Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

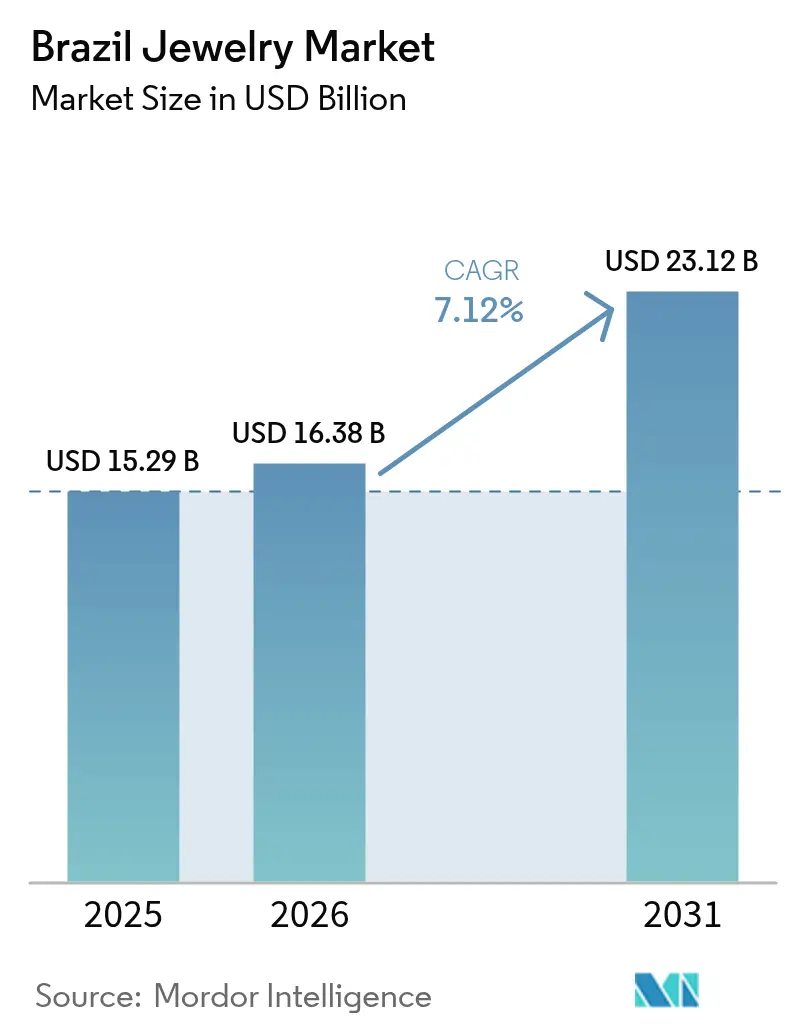

| Base Year Market Size (2025) | USD 15.29 Billion |

| Market Size (2026) | USD 16.38 Billion |

| Market Size (2031) | USD 23.12 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Brazil Jewelry Market Analysis by Mordor Intelligence

The Brazilian jewelry market size is expected to grow from USD 15.29 billion in 2025 to USD 16.38 billion in 2026 and is forecast to reach USD 23.12 billion by 2031 at 7.12% CAGR over 2026-2031. Rising disposable incomes, a deepening preference for personalized luxury, and Brazil’s status as a major gemstone producer underpin this solid growth trajectory, helping the Brazilian jewelry market reinforce its role as Latin America’s flagship jewelry hub. Demand is further supported by a strong bridal culture that sustains ring purchases, growing fashion consciousness that accelerates costume jewelry volumes, and omnichannel investments that meet the nation’s e-commerce boom. Competitive advantages also stem from abundant domestic gemstone resources, particularly emeralds, tourmalines, and aquamarines sourced from Minas Gerais, Bahia, and Goiás, positioning local firms for import substitution and export gains. Counterfeit risks, precious-metal price spikes, and complex import duties remain headwinds, but industry players are offsetting these threats through traceability initiatives, lab-grown diamond introductions, and mixed-material innovations that lower input cost exposure and protect price-sensitive customers.

Key Report Takeaways

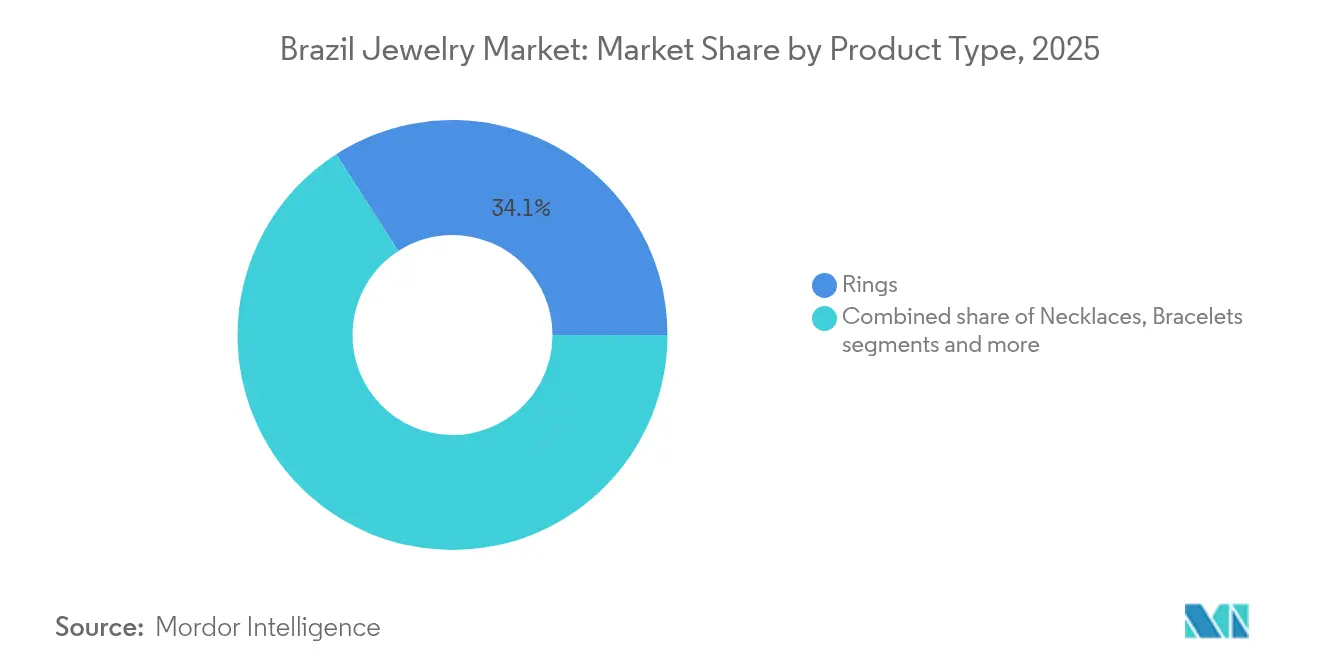

- By product type, rings held 34.10% of the Brazilian jewelry market share in 2025, while bracelets are forecast to post a 6.78% CAGR through 2031.

- By material, precious metals captured 61.92% share of the Brazilian jewelry market size in 2025, and mixed materials are projected to advance at a 7.05% CAGR during the outlook period.

- By category, real jewelry accounted for 84.65% of the Brazilian jewelry market size in 2025; costume jewelry is set to accelerate at a 7.52% CAGR to 2031.

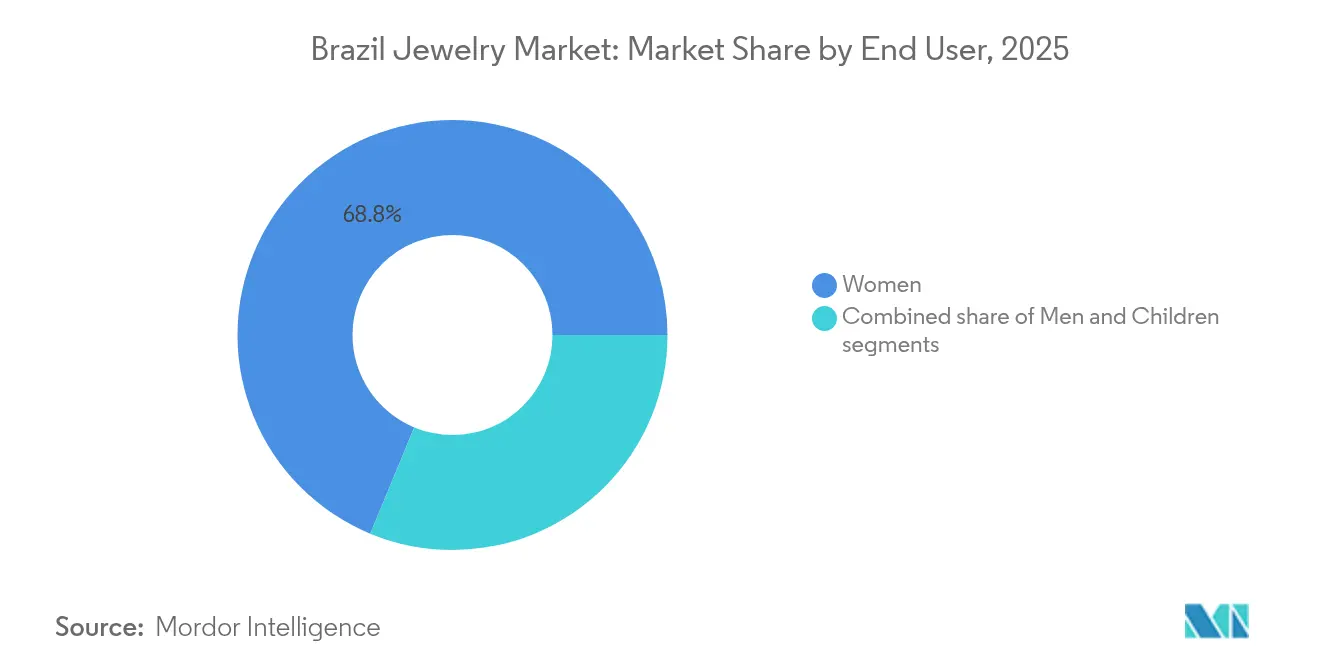

- By end user, women dominated with 68.75% share of the Brazilian jewelry market in 2025, whereas men’s lines carry the highest forecast CAGR at 7.31%.

- By distribution channel, offline retail controlled 88.82% of the Brazilian jewelry market share in 2025, but online platforms are projected to grow at an 7.76% CAGR owing to mobile commerce adoption.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Jewelry Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lab-grown diamond introduction | +1.2% | National, with early adoption in São Paulo, Rio de Janeiro | Medium term (2-4 years) |

| Consumers seek customized, made-to-order, and personalized pieces | +1.8% | National, concentrated in urban centers | Short term (≤ 2 years) |

| Rising demand for certified and traceable jewelry | +1.1% | National, with premium segments leading | Medium term (2-4 years) |

| Surge in fashion consciousness | +1.4% | National, Gen Z and Millennial focused | Short term (≤ 2 years) |

| Rich gold and gemstone resources drives production and exports | +0.9% | Minas Gerais, Bahia, Goiás production centers | Long term (≥ 4 years) |

| BRICS diamond-trade cooperation enhancing supply access | +0.8% | National, with São Paulo trading hub benefits | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lab-grown diamond introduction

Global retailers are allocating 40-60% of their showcase space to lab-grown diamonds, capitalizing on 50-70% cost savings compared to natural stones, as per CaratX. In Brazil, consumers, particularly Gen Z and Millennials, are prioritizing sustainability and value, favoring ethical alternatives over traditional diamond provenance. This shift presents a lucrative opportunity for retailers to expand accessible luxury offerings. Advancements in technology enable Brazilian jewelers to offer larger carat weights at competitive prices, directly challenging the traditional diamond market hierarchy. For example, Pandora has strategically integrated lab-grown diamonds into its Brazilian offerings, demonstrating how established brands are adapting to attract price-sensitive consumers while maintaining their premium image. This evolution is occurring alongside global diamond market volatility, with prices for smaller natural diamonds declining by 3.3-4.7% in 2024, creating pricing arbitrage that Brazilian retailers can exploit. As demand for ethically sourced and cost-effective luxury rises, lab-grown diamonds are at the forefront of this market evolution. Their appeal aligns with a broader consumer shift toward eco-consciousness and technological advancements in jewelry retail. This combination of affordability, sustainability, and innovative marketing is set to disrupt traditional diamond purchasing patterns, reshape Brazil's luxury segment, and extend the reach of fine jewelry to a wider audience. These developments are solidifying Brazil’s position as a leading national market in Latin America for lab-grown diamonds.

Consumers seek customized, made-to-order, and personalized pieces

Consumers in Brazil are increasingly prioritizing unique jewelry experiences over material possessions. This trend reflects a broader generational shift that emphasizes authenticity and individual expression over traditional luxury markers. Limeira, a semi-jewelry capital in São Paulo, is well-positioned to benefit from this change. The city’s made-to-order production thrives, supported by a predominantly female workforce, aligning with a 2024 World Bank statistic indicating that women make up 43.3% of Brazil’s labor force [1]Source: World Bank Group, "Labor force, female (% of total labor force) - Brazil", data.worldbank.org. Jewelers in Brazil are leveraging digital tools, such as virtual consultations and 3D modeling, to deliver personalized services. By focusing on customer connection rather than scale, they effectively compete with major international brands. Customized jewelry, with its emotional appeal, commands premium pricing, resulting in higher margins and fostering strong customer loyalty. The rise of e-commerce further enhances access to these personalized offerings, particularly among younger consumers who value self-expression. Leading brands like Vivara and Pandora are capitalizing on this trend by integrating technology with personal engagement to meet evolving consumer preferences. This approach not only strengthens the competitive position of Brazil's jewelry market but also makes luxury experiences more inclusive. The growing focus on bespoke pieces is expected to remain a key growth driver for the jewelry sector. This trend highlights the cultural significance of jewelry in Brazil as both personal and social symbols, reinforcing the market’s resilience and expansion potential.

Rich gold and gemstone resources drives production and exports

The abundant gold and gemstone resources in Brazil serve as a cornerstone for the country's production and export activities, significantly influencing the jewelry market. The U.S. Geological Survey reported that Brazil's gold production in 2024 reached an estimated 70 metric tons, supported by a substantial reserve base of approximately 2,400 metric tons [2]Source: U.S. Geological Survey, "mcs2025.pdf - Mineral Commodity Summaries 2025", pubs.usgs.gov. This resource wealth enables Brazilian jewelers to procure high-quality materials domestically, reducing import dependency and enhancing competitiveness in both local and international markets. Alongside gold, the availability of native gemstones strengthens the country's jewelry manufacturing capabilities, offering a diverse portfolio of premium and semi-precious products. Luxury brands, such as H. Stern, have effectively leveraged these resources by incorporating Brazil's natural heritage into their collections, boosting authenticity and market appeal. Additionally, global demand for Brazilian gold and gemstones drives strong export performance, positioning the country as a key player in the precious metals supply chain. This resource advantage, coupled with technological advancements and artisanal expertise from regions like Limeira, fosters innovation and market growth. The synergy between resource abundance and skilled craftsmanship continues to support sustainable growth in the jewelry industry, enhancing export potential and international brand recognition. This inherent resource strength provides a solid foundation for the ongoing development of Brazil's dynamic jewelry sector.

Surge in fashion consciousness

A surge in fashion consciousness is driving growth in the jewelry sector, with jewelry increasingly serving as a tool for personal branding rather than mere ornamentation. Urban millennials and Gen Z, in particular, view accessories as critical expressions of identity. This demographic's demand for trend-responsive designs, aligned with fast fashion cycles, has significantly boosted the costume jewelry segment, which thrives on affordability and rapid style turnover. This trend aligns with Brazil's strengthening retail environment, where fashion brands, supported by economic recovery and the annual 13th salary, report optimistic projections and experience spikes in consumer spending. Social media platforms like TikTok Shop play a crucial role in accelerating trend adoption and impulse buying, enabling emerging styles to gain quick traction among younger consumers. The evolving fashion consciousness is also elevating the premium positioning of Brazilian gemstones, as consumers increasingly value locally sourced, unique mineral heritage over imported alternatives. Brands such as Rommanel are leveraging this cultural and digital shift by blending affordable fashion with Brazilian gemstone pride to capture the evolving market. This transformation enhances market diversity and supports the growth of both luxury and costume jewelry, positioning Brazil as a dynamic and trend-sensitive jewelry hub in Latin America.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of inexpensive counterfeits diluting brand equity | -1.5% | São Paulo, Rio de Janeiro commercial centers, national e-commerce | Short term (≤ 2 years) |

| Elevated precious-metal prices squeezing consumer budgets | -1.3% | National, with middle-income segments most affected | Medium term (2-4 years) |

| Informal mining and supply-chain opacity hurting brand trust | -0.9% | Minas Gerais, Bahia, Goiás mining regions, export markets | Long term (≥ 4 years) |

| Complex tax and customs regime inflating import costs | -0.7% | National, with São Paulo import hub concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of inexpensive counterfeits diluting brand equity

The counterfeit jewelry market in Brazil poses significant risks to the integrity of legitimate brands. Enforcement challenges are particularly evident in major commercial hubs, where counterfeit goods infiltrate both physical stores and increasingly complex digital channels. The mid-market segment is most affected, as consumers' price sensitivity makes them prone to purchasing counterfeit alternatives that replicate premium designs at significantly lower costs. The rapid growth of e-commerce further intensifies these issues. Online platforms complicate authentication processes, forcing legitimate retailers to allocate substantial resources to anti-counterfeiting technologies and consumer education on authenticity. Smaller Brazilian jewelers face heightened challenges, as they often lack the financial capacity to implement robust brand protection measures. This situation may drive market consolidation, with larger players, equipped with stronger enforcement capabilities, capturing greater market share. For instance, major brands like Vivara invest in authentication systems and consumer awareness programs to mitigate the spread of counterfeit products. This ongoing issue undermines consumer trust and damages the reputation of genuine Brazilian jewelry, making anti-counterfeiting efforts a critical restraint within the expanding market.

Elevated precious-metal prices squeezing consumer budgets

Rising gold and silver prices are creating significant affordability barriers in the jewelry market, particularly for Brazil's large middle-class segment. This group, both a core growth driver and highly sensitive to commodity fluctuations, is facing increased financial strain. Economic pressures, such as inflation and currency volatility, are exacerbating these challenges. Consequently, many consumers are delaying purchases or opting for lower-quality alternatives. Global supply chain disruptions and geopolitical tensions are further fueling precious metal price volatility. Brazilian retailers, however, face difficulties in hedging these risks due to the limited sophistication of the country's financial markets. Additionally, Brazil's complex tax and customs framework, including high import duties on precious metals, inflates final prices beyond those of regional competitors, further reducing affordability. Amid these challenges, the mixed-material jewelry segment is experiencing robust growth, with a 7.42% CAGR. Consumers are increasingly drawn to these aesthetically appealing yet cost-effective alternatives, which feature reduced precious metal content. Brands like Rommanel are leveraging this trend by incorporating mixed materials to maintain style and appeal while addressing price sensitivity. As a result, while the jewelry market in Brazil continues to expand, metal price volatility remains a critical restraint, compressing consumer spending power.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rings Dominate While Bracelets Surge

Rings hold a dominant 34.10% market share in 2025, highlighting their critical role in Brazil's strong bridal and engagement traditions. Meanwhile, bracelets are positioned as the fastest-growing segment, with a 6.78% CAGR projected through 2031. The ring segment's leadership is driven by its cultural importance in relationships and celebrations, further supported by customization trends that enable personalized engagement and wedding designs. In contrast, bracelets benefit from a surge in fashion consciousness and the influence of social media, particularly among younger demographics who layer multiple pieces to express their individuality.

Necklaces secure a significant market share due to their versatility across casual and formal occasions. Earrings maintain a steady demand, supported by Brazil's vibrant social culture and frequent celebrations. Chains and pendants address the growing demand for customization, allowing consumers to mix and match components to create personalized looks that align with their style preferences. Other product categories, such as brooches and cufflinks, cater to niche segments but gain traction from Brazil's formal business culture and traditions of gifting for special occasions. This creates opportunities for specialized retailers to capture premium margins through unique designs.

By Material: Precious Metals Lead Mixed Material Innovation

Brazil's world-class gold mining capabilities and its gemstone-rich regions of Minas Gerais and Bahia drive the dominance of precious metals, which hold a 61.92% market share in 2025. Meanwhile, the mixed materials segment is the fastest-growing, recording a 7.05% CAGR. This growth reflects a consumer preference for affordable luxury, combining precious metals with alternative materials to achieve desired aesthetics at accessible price points. Brazilian manufacturers benefit significantly from this trend, leveraging locally sourced gold and gemstones while incorporating international design elements into their products.

Base metals support the expanding costume jewelry segment, catering to fashion-conscious consumers seeking trend-responsive pieces that align with fast-fashion cycles without the investment in precious metals. This material segmentation aligns with broader economic dynamics, where volatility in precious metal prices drives demand for mixed-material alternatives that maintain a luxury appearance while reducing cost sensitivity. Brazilian jewelers increasingly utilize local gemstone varieties, such as tourmaline, aquamarine, and topaz, to differentiate their mixed-material offerings, creating unique value propositions that are difficult for international competitors to replicate.

By Category: Real Jewelry Dominance Faces Costume Challenge

Real jewelry holds a dominant 84.65% market share in 2025, reflecting consumer preferences for investment-grade pieces that retain value and align with family inheritance traditions. Costume jewelry, on the other hand, is growing at a notable 7.52% CAGR, emerging as the fastest-expanding category. This growth is driven by increasing fashion consciousness and younger demographics prioritizing trend responsiveness over long-term value retention. These dynamics create bifurcated market opportunities, with established players focusing on premiumizing real jewelry while emerging brands capitalize on the expanding costume segment.

The category split highlights economic stratification within Brazilian society. Affluent consumers invest in real jewelry for special occasions and wealth preservation, while middle-income segments increasingly adopt costume jewelry for everyday fashion expression. Real jewelry benefits from Brazil's gemstone heritage and skilled craftsmanship, particularly in production hubs like Limeira, which support its premium positioning. Meanwhile, costume jewelry is closely linked to the expansion of e-commerce and the influence of social media, where frequent style changes drive demand for affordable alternatives over permanent investment pieces.

By End User: Women's Dominance Challenged by Men's Growth

Women account for a commanding 68.75% share of the jewelry market in 2025, reflecting traditional purchasing patterns and Brazil's strong gift-giving culture, where men frequently buy jewelry for female recipients during celebrations and special occasions. Meanwhile, men's jewelry is emerging as the fastest-growing segment, with a 7.31% CAGR. This growth is driven by evolving perceptions of masculinity and increased fashion consciousness among urban millennials and Gen Z consumers, who increasingly view jewelry as a tool for personal branding. Retailers are well-positioned to leverage this trend by developing male-specific product lines and targeted marketing strategies.

Children's jewelry represents a smaller yet stable segment, supported by Brazil's family-oriented culture and religious traditions, where jewelry is often gifted during baptisms, communions, and birthdays. The end-user segmentation highlights broader societal changes, as traditional gender roles shift and personal expression becomes more individualized across demographic groups. The men's segment, in particular, benefits from customization trends, with male consumers seeking unique pieces that reflect personal style rather than adhering to traditional masculine jewelry conventions. This shift creates opportunities for innovative designs and materials in the market.

By Distribution Channel: Digital Transformation Accelerates

Offline retail stores maintain a dominant 88.82% share of the jewelry market in 2025, reflecting consumer preferences for tactile evaluations and personalized services offered by traditional outlets. Urban consumers in Brazil prioritize in-person interactions, particularly for authentication and high-value purchases, which reinforces the strength of offline channels. However, online retail represents the fastest-growing segment, achieving an 7.76% CAGR. This growth is driven by Brazil's leading position in e-commerce expansion and increasing consumer confidence in digital transactions. Younger demographics are especially drawn to the convenience, price comparisons, and product discovery facilitated by social media platforms.

Omnichannel strategies are becoming critical for competitive positioning as the retail landscape transforms. Offline stores retain a competitive edge for premium purchases requiring personal consultation, while online platforms excel in fashion and repeat purchases where convenience is a key factor. Digital innovations, such as the TikTok Shop launch in Brazil, leverage influencer partnerships to encourage impulsive jewelry purchases among digitally native consumers. This trend is supported by the rise in social media engagement, with 81% of Brazil's internet users active in 2024, up from 72% in 2022, as per the Regional Center for Studies on the Development of the Information Society . These figures highlight the growing influence of social commerce on jewelry trends and purchasing behavior. Brands like Vivara effectively integrate traditional luxury with digital convenience, addressing evolving consumer expectations.

Geography Analysis

The jewelry industry in Brazil demonstrates strong domestic concentration, with regional production centers driving both local consumption and export activities. Minas Gerais stands out as the gemstone capital, renowned for producing world-class emeralds in Itabira and tourmalines in the Araçuaí-Itinga and Araçuaí-Salinas districts. Meanwhile, São Paulo, anchored by Limeira's semi-jewelry sector, has established itself as the commercial and manufacturing nucleus. This geographic concentration not only offers competitive advantages but also fosters vertical integration and specialized workforce development, setting Brazil apart from its international competitors.

Regional dynamics mirror Brazil's rich mineral distribution. Bahia is a significant contributor of diverse gemstones, while Goiás boasts gold mining capabilities that bolster the nation's jewelry production. Furthermore, Brazil's exclusive gemstone varieties, such as Paraíba tourmalines and imperial topazes, fetch premium prices on the global stage, presenting differentiation opportunities for local jewelry brands. Additionally, BRICS cooperation bolsters supply chain access, especially for diamond imports, enriching Brazil's already diverse gemstone portfolio and offering retailers a comprehensive product lineup.

Urban hubs like São Paulo and Rio de Janeiro, with their affluent and fashion-savvy populations, are at the forefront of driving jewelry consumption. These cities not only embrace traditional styles but also contemporary trends. This geographic distribution bolsters omnichannel strategies, allowing major cities to host physical retail outlets while digital platforms reach Brazil's expansive smaller markets. Such geographic leverage is crucial, especially with online channels witnessing an 7.76% CAGR growth. It empowers Brazilian jewelers to cater to national markets from centralized hubs, all while staying attuned to local preferences through regional partnerships and tailored offerings.

Regulatory Landscape

Brazilian jewelry and costume jewelry are subject to mandatory safety and conformity rules led by INMETRO (Instituto Nacional de Metrologia, Qualidade e Tecnologia). INMETRO Ordinance No. 123/2021 consolidates technical requirements and sets chemical limits for items intended for skin contact, including maximum lead content of 0.03% (300 ppm) and cadmium content of 0.01% (100 ppm), which shapes testing, labeling, and market-surveillance obligations for manufacturers and importers.

Trade and manufacturing compliance is also influenced by Brazil's tax and customs framework administered by Receita Federal, where import duties and related charges vary by NCM classification and applicable tariff agreements, adding cost and documentation complexity for precious metals, gemstones, and finished jewelry. For local production incentives, the Basic Productive Process (PPB) applicable to jewelry in the Zona Franca de Manaus is defined via interministerial ordinances (for example, SEPEC/ME/SEXEC/MCTI No. 7.252/2021). ABNT (Associacao Brasileira de Normas Tecnicas) standards such as NBR 17041 further support technical design and specification practices used across the sector.

Competitive Landscape

Moderate consolidation characterizes the competitive landscape of the jewelry market in Brazil, enabling companies to prioritize strategic differentiation over scale. For example, market leader Vivara operates 457 points of sale as of December 2024, including 266 Vivara stores and 180 Life units, while also expanding internationally to Panama. This diversified presence highlights Vivara's vertical integration and strong brand equity, supporting both domestic leadership and international growth. Meanwhile, the market reflects fragmented consumer preferences across price segments. Luxury players like H. Stern leverage Brazil’s gemstone heritage to attract high-value clientele, while accessible fashion jewelry brands target price-sensitive consumers.

Strategic emphasis on technology adoption serves as a key differentiator in Brazil's jewelry market. Leading companies are investing heavily in omnichannel capabilities and digital engagement platforms to compete effectively against international e-commerce entrants. Online channels, growing at an 8.13% CAGR, present significant opportunities, particularly in men’s jewelry, which is expanding at a 7.65% CAGR. Established brands are leveraging their existing brand equity to capture these emerging segments effectively. Balancing offline and online strengths remains critical for sustaining competitive advantage and addressing diverse consumer demands.

The market structure fosters a dynamic interplay between scale, brand positioning, and innovation, where differentiation through sustainability, craftsmanship, and digital channels defines success. Brands like Pandora integrate personalized offerings and lab-grown diamond collections as part of their strategy to align luxury with emerging consumer trends. This multifaceted competitive environment positions Brazil as a vibrant and evolving jewelry market with distinct opportunities for growth across segments and channels.

Brazil Jewelry Industry Leaders

-

Jóias Vivara

-

H. Stern Jewelers Inc.

-

Pandora A/S

-

Manoel Bernardes S.A.

-

LVMH Moët Hennessy Louis Vuitton SE

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Omnichannel and marketplace-led distribution is a practical growth lever, with leading brands setting up official storefronts to improve reach, assortment control, and authenticity signaling in a channel where counterfeit risks are a recurring concern. In 2026, Vivara expanded its digital presence by launching two official stores on Mercado Livre, with Vivara focused on watches and Life by Vivara for silver jewelry. Pandora also opened an official Mercado Livre store in 2025, pointing to marketplace channel governance and brand-operated experiences as a way to build online penetration while still leveraging offline trust advantages.

Store-network buildouts and cross-border playbooks are also creating opportunities across fittings, fixtures, merchandising, and localized assortment development. Swarovski announced an expansion phase in Brazil to open six stores in 2026, with a longer runway of additional stores planned through 2028, while Brazilian costume jewelry chain Morana outlined a Latin America expansion step via a joint venture in Argentina using Brazil as an operational base. On the supply and capability side, industry bodies in Minas Gerais (SINDIJOIAS MG/FIEMG) have been running digital transformation and generative AI workshops, which supports opportunities for faster design iteration, made-to-order personalization, and productivity upgrades in manufacturing clusters tied to gemstones and semi-jewelry production.

Recent Industry Developments

- May 2026: Vivara launched two official stores on Mercado Livre, one dedicated to Vivara watches and another for Life by Vivara silver jewelry. The company is adding a controlled marketplace presence to strengthen omnichannel execution, widening digital reach while improving brand presentation and authenticity cues in a channel exposed to counterfeits.

- July 2025: Pandora inaugurated its official store on Mercado Livre to expand digital distribution in Brazil. The direct marketplace operation supports assortment expansion beyond core charm categories and improves performance marketing efficiency by connecting demand on a high-traffic platform to an official brand source.

- December 2024: Tiffany & Co. opened a flagship at Iguatemi Sao Paulo with a multi-floor format and dedicated areas for watches, engagement rings, and high jewelry. The flagship investment lifts the bar for premium in-store experiences in Brazil and reinforces Sao Paulo as a high-end retail hub for luxury jewelry.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Brazil jewelry market is defined as the value of jewelry products sold to end users within Brazil through offline and online retail, captured in current USD terms.

Scope exclusions: This sizing excludes watches, loose gemstones sold without a jewelry setting, and purely industrial uses of precious metals.

Segmentation Overview

-

By Product Type

- Necklaces

- Rings

- Earrings

- Bracelets

- Chains and Pendants

- Other Product Types

-

By Material

- Precious Metals

- Base Metals

- Mixed Materials

-

By Category

- Fine Jewelry

- Costume Jewelry

-

By End User

- Women

- Men

- Children

-

By Distribution Channel

- Offline Retail Stores

- Online Retail Stores

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the market model and to anchor assumptions that can be checked outside of interviews. We reviewed public data points such as Brazil trade and tariff statistics from Comex Stat, macro and household spending indicators from IBGE, and relevant industry classification notes from Receita Federal where product mapping was required.

To refine context around demand and supply signals, we also referenced sources such as UN Comtrade for cross-checks on import flows, World Bank inflation and currency series for deflators and conversion timing, and association and exchange publications linked to jewelry and precious materials where available. Company filings, investor presentations, and reputed press were used to sense-check channel shifts (offline versus online) and price movements. Paid subscriptions were used selectively for company financials and for shipment-level import-export views to validate directionally where public tables were too aggregated. These desk sources are illustrative only, and many other public and paid references were used to collect, validate, and clarify data points during the study.

Primary Interviews and Surveys

Primary work was used to confirm what is actually being counted as jewelry revenue in Brazil and to test pricing and channel assumptions that desk sources rarely spell out. We spoke with a mix of brand and retailer teams, distributors, material and component participants, and independent industry experts across Brazil to validate category splits, typical price bands, and how online sales are recorded versus store sales.

Feedback from these discussions helped tighten the model around product mix changes, promotion intensity, and the practical difference between fine and costume jewelry spending, which were then used to reconcile the final totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 12% | |

| Mid tier: 54% | Functional/Unit leaders: 42% | |

| Smaller Players: 20% | Managers: 46% |

Market-Sizing & Forecasting

The market size was first constructed using a top-down approach where retail jewelry demand in Brazil is rebuilt from a spending pool and then distributed across jewelry categories and channels. In practice, the model starts from consumer spending and retail activity indicators, and then applies jewelry-relevant splits that were validated through interviews.

To keep the totals realistic, we also ran selective bottom-up approximations, such as sampled average selling price (ASP) by product type multiplied by estimated unit movement for key channels, followed by simple supplier and retailer roll-ups where financial disclosure allowed it. When a bottom-up view looked thin for smaller retailers or informal trade, gaps were handled through calibrated expansion factors that were tied back to interview inputs and public retail penetration signals.

Variables used in the model included the fine versus costume jewelry mix, offline versus online share, ASP progression by material group (precious metals versus base and mixed materials), currency and inflation timing for value normalization, and import duty and trade flow direction for stress testing supply sensitivity. For forecasting, scenario analysis was applied around a central path, with scenarios mainly changing assumptions on discretionary spend strength, online adoption pace, and precious metal price pass-through. The scenario ranges were then narrowed using expert consensus gathered in primary calls so the forecast remains explainable and repeatable.

Data Validation & Update Cycle

Validation is done through multi-step checks so the model does not rely on any single data stream. We compare outputs against independent signals such as trade value direction, retail channel trends, and price movement markers, and then investigate unusual jumps before final sign-off.

Where large variances are found, assumptions are revisited and the team re-contacts selected respondents to confirm whether the change is real or only a data artifact. Each report is refreshed annually, and interim updates are triggered when material events occur, such as sudden currency swings, major tax or duty changes, or a clear shift in channel mix. Before delivery, an analyst performs a final pass so clients receive the latest updated view based on the newest public releases and market feedback.

Mordor Intelligence's Brazil Jewelry Market Market Size Compared Against Other Published Estimates

It is normal to see different market sizes for Brazil jewelry because publishers do not always count the same product set, the same channel boundary, or the same price basis. Timing also matters, since some figures are updated after a currency or inflation swing, while others remain on an older base year view.

The table shows a wide spread, and in Mordor Intelligence's model the value is counted as jewelry sold within Brazil across offline retail stores and online retail stores, with fine and costume jewelry included, which can differ from estimates that focus on narrower product lists or different channel capture.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.29 B (2025) | |

| Industry Research Group A | USD 3.20 B (2025) | This estimate appears to run on a much tighter value base for the market, which may come from a narrower capture of retail jewelry revenue or different currency conversion and inflation timing for the same year. |

| Global Analytics Desk B | USD 3.18 B (2025) | The figure is presented as revenue with a product-led breakdown, and it can differ if parts of the jewelry spend are excluded, if channel coverage is not fully aligned, or if the price basis is held constant rather than reflecting current-value selling prices. |

Looking across the three values, the main takeaway is that scope choices and price basis decisions can move the number more than the growth outlook itself. By keeping the model tied to clear demand signals, practical channel splits, and repeatable ASP assumptions, we get a market value that can be traced back to inputs and rechecked when new data is released.

Key Questions Answered in the Report

How large is the Brazil jewelry market in 2026?

The Brazil jewelry market size is USD 16.38 billion in 2026.

Which product category currently leads jewelry sales in Brazil?

Rings hold the largest share at 34.10% of 2025 revenue.

Which sales channel is growing fastest for jewelry in Brazil?

Online retail, including social commerce, is forecast to expand at an 7.76% CAGR.

What market share do women account for in Brazil’s jewelry purchases?

Women generate 68.75% of Brazil’s 2025 jewelry sales.

Page last updated on: