Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.95 Billion |

| Market Size (2026) | USD 2 Billion |

| Market Size (2031) | USD 2.33 Billion |

| Growth Rate (2026 - 2031) | 3.11% CAGR |

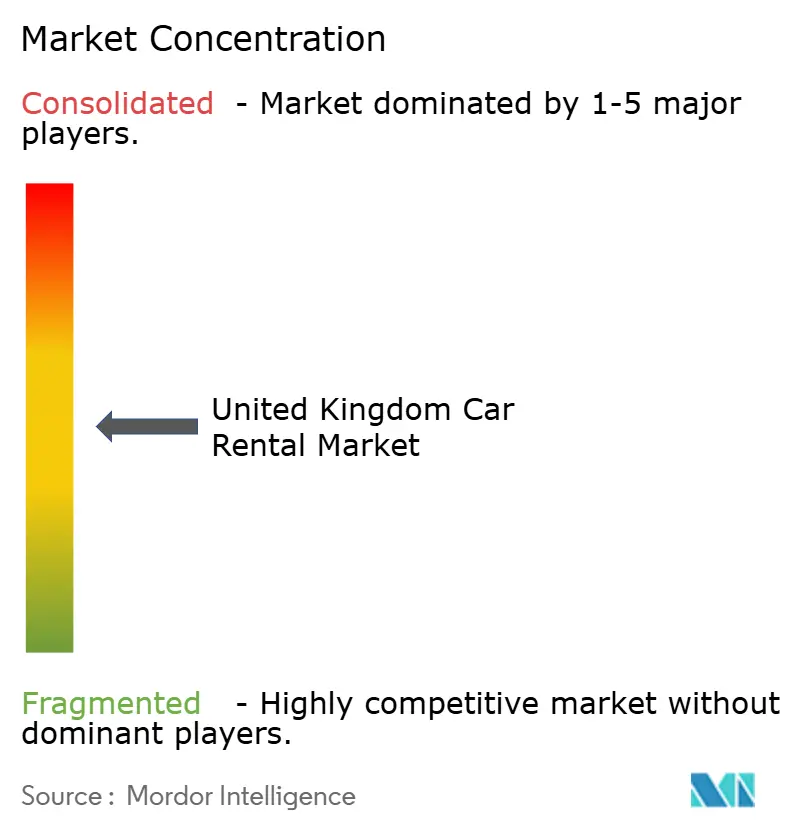

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom Car Rentals Market Analysis by Mordor Intelligence

The United Kingdom car rental market size is expected to grow from USD 1.95 billion in 2025 to USD 2 billion in 2026 and is forecast to reach USD 2.33 billion by 2031 at a 3.11% CAGR over 2026–2031. Fleet electrification mandates, widening digital adoption, and shifting corporate travel patterns are reshaping growth dynamics without altering the modest headline expansion. Operators are balancing elevated vehicle-acquisition costs against residual-value uncertainty, while mobile-first booking is compressing lead times and forcing heavier investment in yield-management technology. The closure of Zipcar’s local operations in December 2025 removed a high-fixed-cost competitor yet underscored that cost-of-living pressures and expanding congestion zones continue to test capital-intensive models. Growth pockets remain in long-term subscription programs, premium vehicle rentals linked to international arrivals, and business travel demand buoyed by rail strike disruption.

Key Report Takeaways

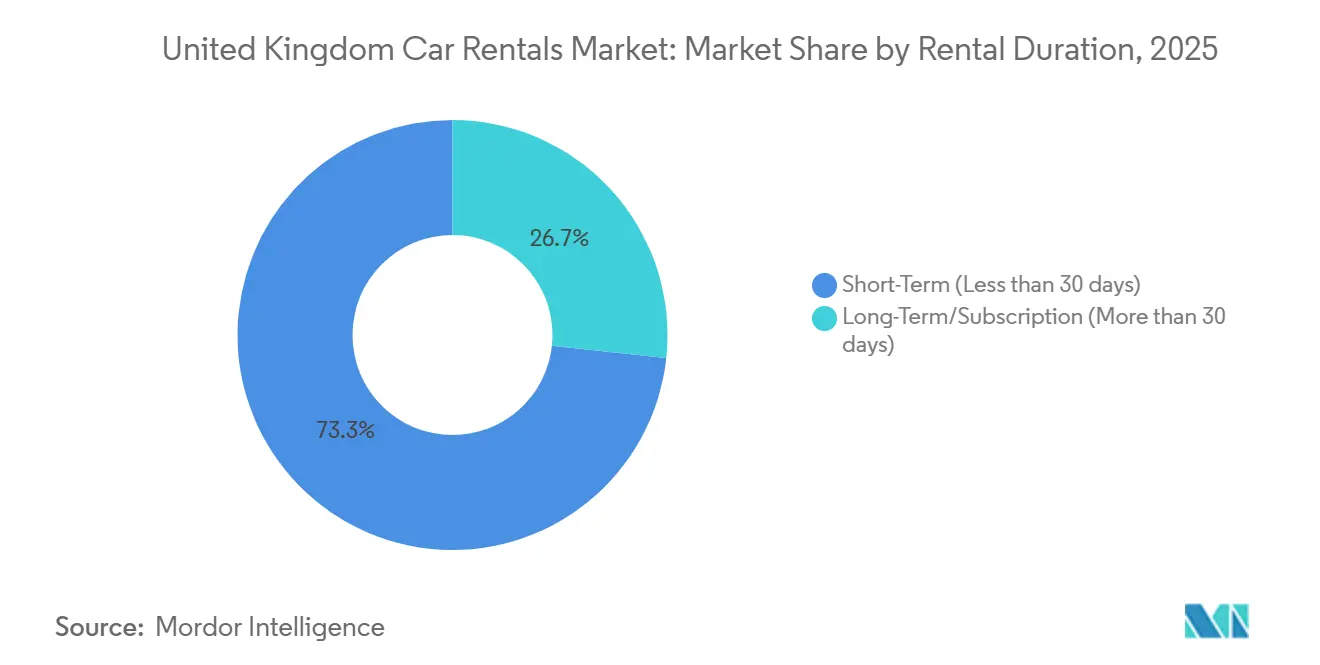

- By rental duration, short-term rentals held 73.30% revenue share in 2025; long-term and subscription models are projected to expand at a 12.67% CAGR through 2031.

- By booking type, online channels led with a 67.50% revenue share in 2025 and are projected to advance at a 10.81% CAGR through 2031.

- By application, leisure and tourism accounted for a 55.70% revenue share in 2025, while business rentals are projected to grow at a 9.63% CAGR through 2031.

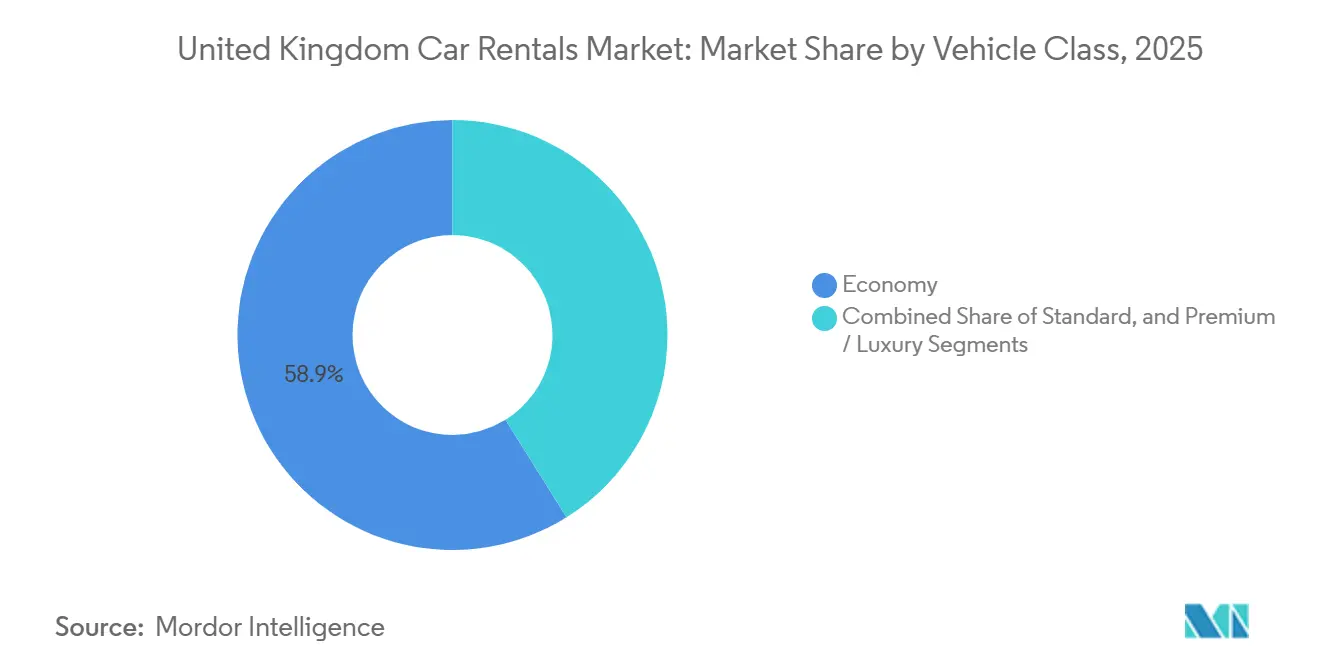

- By vehicle class, economy cars dominated with a 58.90% revenue share in 2025; premium and luxury vehicles are expected to expand at an 11.86% CAGR through 2031.

- By propulsion type, internal-combustion engines represented 81.10% revenue share in 2025, whereas battery-electric vehicles are surging at a 26.60% CAGR through 2031.

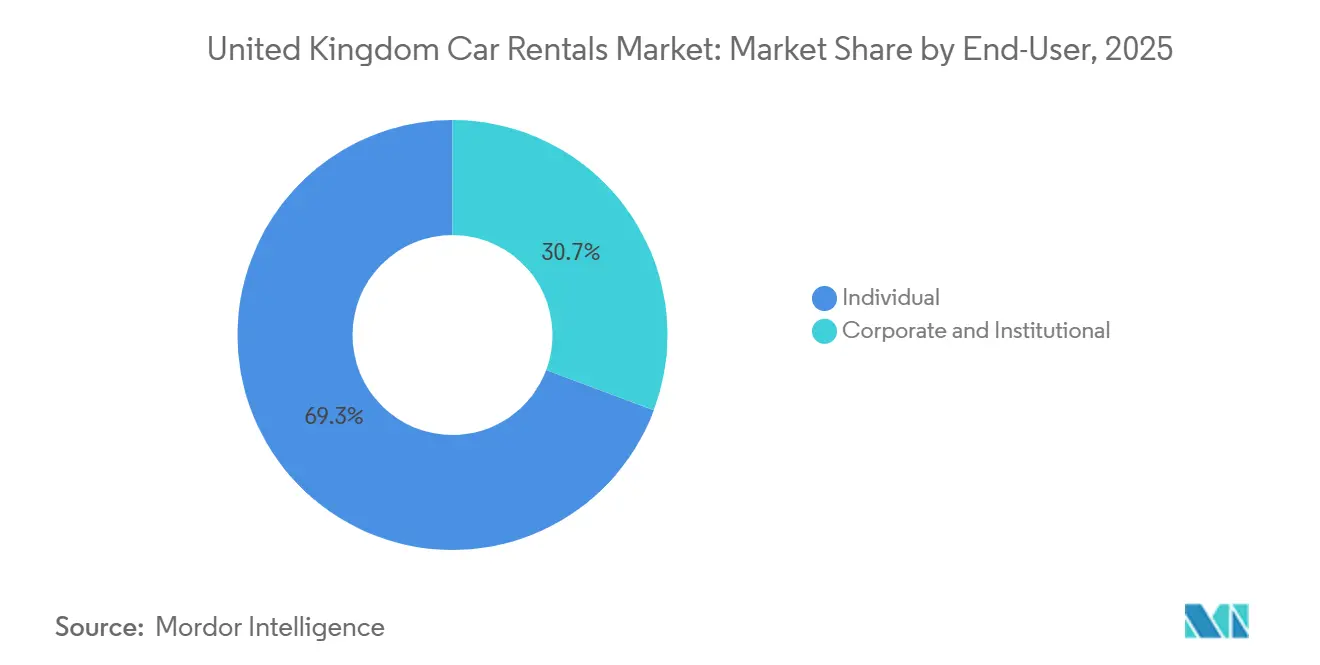

- By end-user, individuals generated a 69.30% revenue share in 2025 and are projected to progress at a 10.80% CAGR through 2031.

- By booking channel, off-airport and downtown locations held a 53.50% revenue share in 2025 and are projected to rise at an 11.60% CAGR through 2031.

- By geography, England captured 74.80% revenue share in 2025 and is forecast to grow at an 8.90% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Car Rentals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-First Booking Boom | +0.8% | England (London, Southeast), Scotland (Edinburgh, Glasgow) | Short term (≤ 2 years) |

| EV Incentives and Fleet Mandates | +0.7% | National | Long term (≥ 4 years) |

| Post-Pandemic Leisure Surge | +0.6% | England (coastal regions), Wales, Scotland (Highlands) | Medium term (2-4 years) |

| Duty-of-Care Drives Rentals | +0.5% | England (London, Birmingham, Manchester), Scotland (Edinburgh) | Medium term (2-4 years) |

| Growth of Flex-Rent Models | +0.4% | England (urban centers), Scotland (Glasgow) | Medium term (2-4 years) |

| OEM-Backed Captive Programs | +0.3% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Digital-first Consumer Journey and Mobile Booking Boom

Mobile app downloads for travel services experienced growth, even as website traffic declined. This trend encouraged rental operators to prioritize investments in native apps to sustain their visibility. Online platforms hold a significant share of the UK's car rental market and continue to grow steadily. However, their influence extends beyond just facilitating transactions. Same-day reservations have become increasingly popular, reducing the average booking lead time and emphasizing the importance of real-time fleet allocation tools. Locations situated off-airport and in downtown areas benefit from this shift, as location-based searches now favor proximity over brand loyalty. Independent operators are capitalizing on walk-in demand, while global chains are focusing on algorithm-driven pricing strategies that resemble those used by airlines in yield management practices[1]"Rental Outlook 2025,”, British Vehicle Rental and Leasing Association, bvrla.co.uk. This strategic shift is driving higher IT expenditures while simultaneously increasing revenue per available car through improved utilization.

EV-Friendly Government Incentives and Zero-Emission Fleet Mandates

The Zero Emission Vehicle mandate aims to significantly increase the adoption of battery-electric vehicles in new car sales over the coming years. Battery-electric vehicles, while currently a small portion of rental fleets, are experiencing the fastest growth within the United Kingdom's car rental market. Public charging infrastructure has seen substantial expansion, including the addition of rapid charging units to support the growing demand. However, challenges persist, as many operators identify charging availability and customer unfamiliarity with the technology as key obstacles to broader adoption. Collaborations with original equipment manufacturers are helping to address these issues. For example, a partnership between SIXT and Stellantis ensures a consistent supply of battery-electric models equipped with advanced telematics, while also sharing the costs associated with charging infrastructure throughout the rental lifecycle. Additionally, the government's commitment to transitioning all departmental fleets to zero-emission vehicles demonstrates a stable policy environment, which helps reduce uncertainties for private-sector stakeholders.

Post-Pandemic Domestic Leisure Travel Surge

Domestic staycations in the UK have been a significant contributor to the tourism industry, generating substantial revenue. Although the number of trips has not yet returned to pre-pandemic levels, the spending per trip has shown an increase. Leisure travelers hold a dominant share of the car rental market in the United Kingdom, driven by the popularity of self-catering holidays in destinations such as Cornwall, the Lake District, and the Scottish Highlands. These locations have fueled the demand for multi-day car rentals. Scotland has emerged as a key destination for overnight visitors, with a notable portion of tourism revenue linked to self-drive itineraries along scenic routes like the North Coast 500. Car rental operators face challenges in managing fleet deployment to rural areas, which often ties up capital during periods of low demand. However, seasonal shortages in vehicle availability can lead travelers to explore peer-to-peer car rental platforms. To optimize revenue during peak travel periods, operators are increasingly adopting flexible fleet-rotation strategies and implementing dynamic pricing models.

Growth of Subscription-Based Flex-Rent Models

Long-term and subscription products are experiencing significant growth, far outpacing the overall market expansion. Consumers are increasingly shifting away from ownership due to challenges such as limited new-car availability and unpredictable used-car pricing. Instead, they are opting for flexible month-to-month access. Services like SIXT+ in London and Enterprise Travel Direct provide comprehensive offerings that include insurance, maintenance, and mileage within a single payment structure. Additionally, OEM captive programs are leveraging excess production by channeling it into these subscription models, which offer favorable financing terms. While this approach helps distribute inventory risk, it also exposes operators to potential fluctuations in residual values, particularly if manufacturers withdraw their support. Subscription customers typically demonstrate greater loyalty and higher lifetime value, thereby improving revenue stability for providers that can effectively manage the associated capital demands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| New-Car Supply Crunch | −0.5% | National | Short term (≤ 2 years) |

| Used-Car Price Swings | −0.4% | National | Medium term (2-4 years) |

| Patchy EV Charging | −0.3% | Rural England, Wales, Highlands, Northern Ireland | Medium term (2-4 years) |

| Strict VAT Rules | −0.2% | Northern Ireland, border regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tight New-car Supply Inflating Fleet Costs

New-car registrations in the United Kingdom have shown steady growth, with expectations of further increases in the near future [2]“UK New Car Registration Data 2025,”, Society of Motor Manufacturers and Traders, smmt.co.uk. Fleet and business volumes have experienced a notable increase, contributing to a tighter market supply. Although semiconductor shortages have improved, they continue to cause delays in delivery times, prompting rental companies to incur additional costs for securing allocations. Premium vehicle models are more readily available compared to high-volume economy cars, which benefits operators focused on airport locations. However, independent operators, who depend on low-margin turnover, face challenges due to this disparity. As vehicle fleets age, maintenance expenses increase, and customer satisfaction declines, which limits the ability to adjust pricing effectively.

Used-Car Price Volatility Depressing Residual Values

Average used-car prices have declined from their peak levels during the pandemic. However, the market continues to experience volatility due to increased auction volumes, primarily driven by the disposal of rental fleets. Battery-electric models experience significant depreciation in their initial year of use. This trend is attributed to rapid advancements in technology and ongoing concerns about driving range, which reduce demand in the second-hand market. Consequently, operators are cautious about accelerating the transition to electrification. They must balance the need to comply with regulatory mandates against the potential for reduced profit margins. Mid-sized firms, lacking access to advanced hedging mechanisms, remain particularly vulnerable to price fluctuations that could significantly impact their profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rental Duration – Subscriptions Gain Traction

Short-term hires dominated revenue, accounting for 73.30% in 2025, yet face slowing growth as cost-conscious travelers reduce discretionary trips. Long-term and subscription rentals, growing at a 12.67% CAGR, appeal to drivers who are delaying ownership while enjoying bundled insurance and maintenance. The United Kingdom car rental market size for subscriptions is projected to rise sharply from a modest base, driven by OEM financing that reduces operator capital expenditures. Subscription fleets feature newer cars with advanced driver-assistance systems that justify premium fees and enhance safety and compliance metrics for corporates. Operators split their asset pools accordingly, cycling high-mileage economy units through short-term channels and reserving late-model inventory for subscription customers to maximize residual values. Heightened capital intensity is offset by predictable monthly revenue and lower churn rates.

The preference shift reflects trends in structural mobility. Younger urban residents increasingly value on-demand access over ownership, and corporates use subscriptions to cover project-based assignments without expanding company fleets. The United Kingdom car rental market, therefore, benefits from dual demand drivers that mitigate volatility for operators. Providers continue to refine pricing algorithms to account for mileage variability and optional services, improving margin visibility across the subscription term. As OEMs expand direct-to-consumer pilots, rental companies leverage brand recognition and nationwide service footprints to maintain a competitive edge.

By Booking Type – Mobile Apps Reshape Channel Economics

Online reservations accounted for 67.50% of 2025 revenue and are advancing at a 10.81% CAGR, outpacing offline channels as consumers prioritize convenience and price comparison. Mobile apps capture the largest share of digital growth, driven by a 6.3% year-over-year increase in downloads. Same-day bookings compress fleet-planning windows, prompting deeper investment in real-time inventory management. The United Kingdom car rental market share captured by offline methods continues to decline, yet remains significant, particularly at airports and for corporate itineraries that require bespoke billing arrangements.

Aggregators help smaller firms gain exposure but erode pricing control, whereas global chains funnel loyalty members into proprietary apps to limit comparison shopping. Off-airport sites, backed by lower real estate costs, channel savings into dynamic price discounts that attract cost-sensitive leisure travelers. The United Kingdom car rental market size allocated to online channels is projected to exceed USD 1.50 billion by 2030, magnifying the strategic value of digital capabilities. Operators experiment with AI chatbots for guided reservations, though uptake lags visual interfaces where customers compare vehicle classes.

By Application – Business Rentals Outpace Leisure Growth

Leisure retained 55.70% revenue share in 2025, fueled by domestic tourism and international inbound traffic. However, business rentals are growing faster at a 9.63% CAGR, driven by duty-of-care compliance and rail network disruption. Employers view professionally managed fleets as essential for tracking mileage, emissions, and driver behavior. Rentals become cost-effective beyond 100 miles, a standard threshold for inter-city trips between London, Manchester, and Birmingham. Rail strikes reinforce this preference, reallocating travelers to road-based modes.

Leisure demand remains seasonally influential, peaking during July–August holiday periods. Cornwall, Snowdonia, and the Highlands attract staycationers who prefer multi-day hires, creating vehicle allocation challenges for operators. The United Kingdom car rental market benefits from diversified demand streams that mitigate cyclical risk. Customer segmentation enables tailored marketing: digital campaigns target leisure users with early-booking discounts, while account managers service corporate travel departments that schedule block reservations months in advance.

By Vehicle Class – Premium Segment Capitalizes on Airport Traffic

Economy cars dominated the market with a 58.90% share in 2025, catering to budget-minded travelers. Premium and luxury fleets, however, are growing at an 11.86% CAGR, driven by international arrivals at Heathrow, Gatwick, and Manchester airports, which collectively processed over 150 million passengers in 2024. Operators shift fleet mix toward higher-margin vehicles at major terminals, capitalizing on the willingness to pay among inbound tourists and executive travelers. Standard-class cars provide a middle ground, yet they face a margin squeeze between nimble economy rivals and aspirational premium offerings.

Airport infrastructure investments support this trend. Terminal upgrades at Manchester and Heathrow introduce dedicated rental facilities, accelerating pickup times and reinforcing premium customer expectations. The United Kingdom car rental market size for premium vehicles is forecast to nearly double by 2030, driven by OEM partnerships that supply high-spec models under favorable financing terms. Providers must balance inventory rotation to avoid residual-value shocks yet sustain availability for high-yield bookings.

By Propulsion Type – EV Mandate Drives Fastest Growth

Internal-combustion engines remained 81.10% of the 2025 fleet mix but are ceding ground to battery electrics, which are scaling at 26.60% CAGR. The United Kingdom car rental market faces the dual challenge of meeting the 2025 zero-emission quota while managing 20-30% first-year depreciation on EVs. Hybrid models bridge the transition, offering lower emissions without charging downtime. Infrastructure concentration in urban zones constrains the adoption of long-distance leisure, yet the rapid roll-out of chargers and government fleet commitments bolster long-term confidence.

OEM alliances help defray capital costs. SIXT’s Stellantis agreement incorporates telemetry that optimizes charging schedules and reduces downtime, enhancing utilization. Hertz’s earlier U.S. sell-down of EVs serves as a cautionary tale about repair costs and customer education. Operators in the United Kingdom car rental market deploy pilot programs to refine pricing, mileage caps, and charging-fee structures, building operational expertise ahead of stricter quotas.

By End-User – Individual Segment Dominates and Accelerates

Individuals generated a 69.30% revenue share in 2025 and are progressing at a 10.80% CAGR, driven by staycations, city breaks, and subscription uptake. Corporations grow more modestly yet deliver steady cash flow and upsell potential through telematics and reporting bundles. Individual renters exhibit higher price sensitivity and book heavily via apps, encouraging promotional pricing and loyalty-point incentives. Corporations negotiate volume discounts and favor central billing, allowing operators to forecast utilization more accurately.

The United Kingdom car rental market benefits from this dual-engine demand model. Operators tailor marketing spend: performance ads target consumers, whereas relationship managers engage travel-procurement teams. As duty-of-care rules tighten, corporates may shift additional volume to managed fleets, marginally reducing individual share yet stabilizing revenue diversity.

By Booking Channel – Off-Airport Gains Share

Off-airport locations held a 53.50% share in 2025 and are projected to rise at an 11.60% CAGR, aligning with the growth of domestic tourism and app-based proximity search. Airport counters remain pivotal for international visitors but face slowing growth relative to broader market expansion. Rental hubs near rail stations and city centers attract travelers continuing journeys after inter-city trains, especially during strike-affected periods. Lower facility costs permit off-airport operators to undercut terminal pricing, widening their appeal.

Operators reposition older vehicles to off-airport fleets while reserving late-model, premium cars for terminals, optimizing yield across channels. The United Kingdom car rental market share for airport channels is resilient but increasingly dependent on premium-focused segmentation. Continuous investment in shuttle-bus efficiency and digital check-in helps mitigate customer wait-time concerns that have historically disadvantaged off-site pickups.

Geography Analysis

England generated 74.80% of market value in 2025 and is set to grow at an 8.90% CAGR through 2031. London's status as a financial-services hub, coupled with its multiple international gateways and a dense motorway network, fuels a consistent demand for transportation services. Business travel spending in England constitutes a significant portion of the national total and drives weekday utilization. While coastal tourism in Cornwall and the South Coast boosts revenues during the summer months, the impending expansion of the congestion charge is pushing operators to hasten the deployment of low-emission fleets.

Scotland, Wales, and Northern Ireland collectively contribute a notable share to the market. Scotland takes the lead, thanks to the allure of self-drive tourism along the North Coast 500 and the burgeoning activity at Edinburgh and Glasgow airports. International visitors make a significant contribution to Scotland's tourism revenue. While Wales attracts tourists to Snowdonia and Pembrokeshire, its smaller population density limits overall revenue. Northern Ireland grapples with the challenge of VAT compliance on cross-border hires, prompting some providers to withdraw from those routes.

Fleet planning across the regions is a complex task. Operators need to schedule vehicles months ahead of peak seasons in the Highlands and coastal areas, all while ensuring acceptable utilization during the shoulder seasons. Disparities in public charging infrastructure hinder the rollout of electric vehicles in rural locales, allowing internal combustion cars to remain prevalent outside major urban centers. As a result, the UK car rental market showcases distinct geographic segmentation, both in terms of vehicle propulsion types and fleet allocation strategies.

Competitive Landscape

Global giants—Enterprise, Hertz, Avis Budget, SIXT, and Europcar—command a significant combined share, indicating a moderately concentrated market. Through a long-term partnership with Stellantis, SIXT ensures a steady supply of vehicles and advances its goals for electrification. Meanwhile, Hertz has achieved notable growth in its international operations, improving utilization rates and increasing daily revenue [3]“Q3 2025 Earnings Release,”, Hertz Global Holdings, hertz.com. However, Zipcar's exit from the market not only removed a costly competitor but also highlighted the challenges faced by asset-heavy sharing models in high-cost urban areas.

Private equity is increasingly showing interest in the market, as demonstrated by KKR's acquisition of Dawsongroup, which reflects the growing convergence between leasing and rental services. Platforms like Turo, through their partnership with Uber, are expanding their distribution networks and targeting a larger share of the price-sensitive leisure market. As technology becomes a critical differentiator, innovations such as dynamic pricing systems and telematics-based maintenance are helping industry leaders stand out. While the car rental market in the United Kingdom continues to benefit from economies of scale in procurement and residual value management, there remains significant potential in areas such as subscription-based models, rural service coverage, and electric vehicle charging infrastructure.

United Kingdom Car Rentals Industry Leaders

-

SIXT SE

-

Avis Budget Group

-

The Hertz Corporation

-

Europcar Mobility Group

-

Enterprise Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Lyft, a United States-based ride-hailing company, entered into a definitive agreement to acquire the taxi platform FREENOW for EUR 175 million (USD 199 million).

- April 2025: Europcar Expands Electric Fleet with Hyundai KONA, Enhancing Choices for Eco-Conscious Renters. The popular SUV offers drivers an extended range and rapid charging capabilities, providing customers with real-world experience in driving fully electric vehicles. Europcar has introduced the Hyundai KONA to its fleet for both business and leisure rentals, further broadening its selection of electric vehicles.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Kingdom car rental market as the revenue generated from short-term and subscription contracts (under twelve months) for passenger cars rented without a driver, whether booked online or offline and fulfilled at airport, rail, and downtown locations. This scope follows the segmentation shown in Mordor Intelligence's report for 2025 to 2030.

Exclusion note: operating leases exceeding twelve months, chauffeur-drive services, and light commercial van hire sit outside this assessment.

Segmentation Overview

-

By Rental Duration

- Short-Term (Less than 30 days)

- Long-Term/Subscription (More than 30 days)

-

By Booking Type

- Online

- Offline

-

By Application

- Leisure / Tourism

- Business / Corporate

-

By Vehicle Class

- Economy

- Standard

- Premium / Luxury

-

By Propulsion Type

- Internal-Combustion Engine (ICE)

- Hybrid

- Battery Electric Vehicle (BEV)

-

By End-User

- Individual

- Corporate and Institutional

-

By Booking Channel

- Airport

- Off-Airport / Downtown

- Rail and Mobility Hubs

-

By Geography

- England

- Scotland

- Wales

- Northern Ireland

Detailed Research Methodology and Data Validation

Primary Research

Interviews with airport concession managers, regional franchise owners, corporate travel buyers, and digital aggregator executives across England, Scotland, Wales, and Northern Ireland allowed us to verify seasonality curves, emerging EV subscription pricing, and average fleet turn cycles before we finalized assumptions.

Desk Research

We pieced together foundational demand signals from tier-1 public sources such as the Office for National Statistics tourism arrivals, Department for Transport licensed vehicle stocks, British Vehicle Rental & Leasing Association fleet bulletins, Civil Aviation Authority passenger flows, and Eurostat household mobility surveys. Company filings and investor decks from listed rental groups augmented pricing and utilization ratios, while D&B Hoovers offered snapshot financials of key operators. These references illustrate, not exhaust, the secondary pool that fed our baseline.

Market-Sizing and Forecasting

A top-down build starts with reconstructed spending pools derived from inbound tourist nights, domestic business trip counts, and average rental length; these are converted into transaction volumes and multiplied by blended daily rates. Supplier roll-ups for a sample of major brands acted as a bottom-up sense check. Key model levers include fleet utilization, new vehicle registration trends, corporate penetration of subscription products, EV share targets, and airport passenger growth. Forecasts are produced with ARIMA complemented by scenario analysis, the preferred approach cited by primary experts to balance pandemic echoes with regulatory EV mandates. Gaps in bottom-up data are bridged by channel-specific utilization proxies and verified against survey feedback.

Data Validation and Update Cycle

Our analysts run variance and anomaly screens, compare outputs with independent cost and fleet metrics, and escalate discrepancies for peer review. The model refreshes annually, with interim revisions triggered by material events such as duty-free policy changes or large fleet acquisitions; a last-mile check is completed before report delivery.

Why Mordor's United Kingdom Car Rental Baseline is dependable

Published estimates often vary because providers pick different service mixes, contract horizons, and refresh cadences.

Key gap drivers center on scope breadth (some firms fold in long-term leasing), currency treatment, and whether airport and peer-to-peer channels are modeled separately or pooled into one revenue line, which can inflate totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.97 B (2025) | Mordor Intelligence | - |

| USD 7.27 B (2024) | Global Consultancy A | Includes long-term leases and chauffeur services; single blended ASP applied nationally |

| USD 7.15 B (2024) | Regional Consultancy B | Uses airport-driven volume extrapolated to all channels; limited validation of subscription discounts |

These contrasts show that Mordor's disciplined scope, variable-level cross-checks, and annual refresh give decision-makers a balanced, transparent baseline anchored to traceable inputs rather than broad generalizations.

Key Questions Answered in the Report

What growth rate is expected for the United Kingdom car rental market through 2031?

The market is projected to expand at a 3.11% CAGR, rising from USD 2 billion in 2026 to USD 2.33 billion by 2031.

Which rental segment is growing fastest in the country?

Long-term and subscription rentals are advancing at a 12.67% CAGR, outpacing all other duration categories.

How large is online booking’s role in United Kingdom car rentals?

Online channels accounted for 67.50% of 2025 revenue and are expanding at a 10.81% CAGR as mobile apps dominate new demand.

What share of rental fleets are battery electric vehicles?

Battery electric units comprised a small share of fleets in 2025, yet they are scaling at a 26.60% CAGR under zero-emission sales mandates.

Page last updated on: