh, now home to esteemed brands like Balenciaga and Dolce & Gabbana. Concurrently, Dubai is reinforcing its reputation as a premier luxury shopping destination, underscored by the 2024 debut of Chanel's largest regional boutique.

Consumers' inclination towards limited edition products

Limited-edition luxury goods are increasingly captivating consumers, driving the luxury goods market's expansion. The allure of these exclusive items lies in their rarity, which not only elevates their perceived value but also enables brands to set premium prices, bolstering their prestige. Such limited releases cultivate urgency and emotional ties among buyers, often leading to swift purchasing choices. Take, for example, Louis Vuitton's 2024 debut of “LV By The Pool,” a tropical-themed capsule collection. Promoted through influencers and global pop-up events, it saw a swift sellout and boosted brand visibility. In a similar vein, Dior collaborated with artist Pietro Ruffo for the “Dior Jardin” collection, spotlighting hand-embroidered, art-inspired pieces that emphasized craftsmanship and creative exclusivity. Meanwhile, in the luxury watch arena, Audemars Piguet unveiled its Royal Oak Concept Tourbillon “Spider-Man” edition, limited to a mere 250 units, generating worldwide buzz and an instant sellout. Such launches not only drive immediate sales but also enhance brand allure, owing to social media buzz and increased collector interest, cementing the status of limited editions as both cultural milestones and commercial triumphs.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Proliferation of counterfeit products | -0.9% | Global, with highest impact in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Lesser demand from price sensitive consumers | -0.6% | Global, with strongest impact in emerging markets | Medium term (2-4 years) |

| Stringent regulatory environment and compliance costs | -0.4% | EU leading, with spillover to global operations | Long term (≥ 4 years) |

| Economic uncertainty and inflation impact on consumer spending | -0.3% | Global, with varying regional intensity | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of counterfeit products

The rise of high-quality “superfakes” in the luxury goods market has made it harder to distinguish between genuine and counterfeit luxury products, pushing brands to adopt advanced technologies to protect their authenticity. In June 2025, Australian authorities arrested three individuals for selling counterfeit luxury goods worth AUD 10.7 million online. The operation also led to the seizure of over 500 fake luxury items, including handbags and watches, along with AUD 250,000 in cash and a gel blaster firearm. According to the OECD, the global trade in counterfeit goods reached USD 467 billion in 2025, posing significant risks to consumer safety and intellectual property rights [3]Source: Organisation for Economic Co-operation and Development, “Global Trade in Fake Goods Reached USD 467 Billion, Posing Risks to Consumer Safety and Compromising Intellectual Property," oecd.org. To combat this growing issue within the luxury goods market, brands like Prada and Vacheron Constantin have started using blockchain-based certificates to verify the authenticity of their products. The Aura Blockchain Consortium, supported by LVMH, Cartier, and Prada, has expanded its digital product passport initiative, which now tracks tens of millions of luxury items. As counterfeit goods become more normalized among younger consumers, luxury brands are not only increasing their enforcement efforts but also launching educational campaigns to emphasize the importance of authenticity as a core part of the luxury experience.

Stringent regulatory environment and compliance costs

In the luxury goods market, luxury brands are facing increasing challenges due to complex regulations and high compliance costs, which are slowing down growth in 2024. Companies are now required to dedicate significant resources to meet various legal requirements, including ESG (Environmental, Social, and Governance) reporting, supply chain monitoring, digital product passports, green claims verification, and anti-forced labor compliance. These measures are mandated by EU laws such as the Corporate Sustainability Reporting Directive (CSRD), Corporate Sustainability Due Diligence Directive (CSDDD), Green Claims Directive, and Eco-design regulation. In France, additional challenges such as increased corporate taxes and extended producer responsibility rules are putting pressure on profit margins. Smaller suppliers, especially those producing "Made in Italy" goods, are struggling to manage rising costs related to energy, software, audits, and labor compliance. For example, Dior’s 2024 subcontractor scandal in Milan highlighted the difficulties of managing complex and often opaque supply chains. The incident revealed the heavy administrative burden of conducting frequent supplier audits, which are necessary to ensure compliance and protect brand reputation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Investment Momentum Shifts from Apparel to Watches

In 2025, clothing and apparel dominated the global luxury goods market, claiming a 37.02% share. This underscores their pivotal role in shaping brand identities and weaving emotional narratives. Apparel, being one of the most prominent luxury categories, often acts as the initial touchpoint for consumers venturing into the luxury realm. Its engagement is perpetually heightened, influenced by seasonal trends, fashion weeks, and the sway of influencer marketing. In the luxury goods market, the luxury beauty segment thrives, buoyed by the "lipstick effect." The premium skincare and cosmetics not only shine but also serve as more approachable gateways into the luxury world. This segment's vitality is further amplified by a resurgence in travel retail and an escalating self-care culture.

In the luxury goods market, luxury watches, however, are set to outpace all, with a projected CAGR of 4.38% through 2031. This surge underscores a notable pivot in consumer focus towards items that promise enduring value and emotional resonance. The allure of watches is bolstered by climbing auction prices, a burgeoning community of collectors, and the recognition of high-end mechanical timepieces as coveted, appreciating assets. In contrast to the ever-shifting world of fashion, watches boast a timeless charm, enduring functionality, and a storied brand legacy. Jewelry, too, stands resilient, cherished for its sentimental significance, cultural ties, and its reputation as a safeguard against inflation. Footwear and eyewear are carving out their niches, emphasizing comfort, sustainability, and advanced fitting technologies, ensuring their relevance in a luxury landscape increasingly driven by performance and values.

By End User: Women Lead but Men’s Premium Appetite Rises

In 2025, women made up 56.08% of purchases in the luxury goods market, largely due to their strong interest in categories like fashion, beauty, and accessories. Men’s spending on luxury goods is also expected to grow at a 4.69% CAGR through 2031, as their preferences expand to include skincare, high-end clothing, and lifestyle products, alongside traditional items like watches and cars. To cater to these changing trends, luxury brands are introducing gender-neutral product lines, such as bags and fragrances, which appeal to a broader audience and reflect evolving household buying patterns. Wealthy male shoppers often focus on items with long-term value, such as luxury watches and limited-edition sneakers, which are highly sought after for their exclusivity and potential as investments. These shifts in consumer behavior are encouraging brands to diversify their offerings and target both genders more effectively.

In the luxury goods market, younger female consumers are increasingly using digital platforms to explore luxury products, relying on tools like virtual try-ons and social media shopping features before visiting stores. The growing popularity of unisex products is also helping brands attract Gen Z shoppers, who value inclusivity and affordability. Additionally, personalized services, such as custom tailoring and co-creation workshops, are becoming essential for building stronger customer relationships and enhancing the shopping experience. These strategies not only help brands connect with younger, tech-savvy audiences but also foster customer loyalty. As a result, these efforts are driving sustained growth in the global luxury goods market.

By Distribution Channel: Flagship Authority Meets Digital Velocity

In 2025, single-brand boutiques in the luxury goods market accounted for 38.20% of total sales, reflecting consumers’ strong preference for shopping in exclusive stores that showcase the craftsmanship and heritage of luxury brands. These boutiques offer a unique and premium shopping experience, but their high operating costs mean brands are carefully selecting locations in popular tourist destinations and high-traffic malls. At the same time, online stores are becoming increasingly important, with a projected CAGR of 5.05%. They cater to younger, tech-savvy shoppers who value the convenience of discovering and purchasing luxury items online, making e-commerce a vital part of the luxury goods market's growth strategy.

The integration of physical and digital retail is reshaping how luxury brands engage with customers. Innovations like inventory-free showrooms, same-day delivery services, and appointment-based shopping are enhancing customer experiences while reducing the need for large retail spaces. In the department store sector, mergers such as the USD 2.65 billion Saks Global-Neiman Marcus deal completed in 2024 highlight how traditional retailers are joining forces to stay competitive by leveraging advanced data and logistics capabilities. Additionally, resale platforms, pop-up stores, and duty-free zones are helping brands expand their reach. Technologies like augmented reality try-ons and video shopping are also making it easier for customers to explore and purchase products from anywhere. These advancements ensure that the luxury goods market remains focused on delivering exceptional experiences across all shopping channels.

Geography Analysis

Europe contributed 52.10% of the revenue in the luxury goods market in 2025, driven by its famous luxury brands and strong tourism industry. Companies like Hermès, LVMH, and Kering have shown positive growth, but challenges such as currency changes and potential US tariffs create some uncertainty. Additionally, new EU sustainability rules are increasing costs, encouraging brands to invest in local production and innovative materials. European customers still prefer in-store shopping, making excellent service and exclusive product launches essential for maintaining loyalty. The region’s mature market emphasizes the importance of creating unique shopping experiences to attract repeat customers and sustain growth in the luxury goods market.

In the luxury goods market, Asia-Pacific is expected to lead future growth, with a projected CAGR of 5.41% through 2031. China’s recovery is supported by increased domestic spending and duty-free shopping policies in Hainan. India’s growing beauty market and rising demand for designer clothing are also expanding the customer base. South-East Asia benefits from the rise of digital payments and the development of luxury-focused malls. To stay competitive, brands are adapting their products to local preferences, such as using lighter fabrics for tropical climates and launching special collections during regional festivals. This region’s diverse markets offer significant opportunities for luxury brands to expand their presence.

North America continues to grow steadily, while unique shopping experiences in cities like Miami and Las Vegas encourage higher spending. The Middle East and Africa also show strong potential, with Dubai’s flagship stores and Riyadh’s Vision 2030 projects boosting demand for luxury goods. Africa’s growing wealthy class is showing interest in jewelry and watches, though challenges like high import duties and logistics remain.

In South America, Brazil leads the luxury goods market, offering growth opportunities but requiring strategies like currency hedging and localized pricing to succeed.

Mordor Intelligence provides coverage of the luxury goods market across other key regional markets, including Middle East, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Russia incorporating local coverage and market participation, as required.

Competitive Landscape

The global luxury goods market maintains a moderately fragmented structure, with major companies like LVMH, Richemont, Kering, and Hermès holding substantial market share through their diverse brand portfolios and extensive retail networks. Independent brands are carving out market positions by focusing on niche segments, emphasizing heritage and craftsmanship. LVMH's relaunch of Patou as a sustainable, digital-first brand has resonated with younger consumers seeking ethical luxury. Similarly, Marine Serre has established recognition through eco-conscious designs and circular fashion collections. The competitive landscape in luxury e-commerce continues to evolve, as evidenced by Mytheresa's EUR 555 million acquisition of YOOX NET-A-PORTER.

Digital transformation is fundamentally altering luxury retail operations and customer engagement. Balenciaga's integration of Apple Vision Pro demonstrates the shift toward immersive shopping experiences, while LVMH's FancyTech collaboration implements AI-driven personalization across customer service platforms. Blockchain technology adoption helps verify product authenticity and reduces counterfeiting risks. Sustainability initiatives have become essential to market strategies, with luxury brands investing in low-carbon leather production, bio-based materials, and environmentally conscious manufacturing facilities to meet regulatory requirements and consumer expectations.

Luxury brands are diversifying their market approach through various strategies. Companies are introducing entry-level products in the accessories and cosmetics categories to attract younger consumers and develop long-term customer relationships. The market is expanding into experiential luxury, exemplified by Bulgari's hotel ventures and Louis Vuitton's heritage exhibitions. These approaches, combined with brand storytelling, strategic collaborations, and personalized services, support luxury goods market growth for both established and emerging companies. Market success increasingly requires companies to integrate traditional luxury values with technological advancement while balancing exclusivity and broader market accessibility.

Luxury Goods Industry Leaders

-

LVMH Moet Henessy Louis Vuitton

-

Hermès International S.A.

-

Kering S.A

-

Chanel SA

-

Compagnie Financière Richemont SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Tissot introduced a new evolution of its Seastar collection with a 38mm chronograph that combines heritage elements with modern design. The collection features six models, each with distinct characteristics. The 38mm Seastar Chronograph delivers water sport functionality in a compact design. The watch, constructed from stainless steel and water-resistant to 30 bar (300 meters), suits both aquatic activities and daily wear.

- March 2025: Jacadi Paris, the French luxury children's wear brand, established its presence in India by opening its first store in Mumbai. The company partnered with Burgundy Brand Collective, an India-based firm, to facilitate its market entry.

- March 2025: Dua Lipa collaborated with YSL Beauty for a limited-edition cosmetics collection which aimed to attract younger consumers to the luxury beauty market. The partnership demonstrated the value of celebrity endorsements, as her global popularity increased YSL's brand visibility among target demographics.

- January 2025: Fendi launched a holiday collection featuring its FF monogram with festive colors. The collection encompasses accessories, ready-to-wear items, and footwear incorporating motifs of luck, renewal, and prosperity. The designs feature seasonal elements, including florals, metallic accents, and symbolic colors. The collection integrates traditional red and gold colors across signature products, including the Peekaboo and Baguette bags.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our team defines the luxury goods market as the annual sales of premium clothing, footwear, leather accessories, eyewear, jewelry, watches, and beauty-oriented personal care that command above-average price points because of brand equity, craftsmanship, and scarcity.

Scope exclusion: We deliberately leave out luxury automobiles, travel services, second-hand items, and fine wines or spirits to keep value pools homogeneous.

Segmentation Overview

-

By Product Type

- Clothing and Apparel

- Footwear

- Eyewear

- Handbags and Wallets

- Jewelry

- Watches

- Beauty and Personal Care

-

By End User

- Men

- Women

- Unisex

-

By Distribution Channel

- Single Brand Stores

- Multi Brand Stores

- Online Stores

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Rest of North America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Desk Research

We begin by screening open datasets such as UN Comtrade trade codes, IMF household spending tables, World Bank income tiers, and WTO counterfeit seizure statistics, and then we mine association portals, LuxeVision, CECED Europe, and the Jewellery Association of India, for segment clues that traditional statistics miss. Company 10-Ks, investor decks, and news archives inside Dow Jones Factiva add brand-level revenue splits, while Questel patent alerts hint at pipeline launches. These strands anchor baseline demand, channel shifts, and price dispersion. The examples above are illustrative; many other public and proprietary sources were consulted to validate figures and context.

Primary Research

Next, we conduct structured interviews and short surveys with brand managers, upscale retailers, duty-free buyers, and wealth-management advisors across Europe, Asia, and the Americas. Their insights fine-tune our average selling prices, online penetration, and emerging cohort preferences, giving us sharper checks on the desk-based assumptions.

Market-Sizing & Forecasting

According to Mordor Intelligence, the market stands at a significant value. We use a top-down household-income demand pool that layers spending propensities by income decile and region, followed by one pass of supplier roll-ups to cross-check totals. Key model variables include HNWI counts, per-capita discretionary spend, counterfeiting leakage rates, average unit retail prices, and e-commerce share of luxury sales. A multivariate regression with ARIMA error correction projects each driver to the end of the forecast period. Where bottom-up estimates lag duty-free or e-commerce data, proportional adjustments are applied so totals align with observable trade flows.

Data Validation & Update Cycle

Before sign-off, analysts compare model outputs with export receipts, brand disclosures, and social-media sentiment spikes; any variance above three percentage points triggers re-contact of respondents. The model is refreshed every twelve months, with interim updates when currency shocks, tax changes, or major M&A events occur.

Why Mordor's Luxury Goods Baseline Earns Trust

Published estimates differ because firms pick dissimilar product baskets, currency years, and refresh cadences.

Key gap drivers include rivals counting second-hand items, narrower regional cuts, or relying on static ASP assumptions that ignore pricing power swings. Mordor's annual update cadence and dual cross-checks on income and brand shipments curb such drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 464.1 B (2025) | Mordor Intelligence | - |

| USD 284 B (2023) | Global Consultancy A | Excludes beauty goods, uses pre-COVID base year |

| USD 390.17 B (2024) | Trade Journal B | Omits eyewear; assumes constant 6.8 % ASP lift |

| USD 462.77 B (2024) | Industry Portal C | Adds second-hand sales and luxury experiences |

In sum, our disciplined scope, live primary validations, and yearly recalibration provide decision-makers with a balanced, reproducible baseline that sits between optimistic channel-heavy views and conservative product-only tallies.

Key Questions Answered in the Report

What is the current global luxury goods market size?

The global luxury goods market size reached USD 484.15 billion in 2026 and is projected to hit USD 598.17 billion by 2031 at a 4.32% CAGR.

Which region will grow fastest in luxury goods sales through 2031?

Asia-Pacific is expected to post the highest 5.41% CAGR, propelled by China’s continued recovery and India’s expanding affluent middle class.

Which product category is projected to grow quickest?

Watches lead growth with an anticipated 4.38% CAGR, reflecting rising collector demand and the perception of timepieces as investment assets.

How big is Europe’s share of global luxury revenue?

Europe accounted for 52.10% of global luxury goods market share in 2025, supported by its heritage brands and high tourism footfall.

Page last updated on: