India Car Rental Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

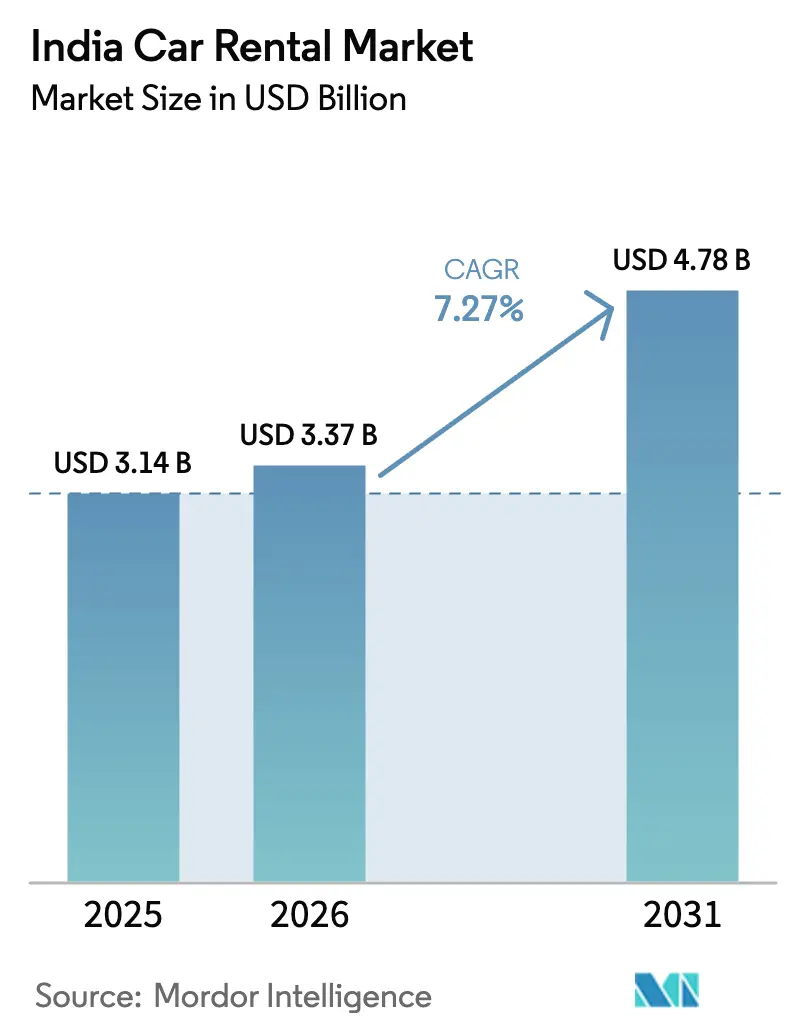

| Base Year Market Size (2025) | USD 3.14 Billion |

| Market Size (2026) | USD 3.37 Billion |

| Market Size (2031) | USD 4.78 Billion |

| Growth Rate (2026 - 2031) | 7.27% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Car Rental Market Analysis by Mordor Intelligence

The India car rental market size is expected to grow from USD 3.14 billion in 2025 to USD 3.37 billion in 2026 and is forecast to reach USD 4.78 billion by 2031 at 7.27% CAGR over 2026-2031. Economic reopening, improving highways, and supportive tax policy keep demand resilient even as price-sensitive travelers scrutinize mobility budgets. Organized operators continue consolidating small fleets, bringing standardized safety features and digital booking tools to a broader customer base. Smartphone penetration surpassing 80% among urban adults has pushed online bookings above two-thirds of all reservations, while subscription models help corporate buyers avoid upfront capital outlays. Policy incentives for electric vehicle uptake and interstate permit simplification give the Indian car rental market additional growth vectors despite near-term cost pressures from insurance inflation.

Key Report Takeaways

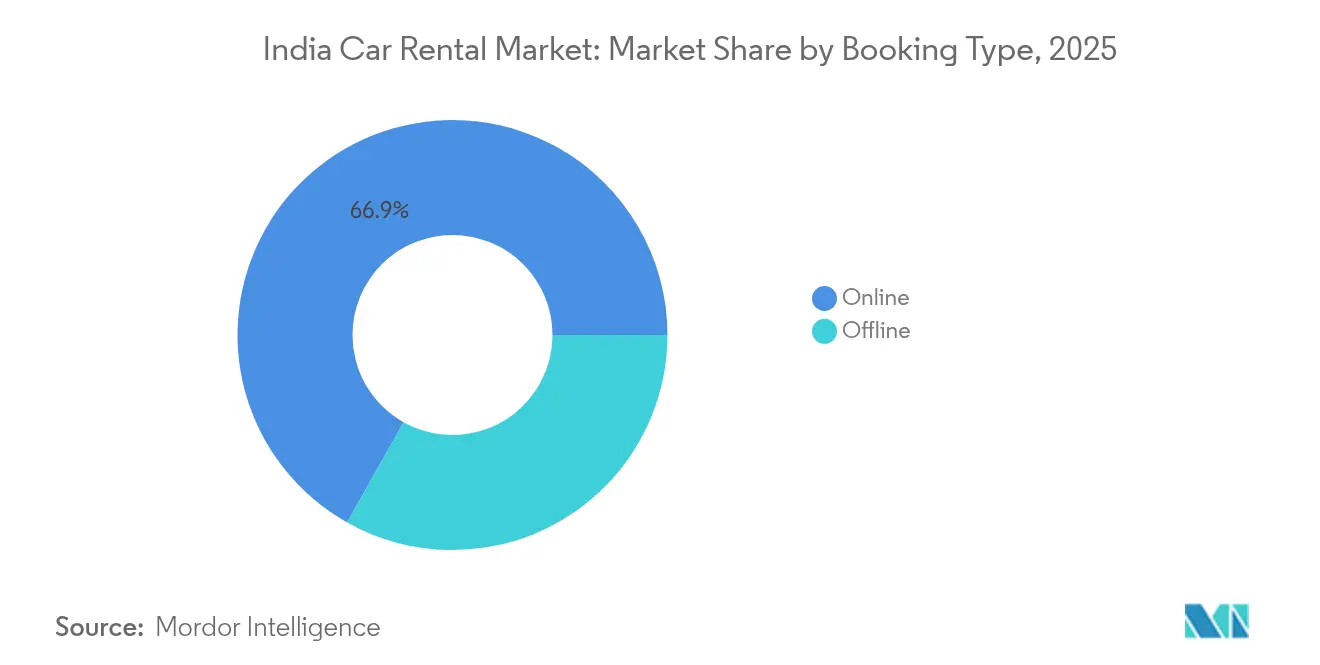

- By booking type, online channels controlled a 66.85% share of the India car rental market in 2025, and are projected to expand at a 7.60% CAGR during the forecast period (2026-2031).

- By application, tourism accounted for a 57.74% share of the Indian car rental market in 2025, while commuting and daily mobility are projected to grow at an 8.42% CAGR during the forecast period (2026-2031).

- By service model, chauffeur-driven controlled a 56.12% share of the Indian car rental market in 2025, while the Self-Drive segment is expected to post an 7.92% CAGR during the forecast period (2026-2031).

- By vehicle class, economy/budget cars controlled 71.88% share of the Indian car rental market in 2025, while the luxury/premium segment is expected to post a 8.82% CAGR during the forecast period (2026-2031).

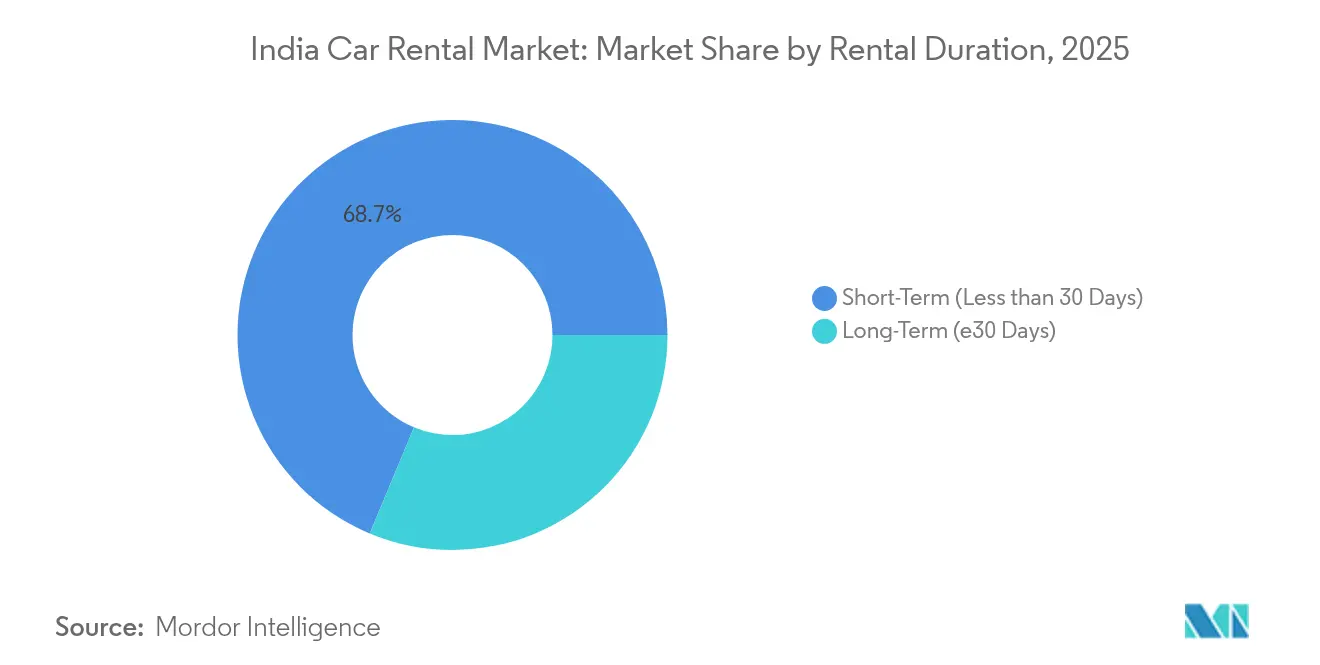

- By rental duration, short-term rentals dominated the Indian car rental market, with a 68.71% share in 2025, while long-term subscriptions are poised for a 9.18% CAGR during the forecast period (2026-2031).

- By rental channel, off-airport rentals controlled 76.10% of the India car rental market share in 2025, whereas airport rentals are projected to expand at an 8.39% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Car Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tourist Flow Fuels Domestic Market | +1.8% | Major metros and tourist circuits | Medium term (2-4 years) |

| Corporates Drive Gig Mobility | +1.5% | Metro cities and industrial hubs | Medium term (2-4 years) |

| Mobile App Bookings Rise | +1.2% | Tier-I cities expanding to Tier-II/III | Short term (≤ 2 years) |

| EV Fleets Grow Via Incentives | +0.9% | Policy-supportive states | Long term (≥ 4 years) |

| GST, Permits Boost Inter-State Travel | +0.7% | National corridors | Short term (≤ 2 years) |

| Rentals Integrate With Travel Ecosystems | +0.6% | Airports and transit hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Domestic and Inbound Tourism Flow

Domestic holidaymakers are projected to drive a considerable revenue growth for tourism enterprises in FY25, prompting rental firms to deploy an incremental fleet in spiritual, coastal, and heritage destinations. Flexible short-duration hires appeal to travelers seeking “micro-holiday” itineraries that public transit cannot cover. Hotel occupancy approaching 68% in 2024 resurrects airport-ground transport synergies. Small-and medium-sized events and a steady rise in meetings demand amplify weekday utilization rates, cushioning seasonal volatility. Government investment in roads, rail connectivity, and destination marketing multiplies demand for legally compliant, tech-enabled car rentals.

Growth of Corporate Travel and Gig-Economy Mobility Demand

India's business travel sector is projected to recover to pre-2019 spending levels by 2025. In 2024, business travel spending in India reached an estimated USD 38.3 billion, making it the 8th largest market globally and 4th in the Asia-Pacific (APAC) region, according to the Global Business Travel Association (GBTA). Hybrid work has increased the need for sporadic yet premium door-to-door transport as firms curtail long-term chauffeur contracts. Employee transportation and chauffeur-car rental services currently penetrate only one-fifth of an addressable INR 1 lakh-crore opportunity, leaving wide space for organized entrants. Gig-economy workers favor daily or weekly packages that blend unlimited kilometers with predictable rates, generating a new mid-duration niche within the Indian car rental market. AI-driven routing helps operators hit punctuality targets despite urban congestion.

Rising Penetration of Mobile-App Based Booking Platforms

Integrations such as Zoomcar’s tie-up with Mappls allow users to locate nearby vehicles, compare tariffs, and complete payment inside a single navigation interface. Subscription features branded “Drive Longer, Pay Less” encourage multi-month commitments, improving fleet utilization. AI-based model selectors bypass the long-standing ambiguity of “Sedan” or “SUV” categories, giving travelers certainty on boot space, safety ratings, and infotainment features. Peer-to-peer listings enlarge supply in smaller towns without asset purchases, broadening the Indian car rental market while keeping overhead light for platform operators. Embedded booking journeys in airline, train, and hotel apps are expected to capture incremental impulse rentals over the next two years.

EV Adoption in Rental Fleets Fueled by FAME II Incentives

The PM E-DRIVE scheme running through March 2026 reimburses up to INR 10,000 per kilowatt-hour for qualifying commercial EVs, offsetting 15-20% of the upfront cost [1]“PM E-DRIVE Scheme Guidelines,” Directorate of Heavy Industries, india.gov.in. Maharashtra's proposal to waive freeway tolls for electric cars aims to reduce costs for operators on intercity routes. Demonstrating industry confidence, private partnerships are emerging, like an energy giant backing thousands of ride-share charging stations. However, the nation grapples with a scarcity of public chargers, operating only a fraction of the millions projected to be necessary by decade's end. Consequently, rental companies are strategically concentrating their EV fleets in Delhi, Bengaluru, and Mumbai, aligning with areas of higher charging density and corporate demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Tier-I City Presence | -1.4% | Tier-II/III nationwide | Medium term (2-4 years) |

| Ride-Hailing Undercuts Multi-Day Rentals | -1.1% | Metro areas with dense ride-hailing fleets | Short term (≤ 2 years) |

| High Compliance Burdens Fleet Operators | -0.8% | National | Short term (≤ 2 years) |

| Sparse EV-Charging Network Hurts Rentals | -0.6% | Non-metro regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Presence Beyond Tier-I Cities

Ecos (India) Mobility derives 60% of its turnover from just four metros, highlighting the difficulty of scaling service quality in smaller markets where maintenance vendors and roadside assistance coverage remain thin. Fragmented local taxes, divergent driver-license categories, and gaps in airport connectivity combine to raise the break-even fleet size in Tier-II towns. Yet used-car ownership is rising rapidly in these cities, signaling latent demand that organized rentals could unlock through franchise partnerships and asset-light peer fleets.

Ride-Hailing Price Advantage Over Multi-Day Rentals

Ride-hailing platforms can offer point-to-point trips at per-kilometer tariffs that are 10-30% lower than full-day rental rates, particularly during off-peak hours when dynamic pricing remains subdued. Their variable-cost driver model eliminates idle-time overhead, enabling frequent discount vouchers that attract price-sensitive travelers away from multi-day packages. Pay-as-you-go billing aligns with sporadic urban travel habits, reducing the perceived need to retain a vehicle for an entire day. Car-rental operators struggle to match these headline fares because daily bundles must absorb parking, insurance, and minimum driver wages even while the vehicle is parked. Rising adoption of ride-sharing passes and corporate wallet integrations further shifts price comparisons in favor of app taxis, leaving rental fleets with lower weekday utilization and heavier reliance on weekend tourism peaks to protect margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Booking Type: Online Platforms Cement Control

The India car rental market accounts for a 66.85% share in the India Car Rental Market in 2025, as bookings through websites or apps, and that are expected to grow with a 7.60% CAGR during the forecast period (2026-2031). Platform integrations with navigation suites reduce discovery friction and feed data back to fleet-planning algorithms. Offline counters persist at railway hubs where walk-up travelers favor human assistance, but automated kiosks and QR code unlocks are rapidly closing the convenience gap.

Peer-to-peer engines diversify fleet make-up and penetrate housing societies and tech parks where traditional rental storefronts are absent. AI chatbots handle most service queries, significantly reducing the average resolution time. Cashback campaigns tied to e-wallets lure budget travelers, while subscription bundles with smartphone upgrades signal cross-industry alliances.

By Application Type: Commuting Demand Outpaces Leisure

Tourism still supplied a 57.74% share in the India Car Rental Market in 2025, but weekday commuting packages show the fastest trajectory at an 8.42% CAGR during the forecast period (2026-2031), as city dwellers pivot away from private ownership. The Indian car rental market share for commuting could rise significantly by the decade-end, narrowing the gap with leisure segments. Organized rental agreements tied to corporate travel platforms ensure predictable pricing and duty-of-care compliance.

Spiritual tourism and “micro-holiday” culture elongate peak seasons, smoothing fleet utilization across quarters. Meanwhile, growth in micro, small, and medium enterprises translates into demand for chauffeur-driven shuttles to ferry staff between suburban factories and transit nodes. Daily subscription passes bundle four intra-city trips under a fixed kilometer cap, reflecting operators' creative packaging.

By Service Model: Self-Drive Continues to Erode Chauffeur Reliance

Chauffeur-driven rides held a 56.12% share in the India Car Rental Market in 2025. Still, self-drive bookings are predicted to grow at an 7.92% CAGR during the forecast period (2026-2031), as navigation apps and automatic transmissions simplify do-it-yourself driving. Indian car rental market players are modernizing fleets with telematics that monitor speed, fuel use, and driver behavior, reducing misuse and insurance claims.

Subscription hybrids merge self-drive flexibility with on-call driver availability for select legs, blurring category lines. Premium cab launches with AI vehicle-match engines allow passengers to guarantee exact models, raising average revenue per trip. Asset-light sourcing—where vendors own 94% of vehicles—keeps balance sheets nimble and supports rapid geographic roll-outs.

By Vehicle Type: Premium Upswing Amid Economy Core

Economy models supplied a 71.88% share in the India Car Rental Market in 2025. Still, luxury and premium vehicles are clocking a 8.82% CAGR during the forecast period (2026-2031) due to rising disposable income and corporate upgrades. The planned rollout of 100% connected-car fleets by several players will push infotainment and ADAS features into mid-segment classes, eroding the experiential gap. The size of premium cars in the Indian car rental market is projected to triple between 2025 and 2030.

SUVs dominate leisure and business hires, capturing customers who value ride height and luggage capacity on intercity highways. EV adoption remains skewed toward premium sub-segments because high sticker prices align better with premium tariff structures and corporate ESG targets.

By Rental Duration: Long-Term Packages Shift Revenue Mix

Short-term hires under 30 days represented 68.71% share in the India Car Rental Market in 2025, but multi-month subscriptions are forecast to lift the long-term slice at a 9.18% CAGR during the forecast period (2026-2031). Corporations view operational leases as a hedge against residual-value swings and regulatory shifts. The Indian car rental market size generated by long-term packages is projected to double by 2030.

Gig-economy professionals subscribe for 28-day cycles, allowing unlimited intra-city kilometers, bolstering weekday utilization. Dynamic pricing engines adjust deposits and per-kilometer charges based on credit scores and telematics-verified driving behavior, rewarding safe use with lower renewals.

By Rental Channel: Airports Rebound, Off-Airport Retains Bulk

Off-airport pickups still own 76.10% share in the India Car Rental Market in 2025, due to lower rents and flexible storefront placement. Airport counters, however, are on an 8.39% CAGR during the forecast period (2026-2031), as international arrivals bounce back. The Indian car rental market participants deploy self-service lockers that cut hand-over time to under five minutes, meeting tight connection schedules.

The government’s Bharatmala initiative has opened new six-lane corridors funneling tourists straight from runways to emergent leisure hubs, raising airport-origin one-way bookings. Off-airport operators respond by launching free doorstep delivery within a 15 km radius, leveraging shared-driver pools to optimize routing.

Geography Analysis

Revenue remains highly metropolitan: Mumbai, Delhi, Bengaluru, and Hyderabad account for a major share of the India car rental market, yet they cover less than 4% of cities served. Each metro records penetration levels above 35 cars per 10,000 residents versus below 5 for Tier-II towns. Interstate projects such as the Delhi–Mumbai Expressway trim transit times by 12 hours, stimulating one-way hires and widening catchment radii for urban suppliers . Maharashtra’s aggregator rules, effective October 2025, harmonize fares across app and offline operators, boosting consumer trust and formal fleet registrations.

Second-tier clusters—Ahmedabad, Kochi, Chandigarh, and Lucknow—display double-digit growth as airport expansion and hotel pipeline investments materialize. However, patchy charging infrastructure limits EV deployment outside metros; less than 400 public chargers operate across all Tier-II locations combined. State incentives such as road-tax waivers in Gujarat and toll discounts in Maharashtra narrow operating costs but remain inconsistent nationwide.

Tourism circuits in Uttarakhand, Rajasthan, and Goa show robust weekend demand; operators therefore document 30-40% above-average kilometer utilization on Friday-Monday blocks. Spiritual corridors encompassing Varanasi, Ayodhya, and Puri witness spikes during festival periods, prompting fleet repositioning strategies. The government’s priority rural road program complements expressways by connecting villages to arterial highways, allowing operators to offer last-mile extensions and tap fresh visitor segments.

Competitive Landscape

The India car rental market is fragmented. Recent consolidation moves - MakeMyTrip’s majority stake in Savaari and CarDekho’s purchase of Revv- mirror a strategic pivot toward scale economies and multi-service super-apps [3]“MakeMyTrip Acquires Savaari Stake,” Economic Times, economictimes.indiatimes.com. Incumbents improve differentiation through AI fleet-planning, IoT-based preventive maintenance, and customizable subscriptions. Technology spending averages 5-6% of revenue, covering proprietary telematics stacks and cloud-native booking engines.

Ride-hailing aggregators enter multi-day rental segments, leveraging captive driver networks and data. Traditional rental operators counter with vendor-sourced fleets to stay asset-light and geographic-agile. Corporate clients increasingly demand ESG-compliant transport; in response, suppliers commit to deploying 25% electric units by 2027. Partnerships with domestic OEMs accelerate electric asset availability while shared battery-swap stations lower range anxiety.

State-level fare and safety regulations raise compliance thresholds that could squeeze micro fleets out of the market, indirectly lifting market share for larger platforms. Yet customer loyalty remains fluid, hinging on vehicle quality and booking transparency rather than brand heritage. Investment capital flows to tech-centric challengers emphasizing subscription suites and embedded APIs for travel portals.

India Car Rental Industry Leaders

Zoomcar

Revv

Ola Drive

Avis India

Myles

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: GoWheelo, India’s leading two-wheeler rental platform, expanded into four-wheeler rentals under a unified brand identity, aiming to position itself as a comprehensive urban mobility partner.

- December 2024: Zoomcar introduced “Zoomcar Cabs” in Bengaluru, offering AI-powered vehicle selection for two hours to 30 days.

- September 2024: Zoomcar and Mappls MapmyIndia integrated direct car-rental booking inside the Mappls navigation app, covering 99 cities.

- March 2024: Eco Mobility extended its corporate car-rental footprint to 10 additional cities, targeting service in 125 cities by FY 2025.

India Car Rental Market Report Scope

Car rental refers to a service wherein a car fleet operating company lends automotive vehicles to customers for a specific period at a pre-defined cost. The car rental market consists of a wide range of companies involved in extending vehicle rental services to its customers across India.

The India car rental market is segmented by booking type, application type, vehicle type, and rental duration. By booking type, the market is segmented into online and offline. By Application type, the market is segmented into tourism and commuting. By Vehicle Type, the market is segmented into luxury/premium cars and economy/budget cars. By Rental Duration, the market is segmented into short-term and long-term.

The report offers market size and forecast value (USD) for all the above segments.

| Online |

| Offline |

| Tourism |

| Commuting / Daily Mobility |

| Self-Drive |

| Chauffeur-Driven |

| Corporate Leasing / Subscription |

| Luxury / Premium Cars |

| Economy / Budget Cars |

| Short-Term (Less than 30 Days) |

| Long-Term (Greater than/equals 30 Days) |

| Airport |

| Off-Airport |

| By Booking Type | Online |

| Offline | |

| By Application Type | Tourism |

| Commuting / Daily Mobility | |

| By Service Model | Self-Drive |

| Chauffeur-Driven | |

| Corporate Leasing / Subscription | |

| By Vehicle Type | Luxury / Premium Cars |

| Economy / Budget Cars | |

| By Rental Duration | Short-Term (Less than 30 Days) |

| Long-Term (Greater than/equals 30 Days) | |

| By Rental Channel | Airport |

| Off-Airport |

Key Questions Answered in the Report

How fast is the India car rental market expected to grow through 2031?

It is anticipated to advance at a 7.27% CAGR, taking revenue from USD 3.37 billion in 2026 to USD 4.78 billion in 2031.

Which booking channel currently dominates national car-rental reservations?

Online platforms captured 66.85% of 2025 bookings and are projected to widen that lead.

What role will electric vehicles play in the next five years?

EV uptake should accelerate as FAME II and PM E-DRIVE incentives cut capex, though charging density outside metros remains a constraint.

Which customer segment is driving the fastest rental-duration growth?

Long-term subscriptions tied to corporate and gig-economy users are forecast to grow at a 9.18% CAGR, outpacing short-term leisure hires.

Page last updated on: