Luxury Car Rental Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

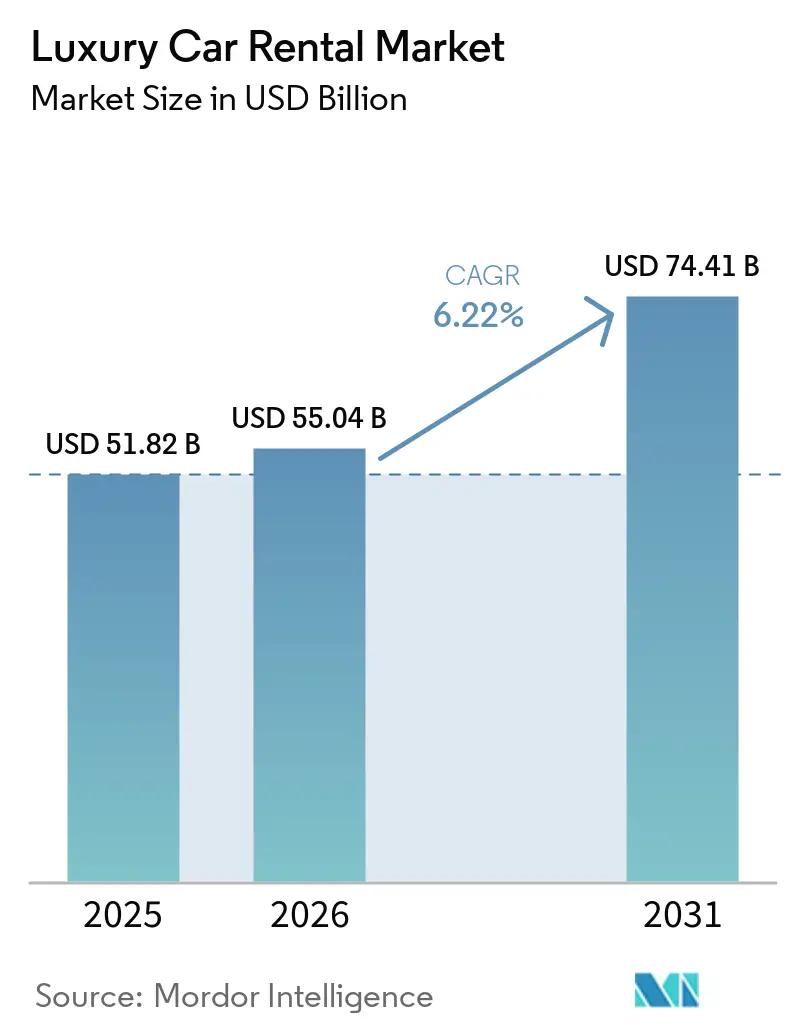

| Market Size (2026) | USD 55.04 Billion |

| Market Size (2031) | USD 74.41 Billion |

| Growth Rate (2026 - 2031) | 6.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Luxury Car Rental Market Analysis by Mordor Intelligence

The Luxury Car Rental market size was valued at USD 51.82 billion in 2025 and estimated to grow from USD 55.04 billion in 2026 to reach USD 74.41 billion by 2031, at a CAGR of 6.22% during the forecast period (2026-2031). Strong pent-up demand for premium travel, the rapid expansion of digital booking channels, and sustained growth in the global high-net-worth individual (HNWI) base are accelerating fleet utilization. China’s 14% annual rise in luxury-vehicle purchases, the rebound of corporate “bleisure” travel, and record vehicle availability in airport and downtown locations continue to underpin double-digit growth in Asia-Pacific, which already commands the largest regional share. Operators are prioritizing battery-electric vehicles (BEVs) to comply with zero-emission rules. Yet, elevated repair costs and depreciation risk—highlighted by Hertz’s sale of 20,000 EVs—are prompting a more selective electrification path. Competitive intensity is rising as peer-to-peer platforms and subscription models redraw the lines between rental, leasing, and ownership, compelling incumbents to scale technology and fleet partnerships to protect margins[1]“Enterprise Holdings Reports FY 2024 Results,”, Enterprise Holdings, enterpriseholdings.com.

Key Report Takeaways

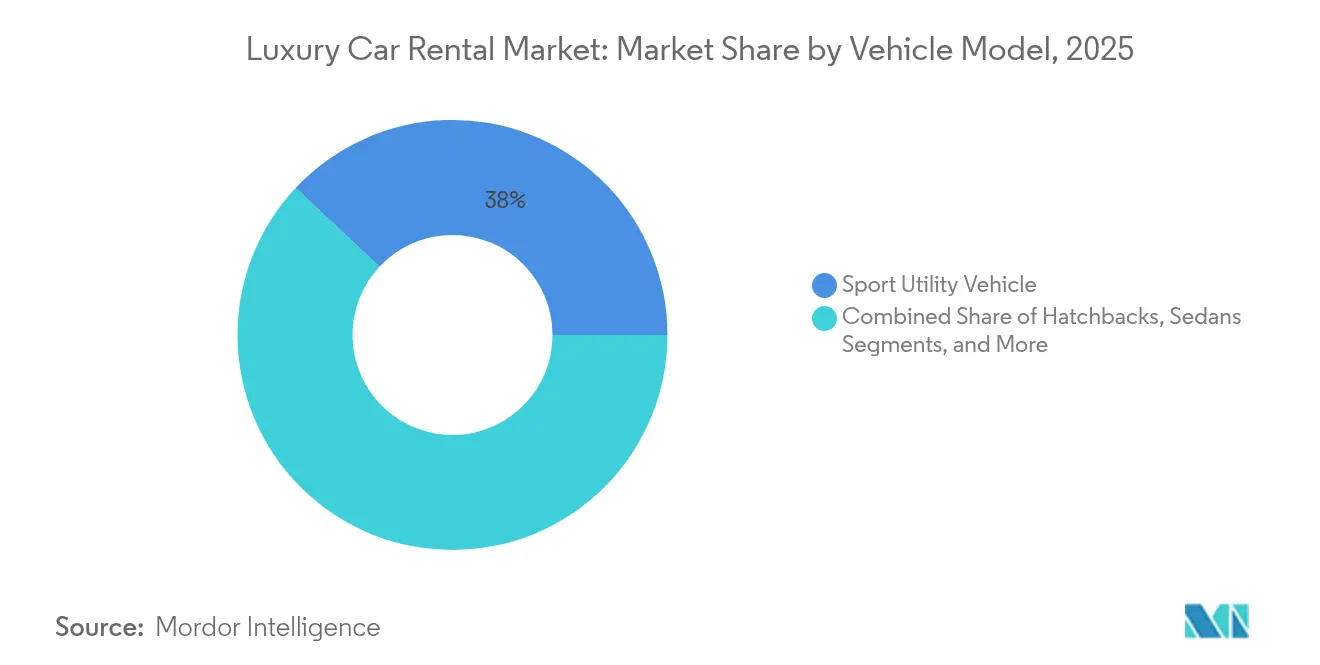

- By vehicle model style, Sport Utility Vehicle led with 38.02% of the luxury car rental market share in 2025 and is projected to expand at an 8.27% CAGR between 2026-2031.

- By rental duration, short-term hires accounted for 63.58% of the luxury car rental market size in 2025, whereas long-term and subscription services are the fastest-growing at a 9.31% CAGR through 2031.

- By booking channel, online reservations captured 47.12% of transactions in 2025, while aggregator and OTA platforms are set to grow at a 10.34% CAGR during 2026-2031.

- By drive type, self-drive rentals dominated with 68.05% luxury car rental market share in 2025 and are advancing at a 7.05% CAGR over the forecast period.

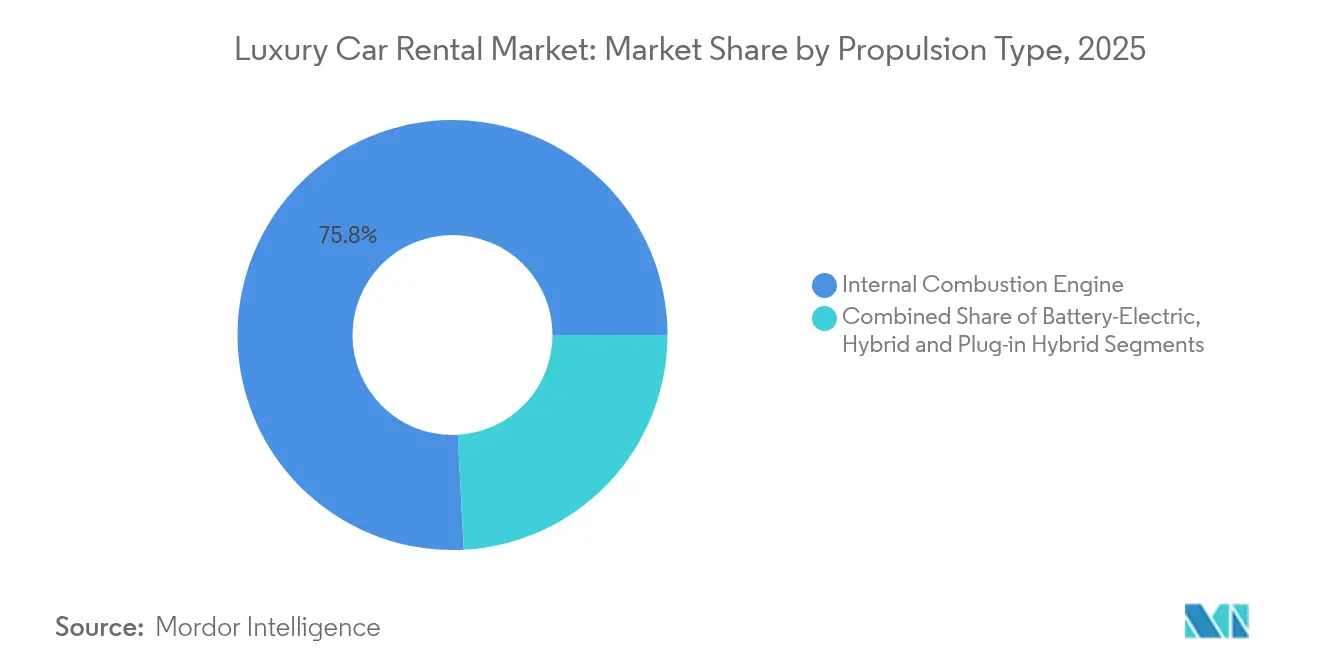

- By fuel type, internal-combustion vehicles held 75.84% of the luxury car rental market size in 2025, whereas battery-electric vehicles represent the fastest-growing segment at a 15.02% CAGR.

- By customer type, leisure and individual renters commanded 55.88% share in 2025, while the corporate and MICE segment is recording the highest 8.87% CAGR through 2031.

- By service location, airport stations maintained 46.12% of luxury car rental market share in 2025, yet downtown urban outlets are growing quickest at an 8.54% CAGR.

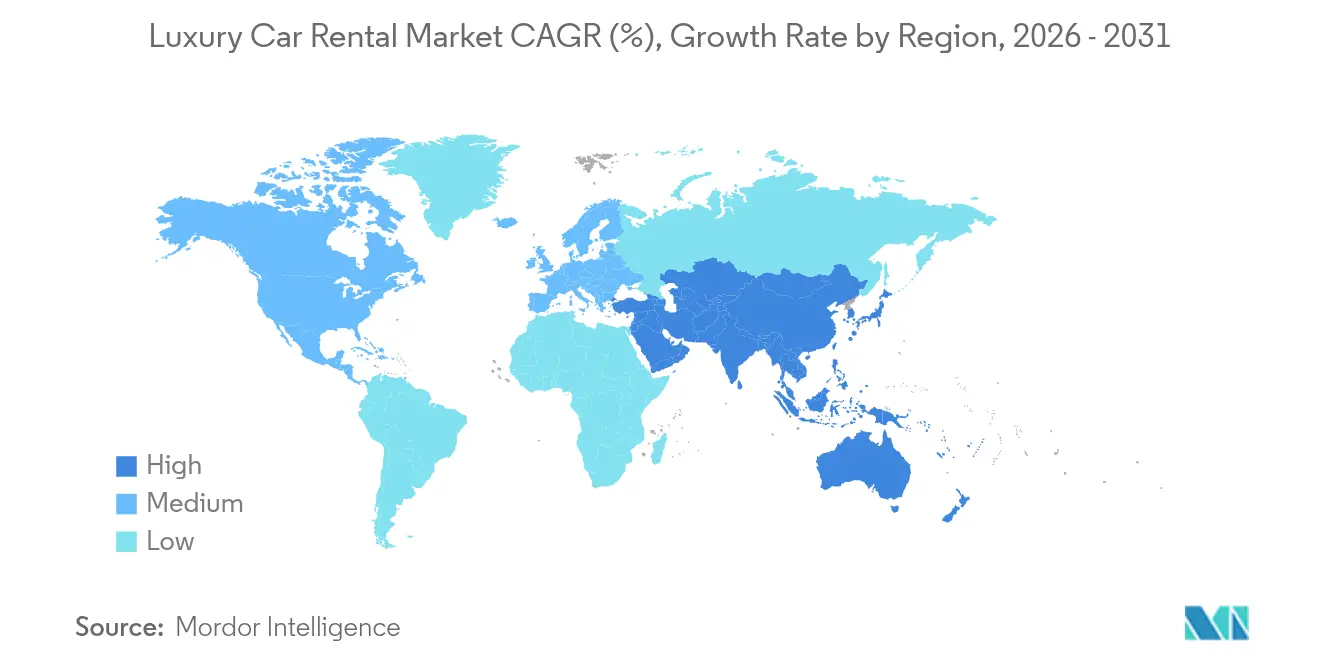

- By geography, Asia-Pacific captured 38.24% revenue share of the luxury car rental market in 2025 and is forecast to post the strongest 11.52% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Luxury Car Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic leisure & business travel surge | +1.8% | North America & Europe lead, global spill-over | Medium term (2-4 years) |

| Rising global HNWI population | +1.5% | Asia-Pacific core, North America & Europe spill-over | Long term (≥ 4 years) |

| Digital-first aggregator & subscription rise | +1.2% | Early traction in North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Rapid EV penetration to meet zero-emission rules | +0.9% | Europe & Asia-Pacific dominant, early adoption in North America | Medium term (2-4 years) |

| Experiential gifting & influencer marketing | +0.6% | Major urban centers worldwide | Short term (≤ 2 years) |

| Blockchain-enabled asset tracking | +0.3% | North America & Europe first movers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Post-Pandemic Leisure & Business Travel

Global business-travel outlays are increasing, and fifty-two percent of corporate buyers increased budgets in 2024, and 46% of employees extended work trips for personal leisure, reinforcing premium rental demand. Luxury travel spending among affluent segments is on track to rise 42% by 2028, with experiential mobility now a core component of vacation packages. Operators report longer average rental lengths as travelers look to maximize value from high-end vehicles during multi-purpose trips. Corporate accounts are taking bigger fleets under master contracts, guaranteeing supply during peak periods, and increasing pricing power[2]“2024 BTI Outlook,”, Global Business Travel Association, gbta.org.

Growing Global HNWI Population & Disposable Incomes

China is forecast to become the world’s largest personal-luxury arena by 2030, and 40% of its consumers will pay premiums for ESG-aligned products. Millennials and women now hold one-third of HNWI wealth, demanding digital booking, wellness integration, and brand authenticity. Eighty percent of luxury travelers under 60 prefer experiences over possessions, a mindset that favors on-demand access to marquee models. These demographic shifts are reshaping fleet mixes toward bespoke interiors, in-car wellness tech, and limited-edition trims that command higher daily rates.

Expansion of Digital-First Aggregator & Subscription Platforms

Online aggregator bookings are growing at 10.78% CAGR; vehicle subscriptions could balloon from 2025 to 2030. Eighty-five percent of subscription interest clusters are in premium marques, with 28% of consumers aged 18-34 favoring flexible access over outright rental. Avis Budget Group now secures 87% of reservations through digital channels. At the same time, Turo’s partnership with Uber will list privately owned luxury cars on Uber Rent from 2025, tapping a USD 150 billion car-sharing prize pool. AI-enabled dynamic pricing, usage-based insurance, and keyless entry APIs are becoming table stakes for large operators.

Rapid EV Penetration in Premium Fleets to Meet City-Center Zero-Emission Rules

Europe’s impending ban on new internal-combustion sales by 2035 and the UK’s 2030 deadline are forcing fleets to electrify. SIXT agreed to purchase up to 250,000 Stellantis vehicles, aiming for 70-90% electrified European units by 2030. Nevertheless, Hertz incurred a USD 245 million charge after disposing of 20,000 EVs, proving residual-value volatility remains a hurdle. Luxury EV revenue could still reach USD 345.51 billion by 2027 as charging infrastructure stabilizes and city-center access rules tighten. Operators are piloting battery-health analytics to optimize resale timing and hedge depreciation risk[3]“Rental & Car Club Members’ Road to Zero Report,”, BVRLA, bvrla.co.uk.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost & accelerated depreciation of luxury vehicles | −1.4% | Europe & North America most exposed | Medium term (2-4 years) |

| Urban shift toward ride-hailing & micro-mobility | −0.8% | Asia-Pacific & Europe dense metros | Short term (≤ 2 years) |

| Stringent insurance, liability & age-limit regulations | −0.6% | Europe & North America legislative hotspots | Long term (≥ 4 years) |

| Supply constraints for premium EV models delaying fleet renewal | −0.9% | Europe & Asia-Pacific showroom shortages | Medium term (2-4 years |

| Source: Mordor Intelligence | |||

High Capital Cost & Accelerated Depreciation of Luxury Vehicles

Acquiring flagship models now requires 22% higher capex than pre-pandemic levels, driven by advanced driver-assist hardware and battery packs. Tesla’s price cuts shaved up to 17% off used-EV residuals in 2024, prompting Hertz to liquidate 20,000 cars and absorb a USD 245 million writedown. Average global daily rental rates are expected to climb 2.4% to USD 46.5 in 2025 as operators pass on higher holding costs. Smaller franchisees with limited financing flexibility face slower fleet refresh cycles, widening the technology gap versus majors[4]“Hertz Updates Fleet Strategy,”, Hertz Global Holdings, hertz.com.

Rising Preference for Ride-Hailing & Micro-Mobility in Urban Cores

Premium ride-hail tiers now cover 210 global cities, offering on-demand Mercedes, BMW, and Lexus models that compete directly with short-term rentals. Millennials living in dense urban zones cite parking hassle and congestion fees as key reasons for skipping rentals in favor of chauffeurs or e-scooters. In Shanghai and Paris, municipal policies encourage shared mobility by allocating curb space to app-based services, cutting point-to-point travel time by up to 15%. The luxury car rental industry must adapt by integrating ride-hail APIs or repositioning depots to the city edge where self-driving demand persists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Model Style: SUVs Drive Premium Segment Growth

In 2025, Sport Utility Vehicles (SUVs) captured 38.02% of the luxury car rental market, underscoring a growing consumer preference for spacious interiors, elevated seating, and adaptable cargo space. This segment is set to expand at an annual rate of 8.27% through 2031, with prominent brands like Range Rover, Mercedes-Benz G-Class, and BMW iX leading the charge. Electric SUVs like the Lotus Eletre are trickling into flagship rental garages, signaling how sustainability and luxury converge. Sedans retain relevance among chauffeur-driven executives, while sports and supercars cater to weekend indulgence and influencer content creation.

Hatchbacks maintain niche appeal in Europe’s narrow streets, whereas MPVs support luxury family travel in Gulf Cooperation Council (GCC) resorts. As OEMs allocate marketing budgets toward high-riding silhouettes, rental companies expand premium SUV inventory to future-proof demand. The luxury car rental market size for SUVs is expected to widen its lead by adding 4.3 percentage points of share during the forecast horizon.

By Rental Duration: Subscription Models Reshape Long-Term Demand

In 2025, short-term rentals (under 30 days) dominated the luxury car rental market with a 63.58% share, primarily driven by airport-origin trips. However, long-term rentals and subscription models are emerging as the fastest-growing segments, boasting a 9.31% CAGR. This surge is largely attributed to the customer preference for predictable monthly payments, bundled maintenance, and a diverse vehicle selection. Half of subscribers swap models every four months, driving higher utilization cycles per asset and improving return on capital employed.

Corporate fleet managers lean on six- to 24-month rentals to avoid depreciation exposure and to pilot EV adoption before making procurement decisions. As a result, the luxury car rental market is integrating fintech payment plans, telematics-based wear-and-tear monitoring, and concierge drop-off services. Therefore, the luxury car rental industry is blurring boundaries with operating lease providers, galvanizing policymakers to update tax codes around benefit-in-kind treatment.

By Booking Channel: Digital Aggregators Accelerate Market Transformation

Online bookings secured a 47.12% share of the luxury car rental market in 2025 and are on a double-digit growth trajectory, while aggregator and OTA platforms are set to grow at a 10.34% CAGR during 2026-2031.. This momentum is fueled by mobile-centric designs, real-time availability showcases, and seamless checkout processes. Aggregators bundle loyalty perks across airlines and hotels, amplifying exposure without heavy marketing spend by operators. Direct apps run by majors such as SIXT now embed one-tap upgrades and tiered carbon-offset options, deepening wallet share.

Offline travel advisers still handle complex multi-country itineraries but now rely on cloud-based inventory pipes to quote in real time. Keyless pickup technology lets clients bypass counters altogether, shrinking labor costs and raising customer satisfaction scores. These innovations keep the luxury car rental market competitive against ride-hail alternatives in high-yield segments.

By Drive Type: Self-Drive Dominance Reflects Independence Preferences

Self-drive rentals constituted 68.05% of the luxury car rental market in 2025, with projections indicating a 7.05% annual growth. This trend is driven by discerning drivers' desire for hands-on experiences with advanced infotainment and premium performance features. Advanced safety suites and over-the-air updates reinforce confidence in navigating unfamiliar terrain.

Chauffeur demand endures for diplomatic convoys, VIP roadshows, and red-carpet events, where privacy and protocol weigh heavily. Premium ride-hail encroaches on short urban hops, yet multi-day event itineraries still favor chartered chauffeurs for scheduling flexibility. Autonomous driving pilots under Level 3 standards could redefine drive-type segmentation later in the decade.

By Propulsion Type: Electric Vehicles Surge Despite Operational Challenges

While internal combustion vehicles dominated the luxury car rental market with a 75.84% share in 2025, battery electric vehicles (BEVs) are making significant inroads, registering a 15.02% CAGR, propelled by regulatory incentives and eco-conscious luxury consumers. Jaguar, Bentley, and Rolls-Royce committed to full electrification timelines, compelling rental partners to secure allocation slots years ahead. Luxury car rental market share for BEVs is limited by charging-station density and extended repair cycles, which elevate downtime.

Hybrid and Plug-in hybrids play a bridging role by extending combined range beyond 600 km, meeting chauffeur-drive expectations for airport transfers without recharge stops. Residual-value insurance is emerging to cushion fleets against tech obsolescence risk, forwarding-hedging one of the sector’s most acute cost exposures.

By Customer Type: Corporate Segment Drives Recovery Momentum

In 2025, leisure renters accounted for 55.88% of the luxury car rental market. However, corporate clients and MICE (Meetings, Incentives, Conferences, and Exhibitions) travelers are the segment's fastest-growing demographic, with a projected 8.87% CAGR through 2031. This growth is fueled by a resurgence in conference activities and heightened duty-of-care standards that lean towards premium service providers. Firms view luxury rentals as brand-extension tools and employee-experience boosters, often bundling carbon offsets to align with ESG reporting.

Bleisure itineraries lengthen hire periods by an average of 1.6 days, supporting higher fleet utilization. Event planners negotiate multi-vehicle packages for delegate shuttles and board-level hospitality journeys, including branded in-car ambient media.

By Service Location: Urban Centers Challenge Airport Dominance

Airports contributed 46.12% of the luxury car rental market's revenue in 2025, capitalizing on the influx of arriving passengers. Yet, downtown pickup locations and hotel lobbies are witnessing an 8.54% CAGR growth. This shift is attributed to the revival of business districts and tourists' preference for centrally situated lodgings. Furthermore, businesses collaborate with upscale malls and luxury hotels to establish micro-depots, streamlining the last-mile delivery process.

Resort locations deliver strong average daily rate (ADR) premiums, especially where scenic drives are part of the destination allure, such as the Amalfi Coast or Queenstown. Urban congestion pricing could nudge more leisure drivers toward public transit, yet upscale shoppers booking “experience weekends” still justify inner-city branches. Fleet allocation thus rotates seasonally between airports, downtown, and resort nodes to balance peaks.

Geography Analysis

Asia-Pacific accounted for 38.24% of the luxury car rental market revenue in 2025, propelled by China’s thriving luxury ecosystem and rapid urban affluence. Regional CAGR of 11.52% through 2031 surpasses all peers, driven by supportive EV incentives, inbound tourism rebounds in Japan and Thailand, and the surge of ultra-high-net-worth families in Singapore and India. Enterprise Mobility’s entrance into Phuket and Bangkok via franchise partnerships illustrates the magnetism of Southeast Asian leisure hubs.

North America remains a mature, high-yield arena with deep corporate-travel roots and sophisticated loyalty programs. By late 2024, U.S. airport throughput had neared 2019 records, revitalizing premium rentals, while cross-border traffic with Canada and Mexico broadened trip patterns. Enterprise Mobility's record USD 38 billion turnover underscores pricing power amid constrained fleet supply. The high penetration of digital payment wallets and contactless pick-up further cements the region’s technological edge.

Climate mandates, heterogeneous tax regimes, and volatile macroeconomic conditions shape Europe’s pathway. Operators accelerate fleet electrification to comply with zero-emission zones in Amsterdam, Paris, and Milan, often re-routing older ICE cars to less restrictive markets in Eastern Europe. The Middle East and Africa post mid-single-digit growth, led by GCC tourism recovery and premium safari circuits in South Africa and Kenya, although currency volatility and import duties temper margin expansion.

Competitive Landscape

The luxury car rental market features moderate concentration. The major players like Enterprise Mobility leverage a multi-brand portfolio—from National to Exotic Car Collection—to maximize channel coverage, whereas SIXT differentiates via tech-forward user interfaces and premium station design. Avis Budget Group funnels predictive AI into dynamic pricing, lifting utilization rates by 320 basis points yearly.

Peer-to-peer platforms such as Turo and Getaround unlock idle private luxury inventory, pressuring incumbents on price transparency and customer review visibility. Turo’s 2025 alliance with Uber will expose its hosts to 150 million ride-hail users, exponentially enlarging its demand pipeline. Subscription providers, including Care by Volvo and Porsche Drive, deepen competition by offering fixed-monthly packages that blur the lines between rental and ownership.

Electrification strategy is a major differentiator: SIXT’s Stellantis deal secures future EV supply, whereas Hertz’s partial divestiture spotlights operational growing pains. Smaller regional specialists such as Midway Car Rental in California and Prestige in the UAE maintain niche leadership through bespoke concierge services, local know-how, and exotic supercar fleets.

Luxury Car Rental Industry Leaders

Enterprise Holdings Inc.

The Hertz Corporation

Avis Budget Group Inc.

Sixt SE

Europcar Mobility Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: SIXT USA, a subsidiary of global premium mobility leader Sixt SE, has inaugurated its 50th U.S. airport outlet at John Wayne Airport (SNA) in Orange County, California. This location is in the greater Los Angeles metropolitan area, the third most populous county in the state. This milestone underscores SIXT's aggressive expansion in the U.S., which now caters to 50 key airports and boasts over 100 locations across 25 states.

- January 2024: Turo partnered with Uber to list privately owned luxury vehicles on Uber Rent, opening fresh premium supply streams.

- January 2024: SIXT sealed a multi-billion-euro agreement with Stellantis for up to 250,000 vehicles through 2026.

Global Luxury Car Rental Market Report Scope

Luxury car rental involves renting high-end vehicles from rental service providers for travel, leisure, or business purposes on an hourly or longer-term basis, offering a flexible transportation solution without the commitment of ownership.

The luxury car rental market is segmented by vehicle model style, rental duration, booking type, drive type, and geography. By vehicle model style, the market is segmented into hatchbacks, sedans, sports utility vehicles, and multi-purpose vehicles. By rental duration, the market is segmented into short-term and long-term. By booking type, the market is segmented into online booking and offline booking. By drive type, the market is segmented into self-driven and chauffeur-driven. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. For each segment, the market sizing and forecast have been done based on the value (USD).

| Hatchback |

| Sedan |

| Sport Utility Vehicle |

| Multi-Purpose Vehicle |

| Sports & Super-car |

| Short-term ( Less Than 30 days) |

| Long-term / Subscription (More Than 30 days) |

| Online Direct (own website / app) |

| Online Aggregator / OTA |

| Offline Travel Agent / Walk-in |

| Self-drive |

| Chauffeur-drive |

| Internal Combustion Engine |

| Battery-Electric Vehicle |

| Hybrid and Plug-in Hybrid Vehicle |

| Leisure Individual |

| Corporate / MICE |

| Airport |

| Urban Downtown |

| Resort / Tourist Hotspot |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| By Vehicle Model Style | Hatchback | |

| Sedan | ||

| Sport Utility Vehicle | ||

| Multi-Purpose Vehicle | ||

| Sports & Super-car | ||

| By Rental Duration | Short-term ( Less Than 30 days) | |

| Long-term / Subscription (More Than 30 days) | ||

| By Booking Channel | Online Direct (own website / app) | |

| Online Aggregator / OTA | ||

| Offline Travel Agent / Walk-in | ||

| By Drive Type | Self-drive | |

| Chauffeur-drive | ||

| By Propulsion Type | Internal Combustion Engine | |

| Battery-Electric Vehicle | ||

| Hybrid and Plug-in Hybrid Vehicle | ||

| By Customer Type | Leisure Individual | |

| Corporate / MICE | ||

| By Service Location | Airport | |

| Urban Downtown | ||

| Resort / Tourist Hotspot | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the luxury car rental market?

The luxury car rental market stands at USD 55.04 billion in 2026 and is projected to grow to USD 74.41 billion by 2031, reflecting a 6.22% CAGR.

Which region leads the luxury car rental market?

Asia-Pacific leads with 38.24% share in 2025 and is forecast to grow at an 11.52% CAGR, driven by China’s expanding luxury-consumer base and EV incentives.

Why are subscription services important for luxury car rentals?

Subscription models offer flexible, all-inclusive access and are expanding at 9.31% CAGR, appealing to younger consumers and corporates seeking predictable costs.

Who are the key players in the luxury car rental space?

Major operators include Enterprise Mobility, SIXT, Avis Budget Group, Hertz, and Europcar.

How are zero-emission regulations affecting luxury car rental strategies?

European and U.K. bans on new ICE vehicle sales are accelerating fleet electrification, prompting deals such as SIXT’s purchase of up to 250,000 electrified models from Stellantis.

Page last updated on: