Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

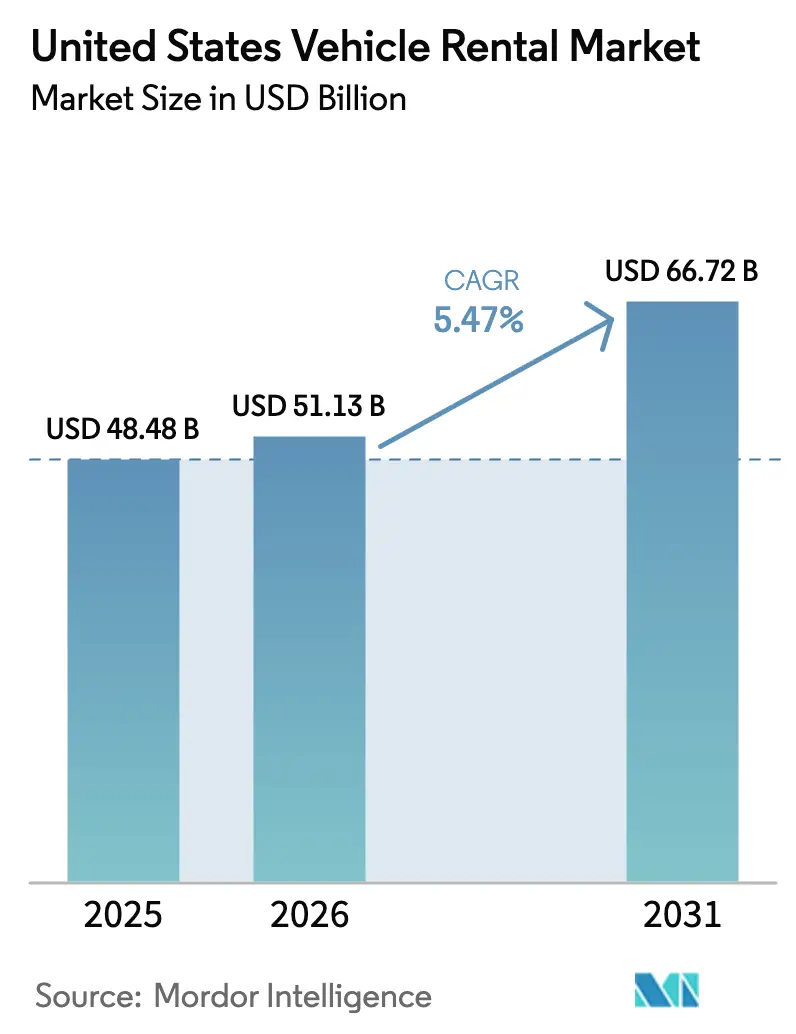

| Base Year Market Size (2025) | USD 48.48 Billion |

| Market Size (2026) | USD 51.13 Billion |

| Market Size (2031) | USD 66.72 Billion |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

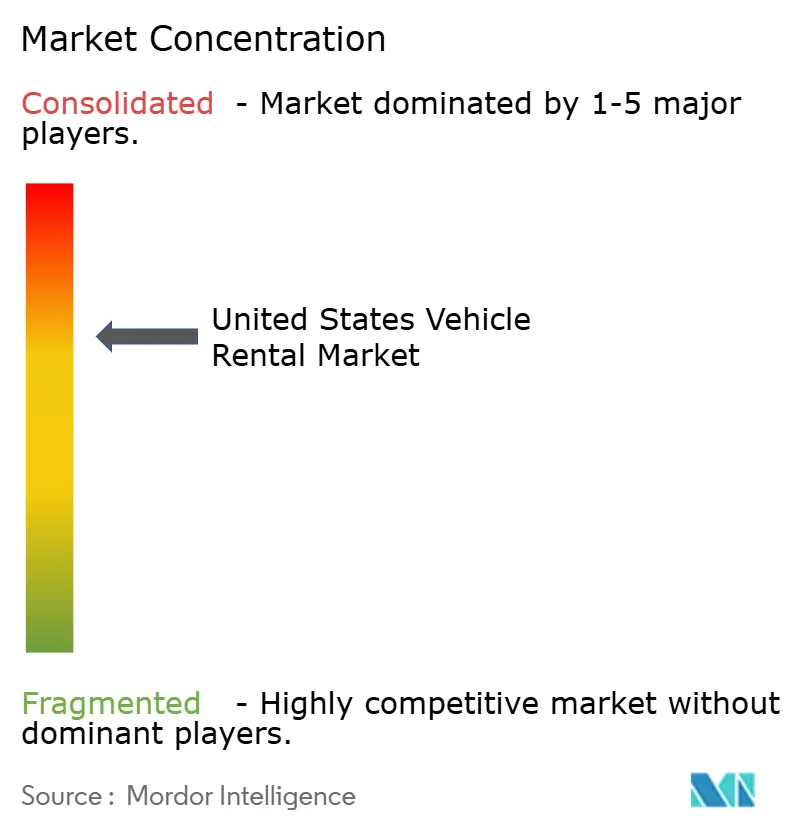

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Vehicle Rental Market Analysis by Mordor Intelligence

The United States vehicle rental market size is expected to grow from USD 48.48 billion in 2025 to USD 51.13 billion in 2026 and is forecast to reach USD 66.72 billion by 2031 at a 5.47% CAGR over 2026–2031. Despite facing challenges like persistent vehicle shortages and rising airport fees, the U.S. car rental market is witnessing a revenue boost. Factors such as pent-up leisure demand, hybrid-work travel patterns, and a surge in digital bookings, coupled with OEM fleet incentives, are driving this uptick. Operators are turning to advanced strategies: dynamic pricing engines that frequently adjust rates, telematics significantly reducing downtime, and cross-regional fleet rebalancing, all aimed at maintaining high utilization rates. While electrification is a key focus—especially with California's Advanced Clean Cars II rule pushing for a substantial share of zero-emission sales in the near future—Hertz's significant EV write-down has instilled a cautious approach to procurement. Peer-to-peer platforms are expanding their reach, utilizing a large number of privately owned vehicles. However, potential tax parity bills in several states pose a risk, threatening to diminish their competitive price advantage. In this evolving landscape, the U.S. car rental industry is transitioning from a traditional asset-management approach to a more sophisticated, data-centric mobility services model.

Key Report Takeaways

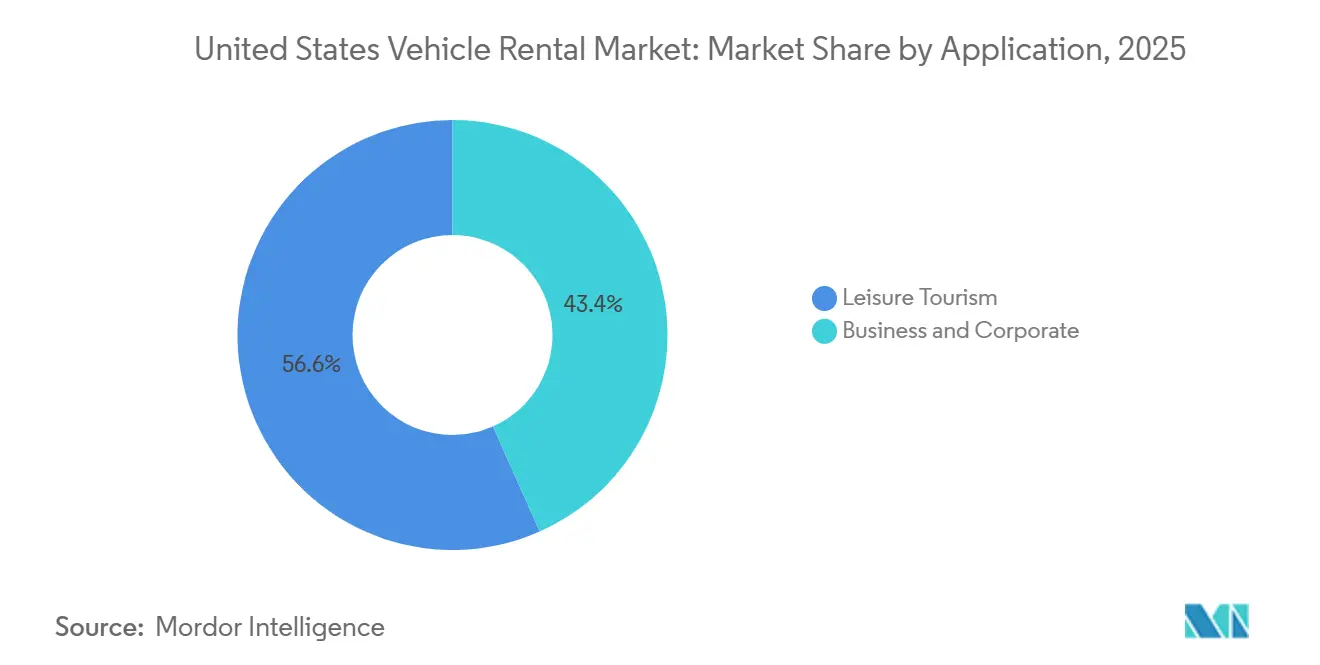

- By application, leisure and tourism captured 56.71% of the United States car rental market share in 2025, while business and corporate is projected to grow at a 5.49% CAGR through 2031.

- By vehicle type, passenger cars commanded 63.37% of the United States car rental market size in 2025 and are expanding at the segment-leading 5.57% CAGR to 2031.

- By booking channel, online reservations held a 71.35% share in 2025; this channel is expected to advance at a 5.59% CAGR through 2031.

- By rental duration, short-term rentals accounted for 67.73% revenue in 2025, whereas long-term rentals exhibited the fastest 5.51% CAGR over the forecast.

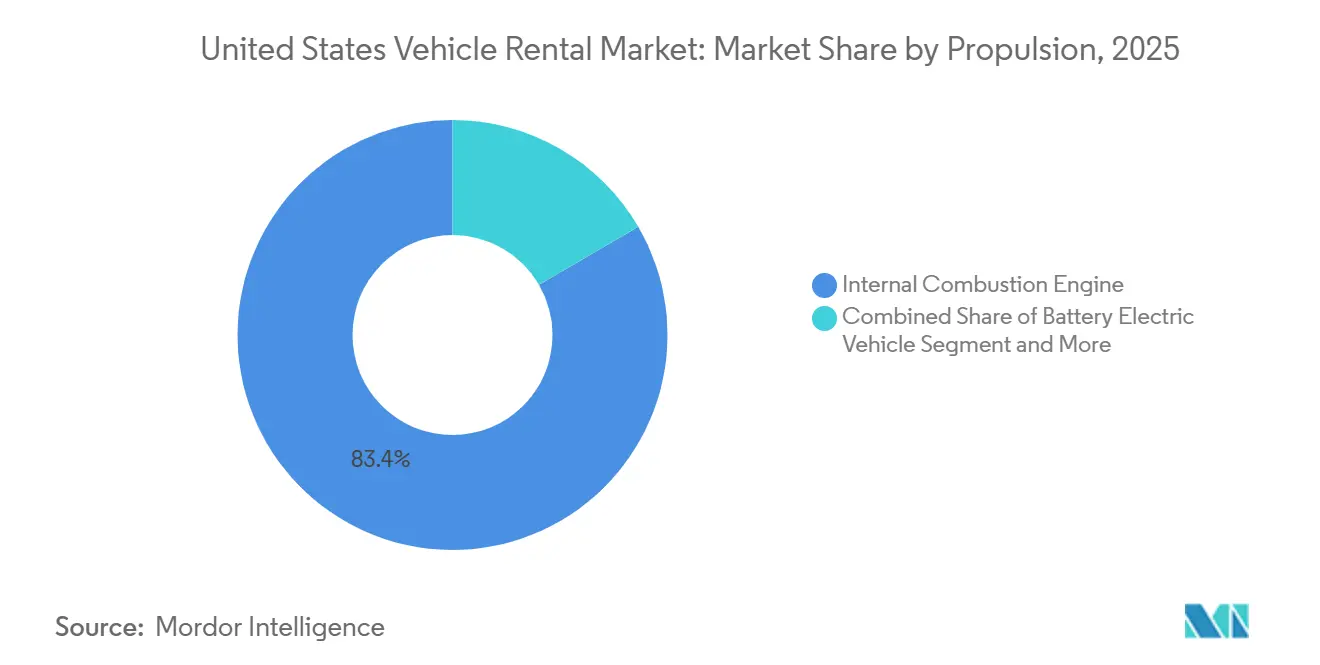

- By propulsion, internal-combustion vehicles retained 83.35% share in 2025, yet battery-electric vehicles are growing at the highest 5.62% CAGR.

- By service model, traditional corporate fleets controlled 89.91% share in 2025, while peer-to-peer platforms record a 5.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Vehicle Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Domestic Road-Trip/Leisure Demand | +1.2% | National, with peaks in Florida, California, Texas | Short term (≤ 2 years) |

| Rapid Growth of Online & Mobile Booking Channels | +0.9% | National, concentrated in urban metros | Medium term (2-4 years) |

| Flexible Fleet-Leasing Demand | +0.8% | National, strongest in tech hubs (San Francisco, Austin) | Medium term (2-4 years) |

| OEM-Backed Electrification of Rental Fleets | +0.7% | California, Northeast states with ZEV mandates | Long term (≥ 4 years) |

| Peer-to-Peer Supply Expansion | +0.6% | Urban metros (NYC, LA, Chicago, Seattle) | Medium term (2-4 years) |

| Telematics-Driven OPEX Optimisation | +0.5% | National, early adopters in large fleet operators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Domestic Road-Trip/Leisure Demand

In 2025, U.S. travelers, opting for national parks and coastal drives over international vacations, drove a notable increase in domestic person-trips compared to pre-pandemic levels [1]“Domestic Travel Volume Report 2025,” U.S. Travel Association, ustravel.org . While daily rental rates remained steady, a longer average rental duration significantly boosted revenue per transaction. With a substantial share of leisure rentals concentrated in key states like Florida, California, and Texas, operators strategically shifted their inventory towards sunbelt airports during peak quarters. The growing preference for SUVs and minivans, which typically generate higher revenue, enhanced fleet mix economics. However, this shift introduced seasonal volatility, particularly during the less busy quarters when utilization rates dropped. To navigate these challenges, companies have turned to dynamic pricing algorithms and real-time telematics for cross-regional transfers.

Rapid Growth of Online & Mobile Booking Channels

In 2025, digital bookings constituted a significant majority of transactions in the U.S. car rental market, showing a notable increase from the previous year. This growth can be attributed to mobile apps, like those of Enterprise Holdings, which have significantly reduced booking times and driven a considerable rise in ancillary revenue [2]“Fiscal 2024 Annual Review,” Enterprise Holdings, enterpriseholdings.com . Meanwhile, Hertz's strategic move to integrate rental options within the Uber app has successfully converted a notable portion of Uber's users for multi-day rentals, highlighting the increasingly blurred lines between ride-hailing and car rentals due to platform convergence. While digital channels have substantially lowered customer acquisition costs, incidents such as a ransomware attack that temporarily disrupted operations for a mid-tier operator in 2024 emphasize the critical need for robust ISO 27001-grade cybersecurity defenses.

OEM-Backed Electrification of Rental Fleets

In 2024, General Motors significantly reduced prices on Chevrolet Equinox EV and Blazer EV units for fleet buyers, aiming to encourage consumer trials. This move comes on the heels of Hertz's substantial impairment on EVs, attributed to swift depreciation [3]“EV Life-Cycle Cost Study 2025,” U.S. Department of Energy, energy.gov . Despite challenges, battery-electric vehicles are set to lead the market with strong growth. This growth is fueled by the total cost of ownership becoming advantageous once vehicles reach a high annual mileage. With California enforcing a rule for a significant percentage of zero-emission sales by 2026, national brands with a presence on the West Coast find electrification imperative. However, a significant hurdle remains: by the end of 2024, only a small portion of rental sites had the necessary high-capacity charging capability.

Peer-to-Peer Supply Expansion & Price Discovery

In recent times, Turo has demonstrated how asset-light platforms can scale effectively by offering prices significantly lower than airport counters. Meanwhile, Getaround's keyless entry feature is enabling supply to expand into residential areas, meeting the needs of Airbnb patrons. However, proposed legislation in several states aiming to impose airport facility charges and sales taxes could significantly reduce P2P's pricing advantage. Additionally, increasing commercial insurance premiums are creating challenges for host economics.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent New-Vehicle Supply Constraints | -0.8% | National, acute in EV-heavy California fleets | Medium term (2-4 years) |

| Modal Substitution by Ride-Hailing | -0.7% | Urban metros with dense transit (NYC, SF, Boston, DC) | Medium term (2-4 years) |

| Residual-Value Risk from Low-Priced Chinese EV Imports | -0.6% | National, concentrated in West Coast ports | Long term (≥ 4 years) |

| Escalating Airport Concession & Local Taxation Costs | -0.5% | Major hubs (LAX, JFK, ORD, ATL, DFW) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent New-Vehicle Supply Constraints & High CAPEX

In 2025, U.S. light-vehicle production experienced a notable decline compared to pre-pandemic levels. As a result, OEMs prioritized retail channels, achieving significantly higher transaction prices compared to the discounts offered in fleet sales. Hertz reported a considerable increase in average acquisition costs, with the fleet's average age extending, leading to a noticeable rise in monthly maintenance expenses per vehicle. Meanwhile, Avis Budget's bond issuance in May 2025, set at a high-interest rate, highlights the intensified capital demands for fleet renewals amid rising interest rates.

Modal Substitution by Ride-Hailing & Subscription MaaS

In 2024, Uber and Lyft collectively facilitated billions of trips across the U.S. As bundled mobility subscriptions gained traction, they began siphoning demand away from short-term urban rentals. With ride-hailing services frequently offering a more economical option than the combined cost of a short car rental and parking, their popularity continues to grow. A significant portion of U.S. business travelers now rely on corporate travel platforms that seamlessly integrate trains, rideshares, and rentals. This shift pressures rental companies to either navigate the lower-margin aggregator landscape or face the threat of disintermediation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Dual-Track Growth Across Leisure and Corporate Needs

Leisure and tourism captured 56.71% of the United States car rental market in 2025 as remote work let families extend vacations, pushing summer utilization above four-fifths in Florida and California. Business and corporate clients, though smaller, will outpace leisure at a 5.49% CAGR because firms are substituting ownership with flexible rentals that trim fixed fleet costs by one-fourth. Such a strategy not only streamlines expenses but also smooths out seasonal fluctuations: leisure rentals peak during the summer months, while corporate demand bolsters occupancy during the beginning and end of the year. Premium SUVs and convertibles command higher rental rates, pushing the average daily revenue upward compared to the previous year.

Avis Budget witnessed a significant surge in corporate subscriptions, especially from tech giants in Austin and San Francisco. These firms are consolidating their hybrid workforce, leading to fewer but extended client engagements. Another resilient segment, insurance replacements, saw steady growth. This growth comes as vehicle repair timelines are extended, prompting operators to allocate lower-cost fleets, ensuring margins on fixed-rate contracts. The landscape of EV adoption reveals a stark divide: leisure renters exhibit a much greater inclination to trial EVs for shorter trips. In contrast, corporate clients prefer traditional ICE vehicles, prioritizing the need for swift refueling.

By Vehicle Type: Passenger Cars Anchor Revenue, Commercial Units Diversify

Passenger cars held 63.37% of the United States car rental market size in 2025 and will expand at the leading 5.57% CAGR because sedans and compact SUVs balance fuel economy, acquisition cost, and airport space fees. Light commercial vehicles are growing at a minimal rate annually as e-commerce firms rent vans and pickups for flexible last-mile capacity without large capital outlays. Enterprise added 18,000 Ford F-150s in 2024 to meet contractor demand, realizing slightly higher revenue per vehicle but accepting faster depreciation.

Regional preferences diverge: compact sedans dominate in California and the Northeast, where fuel costs and parking constraints are acute, while pickups and full-size SUVs lead in Texas and Florida, where trip distances and family travel justify size premiums. Commercial electrification lags; only 3% of rented vans were EVs in 2024, but Ford E-Transit pilots in dense urban routes signal incremental change.

By Booking Channel: Digital Platforms Set the Pace

Online channels controlled 71.35% of bookings in 2025 and will rise at a 5.59% CAGR, propelled by AI-driven dynamic pricing and sub-90-second mobile workflows. Hertz’s Uber integration turned ride-hail users into multi-day rental clients and showcases cross-platform convergence that future-proofs distribution. Offline booking remains essential for negotiated corporate rates and insurance replacement, but is losing three to four share points per year.

AI-driven prompts have significantly boosted ancillary revenue per rental compared to the previous year. However, ransomware-induced outages highlight substantial operational risks, with downtime causing severe financial losses for operators. In response, companies are increasingly adopting multi-cloud architectures and ISO 27001 standards to ensure uptime and mitigate risks.

By Rental Duration: Balancing Volume and Margin

Short-term rentals generated 67.73% of 2025 revenue due to leisure trips averaging four days, yet long-term rentals will climb at the fastest 5.51% CAGR as corporates embrace month-plus leases that sidestep residual-value risk. Long-term contracts deliver a little higher margins because turnover costs drop to USD 18 per vehicle, but they tie up inventory during peak leisure months, forcing careful fleet segmentation.

In high-demand windows, dynamic pricing can significantly boost short-term yields. Meanwhile, peer-to-peer platforms are sidestepping airport fees, allowing them to capture a larger share of the urban short-stay market. Adding to the complexity, rideshare drivers are renting vehicles for extended periods, which helps increase long-term volumes. However, the segment's volatility is evident from the recent revenue decline reported by HyreCar.

By Propulsion: ICE Prevalence with EV Acceleration

Internal combustion engines held 83.35% share in 2025, reflecting refueling convenience on long trips, yet battery-electric vehicles will post a 5.62% CAGR through 2031 as total cost of ownership tips in their favor over 30,000 annual miles. Hertz’s impairment demonstrates residual-value risk, prompting shorter EV hold periods and manufacturer buyback clauses. Hybrid-electric vehicles appeal to corporate fleets seeking lower fuel burn without charging needs.

Infrastructure gaps persist: only a minimal number of rental sites boast 150 kW DC chargers, so EV deployment clusters in California, Washington, and New York, where public charging density is higher. Federal tax credits flow to retail buyers, not fleets, creating a cost gap partly offset by certain state incentives for commercial users.

By Service Model: Incumbents Defend While P2P Scales

Traditional corporate fleets controlled 89.91% of the United States car rental market in 2025, leveraging established airport footprints and brand loyalty. Peer-to-peer platforms are expanding at a 5.54% CAGR by mobilizing private vehicles that avoid the USD 25,000-35,000 capital hit. Turo, boasting significant revenue, showcases its scale, yet the proposed tax parity threatens to diminish its cost edge.

In response, traditional firms are broadening their horizons: Enterprise recently expanded its neighborhood locations and is now offering P2P-style keyless delivery services. However, hosts grapple with soaring insurance costs, as commercial premiums are substantially higher compared to personal rates. The landscape shifted recently when multiple carriers exited the segment, compelling platforms to turn to self-insurance.

Geography Analysis

In 2025, California, Florida, and Texas generated a significant portion of total revenue, driven by robust tourism, a sizable population, and a high density of airports. California is at the forefront of electrification, with electric vehicles (EVs) making up a notable share of its rental fleets, surpassing the national average. This surge is largely attributed to stringent Zero Emission Vehicle (ZEV) mandates and the public's growing affinity for brands like Tesla. Florida stands as the leader in leisure demand; Orlando and Miami together account for a substantial number of rental transactions. Meanwhile, Texas, bolstered by corporate travel in the energy and tech sectors, has seen a notable increase in long-term rentals at both Houston and Dallas airports.

The Northeast grapples with modal substitution challenges, due to its dense transit networks. For instance, even as tourism rebounded, New York City witnessed a decline in rental volume, as many travelers opted for ride-hailing services for shorter trips. In the Midwest, states like Illinois and Ohio demonstrate resilience, particularly through insurance replacements. Notably, a significant portion of Enterprise’s fleet in the Midwest is allocated for claims, with an average rental duration of over two weeks. Meanwhile, Mountain West states—namely Colorado, Utah, and Arizona—experienced a notable surge in demand, driven by outdoor recreation and a tech migration to Phoenix.

Peer-to-peer rental platforms have found a stronghold in major metropolitan areas like New York City, Los Angeles, Chicago, and Seattle, collectively securing a notable market share by sidestepping airport surcharges. However, a significant portion of rural counties remain underserved, lacking a rental outlet within a reasonable distance. This gap presents a lucrative opportunity for delivery-first models, such as Kyte. Climate events are also influencing rental demand: while hurricanes in Florida and Texas led to a noticeable spike in insurance rentals in the latter half of 2024, wildfires in California dampened tourism but saw a rise in rentals for long-term evacuees. Furthermore, state mandates in California, New York, and Massachusetts are set to elevate regional fleet electrification to a significantly higher level by 2027, a notable jump from the current national average.

Regulatory Landscape

In the United States, vehicle rental operators operate under a combination of federal motor-vehicle safety rules and consumer-protection oversight. Under the National Traffic and Motor Vehicle Safety Act framework administered by NHTSA (FMVSS), rental firms must not make inoperative any safety device or element of design installed to comply with FMVSS, with limited allowances for temporary modifications to accommodate passengers with disabilities (49 CFR 595.8). Separately, 49 USC 30106 provides federal protection against state vicarious-liability claims for rental and leasing companies, provided there is no negligence or criminal wrongdoing by the owner, helping standardize risk exposure across states.

Commercial practices are also examined through Federal Trade Commission enforcement tools that address deceptive or unfair acts in the car rental industry, including fee and add-on disclosures (for example, fuel options and damage waivers). Accessibility obligations are governed by the ADA, including DOT 49 CFR Part 37 requirements for transportation services for individuals with disabilities and related accessibility standards, which can influence fleet-equipment choices and airport and neighborhood counter processes. At airport locations, DOT guidance on ACDBE participation for car-rental concessions shapes concession and procurement compliance for operators serving covered airports.

Value Chain Analysis

The value chain starts with vehicle sourcing and financing (OEM fleet programs, captives, banks, and ABS facilities). It then moves through upfitting and telematics enablement, branch and airport operations, and downstream remarketing via wholesale and direct-to-consumer channels. With supply constraints and high capital intensity, procurement and fleet-funding terms remain central to operator economics, while remarketing execution is increasingly used to manage residual-value risk and cycle-time. Distribution covers direct channels (operator apps and websites), corporate travel and insurance replacement intermediaries, and mobility platforms that embed rentals within broader travel and rideshare journeys.

Operational-layer partners are taking on more visibility as operators use technology to protect utilization and cut turnaround time. For example, Hertz partnered with UVeye (April 2025) to deploy AI-driven vehicle inspection systems across major US airports, and Stellantis partnered with Zubie through Mobilisights (April 2025) to provide embedded telematics data for fleet operations. The chain is also expanding toward autonomous and advanced mobility operations, supported by Avis Budget Group's multi-year partnership with Waymo (July 2025) to provide fleet operations, maintenance, and depot services for Waymos autonomous ride-hailing service in Dallas, effectively extending robotaxi fleet services as an adjacent downstream customer for rental operators.

Competitive Landscape

Enterprise Holdings, Hertz Global Holdings, and Avis Budget Group dominate airport transactions, controlling a significant portion of the market. In contrast, the off-airport and peer-to-peer segments are scattered among numerous operators. Leading the pack, Enterprise generates substantial revenue and operates an extensive network of locations under its National and Alamo brands. Both Hertz and Avis grapple with elevated borrowing costs—evident from Avis’ high-interest notes—and fluctuations in residual values linked to electric vehicles (EVs). Meanwhile, Sixt SE has expanded its presence across the U.S., featuring a premium European fleet, and holds a notable market share in major gateway cities.

Investments in technology are carving out competitive advantages. For instance, Enterprise's implementation of Geotab technology significantly boosted vehicle utilization and reduced downtime. On another front, Hertz's collaboration with Carvana allows for direct-to-consumer de-fleeting, enabling Hertz to capture retail margins and lessen dependence on auctions. Turo and Getaround, operating without physical inventory, are scaling up but are contending with regulatory efforts to standardize taxes. Their future hinges on how adeptly they manage rising insurance costs.

Brands like Fox and Advantage are strategically targeting secondary airports, opting for lower fees in exchange for diminished occupancy rates. In a nod to the industry's future, Hertz's provision of a large fleet of Teslas for Uber's autonomous trial underscores a significant bet on the robotaxi evolution.

United States Vehicle Rental Industry Leaders

Enterprise Holdings Inc.

Hertz Global Holdings Inc.

Avis Budget Group Inc.

Sixt SE

Fox Rent A Car

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity centers on disciplined fleet optimization and service-led differentiation as operators manage acquisition costs, depreciation, and utilization rather than focusing on pure fleet growth. Hertz's February 2026 update is one indicator, stating that it completed fleet rotation and secured model year 2026 vehicle buys at target prices and volumes, reaching its lowest average fleet age in nearly a decade. The market is also working through EV residual-value volatility, illustrated by Avis Budget Group recording USD 518 million in long-lived asset impairment and related charges in Q4 2025 to reduce the carrying value of certain US electric-vehicle rental fleets. This creates room for improved EV remarketing playbooks, tighter trim and model selection, and charger-ready depot networks when utilization supports total-cost outcomes.

Another opportunity involves extending rental operators into broader mobility and fleet-services roles, leveraging branch networks, maintenance know-how, and telematics to serve third parties. Avis Budget Group's Waymo partnership for Dallas robotaxi fleet operations (announced July 2025) shows how depot operations, maintenance, and fleet orchestration can be monetized beyond conventional daily rentals. Technology-enabled inspection, predictive maintenance, and remote vehicle logistics also create pathways to reduce cycle time and raise asset availability, supported by initiatives such as Hertz's UVeye airport inspection deployment (April 2025) and OEM embedded-telematics integrations like Mobilisights with Zubie (April 2025).

Recent Industry Developments

- May 2026: Hertz reported Q1 2026 results and highlighted the launch of its affiliated operating company, Oro Mobility. The move expands Hertzs operating footprint beyond traditional daily rentals and reinforces its push into mobility and fleet-related services under its transformation program.

- April 2026: Avis Budget Group reported first quarter 2026 results, including USD 2.5 billion in revenue and 70% vehicle utilization across its Americas and International segments, alongside stated fleet funding capacity. The update indicates tighter fleet discipline and capital flexibility, supporting utilization-focused operations amid procurement and residual-value pressures.

- October 2024: Aero Corporation partnered with Mapless AI to pilot remote tele-operations on its Avis and Budget franchise rental fleet in the United States, focusing on vehicle shuttling and EV charging. Remote operations aim to support faster vehicle repositioning and improved charging logistics, with potential to increase asset availability at constrained airports and dense urban markets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the United States vehicle rental market covers paid rental revenue generated from passenger-vehicle hire where the vehicle is returned to the owner at the end of the contract, across both short-term and long-term rentals in the United States.

Scope exclusions: Recreational vehicles, heavy trucks, chauffeur-driven limousine services, and pure operating-lease contracts are excluded.

Segmentation Overview

- By Application

- Leisure and Tourism

- Business and Corporate

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Medium and Heavy-duty Commercial Vehicles

- By Booking Channel

- Online

- Offline

- By Rental Duration

- Short-Term

- Long-Term

- By Propulsion

- ICE Vehicles

- Battery-Electric Vehicles

- Hybrid-Electric Vehicles

- By Service Model

- Traditional Corporate Fleets

- Peer-to-Peer Platforms

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries and build a demand story before the model was finalized. We focused on public travel and mobility signals, including U.S. Bureau of Transportation Statistics (BTS) series on air travel activity, U.S. Energy Information Administration (EIA) fuel price trends, and U.S. Census Bureau population and income indicators that influence trip frequency and rental behavior.

To sharpen assumptions around airport exposure, seasonality, and replacement cycles, we also reviewed sources such as Federal Aviation Administration (FAA) passenger traffic publications, U.S. DOT updates on travel conditions, and relevant trade association releases and press coverage. Company filings, investor presentations, and earnings call commentary were used to cross-check pricing, utilization, and fleet actions, then a paid subscription database for company financials and a vehicle park and sales database were referenced to sanity-check fleet growth and used-vehicle disposal timing. The sources listed here are illustrative only, and additional public references were consulted to collect, validate, and clarify data points during the work.

Primary Interviews and Surveys

Primary work was completed through expert interviews and structured questionnaires with rental operators, fleet and pricing leaders, channel partners, and travel ecosystem participants. These interviews were used to confirm how airport versus off-airport demand behaves, how daily rates are set across channels, and what fleet availability looks like under different travel scenarios, then we rechecked any weak assumptions before locking the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 16% | |

| Mid tier: 56% | Functional/Unit leaders: 30% | |

| Smaller Players: 16% | Managers: 54% |

Market-Sizing & Forecasting

The core sizing approach starts with a top-down reconstruction of the rental revenue pool, where travel activity and fleet supply signals are translated into expected rental days and revenue, and the total is then reconciled to what operators can realistically deliver. In practice, this means airport passenger volumes, broader trip demand, and fleet availability are tied together using utilization and pricing logic to arrive at an annual market value.

Once the top-line is shaped, we run selective bottom-up checks to validate it, including sampled operator revenue trajectories, typical daily rate ranges by channel, and volume proxies such as fleet counts multiplied by utilization days. Inputs that mattered most for this market included the airport versus neighborhood location mix, average daily rate progression, fleet size and age mix, utilization rate bands during peak and shoulder periods, and the split between leisure and corporate rental days. Where data gaps existed, we filled them with bounded ranges gathered from interviews, then tested sensitivity so no single assumption could shift the outcome without being noticed.

For forecasting, scenario analysis was used so the forward view stays practical when travel demand or fleet supply shifts quickly. Growth drivers and constraints were translated into a small set of forecast variables, including domestic travel intensity, airfare and fuel price influence on trip patterns, fleet replacement pace, and expected normalization in utilization and pricing. Those scenarios were then aligned to what primary respondents described as realistic planning cases.

Data Validation & Update Cycle

Validation was done through multiple passes, starting with basic consistency checks and moving into variance reviews against independent signals such as passenger travel trends, fleet movement, and pricing direction discussed by market participants. When a modeled shift looked too sharp for a given year, we revisited the underlying driver, and respondents were re-contacted when clarification was needed on items like rate resets, fleet cuts, or channel mix changes.

Before sign-off, an analyst review confirms assumptions are stated clearly, the math ties out across steps, and the result aligns with what is feasible on both supply and demand. Reports are refreshed annually, and interim updates are made when material events change travel patterns, fleet supply, or pricing, followed by a final pre-delivery check so clients receive the latest updated view.

Mordor Intelligence's United States Vehicle Rental Market Sizing Compared With Other Published Estimates

Published market sizes for United States vehicle rental do not always match, even when the topic name looks the same. The differences usually come from what is counted as rental revenue, what vehicle types are included, and how pricing and utilization are carried forward into the forecast.

The table shows a spread that is mainly explained by scope and counting rules, where some estimates narrow the market to short-term, self-drive car rental only, and others blend in adjacent mobility services or leasing-like contracts. It also reflects timing differences, since daily-rate normalization assumptions and used-vehicle resale cycles can shift annual value if the refresh cadence is not aligned to recent travel and fleet signals. Even within USD reporting, currency timing can add noise when calendar cutoffs differ.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 51.13 B (2026) | |

| Industry Publisher A | USD 38.50 B (2025) | This figure appears anchored to a narrower car-rental framing and an earlier base year, which can understate the market if longer-term rentals and peer-to-peer host activity are treated lightly or not counted in operator revenue. |

| Industry Publisher B | USD 41.94 B (2024) | This estimate is based on short-term, self-driven car rentals and uses a different year, which can create a lower value by excluding long-term rental demand and by not fully reflecting later pricing and utilization shifts. |

The table shows that year selection and what gets counted as rental revenue are the biggest practical drivers of the gap. In Mordor Intelligence's model, the market includes paid short-term and long-term passenger-vehicle rental revenue (including peer-to-peer hosts) while excluding RVs, heavy trucks, chauffeur-driven services, and pure operating-lease contracts. With that scope locked first and then checked against travel, fleet, utilization, and rate signals, the final number stays traceable to clear inputs that can be re-tested as conditions change.

Key Questions Answered in the Report

How large is the United States car rental market in 2026?

The United States car rental market size is estimated at USD 51.13 billion in 2026 and is expected to reach USD 66.72 billion by 2031.

Which vehicle category holds the biggest share of rented fleets?

Passenger cars account for 63.37% of fleet mix and lead forecast growth with a 5.57% CAGR to 2031.

What drives the shift toward long-term car rentals?

Hybrid-work schedules and subscription-style corporate contracts are raising demand for 30-plus-day rentals, which show a 5.51% CAGR.

How fast are electric vehicles expected to grow in rental fleets?

Battery-electric vehicles represent the fastest propulsion segment, expanding at a 5.62% CAGR through 2031 despite infrastructure gaps.

Which booking channel is expanding the quickest?

Online and mobile reservations dominate with 71.35% share and are forecast to grow at 5.59% CAGR as digital interfaces reduce friction.

What competitive risks do peer-to-peer platforms face?

Proposed state legislation to impose airport fees and rising insurance premiums could erode up to 40% of P2P platforms’ price advantage.

Page last updated on: