Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

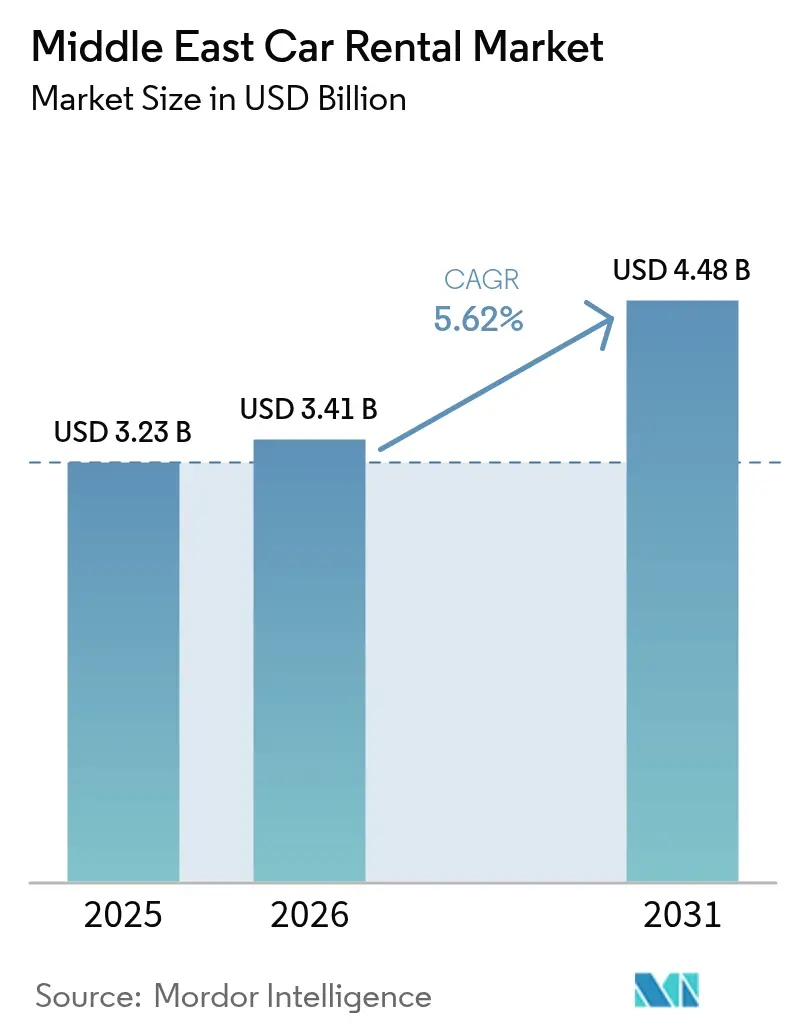

| Base Year Market Size (2025) | USD 3.23 Billion |

| Market Size (2026) | USD 3.41 Billion |

| Market Size (2031) | USD 4.48 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East Car Rental Market Analysis by Mordor Intelligence

The Middle East Car Rental Market size was valued at USD 3.23 billion in 2025 and is estimated to grow from USD 3.41 billion in 2026 to reach USD 4.48 billion by 2031, at a CAGR of 5.62% during the forecast period (2026-2031). Customer demand is reorganizing around leisure tourism, digital booking, and experiential vehicle classes, while labor-nationalization rules and ride-hailing substitution pressure temper near-term margins. Operators that automate counter processes, embrace electric fleets, and unlock off-airport delivery efficiency are capturing share as mega-projects in Saudi Arabia and the UAE redraw mobility corridors. Supply-chain delays, limited EV insurance capacity, and fragmented regulatory regimes widen the performance gap between well-capitalized multinationals and smaller local fleets.

Key Report Takeaways

- By application, leisure tourism led with 92.45% revenue share in 2025; daily utility and business rentals are forecast to expand at a 7.33% CAGR through 2031.

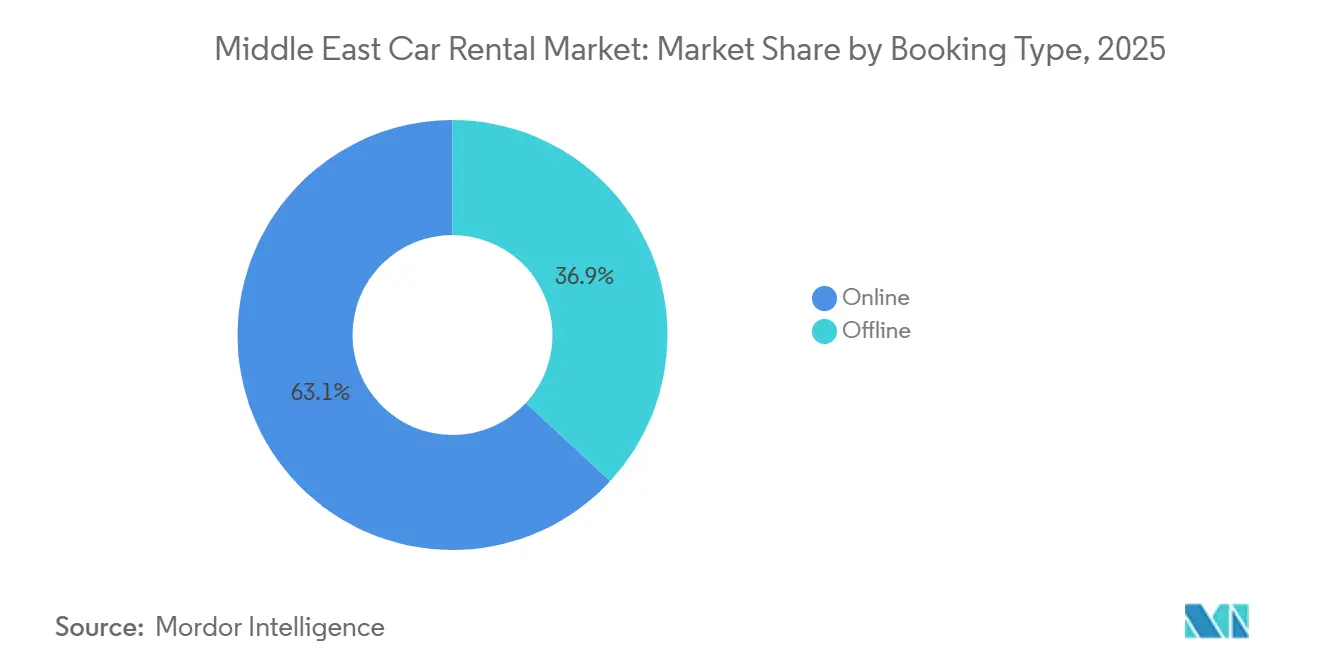

- By booking type, online channels captured 63.12% of transactions in 2025, while offline contracts are projected to grow more slowly at a 2.1% CAGR to 2031.

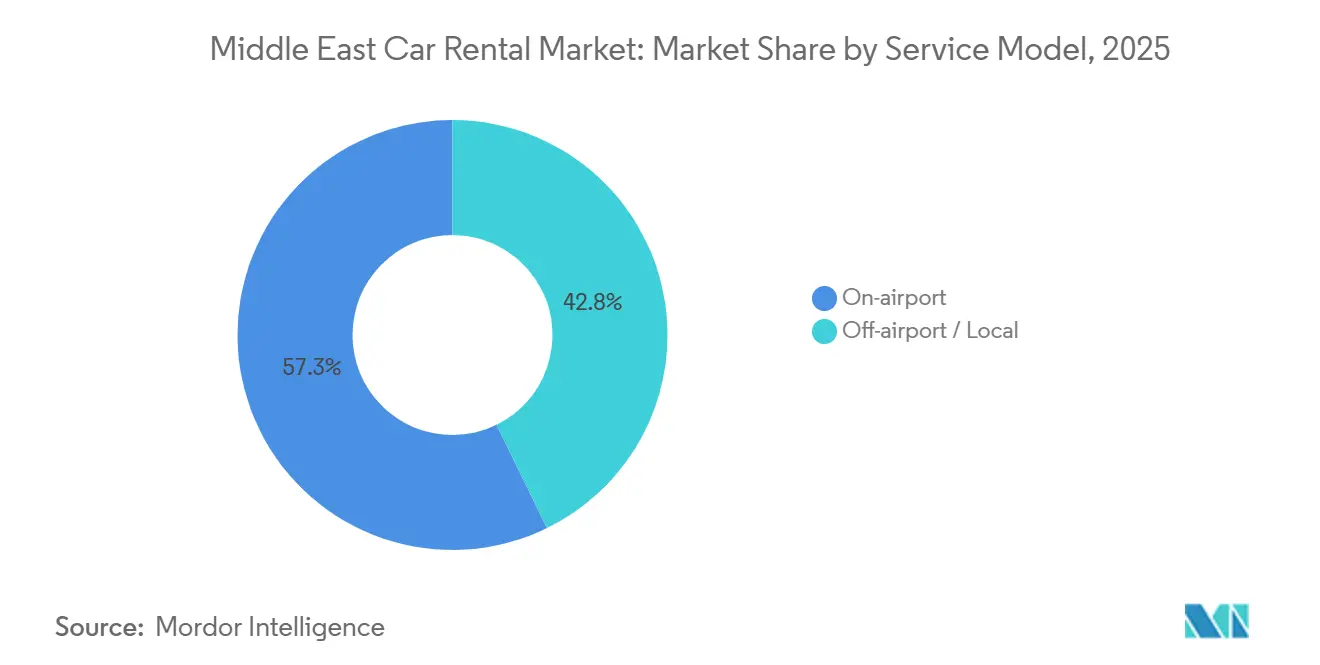

- By service model, on-airport locations held a 57.25% share in 2025; off-airport delivery is the fastest-growing format at a 7.84% CAGR to 2031.

- By vehicle class, economy cars commanded 77.45% share in 2025, whereas luxury and premium rentals are advancing at a 76.13% CAGR through 2031.

- By propulsion, internal-combustion engines retained 92.61% share in 2025; electric and hybrid vehicles are expected to rise at a 12.45% CAGR over 2026-2031, supported by Saudi and UAE incentives.

- By geography, the Rest of Middle East cluster accounted for 40.75% market share in 2025, while the UAE is set to register the highest CAGR of 8.32% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Car Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tourism Rebound in GCC | +1.5% | GCC-wide; strongest in United Arab Emirates and Saudi Arabia | Medium term (2-4 years) |

| Shift to App-based Bookings | +1.2% | UAE and Saudi Arabia | Short term (≤ 2 years) |

| Mega-Events and Infrastructure | +0.8% | Primarily Saudi Arabia; spillover across GCC | Long term (≥ 4 years) |

| Corporate Mobility Subscriptions | +0.6% | UAE and Saudi Arabia | Medium term (2-4 years) |

| Government EV Rental Incentives | +0.4% | UAE leading, expansion across Saudi Arabia | Long term (≥ 4 years) |

| Integrated Mobility Super-Apps | +0.3% | Early adoption in UAE and Saudi Arabia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tourism Rebound Across GCC Corridors

The GCC experienced a significant increase in international arrivals, surpassing pre-pandemic levels, with an extended average rental duration as visitors opted for multi-city road trips [1]“International Tourism Highlights 2025,”, World Tourism Organization, unwto.org. Saudi Arabia emerged as a key destination, while the UAE also attracted a substantial number of visitors, driving demand for both economy sedans and premium SUVs. Additionally, Kuwait's liberalization of visa-on-arrival and Qatar's enhanced infrastructure boosted regional weekend travel, reinforcing leisure's dominance in the Middle East car rental market.

Rapid Shift to App-Based Bookings

Mobile-first platforms have captured a significant share of bookings and are experiencing steady growth. This expansion is driven by innovations like keyless access and self-service kiosks, which have notably reduced labor costs per transaction. The confidence in peer-to-peer models is evident through venture capital inflows, such as WheelsOn’s recent funding round, suggesting these models can undercut legacy rates by a substantial margin. While digital adoption is strongest in the UAE, Kuwait, and Qatar still rely heavily on traditional contracting methods, highlighting a digital divide that benefits tech-savvy operators.

Mega-Events and Infrastructure Projects (Vision 2030, Expo 2030)

Saudi Arabia's Public Investment Fund allocated a significant amount to develop roads and airports connecting NEOM, the Red Sea Project, and Qiddiya [2]“PIF Funds New Transport Links to NEOM,”, Bloomberg News, bloomberg.com. This move is set to generate new demand corridors for rental fleets. With Expo Riyadh projected to attract a substantial number of visitors and contribute significantly to economic output, operators are strategically positioning their inventory close to construction sites. Meanwhile, Dubai's ambitious Universal Blueprint aims to welcome a large number of tourists annually. However, rezoning efforts near Al Maktoum International Airport are driving up land prices.

Corporate Mobility-Subscription Adoption

Udrive's B2B subscriptions experienced significant growth as CFOs increasingly treated fleet ownership as an operating expense, a trend mirrored by Sixt's revenue growth from flexible packages in GCC hubs. The highest uptake is observed in Dubai, Abu Dhabi, and Riyadh, where telematics and real-time invoicing align with hybrid work mobility. Meanwhile, Kuwait and Qatar lag behind, grappling with traditional fleet-ownership practices and ambiguities in commercial registration rules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ride-hailing Substitution Pressure | –0.7% | UAE and Saudi Arabia | Short term (≤ 2 years) |

| Labor-nationalization Compliance Costs | –0.5% | GCC-wide; strongest in Saudi Arabia | Medium term (2-4 years) |

| Thin EV Rental Insurance | –0.4% | Initially UAE; expanding regionwide | Medium term (2-4 years) |

| Import Driven Supply Bottlenecks | –0.3% | Regionwide; most acute in smaller markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ride-Hailing Substitution Pressure

Careem and Uber recorded significant growth in trips in Saudi Arabia, marking a notable surge from prior levels. This growth has diminished demand for one-day rentals, especially for short-distance urban journeys[3]"Saudi ride-hailing trips surge", Arab News, arabnews.com. Ride-hailing services in the UAE captured a substantial share of the urban mobility market, encroaching on the rental market traditionally dominated by airport-to-hotel services. In response, operators are pivoting towards longer-duration leisure rentals and corporate packages to safeguard their profit margins.

Labor-Nationalization Compliance Costs

Saudi Arabia’s Saudization policy requires rental firms to employ local nationals, significantly increasing payroll costs and prompting temporary shutdowns as enforcement takes effect in early 2024. In the medium term, companies that adapt to these regulations stand to gain preferential licensing opportunities and streamlined access to government contracts. In response to these challenges, operators are investing in robust training academies and cutting-edge digital workflow tools to enhance employee productivity. This proactive approach not only helps them manage higher wage structures but also ensures that profit margins remain intact despite rising expenses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Booking Type: Digital Channels Redefine Experience

Online channels’ 63.12% share in 2025 signals a structural change in the Middle East car rental market. Automating check-in trimmed labor costs and cut average transaction time to below 4 minutes, yet heightened price transparency narrowed walk-in premiums. In Kuwait and Qatar, government tenders and corporate annual agreements continue to rely on offline contracts. Those adept at omnichannel fulfillment can leverage location economics and gather detailed data to enhance their dynamic pricing strategies.

As a result, app-native fleets, which benefit from significantly lower customer-acquisition costs than their kiosk-dependent counterparts, are seeing a decrease in marketing expenditures. While peer-to-peer startups grapple with unresolved insurance liabilities, strong investor interest suggests a belief in forthcoming regulatory solutions, potentially enriching platform diversity.

By Application: Leisure Dominance Masks Corporate Opportunity

Leisure rentals accounted for 92.45% of 2025 revenue, yet corporate mobility subscriptions reveal a faster-growing 7.33% CAGR sub-segment that offers predictable margins through bundled maintenance and insurance.

While cross-border weekend tourism and visits to mega-project sites bolster the leisure sector, consulting and technology firms are increasingly adopting CFO-driven, asset-light models. These models enable firms to optimize operational efficiency by reducing fixed costs and focusing on scalable solutions. As a result, project teams are being deployed across various cities in the GCC, ensuring flexibility and adaptability in meeting client demands.

By Vehicle Type: Economy Volume, Luxury Margin

Economy cars still own 77.45% of fleet volume. Still, luxury and premium categories are compounding at 76.13% CAGR as Dubai’s social-media culture fuels exotic-car rentals and Riyadh’s expatriate executives demand high-status transport.

Operators of supercars often face insurance premiums that can reach a significant percentage of their vehicle's annual value. This hefty expense frequently drives them to consider self-insurance or to accept substantial deductibles. These premiums are influenced by factors such as the high value of the vehicles, their susceptibility to damage, and the elevated repair costs associated with luxury components. Yet, bolstered by consistently high daily rental rates, these operators successfully uphold robust profit margins, adeptly offsetting their risk exposure.

By End-User Type: Self-Drive Dominance

Self-drive accounted for 88.23% of demand in 2025, underpinned by regional preference for personal control, but its 5.98% CAGR lags the overall Middle East car rental market. Chauffeur-driven services are expanding more quickly as multilingual drivers and premium vehicles appeal to affluent tourists and executives navigating unfamiliar road rules.

Fleet owners are increasingly embracing self-service technology, integrating smart lockers, in-app vehicle unlocking, and AI-driven damage inspections to efficiently manage their labor costs. This innovative approach not only streamlines operations but also enhances customer convenience. However, maintaining a chauffeur service enables them to cater to high-value clients, offering luxurious experiences and specialized services such as airport meet-and-greet and multilingual driver assistance. This dual strategy broadens their revenue opportunities, creating a richer, more diverse offering that appeals to a broader range of customers.

By Service Model: Off-Airport Ascendance

On-airport outlets held a 57.25% share in 2025, yet off-airport delivery grew at a 7.84% CAGR as mobile apps eroded the convenience premium. Operators are renegotiating real-estate footprints, trading high-fee terminals for suburban lots linked to 60-minute hotel deliveries that improve fleet rotation efficiency.

The model mandates sophisticated logistics, including digital booking, on-demand delivery, and flexible return points. Operators leverage telematics to stage vehicles near high-demand clusters and deploy mobile service vans for quick turnarounds. Airport counters, meanwhile, evolve into branding and customer-acquisition nodes, funneling repeat users to less costly downtown outlets on subsequent trips.

By Propulsion: Early-Stage Electrification Momentum

ICE vehicles retained 92.61% share in 2025, but government incentives reduced EV operating costs, enabling a 12.45% CAGR for electrified fleets. Charging coverage remains uneven outside Dubai and Abu Dhabi, and high insurance premiums deter widespread adoption, but policy momentum suggests a tipping point post-2028.

Battery models are revolutionizing the transport landscape by significantly reducing fuel and maintenance costs. However, they face challenges such as limited insurance options and sparse charging infrastructure, particularly in areas beyond major metropolitan centers. To navigate these hurdles, operators are actively forming strategic partnerships with charging network providers and insurers willing to address the unique risks associated with electric vehicles. These collaborations are setting the stage for a broader, more ambitious rollout of zero-emission technologies, paving the way for a cleaner, more sustainable future.

Geography Analysis

The rest of the Middle East's economies together generated 40.75% of 2025 revenue, lifted by Kuwait’s tourist growth after visa reforms and Qatar’s highway expansion, which sustains weekend leisure travel. Regulatory fragmentation across import tariffs and licensing favors regional specialists fluent in local compliance.

The UAE is the fastest-growing geography, with an 8.32% CAGR to 2031. Dubai’s significant tourist arrivals and numerous fast chargers underscore its position as an EV testbed, yet rezoning near Al Maktoum International Airport is inflating land costs and encouraging off-airport delivery models. Abu Dhabi’s MICE events accelerate corporate subscription uptake.

Saudi Arabia advances steadily under Vision 2030, but the Saudization requirements inflate operating costs. Expo Riyadh and giga-projects such as NEOM create new rental corridors, yet ride-hailing recorded substantial trips, intensifying substitution pressure on short-term rentals.

Competitive Landscape

In the Middle East car rental market, fragmentation reigns: no single operator commands a significant share, and the top players collectively account for only a small share of total revenue. Hertz and Sixt spearhead the charge towards fleet electrification. Theeb and Lumi capitalize on domestic networks, while eZhire and Udrive stand out with their app-centric approach.

WheelsOn, a peer-to-peer platform, taps into underutilized private vehicles, significantly reducing hourly rates. Meanwhile, integrated mobility super-apps, though they take a bite with high commissions that squeeze margins, also drive significant volume, presenting a dilemma for smaller fleets. Additionally, rules favoring workforce nationalization and existing supply bottlenecks play into the hands of capital-rich incumbents, enabling them to pre-order vehicles and ramp up automation investments.

Middle East Car Rental Industry Leaders

-

Avis Budget Group

-

Theeb Rent A Car

-

Hertz Corporation

-

Sixt SE

-

Lumi Rental Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Thrifty Car Rentals UAE has unveiled the UAE’s inaugural self-service digital car rental kiosk, marking a significant step in its tech-centric growth strategy. Located at Novotel and Ibis Deira Creekside Dubai, the kiosk empowers customers to swiftly browse vehicles, verify their identity, and make secure payments, all in just minutes. This innovation directly tackles frequent pain points such as lengthy queues, tedious paperwork, and restricted accessibility.

- July 2025: Faster Rent a Car, a leading name in luxury car rentals, unveiled an expanded fleet in Dubai, featuring a stunning array of high-performance, custom-modified vehicles. Each car seamlessly marries elegance with power, promising an unforgettable driving experience on the city's iconic streets.

Middle East Car Rental Market Report Scope

The Middle East car rental market is segmented by booking type (online and offline), application (leisure/tourism, daily utility/business), vehicle type (economy, luxury and premium), end-user type (self-driven and chauffeur), service model (on-airport, and off-airport/local), propulsion (internal-combustion ice, electric, and hybrid) and country (Saudi Arabia, Kuwait, United Arab Emirates, Qatar, and rest of the Middle East). The report offers market size and forecasts for the Middle East car rental in terms of value (USD) for all the above segments.

By Booking Type

| Online |

| Offline |

By Application

| Leisure / Tourism |

| Daily Utility / Business |

By Vehicle Type

| Economy |

| Luxury and Premium |

By End-User Type

| Self-driven |

| Chauffeur |

By Service Model

| On-airport |

| Off-airport / Local |

By Propulsion

| Internal-Combustion (ICE) |

| Electric and Hybrid |

By Country

| Saudi Arabia |

| United Arab Emirates |

| Kuwait |

| Qatar |

| Rest of Middle East Countries |

| By Booking Type | Online |

| Offline | |

| By Application | Leisure / Tourism |

| Daily Utility / Business | |

| By Vehicle Type | Economy |

| Luxury and Premium | |

| By End-User Type | Self-driven |

| Chauffeur | |

| By Service Model | On-airport |

| Off-airport / Local | |

| By Propulsion | Internal-Combustion (ICE) |

| Electric and Hybrid | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Kuwait | |

| Qatar | |

| Rest of Middle East Countries |

Key Questions Answered in the Report

What is the current value of the Middle East car rental market?

The Middle East Car Rental Market size was valued at USD 3.23 billion in 2025 and is estimated to grow from USD 3.41 billion in 2026

How fast is the Middle East car rental market expected to grow?

The market is projected to register a 5.62% CAGR between 2026 and 2031.

Which booking channel is gaining the most traction in Middle East car rentals?

Online and mobile platforms already account for 63.12% of 2025 bookings and are advancing at a 7.81% CAGR.

What challenges slow the adoption of electric rental fleets?

Limited EV insurance capacity, high premiums, and uneven charging infrastructure outside major UAE cities temper near-term fleet electrification.

Page last updated on: