Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

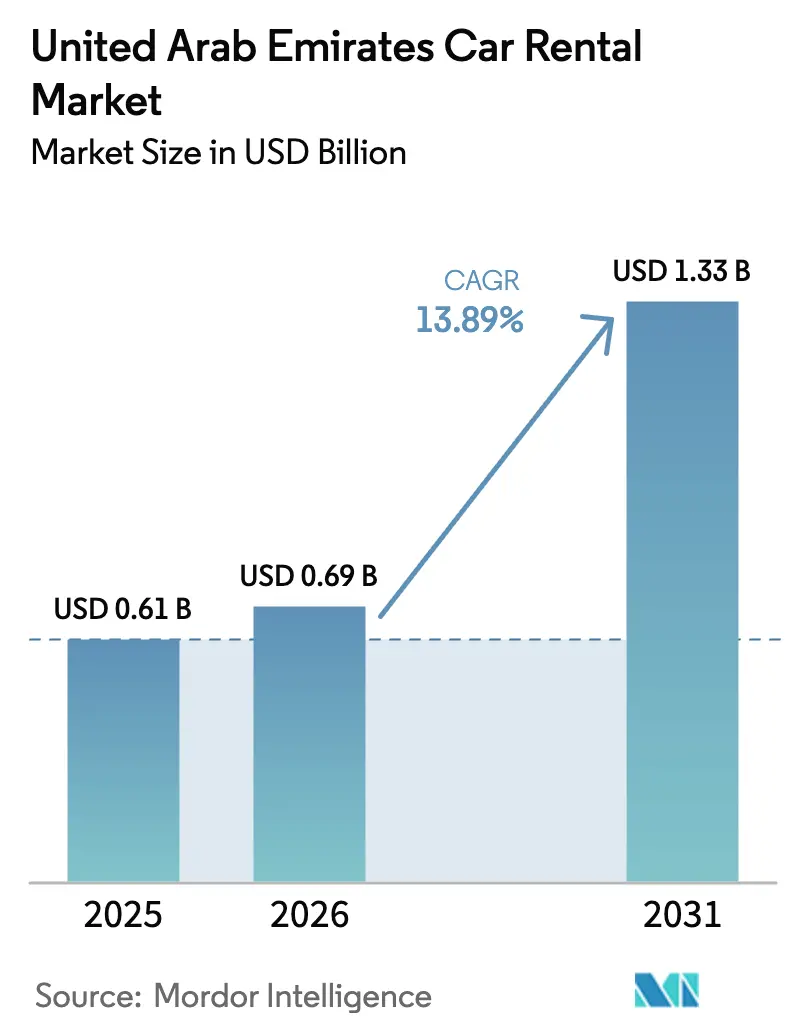

| Base Year Market Size (2025) | USD 0.61 Billion |

| Market Size (2026) | USD 0.69 Billion |

| Market Size (2031) | USD 1.33 Billion |

| Growth Rate (2026 - 2031) | 13.89% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Arab Emirates Car Rental Market Analysis by Mordor Intelligence

The UAE car rental market size was valued at USD 0.61 billion in 2025 and estimated to grow from USD 0.69 billion in 2026 to reach USD 1.33 billion by 2031, at a CAGR of 13.89% during the forecast period (2026-2031). Strong inbound tourism, steady corporate travel recovery, and rapid digitalization reinforce rental demand, while government policies favor fleet electrification and contactless service models. Platform-based operators continue to reduce customer acquisition costs, enabling dynamic pricing that boosts fleet utilization. Growing executive travel across free zones sustains premium fleet demand, even as stringent traffic-violation fines and ride-hailing price wars squeeze margins. Investment momentum remains intact because a large, diversified visitor base ensures resilience against cyclical shocks, and regulatory initiatives such as extended lifespans for electric vehicles improve total cost-of-ownership economics.

Key Report Takeaways

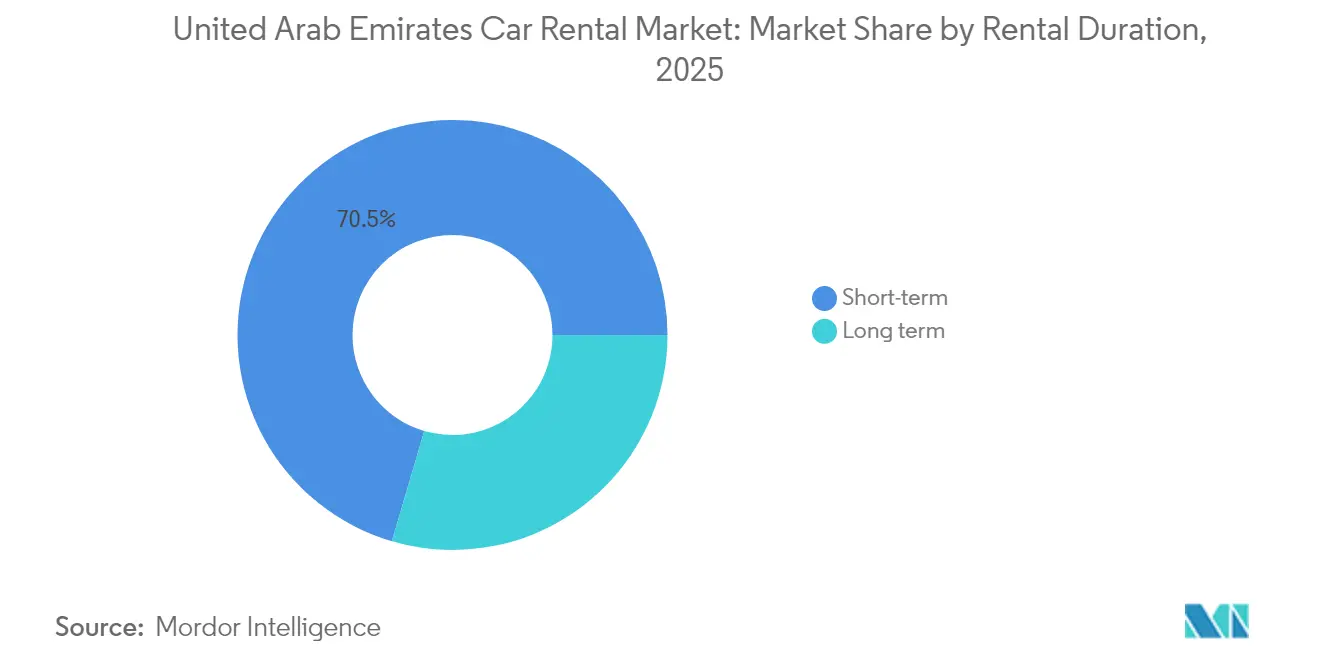

- By rental duration, short-term rentals held 70.45% of the United Arab Emirates car rental market share in 2025, while long-term rentals are projected to expand at an 11.21% CAGR through 2031.

- By booking type, online channels captured 63.25% revenue share of the United Arab Emirates car rental market size in 2025 and are forecast to grow at a 14.35% CAGR to 2031.

- By driving type, self-driven rentals commanded 77.12% of the United Arab Emirates car rental market in 2025; chauffeur-driven services represent the fastest-growing niche with a 14.24% CAGR through 2031.

- By vehicle type, budget and economy cars led with 68.35% revenue share of the United Arab Emirates car rental market in 2025, whereas premium and luxury rentals are advancing at a 14.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Car Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of Inbound Tourism | +1.8% | UAE-wide, concentrated in Dubai and Abu Dhabi | Short term (≤ 2 years) |

| Government Push for EV-based Rental Fleets | +1.5% | National, with early adoption in Dubai and Abu Dhabi | Medium term (2-4 years) |

| Rising Digital-first Consumer Behaviour | +1.2% | UAE-wide, strongest in urban emirates | Short term (≤ 2 years) |

| Expansion of Corporate Long-term Leasing Programs | +0.8% | Dubai, Abu Dhabi business districts | Medium term (2-4 years) |

| Rise in Mega-events | +0.7% | Dubai, with spillover to Abu Dhabi and Northern Emirates | Long term (≥ 4 years) |

| Surge in Gig-economy | +0.6% | Urban emirates, concentrated in Dubai and Sharjah | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth of Inbound Leisure Tourism

Visitor arrivals continued to climb through 2025, sustaining all-season rental demand that peaks during November–May when cooler weather favors outdoor activities. Expanded airport capacity, new hotel inventory, and event-centric attractions—from World Expo legacies to Formula 1 in Abu Dhabi—translate directly into higher fleet utilization for operators positioned near key arrival hubs. Airline partnerships and visa-on-arrival privileges now attract tourists from Asia and Africa, broadening the addressable customer pool. Leisure travelers prefer the flexibility of multiday rentals for inter-emirate itineraries, driving average rental durations higher. Seasonality remains pronounced, with Ramadan and Eid holidays boosting volumes by roughly one-third, allowing companies to deploy surge pricing strategies. Demand predictability enables proactive fleet planning, reducing idle time and enhancing return on assets. Additionally, according to eZhire, car ownership in major GCC cities is projected to decline by 10% by 2030, driven by the rapid adoption of AI-powered mobility solutions and shifting lifestyle preferences[1]"On-Demand Mobility Gains Traction: eZhire Predicts a 10% Drop in Car Ownership by 2030," Bizpreneur Middle East, bizpreneurme.com.

Government Push for EV-Based Rental Fleets

The National EV Policy mandates 50% electric adoption by 2050 and already grants electric rentals six-year lifespans, versus four years for internal-combustion fleets. Dubai regulations go further, allowing premium electric cars to operate for up to 10 years, which favorably shifts residual value curves for high-end fleets. Early movers enjoy marketing advantages with sustainability-minded tourists and corporate clients that prioritize ESG reporting. Capital outlays are partially offset by lower energy and maintenance costs as fast-charging infrastructure expands along major corridors. Fleet rotation strategies are changing, with operators phasing out older sedans to finance electric crossovers that meet range requirements for inter-city trips. For lagging firms, compliance costs rise as internal-combustion residuals soften ahead of stricter 2030 targets.

Rising Digital-First Consumer Behavior

Mobile booking apps captured principal transaction value in 2024 and are still growing double-digit, underpinning the competitive edge of technology-centric operators. Seamless e-KYC, digital key handovers, and AI-driven damage assessment shorten pickup times, reducing branch overheads. Real-time data feeds enable predictive maintenance scheduling, cutting unexpected downtime and safeguarding the customer experience. Government-approved car-sharing pilots such as Udrive legitimize app-based rentals, spurring further consumer adoption. Cashless payments lower fraud risks and accelerate working-capital cycles, but smaller firms struggle with the upfront cost of platform development. Data analytics deepen customer insight, empowering loyalty-based upselling of insurance, accessories, and premium models.

Expansion of Corporate Long-Term Leasing Programs

Free-zone multinationals outsource fleet management to rental specialists to sidestep ownership depreciation and administration tasks. Contracts spanning 24–48 months assure operators of baseline utilization, stabilizing revenue in off-peak tourist seasons. Employers value bundled offerings—insurance, servicing, replacement vehicles—because they cap transportation budgets and simplify expense audits. Gig-economy delivery partners likewise demand month-to-month light-commercial vans, creating a new recurring-revenue pocket. Regulatory familiarity with tender processes favors incumbents, while telematics provided to corporate clients enable mileage-based billing and proactive safety coaching. Competitive tendering, however, pushes margins lower, reinforcing the need for scale economies and efficient life-cycle cost control.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Traffic-Violation Penalties | -1.1% | UAE-wide, particularly Dubai and Abu Dhabi | Short term (≤ 2 years) |

| Growing Ride-Hailing Price Competitiveness | -0.9% | Urban emirates, concentrated in Dubai | Short term (≤ 2 years) |

| Limited Residual-Value For ICE Fleets | -0.7% | National, affecting all fleet operators | Long term (≥ 4 years) |

| High Insurance Premiums | -0.5% | UAE-wide, strongest impact in Dubai and Abu Dhabi | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Traffic-Violation Penalties and Fines

Enhanced smart-camera networks automatically bill violations to car owners, shifting liability to rental companies when tourists depart before fines clear. Operators now pre-authorize larger deposits and deploy in-vehicle telematics to alert drivers of speeding thresholds. Insurance premiums for under-25 drivers rose in 2024, inflating total rental cost and dampening youth uptake. Additional back-office staffing is required to reconcile fines across multiple emirates, adding overhead. Firms educate customers through multilingual tutorials at pickup, yet longer check-in times reduce throughput. Persistent enforcement keeps accident rates low, but the administrative burden constrains smaller agencies lacking digital violation-management tools.

Growing Ride-Hailing Price Competitiveness

Daily ride-hailing bundles rival short-term rental rates for city-center stays where parking fees erode rental value. Surge promotions by Uber and Careem during peak tourist seasons intensify customer switching. Autonomous pilot fleets in Abu Dhabi hint at future structural cost declines that could undercut economy rentals. Corporate clients test mobility-as-a-service subscriptions for urban staff, reallocating travel budgets away from traditional leases. Rental companies respond with weekend packages and loyalty points redeemable for free upgrades to preserve share. Ride-hailing remains less suitable for multi-day desert excursions and luggage-heavy family trips, ensuring coexistence rather than wholesale displacement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rental Duration: Short-Term Leasing Accelerates Revenue Stability

Short-term contracts contributed a 70.45% share of the United Arab Emirates car rental market in 2025, and long-term rentals posted an 11.21% CAGR to 2031. The UAE car rental market size attributed to this segment is forecast to rise rapidly as multiyear fleet outsourcing gains board-level approval across finance, tech, and energy sectors. Mileage-inclusive packages lower total mobility cost, and telematics-supported preventive maintenance minimizes downtime. Rental firms deploy residual-value forecasting tools to align lease pricing with evolving EV resale curves, lowering balance-sheet risk.

Short-term rentals continue anchoring the UAE car rental market through tourist inflows, but growth moderates as ride-hailing absorbs some city-use occasions. Seasonal fleet swelling remains essential; firms leverage auction partnerships for quick divestment after peak periods. Add-on revenue—from navigation units to child seats—keeps per-transaction profitability attractive. Collaboration emerges when operators cross-market weekend deals to corporate lessees, smoothing utilization across weekdays and holidays.

By Booking Type: Online Channels Cement Dominance

Online platforms generated 63.25% of the United Arab Emirates car rental market revenue in 2025, with a 14.35% CAGR during the forecast period. Operators leverage AI-enabled rate engines to alter prices hourly, capturing consumer surplus during demand spikes. In-app upselling of collision-damage waivers lifts ancillary margins. Partnerships with airline and hotel apps funnel high-intent traffic directly into booking funnels, cutting aggregator fees.

Offline counters remain relevant for luxury rentals involving personalized vehicle handover and corporate invoice processing requiring on-site signatures. Yet branch networks are rationalizing footprints, relocating space savings into fleet electrification and software. Contactless kiosks in hotel lobbies combine the immediacy of physical presence with the efficiency of QR-code transactions, blending both channels.

By Driving Type: Self-Driven Services Gain Executive Traction

Self-drive options secured a 77.12% share of the United Arab Emirates car rental market in 2025, thanks to cost-effectiveness and privacy preferences. Still, chauffeured rides are projected to outpace overall market growth at a 14.24% CAGR through 2031, as productivity-minded executives outsource driving. Companies recognize value in en-route virtual meetings, justifying premium rates. Concierge-style perks—gate-side airport pickups, multilingual drivers—differentiate top-tier providers. Google Maps is widely used across the UAE, and Senyar offers an integrated navigation system for locating addresses.

Regulations stipulating RTA-licensed drivers and enhanced insurance elevate entry barriers, limiting supply to vetted operators. Fleet managers rotate drivers among EV sedans to showcase sustainability credentials to C-suite clients. Self-drive services counter with optional roadside-assistance apps and flexible return stations, sustaining their appeal among leisure travelers who prize spontaneity and extended mileage allowances.

By Vehicle Type: Premium and Luxury Rentals Accelerate

Budget and economy cars hold a 68.35% share of the United Arab Emirates car rental market in 2025, providing essential mobility for price-sensitive tourists and expatriates. However, premium models such as high-performance SUVs are expanding at a 14.05% CAGR through 2031, well ahead of the United Arab Emirates car rental market growth. Social-media-driven status signaling fuels demand for exotic models, especially during high-profile events. Extended 10-year operating windows for luxury EVs increase lifetime revenue potential, encouraging fleet diversification toward Tesla, Mercedes-EQ, and BMW i lines.

Economy fleets increasingly consist of fuel-efficient compacts that meet corporate sustainability metrics without premium pricing. Operators hedge residual risk via manufacturer buy-back programs, keeping refresh cycles under three years. Cross-segment bundling—upgrade offers for birthdays or conference delegations—creates revenue synergies and raises brand equity.

Geography Analysis

Dubai dominated the United Arab Emirates car rental market value in 2024 due to unmatched air connectivity, an extensive hotel pipeline, and dense business clusters. Mega-events such as COP28 and Art Dubai create predictable occupancy spikes that allow dynamic fleet deployment into downtown and resort corridors. Regulatory agility, including pilot approvals for autonomous shuttles, positions Dubai as a test-bed for future mobility formats.

Abu Dhabi is anchored by sovereign-wealth-fund headquarters, energy majors, and government agencies that require long-term executive transport. Cultural landmarks like Louvre Abu Dhabi and the Yas Marina circuit attract affluent tourists who favor luxury models, reinforcing premium-fleet utilization. The emirate’s Green Mobility strategy subsidizes fast chargers at hotels and malls, driving early electric-fleet ROI.

Tourism boosters—from Khor Fakkan cruises to mountain adventure parks—are widening leisure itineraries beyond Dubai-Abu Dhabi corridors, stimulating inter-emirate rental demand. Federal initiatives to harmonize parking regulations and toll-payment systems are easing cross-border fleet operations, making regional expansion financially viable for mid-scale firms.

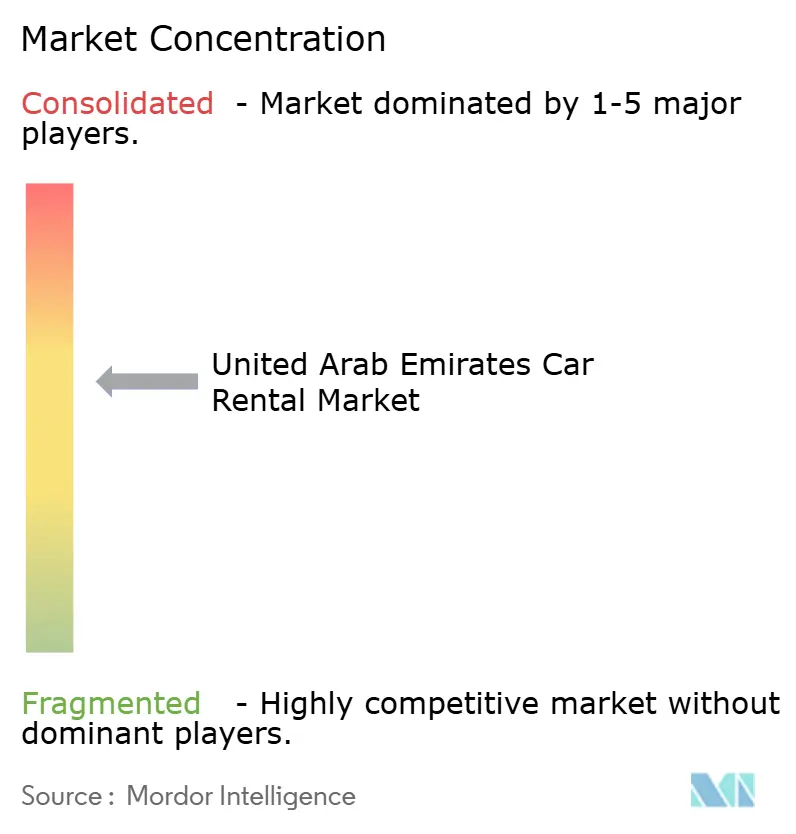

Competitive Landscape

Global giants leverage airport concessions, loyalty programs, and multi-country corporate contracts to secure volume. Local specialists counter with hyper-localized pricing, flexible payment options, and Arabic-language customer support. Digital-native entrants like eZhire and Udrive pursue asset-light models, sourcing cars from partner fleets and monetizing through subscription plans.

Technology has become the primary battlefield: API-driven booking, AI-guided dynamic pricing, and telematics-based risk scoring differentiate winners. Capital requirements for constant software upgrades and EV procurement nudge smaller firms toward mergers or niche specialization. Fleet insurers reward telematics adoption with premium discounts, providing a financial incentive for data-rich platforms. The Dubai Roads and Transport Authority's regulatory framework supports market development through streamlined licensing procedures and technology integration initiatives, while maintaining safety standards through comprehensive oversight mechanisms.

White-space opportunities persist in corporate long-term leasing, luxury EV experiences, and logistics van rentals supporting last-mile delivery. Heightened compliance audits by the RTA further professionalize the sector, tilting competitive advantage toward firms with robust governance footprints.

United Arab Emirates Car Rental Industry Leaders

-

SIXT SE

-

The Hertz Corporation

-

Avis Budget Group Inc.

-

Europcar International

-

Enterprise Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: RentCarUAE.com unveiled a cutting-edge car rental aggregation platform, designed to boost business growth for car rental firms throughout the United Arab Emirates.

- February 2025: Al Dhile Rent A Car introduced its premium car rental services in Dubai, UAE. By prioritizing a seamless and hassle-free experience, the company aims to revolutionize convenience and affordability in the car hire sector.

United Arab Emirates Car Rental Market Report Scope

Car renting refers to the business of leasing and renting a car from rental service providers based on some valuation. This renting can be on an hourly basis or for a longer time span.

The car renting market is segmented by rental duration type, booking type, application type, driving type and vehicle type. By rental duration type , the market has been segmented into short term and long term. By booking type, the market has been segmented into online and offline. By application type, the market has been segmented into daily utility and tourism. By driving type, the market has been segmented into self-driven and chaffeur and by vehicle type, the market is segmented into economy cars, luxury cars and SUV. For each segment, the market sizing and forecasting are based on value (USD million).

By Rental Duration

| Short-Term (Less than 30 days) |

| Long-Term (More than 30 days) |

By Booking Type

| Online |

| Offline |

By Driving Type

| Self-Driven |

| Chauffeur-Driven |

By Vehicle Type

| Budget/Economy |

| Premium/Luxury |

| By Rental Duration | Short-Term (Less than 30 days) |

| Long-Term (More than 30 days) | |

| By Booking Type | Online |

| Offline | |

| By Driving Type | Self-Driven |

| Chauffeur-Driven | |

| By Vehicle Type | Budget/Economy |

| Premium/Luxury |

Key Questions Answered in the Report

How big is the UAE car rental market in 2026?

The UAE car rental market size is USD 0.69 billion in 2026 and is projected to reach USD 1.33 billion by 2031.

What is the forecast growth rate for car rentals in the UAE?

Market revenue is expected to advance at a 13.89% CAGR between 2026 and 2031.

Which rental duration segment is growing fastest?

Long-term leasing leads growth with an 11.21% CAGR, driven by corporate outsourcing of fleet management.

How prominent are online bookings in UAE car rentals?

Digital platforms already account for 63.25% of revenue and are expanding at a 14.35% CAGR.

What impact does fleet electrification have on rental operators?

Extended vehicle lifespans, lower operating costs, and ESG-driven demand make electric fleets increasingly profitable, although high upfront investment remains a hurdle.

Which emirate generates the highest rental demand?

Dubai contributes major market share owing to its tourism infrastructure and international business hub status.

Page last updated on: