North America Learning Management Systems (LMS) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

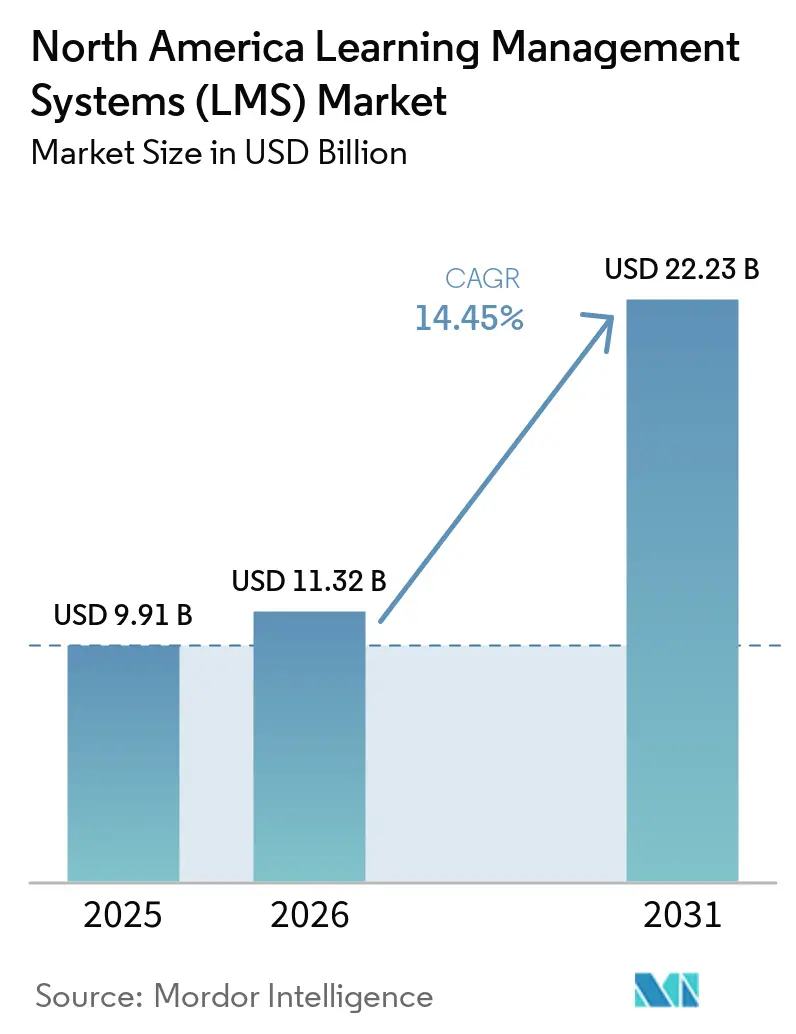

| Base Year Market Size (2025) | USD 9.91 Billion |

| Market Size (2026) | USD 11.32 Billion |

| Market Size (2031) | USD 22.23 Billion |

| Growth Rate (2026 - 2031) | 14.45% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Learning Management Systems (LMS) Market Analysis by Mordor Intelligence

The North America learning management systems (LMS) market size is projected to expand from USD 9.91 billion in 2025 and USD 11.32 billion in 2026 to USD 22.23 billion by 2031, registering a CAGR of 14.45% between 2026 and 2031. The North America learning management systems market is experiencing sustained demand because employers are treating AI-related reskilling as a business requirement rather than a short-term response to digital disruption. Replacing older on-premises learning stacks also supports expansion, especially when organizations need stronger analytics, easier administration, and better support for distributed users. The growing use of verifiable credentials is expanding the role of learning platforms in hiring, workforce development, and institutional outcomes, giving the category relevance beyond course delivery alone. Spending in the North America learning management systems market is also more protected than in many other software categories because a meaningful share of budgets is tied to auditable training and accountability requirements. Privacy obligations and integration challenges are still slowing some deployments, yet the broader direction remains strong because buyers continue to prioritize workforce readiness, skills visibility, and documented learning records.

Key Report Takeaways

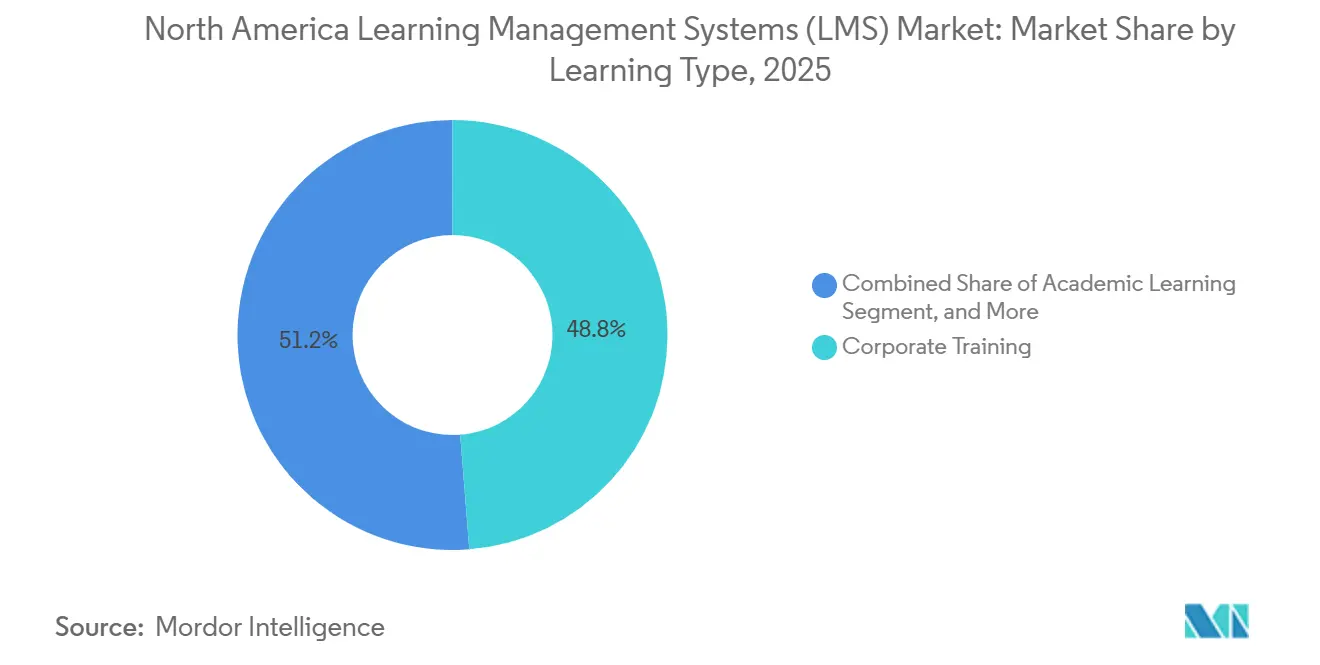

- By learning type, corporate training held a 48.76% share of the the North America learning management systems (LMS) market in 2025, while academic learning is forecast to expand at a 16.82% CAGR from 2026 to 2031.

- By geography, the United States accounted for 75.91% share in 2025, while Mexico is projected to grow at a 16.46% CAGR from 2026 to 2031.

- By end-user vertical, BFSI captured a 40.68% share in 2025, while Healthcare and Life Sciences are set to advance at a 15.92% CAGR from 2026 to 2031.

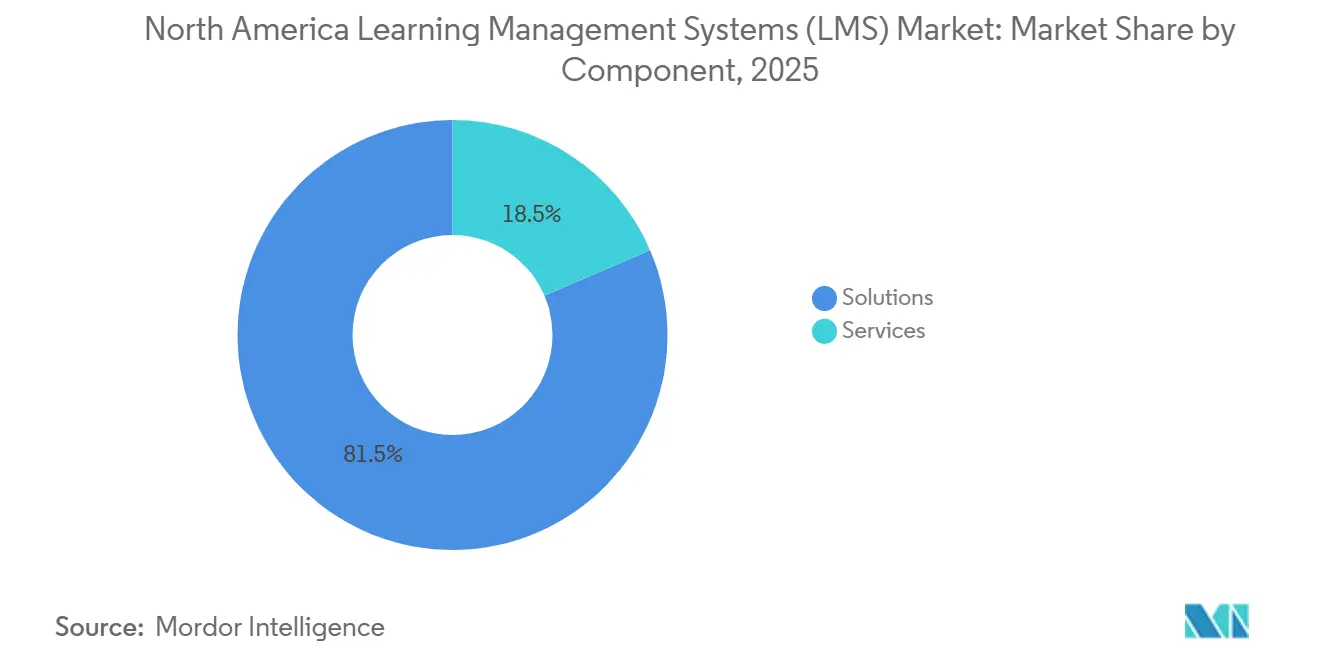

- By component, solutions accounted for 71.44% of the market in 2025, while services are projected to record a 16.27% CAGR from 2026 to 2031.

- By deployment, cloud led with 65.32% share in 2025, while hybrid deployment is forecast to grow at a 15.34% CAGR from 2026 to 2031.

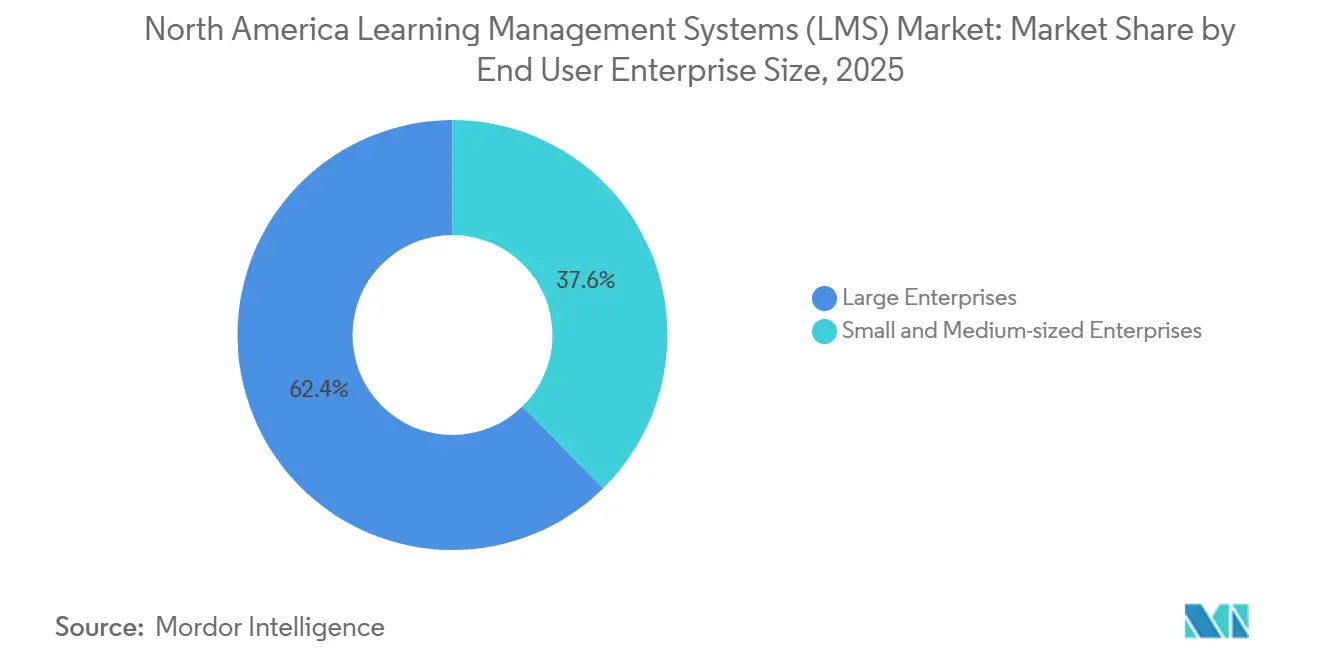

- By enterprise size, large enterprises held 62.36% share in 2025, while small and medium-sized enterprises are projected to expand at a 17.11% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Learning Management Systems (LMS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise Upskilling and Compliance Digitization | +3.8% | Global, with concentration in United States and Canada | Short term (≤ 2 years) |

| AI-Powered Personalization and Learning Analytics Adoption | +3.2% | Global, early gains concentrated in United States | Medium term (2-4 years) |

| Hybrid and Asynchronous Learning Normalization | +2.3% | United States and Canada, spill-over to Mexico | Short term (≤ 2 years) |

| Cloud-Native LMS Modernization for Distributed Training | +1.8% | United States primarily, expanding across North America | Medium term (2-4 years) |

| Verifiable Digital Credentials and Skills-Based Hiring Integration | +1.2% | United States and Canada, early gains in higher education hubs | Medium term (2-4 years) |

| Learner Record Interoperability and Short-Form Credential Accountability | +0.8% | United States, with expanding influence in Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Enterprise Upskilling and Compliance Digitization

The North America learning management systems market is receiving steady support from employers that now treat reskilling as an operating requirement rather than an occasional talent initiative. Instructure announced the broad availability of Canvas Career in January 2026 to support skills-first workforce learning for adult learners and workforce-aligned education programs, underscoring how closely platform demand is now tied to employability and internal mobility needs. Regulated buyers are also keeping spending consistent because training completion, certification status, and learner records must be documented and retrievable across large user populations. TotaraGov states that its platform serves more than 50 U.S. government agencies, including USDA's AgLearn environment, which has 140,000 users across 30 agencies, demonstrating how deeply auditable digital learning is embedded in public-sector operations. Docebo also disclosed customer wins with a major U.S. financial services regulator, reinforcing the importance of learning systems in highly supervised environments. This blend of skills, pressure, and recurring compliance needs gives the North America learning management systems market a durable demand floor even when general software budgets face scrutiny.[1]Docebo Launches Docebo AgentHub and Unites Skills Intelligence, Enterprise Knowledge, and Agentic AI in a Single Platform,” Docebo Newsroom, docebo.com

AI-Powered Personalization and Learning Analytics Adoption

The North America learning management systems market is moving from basic content delivery toward platforms that guide learning decisions in real time. Docebo launched AgentHub in April 2026 to combine learning delivery, enterprise knowledge, skills intelligence, and agentic AI in a single environment, demonstrating how vendors are repositioning the LMS as a more active system layer. Litmos is promoting AI and machine learning video assessments that evaluate learner tone, clarity, and keyword use without manual grading, which expands scalable skills validation for distributed teams. Instructure also introduced AI Nutrition Facts within its April 2026 Canvas tier update, giving buyers clearer visibility into how AI-enabled features work and what they process. Those releases matter because many education, public-sector, and regulated enterprise buyers want automation that improves learner outcomes without weakening governance or explainability. As a result, vendors that can show transparent AI workflows are gaining a stronger position in the North America learning management systems market.[2]April 2026 Product Release, Learning Everywhere You Work,” Docebo, docebo.com

Hybrid and Asynchronous Learning Normalization

The North America learning management systems market is also benefiting from training formats that now combine live instruction, self-paced modules, and in-person sessions within a single operating model. Organizations with shift-based labor and geographically dispersed teams are relying more on asynchronous content because staff cannot always attend instructor-led sessions at fixed times, which keeps platform usage tied to daily operations. Instructure's February 2026 partnership with Orijin expanded Canvas into more than 300 correctional facilities across 20 states, where asynchronous delivery is necessary because standard cohort scheduling is not practical. That move shows how flexible delivery models are opening institutional settings that were historically hard to serve through conventional classroom methods. Hybrid design also improves content reuse across campuses, worksites, and workforce programs, helping learning teams expand course libraries without matching staffing growth. This normalization of blended delivery keeps the North America learning management systems market aligned with long-term operating needs rather than one-time digitization projects.[3]Home - Totara Gov,” TotaraGov, totaragov.com

Cloud-Native LMS Modernization for Distributed Training

Distributed users need easier access, faster upgrades, and more centralized administration. Instructure announced an exclusive strategic partnership with K16 Solutions in April 2026 to automate complex LMS transitions into Canvas, including course migration, assessment transfer, and preservation of course structure. The prominence of a dedicated migration partnership shows that replacement cycles are active and that switching barriers are now being addressed more directly than before. TotaraGov states that its platform serves more than 50 U.S. agencies, including USDA's AgLearn deployment, indicating that even security-sensitive buyers are willing to modernize learning environments when governance expectations are met. Instructure's April 2026 product update also embedded new AI capabilities into Canvas tiers, underscoring how advanced features are increasingly delivered through existing cloud environments. Cloud readiness, therefore, matters not only for infrastructure simplicity, but also because it supports the analytics, AI, and product velocity that buyers increasingly expect from the North America learning management systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and Cybersecurity Concerns | -1.8% | United States nationally, concentrated in K-12 and higher education | Short term (= 2 years) |

| Legacy HRIS, SIS, and Content-System Integration Complexity | -1.3% | United States and Canada, enterprise and government segments | Medium term (2-4 years) |

| Fragmented State AI and Student-Data Regulation | -0.8% | United States, with highest concentration in California and Colorado | Medium term (2-4 years) |

| Rising Cyber-Insurance and Security-Control Costs for School Districts | -0.5% | United States, concentrated in K-12 public school districts | Long term (= 4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Cybersecurity Concerns

The North America learning management systems market still faces slower procurement where student or employee data governance is highly sensitive. CoSN's 2025 National Student Data Privacy Report found that 88% of district ed-tech leaders ranked student data privacy as a top-two priority, underscoring how central this issue has become in education purchasing decisions. The same report showed that only 43% conducted regular audits of their privacy practices, indicating that many institutions are still working through governance gaps as they expand digital learning use. CoSN also found that 55% of respondents were concerned about managing the influx of unvetted classroom technologies, which raises the bar for LMS vendors adding AI and third-party capabilities. Buyers are therefore asking harder questions on data access, retention, oversight, and institutional control before approving deployments. The result is not a collapse in demand, but a longer path to conversion across privacy-sensitive segments of the North America learning management systems market.

Legacy HRIS, SIS, and Content-System Integration Complexity

Integration work remains a practical brake on the North America learning management systems market, especially when buyers must connect learning records with HR, student, and identity systems. Instructure's April 2026 partnership with K16 Solutions centered on automated migration of course content, assessments, and course structure from legacy LMS platforms into Canvas, indicating that migration friction remains significant enough to warrant specialized tooling. The prominence of that offer makes clear that many projects are delayed not by lack of interest but by the complexity of preserving data continuity while switching platforms. Class and Docebo also announced a partnership that lets customers launch virtual instructor-led training directly from Class while centralizing learner performance and completion data in Docebo's analytics environment, which reflects the same need for cross-platform continuity. When buyers expect audit-ready histories, incomplete mappings or broken records can push projects beyond original timelines and raise switching risk. This is why implementation partners, migration services, and clean, prebuilt integrations remain important for driving conversion across the North America learning management systems market.[4]Michael Chasen, “Class and Docebo Announce Partnership and Integration,” Class, class.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Reflects Implementation Complexity at Scale

Solutions accounted for 71.44% of the North America learning management systems market share by component in 2025, indicating that software subscriptions and platform licenses remained the core spending areas. Services are projected to grow at a 16.27% CAGR, marking the fastest expansion in the North America learning management systems market size by component from 2026 to 2031. That gap between current scale and future growth shows that buyers increasingly value the work around the platform rather than the platform itself. Migration from legacy systems, integration with enterprise applications, AI configuration, learner support, and ongoing optimization are now part of the buying decision in many larger accounts. Instructure's exclusive access to K16 Solutions directly monetizes migration demand and shows that vendors now treat services as a strategic revenue line rather than a peripheral attachment.

The North America learning management systems market is therefore placing more value on services that extend well beyond initial setup. Mid-market buyers also need support, as many lack in-house teams to manage learning integrations, AI policy tuning, and content restructuring. This is widening the addressable opportunity into managed learning support, operational administration, and continuous improvement work. Absorb's 2025 roadmap emphasized AI-driven personalized learning, strategic learning playbooks, and peer learning communities, which indicates that even customer-facing innovations can create new implementation and enablement needs after go-live. As the North America learning management systems industry becomes more dependent on analytics, automation, and migration work, services are likely to remain the faster-moving component, even as solutions maintain the larger revenue base.

By Deployment: Hybrid Configurations Bridge Cloud Aspiration and Data-Sovereignty Constraints

Cloud deployment captured 65.32% of the North America learning management systems market by deployment mode in 2025, confirming that the long migration away from older infrastructure is well advanced. Hybrid deployment is projected to expand at a 15.34% CAGR from 2026 to 2031, which makes it the fastest-growing mode in this segmentation. That pattern shows that many buyers are not choosing between cloud and on-premises in absolute terms. They are instead building staged architectures that preserve sensitive repositories or local controls while moving user-facing learning functions into more flexible environments. TotaraGov's public-sector presence across more than 50 U.S. agencies demonstrates that modern learning deployments can meet strict governance requirements without forcing every buyer onto the same architectural path.

In higher education and government, migration timing often matters as much as the final target architecture, because institutions need continuity of access, preservation of legacy content, and dependable audit trails during transition periods. Instructure's K16 partnership reflects this reality by focusing directly on course migration, assessment transfer, and preservation of structure for institutions leaving older platforms. Cloud delivery is also becoming more strategic, as major vendors are placing new AI capabilities within existing product tiers rather than reserving them for custom environments. Instructure embedded IgniteAI Agent capabilities in Canvas Next during April 2026, and Docebo's 2026 release cycle highlighted continued delivery of AI-enabled features through its cloud platform. For the North America learning management systems market, hybrid deployment is serving as the bridge between current operational constraints and a longer-term move toward cloud-led learning environments.

By Learning Type: Academic Learning Acceleration Reflects a Credential Ecosystem in Transition

Corporate training held 48.76% of the North America learning management systems market by learning type in 2025, supported by recurring compliance, onboarding, and workforce readiness needs across regulated sectors. Academic learning is projected to grow at a 16.82% CAGR from 2026 to 2031, making it the fastest-growing learning type in the current study. Universities and colleges are expanding hybrid and asynchronous delivery while also facing stronger pressure to make credentials easier to verify and move across systems. 1EdTech announced the release of the Comprehensive Learner Record 2.0 standard in March 2025, emphasizing improved security, portability, and verification of digital credentials. That development gives academic LMS platforms a more direct role in how learning evidence is packaged, exchanged, and interpreted beyond the classroom.

AACRAO announced an inaugural cohort of 25 projects for its LER Accelerator in May 2025 to advance learner-centered, interoperable digital credentialing across postsecondary institutions. That matters because institutions are increasingly expected to connect learning activity with portable records that employers and workforce programs can recognize more easily. Academic platforms, therefore, gain value not only as delivery systems but also as part of the credential and employability workflow. Government training and skill development programs are moving in a similar direction as agencies modernize mandatory learning into digital and auditable formats. This combination keeps academic learning the fastest-growing area in the North America learning management systems market and supports a broader role for the North America learning management systems industry in skills signaling.

By End User Vertical: Healthcare Urgency Is Rising Alongside a Strong BFSI Base

BFSI commanded the largest share among end-user verticals at 40.68% in 2025, which reflects the steady pull of compliance-heavy learning demand in financial institutions. Healthcare and Life Sciences is forecast to grow at a 15.92% CAGR from 2026 to 2031, making it the fastest-growing end-user vertical in the study period. Financial services buyers depend on continuous employee education in areas such as conduct, anti-money laundering, cybersecurity awareness, and role-based certification, which supports recurring platform usage. Docebo disclosed a major U.S. financial services regulator among its Q4 2025 customer wins, reinforcing the weight of regulated demand in this segment. Because training records in this vertical carry operational and supervisory value, LMS budgets tend to be harder to defer than many discretionary software projects.

Healthcare growth is being reinforced by tighter oversight, the need for traceable staff education, and broader pressure to align learning activity with operational quality. Instructure's expansion of Canvas Career into skills-first, workforce-oriented learning shows how vendors are building products that can support training tied closely to real job outcomes and structured pathways. Manufacturing and industrial employers add another durable pool of demand because safety training and equipment skill verification must reach distributed locations with reliable records. Education, government, retail, IT, energy, and media also contribute to the North America learning management systems market, as each vertical blends onboarding, compliance, and skill development in different proportions. This broad end-user spread helps the North America learning management systems market remain resilient even as growth rates vary across verticals.

By End User Enterprise Size: SME Acceleration Signals a Broader Buyer Base

Large enterprises retained a 62.36% share by end-user enterprise size in 2025, reflecting their established need for advanced integration, broad deployment, and detailed audit trails. Small and medium-sized enterprises are projected to expand at a 17.11% CAGR from 2026 to 2031, which is the fastest rate across all segmentation types in this market. That difference shows how quickly barriers to adoption are falling for buyers who once found LMS platforms too expensive or too complex. SaaS pricing, simpler connector frameworks, and AI-assisted authoring are reducing the need for large internal learning and technical teams. Absorb reported 28% year-over-year revenue growth in 2024 and outlined a 2025 roadmap centered on AI-driven personalized learning and broader product innovation, which fits the needs of buyers seeking faster setup and easier ongoing use.

Smaller employers are also facing more formal training needs in healthcare, manufacturing, privacy, and safety environments, which is creating a larger pool of first-time LMS buyers. Instructure's workforce-oriented expansion through Canvas Career shows that vendors are targeting users beyond the traditional large-enterprise base, into institutions and organizations with more practical skills pathways. The North America learning management systems market is therefore widening from its historical core into a broader mix of sub-500 and mid-sized organizations. Vendors that balance ease of deployment with solid reporting and clean governance are likely to gain traction faster than systems designed only for large, complex rollouts. This widening buyer profile is one of the clearest signs that the North America learning management systems market has become a more mainstream digital training layer rather than a narrow enterprise niche.

Geography Analysis

The United States accounted for 75.91% of the North America learning management systems market share in 2025, making it the clear center of regional demand. Public-sector deployment remains substantial, and TotaraGov states that its platform serves more than 50 U.S. agencies, including USDA's AgLearn environment, which has 140,000 users across 30 agencies. Docebo also reported expanded engagement with the Department of War Cyber Crime Center through a Deloitte partnership in 2025, demonstrating continued traction in government-linked training environments. The country also hosts a dense concentration of leading LMS vendors, which keeps product development active and pricing pressure visible across many buyer categories. AACRAO's LER Accelerator announced 25 projects in May 2025 to advance interoperable digital credentialing, which supports broader LMS requirements around learner records and credential portability in U.S. higher education.

Canada ranked second among regions in 2025, with demand concentrated in financial services, government, and higher education. Canadian privacy expectations and data handling requirements keep residency, contracting, and governance terms important during vendor evaluation, which supports demand for providers that can adapt beyond standard U.S. configurations. The country also has a meaningful domestic vendor base, including D2L, Absorb Software, Axonify, and SkyPrep, which helps sustain product familiarity and cross-border reach. AACRAO's broader work on innovative credentials also reflects a North American push toward more interoperable learner records, which supports Canadian institutions pursuing similar modernization paths. Renewal and upgrade cycles at colleges and universities remain important in Canada because many institutions are now moving from emergency-era digital adoption toward more deliberate platform selection.

Mexico is the fastest-growing geography in the region, with a projected 16.46% CAGR from 2026 to 2031, marking the quickest expansion in the North America learning management systems market by geography. D2L established a legal entity in Mexico in April 2024, formalizing direct market presence in education and corporate training and signaling stronger vendor commitment to the country. Nearshoring activity in automotive, aerospace, and electronics manufacturing is driving demand for standardized, multilingual, and audit-ready training systems in formal workforce environments. Because many organizations are still in first-generation enterprise LMS deployment rather than replacement mode, mobile-first platforms with fast implementation cycles are especially well positioned in the North America learning management systems market.

Competitive Landscape

The North America learning management systems market remains moderately fragmented, with Instructure and Blackboard stronger in academic and public-sector environments, and a broader competitive field in corporate training. Buyers often maintain multi-vendor ecosystems because content delivery, virtual classrooms, skills intelligence, and credential workflows do not always come from a single provider. KKR and Dragoneer completed the USD 4.8 billion acquisition of Instructure in November 2024, which shows that large investors see room for further scale and consolidation in this category. That transaction also signaled confidence that the category can support long-duration investment rather than short-lived pandemic demand. Even so, fragmentation persists because buyers in regulated and institution-specific segments still value specialized workflows, deployment flexibility, and integration depth.

Strategic moves in 2025 and 2026 show that leading vendors are extending beyond the traditional LMS core. Docebo launched AgentHub in April 2026 and then moved its MCP Server to public beta in May 2026, positioning its learning library as a native knowledge source for major external AI assistants. Instructure paired simplified Canvas tiers with exclusive access to K16 migration services in April 2026, combining feature expansion with a direct answer to switching friction. Instructure had already partnered with OpenAI in July 2025 to embed AI learning experiences in Canvas, thereby strengthening its position in both academic and workforce settings. Absorb's 2025 roadmap emphasized AI-driven personalized learning, strategic learning playbooks, and peer learning communities, which shows how mid-sized challengers are broadening their value proposition around engagement and outcomes.

White-space opportunities remain strongest in SME compliance platforms, government and corrections learning, and extended enterprise training for customers, dealers, and partners. Instructure's Orijin partnership across more than 300 correctional facilities shows how underserved institutional settings can open meaningful new demand pockets. Vendors that combine fast implementation with strong security evidence and clean interoperability are likely to win more deals than vendors that compete only on feature count. The North America learning management systems market, therefore, supports both scaled platforms and focused specialists, which is why competitive pressure is rising without collapsing into a winner-take-most structure.

North America Learning Management Systems (LMS) Industry Leaders

Instructure, Inc.

Blackboard LLC

D2L Corporation

Docebo Inc.

Absorb Software Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Docebo MCP Server entered public beta, linking its learning library to external AI assistants like Copilot, Claude, and ChatGPT, embedding LMS content into enterprise AI workflows.

- April 2026: Instructure and K16 Solutions formed an exclusive partnership to automate LMS migrations into Canvas, easing course, assessment, and structure transfers.

- April 2026: Docebo AgentHub launched, merging learning delivery, knowledge management, and skills intelligence with agentic AI, reflecting accelerated AI-driven product releases.

- April 2026: Instructure Canvas tiers debuted (Core, Plus, Next), with Canvas Next embedding IgniteAI Agent via Amazon Bedrock. U.S. institutions received free advanced AI access through June 2026.

North America Learning Management Systems (LMS) Market Report Scope

The North America Learning Management Systems (LMS) market refers to the ecosystem of digital platforms and services that deliver, manage, and track training, education, and skill development across corporate, academic, and government sectors. It encompasses cloud, hybrid, and on-premises deployments, supporting compliance, credentialing, workforce readiness, and learner engagement. Driven by AI integration, blended delivery, and governance needs, the market enables scalable, auditable, and outcome-focused learning experiences.

The North America Learning Management Systems (LMS) Market Report is segmented by Component (Solutions, and Services), Deployment (Cloud, On-Premises, and Hybrid), Learning Type (Academic Learning, Corporate Training, Government/Public Training, and Skill Development/Certification), Enterprise Size (Large Enterprises and Small and Medium-sized Enterprises), Industry Vertical (Information Technology and Telecommunications, Banking Financial Services and Insurance, Healthcare and Life Sciences, Manufacturing and Industrial Operations, Retail and E-commerce, Education, Government and Public Sector, Energy and Utilities, Media and Entertainment, and Others), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions |

| Services |

| Cloud |

| On-premises |

| Hybrid |

| Academic Learning |

| Corporate Training |

| Government / Public Training |

| Skill Development / Certification |

| Information Technology (IT) and Telecommunications |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Manufacturing and Industrial Operations |

| Retail and E-commerce |

| Education |

| Government and Public Sector |

| Energy and Utilities |

| Media and Entertainment |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| United States |

| Canada |

| Mexico |

| By Component | Solutions |

| Services | |

| By Deployment | Cloud |

| On-premises | |

| Hybrid | |

| By Learning Type | Academic Learning |

| Corporate Training | |

| Government / Public Training | |

| Skill Development / Certification | |

| By End User Vertical | Information Technology (IT) and Telecommunications |

| Banking, Financial Services, and Insurance (BFSI) | |

| Healthcare and Life Sciences | |

| Manufacturing and Industrial Operations | |

| Retail and E-commerce | |

| Education | |

| Government and Public Sector | |

| Energy and Utilities | |

| Media and Entertainment | |

| By End User Enterprise Size | Large Enterprises |

| Small and Medium-sized Enterprises | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the size outlook for the North America learning management systems market?

The North America learning management systems market is projected to expand from USD 9.91 billion in 2025 and USD 11.32 billion in 2026 to USD 22.23 billion by 2031, at a 14.45% CAGR.

Which learning type is largest and which is growing fastest?

Corporate training held the largest share at 48.76% in 2025, while academic learning is forecast to grow the fastest at a 16.82% CAGR through 2031.

Why are companies continuing to invest in LMS platforms after the initial digital learning wave?

Spending remains durable because employers need AI-related upskilling, auditable compliance training, and better systems for distributed learning delivery and credential tracking.

Which deployment model is leading adoption in North America?

Cloud led with 65.32% share in 2025, but hybrid deployment is growing faster at 15.34% CAGR as buyers balance cloud goals with legacy systems and data control needs.

Which country is driving the strongest regional growth?

The United States led regional demand with 75.91% share in 2025, while Mexico is expected to post the fastest growth at a 16.46% CAGR through 2031.

What is shaping vendor competition across the region?

Competition is being shaped by AI product expansion, migration partnerships, credential interoperability, and demand from regulated sectors that often require multi-vendor ecosystems rather than a single platform.

Page last updated on: