Gold Jewelry Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

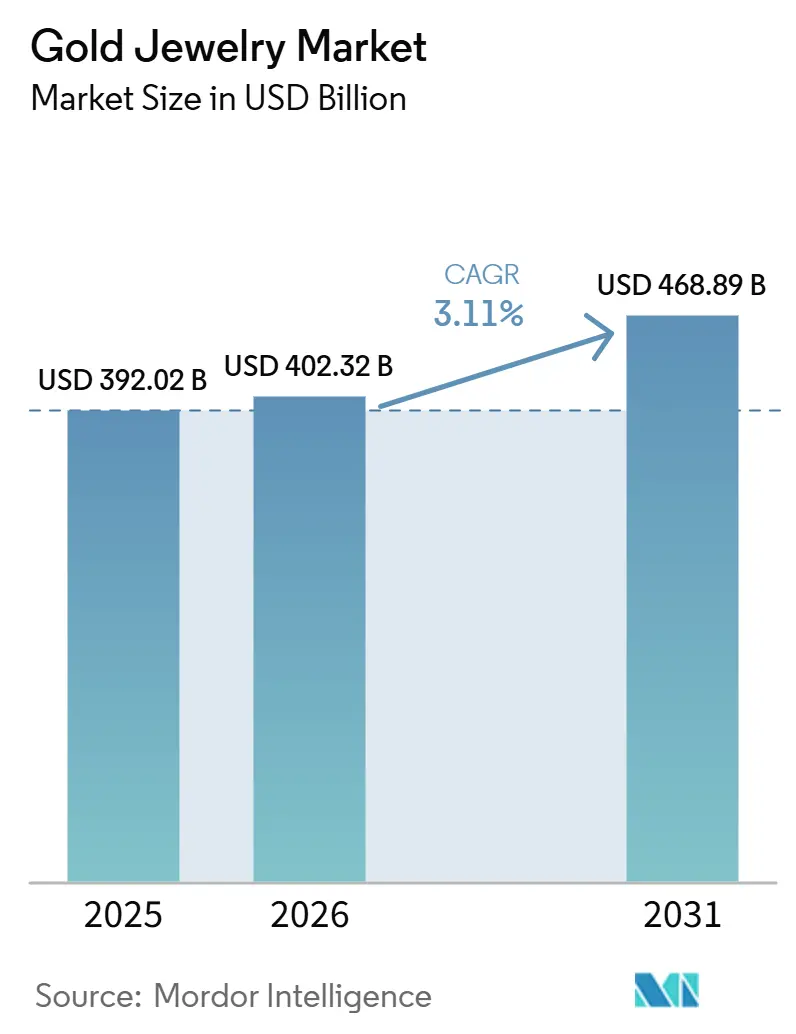

| Market Size (2026) | USD 402.32 Billion |

| Market Size (2031) | USD 468.89 Billion |

| Growth Rate (2026 - 2031) | 3.11% CAGR |

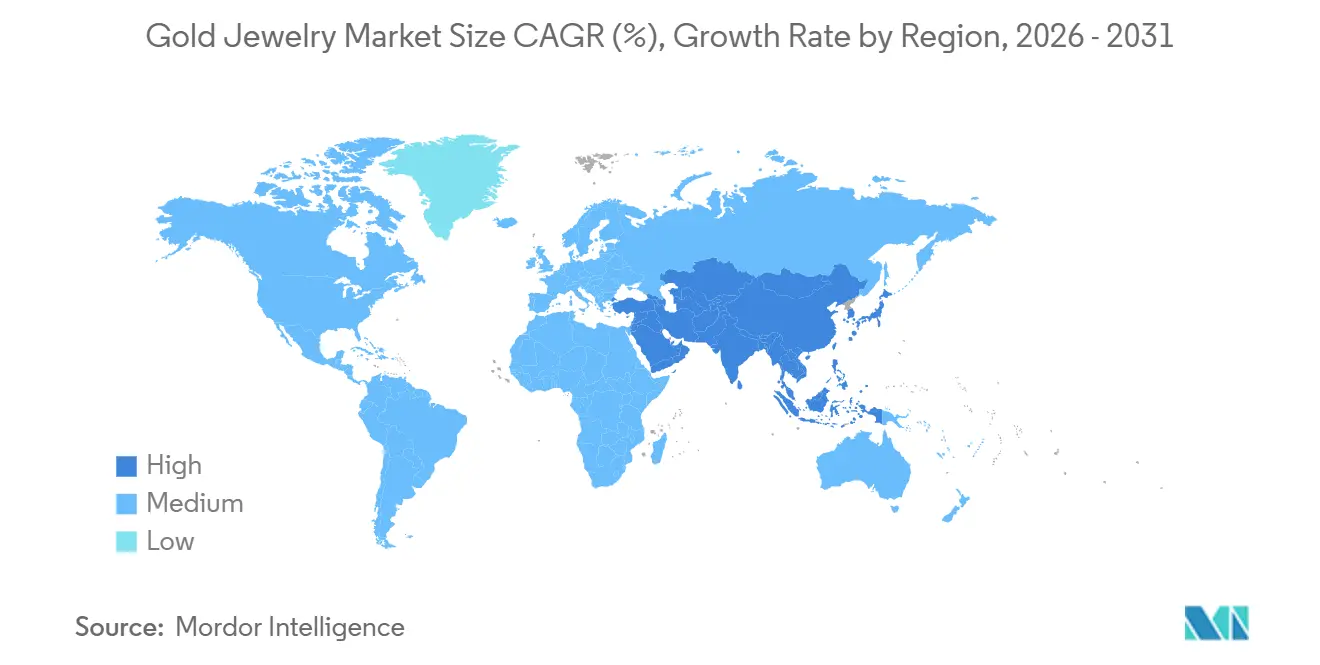

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gold Jewelry Market Analysis by Mordor Intelligence

The Gold Jewelry Market size is expected to increase from USD 392.02 billion in 2025 to USD 402.32 billion in 2026 and reach USD 468.89 billion by 2031, growing at a CAGR of 3.11% over 2026-2031. Market growth is driven by the unique positioning of gold jewelry as both a fashion accessory and a long-term value-preserving asset, supporting consistent demand across ceremonial, gifting, investment, and everyday wear categories. Increasing consumer preference for lightweight and contemporary designs, coupled with rising demand for personalized jewelry featuring engravings, modular elements, and symbolic motifs, is broadening product adoption across diverse consumer groups. Continuous innovation in manufacturing technologies, including 3D printing, precision casting, and AI-assisted jewelry design, is enabling brands to introduce intricate collections while improving production efficiency and reducing material wastage.

Key Report Takeaways

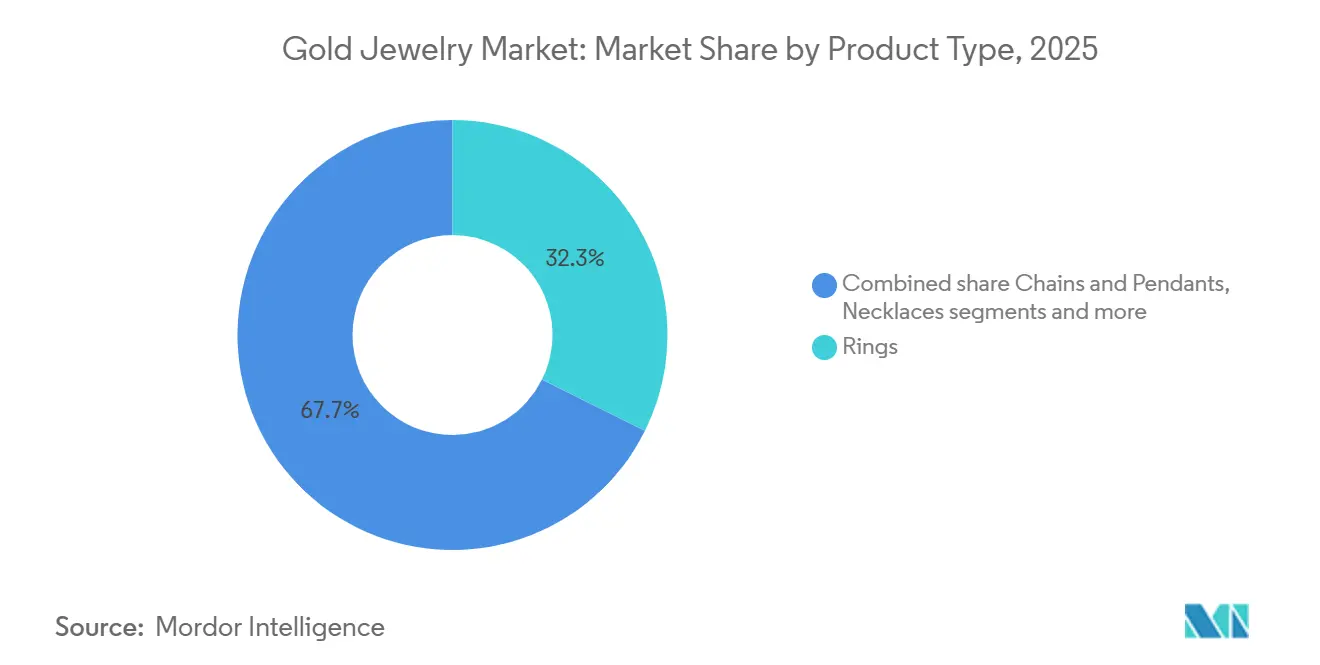

- By product type, rings led with 32.34% revenue share in 2025, while chains and pendants are forecast to expand at 4.45% CAGR through 2031.

- By karat or purity, 22-karat jewelry held 47.23% of the gold jewelry market size in 2025, while 18-karat jewelry is projected to grow at 3.81% CAGR through 2031.

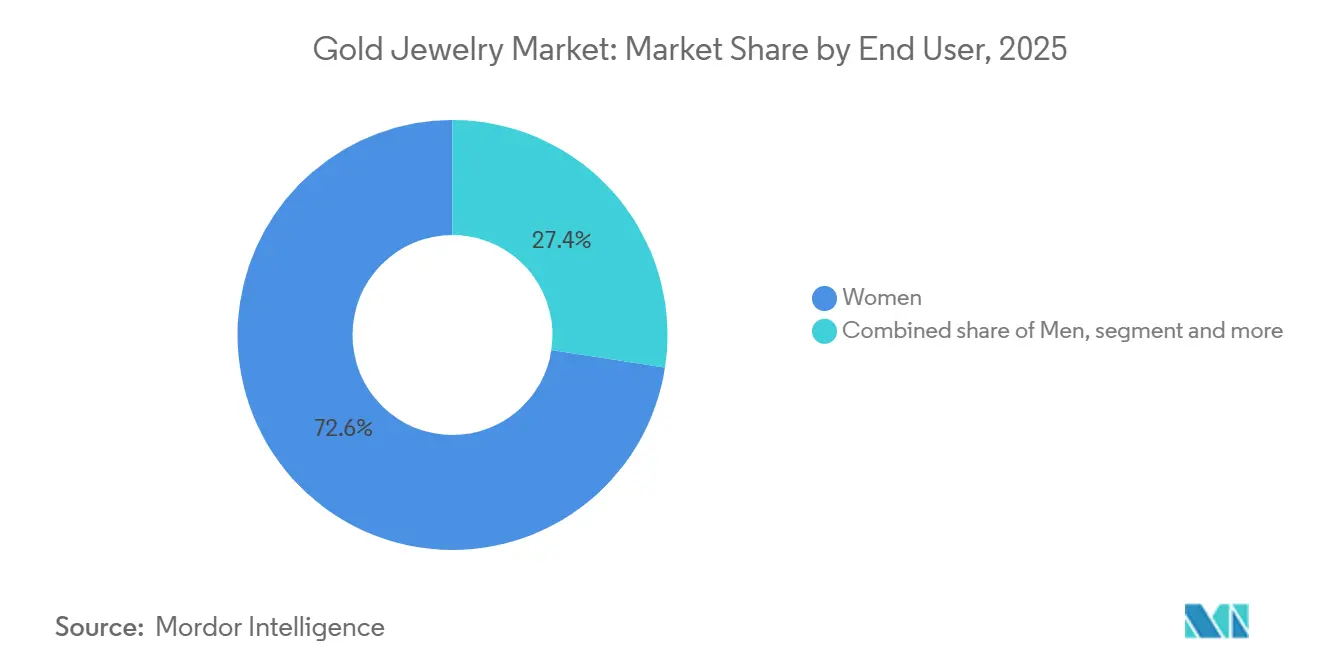

- By end user, women accounted for 73.24% of revenue in 2025, while men are forecast to record the highest CAGR at 4.86% through 2031.

- By distribution channel, offline retail stores held 81.27% share in 2025, while online retail stores are projected to advance at 5.23% CAGR through 2031.

- By geography, Asia-Pacific held 46.73% share in 2025, while the Middle East and Africa is forecast to grow at 4.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Gold Jewelry Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preference for lightweight and everyday wearable gold jewelry | +0.5% | Global; Asia-Pacific as primary demand centres, with early adoption in South and Southeast Asia | Short term (≤ 2 years) |

| Growing adoption of ethically sourced and responsibly produced gold | +0.4% | North America and Europe primary; spill-over to Asia-Pacific core urban markets | Long term (≥ 4 years) |

| Popularity of bridal, wedding, and ceremonial jewelry collections | +0.7% | Asia-Pacific core (India, China), Middle-East and Africa (Saudi Arabia), South America (Brazil, Colombia) | Short term (≤ 2 years) |

| Gold jewelry's role as a dual-purpose asset (adornment and investment) | +0.6% | Global; highest intensity in Asia-Pacific where formal savings instruments are limited | Medium term (2–4 years) |

| Demand for personalized and customized jewelry | +0.4% | North America, Europe, urban Asia-Pacific (China, South Korea, Japan) | Medium term (2–4 years) |

| Innovation in jewelry design and manufacturing technologies | +0.3% | Global; early commercial adoption in Asia-Pacific and Europe manufacturing clusters | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

Preference for lightweight and everyday wearable gold jewelry

The growing preference for lightweight, everyday wearable gold jewelry is a significant driver of the global gold jewelry market. Consumers are increasingly shifting from purchasing gold solely for weddings and special occasions to incorporating it into their daily wardrobes. Rising demand for minimalist rings, delicate chains, pendants, bracelets, and earrings that combine comfort, versatility, and contemporary aesthetics has encouraged manufacturers to expand lightweight collections using advanced production techniques such as precision casting, hollow construction, and 3D design. These techniques enable intricate craftsmanship with lower gold content. The market is further supported by regulatory initiatives that enhance consumer confidence in lightweight gold products. For instance, the Bureau of Indian Standards (BIS) announced that from July 2025, 9-karat gold will be included under mandatory hallmarking categories, expanding certified purity options and supporting the wider commercialization of affordable, hallmarked gold jewelry, thereby encouraging greater adoption of lightweight everyday wear collections [1]Source: Bureau of Indian Standards (BIS), "HALLMARKING", bis.gov.in.

Growing Adoption of ethically sourced and responsibly produced gold

The growing adoption of ethically sourced and responsibly produced gold is driving the global gold jewelry market, as consumers increasingly prioritize sustainability, transparency, and responsible sourcing when purchasing fine jewelry. Jewelry manufacturers are responding by strengthening traceability across their supply chains, adopting recycled gold, and sourcing precious metals from certified responsible mining and refining operations. These initiatives enhance brand credibility and help companies comply with evolving environmental, social, and governance (ESG) expectations, while differentiating their products in the premium jewelry segment. For instance, Chopard sources Chain of Custody Gold from Responsible Jewellery Council (RJC)-certified refineries, ensuring full traceability and adherence to internationally recognized responsible sourcing standards. Such initiatives are reinforcing consumer trust and accelerating the adoption of ethically produced gold jewelry worldwide.

Popularity of bridal, wedding, and ceremonial jewelry collections

The growing popularity of bridal, wedding, and ceremonial jewelry collections is a major driver of the global gold jewelry market. Gold holds strong cultural, religious, and symbolic significance in marriage ceremonies, festivals, and family celebrations across many regions. Consumers increasingly invest in elaborate bridal sets, necklaces, bangles, earrings, and other traditional ornaments that are often regarded as heirlooms and passed down through generations. To meet this demand, jewelry manufacturers are continuously launching bridal collections featuring contemporary craftsmanship, customizable designs, and coordinated jewelry sets that cater to evolving consumer preferences while preserving traditional aesthetics. The growing trend toward destination weddings, themed ceremonies, and premium bridal experiences is further encouraging purchases of high-value and designer gold jewelry, supporting market growth across both organized retail and luxury jewelry segments.

Gold jewelry's role as a dual-purpose asset

Gold jewelry serves a dual purpose as both a wearable luxury product and a tangible store of value, making it a key driver of the global gold jewelry market. Unlike many other jewelry categories, gold jewelry is widely perceived as an asset that can be resold, exchanged, pledged as collateral, or passed down through generations while retaining its intrinsic value. This combination of adornment and wealth preservation encourages consumers to purchase gold jewelry not only for personal use but also for long-term financial security and family legacy. In markets such as India and China, gold jewelry purchases are deeply embedded in cultural and ceremonial traditions, further reinforcing demand beyond purely financial motivations. Buyback, exchange, and gold upgrade programs offered by organized jewelry retailers further reinforce consumer confidence, supporting repeat purchases and sustained demand across both traditional and contemporary gold jewelry collections.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing competition from alternative jewelry materials | -0.5% | North America and Europe primary; spill-over to urban Asia-Pacific (China, South Korea, Japan) | Medium term (2–4 years) |

| Prevalence of counterfeit and low-purity gold products | -0.4% | Asia-Pacific (India, Southeast Asia), Middle-East and Africa | Short term (≤ 2 years) |

| Incidences of jewelry theft, robbery, and supply chain security risks | -0.2% | Global; concentrated in South Asia and North America | Short term (≤ 2 years) |

| Increasing preference for jewelry rental and sharing platforms | -0.2% | North America, Europe, and urban Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing competition from alternative jewelry materials

Growing competition from alternative jewelry materials is restraining the global gold jewelry market, as consumers increasingly explore products made from platinum, silver, titanium, stainless steel, tungsten, ceramics, and lab-grown diamond settings. These materials offer distinctive aesthetics, durability, and contemporary designs, and many are well suited for everyday wear, appealing to consumers seeking lightweight, low-maintenance, or fashion-oriented jewelry. Jewelry manufacturers are also expanding their portfolios with mixed-material and non-gold collections to address changing style preferences, intensifying competition for traditional gold jewelry. The rising popularity of these alternatives, particularly among younger consumers who prioritize design versatility and personalization over precious metal content, is limiting the growth potential of conventional gold jewelry across several product categories.

Prevalence of counterfeit and low-purity gold products

The prevalence of counterfeit and low-purity gold products is a significant restraint on the global gold jewelry market. It undermines consumer confidence, damages brand reputation, and creates uncertainty regarding product authenticity and purity. Counterfeit jewelry and fraudulent hallmarking practices expose consumers to financial losses while increasing compliance, testing, and certification costs for legitimate manufacturers and retailers. These challenges also lead to stricter regulatory oversight and additional verification requirements across the jewelry supply chain, raising operational complexity for industry participants. For instance, according to the United States Customs and Border Protection (CBP), in August 2025, CBP officers in Louisville intercepted a shipment containing more than 7,000 counterfeit luxury jewelry items [2]Source: Customs and Border Protection (CBP), "$30 million in counterfeit jewelry seized by Louisville CBP", cbp.gov. This highlights the growing scale of counterfeit jewelry entering global markets and reinforces the need for stronger authentication and traceability measures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rings Lead, Chains and Pendants Signal Everyday Momentum

Rings accounted for 32.34% of the global gold jewelry market in 2025, making them the largest product segment. This is largely due to their role in milestone purchases and long-standing cultural significance. Demand remains consistently strong as rings are widely purchased for engagements, weddings, anniversaries, graduations, and other commemorative occasions, creating a steady replacement and gifting cycle. The segment also benefits from continuous product innovation through adjustable sizing, mixed-metal craftsmanship, gemstone integration, and customizable engravings that enhance personalization. Retailers regularly introduce seasonal collections and limited-edition designs, encouraging repeat purchases and expanding the consumer base beyond traditional ceremonial use.

Chains and pendants are expected to record the fastest CAGR during 2026–2031, driven by evolving fashion preferences toward versatile, everyday jewelry. Unlike occasion-specific ornaments, chains and pendants are increasingly incorporated into daily wardrobes due to their lightweight construction, layering compatibility, and ability to complement both traditional and western attire. Growth is further supported by the rising popularity of symbolic and personalized pendants, including initials, religious motifs, birthstones, zodiac signs, and meaningful charms that create emotional attachment and gifting opportunities. Manufacturers are also introducing interchangeable pendant systems and modular collections that allow consumers to customize a single chain with multiple pendant designs, increasing product utility and encouraging additional purchases over time.

By Karat/Purity: 22 Karat Anchors Tradition as 18 Karat Captures New Audiences

22 Karat gold accounted for 47.23% of the global gold jewelry market in 2025, maintaining its dominant position due to its balance between high gold purity and practical durability. The segment benefits from strong consumer preference for jewelry that retains the traditional appearance and intrinsic value of gold while being suitable for intricate craftsmanship. Its widespread acceptance across ceremonial, bridal, festive, and heirloom jewelry collections has enabled manufacturers to offer a broad range of designs without compromising perceived value. Additionally, standardized hallmarking practices and increasing consumer awareness of purity certification continue to strengthen confidence in 22 Karat jewelry, reinforcing its position as the preferred choice for premium gold ornaments.

The 18 Karat segment is projected to register the fastest CAGR of 3.81% during 2026–2031, supported by growing demand for contemporary and design-oriented jewelry. Its enhanced hardness allows manufacturers to create lightweight, stone-studded, and precision-crafted pieces with greater structural strength than higher-purity gold, making it well suited for modern fashion collections. The segment is also witnessing increasing adoption in white gold and rose gold jewelry, where alloy composition enables diverse color finishes and innovative aesthetics. As consumers increasingly seek jewelry that combines durability with modern styling for regular wear, 18 Karat gold continues to gain traction across premium lifestyle collections and designer jewelry portfolios.

By End User: Women as the Core, Men as the Growth Frontier

Women accounted for 73.24% of the global gold jewelry market in 2025, maintaining the largest share due to the extensive use of gold jewelry across multiple life stages and wardrobe categories. Demand is supported by the wide variety of products designed specifically for women, ranging from everyday essentials to bridal, festive, office wear, and luxury collections. Jewelry brands continue to expand their women's portfolios through trend-driven collections, seasonal launches, and designer collaborations that cater to diverse fashion preferences. Additionally, the increasing availability of lightweight designs, interchangeable jewelry sets, and contemporary styling has encouraged more frequent purchases beyond traditional occasions, reinforcing the segment's market leadership.

The men's segment is projected to register the fastest CAGR of 4.86% during 2026–2031, driven by the growing acceptance of gold jewelry as a fashion and personal style accessory. Rising demand for minimalist chains, bracelets, signet rings, cufflinks, and pendants has encouraged manufacturers to develop dedicated men's collections featuring modern aesthetics and understated designs. The segment is also benefiting from expanding premium grooming and luxury lifestyle trends, with brands introducing gender-specific product lines and contemporary designs suited for professional and casual wear. Increasing adoption of personalized and statement jewelry among younger male consumers, supported by celebrity fashion influence and evolving style preferences, is further accelerating growth in this segment.

By Distribution Channel: Offline Dominates, Online Accelerates

Offline retail stores accounted for 81.27% of the global gold jewelry market in 2025, retaining their dominant position because gold jewelry purchases typically involve high-value transactions that require product inspection, purity verification, and personalized consultation before purchase. Consumers continue to prefer visiting physical stores to assess craftsmanship, weight, fit, and design while obtaining hallmark certification and after-sales services such as resizing, repairs, polishing, and exchange programs. The segment is further supported by the aggressive showroom expansion strategies of organized jewelry retailers, increasing accessibility across metropolitan, tier-II, and tier-III cities. For instance, by March 2026, Kalyan Jewellers operated 507 showrooms, while Malabar Gold & Diamonds expanded its retail network to more than 445 showrooms, reinforcing customer trust and enhancing market penetration through an extensive physical presence.

Online retail stores are projected to register the fastest CAGR of 5.23% during 2026–2031, driven by advancements in digital commerce and customer engagement technologies. Jewelry retailers are increasingly integrating virtual try-on solutions, AI-powered product recommendations, 360-degree product visualization, live video consultations, and secure digital payment options to replicate the in-store buying experience. The availability of extensive product catalogs, personalized customization tools, transparent purity certification, and convenient home delivery has broadened online adoption, particularly for lightweight and contemporary jewelry collections. Additionally, the growing integration of omnichannel retail models, enabling consumers to browse online, reserve products digitally, and complete purchases through flexible fulfillment options, is accelerating the shift toward online gold jewelry sales.

Geography Analysis

Asia-Pacific accounted for 46.73% of the global gold jewelry market in 2025, maintaining its position as the largest regional market. This is driven by a strong cultural affinity for gold, well-established jewelry production clusters, advanced craftsmanship, extensive retail networks, and continuous design innovation that support both domestic consumption and international trade. China and India remain the primary growth engines, supported by longstanding traditions of gold ownership, bridal jewelry demand, and a strong preference for high-purity gold ornaments. The region also plays a critical role in the global supply chain through large-scale gold refining and jewelry manufacturing capabilities. According to the World Gold Council, China produced approximately 384.3 tonnes of gold in 2025, reinforcing the region's position in raw material availability and downstream jewelry production [3]Source: World Gold Council, "Global mine production", gold.org.

The Middle East and Africa is projected to register the fastest CAGR of 4.83% during 2026–2031, supported by expanding organized jewelry retail, increasing tourism-driven luxury shopping, and sustained demand for high-purity gold jewelry. Growth is further supported by Saudi Arabia's Vision 2030 initiatives, which are encouraging retail modernization, luxury retail expansion, and greater participation of international jewelry brands. Across the Gulf Cooperation Council, gold jewelry continues to play an integral role in weddings, religious celebrations, and gifting traditions, sustaining strong demand for 22-karat collections. In Sub-Saharan Africa, the expansion of branded jewelry retailers, improved retail infrastructure, and increasing local jewelry manufacturing capabilities are further strengthening the region's growth prospects.

North America, Europe, and South America continue to contribute steadily to the global gold jewelry market through evolving consumer preferences and product innovation. North America is witnessing growing demand for lightweight, personalized, and contemporary gold jewelry, supported by expanding online retail, customization services, and premium branded collections. Europe remains a key center for luxury gold jewelry, benefiting from renowned craftsmanship, designer collections, and increasing adoption of sustainable and recycled gold, which is reshaping product development across the region. South America is experiencing gradual market expansion through the modernization of jewelry retail, rising popularity of branded collections, and increasing preference for everyday wearable gold jewelry, alongside the region's growing domestic gold refining and jewelry manufacturing capabilities.

Competitive Landscape

The global gold jewelry market features large multinational luxury brands, vertically integrated manufacturers, and organized retail chains competing through product innovation, retail expansion, purity assurance, and omnichannel strategies. Major players, including Chow Tai Fook Jewellery Group Limited, Signet Jewelers Limited, Titan Company Limited, Rajesh Exports Limited, and Lao Feng Xiang Co., Ltd., continue to strengthen their market positions by expanding branded showroom networks, introducing contemporary and lightweight collections, enhancing hallmark certification practices, and investing in digital customer engagement platforms. Competition is increasingly centered on design differentiation, customer trust, customization capabilities, and integration of online and offline sales channels rather than price alone.

Manufacturers are increasingly adopting advanced jewelry production technologies to improve operational efficiency and accelerate product development. AI-assisted jewelry design, automated manufacturing, 3D printing, and digital product visualization are enabling companies to shorten product development cycles while offering personalized collections at scale. AI-powered mass-customization infrastructure is reducing the operational barriers associated with personalized gold jewelry, allowing manufacturers to deliver customized engravings, modular designs, and made-to-order collections at non-luxury price points. Investments in traceability technologies, digital hallmark verification, and responsible gold sourcing are also becoming important competitive differentiators as consumer demand for transparency continues to grow.

The competitive landscape presents opportunities in the mid-market digital retail segment, where established physical jewelry brands remain comparatively underrepresented. Growing adoption of e-commerce, virtual try-on solutions, AI-based styling recommendations, and omnichannel fulfillment models is enabling both established players and emerging brands to expand beyond traditional showroom-led sales. Companies that successfully combine digital-first customer experiences with efficient customization capabilities, certified product authenticity, and agile design innovation are expected to strengthen their competitive positioning as the global gold jewelry market continues to evolve.

Gold Jewelry Industry Leaders

-

Chow Tai Fook Jewellery Group Limited

-

Signet Jewelers Limited

-

Titan Company Limited

-

Rajesh Exports Limited

-

Lao Feng Xiang Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Dhirsons has introduced AAROH, a lightweight 14K and 18K gold jewellery collection targeting younger consumers seeking fine jewellery for personal milestones and everyday occasions.

- March 2026: Jos Alukkas has introduced an augmented reality (AR)-based virtual try-on feature on its online store, developed in partnership with mirrAR. The feature allows customers to virtually try on jewellery products, including necklaces, earrings, bangles, and rings, using their device cameras.

- July 2025: Arjun Jewellers launched a new gold jewellery showroom in Jamnagar. The showroom offers a range of handcrafted modern gold ornaments that combine traditional designs with contemporary styles.

Global Gold Jewelry Market Report Scope

Gold jewellery refers to personal ornaments such as rings, necklaces, earrings, and others, often serving as a symbol of wealth, prestige, and cultural heritage. The gold jewelry market is segmented by product type, karat/purity, end user, distribution channel, and geography. Based on product type, the market is segmented into rings, necklaces, earrings, bracelets, chains and pendants, and other product types. Based on karat/purity, the market is segmented into 24 karat, 22 karat, 18 karat, and others. Based on end user, the market is segmented into men, women, and children. Based on distribution channel, the market is segmented into offline retail stores and online retail stores. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecast have been done based on the value (in USD million).

| Rings |

| Necklaces |

| Earrings |

| Bracelets |

| Chains and Pendants |

| Other Product Types |

| 24 Karat |

| 22 Karat |

| 18 Karat |

| Others |

| Men |

| Women |

| Children |

| Offline Retail Stores |

| Online Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Rings | |

| Necklaces | ||

| Earrings | ||

| Bracelets | ||

| Chains and Pendants | ||

| Other Product Types | ||

| By Karat/Purity | 24 Karat | |

| 22 Karat | ||

| 18 Karat | ||

| Others | ||

| By End User | Men | |

| Women | ||

| Children | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected value of the gold jewelry market by 2031?

The gold jewelry market is forecast to reach USD 468.89 billion by 2031, rising from USD 402.32 billion in 2026 at a 3.11% CAGR.

Why is market value rising even though jewelry volumes have declined?

In 2025, global jewelry consumption fell to 1,542.3 tonnes, but demand value still rose to USD 172 billion because higher gold prices lifted spending per purchase.

Which product category leads global demand for gold jewelry?

Rings led the market in 2025 with 32.34% share, supported by bridal demand, gifting use, and broad price accessibility.

Which channel is growing fastest for gold jewelry sales?

Online retail stores are projected to grow at 5.23% CAGR through 2031, even though offline stores still held 81.3% share in 2025.

Page last updated on: