HCM Software In Manufacturing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

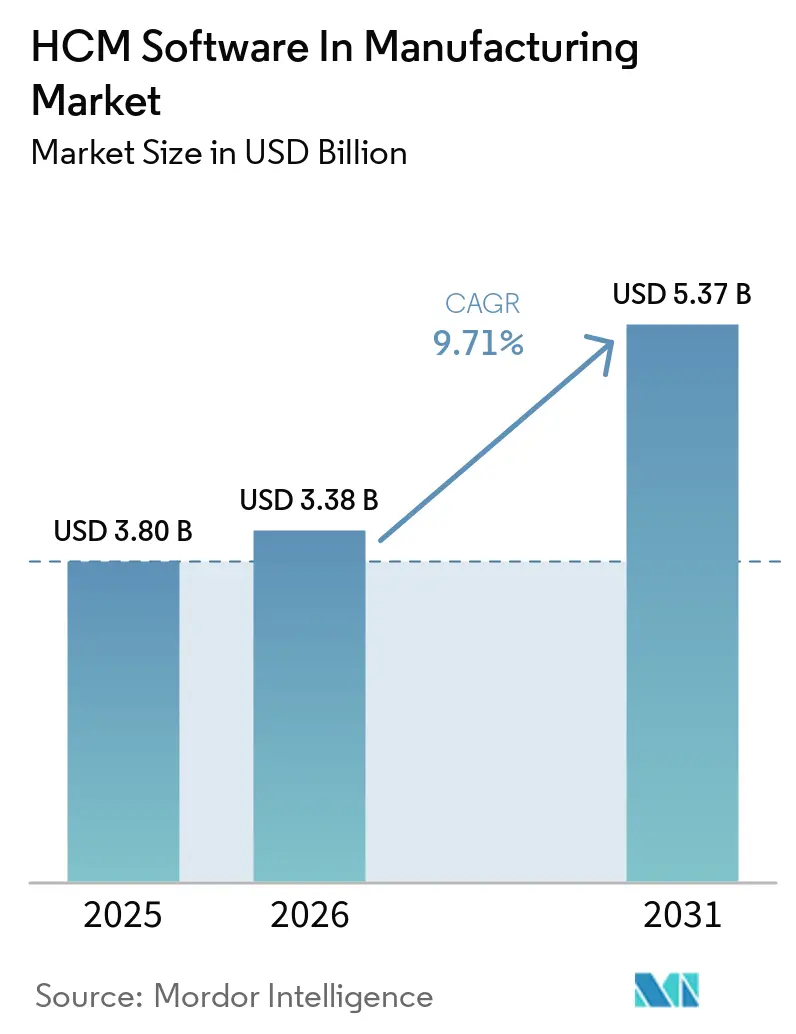

| Market Size (2026) | USD 3.38 Billion |

| Market Size (2031) | USD 5.37 Billion |

| Growth Rate (2026 - 2031) | 9.71% CAGR |

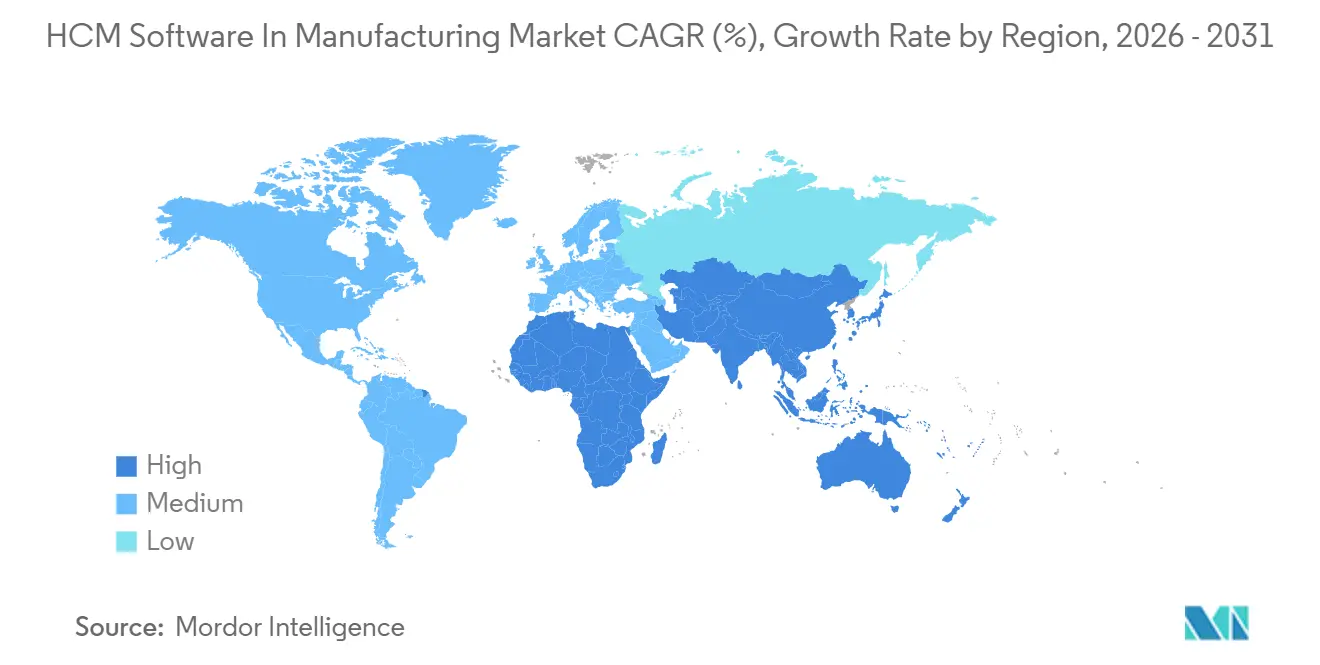

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HCM Software In Manufacturing Market Analysis by Mordor Intelligence

The HCM Software in Manufacturing Market is expected to increase from USD 3.08 billion in 2025 to USD 3.38 billion in 2026 and reach USD 5.37 billion by 2031, growing at a CAGR of 9.71% over 2026-2031. Cloud-first procurement now dominates vendor short-lists, yet persistent data-residency mandates keep nearly one-half of installed systems on-premises. Analytics modules that translate real-time production data into labor decisions are shifting buyer priorities away from payroll point solutions toward predictive platforms. Edge computing tie-ins are emerging as a competitive differentiator because they let manufacturers rebalance shifts instantly when IoT sensors flag equipment downtime. At the same time, labor shortages in North America, Europe, and Japan are pushing HR leaders to treat HCM as a production-planning tool to secure scarce skills before capacity bottlenecks emerge.

Key Report Takeaways

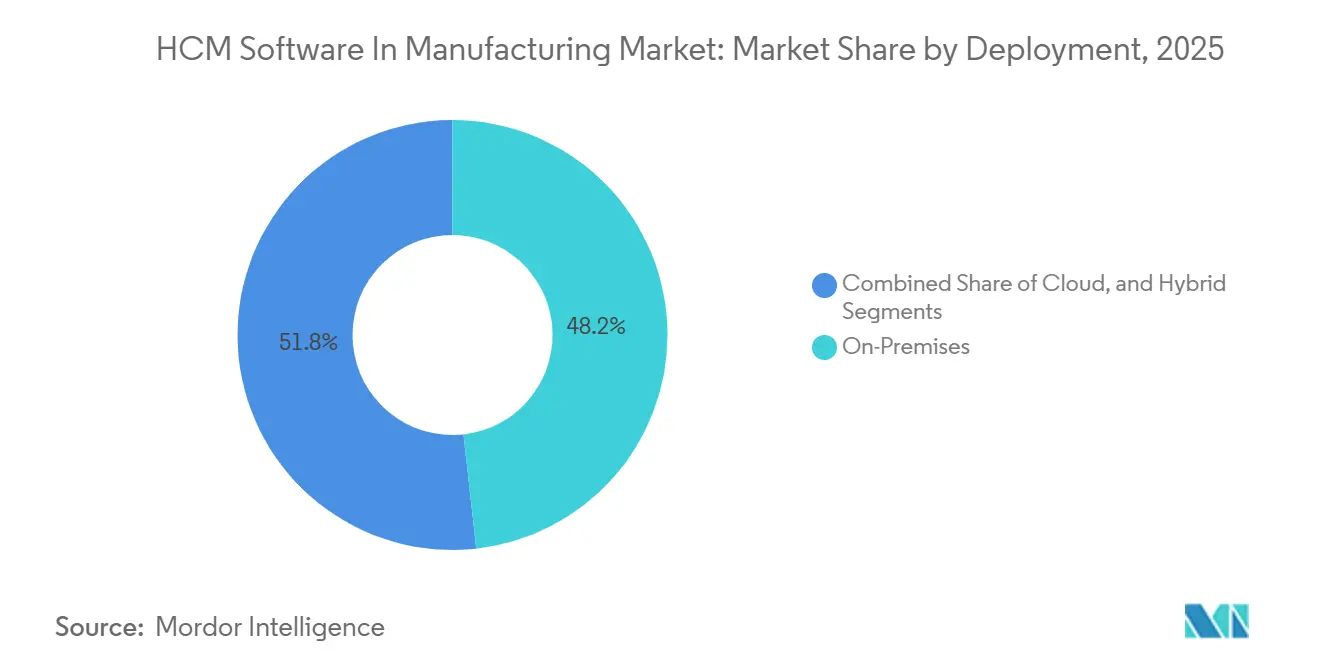

- By deployment, on-premises held 48.23% of the HCM software market share in manufacturing in 2025, while cloud is forecast to expand at a 10.43% CAGR through 2031.

- By organization size, large enterprises accounted for 63.12% of 2025 revenue; small and medium-sized enterprises are projected to grow at a 11.35% CAGR through 2031.

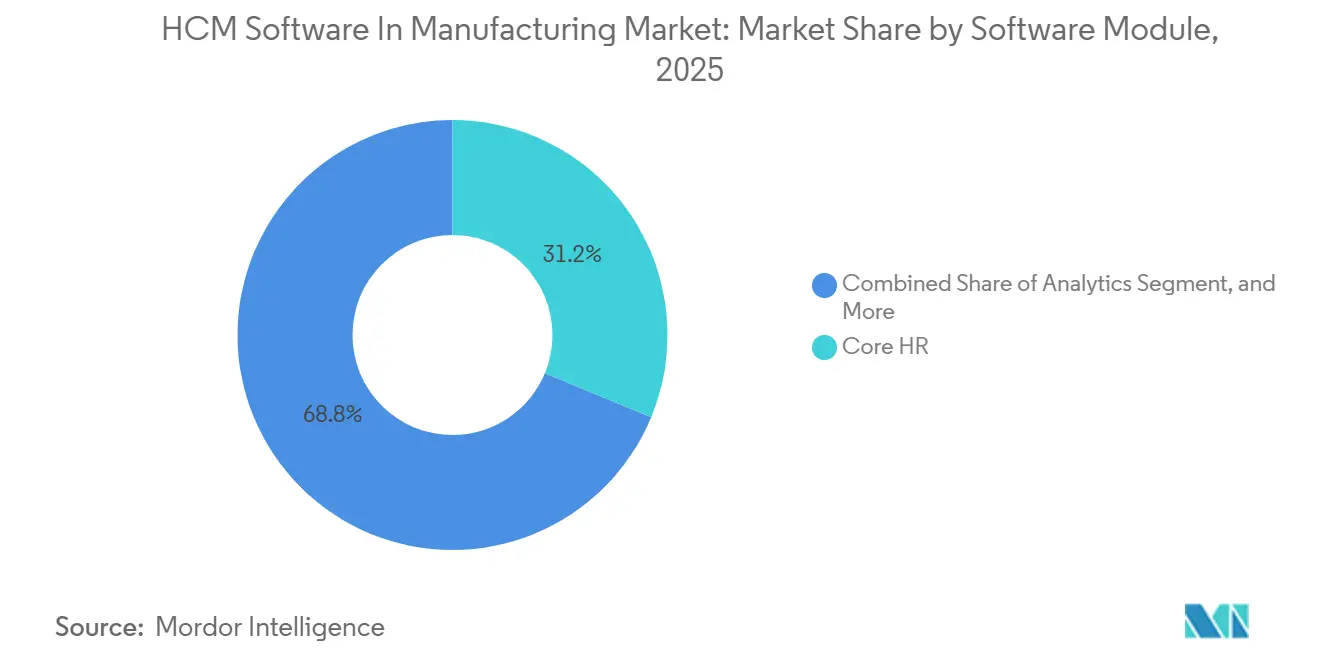

- By software module, core HR accounted for 31.24% of the 2025 HCM software market in manufacturing, whereas analytics is advancing at a 12.82% CAGR between 2026 and 2031.

- By manufacturing sub-industry, automotive led with a 27.83% revenue share in 2025, yet electronics is the fastest riser at a 10.93% CAGR through 2031.

- North America captured 34.19% of 2025 revenue, while Asia-Pacific is expected to post an 11.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HCM Software In Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-First Manufacturing HR Transformations | +2.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| AI-Driven Predictive Workforce Analytics Adoption | +2.3% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Labor Shortages Accelerating Digital Workforce Planning | +1.9% | Global, acute in North America, Europe, Japan | Short term (≤ 2 years) |

| Compliance Complexity in Multisite Manufacturing | +1.2% | Global, heightened in Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| Edge Computing and IoT Integration with HCM Platforms | +0.8% | Asia-Pacific, North America | Long term (≥ 4 years) |

| Shift-Based Employee Experience Imperatives | +0.7% | Global, notable in automotive, electronics, food and beverage | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud-First Manufacturing HR Transformations

Cloud deployments represented 52% of new contracts in 2025, up from 38% two years earlier. Manufacturers cite quarterly feature drops that embed regulatory updates and machine-learning enhancements as the primary driver. Hybrid models gained favor because they keep payroll data on-site while pushing talent and analytics workloads into vendor-managed clouds.[1] Oracle Corporation, “Oracle Fusion Cloud HCM for Manufacturing,” oracle.com Automotive tier-1 suppliers moved fastest, synchronizing labor requirements across global plants with SaaS suites. European plants faced additional latency after providers opened regional data centers to comply with GDPR rules, yet accepted the trade-off to remain compliant.

AI-Driven Predictive Workforce Analytics Adoption

Predictive attrition engines entered production at 38% of large manufacturers in 2025, flagging at-risk employees 90 days before resignation. Input signals now range from shift attendance to collaboration metrics, which together cut unplanned turnover in several electronics factories by more than one-fifth. Aerospace firms run similar models to spot skill obsolescence as additive manufacturing scales, then trigger retraining paths rather than external hiring. Reported gains include up to 28% shorter time-to-fill and noticeable first-year retention improvements.

Labor Shortages Accelerating Digital Workforce Planning

Vacancy rates hit 623,000 unfilled U.S. production positions in December 2025, while Germany posted 3.2% openings in the same month. To protect throughput, manufacturers adopted skills ontologies that map every worker’s micro-competencies and recommend lateral moves when engine lines convert to electrified platforms. Food and beverage plants in Southeast Asia used the same scheduling logic to curb seasonal temp-staff spending by nearly one-third. Organizations that overlay HCM intelligence onto MES data report quicker shift rebalancing and higher plant uptime.

Compliance Complexity in Multisite Manufacturing

The January 2025 EU Platform Work Directive pulled gig workers into full benefit coverage, forcing HCM suites to auto-classify contingent labor and launch compliance workflows. OSHA’s revised U.S. recordkeeping rules broadened injury definitions to cover mental health incidents, prompting real-time incident capture in workforce apps. China raised social-insurance ceilings in mid-2025, compelling immediate payroll recalibration. Aerospace primes also added clearance-aware permission controls to ensure compliance with ITAR requirements. Together, these changes lengthen deployment cycles but fortify demand for configurable rule engines.[2]Occupational Safety and Health Administration, “Improved Recordkeeping Requirements,” osha.gov

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy System Integration Challenges | -1.4% | Global, most visible in North America and Europe | Short term (≤ 2 years) |

| Data Security and Privacy Constraints | -1.1% | Europe, North America, Asia-Pacific | Medium term (2-4 years) |

| Change Management Resistance on Factory Floors | -0.6% | Global, traditional regions | Short term (≤ 2 years) |

| Budgetary Pressures in Mid-Sized Manufacturers | -0.5% | South America, Middle East, Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Legacy System Integration Challenges

Roughly one-third of scheduled go-lives slipped in 2025 because custom middleware costs outstripped budgets by up to 60%. Automotive plants running SAP ECC struggled to align S/4HANA upgrades with cloud HCM pilots, causing payroll mismatches that risked compliance penalties. Food processors tethered to proprietary MES had to manually reconcile schedules between production and HR, delaying efficiency gains for nearly two years. Vendors shipping pre-built connectors now have a clear edge in brownfield engagements.[3] SAP SE, “SuccessFactors Manufacturing Industry Brief,” sap.com

Data Security and Privacy Constraints

GDPR, CCPA, and China’s PIPL collectively raised compliance spend by as much as 18% of total HCM ownership costs. European plants require encryption at rest and strict role-based access controls, while U.S. counterparts must process data-subject requests within 45 days. Defense contractors restrict hosting to FedRAMP-authorized environments, shrinking the approved vendor list. Cross-border retention conflicts mean systems must auto-archive or delete records based on worker location, increasing configuration complexity.[4]European Commission, “Platform Work Directive Overview,” europa.eu

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Hybrid Architectures Gain Traction

On-premises deployments held 48.23% of the HCM software market share in manufacturing in 2025, standing as the default option for plants bound by data sovereignty mandates. Cloud contracts, however, are projected to climb at a 10.43% CAGR through 2031. The HCM software market in manufacturing is growing as organizations keep payroll engines behind the firewall while shifting analytics and talent to the cloud for continuous feature delivery. In automotive, 61% of tier-1 suppliers already rely on cloud modules to align staffing with interconnected assembly lines. Aerospace lags because multi-tenant hosting often conflicts with export-control regulations, yet selective lift-and-shift moves are underway.

Hybrid uptake accelerated where vendors introduced connectors that cut middleware spend by up to 40%, making previously rigid MES integrations feasible. Food and beverage producers still cling to full-on-premises estates, but 43% now have board approval for a phased hybrid migration by 2027. Electronics greenfield sites in Taiwan and Vietnam bypassed legacy hurdles altogether, recording 22% faster new-hire productivity thanks to mobile onboarding. Decision criteria have shifted from total cost toward regulatory posture, integration readiness, and appetite for vendor-run infrastructure.

By Organization Size: SMEs Embrace Modular SaaS

Large enterprises captured 63.12% of 2025 revenue, wielding scale to negotiate enterprise-wide license bundles that stitch together HR, payroll, workforce management, and analytics. In contrast, small and medium-sized manufacturers are set to post an 11.35% CAGR to 2031 as pay-as-you-go pricing lowers entry barriers. The HCM software market in manufacturing is growing among SMEs as vendors now sell best-of-breed modules that eliminate the need to purchase full suites. Sub-USD 5-per-employee monthly plans resonate with mid-tier electronics firms in India and Indonesia.

Large automotive OEMs manage headcounts above 50,000 across 20-plus countries and therefore prize single-stack suites that guarantee multi-currency payroll and multilingual interfaces. Yet even some conglomerates are consolidating from seven-point tools to one or two core platforms to curb integration debt. SME buyers gravitate toward providers with vernacular interfaces and self-service setup wizards that slash deployment time from nine months to six weeks. The resulting democratization suggests sustained double-digit growth at the lower end of the segment pyramid.

By Software Module: Analytics Modules Surge

Core HR accounted for 31.24% of 2025 revenue and remains the mandatory system of record, but manufacturers increasingly view it as basic plumbing. Workforce management still accounts for the largest seat count, yet analytics is forecast to expand at a 12.82% CAGR, making it the fastest-growing module in the HCM software market in manufacturing. Vendors that treat analytics as a differentiator bundle pre-built dashboards for overtime variance, absenteeism hotspots, and skill-gap heat maps, all of which ingest data from ERP and MES feeds.

Payroll remains mission-critical, particularly when mid-quarter statutory changes, such as China’s July 2025 social-insurance adjustment, require hot fixes within days. Talent suites gained traction once predictive models began flagging high-risk employees 90 days before exit, giving HR a window to intervene. Electronics plants in South Korea that tied analytics to real-time shift planning trimmed overtime bills by 16% and lifted on-time delivery by 11%. Vendors are slow to embed AI risk, ceding deals to rivals with pre-trained manufacturing models.

By Manufacturing Sub-Industry: Electronics Outpaces Automotive

Automotive contributed 27.83% of 2025 spending, leveraging HCM to coordinate unionized multi-shift operations and retrain workers for battery-pack lines. Yet electronics and high-tech manufacturers will grow fastest, at a 10.93% CAGR, helped by short product cycles that demand agile head-count redeployment. The HCM software market in manufacturing is expanding, driven by greenfield projects in Asia that opt for cloud-native stacks from day one.

Aerospace and defense adopters prioritize clearance-aware permission controls to remain in compliance with ITAR regulations. Food and beverage producers depend on certification trackers that keep HACCP or SQF credentials current to avoid costly shutdowns. Pharmaceutical plants, under FDA scrutiny, integrate training validation deeply into quality management. Vendors that package vertical templates and factory-floor vernacular are winning a disproportionate share in the fastest-moving subsectors.

Geography Analysis

North America accounted for 34.19% of 2025 revenue courtesy of early cloud acceptance and tight labor markets that made predictive scheduling a board-level priority. U.S. vacancy counts crossing 600,000 spurred the adoption of skills inventories that propose lateral moves before roles open. Canadian automotive suppliers unified payroll across continental plants, while midwestern food producers kept systems on-site due to entrenched ERP cores.

Asia-Pacific is forecast to log an 11.41% CAGR through 2031, powered by greenfield smart factories in India, Vietnam, and Indonesia that sidestep legacy lock-in. Chinese electronics hubs faced PIPL constraints and therefore demanded in-country data residency. Japan’s aging workforce triggered urgency around knowledge-transfer tooling that captures veteran expertise before retirements peak.

Europe saw healthy volume but slower migration due to GDPR cross-border rules and the Platform Work Directive, which stretched compliance timelines. German OEMs tie HCM upgrades to electric-vehicle production pivots, while French food plants fine-tune rosters to respect the Working Time Directive’s rest-period mandates. South America lags due to budget limits, yet modular SaaS at sub-USD 5 per head is breaking through among mid-sized exporters. The Middle East accelerated adoption in Saudi Arabia and the UAE under state digital-industry programs, whereas Africa remains nascent outside South Africa and a handful of Nigerian pilots.

Competitive Landscape

The top five suppliers, SAP, Oracle, Workday, ADP, and Ceridian, captured revenue in 2025, leaving a sizable long tail of specialists. Incumbents now bundle agentic AI that drafts job posts, recommends pay bands, and routes approvals, shaving up to 40% off HR administrative hours. Asia-Pacific challengers such as Darwinbox, Ramco Systems, and Zoho win on localized payroll and vernacular UX priced below tier-1 suites, appealing to cost-sensitive mid-caps.

White-space growth lies in shift-based employee-experience apps that let frontline workers swap shifts and access micro-learning on any device. Edge-aware solutions that pull IoT sensor alerts directly into roster engines are also emerging, but few legacy vendors can yet deliver true real-time rescheduling. Mergers and partnerships intensified: Oracle introduced Fusion Agile Applications in April 2026, SAP upgraded SuccessFactors, including the same month with skills ontology frameworks, and Workday teamed with Sana to personalize learning based on detected skill gaps. UKG bolstered multistate payroll via the Inova buyout in December 2025, while ADP purchased Pequity to embed compensation analytics.

HCM Software In Manufacturing Industry Leaders

Automatic Data Processing Inc.

UKG Inc.

Oracle Corporation

IBM Corporation

Workday Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Oracle Corporation launched Fusion Agentic Applications, adding autonomous onboarding and benefits enrollment.

- April 2026: SAP SE released SuccessFactors 1H 2026 with real-time analytics linked to S/4HANA.

- April 2026: Sona secured USD 45 million Series B to scale its shift-experience platform.

- March 2026: Workday partnered with Sana to insert AI learning recommendations into talent modules.

Global HCM Software In Manufacturing Market Report Scope

The HCM Software in Manufacturing Market comprises digital platforms that manage workforce operations across manufacturing environments, including payroll, workforce scheduling, talent management, compliance, analytics, and employee engagement. These solutions help manufacturers optimize labor productivity, regulatory adherence, workforce planning, and multi-site operational efficiency.

The HCM Software in Manufacturing Market Report is Segmented by Deployment (Cloud, On-Premises, and Hybrid), Organization Size (Small and Medium-Sized Enterprises, and Large Enterprises), Software Module (Core HR, Workforce Management, Talent Management, and Payroll, Analytics), Manufacturing Sub-Industry (Automotive, Aerospace and Defense, Electronics and High-Tech, Food and Beverage, and Other Manufacturing Sub-Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-Premises |

| Hybrid |

| Small and Medium-Sized Enterprises |

| Large Enterprises |

| Core HR |

| Workforce Management |

| Talent Management |

| Payroll |

| Analytics |

| Automotive |

| Aerospace and Defense |

| Electronics and High-Tech |

| Food and Beverage |

| Other Manufacturing Sub-Industries |

| North America |

| South America |

| Europe |

| Asia Pacific |

| Middle East |

| Africa |

| By Deployment | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Small and Medium-Sized Enterprises |

| Large Enterprises | |

| By Software Module | Core HR |

| Workforce Management | |

| Talent Management | |

| Payroll | |

| Analytics | |

| By Manufacturing Sub-Industry | Automotive |

| Aerospace and Defense | |

| Electronics and High-Tech | |

| Food and Beverage | |

| Other Manufacturing Sub-Industries | |

| By Geography | North America |

| South America | |

| Europe | |

| Asia Pacific | |

| Middle East | |

| Africa |

Key Questions Answered in the Report

How large is the HCM Software in Manufacturing Market today?

The market reached USD 3.38 billion in 2026, on track to hit USD 5.37 billion by 2031.

Which deployment model is growing fastest inside manufacturing plants?

Cloud contracts are expanding at an expected 10.43% CAGR as factories adopt hybrid or full SaaS to accelerate feature uptake.

Why are analytics modules attracting new budget?

Manufacturers increasingly need real-time insights that cut overtime and predict turnover; analytics modules therefore show a 12.82% CAGR to 2031.

What is driving SME adoption of HCM systems?

Low per-employee subscription pricing and self-service setup tools allow smaller manufacturers to deploy targeted modules without heavy upfront spend.

Which geographic region will contribute the most incremental revenue through 2031?

Asia-Pacific is forecast to log the fastest expansion, posting an 11.41% CAGR as new smart factories deploy cloud-native HCM from day one.

How are vendors differentiating in a fragmented landscape?

Leading providers embed agentic AI for autonomous HR tasks, while challengers focus on localized payroll, shift-based mobile UX, and edge-aware scheduling.

Page last updated on: