Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

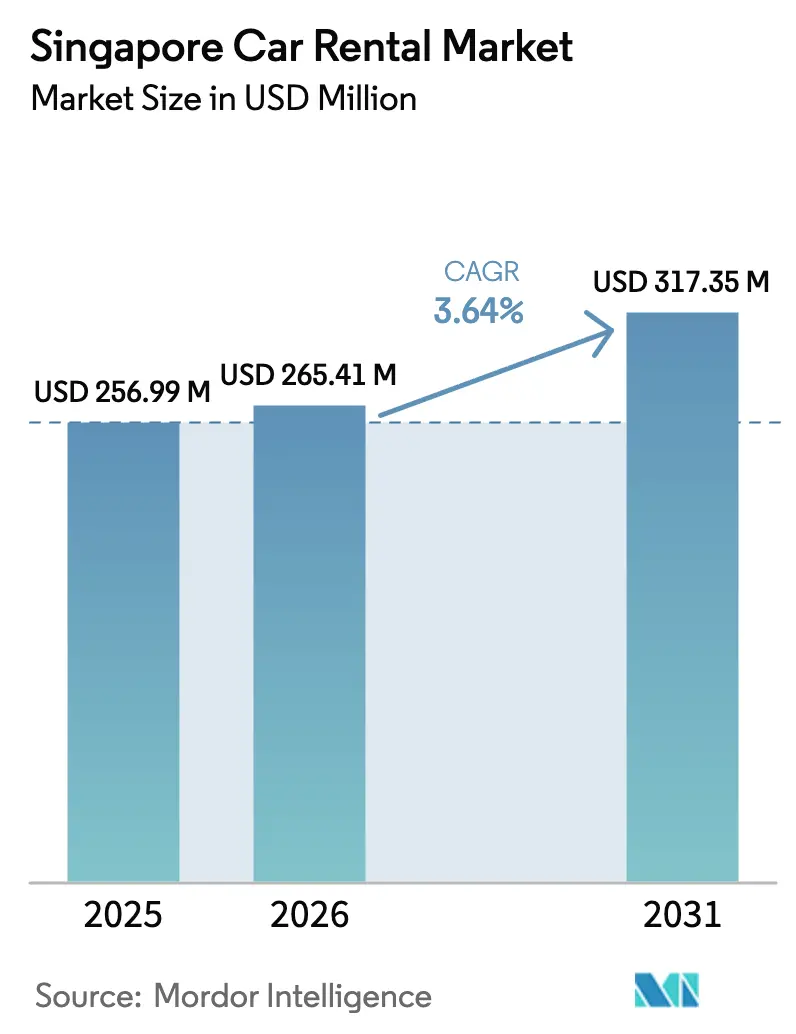

| Base Year Market Size (2025) | USD 256.99 Million |

| Market Size (2026) | USD 265.41 Million |

| Market Size (2031) | USD 317.35 Million |

| Growth Rate (2026 - 2031) | 3.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Car Rental Market Analysis by Mordor Intelligence

The Singapore car rental market size was valued at USD 256.99 million in 2025 and estimated to grow from USD 265.41 million in 2026 to reach USD 317.35 million by 2031, at a CAGR of 3.64% during the forecast period (2026-2031). Steep Certificate of Entitlement (COE) premiums, a tourism rebound, and increasing corporate appetite for asset-light mobility are the primary forces behind this steady trajectory. Global franchises continue to defend their airport counters, while digital-first local platforms are scaling rapidly by locating cars within public housing estates and near mass transit exits. Fleets are tilting toward lower-emission models as Commercial Vehicle Emissions Scheme (CVES) incentives neutralize much of the electric-vehicle price premium, while AI-based fleet-management software is trimming idle time and maintenance costs. Although spiking insurance premiums and scarce overnight electric vehicle (EV) chargers present headwinds, elevated ownership costs and a policy push toward cleaner powertrains should keep rental utilization resilient through 2031.

Key Report Takeaways

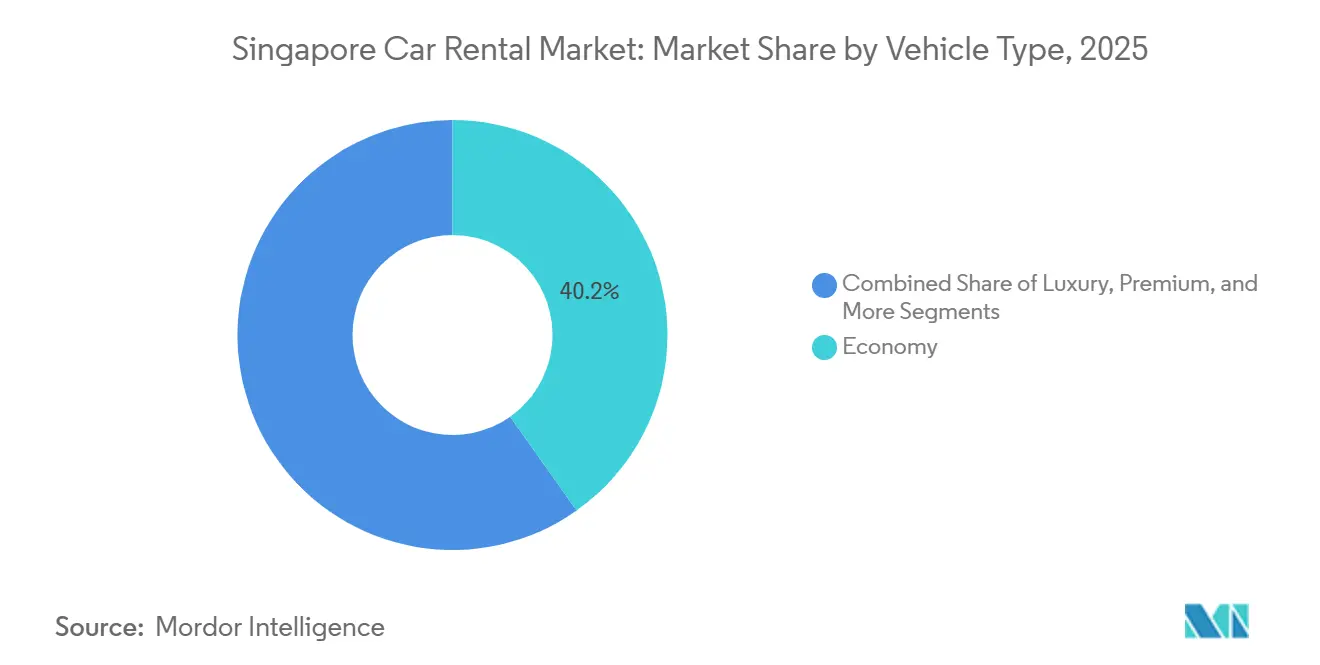

- By vehicle type, economy cars captured 40.21% of 2025 revenue, while sport-utility and multi-purpose vehicles recorded the quickest volume gains at 6.27% over the outlook period.

- By booking channel, online channels still generated 73.29% of the revenue in 2025, and the same platforms are expanding at an 8.24% CAGR through 2031.

- By rental duration, short-term contracts (under 30 days) held a 62.43% share in 2025, whereas long-term leases are projected to advance at an 8.08% CAGR through 2031.

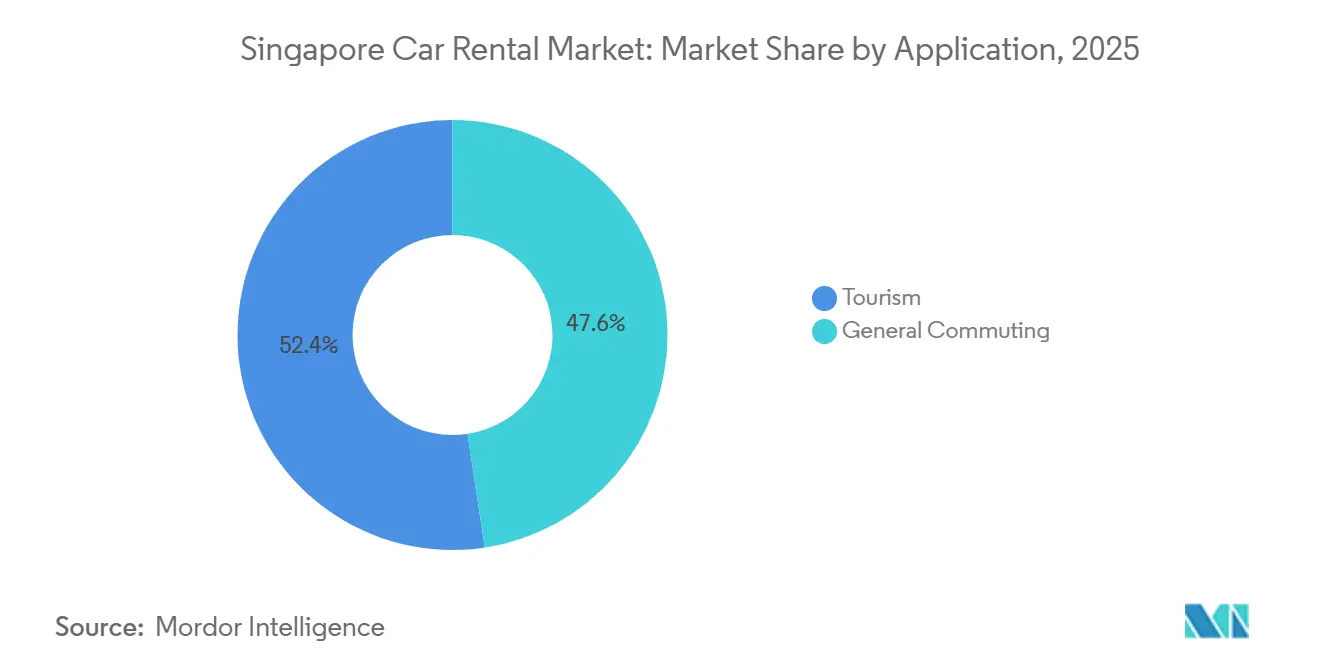

- By application, tourism commanded a 52.39% market share in 2025; however, general commuting is growing faster at a 9.35% CAGR across the forecast window.

- By powertrain, internal-combustion vehicles accounted for 82.26% of fleet mix in 2025, while electric-vehicle rentals are forecast to jump at a 12.27% CAGR through 2031.

- By end user, individuals generated 64.18% of 2025 revenue, but corporate clients are widening at a 9.23% CAGR through 2031 as firms favor subscription-based mobility.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore Car Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Certificate of Entitlement (COE) Premiums | +0.8% | Singapore (nationwide impact, with concentration in Central Region, East Region, North Region, West Region, and North-East Region) | Short term (≤ 2 years) |

| Tourism Rebound | +0.6% | Singapore (concentrated in Changi Airport vicinity, Orchard Road, Marina Bay, Sentosa, and Central Business District) | Medium term (2-4 years) |

| Flexible Corporate Mobility | +0.5% | Singapore (concentrated in Central Business District, Jurong East, Changi Business Park, and one-north) | Medium term (2-4 years) |

| EV-Rental Incentives | +0.4% | Singapore (nationwide impact across all planning regions) | Long term (≥ 4 years) |

| Subscription and P2P Rentals | +0.4% | Singapore (concentrated in HDB estates, MRT station vicinities, and residential clusters in Tampines, Jurong, Woodlands, and Punggol) | Short term (≤ 2 years) |

| AI Fleet Optimization | +0.3% | Singapore (nationwide fleet operations with hubs in Changi, Tuas, and Woodlands) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising COE Premiums Pricing Out Ownership

Category A Certificate of Entitlement (COE) premiums have risen significantly, pushing the all-in cost of a compact sedan to a high level before financing. Despite the Land Transport Authority (LTA) releasing additional quotas, prices remain well above pre-pandemic levels [1]“Monthly COE Open Bidding Results,”, Land Transport Authority, lta.gov.sg. Households priced out of ownership are reserving economy cars for weekends several weeks in advance, indicating a structural reset in mobility budgeting. Affluent buyers migrating to Category B vehicles further amplify rental demand for entry-level sedans because fleet operators focus on segments with the widest addressable base. The shift toward variable-cost mobility suggests that a mild COE retreat will not immediately prompt consumers to revert to outright ownership.

Tourism Rebound and Inbound Arrivals

International arrivals reached 16.5 million in 2024, a 21.5% increase year-over-year, while tourism receipts totaled SGD 29.8 billion (USD 22.1 billion) [2]“International Visitor Arrivals 2024,”, Singapore Tourism Board, stb.gov.sg. During holiday peaks, airport-based rental operators experienced a significant increase in utilization rates compared to off-peak months. Economy-class bookings are predominantly led by visitors hailing from Indonesia, Malaysia, and China. However, there is a noticeable trend: renters from India and the Middle East are increasingly gravitating toward premium sport-utility vehicles (SUVs), even willingly paying a cross-border surcharge for drives into Malaysia. Meanwhile, peer-to-peer hosts are capitalizing on their idle cars, listing them while abroad, which in turn amplifies fleet supply without any capital expenditure from operators. The outlook for the Singapore car rental market remains optimistic, buoyed by steady weekend and holiday utilization driven by inbound leisure travel.

Government EV-Rental Incentives Drive Electrification

The Commercial Vehicle Emissions Scheme (CVES) provides rebates for Band A electric cars while levying fees on high-emission Band C models. This creates a significant incentive gap, steering renewal cycles towards electric vehicles (EVs). While the Early Adoption Incentive is set to conclude, commercial operators continue to benefit from the complete CVES relief. This advantage allows them to purchase vehicles like the BYD Atto 3 or Tesla Model 3 at prices comparable to petrol compact cars. GetGo, capitalizing on these savings, charges renters a lower rate for EVs compared to petrol models. In a strategic move, Grab has inked a regional partnership with BYD, aiming to acquire a significant number of electric vehicles (EVs) throughout Southeast Asia. This collaboration also emphasizes the integration of live vehicle data for enhanced predictive maintenance. The swift electrification of rental fleets not only underscores the industry's shift but also resonates with the government's vision of achieving cleaner public road traffic.

AI-Driven Fleet Optimization Lowering Operator Costs

Many local rental companies plan to adopt AI-enabled fleet software. A telematics suite, supported by a government grant, provides dashboards with insights on utilization data, driver scoring, and predictive maintenance alerts, enabling managers to reallocate idle assets. Early adopters of this technology have reported improved utilization and reduced maintenance costs. Another platform uses GPS and battery-state data to guide users to nearby cars with sufficient charge, effectively reducing repositioning mileage. Software as a Service (SaaS) vendors are now offering similar toolkits to smaller fleets, thereby enhancing cost efficiency across the car rental landscape.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Insurance Premiums | -0.5% | Singapore (nationwide impact on all commercial fleet operators) | Medium term (2-4 years) |

| EV Charger Scarcity | -0.3% | Singapore (acute in Central Business District, Orchard, and tourist precincts; less severe in HDB estates with resident chargers) | Long term (≥ 4 years) |

| Deposit Disputes | -0.2% | Singapore (nationwide impact across all rental touchpoints) | Short term (≤ 2 years) |

| High ERP Charges | -0.2% | Singapore (concentrated in Central Business District, Orchard Road, Marina Bay, and major expressways) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Spiking Insurance Premiums for Rental Fleets

Motor gross written premiums have increased, while underwriting losses have significantly risen. Renewal quotes for rental fleets are notably higher than previous levels, and deductibles on standard policies have also increased [3]“Motor Insurance Statistics 2025,”, General Insurance Association of Singapore, gia.org.sg. To mitigate exposure, Avis imposes daily charges for zero-deductible waivers and partial options, which can substantially raise weekly expenses for customers. FIDReC’s expanded remit to handle third-party motor disputes offers a means of redress but also prolongs settlement timelines, tying up operators' cash. Small fleets, with limited bargaining power, are facing compressed margins, which is slowing the entry of new players into the market.

Scarcity of Overnight Public EV Chargers

Public chargers in Singapore are predominantly located within Housing & Development Board carparks, limiting access primarily to residents. As a result, urban rental hubs and commercial lots find themselves vying for a limited number of available chargers. This competition drives operators to incur additional costs for charging and parking. Weekend usage of EVs sees a decline, mainly due to renters' concerns over range anxiety. This is particularly pronounced for trips to Malaysia, where fast charging stations are not as prevalent. The absence of 24-hour curbside chargers in tourist hotspots and downtown garages raises concerns. If this trend continues, the share of EVs in Singapore's car rental market might fall short of the government's policy aspirations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Economy Segment Drives Democratic Access

The economy category accounted for 40.21% of the Singapore car rental market share in 2025 and is on track to post a 6.27% CAGR through 2031, demonstrating that value-oriented demand remains the backbone of fleet utilization. As operators cascade EV rebates into seven-seater models, the Singapore car rental market for SUVs is poised for growth. Eurokars Leasing revamped its digital platform, allowing customers to switch from a Mazda 3 to a Porsche Cayenne mid-booking, contingent on availability. While GetGo continues to use hatchbacks to optimize parking across its sites, its pilot of Tesla Model 3 units tests the market's appetite for premium EVs. Hertz's global deal for Tesla vehicles is now seeding the local fleet, and the LTA's cleaner-energy mandate is poised to reshape the vehicle mix.

Operators note an uptick in cross-booking from economy to premium tiers during holidays, hinting at potential upsell revenue. However, as battery EV residuals stabilize and their servicing costs drop compared to combustion engines, the margin gap tightens. Fleet managers are expected to shift their focus towards mid-priced EV sedans that align with regulatory, cost, and consumer experience benchmarks.

By Booking Channel: Digital Transformation Accelerates

Online channels captured more than 73.29% of 2025 revenue and are on track for an 8.24% CAGR to 2031. The shift reflects consumer comfort with app-based contracts, real-time pricing, and keyless entry. GetGo, which leverages a mobile-only approach that eliminates counter staff and paper forms, has amassed a significant subscriber base. Europcar, capitalizing on high-intent traffic, embedded rental offers into Singapore Airlines’ KrisFlyer booking path, earning miles for each leisure transaction. However, offline channels remain vital for those seeking last-minute or personalized services. Sixt’s myDriver, in collaboration with Cathay Pacific, offers chauffeur services to the airline’s premium clientele, steering high-value clients straight to Sixt.

Operators face mounting pressure from digital price-discovery tools, prompting them to either tighten their cost structures or differentiate themselves with flexible pickup points and bundled services. With API integrations into SAP Concur and Navan, automatic expense reconciliation is now a reality, broadening corporate engagement. As the rollout of distance-based charging progresses, the integration of real-time trip pricing in booking apps is set to bolster the appeal of digital channels.

By Rental Duration: Long-Term Contracts Gain Corporate Traction

Short-term rentals of under 30 days retained a 62.43% share in 2025; however, the Singapore car rental market size for long-term contracts is forecasted to advance at an 8.08% CAGR through 2031. Corporates hedge COE volatility by locking in six- to 24-month subscriptions that bundle insurance, maintenance, and roadside assistance into a single invoice. GetGo's ZipZap program features a "Subscribe and Share" option, enabling primary users to sub-rent to family members, seamlessly blending rental services with fractional ownership. Smaller operator Ecube expanded its fleet to target expatriates on extended assignments. While volume fluctuations are influenced by inbound tourism, the more stable revenue from corporate multi-month agreements supports cash-flow predictability in uncertain economic conditions.

Leisure travelers and spontaneous errands drive short-term demand, particularly during holiday peaks, which push airport usage to high levels. However, operators are increasingly focusing on long-term subscribers due to benefits such as lower acquisition costs, consistent usage patterns, and quicker vehicle turnover. With elevated COE premiums, long-term subscriptions are expected to gain traction over short-term ones. Nevertheless, the influence of tourism ensures that short-term demand remains a dominant factor.

By Application: General Commuting Emerges as Growth Driver

Tourism accounted for 52.39% of 2025 revenue, but general commuting bookings are rising at an annual rate of 9.35%, reflecting the COE-induced shift away from outright ownership. Partnerships like GetGo's collaboration with SBS Transit, deploying cars near MRT stations, effectively bridge the first- and last-mile gaps, seamlessly integrating rentals with public transport. Middle-income families typically rent cars for grocery shopping and family outings, avoiding the burden of high fixed costs. Corporate activities, including sales calls, project shuttles, and off-site meetings, contribute to a steady volume, helping to balance operator utilization curves without being tied to seasonal peaks.

While leisure travel will continue to dominate tourism, the frequent and off-peak nature of commuting plays a crucial role in fleet economics. Operators utilize AI algorithms to strategically position cars, directing them to residential areas on weeknights and tourist hotspots at dawn, thereby minimizing empty mileage.

By Powertrain Type: Electric Transition Accelerates

Internal-combustion engines held 82.26% of the 2025 fleet share, yet electric vehicles are projected to surge at a 12.27% CAGR, carving out one-fifth of active units by 2031. Due to the CVES rebate and reduced energy costs, EV rentals enjoy a significant price advantage. This is evident, as EVs are more cost-effective than petrol cars. Meanwhile, Grab, in partnership with BYD, is expanding its EV fleet across the region. This ambitious move not only boosts Grab's bargaining power for bulk pricing but also enhances its leverage in securing charging packages. While hybrids serve as a stopgap amid charger shortages, current policies indicate a strong push towards full electric adoption. To navigate potential public network challenges, rental operators are likely to invest in modular charging pods at their depots and forge agreements with private garages.

Residual-value uncertainty poses a challenge, particularly if advancements in next-gen batteries lead to reduced depreciation. However, the Singapore car rental sector enjoys an advantage: shorter holding periods compared to owning a car privately. This allows them to swiftly refresh their fleets and capitalize on technological advancements. As older units phase out and operators pursue CVES rebates for cost optimization, the share of internal combustion engines (ICE) in the market is set to decline.

By End User: Corporate Adoption Accelerates

In 2025, individuals accounted for a 64.18% share of the market, but the corporate segment is expanding at a 9.23% CAGR, as companies favor operating-expense models over traditional capital outlays. For instance, SP Mobility launched a corporate fleet card that includes EV charging credits. Meanwhile, Element Fleet Management has partnered with BYD, aiming to attract multinationals interested in outsourced lifecycle management. GetGo's ZipZap subscription is gaining traction among SMEs, offering them a predictable mobility budget without requiring deposits. Corporate contracts, often characterized by longer tenures and reduced churn, enhance the lifetime value per customer, even if their daily rates are less than those for casual tourists.

While individual leisure will continue to dominate the number of days rented, driven by tourism volumes, corporate users are poised to capture an increasing share of revenue, thanks to their preference for premium vehicles and bundled services. Furthermore, as companies pivot towards EV pools to meet carbon targets, sustainability mandates could further hasten this shift.

Geography Analysis

In Singapore, where land is scarce, the focus is on app usability, fleet diversity, and convenience rather than geographic expansion. The mandatory ERP 2.0 GPS-based tolling system has been implemented, with a significant number of on-board units installed. With dynamic congestion pricing in effect, peak-hour drives downtown become more expensive, steering renters towards off-peak times or public transportation pickups. Tourist arrivals have been increasing, on track to reach pre-pandemic levels, bolstering consistent airport demand. While cross-border rentals to Johor Bahru and Malacca remain in vogue, heightened customs checks in Malaysia occasionally extend turnaround times, leading operators to increase buffer days between bookings.

Fleet electrification is influenced by geography, as most public chargers are typically located in residential areas. This concentration compels operators in the urban core to seek access to private garages. The Land Transport Authority (LTA) has prohibited the registration of new diesel vehicles and mandated that all new cars adopt cleaner energy sources. These moves push existing internal combustion engine (ICE) fleets to consider earlier renewals. Despite LTA's attempt to alleviate the situation by injecting additional quotas, COE premiums remain high, sidelining the middle class and bolstering rental penetration.

Given Singapore's inland geography, the average trip length is brief, alleviating range anxiety for EV renters. Yet, for weekend trips into Malaysia, many still prefer petrol SUVs due to the scarcity of fast-charging stations on longer routes. The city's policy landscape, limited road capacity, and constrained real estate collectively foster a rental ecosystem tailored for short trips, dense parking, and digital accessibility.

Competitive Landscape

Global brands such as Avis Budget, Hertz, and Sixt have established a strong presence at Changi Airport and in the downtown hospitality clusters. However, local app-based firms are now dominating intra-town point-to-point trips. GetGo has staked the most significant app-based footprint, operating across numerous locations and catering to a vital subscriber base. TribeCar manages a substantial fleet, and Drive Sg features privately owned units on its peer-to-peer marketplace. BlueSG's temporary suspension removed a large number of EVs from circulation, benefiting its rival. Additionally, the LTA introduced a lock-in for business-owned chauffeured private-hire cars, aiming to curb speculative fleet flipping and stabilize supply.

Technology adoption plays a pivotal role in differentiation. For instance, early adopters of Cartrack telematics experienced a notable reduction in unplanned downtime. Meanwhile, white-label AI pricing engines are enabling smaller firms to compete more dynamically. Subscription bundles that integrate insurance and maintenance into a single fee are particularly appealing to professionals seeking predictable expenses. Looking ahead, autonomous trials are introducing a new dimension: Grab-WeRide plans to roll out driverless shuttles in Punggol, and ComfortDelGro-Pony.ai is set to pilot AVs within LTA’s sandbox. As AV adoption brings cost savings, fares might decrease, posing a challenge to traditional rent-and-drive models unless operators adapt to managing autonomous fleets.

Singapore Car Rental Industry Leaders

SIXT SE

Avis Budget Group

Drive Sg

Europcar Mobility Group

Hertz Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Ryde, a prominent technology platform specializing in mobility and quick commerce in Singapore, has unveiled a strategic move to venture into the electric vehicle ("EV") rental market. This pivotal step not only underscores Ryde's commitment to sustainable mobility but also strategically positions the company to tap into Singapore's burgeoning demand for eco-friendly transportation. This demand surge is bolstered by favorable government policies, heightened corporate ESG priorities, and a swift consumer shift towards EV adoption.

- October 2025: Ecube Car Rental, a top car leasing provider in Singapore, has bolstered its fleet with new models to meet surging market demand. The newly added vehicles emphasize modern efficiency, predominantly featuring hybrids, alongside petrol and electric options.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Singapore car rental market as the paid, short-term hire of passenger cars, ranging from small economy units to premium SUVs, made available to individuals or corporate clients for periods under twelve months, whether self-drive or chauffeur-driven.

Scope Exclusion: vehicle subscription schemes and multi-year operating leases fall outside this assessment.

Segmentation Overview

- By Vehicle Type

- Economy

- Premium

- Luxury

- Sport Utility Vehicle and Multi-Purpose Vehicle

- By Booking Channel

- Online

- Offline

- By Rental Duration

- Short-term (Less Than 30 days)

- Long-term (More Than 30 days)

- By Application

- Tourism

- General Commuting

- By Powertrain Type

- Internal Combustion Engine (ICE)

- Hybrid

- Electric Vehicle (EV)

- By End User

- Individual

- Corporate

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with fleet managers, airport concession holders, digital aggregators, and mobility start-ups across Central, Western, and Changi clusters. These conversations validated service mix, utilization rates, and booking-channel shifts that raw statistics alone could not surface.

Desk Research

We collated public data from tier-one bodies such as the Land Transport Authority, Singapore Tourism Board, Department of Statistics Singapore, and ASEANstats, then enriched it with company filings and local press. To profile fleet sizes and average tariffs, D&B Hoovers and Dow Jones Factiva furnished hard numbers on leading operators. Additional cues on EV incentives were drawn from official budget papers and URA policy releases. The listed sources illustrate our wider desk sweep; many others were tapped for spot checks and clarifications.

Market-Sizing & Forecasting

We start with a top-down build: inbound visitor nights, resident car ownership costs, and corporate expatriate headcount create the demand pool, which is priced using average daily rental tariffs. Select bottom-up roll-ups, sampled fleet counts multiplied by utilization, act as a reasonableness cross-check before totals are reconciled. Key variables include Certificate of Entitlement premiums, tourist arrivals, online booking penetration, average tariff, fleet renewal cycles, and EV rebate uptake. A multivariate regression, stress tested through scenario analysis, drives the 2025-2030 forecast.

Data Validation & Update Cycle

Outputs pass variance screens against historical series and peer geographies, then a second analyst reviews anomalies. Reports refresh yearly; interim triggers, such as regulatory shifts or material M&A, prompt ad-hoc updates before client delivery.

Why Mordor's Singapore Car Rental Baseline Earns Client Trust

Published estimates often diverge because firms vary scope, embed untested ASP assumptions, or roll regional figures down to the city-state.

Key gap drivers here include: some studies bundle long-term leasing, others convert SGD to USD at spot rather than period averages, and several apply aggressive tourist growth scenarios unvetted by local stakeholders. Mordor's scoped definition, mixed-method model, and annual refresh cadence minimize such swings.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 256 M (2025) | Mordor Intelligence | - |

| USD 1.97 B (2024) | Regional Consultancy A | Includes car leasing and chauffeur services |

| USD 0.75 B (2024) | Trade Journal B | Uses airport arrivals alone, omits local commuting demand |

| USD 1.78 B (2022) | Global Consultancy C | Applies flat USD-SGD spot rate and global ASP benchmarks |

Taken together, the comparison shows that when scope creep, currency choices, and single-source assumptions are stripped away, Mordor's disciplined approach yields a balanced, transparent baseline that decision-makers can retrace and trust.

Key Questions Answered in the Report

What is the current size of the Singapore car rental market?

What is the current size of the Singapore car rental market?

Why are long-term subscriptions gaining popularity?

Corporations and expatriates prefer six- to 24-month plans that sidestep volatile COE prices and bundle insurance, maintenance, and roadside assistance into a flat monthly fee.

What is the main restraint facing EV rentals?

Overnight charger scarcity remains the biggest bottleneck, with most public chargers located in residential estates rather than commercial lots or tourist districts.

How does ERP 2.0 affect rental pricing?

ERP 2.0 imposes distance- and time-based congestion fees, prompting operators to incorporate dynamic toll estimates into booking apps and encourage off-peak pickups.

Page last updated on: