Pearl Jewelry Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 15.59 Billion |

| Market Size (2031) | USD 23.02 Billion |

| Growth Rate (2026 - 2031) | 8.11% CAGR |

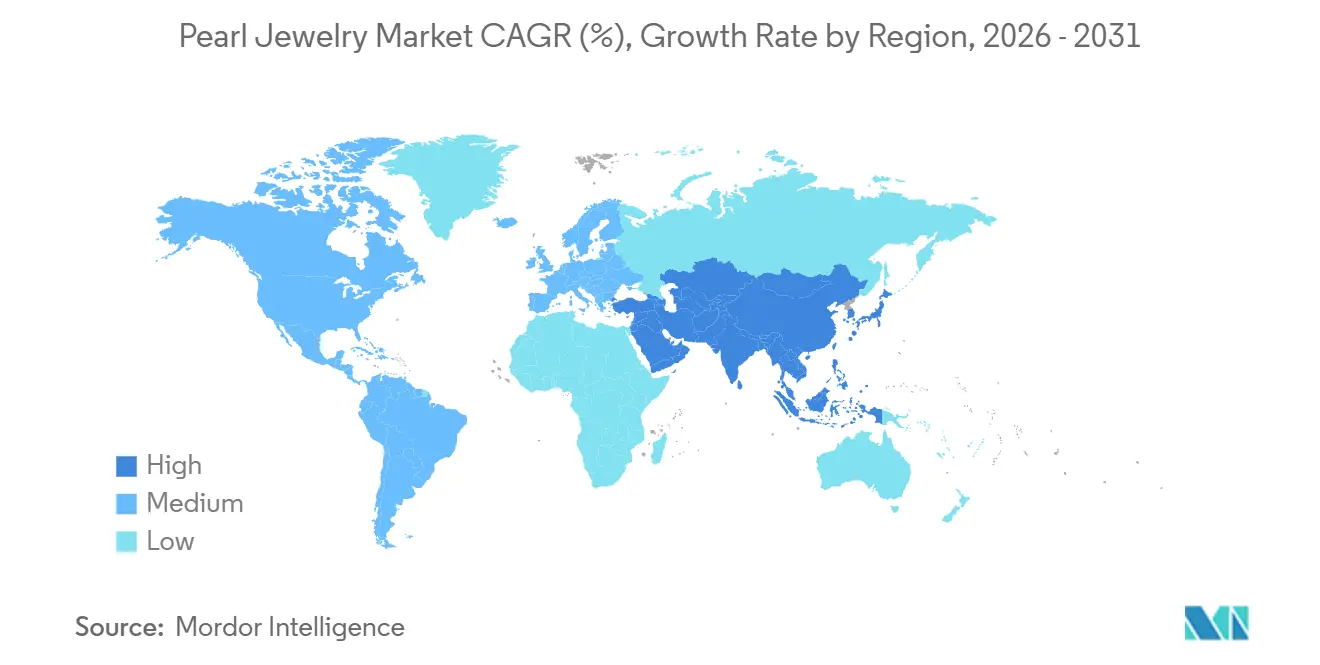

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

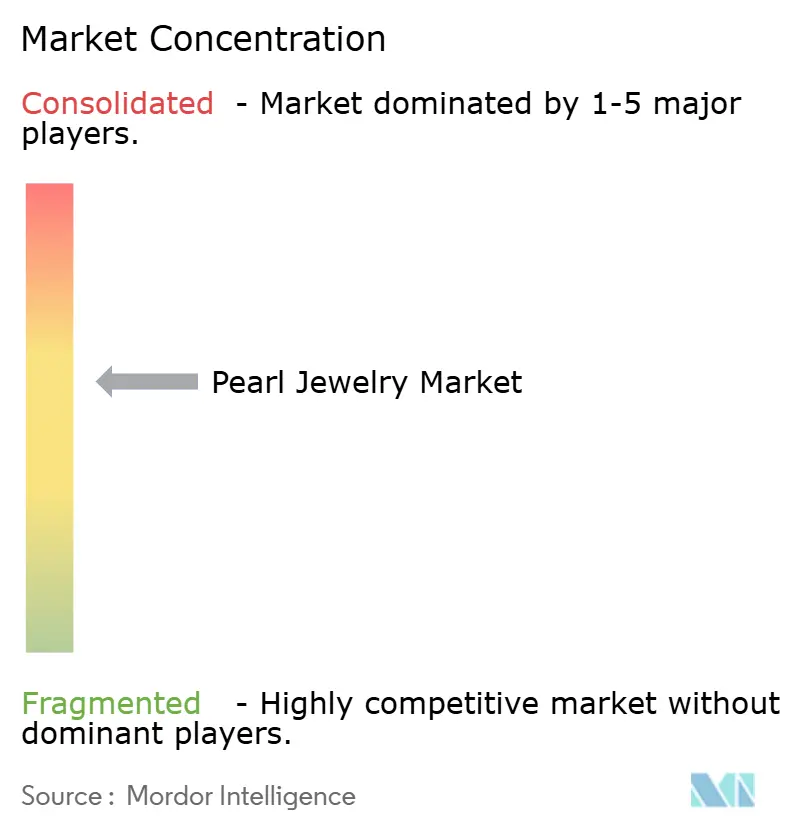

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pearl Jewelry Market Analysis by Mordor Intelligence

The pearl jewelry market size is projected to expand from USD 14.5 billion in 2025 and USD 15.6 billion in 2026 to USD 23.0 billion by 2031, registering a CAGR of 8.1% between 2026 and 2031. The pearl jewelry market is moving away from a narrow occasion-led purchase pattern and is now seen more often as an everyday luxury category with both style and store-of-value appeal. The pearl jewelry market is also benefiting from broader acceptance across casual, workplace, and formal use, as fashion houses, independent designers, and heritage labels keep pearls visible across more wearing occasions. Premium jewelry demand remains firm in 2026, and that supports the pearl jewelry market because consumers are still spending on high-value natural material jewelry despite wider economic pressure. The pearl jewelry market is also seeing stronger value per transaction, as U.S. fine jewelry retail data in 2026 shows higher average pearl ticket sizes and strong gross margins, which point to quality-led spending rather than only volume-led growth, according to the American Gem Trade Association. Verified provenance is becoming more important in the pearl jewelry market, and tools such as NFC certification, expanded grading language, and blockchain-backed authentication are shaping premium demand and future pricing power.

Key Report Takeaways

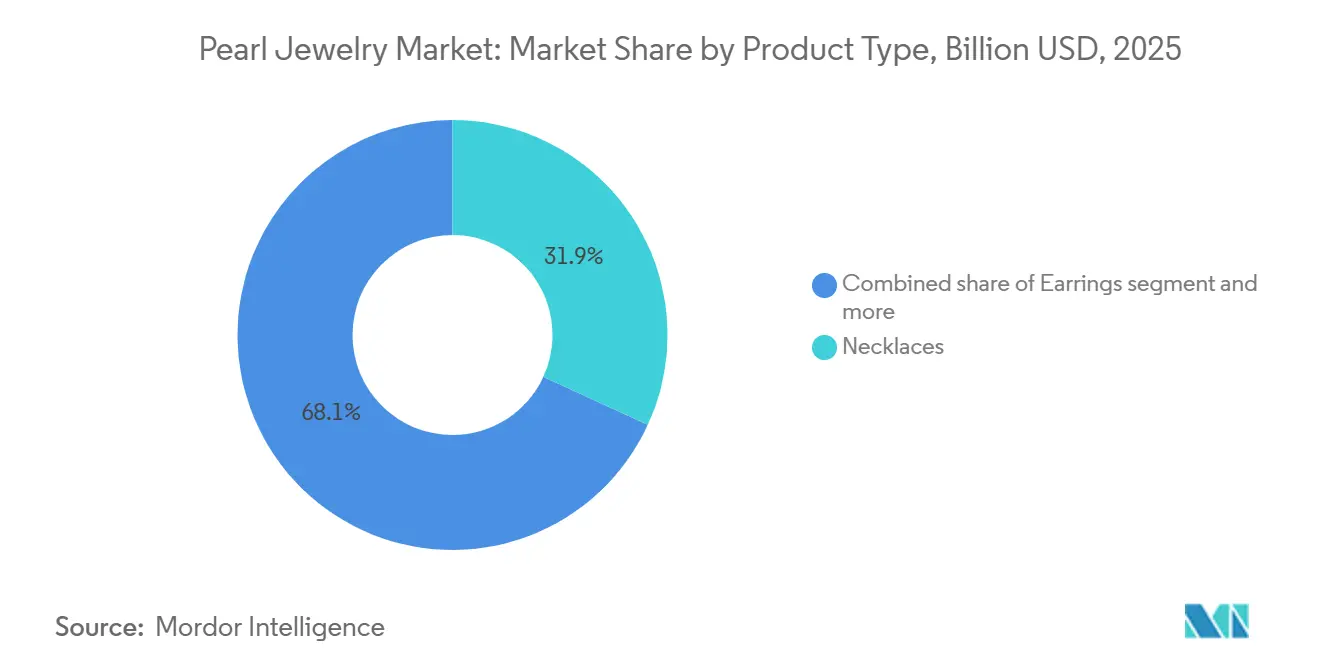

- By product type, necklaces led with 31.86% revenue share in 2025, while earrings are forecast to record the highest CAGR at 8.92% through 2031.

- By pearl nature, cultured pearls held 92.74% share in 2025, while natural pearls are projected to expand at a 9.37% CAGR through 2031.

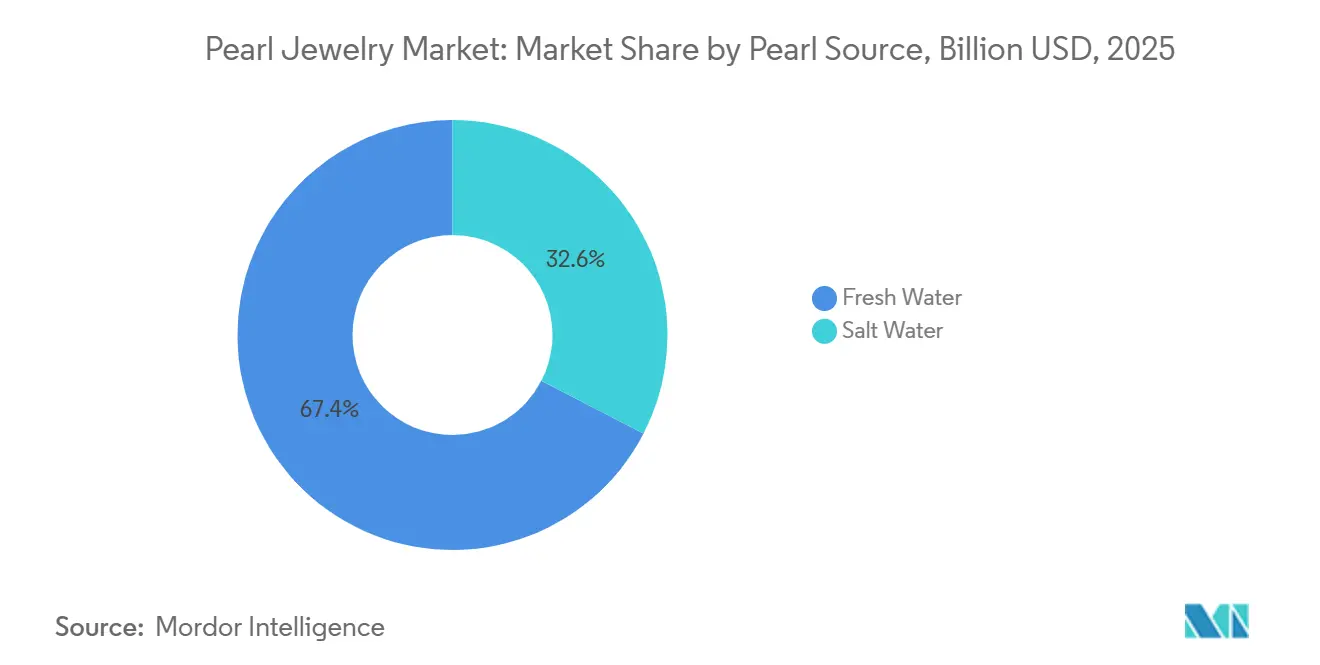

- By pearl source, freshwater pearls accounted for 67.42% share in 2025, while saltwater pearls are projected to grow at a 9.39% CAGR through 2031.

- By material, precious metals represented 72.15% share in 2025, while mixed materials are forecast to advance at a 9.36% CAGR through 2031.

- By distribution channel, offline retail stores held 74.28% share in 2025, while online retail stores are expected to post the fastest CAGR at 10.14% through 2031.

- By geography, Asia-Pacific captured 46.38% share in 2025, while the Middle East and Africa are projected to expand at a 9.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pearl Jewelry Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding use of pearls in contemporary and everyday jewelry collections | +2.2% | Global, concentrated in North America, Europe, and the Asia-Pacific | Medium term (2–4 years) |

| Rising demand for luxury and premium jewelry | +1.9% | Global, most pronounced in the Asia-Pacific and the Middle East | Long term (≥ 4 years) |

| Advancements in pearl cultivation techniques | +1.5% | The Asia-Pacific core (China, Japan, Australia), spills over to MEA | Long term (≥ 4 years) |

| Growth in women's workforce participation and disposable income | +1.2% | Global, high impact in South/Southeast Asia and MEA | Long term (≥ 4 years) |

| Increasing penetration of organized jewelry retail | +0.8% | India, Southeast Asia, the Middle East | Medium term (2–4 years) |

| Increasing demand for freshwater pearls due to cost competitiveness | +0.9% | Global; primary markets in the Asia-Pacific, North America, and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Contemporary design integration broadens pearl's everyday relevance

Pearls are undergoing a design reinvention that is systematically shifting them away from formal-only positioning and expanding demand among younger and more diverse buyer cohorts. TASAKI’s 2026 balance collection, featuring three new interpretations (balance step neo, balance parallel neo, balance arm neo) that integrate sculptural dimensions and architectural lines, shows how premium brands are recasting pearls as daily-wear design statements rather than ceremonial accessories[1]Source: TASAKI, “Balance Collection 2026,” TASAKI, tasaki-global.com. Mikimoto’s 2024 collaboration with Chrome Hearts attracted a notably younger buyer profile and demonstrated that demand for cultured pearl necklace designs is no longer limited to heritage-oriented consumers. This destigmatization of pearl formality is also generating measurable commercial returns. Edge Retail Academy data from nearly 2,000 fine jewelry retailers shows that the average US pearl retail transaction increased by 35% year-on-year in April 2026, with gross profit margins reaching 57.6%. This trend rewards brands that invest in trend-forward, cross-cultural designs over those that rely on legacy formats. The implication is that design diversification, rather than distribution expansion alone, serves as a more direct lever for volume uplift.

Luxury spending resilience elevates pearl's investment positioning

The sustained performance of premium jewelry amid macroeconomic uncertainty creates a structural tailwind for pearls in the upper price tier. Richemont's Jewelry Maisons, comprising Cartier, Van Cleef & Arpels, Buccellati, and Vhernier, are projected to achieve EUR 5.0 billion in operating profit in FY2026 at a 30.5% margin, confirming that natural-material fine jewelry retains pricing power even when broader consumer sentiment weakens. This resilience is also reframing pearls as appreciating assets among consumers. Sri Jagdamba Pearls' Pearl Exchange Program 2026 offers customers 2x appreciation value on sets purchased before April 2025, explicitly positioning pearls as a store of wealth similar to gold. This investment-grade positioning holds particular relevance in markets such as India, the Gulf states, South Asia, and Southeast Asia, where jewelry has historically functioned as portable savings. Brands that communicate provenance, rarity, and value retention alongside aesthetics are best positioned to convert aspiration into transactions in these segments.

Cultivation technology advances compress supply volatility

Pearl aquaculture is integrating biotechnology and precision farming, gradually reducing the yield variability that has historically triggered supply-side price shocks. In May 2025, the Food and Agriculture Organization of the United Nations will designate China’s Zhejiang Deqing Freshwater Pearl Mussel Composite Fishery System, an 800-year-old integrated aquaculture model, as a Globally Important Agricultural Heritage System (GIAHS), giving Chinese freshwater pearl production international sustainability credentials. At the same time, laboratory research published in Molluscan Research (2025) will demonstrate that silane-coated nuclei significantly improve pearl quality and host mussel survival rates in freshwater cultivation, a technique with meaningful commercial implications for yield consistency at scale. Mikimoto’s IoT-based Kai-lingual monitoring system tracks real-time environmental shifts, including red tides, hypoxia, and temperature anomalies in Akoya oyster habitats, representing the leading edge of precision aquaculture in premium pearl cultivation. Collectively, these advances are reducing the biological unpredictability that has kept supply-side pricing opaque.

Rising female economic participation deepens the core buyer base

Women aged 25–45 represent the primary consumer cohort for pearl jewelry globally, and their expanding economic footprint serves as a structural demand driver that is expected to persist through the forecast period. The International Labor Organization's World Employment and Social Outlook (2025) is expected to document steady gains in female labor force participation across Asia-Pacific and the Middle East since 2020, with South and Southeast Asian markets recording notable increases[2]Source: International Labour Organization, “World Employment And Social Outlook 2025,” ILO, ilo.org. This trend directly expands the income cohort with discretionary spending capacity for luxury purchases. Pearl jewelry offers a relatively accessible entry price compared to diamond or gemstone jewelry, making it well-suited for first-time luxury buyers. Organized retail chains in India, including Malabar Gold and Diamonds, have systematically capitalized on this conversion opportunity through dedicated pearl collections. The emergence of men's pearl jewelry as a nascent sub-category, illustrated by Mikimoto's gender-neutral collaborations, also indicates that the addressable buyer base is expected to expand beyond traditional female demographics during the forecast period.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from diamonds, gemstones, and other precious stones | -0.8% | Global | Long term (≥ 4 years) |

| Long cultivation period and limited production cycles | -0.7% | The Asia-Pacific core (Japan, Australia), spills over to the global supply | Medium term (2–4 years) |

| Limited perception among younger consumers in emerging markets | -0.5% | South America, Africa, South/Southeast Asia | Short term (≤ 2 years) |

| Presence of counterfeit and imitation pearl products | -0.4% | The Asia-Pacific, particularly China and Southeast Asia | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Gemstone competition intensifies at the premium price tier

At the USD 1,000-and-above price point, pearl jewelry faces intensifying substitution pressure from diamonds, rubies, sapphires, and emeralds. These gemstones benefit from stronger consumer aspiration scores and decades of high-profile brand investment in grading transparency. Richemont’s FY2026 performance, with Jewelry Maisons growing 14% at constant exchange rates, led by diamond-set Cartier and Van Cleef & Arpels collections, would illustrate how gemstone-centric designs continue to define the aspirational narrative in prestige jewelry. The challenge is partly structural. While pearls perform well on sustainability and organic origin, they lack the cut-and-clarity grading systems that allow consumers to benchmark value with the same confidence that diamond certification provides. Emerging standards initiatives, including the GIA’s expanded nacre continuity classification (May 2025) and the CIBJO-aligned Global Pearl Development Community’s harmonization work, may narrow this perception gap over time[3]Source: CIBJO, “Pearl Special Report 2025,” CIBJO, cibjo.org. However, repositioning pearls as coequal to diamonds at the top of the prestige hierarchy requires brand investment at a scale currently limited to very few players.

Supply-side vulnerability creates structural production constraints

Pearl cultivation follows an inherent biological timeline that creates supply constraints. Technology investments can moderate these constraints but cannot eliminate them in the short term. Akoya production in Japan has remained suppressed since a 2019 mass die-off of pearl oyster hosts. Rising sea temperatures linked to climate variability have worsened this trend, keeping high-quality Akoya inventory below pre-2019 levels and prompting Mikimoto to implement two rounds of price increases in early 2026. South Sea producers face similar constraints. Australian farms contend with limited viable sites, storm exposure, and cultivation cycles of 2–5 years per pearl, which prevent producers from scaling supply rapidly in response to demand surges. Supply volatility also disproportionately affects smaller retailers and independent designers that lack the inventory depth to absorb price shocks. This dynamic may accelerate market consolidation toward vertically integrated players such as TASAKI, which operates wholly owned pearl farms and insulates itself from spot market pricing. Regulatory influence from sustainable aquaculture frameworks, including emerging FAO GIAHS standards, may further tighten production norms, particularly for producers in environmentally sensitive marine zones.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Earrings Accelerate as Necklaces Anchor the Portfolio

Among all product types, necklaces are expected to hold the largest share, at 31.86%, in 2025. Their leadership reflects their enduring association with premium gifting, formal occasions, and iconic cultured pearl necklace formats popularized by Japanese heritage brands. Classic Akoya pearl choker strands, particularly in 6–8 mm sizes, remain the highest-value products within this segment and generate strong repeat purchases among affluent buyers across Asia-Pacific and the Gulf. Earrings are projected to be the fastest-growing product type, registering an 8.92% CAGR from 2026 to 2031, as the normalization of hybrid work environments increases demand for everyday pearl accessories with lower formality cues. TASAKI's 2026 balance collection is expected to lead with earring designs (balance arm neo), reflecting the brand's view that design-driven demand is concentrating in ear-wear formats suited for daily use.

Rings, chains, pendants, and bracelets each serve distinct sub-segments. Rings are gaining traction in bridal markets, particularly in Asia-Pacific and South America, while pendants and bracelets support the layering trend prevalent among millennial and Gen Z buyers. Pandora's incorporation of baroque freshwater pearls into statement pendant designs illustrates how accessible luxury brands use pearls to elevate perceived product value without moving away from their core price architecture. Novelty formats, including baroque pearl brooches, hair accessories, and body jewelry, attract collector interest in premium markets and widen the category's reach without competing directly with established product formats.

By Pearl Nature: Cultured Pearls Dominate; Natural Pearls Reassert a Rarity Premium

Cultured pearls are expected to account for a 92.74% share in 2025, reflecting the near-complete displacement of natural pearls in consumer markets. Decades of Japanese aquaculture refinement and certification frameworks, such as the Japan Pearl Science Laboratory and GIA nacre grading, now give cultured varieties comparable prestige in most retail contexts. This dominance reflects supply economics and consumer education. Cultured pearls are available in consistent quality tiers across freshwater and saltwater types, enabling brands to develop scalable product lines with predictable margin profiles. However, natural pearls are expected to be the fastest-growing segment, registering a 9.37% CAGR from 2026 to 2031. This counterintuitive trend is driven by rarity-led investment demand and provenance-based storytelling among ultra-high-net-worth buyers.

The Gulf states are expected to represent the strongest expression of this demand. In April 2025, Bahrain's DANAT Institute, in partnership with Arabian Gulf University, is set to launch a two-year project to study the impact of climate change on Gulf pearl oyster beds. This initiative underscores rising institutional concern about the viability of natural pearl supply and the resulting rarity premium that such scarcity is likely to command. The Onegemme–Provenance Proof blockchain partnership (2024) enables single-origin natural pearl authentication by verifying whether a pearl originated in specific Gulf or Australian waters. This directly serves top-tier buyers who demand auditable traceability. As natural pearl supply remains constrained by biology and environmental degradation, their investment-grade positioning relative to cultured pearls is likely to strengthen through 2031.

By Pearl Source: Freshwater Pearl Jewelry Scales in Volume; Saltwater Commands the Premium

Freshwater pearl jewelry is expected to dominate by source, with a 67.42% share in 2025, supported by China’s large production base, which accounts for approximately 95% of global freshwater pearl output, and the segment’s broad price accessibility for mid-market buyers. The freshwater segment’s quality trajectory remains notable. Y&M Pearls’ planned 2025 launch of the Lunastra (certified gem-grade white) and Splendora (top-quality white and colored) collections, verified by Japan Pearl Science Laboratory and equipped with NFC-chip traceability, indicates that the quality gap between freshwater and saltwater pearls is narrowing faster than many trade buyers recognize. The GIA’s expanded nacre continuity scale, expected to be introduced in May 2025 as an addition to its 7 Pearl Value Factors, is set to provide premium freshwater producers with a standardized quality framework to support higher price points and reinforce compliance with international pearl valuation standards.

Saltwater pearl jewelry is projected to be the fastest-growing source segment, registering a 9.39% CAGR from 2026 to 2031, supported by persistent rarity premiums and the expanding reach of the luxury market. The Japan Pearl Exporters’ Association expects Japan’s pearl export value to reach approximately JPY 41.2 billion in 2025, exceeding its JPY 37.9 billion target, with more than 80% of exports routed through Hong Kong to the Chinese market. The Association’s 2026 strategy explicitly targets Europe, North and South America, and India for marketing expansion through the “Book of Akoya” initiative, curated by trend forecaster Paola De Luca. This approach reflects institutional recognition that overdependence on the Chinese market creates systemic risk. At the same time, supply constraints on high-quality Akoya and South Sea pearls are strengthening the competitive advantage of producers with secure farm access, favoring vertically integrated players.

By Material: Precious Metals Anchor the Market; Mixed Materials Define the Next Design Cycle

Precious metals are expected to account for a 72.15% material share in 2025, supported by the cultural prestige of gold and platinum settings across the market’s largest geographies, particularly India, China, and the Gulf states. In these markets, precious metal settings carry independent value beyond the mounted gem. Mikimoto’s high-jewelry line, including the Les Petales Place Vendome Roses collection featuring 18K pink gold with Akoya cultured pearls and diamonds, shows how the choice of precious metal strengthens brand positioning and enables price premiums in the luxury tier. Base metals serve the fashion and mid-market segments, typically through sterling-silver settings that support lower retail price points while preserving a premium visual aesthetic. These segments remain commercially important for brands operating across multiple price tiers.

Mixed materials are projected to be the fastest-growing segment, registering a 9.36% CAGR from 2026 to 2031. Contemporary design trends that pair pearls with resin, rubber, textiles, and multi-metal components are driving this growth. The commercial rationale remains strong: mixed-material settings reduce precious metal input costs, allowing brands to reinvest in pearl quality while maintaining accessible retail price points. This approach broadens the consumer base beyond core premium demographics. Pandora’s development of platinum-plated PANDORA EVERSHINE for everyday pearl-integrated jewelry demonstrates this strategy in the accessible luxury tier. Across all material categories, rising gold prices represent a structural cost challenge. This factor is expected to push Richemont’s Jewelry Maisons to implement measured price increases in FY2026 and accelerate brand interest in material substitution and mixed-material experimentation.

By Distribution Channel: Offline Retail Maintains Leadership; Online Commerce Accelerates

Offline retail stores are expected to account for a 74.28% market share in 2025, reflecting consumers’ continued preference for in-store purchases when buying high-value pearl jewelry. Buyers often rely on tactile assessment of luster, nacre depth, and string quality, which digital channels cannot easily replicate. Heritage brands are increasing investments in boutique retail. Mikimoto’s planned opening of its second Singapore boutique at Takashimaya in January 2026, a 1,943 sq. ft. space that is more than twice the size of its original Marina Bay Sands store, signals the brand’s confidence that premium physical environments generate measurable brand premiums and support high-value conversions. Luxury jewelry stores and specialty pearl retailers continue to record the highest per-unit transaction values, supported by in-person authentication and certification services that strengthen buyer confidence for purchases exceeding USD 500.

Online retail stores are expected to be the fastest-growing channel, registering a 10.14% CAGR from 2026 to 2031, as digital platforms expand access to authenticated pearl jewelry across geographies. Freshwater pearl producers in Zhuji and Shanxiahu actively sell through TikTok, Amazon, and AliExpress, using overseas warehouses to reduce delivery lead times for US and European consumers while bypassing traditional wholesale intermediaries. Augmented reality try-on tools, AI-driven personalization, and NFC-enabled product authentication, such as those deployed by Y&M Pearls in 2025, are expected to reduce the friction that has historically limited online pearl sales to lower price points. C&K Group’s planned US IPO filing in February 2026, with 40% of net proceeds earmarked for strategic acquisitions and 10% for brand marketing, reflects the capital appetite among digital-forward pearl traders seeking to capture growth in this channel.

Geography Analysis

Asia-Pacific is expected to hold the largest regional share, accounting for 46.38% of the global pearl jewelry market in 2025. This position is supported by China’s role as the world’s leading freshwater pearl producer and a fast-growing luxury consumer market. Chinese government data shows that annual pearl sales in Zhuji exceeded RMB 50 billion (~USD 6.98 billion) in 2024, with the city producing 600 tonnes of freshwater pearls, representing approximately 70% of global output. Japan strengthens the region’s premium positioning in Akoya pearls, with pearl exports expected to reach approximately JPY 41.2 billion in 2025, exceeding the annual target. However, Akoya supply constraints and yen weakness are creating both a pricing premium and a need for geographic diversification away from the Hong Kong–China corridor. India and Southeast Asian markets, including Indonesia, Thailand, and Singapore, are emerging as high-growth sub-regions, where rising affluence and increasing brand awareness are expanding pearl jewelry’s reach beyond traditional gifting into everyday fashion. Mikimoto’s planned boutique expansion in Singapore in January 2026, its second location in the city-state, reflects the strategic view that Southeast Asian affluent consumers represent an underpenetrated growth opportunity.

North America and Europe represent large, mature markets, where average transaction value expansion, rather than unit volume growth, defines the market trend. US fine jewelry retailers are expected to report a 21% year-on-year increase in pearl sales in April 2026, with average retail prices rising 35% to USD 444 and gross margins reaching 57.6%, indicating a clear premiumization trend. European demand remains concentrated in Italy, France, Germany, and the United Kingdom, where pearl jewelry’s heritage positioning aligns with the region’s preference for artisanal craftsmanship and provenance-verified products. The Japan Pearl Exporters’ Association is expected to expand marketing in Europe and the Americas in 2026 through the Paola De Luca-curated “Book of Akoya” project, positioning Akoya pearl jewelry as an alternative to diamond pieces across the mid-premium and luxury tiers. Canada and Mexico remain smaller but developing markets, benefiting from proximity to US retail trends and rising luxury consumption among aspirational middle-class consumers.

The Middle East and Africa are expected to be the fastest-growing geographies, registering a CAGR of 9.21% from 2026 to 2031. The UAE and Saudi Arabia are expected to lead regional growth, supported by culturally embedded pearl heritage. Bahrain and the wider Gulf were historically among the world’s most important natural pearl sources, creating strong consumer receptivity to pearl jewelry narratives. The Gulf’s gifting culture, particularly during Eid, wedding seasons, and royal gifting occasions, sustains high-value pearl transactions throughout the year, with bridal pearl sets commanding price points that rival mid-tier diamond jewelry. Compliance frameworks enforced by the UAE’s Emirates Authority for Standardization and Metrology, which mandates jewelry hallmarking standards, strengthen product authenticity and support premium pricing, benefiting established international brands with certified provenance. South America remains a smaller contributor, with Brazil, Argentina, and Colombia serving as primary nodes. Growth remains constrained by lower per capita luxury spending and limited organized pearl retail, although the long-term demographic opportunity remains meaningful as middle-class affluence rises. Sub-Saharan Africa, outside South Africa, remains nascent and is largely driven by import activity rather than established retail channels.

Competitive Landscape

The pearl jewelry market operates in a two-tiered structure: a consolidated premium layer led by Japanese heritage brands (Mikimoto, TASAKI, Kojima Pearl) and Australian luxury producers (Paspaley, Autore Group, Kailis Group), and a fragmented mid-market comprising retail conglomerates (Malabar Group, Chow Tai Fook, Luk Fook Holdings) that include pearls within broader jewelry portfolios. Vertical integration remains the clearest strategic differentiator. TASAKI strengthens its supply chain transparency narrative through wholly owned pearl farms, traceable diamond sourcing, and green packaging, creating a positioning that competitors dependent on third-party cultivation cannot easily replicate. Several players are targeting younger consumers through design reinvention (TASAKI’s balance series), celebrity ambassador programs (Mikimoto’s appointment of regional brand ambassadors in Southeast Asia, January 2026), and cross-category collaborations, intensifying brand differentiation at the premium tier.

In the mid-market, DTC digital channels are disrupting traditional models. Chinese freshwater pearl producers selling directly through TikTok Live and Amazon are compressing margins for traditional wholesale intermediaries and regional specialty retailers that lack direct digital reach. A patent filed under the CIBJO framework for pearl provenance systems (the Onegemme–Provenance Proof partnership, 2024) shows how blockchain-based authentication is becoming a strategic asset that brand leaders aim to secure before it becomes table stakes. White space exists across several underserved areas, including men’s pearl jewelry (nascent but gaining commercial validation through Mikimoto’s gender-neutral collaborations), mid-premium freshwater pearl jewelry with NFC-based provenance assurance, and dedicated pearl retail infrastructure in Gulf and Indian bridal segments where international brands have limited specialized presence.

The September 2025 launch of the Global Pearl Development Community to harmonize production standards and sustainability metrics may accelerate consolidation by raising compliance costs for smaller producers, effectively narrowing the competitive field over the medium term. C&K Group’s February 2026 US IPO filing, which allocates 40% of proceeds to strategic acquisitions across Asian markets, reflects the merger and acquisition rationale gaining traction among mid-tier players that lack the organic scale to compete with integrated market leaders. Technology adoption, including IoT farm monitoring, blockchain provenance, and AI-driven virtual try-on, increasingly separates market leaders from followers, as premium-tier consumers now expect digital quality verification as a precondition for high-value purchases.

Pearl Jewelry Industry Leaders

Mikimoto & Co., Ltd.

TASAKI & Co., Ltd.

LVMH Moët Hennessy Louis Vuitton SE

Compagnie Financière Richemont SA

Pandora A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: TASAKI unveiled three new interpretations of its balance collection

- for 2026: balance step neo, balance parallel neo, and balance arm neo. The designs incorporate yellow gold and white gold pavé and draw inspiration from the image of two hands meeting. This launch supports TASAKI’s strategy to reposition pearls as contemporary architectural objects suited for professional daily wear, directly targeting design-driven demand among consumers aged 25–45.

- May 2026: Sahyadri Pearls (India) launched a premium freshwater pearl jewelry collection cultivated entirely by Indian farmers, presented at a public launch event in Navi Mumbai. The launch marks a significant milestone in India's emergence as an integrated freshwater pearl cultivation-to-retail market, reducing dependence on imported Chinese pearl inputs.

- January 2026: Mikimoto opened its second Singapore boutique at Takashimaya Shopping Center (391 Orchard Road), a 1,943 sq ft space more than double the size of its original 2013 Marina Bay Sands store. The boutique showcases Mikimoto's full fine and high jewelry collections, including the Les Petales Place Vendome Roses line, and was launched with global brand ambassadors Freen Sarocha and Song Weilong in attendance.

Global Pearl Jewelry Market Report Scope

Pearl jewelry refers to any ornament, such as necklaces, earrings, rings, or bracelets, that features natural or cultured pearls as its primary design element. The global pearl jewelry market is segmented by product type, pearl nature, pearl source, material, distribution channel, and geography. By product type, the market is segmented into necklaces, earrings, rings, chains, pendants, bracelets, and other product types. By pearl nature, the market is segmented into natural and cultured. By pearl source, the market is segmented into freshwater and saltwater. By material, the market is segmented into precious metals, base metals, and mixed materials. By distribution channel, the market is segmented into offline retail stores and online retail stores. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Necklaces |

| Earrings |

| Rings |

| Chains and Pendants |

| Bracelets |

| Other Product Types |

| Natural |

| Cultured |

| Fresh Water |

| Salt Water |

| Precious Metals |

| Base Metals |

| Mixed Materials |

| Offline Retail Stores |

| Online Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Necklaces | |

| Earrings | ||

| Rings | ||

| Chains and Pendants | ||

| Bracelets | ||

| Other Product Types | ||

| Pearl Nature | Natural | |

| Cultured | ||

| Pearl Source | Fresh Water | |

| Salt Water | ||

| Material | Precious Metals | |

| Base Metals | ||

| Mixed Materials | ||

| Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

Which region leads global demand for pearl jewelry?

Asia-Pacific leads with 46.38% share in 2025, supported by China's production scale, Japan's Akoya heritage, and rising demand across India and Southeast Asia.

Which product format is growing fastest in pearl jewelry?

Earrings are projected to grow fastest at an 8.92% CAGR through 2031, helped by stronger demand for everyday and work-friendly pearl pieces.

Why are freshwater pearls so important to this category?

Freshwater pearls held 67.42% share in 2025 because they combine production scale, price accessibility, and improving quality, especially through the Chinese supply.

What is changing in how premium buyers evaluate pearls?

Premium buyers are placing more weight on provenance, authentication, and grading clarity through tools such as NFC certification, blockchain verification, and expanded nacre classification.

Page last updated on: