Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

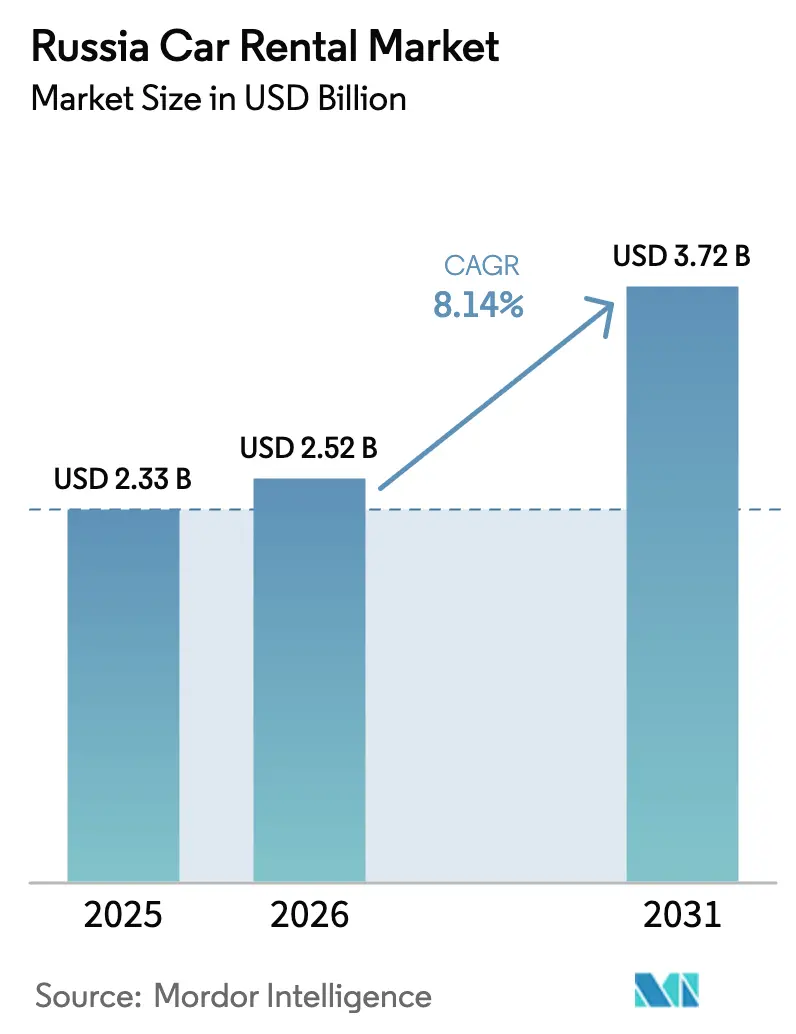

| Base Year Market Size (2025) | USD 2.33 Billion |

| Market Size (2026) | USD 2.52 Billion |

| Market Size (2031) | USD 3.72 Billion |

| Growth Rate (2026 - 2031) | 8.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Car Rental Market Analysis by Mordor Intelligence

The Russia car rental market size is expected to grow from USD 2.33 billion in 2025 to USD 2.52 billion in 2026 and is forecast to reach USD 3.72 billion by 2031 at 8.14% CAGR over 2026-2031. The Russia car rental market size thus reflects a sizeable opportunity that keeps expanding despite lingering supply-chain pressures. Domestic tourism’s 25% rebound in 2024, a 47% jump in new-car registrations, and a swift post-sanctions shift toward Chinese vehicle imports are the three trends that most clearly shape the competitive field[1]“Domestic Tourism Statistics 2024,” Russian Ministry of Economic Development, economy.gov.ru. Operators are adding vehicles quickly, leaning on the record 1.57 million cars sold in 2024 to replenish fleets and accelerating used-vehicle disposal programs to recycle capital[2]“Automobile Sales Report 2024,” Association of European Businesses Russia, aebrus.ru. Digital ecosystems are displacing physical counters: online channels already capture nearly two-thirds of bookings, and free-floating car-sharing has broken through the one-third threshold of total transactions, confirming that Russian consumers now prioritise flexibility, mobile access, and transparent pricing over conventional rental rituals.

Key Report Takeaways

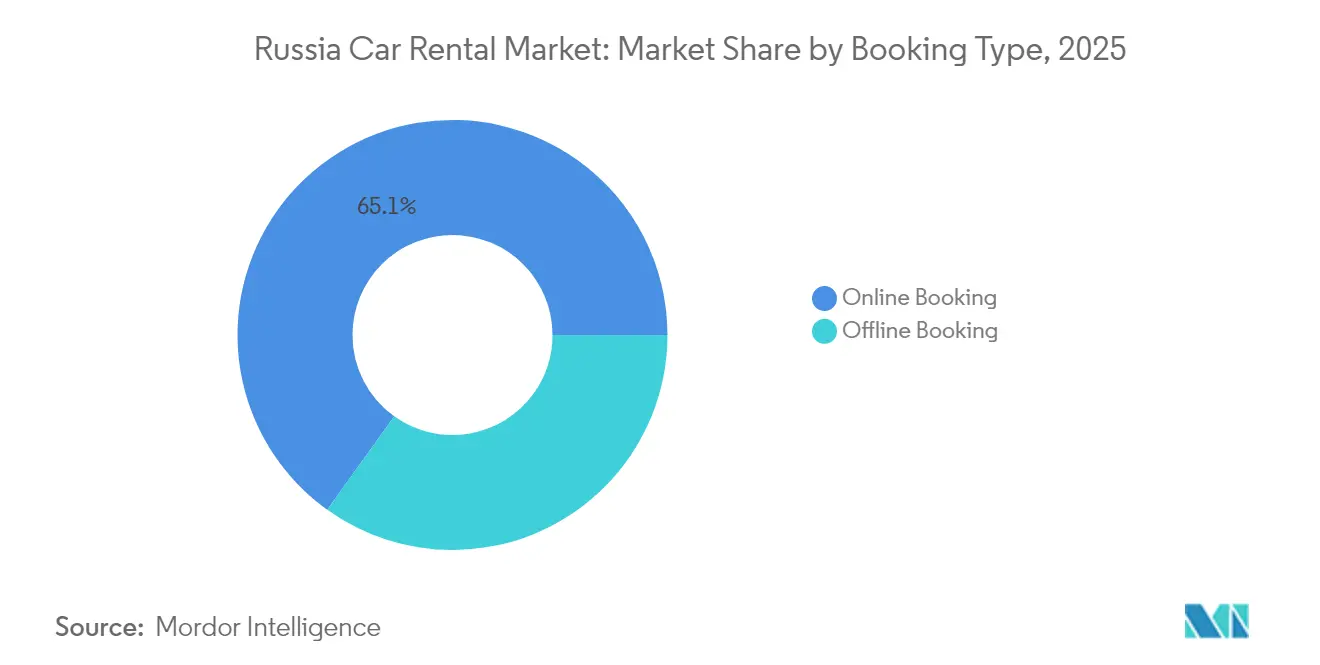

- By booking type, online channels captured 65.10% Russia car rental market share in 2025; offline demand is expected to trail at a 7.41% CAGR.

- By service model, free-floating car-sharing held 36.10% revenue share in 2025; subscription and long-term lease solutions are forecast to expand at a 7.62% CAGR to 2031.

- By vehicle type, sedans accounted for 39.25% of the Russia car rental market size in 2025, yet SUVs are on track for a 9.10% CAGR.

- By rental duration, daily rentals represented 46.05% revenue in 2025; weekly rentals should accelerate at an 8.39% CAGR through 2031.

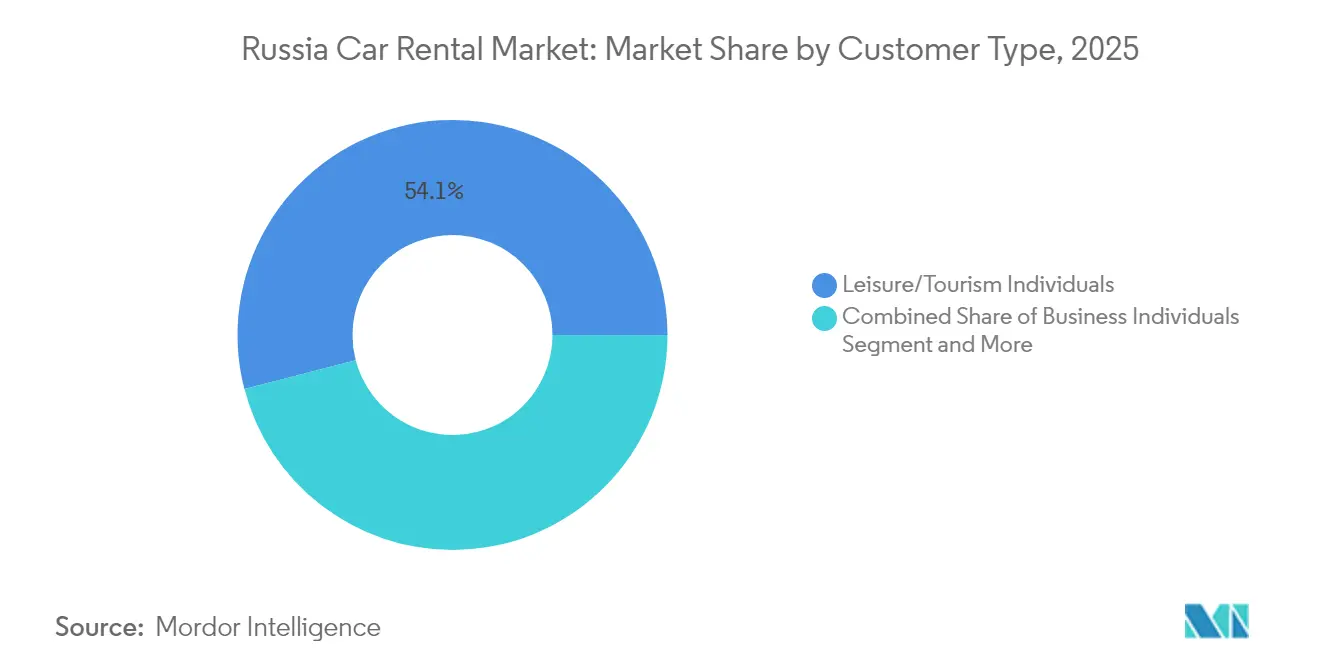

- By customer group, leisure/tourism users retained 54.05% share in 2025 whereas ride-hailing drivers are expected to post a 7.64% CAGR to 2031.

- By propulsion type, the internal combustion engine accounts for 76.25% market share in the Russia car rental market in 2025, however, electric vehicles are anticipated to grow with a CAGR of 8.73% by 2031.

- By geography, the Central Federal District led with 34.05% of the Russia car rental market share in 2025, while the Far Eastern Federal District is projected to grow fastest at 7.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Russia Car Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Domestic Tourism Rebound Boosts Leisure Demand | +2.1% | National; early gains in Central, Southern, North Caucasus districts | Short term (≤ 2 years) |

| Rapid Fleet Expansion of Moscow and St Petersburg Car-Sharing | +1.8% | Central and Northwestern districts; spill-over to Volga | Medium term (2-4 years) |

| Mobile Booking and Digital Payment Penetration | +1.4% | Major cities nationwide | Medium term (2-4 years) |

| Corporate Demand for Regional Business Travel | +1.2% | Central, Volga, Ural districts | Long term (≥ 4 years) |

| Government Tax Breaks for EV/CNG Rental Fleets | +0.9% | National | Long term (≥ 4 years) |

| Fleet Resale Platforms Unlocking Residual Value | +0.7% | Large metropolitan areas | Short term (≤ 2 years |

| Source: Mordor Intelligence | |||

Domestic Tourism Rebound Boosts Leisure Demand

Leisure customers captured 54.43% of the Russia car rental market in 2024 after a 25% jump in domestic trips redirected spend from international holidays to home-market destinations[3]“Domestic Trip Metrics 2024,” Federal Agency for Tourism, tourism.gov.ru. More than half of the 153 million domestic journeys logged in 2024 were undertaken by car, embedding self-drive habits that now stretch average booking windows to three or four months and favour longer-duration contracts. Rental firms have reacted by rebalancing fleets toward economical sedans and hatchbacks and by introducing kilometre-cap packages tailored to multi-city itineraries.

Rapid Fleet Expansion of Moscow and St Petersburg Car-Sharing

Moscow’s 30,000-vehicle free-floating fleet has become a global benchmark that proved the economic viability of short-duration access in a market long dominated by ownership. Operators deploy algorithm-driven pricing, predictive maintenance, and granular utilisation dashboards to maximise average revenue per vehicle hour. St Petersburg’s replication of Moscow’s template underpins a broader roll-out across Volga urban clusters where Delimobil and Yandex Drive are entering tier-two cities at lower customer-acquisition costs thanks to ready user familiarity. Intercity products now link Moscow with St Petersburg, Tula, and Kazan, generating 70% growth in cross-city bookings during 2024 and demonstrating that free-floating models can move beyond intracity confines

Mobile Booking and Digital Payment Penetration

Digital channels owned 65.72% of bookings in 2024, a milestone largely attributable to app-based ecosystems that merge car rental, ride-hailing, and micro-mobility. Yandex Drive’s seamless hand-off to Yandex Taxi gives drivers economical vehicle access while broadening rental companies’ addressable base without extra marketing spend[4]“Yandex Drive 2024 Mobility Report,” Yandex, yandex.com. Machine-learning price engines adjust minute-by-minute to match supply with micro-clusters of demand, lowering idle time and smoothing revenue swings. Embedded wallets further compress friction, and the same data pipes feed personalised offers that raise retention rates for the Russia car rental market.

Corporate Demand for Regional Business Travel

Regional corporate expansion and hub-and-spoke workforce policies push big employers to shun owned fleets in favour of scalable rental accounts. Firms cite a desire to keep balance-sheet assets lean and to avoid residual-value risk in a market dominated by imported spares. These multi-city arrangements also require uniform vehicle quality, prompting operators to standardise trim levels and to roll out centralised customer-service hubs capable of issuing one-click extensions and consolidated invoices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import-Driven Vehicle Supply Crunch Post-Sanctions | -1.9% | Nationwide; most severe in premium tiers | Medium term (2-4 years) |

| Rising Fuel, Parts, and Insurance Costs | -1.4% | Nationwide; regional fuel price dispersion | Short term (≤ 2 years) |

| Parking and Licensing Rule Volatility | -0.8% | Moscow, St Petersburg core | Medium term (2-4 years) |

| High Vandalism and Theft Rates Inflating Premiums | -0.6% | High-density metros | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Import-driven Vehicle Supply Crunch Post-Sanctions

Chinese brands command more than half of new-car registrations, which forces rental buyers to weigh untested residual values, sparser service footprints, and fluctuating parts pipelines. This foreshadows a localised oversupply that might depress rental yields yet still leave premium-class fleets short as European marques remain scarce. Operators must navigate this imbalance by recalibrating category mix and renegotiating bulk discounts with up-and-coming Chinese OEMs.

Rising Fuel, Parts, and Insurance Costs

The Russia car rental market contends with triple-barrel cost inflation: petrol price volatility, parts price leaps, and insurer recalculations that pad premiums for lightly de-risked Chinese models. Delivery lead times for critical spares have stretched to 7–12 days, compelling companies to hold larger on-hand inventories or face utilisation losses. Insurers, meanwhile, are raising base rates because historical loss data on newer brands remains sparse. The pressures shave margins and motivate consolidation among under-capitalised firms unable to recoup outlays through dynamic pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Booking Type: Digital dominance accelerates

Online reservations controlled 65.10% of the Russia car rental market in 2025, underscoring the structural tilt toward app-centric engagement. Offline desks still serve complex corporate itineraries and older users, yet the human-touch niche is narrowing as AI-driven chat interfaces mimic agent advice. Operators embed loyalty points, digital KYC, and one-tap extensions, features that collectively nudge mobile adoption. Offline’s 7.41% CAGR centres on airports and luxury tiers where face-to-face exchanges remain integral.

Offline resilience also owes much to legacy corporate agreements that require wet-ink signatures for insurance riders. Nevertheless, even state-owned enterprises increasingly pilot mobile pre-check-in programs that promise shorter key handover times. As connectivity expands to secondary cities, rural tourists lean on e-vouchers for pick-ups at remote depots, eating into the last bastions of paper-driven workflows.

By Service Model: Car-sharing reshapes traditional rental

Free-floating options claimed a 36.10% share of the Russia car rental market in 2025 by offering per-minute rates and no return-to-origin conditions. Subscription plans, registering a 7.62% CAGR, tap households wanting cost predictability and businesses seeking flexible fleet allowances. Counter-based contracts retain loyalists needing cross-border travel coverage or specialised add-ons such as snow tyres and child seats. Station-based schemes continue to prosper in gated campuses, business parks, and resort complexes where vehicle docks guarantee availability.

Service-model convergence is accelerating: Leading apps now allow customers to toggle between 30-minute bursts, daily caps, or multi-month subscriptions within a single interface. In turn, fleet-planning software optimises the mix per neighbourhood by feeding anonymised usage data into dispatch algorithms so that sedan clusters where airport runs dominate. At the same time, vans fill dormitory-town drop-zones at weekends.

By Vehicle Type: Sedan leadership faces EV disruption

Sedans contributed 39.25% of 2025 invoicing due to their fuel efficiency and boot space balance. Hatchbacks thrive inside high-density cores with tight parking, while SUVs gain share in regions prone to harsh winters or unpaved tourism routes. EVs win on energy cost per kilometre and, under new tax credits, are up to 12% cheaper to insure, leading to expand SUVs with 9.10% CAGR by 2031.

Operators installing 40 kW fast chargers at depots can now rotate an EV back into circulation within 40 minutes—a breakthrough that shrinks downtime. Meanwhile, nascent residual-value curves for Chinese EVs remain volatile, pushing firms to hedge by keeping holding periods short or partnering directly with manufacturers for buy-back guarantees that ring-fence depreciation risk.

By Rental Duration: Daily rentals lead amid weekly growth

Daily hires represented 46.05% share of the Russia car rental market in 2025, yet weekly contracts post the fastest trajectory as domestic holidaymakers stretch their trips. The Russian car rental market share linked to weekly bookings is expected to grow with a CAGR of 8.39% by 2031. Hourly micro-rentals flourish in CBD zones where residents borrow wheels for errands, and monthly packages cater to on-assignment managers who wish to avoid multi-year leases.

Operators increasingly treat rental duration as a separate price segment. AI tools that analyse historic drive paths can now auto-suggest switching from daily to weekly rates once mileage passes threshold levels, improving customer satisfaction while keeping utilisation predictable.

By Customer Type: Leisure dominance amid ride-hailing growth

Leisure travellers commanded 54.05% share of the Russia car rental market in 2025 after Russia’s tourism authority reported that over half of trips were executed by private car. Ride-hailing contractors, the quickest climber at 7.64% CAGR, form a new semi-professional segment whose bookings peak during nighttime hours and call for specific maintenance cycles. Corporate itinerants and permanent fleets still anchor weekday demand, especially on trunk corridors that connect regional head offices.

Gig-economy tie-ins give renters more guaranteed utilisation hours, making them popular during shoulder seasons when tourist flows ebb. Yandex Drive’s hybrid subscription for taxi drivers guarantees off-peak rentals at a capped day rate, creating a floor for asset usage statistics critical to fleet financiers’ lending covenants.

By Propulsion Type: ICE dominance faces electric transition

ICE-petrol cars still captured 76.25% of invoices in 2025. Yet operators are layering hybrids into city fleets to hedge against pump-price volatility. The Russia car rental market size stemming from battery electric models is still small. Still, it grows at 8.73% CAGR, nudged by subsidies that slash acquisition tax to zero and by grid-connected depots where overnight charging pairs with lower off-peak electricity tariffs. Diesel, CNG, and LPG options orbit niche terrain—long-haul logistics shifts or corporate eco-targets—each bearing distinct refuelling infrastructure bottlenecks.

Customers increasingly request a ‘green upgrade’ at the booking step if provided with transparent charging maps and guaranteed roaming interoperability across slabs of the federal highway network. Fleet owners answer by negotiating aggregate electricity tariffs and training technicians to handle high-voltage powertrains, which compresses long-term upkeep outlays.

Geography Analysis

The Central Federal District retained 34.05% of the Russia car rental market share in 2025, underpinned by Moscow’s 30,000-vehicle free-floating fleet and the concentration of corporate headquarters that keep utilisation high. St Petersburg’s inclusion in intercity car-sharing corridors lifted the Northwestern Federal District’s bookings, while the Volga Federal District is quickly becoming the third pillar of demand as Kazan and Samara adopt the Moscow playbook for smart-mobility roll-outs. These three areas together anchor more than half of the Russia car rental market size and provide operators with dense trip clusters, reliable charging access, and advanced road infrastructure that moderate operating costs.

Driving behaviour shifts markedly further south. Average annual mileage peaks at 16,200 km in the North Caucasus and 15,400 km in the Southern Federal District, a pattern tied to milder weather that supports year-round touring and to coastal resort traffic that surges in summer. Fleet managers redeploy surplus vehicles from central depots to meet seasonal spikes, then reposition SUVs to mountain regions for winter sports, using telematics to limit empty return trips. Higher utilisation allows operators in these districts to tolerate bigger fuel and maintenance budgets while still achieving above-average yield per kilometre.

The Ural and Siberian districts rely on business hires linked to mining, metallurgy, and energy, creating steady weekday demand for 4×4 units equipped for sub-zero conditions. Summer tourism to Lake Baikal and the Altai mountains complements that corporate base, though harsh winters necessitate heavier maintenance regimes that push rental pricing upward. The Far Eastern Federal District, despite the nation’s lowest mileage at 13,100 km, is forecast to expand at a 7.28% CAGR as new highways cut travel times and tax incentives attract Asia-oriented commerce economy.gov.ru. Together these frontier regions represent the next growth frontier, provided operators calibrate fleet mixes to local climate, road quality, and evolving customer expectations.

Competitive Landscape

The Russia car rental market operates as a tight duopoly in which Yandex Drive and Delimobil set fleet benchmarks, pricing corridors, and technology cadence for the wider sector. Their scale secures preferential purchase terms from importers and insurers, giving each company cost cushions that smaller rivals lack. Mobile platforms owned by the two leaders now blend car-sharing, ride-hailing, and digital wallets into one interface, making multi-modal travel almost frictionless for end users. Network effects reinforce the advantage: a larger fleet produces shorter wait times, which lifts customer retention and, in turn, justifies further fleet additions. Capital intensity and data-science expertise create formidable entry barriers for new aspirants.

Strategic focus has shifted toward vertical integration and data exploitation. Yandex Drive mines real-time telematics to reposition idle vehicles minutes before demand spikes, while Delimobil’s predictive-maintenance module cuts unscheduled downtime by 18% in 2024. The February 2024 Delimobil IPO, which raised RUB 4.2 billion, provided the funding needed for fleet renewal and geographic rollout while signalling institutional confidence in asset-heavy mobility platforms. Each leader is also pursuing residual-value capture by expanding in-house used-car outlets that quickly dispose of high-mileage units and at higher margins than wholesale auctions. Such moves strengthen cash flow and shield operating margins from parts-price inflation.

Competition now concentrates in specialist pockets rather than in head-to-head national scale. Premium chauffeur services for diplomatic clients, campus-based station rentals, and adventure SUV fleets in resort areas present room for differentiated entrants. Mid-tier operators short on technology and capital increasingly form franchise alliances or accept buyouts, accelerating consolidation. Supply-chain volatility further pressures smaller firms because bulk-buy discounts on Chinese spare parts accrue mostly to the two dominant players. Collectively, these dynamics keep market concentration high and leave Yandex Drive and Delimobil firmly in command of future growth trajectories.

Russia Car Rental Industry Leaders

Delimobil

Yandex Drive

BelkaCar

Citydrive

Rentmotors

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: Delimobil aims to raise used-vehicle disposals to as many as 5,000 units, opening new Kupimobil showrooms in Moscow and St Petersburg.

- February 2024: Delimobil completed Russia’s first car-sharing IPO, securing RUB 4.2 billion in funding.

Russia Car Rental Market Report Scope

Car rental services allow users to hire a car for a certain period of time generally for a few hours to a few weeks. The car rental service allows users to book a car through the internet or mobile application.

Russia Car Rental Service is segmented by booking type, application, rental length, and car type. Based on the booking type, the market is segmented into Online Booking and Offline Booking. Based on the Application, the market is segmented into Leisure/Tourism and Business.

Based on the Rental Length, the market is segmented into Short Term and Long Term. Based on the car type, the market is segmented into Hatchback, Sedan, and Utility Vehicle. For each segment, market sizing and forecast have been done on the basis of value (USD Billion).

By Booking Type

| Online Booking |

| Offline Booking |

By Service Model

| Traditional Counter Rental |

| Free-Floating Car-Sharing |

| Station-Based Car-Sharing |

| Subscription / Long-Term Lease |

By Vehicle Type

| Hatchback |

| Sedan |

| SUV |

| Van / MPV |

By Rental Duration

| Hourly |

| Daily |

| Weekly |

| Monthly / Long-Term |

By Customer Type

| Leisure / Tourism Individuals |

| Business Individuals |

| Corporate Fleets |

| Ride-hailing / TNC Drivers |

By Propulsion Type

| Internal Combustion Engine (ICE) |

| Electric Vehicle |

| Hybrid |

By Region

| Central Federal District |

| Northwestern |

| Volga |

| Ural |

| Siberian |

| Southern |

| Far Eastern |

| By Booking Type | Online Booking |

| Offline Booking | |

| By Service Model | Traditional Counter Rental |

| Free-Floating Car-Sharing | |

| Station-Based Car-Sharing | |

| Subscription / Long-Term Lease | |

| By Vehicle Type | Hatchback |

| Sedan | |

| SUV | |

| Van / MPV | |

| By Rental Duration | Hourly |

| Daily | |

| Weekly | |

| Monthly / Long-Term | |

| By Customer Type | Leisure / Tourism Individuals |

| Business Individuals | |

| Corporate Fleets | |

| Ride-hailing / TNC Drivers | |

| By Propulsion Type | Internal Combustion Engine (ICE) |

| Electric Vehicle | |

| Hybrid | |

| By Region | Central Federal District |

| Northwestern | |

| Volga | |

| Ural | |

| Siberian | |

| Southern | |

| Far Eastern |

Key Questions Answered in the Report

How large is the Russia car rental market in 2026?

The market is valued at USD 2.52 billion in 2026 and is on track to reach USD 3.72 billion by 2031.

Which booking channel is most popular in Russian car rentals?

Online platforms dominate with 65.10% of transactions, reflecting the sector’s rapid digital shift.

Who are the major players in Russian car sharing?

Yandex Drive and Delimobil control most of the free-floating fleet, together setting technology and pricing standards.

Which propulsion segment is expanding the fastest?

Electric vehicles are growing at a 8.73% CAGR, benefitting from tax incentives and lower running costs.

How is cost inflation affecting rental operators?

Parts prices rose 7-12% and insurance premiums climbed, prompting fleet managers to shorten holding cycles and raise dynamic rates.

Page last updated on: