Luxury Watch Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 84.77 Billion |

| Market Size (2031) | USD 114.19 Billion |

| Growth Rate (2026 - 2031) | 6.14% CAGR |

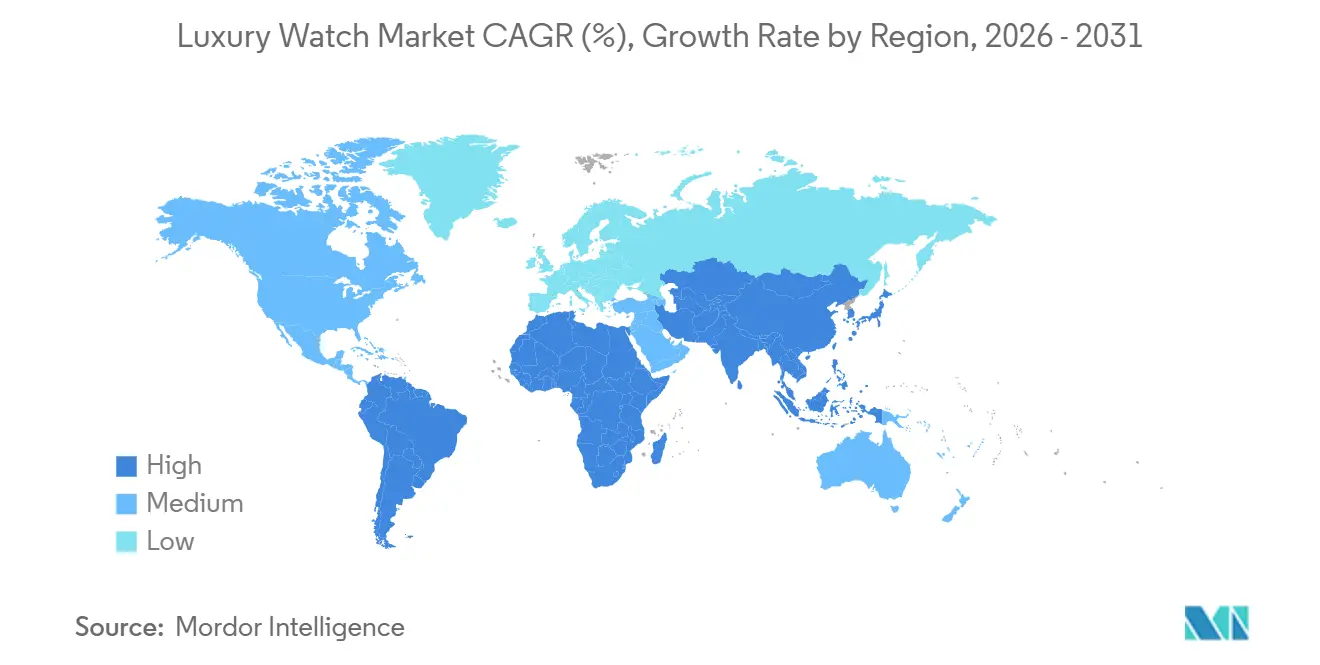

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

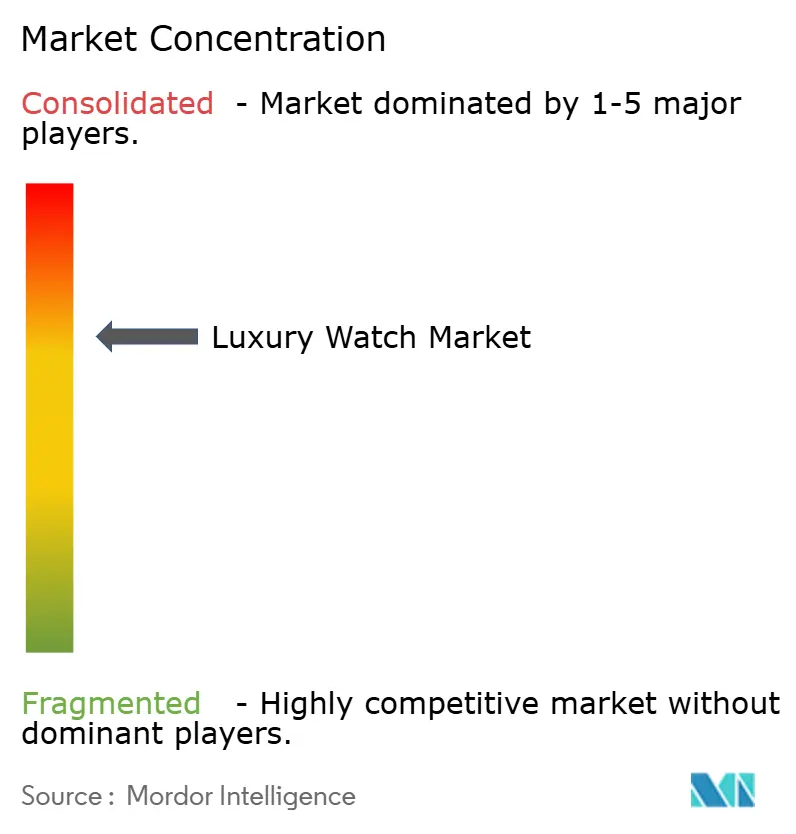

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Luxury Watch Market Analysis by Mordor Intelligence

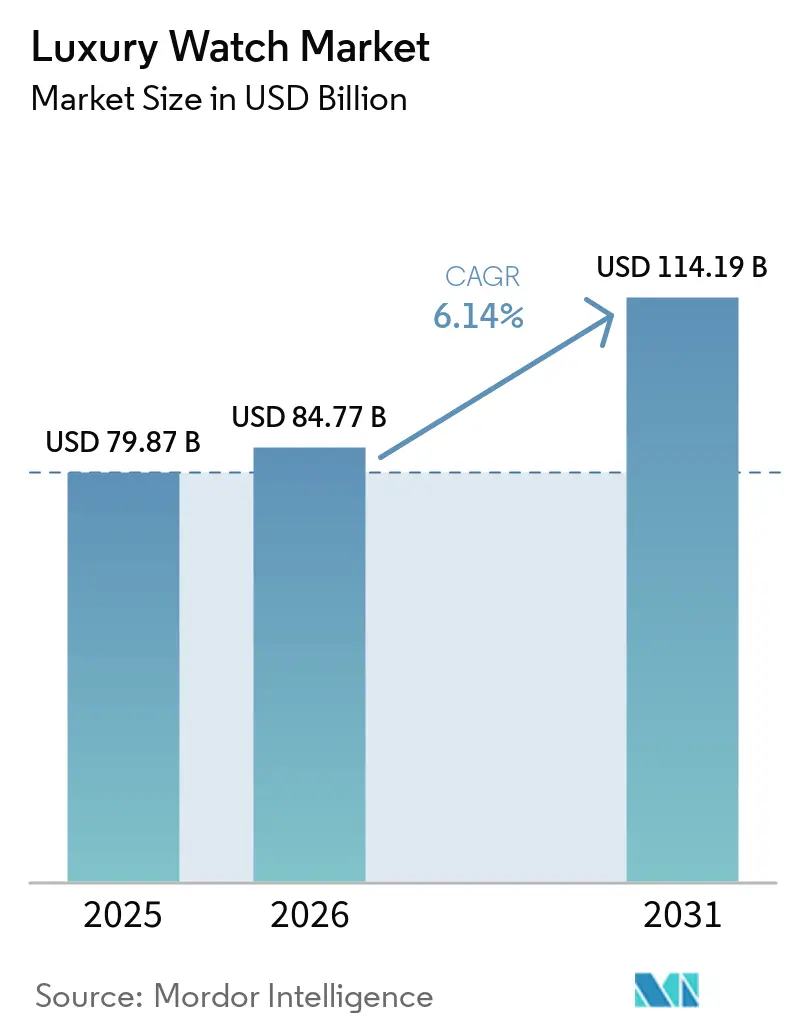

The luxury watch market size was valued at USD 79.87 billion in 2025 and estimated to grow from USD 84.77 billion in 2026 to reach USD 114.19 billion by 2031, at a CAGR of 6.14% during the forecast period (2026-2031). The increasing influence of social media has significantly expanded the customer base, particularly among millennials and Gen Z consumers, who view mechanical watches not only as luxury items but also as valuable assets. Advancements in materials, such as Panerai’s Ecotitanium and Audemars Piguet’s forged carbon, are enabling brands to achieve sustainability goals while maintaining the premium look and feel of their products. While traditional offline boutiques continue to account for the majority of sales, online platforms offering authenticated products are experiencing the fastest growth. Initiatives like Richemont’s Watchfinder platform and Rolex’s Certified Pre-Owned program are driving this trend by providing consumers with trusted options for purchasing luxury watches online. The market remains moderately consolidated, with key players focusing on innovation and expanding their reach to meet the evolving needs of consumers.

Key Report Takeaways

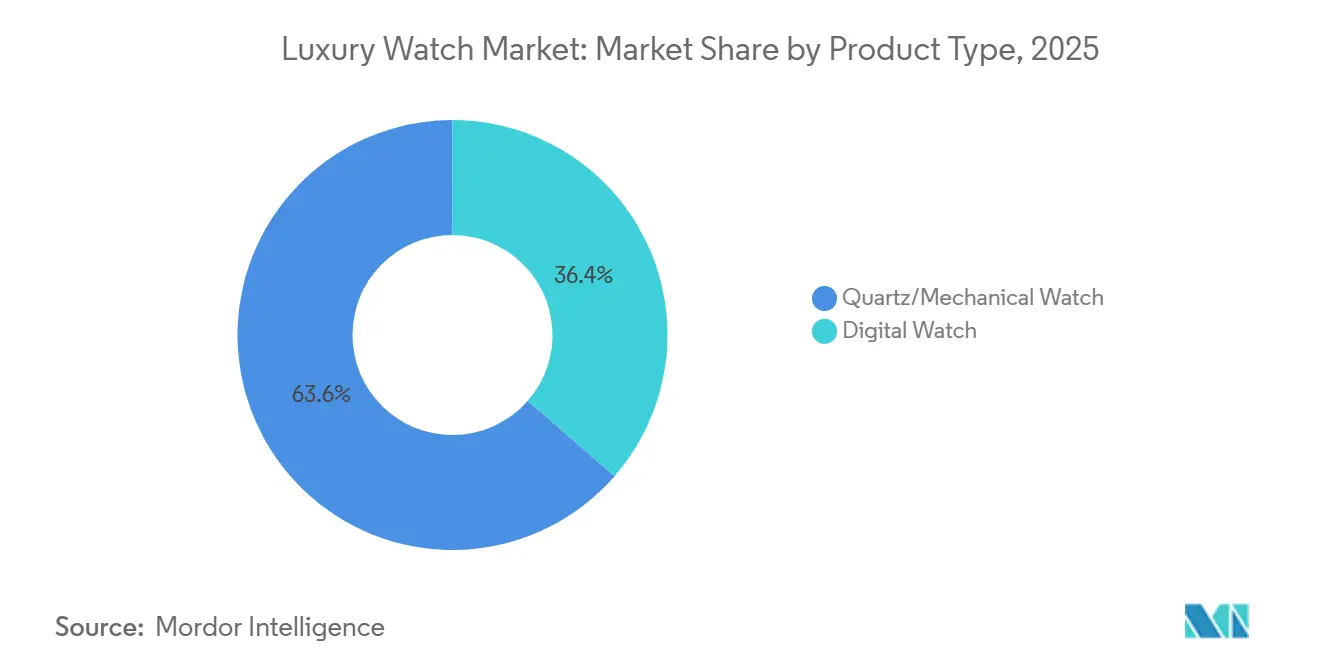

- By product type, quartz/mechanical watches held 63.58% of the luxury watch market share in 2025, while digital models are forecast to post a 6.45% CAGR through 2031.

- By end user, men generated 51.67% of 2025 revenue; women’s lines are projected to expand at a 6.72% CAGR to 2031.

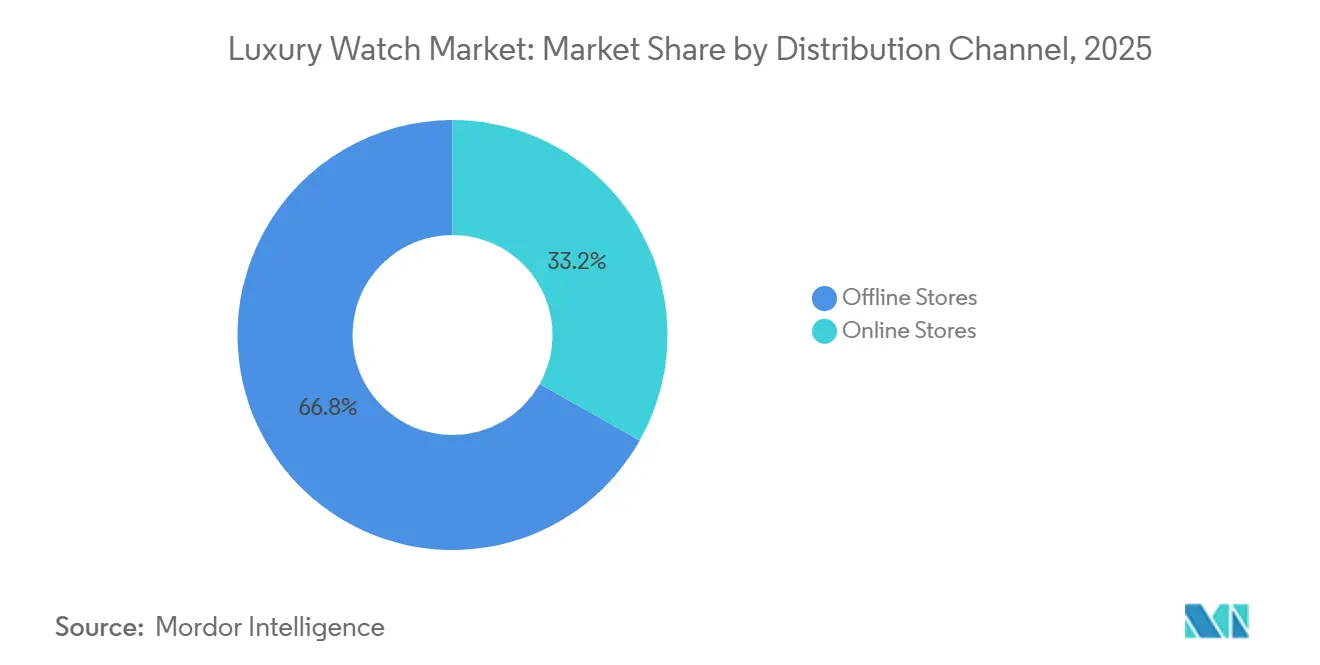

- By distribution channel, offline stores contributed 66.84% of 2025 sales, yet online avenues are expected to register a 7.34% CAGR between 2026 and 2031.

- By geography, Asia-Pacific accounted for 41.58% of the luxury watch market share in 2025, whereas South America is projected to post a 7.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Luxury Watch Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong demand for luxury accessories from millennial consumers | +1.2% | Global, with concentration in North America, Europe, and Asia-Pacific urban centers | Medium term (2-4 years) |

| Influence of social media and celebrity endorsement | +0.9% | Global, particularly North America and Asia-Pacific where digital engagement is highest | Short term (≤ 2 years) |

| Increasing demand for collectible and investment-grade pieces | +1.5% | Global, with early gains in North America, Europe, and select Asia-Pacific markets | Long term (≥ 4 years) |

| Product innovation in terms of raw material and design | +0.8% | Global, led by Switzerland, with adoption in Europe and Asia-Pacific | Medium term (2-4 years) |

| Rising consumer awareness about watch craftsmanship and heritage | +0.7% | Global, with stronger resonance in Europe and Asia-Pacific | Long term (≥ 4 years) |

| Growing interest in vintage and pre-owned luxury watches | +1.3% | Global, with North America and Europe leading, spillover to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing demand for collectible and investment-grade pieces

The demand for luxury watches like Rolex, Patek Philippe, and Audemars Piguet as high-value collectibles and alternative investments is heavily driven by the concentration of high-net-worth individuals (HNWIs) and wealth in key global markets, particularly the United States. The country leads globally with 22.7 million individuals having a net worth of over USD 1 million, far surpassing any other nation, as reported by the World Population Review in 2025[1]Source: World Population Review, "High Net Worth Individuals by Country 2025", worldpopulationreview.com. Both brands and the secondary market are formalizing vintage trading and certified pre-owned programs, offering benefits such as two-year warranties that provide buyers with confidence and help maintain higher valuations. Record-breaking auction sales, like the CHF 31 million Patek Philippe Grandmaster Chime, set price benchmarks for rare and complex watches, establishing them as alternative investment assets. Investments by specialist funds and family offices in rare watch collections, along with advancements in authentication technology that reduce misinformation, are making luxury watches appealing.

Influence of social media and celebrity endorsement

The impact of social media and celebrity endorsements is a key factor driving the growth of the global luxury watch market. According to the World Bank, 71% of the global population was using the internet in 2024, making platforms like Instagram, TikTok, and YouTube highly influential[2]Source: World Bank, "Individuals Using the Internet (% of Population)", data.worldbank.org. These platforms transform celebrity appearances and influencer posts into immediate demand signals, influencing consumer preferences and driving resale activity. For example, when Rafael Nadal wore the Richard Mille RM 27-05, it led to a sharp rise in online searches and inquiries in the secondary market within hours. This trend has led luxury watch brands to actively partner with influencers to enhance their market presence. They are introducing exclusive limited-edition watches and producing engaging digital content to showcase the intricate craftsmanship and advanced technical features of their products. These efforts aim to attract a wider audience and strengthen their brand image in the competitive luxury watch market.

Product innovation in terms of raw material and design

Innovation in materials and design is playing a significant role in shaping the luxury watch market. Brands are increasingly utilizing advanced materials and distinctive designs to enhance the performance, comfort, and sustainability of their watches while upholding the high standards of luxury craftsmanship. For instance, IWC has developed Ceratanium, a material that combines the lightweight properties of titanium with the hardness of ceramic. Similarly, Audemars Piguet uses forged carbon, which reduces weight while ensuring durability, and Hublot has introduced Magic Gold, a material known for its exceptional scratch resistance. These advancements allow luxury watchmakers to meet consumer demands for durable, wearable, and environmentally responsible products. Brands are focusing on innovative designs to attract new customers. For example, Timex launched its Aston Martin watches in September 2024, blending automotive-inspired styling with high-quality watchmaking.

Growing interest in vintage and pre-owned luxury watches

The demand for vintage and pre-owned luxury watches is growing rapidly as more collectors and enthusiasts look for rare, discontinued, or limited-edition timepieces. These watches are sought after for their uniqueness and ability to retain value over time. High-net-worth individuals and younger buyers are turning to secondary markets to purchase these heritage models, which are no longer available through traditional retail channels. Certified pre-owned programs, supported by luxury brands, along with advancements in authentication technology and the rise of digital resale platforms, are making the process of buying pre-owned watches more trustworthy and transparent. For instance, in July 2025, Helios Luxe introduced the Swiss heritage watch brand Auguste Reymond to Indian consumers. This move expanded access to classic timepieces and highlighted the growing demand for traditional watchmaking in emerging luxury markets, such as India.

Restraints Impact Analysis of Luxury Watch Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of counterfeit products | -0.9% | Global, with highest incidence in Asia-Pacific and online marketplaces | Short term (≤ 2 years) |

| Lesser demand from price-sensitive consumers | -0.6% | Global, particularly in emerging markets and middle-income segments | Medium term (2-4 years) |

| High import tariffs increase retail prices globally | -1.1% | North America and Europe, with spillover to Asia-Pacific and South America | Short term (≤ 2 years) |

| Rising smartwatch adoption challenges traditional timepiece sales | -0.4% | Global, with concentration in North America and Asia-Pacific tech-forward markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of counterfeit Products

Proliferation of counterfeit products is a major restraint on the luxury watch market as high-quality replicas produced using Computer Numerical Control (CNC) machining and 3D printing increasingly blur the line between genuine and fake timepieces, especially across online and peer-to-peer resale channels where verification is weaker, forcing brands to invest more in digital certificates, micro-engraving, and hologram rehauts to protect authenticity. The scale of this challenge is reflected in recent enforcement actions, with United States Customs seizing more than USD 186 million worth of counterfeit luxury jewelry and watches in Louisville in July 2025, followed by another 2025 seizure of over 50 fake luxury watches with a real value exceeding USD 6 million at Cincinnati/Northern Kentucky Airport, underscoring how widespread illicit trade continues to undermine consumer confidence and legitimate luxury watch sales.

Rising smartwatch adoption challenges traditional timepiece sales

The growing popularity of smartwatches is posing a significant challenge to traditional wristwatch sales. Smartwatches are becoming the preferred choice for many consumers, especially younger and tech-savvy individuals. These devices have experienced rapid adoption, with 85% of Americans owning smartphones and 31% owning smartwatches as of 2024, according to PubMed Central[3]Source: PubMed Central, "Assessment of Ownership of Smart Devices and the Acceptability of Digital Health Data Sharing", pmc.ncbi.nlm.nih.gov . This trend underscores the profound integration of wearable technology into everyday life. Smartwatches offer a wide range of features that go beyond simply telling time. They include health tracking, fitness monitoring, mobile payment options, notifications, and app connectivity, making them highly practical for daily use. These functionalities appeal to modern consumers who prioritize convenience and versatility. As a result, many potential buyers who might have previously considered purchasing an entry-level mechanical or fashion watch are now opting for smartwatches instead.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Luxury Watch Market Segment Analysis

By Product Type:

Digital Watches Gain Traction amid Mechanical StrengthQuartz and mechanical watches remain the dominant segments in the luxury watch market as of 2025, holding 63.58% of the total market share. These watches are highly valued for their traditional craftsmanship, timeless designs, and the emotional connection they create with buyers. Many consumers, especially collectors and high-net-worth individuals, view these timepieces as symbols of status and sophistication. Their ability to retain or even increase in value over time makes them a preferred choice for those seeking both luxury and investment potential. This enduring appeal ensures that traditional watches remain the cornerstone of the luxury watch market.

Meanwhile, digital and hybrid luxury watches are steadily gaining popularity, driven by the growing demand for smart features combined with stylish designs. This segment is projected to grow at a CAGR of 6.45% through 2031, as more consumers seek watches that offer functionalities like fitness tracking, connectivity, and convenience for daily use. Hybrid models, which blend classic aesthetics with modern technology, are particularly appealing to younger buyers who value both tradition and innovation. These watches cater to a wide range of needs, from lifestyle to wellness, making them a versatile choice. This trend highlights how technological advancements are influencing the luxury watch market while complementing the enduring charm of traditional craftsmanship.

By End User:

Women’s Segment Outpaces Men’s GrowthIn 2025, men remained the primary consumers in the global luxury watch market, contributing 51.67% of the total revenue. This dominance is largely due to the popularity of sports-oriented and complex models, such as the Rolex Submariner and the Patek Philippe Aquanaut. These watches are favored for their advanced features, durability, and the prestige they bring to their owners. Sports and professional models hold strong resale value, making them a preferred choice among male buyers. As a result, men’s collections continue to be the most significant and profitable segment in the luxury watch industry.

Meanwhile, the women’s luxury watch segment is growing rapidly and is expected to achieve a compound annual growth rate (CAGR) of 6.72% through 2031. Brands are shifting their focus from traditional jewelry-style designs to creating watches with larger case sizes, sportier looks, and advanced mechanical movements, which were previously exclusive to men’s collections. This change reflects a growing interest among women in both the technical performance and aesthetic appeal of luxury watches. As more female consumers seek watches that combine functionality with style, the women’s segment is becoming a crucial driver of growth in the global luxury watch market.

By Distribution Channel:

Online Platforms Chip Away at Store DominanceIn 2025, offline retail outlets remained the leading sales channel in the global luxury watch market, contributing 66.84% of total sales. High-value purchases, such as luxury watches, often require a physical shopping experience. Customers prefer visiting stores to try on watches, ensure proper wrist fitting, and interact directly with knowledgeable sales advisors. Boutiques and authorized dealers also offer additional benefits, including authenticity guarantees, after-sales services, and personalized customer relationships. These factors make physical stores a preferred choice for buyers of premium timepieces.

Meanwhile, online sales channels are growing steadily and are projected to expand at a 7.34% CAGR between 2026 and 2031. Digital platforms are becoming increasingly reliable as brands like Rolex enhance their Certified Pre-Owned programs and companies like Richemont integrate platforms like Watchfinder into their operations. These advancements make it easier and safer for customers to buy and sell luxury watches online. As trust in online transactions increases, e-commerce is gradually capturing a larger share of the luxury watch market, offering convenience and accessibility to a broader audience.

Geography Analysis

APAC Luxury Watch Market

The Asia Pacific region remains the largest market for luxury watches in 2025, accounting for 41.58% of global revenue. This dominance is driven by rising wealth, a growing community of collectors, and strong cross-border shopping activity. Major markets, including China, Japan, Singapore, Hong Kong, and India, are key contributors to this growth. Factors such as increasing tourism, currency fluctuations, and evolving consumer preferences further drive demand for luxury timepieces. The region remains the primary growth engine for the global luxury watch industry, driven by its robust economic and consumer dynamics.

South America Luxury Watch Market

South America is rapidly becoming the fastest-growing market for luxury watches, with sales projected to grow at a 7.85% CAGR during the forecast period. An expanding affluent population, improved access to credit, and the growing presence of luxury brands in urban centers fuel the region's growth. Countries such as Brazil, Chile, and Colombia are experiencing a surge in interest in high-end watches. The expansion of luxury boutiques and a rising appreciation for premium goods are further driving this trend. South America presents significant opportunities for global watch brands to tap into untapped demand and expand their market presence.

EMEA and North America Luxury Watch Market

Europe, North America, and the Middle East and Africa remain critical regions for luxury watch sales, even as growth slows in these mature markets. These areas benefit from strong tourism, established retail networks, and a high concentration of wealthy consumers. Cities such as Geneva, Paris, Milan, London, Dubai, and Riyadh serve as major hubs for luxury watch transactions. While these regions provide stability and consistent high-value sales, they complement the faster growth seen in emerging markets like Asia Pacific and South America, ensuring a balanced global market performance.

Competitive Landscape

The luxury watch market is moderately consolidated, primarily dominated by a few major companies, including LVMH Moët Hennessy Louis Vuitton SE, Compagnie Financière Richemont S.A., The Swatch Group Ltd., and Audemars Piguet Holding SA. These companies dominate the industry due to their extensive operations in manufacturing, branding, and retail. Their extensive product range, which spans from entry-level luxury to ultra-premium watches, enables them to cater to a broad spectrum of customers. This dominance gives them significant control over pricing and distribution, making them influential players in the market. Their strong presence is particularly noticeable in key luxury markets worldwide, where demand remains high.

Competition in the luxury watch market is shaped by how these leading companies manage their brands and respond to changing consumer preferences across regions. They frequently update their product lines, marketing strategies, and retail networks to stay aligned with market trends. Some brands focus on creating high-complication and sports watches, while others emphasize designs inspired by fashion or heritage. These companies are streamlining their operations by discontinuing underperforming brands and investing more in their top-performing ones. This approach helps them maintain their competitive edge and lead the market in innovation and trendsetting.

Smaller independent and niche watchmakers also play a significant role by addressing specific customer needs and focusing on high-margin segments. These brands often produce limited-edition watches, sell directly to consumers, and build strong online communities to foster exclusivity. Programs like certified pre-owned platforms and blockchain-based authentication are helping both large and small brands regain control over resale markets and reduce counterfeiting. Furthermore, emerging areas such as women’s mechanical watches, sustainable materials, and hybrid analog-digital designs provide opportunities for smaller players to compete effectively against the larger companies and carve out their own space in the market.

Luxury Watch Industry Leaders

-

Rolex SA

-

Compagnie Financière Richemont S.A.

-

The Swatch Group Ltd

-

LVMH Moët Hennessy Louis Vuitton SE

-

Audemars Piguet Holding SA

- *Disclaimer: Major Players sorted in no particular order

Luxury Watch Market Companies Covered in this Report

- Rolex SA

- Compagnie Financière Richemont S.A.

- The Swatch Group Ltd

- LVMH Moët Hennessy Louis Vuitton SE

- Patek Philippe SA

- Audemars Piguet Holding SA

- Kering S.A

- Seiko Group Corporation

- Breitling SA

- Richard Mille SA

- Chopard Group

- H. Moser & Cie

- F. P. Journe Invenit et Fecit

- Ming Watch

- De Bethune SA

- Armin Strom AG

- Laurent Ferrier SA

- Ressence NV

- Czapek & Cie SA

- Greubel Forsey SA

Recent Industry Developments in Luxury Watch Market

- August 2025: OPUL entered the luxury watch market by introducing a limited-edition timepiece in partnership with music artist Yo Yo Honey Singh. This collaboration combined lifestyle appeal with collectible exclusivity. The launch included a collector ’s-style watch accompanied by branded memorabilia, showcasing a bold design and a compelling narrative.

- March 2025: Citizen introduced a new product category, Citizen Premiere, for its luxury timepieces. The collection combines design and technology elements to establish a position in the modern luxury watch segment.

- August 2024: Ethos opened a new store, Ethos Summit, at Phoenix Mall of Asia in Bengaluru. The boutique offers a selection of luxury watches to customers.

- April 2024: Chopard launched new timepieces for men and women, featuring the L.U.C XPS Forest Green and the Alpine Eagle XL Chrono models. The company incorporated its proprietary alloy, which contains at least 80% recycled materials and offers enhanced technical properties. These watches utilize the in-house L.U.C Calibre 96.12-L movement.

Luxury Watch Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the luxury watch market as new, factory-manufactured wristwatches priced and positioned for conspicuous consumption, built with premium materials such as precious metals or high-grade steel, and powered by mechanical or quartz movements engineered for long-term precision. Luxury smartwatches that retail above typical mass-market price bands are included.

Wearables and fashion watches priced under USD 1,000 are outside the scope.

Segments Covered in This Report

-

By Product Type

- Quartz/Mechanical Watch

- Digital Watch

-

By End User

- Men

- Women

- Unisex

-

By Distribution Channel

- Offline Stores

- Online Stores

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

South America

- Brazil

- Colombia

- Chile

- Peru

- Argentina

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed senior executives at authorized dealers, watchmakers, and aftermarket platforms across Asia, Europe, and North America. They then surveyed affluent consumers and independent horology experts. These conversations clarified gray-market flows, price-mix changes, and online penetration, allowing us to align desk findings with on-ground realities.

Desk Research

We began with tariff-line level export statistics from the Federation of the Swiss Watch Industry, Swiss Customs, UN Comtrade, and Eurostat, which reveal shipment volumes, average unit values, and destination mixes. Macro indicators from the IMF, OECD, and World Bank, together with household wealth data, provided purchasing power context by region. Company filings retrieved through D&B Hoovers and news flows screened via Dow Jones Factiva helped us capture brand revenue trends and channel shifts. Supplementary insights came from trade associations such as Comité Colbert and Jewelers of America. The sources listed here illustrate the breadth consulted; many additional public and subscription datasets informed the analysis.

Market-Sizing & Forecasting

A top-down model converts producer export and domestic shipment values into regional retail sales after mark-up adjustments, which are then verified through selective bottom-up checks such as dealer roll-ups and sampled average selling price times volume estimates. Key variables include Swiss export growth, high-net-worth individual counts, average transaction prices, pre-owned share, discretionary spending indices, and online luxury penetration. Historical relationships were tested with multivariate regression; the resulting drivers feed an ARIMA forecast that projects demand to 2030. Gap areas in bottom-up estimates are reconciled to the top-down control total to keep segment splits internally consistent.

Data Validation & Update Cycle

Outputs pass a two-layer analyst review, variance tests against public earnings, and anomaly flags for currency shifts. Reports refresh annually, while material events such as tax changes or supply shocks trigger interim revisions. A final pre-publication sweep ensures clients receive the latest vetted numbers.

How Mordor Intelligence's Luxury Watch Market Size Compares to Other Published Estimates

Benchmark comparison

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 79.87 B (2025) | Mordor Intelligence | - |

| USD 59.97 B (2025) | Regional Consultancy A | Omits gray-market sales, uses aggressive online mark-up assumptions |

| USD 29.10 B (2024) | Trade Journal B | Narrow luxury definition excludes watches below USD 5,000 and ignores boutique mark-ups |

Published figures often diverge because firms apply different luxury price cut-offs, channel mark-ups, and refresh cadences. By calibrating export data with verified retail multipliers and validating assumptions through continuous primary engagement, we provide a balanced, transparent baseline that decision-makers can confidently track over time.

Key Questions Answered in the Report

What is the current value of the luxury watch market?

The luxury watch market size is USD 84.77 billion in 2026.

How fast is the sector expected to grow?

Revenue is projected to reach USD 114.19 billion by 2031, implying a 6.14% CAGR.

Which product segment is expanding quickest?

Digital and hybrid watches are forecast to post a 6.45% CAGR through 2031.

Which region is projected to grow fastest?

South America, spearheaded by Brazil and Colombia, is expected to advance at a 7.85% CAGR to 2031.

Page last updated on: