Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 112.68 Billion |

| Market Size (2026) | USD 115.58 Billion |

| Market Size (2031) | USD 131.34 Billion |

| Growth Rate (2026 - 2031) | 2.59% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Luxury Goods Market Analysis by Mordor Intelligence

The United States Luxury Goods Market size was valued at USD 112.68 billion in 2025 and is estimated to grow from USD 115.58 billion in 2026 to reach USD 131.34 billion by 2031, at a CAGR of 2.59% during the forecast period (2026-2031). A mature domestic base means the next leg of growth comes from converting younger shoppers and nudging wallet share rather than delivering large-volume jumps. Accessories enjoy higher pricing power than ready-to-wear, while digital convenience, sustainability credentials, and celebrity-fueled visibility collectively expand reach. Competitive intensity remains moderate, anchored by a handful of European groups, yet accessible-luxury players use omnichannel tools to chip away at incumbent share. Persistent counterfeit activity, prime-retail rent inflation, and price-sensitive consumers outside gateway metros temper upside, underscoring the importance of supply-chain control, destination flagships, and differentiated storytelling.

Key Report Takeaways

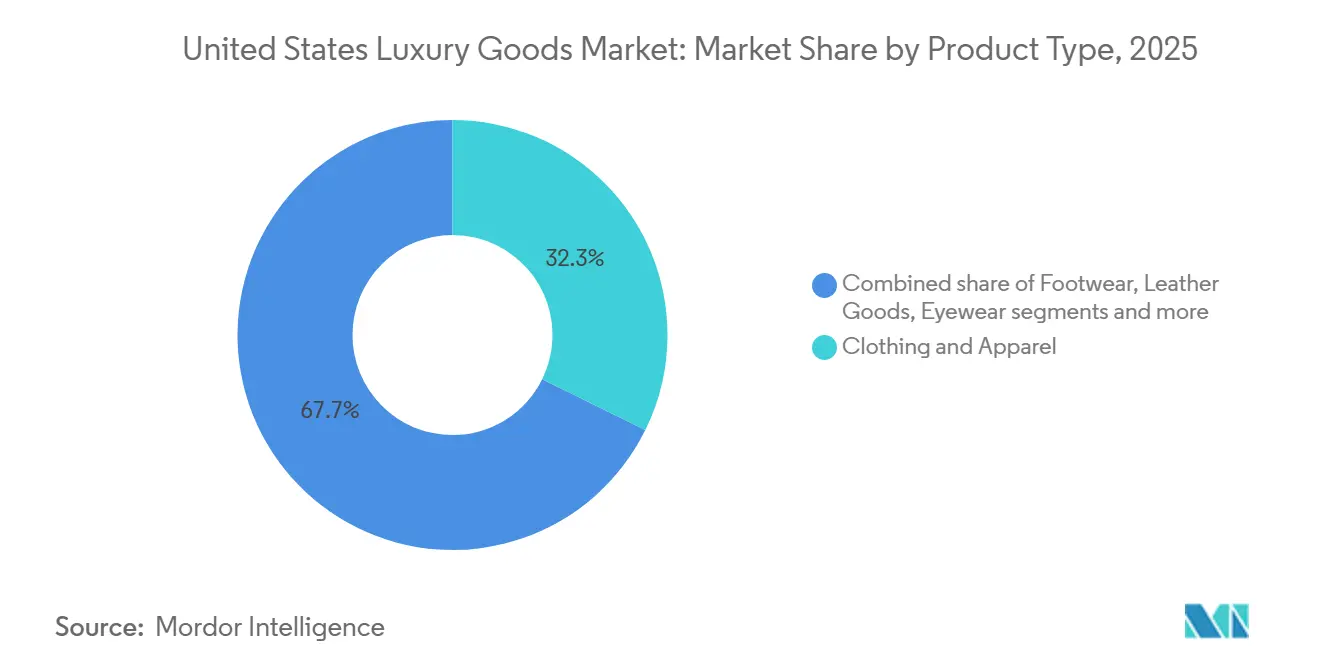

- By product type, clothing and apparel led with a 32.29% market share in 2025, while leather goods are expected to reach a CAGR of 2.76% through 2031.

- By end user, women held a market share of 54.84% in 2025, and the men segment is expected to reach a CAGR of 3.07% during the forecast period 2026-2031.

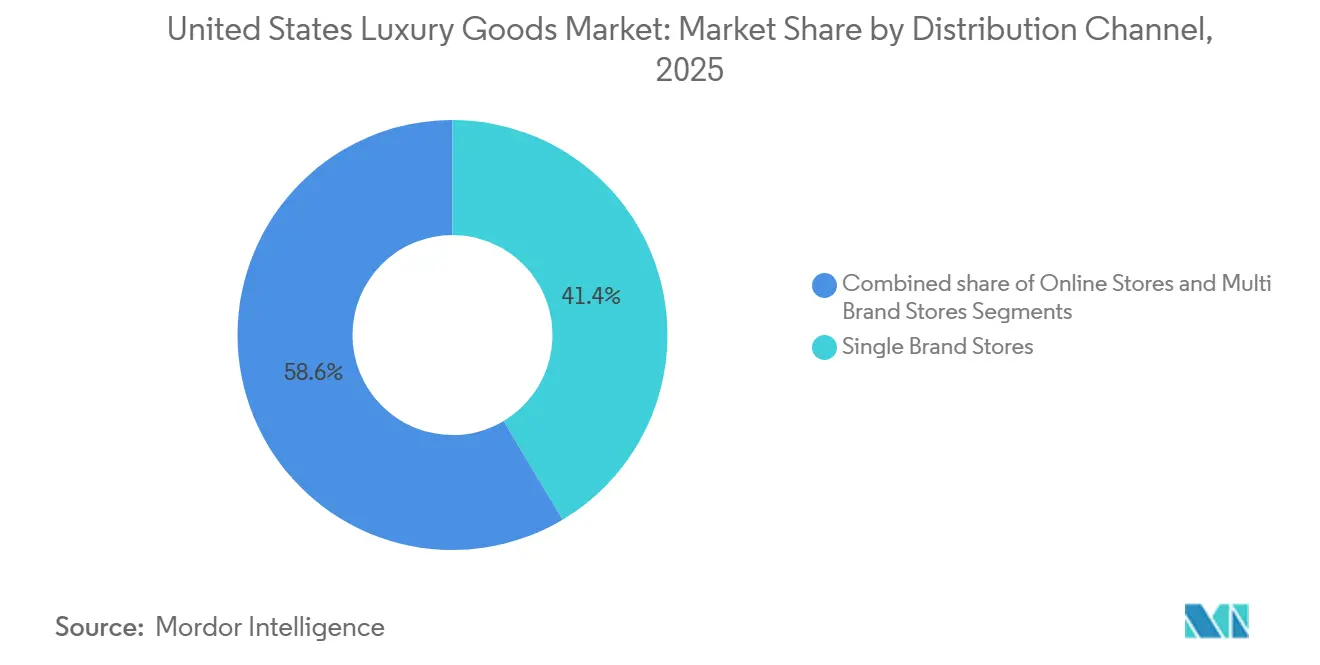

- By distribution channel, single-brand stores hold a market share of 41.44% in 2025, and online stores are expected to reach a CAGR of 3.58% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Luxury Goods Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer emphasis on sustainability | +0.4% | National, with stronger influence in coastal metropolitan areas | Medium term (3-4 years) |

| Influence of social media and celebrity endorsement | +0.6% | National, with higher impact in urban centers | Short term (≤ 2 years) |

| Increasing strategic investment and initiatives propelling the market | +0.5% | National, concentrated in fashion hubs like New York and Los Angeles | Medium term (3-4 years) |

| Product innovation in terms of raw material and design | +0.7% | National, with early adoption in innovation centers | Long term (≥ 5 years) |

| Rising number of high net worth individuals | +0.6% | National, with concentration in financial centers and tech hubs | Medium term (3-4 years) |

| Digital-first luxury purchases by gen Z and millennials | +0.5% | National, with higher adoption in tech-forward metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consumer emphasis on sustainability

Environmental responsibility has become a fundamental business requirement in the US luxury market. Luxury brands are adopting circular economy practices, with companies like Stella McCartney incorporating deadstock fabrics and recycled materials in their high-quality collections to reduce environmental impact. This approach demonstrates the industry's commitment to sustainable practices while maintaining premium quality standards. Moreover, a Stifel survey from October 2023 indicated that 22% of Generation Z and 20% of Millennial consumers in the United States make purchases exclusively from brands demonstrating sustainability practices or value alignment [1]Source: Stifel Financial Corp., “Sustainability Survey Report of Key Findings December 2023”, stifel.com. This purchasing pattern has impacted the U.S. luxury goods market, prompting luxury brands to allocate resources toward ethical sourcing, environmentally friendly materials, and supply chain transparency in order to maintain their market position. For instance, in December 2024, Rolex introduced sustainable packaging for its watches, utilizing plywood and recycled cardboard materials, demonstrating how luxury brands can maintain their premium positioning while embracing environmental stewardship.

Influence of social media and celebrity endorsement

In 2024, Chanel teamed up with Hailey Bieber, while Louis Vuitton featured Zendaya in a 2025 campaign. Both collaborations, launched just 72 hours apart, saw a surge in search intent and conversions, each boasting double-digit percentage increases. In 2024, Swiss watchmakers, who had long relied on print media and sponsorships, made a strategic shift. They turned to TikTok and partnered with creators, leading to limited-edition drops. Collaborations with platforms like Hodinkee resulted in these exclusive items selling out in mere minutes. The influence of social proof on perceived scarcity is undeniable: when a celebrity dons a piece, prices for similar items in the secondary market can jump by 20 to 30 percent. Brands, keenly aware of this dynamic, strategically time their product releases to coincide with red-carpet events and award shows. The 0.3 percentage-point CAGR uplift is notably seen in short-cycle categories, fragrances, cosmetics, and small leather goods, where impulse buying is prevalent, and digital attribution is most accurate.

Increasing strategic investment and initiatives propelling the market

In a bold move, LVMH has pledged over USD 200 million to acquire and revamp Rodeo Drive sites, setting the stage for flagship stores of Tiffany and Louis Vuitton in 2024 and 2025. This investment underscores LVMH's belief in the enduring power of physical retail for brand storytelling and securing high-value sales. Meanwhile, Richemont, with a keen eye on the U.S. market, allocated EUR 865 million (approximately USD 945 million) to retail and manufacturing capital expenditures in fiscal 2024. This move underscores the company's strategic focus on strengthening its domestic infrastructure. In a bid to enhance online order deliveries, Tapestry inaugurated a fulfillment center in Las Vegas in 2024. This initiative not only slashed last-mile costs by 12 percent but also boosted customer satisfaction ratings. Dior, in a strategic move to amplify foot traffic, unveiled its expansive 47,900-square-foot flagship in Beverly Hills in November 2025. Designed by the renowned Peter Marino, the flagship boasts a Monsieur Dior restaurant and exclusive VIP suites, positioning it as a prime destination. The 0.2 percentage-point CAGR contribution is a testament to the dual benefits of new locations: direct revenue and the 'halo effect', where heightened brand visibility in major cities amplifies desirability in secondary markets, drawing consumers eager for flagship experiences.

Product innovation in terms of raw material and design

Product innovation serves as a key differentiator in the US luxury market, as brands utilize advanced materials and design techniques to support premium pricing and appeal to environmentally conscious consumers. Luxury fashion brands are incorporating eco-friendly materials, including mycelium-based leather and organic cotton. This shift toward sustainable materials reflects a broader industry transformation, where environmental responsibility meets luxury craftsmanship. For instance, in October 2023, sustainable luxury footwear brand Koio launched 99% biodegradable shoes. Koio offers a growing collection of carbon-neutral shoes, which are made using leathers from regenerative farms in the Swiss Alps. Moreover, the trend extends beyond materials to product functionality, particularly in the beauty segment, where multi-purpose products are gaining traction as consumers seek value amid increasing living costs. Beauty brands are developing innovative formulations that combine skincare, makeup, and protection benefits in single products. This approach resonates with consumers looking to streamline their routines while maintaining luxury experiences. The convergence of sustainability and functionality in luxury products demonstrates the market's evolution in meeting changing consumer demands while maintaining premium positioning.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of counterfeit products | -0.3% | National, with higher impact in major urban centers | Medium term (3-4 years) |

| Lesser demand from price sensitive consumers | -0.5% | National, with stronger effect in regions with lower disposable income | Short term (≤ 2 years) |

| Escalating rents on prime retail locations | -0.4% | Concentrated in major luxury retail corridors in New York, Los Angeles, and Miami | Medium term (3-4 years) |

| Higher prices and limited accessibility | -0.6% | National, with greater impact on aspirational luxury consumers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Availability of counterfeit products

In fiscal 2024, U.S. Customs and Border Protection (CBP) seized goods with a manufacturer's suggested retail price (MSRP) of USD 5.4 billion, marking a staggering 93% surge from the USD 2.8 billion seized in fiscal 2023. Notably, jewelry constituted a significant portion at USD 1.65 billion, followed closely by watches at USD 1.44 billion, and handbags at USD 1.09 billion. According to CBP, a staggering 90% of the seized counterfeit items, by quantity, originated from China and Hong Kong[2]Source: U.S. Customs and Border Protection, “Intellectual Property Rights Seizure'', cbp.gov. These regions adeptly exploited express-consignment and de-minimis shipment channels, successfully evading traditional cargo screenings. In January 2025, Louisville CBP officers underscored the magnitude of the illicit trade by seizing 28 shipments of counterfeit jewelry, collectively valued at an MSRP of USD 27.5 million. This highlights the scale of counterfeit operations flowing through regional hubs. Further emphasizing the trend, Buffalo Port intercepted 14 counterfeit Rolex watches in July 2025, with a combined value of USD 257,000, spotlighting the allure of high-value items to organized crime networks. The -0.35 percentage-point CAGR drag on the market can be attributed to revenue leakage. Consumers, often unaware, purchase counterfeits either online or through third-party marketplaces, inadvertently diminishing legitimate sales. Moreover, brand dilution occurs as these subpar fakes tarnish the perceived exclusivity of genuine products.

Lesser demand from price-sensitive consumers

In 2024, inflation-adjusted discretionary spending fell by 2.3%, putting pressure on middle-income households. These households have traditionally turned to accessible-luxury brands like Coach and Kate Spade during special moments, according to the U.S. Bureau of Economic Analysis. Tapestry's Kate Spade brand saw a 10% revenue drop in the second quarter of fiscal 2025. This decline was attributed to waning foot traffic in outlet malls and a sense of promotional fatigue among its core customers. Burberry, in 2024, issued a profit warning, pointing to a 15% sales drop in the Americas. The luxury brand noted that price-sensitive shoppers were either postponing purchases or opting for fast-fashion alternatives. Data from the National Retail Federation highlighted a shift in consumer behavior: 18% more shoppers postponed luxury buys in 2024 than in 2023. Many are now prioritizing essential needs and debt repayment over luxury splurges. The impact of a -0.25 percentage-point CAGR is felt most strongly in non-gateway markets. Here, the absence of flagship experiences means brand equity hinges on wholesale distribution. However, this distribution lacks the service differentiation needed to justify premium pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Leather Goods Outpace Apparel Growth

In 2025, the clothing and apparel sector captured 32.29% of the market share, driven by a fusion of casual wear and athleisure that combines luxury with performance. Meanwhile, leather goods, bags, and small leather accessories are on a growth trajectory, expanding at an annual rate of 2.76% through 2031, marking the fastest pace among product categories. Handbags, with their higher average unit retail and frequent repeat purchases, outpace ready-to-wear items. Tapestry's Coach brand celebrated mid-teens average unit retail gains in fiscal 2025, as consumers gravitated towards its signature leather lines. In contrast, Kate Spade faced a 10 percent revenue dip, attributed to its reliance on promotions in the nylon and canvas segments. Jewelry and watches command a notable market presence, underscored by Chopard's Alpine Eagle TimeForArt 2024 edition and Rolex's Land-Dweller 2025, boasting 32 new patents, a testament to how innovation bolsters pricing power. The beauty and personal care sector, spanning fragrances, cosmetics, and skincare, witnessed mid-single-digit growth in 2024 and 2025. This uptick was largely fueled by Estée Lauder's Balmain Beauty debut in August 2024 and Jo Malone's AI Scent Advisor launch in December 2025, both of which curbed return rates and enhanced conversions.

Footwear and eyewear, while holding smaller market shares, showcase unique trends. Tapestry's February 2025 divestiture of Stuart Weitzman for USD 105 million underscores the challenges faced by footwear brands without vertical integration, especially when pitted against conglomerate-backed competitors. Eyewear enjoys the advantage of prescription-driven repeat purchases and licensing deals, enabling brands to profit from their intellectual property without the burden of inventory. However, online disruptors like Warby Parker have introduced margin pressures. Home décor and luxury items cater to a niche audience, primarily ultra-high-net-worth individuals with multiple residences. In 2024, charm bracelets surged in popularity, with Lyst noting a 150 percent spike in search volumes. Dior, capitalizing on the trend, reported a staggering 750 percent increase in charm-related queries, highlighting the potent influence of social media in driving fleeting demand surges.

By End User: Men's Luxury Closes the Gender Gap

In 2025, women accounted for 54.84% of end-user demand, underscoring the historical female skew in categories such as handbags, jewelry, cosmetics, and apparel. However, men's luxury is on the rise, expanding at an annual rate of 3.07% through 2031, outpacing the overall market. This growth is fueled by heightened interest in grooming, athleisure, and tailored casualwear, which command higher average retail prices. Ralph Lauren's Modern Sportswear line, with prices ranging from USD 79.50 for Henley shirts to USD 898 for doeskin blazers, showcases how brands strategically position price points to appeal to both aspirational and affluent male consumers. Meanwhile, Rolex's Land-Dweller 2025 and Patek Philippe's limited-edition releases cater to male collectors who view mechanical watches as a symbol of portable wealth. This segment experienced a 12% growth in 2024, driven by financial market volatility and heightened demand for alternative assets. In the first quarter of fiscal 2026, Tapestry welcomed over 2.2 million new customers globally, with about 35% being Gen Z[3]Source: Tapestry, “Fiscal 2026 Q1 Results”, tapestry.com. Notably, a significant portion of these new male buyers gravitated towards Coach's leather accessories and sneakers.

While unisex offerings remain modest in scale, they play a pivotal role in brand-building, signaling inclusivity and cultural relevance. Moncler's October 2024 collaboration with Rick Owens, featuring gender-neutral silhouettes, sold out in just 48 hours, underscoring the commercial potential of non-binary design. Historically, men's grooming and fragrance lagged behind women's beauty, but the gap is narrowing. Brands like Dior and Tom Ford are launching premium-priced dedicated lines, while Jo Malone's December 2025 introduction of the AI Scent Advisor tailors recommendations for male users, demystifying fragrance counters for those previously hesitant. The 3.07% CAGR for men's luxury is attributed to the expansion of categories like tailored casualwear, sneakers, and tech accessories entering the luxury realm, alongside demographic shifts. Millennial and Gen Z men are now dedicating a larger portion of their discretionary spending to personal appearance than earlier generations.

By Distribution Channel: Online Gains Share from Physical Retail

In 2025, single-brand stores accounted for 41.44% of the distribution landscape, utilizing immersive environments and exclusive product offerings to justify their premium pricing. However, online channels, propelled by Gen Z and millennial shoppers, are on a growth trajectory, advancing at an annual rate of 3.58% through 2031. Dior's flagship store in Beverly Hills, spanning 47,900 square feet and inaugurated in November 2025, boasts a Monsieur Dior restaurant and private VIP suites, elevating the venue to a hotspot for foot traffic and social media buzz. In October 2025, Hermès unveiled a new U.S. store, curating exclusive product allocations for high-net-worth individuals that aren't available through wholesale or online channels, highlighting the strategic importance of controlled distribution. Meanwhile, multi-brand outlets, including department giants like Saks and Neiman Marcus, grapple with structural challenges. Despite Saks Global's ambitious USD 2.7 billion takeover of Neiman Marcus in 2024, aimed at consolidating buying power and trimming redundant overheads, both chains sounded alarms of financial distress in December 2025, citing dwindling foot traffic and squeezed wholesale margins.

Tapestry reported a robust high-teens percentage surge in digital revenue for fiscal 2025, with Coach's handbag lineup playing a pivotal role, bolstered by dynamic pricing and tailored recommendations. Estée Lauder's foray into Amazon's Premium Beauty store in October 2024, featuring virtual try-ons and same-day delivery in select metros, is successfully siphoning customers from traditional department-store counters, which can't match that level of convenience. Ralph Lauren, during its Investor Day 2025, unveiled ambitions to amplify a digitally-centric ecosystem across the top 30 U.S. cities. They recognized that existing geographic voids limit growth potential and emphasized the importance of omnichannel strategies, such as 'buy online, pick up in store' and virtual appointments, to seamlessly merge the physical and digital realms. The projected 3.58% CAGR for online platforms is a testament to evolving customer preferences for 24/7 access, diverse product assortments, and smooth checkouts, coupled with operational efficiencies stemming from scaling fulfillment costs and maturing last-mile networks.

Geography Analysis

In fiscal 2024, Richemont identified the U.S. as its leading revenue source, underscoring the nation's significance as the primary market for many European luxury giants. The conglomerate further solidified its commitment by allocating approximately USD 945 million to retail and manufacturing capital expenditures, thereby bolstering its domestic infrastructure. Los Angeles is eclipsing New York City as the favored site for inaugural U.S. outlets, spurred by the 2028 Olympics and lower occupancy rates than on Fifth Avenue. LVMH's strategic investment of over USD 200 million to acquire and revamp Rodeo Drive sites for Tiffany and Louis Vuitton flagship stores in 2024 and 2025 highlights this westward momentum. Despite Beverly Hills rents soaring to USD 960-1,200 per square foot in 2025, brands deem the locale vital for narrative-building and high-value sales. Esteemed names like Givenchy, Cartier, Patek Philippe, and Rolex are either expanding or renovating their stores on Rodeo Drive. Savills' Global Luxury Retail 2024 report highlighted a 12 percent uptick in North American store openings compared to 2022, with cities in the Sun Belt, including Miami, Dallas, and Phoenix, reaping the lion's share, thanks to an influx of affluent retirees and remote workers from high-tax states.

While New York City holds its symbolic stature, foot traffic in its flagship areas dipped by 8% in 2024. This decline, attributed to organized retail crime and shifts in remote work, diminished both tourist and commuter presence, as reported by the National Retail Federation. Rents on Fifth Avenue surged by 12 percent year-over-year in 2024. In response, brands like Saks consolidated their operations, shuttering underperforming outlets. Meanwhile, Target ventured into SoHo in 2024, experimenting with urban-format stores. This move underscores New York's status as a testing ground for omnichannel retailing, even among mass-market players. Miami's Design District has solidified its position as a luxury nexus. Flagship stores from Hermès, Louis Vuitton, and Dior cater not only to Latin American tourists but also to domestic clientele enticed by Florida's tax benefits. Las Vegas, long synonymous with outlet shopping, is now embracing full-price luxury. Tapestry, in a bid to enhance online order deliveries, inaugurated a fulfillment center in 2024, achieving a 12 percent reduction in last-mile costs.

Residents in mid-tier cities like Phoenix, Charlotte, and Nashville find themselves without flagship stores from most European luxury brands. This absence compels them to either journey to major metropolitan areas or shop online, often missing the in-person experience and consequently seeing a 25 to 30% dip in conversion rates. Ralph Lauren, during its Investor Day 2025, spotlighted this market gap. The brand unveiled a three-year blueprint to cultivate a digitally-driven ecosystem across the top 30 U.S. cities, with plans to explore an additional 20, harnessing data analytics to pinpoint promising markets. Despite gateway metros, which account for 65% of luxury revenue, housing only 25% of the affluent populace, presenting lucrative opportunities in secondary markets, challenges like high occupancy costs and intricate logistics dampen the enthusiasm for many brands.

Competitive Landscape

The U.S. luxury goods market is moderately concentrated, with major players such as LVMH, Kering, Richemont, Chanel, and Hermès dominating it. This concentration leaves opportunities for accessible-luxury brands like Tapestry and mid-tier specialists, who are leveraging omnichannel strategies and data-driven planning to carve out their share. Kering faced a 15% revenue dip in Q3 2024, with Gucci plummeting 26%. This downturn underscores the risks of brand fatigue and the consequences of delayed creative updates, even in a burgeoning market. In contrast, Tapestry's Coach brand thrived, boasting double-digit revenue growth in fiscal 2025 by appealing to Gen Z and millennials with its leather accessories and sneakers.

Strategic maneuvers are evident: LVMH bolsters its retail presence with acquisitions on Rodeo Drive, while Richemont's EUR 265 million (around USD 290 million) buyout of Gianvito Rossi in fiscal 2024 underscores a push for tighter control over supply chains and retail spaces. Digital initiatives are also a focus, as seen with Estée Lauder's Amazon Premium Beauty store and Ralph Lauren's digital ecosystem strategy, both aimed at countering direct-to-consumer threats. There's untapped potential in men's grooming, lagging 40 percentage points behind women's beauty in market penetration, and in home décor. The latter, while appealing to ultra-high-net-worth individuals with multiple residences, remains largely overlooked by many fashion brands.

New entrants are capitalizing on sustainability and transparency: In July 2024, Uncaged Innovations secured USD 5.6 million in seed funding to expand its plant-based leather alternatives, posing a challenge to traditional tanneries supplying European giants. Adoption of technology is inconsistent across the board; Rolex's 32 patents for the Land-Dweller 2025 highlight how mechanical advancements can bolster pricing power. Meanwhile, Jo Malone's AI Scent Advisor and Estée Lauder's virtual foundation tool showcase the potential of digital innovations, not as replacements, but as enhancements to traditional in-person services by reducing return rates and boosting conversions. New regulations, like the FDA's 2024 Modernization of Cosmetics Regulation Act, mandate registration and adverse-event reporting. Such requirements tend to benefit larger entities with established compliance infrastructures, inadvertently sidelining smaller indie brands and further consolidating market share among industry stalwarts.

United States Luxury Goods Industry Leaders

LVMH Moët Hennessy Louis Vuitton

Kering SA

Compagnie Financière Richemont SA

Chanel Limited

Hermès International SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Tacori launched a branded luxury shop-in-shop concept at 15 authorized retail partner locations. This initiative delivers an exclusive retail environment designed to showcase the brand's jewelry collections.

- November 2024: Louis Vuitton opened a new flagship store in New York. The new store is a five-story-tall, multi-faceted, immersive space. The products include clothes, watches, food products, and many others.

- April 2024: Gucci, a luxury brand, expanded its presence in the United States by opening a sprawling boutique in Southern California. The boutique has an area of 17,500 square feet, and it offers men's clothes, shoes, accessories, and other items. The store also offers handbags, fine jewelry, and women's clothing.

- January 2024: Prada officially launched Prada Beauty in the U.S. The new skincare line offers a comprehensive range, from cleansers to foundations. Notably, the products incorporate Prada's innovative “Adapto.gn Smart Technology,” a multi-potent complex designed to help skin adapt to its environment in real-time.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States luxury goods market as the value of personal premium items (designer apparel, leather accessories, fine jewelry, watches, prestige cosmetics, and upscale eyewear) sold to consumers inside the country.

Scope Exclusion: Automobiles, yachts, private aviation, hospitality, and real estate are excluded so the focus remains strictly on tangible personal goods.

Segmentation Overview

- By Product Type

- Clothing and Apparel

- Footwear

- Leather Goods (Bags and Small Leather Accessories)

- Jewelry

- Watches

- Beauty and Personal Care (Fragrances, Cosmetics, Skincare)

- Eyewear

- Home Décor and Fine Living Items

- By End User

- Women

- Men

- Unisex

- By Distribution Channel

- Single Brand Stores

- Multi-Brand Stores

- Online Stores

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured calls with brand commercial heads, boutique managers, luxury e-tail executives, and affluent shoppers in New York, Miami, Dallas, and Los Angeles. These conversations clarified parallel-import leakage, validated average ticket values, and stress-tested our online channel share before assumptions were locked.

Desk Research

We compiled public datasets from the U.S. Bureau of Economic Analysis, Census Monthly Retail Trade, International Trade Commission shipment codes, Federal Reserve consumer-finance surveys, and trade groups such as the Jewelers Board of Trade. Company 10-Ks, investor decks, and curated news streams from Dow Jones Factiva and D&B Hoovers added brand volumes and average selling prices. The sources listed are illustrative, and many additional references guided data collection and cross-checks.

Market-Sizing & Forecasting

We applied a top-down income-band demand pool that multiplies households earning above a specified threshold by luxury spend propensity. We then reconciled it with sampled brand revenue roll-ups and flagship store footprints. Key drivers include inbound tourist spending, SKU-level price inflation, e-commerce penetration, and gray-market leakage. A multivariate regression on these variables supports the outlook for the forecast period, while scenario overlays capture tariff or tax shocks.

Data Validation & Update Cycle

Outputs undergo peer review, variance checks against Federal Reserve card-spend dashboards, and management sign-off. Figures refresh every year, and interim updates follow material events, with a final sweep just before delivery.

Why Mordor's US Luxury Goods Baseline Commands Reliability

Published estimates often diverge because some studies mix services, use outdated prices, or freeze models for years. We revise scope annually, update prices city-by-city, and validate with both desk and primary inputs, giving decision-makers a dependable yardstick.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 112.68 B (2025) | Mordor Intelligence | - |

| USD 67.9 B (2024) | Regional Consultancy A | Excludes online resale and uses a lower prestige price floor. |

| USD 66.44 B (2024) | Global Consultancy A | Relies on limited customs codes and omits the beauty segment. |

| USD 106.97 B (2024) | Trade Journal B | Uses wholesale values rather than consumer-level sales. |

Different scopes, channels, and refresh cadences create wide swings in totals, whereas Mordor's disciplined variable set and yearly validation keep our baseline balanced, transparent, and ready for confident decision-making.

Key Questions Answered in the Report

How large is the United States luxury goods market today?

It generated USD 115.58 billion in 2026 and is forecast to rise to USD 131.34 billion by 2031 at a 2.59% CAGR.

Which product segment is growing fastest?

Leather goods are pacing at a 2.76% CAGR through 2031, outstripping apparel.

Why is men’s luxury important?

Men’s categories grow at a 3.07% CAGR, faster than the overall market, driven by grooming, sneakers, and tech-infused apparel.

How big is the counterfeit problem?

CBP seized USD 5.4 billion worth of fake luxury items in fiscal 2024, up 93% year over year.

What share did single-brand stores hold in 2025, and how fast are online sales growing?

Single-brand stores held 41.44% of sales in 2025, and online store sales are expanding at 3.58% annually through 2031.

Page last updated on: