Management Decision Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

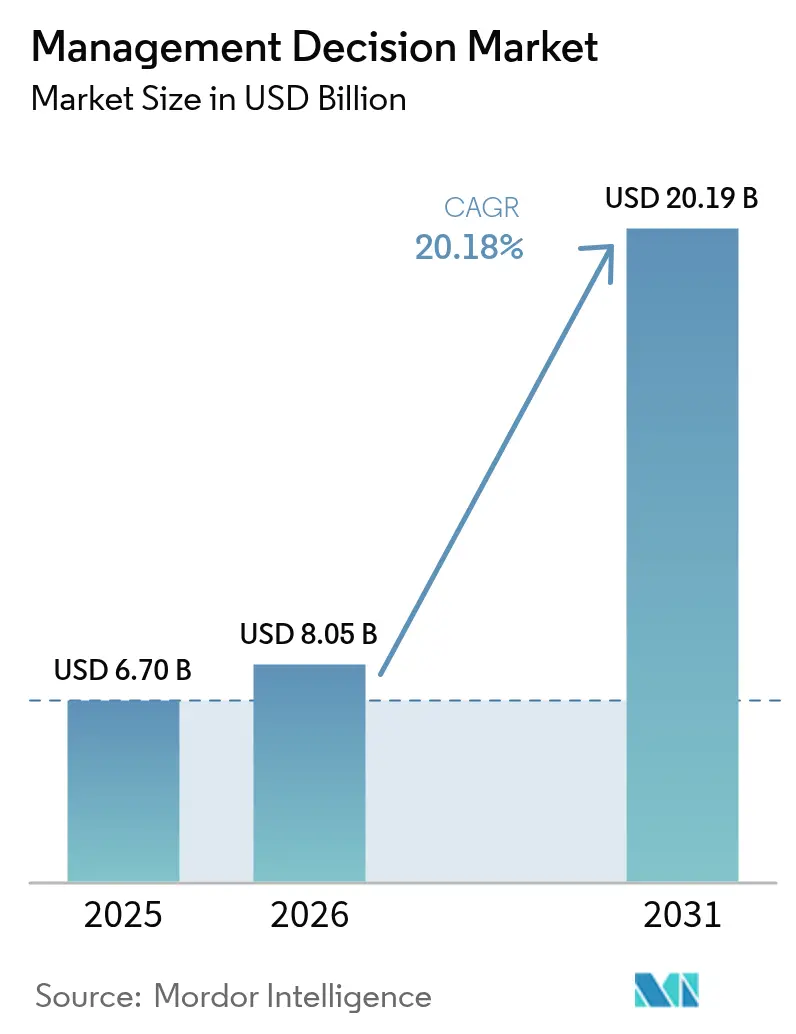

| Market Size (2026) | USD 8.05 Billion |

| Market Size (2031) | USD 20.19 Billion |

| Growth Rate (2026 - 2031) | 20.18% CAGR |

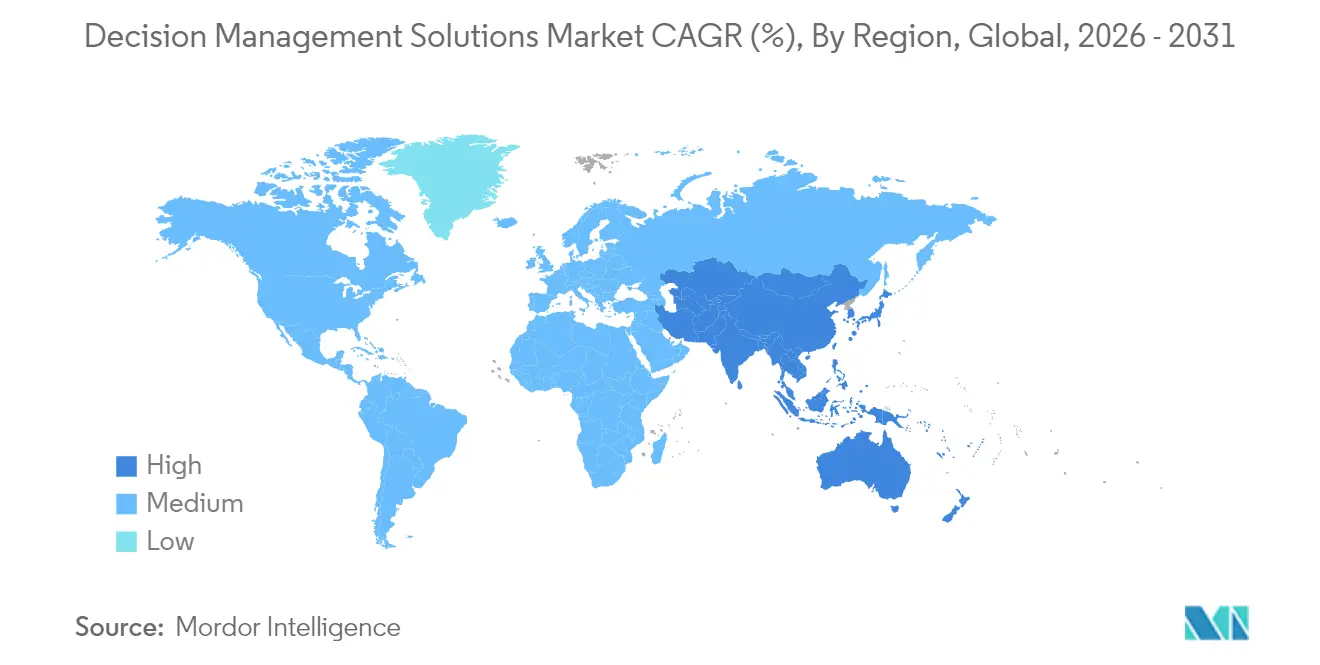

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Management Decision Market Analysis by Mordor Intelligence

The management decision market size in 2026 is estimated at USD 8.05 billion, growing from 2025 value of USD 6.70 billion with 2031 projections showing USD 20.19 billion, growing at 20.18% CAGR over 2026-2031. Growth reflects the corporate shift from descriptive analytics toward decision intelligence that blends business rules with artificial intelligence (AI) to speed and enhance outcomes. Cloud-native deployment, heightened regulatory scrutiny that requires explainable AI, and the spread of low-code tooling are central drivers as enterprises seek faster insight-to-action cycles.[1]American Hospital Association, “AI Adoption in Revenue Cycle Management,” aha.org Vendors are now converging decision engines, process orchestration, and machine learning in unified platforms, allowing firms to automate more operational decisions while retaining governance controls.

Key Report Takeaways

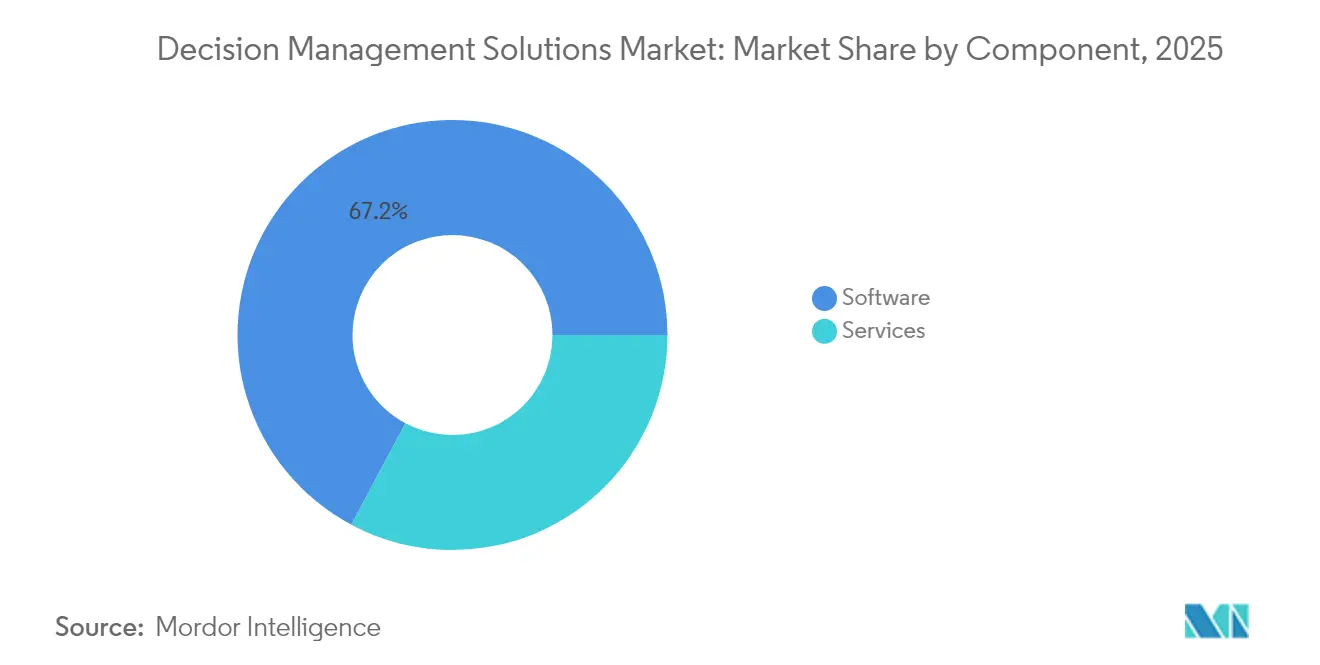

- By component, software held 67.20% of the management decision market size in 2025, whereas services are projected to grow at a 21.95% CAGR to 2031.

- By deployment type, the cloud segment captured 79.30% of the management decision market size in 2025, and is advancing at a 21.56% CAGR through 2031.

- By organization size, large enterprises commanded 61.40% of the management decision market size in 2025; small and mid-sized enterprises (SMEs) are forecast to expand at a 21.25% CAGR between 2026-2031.

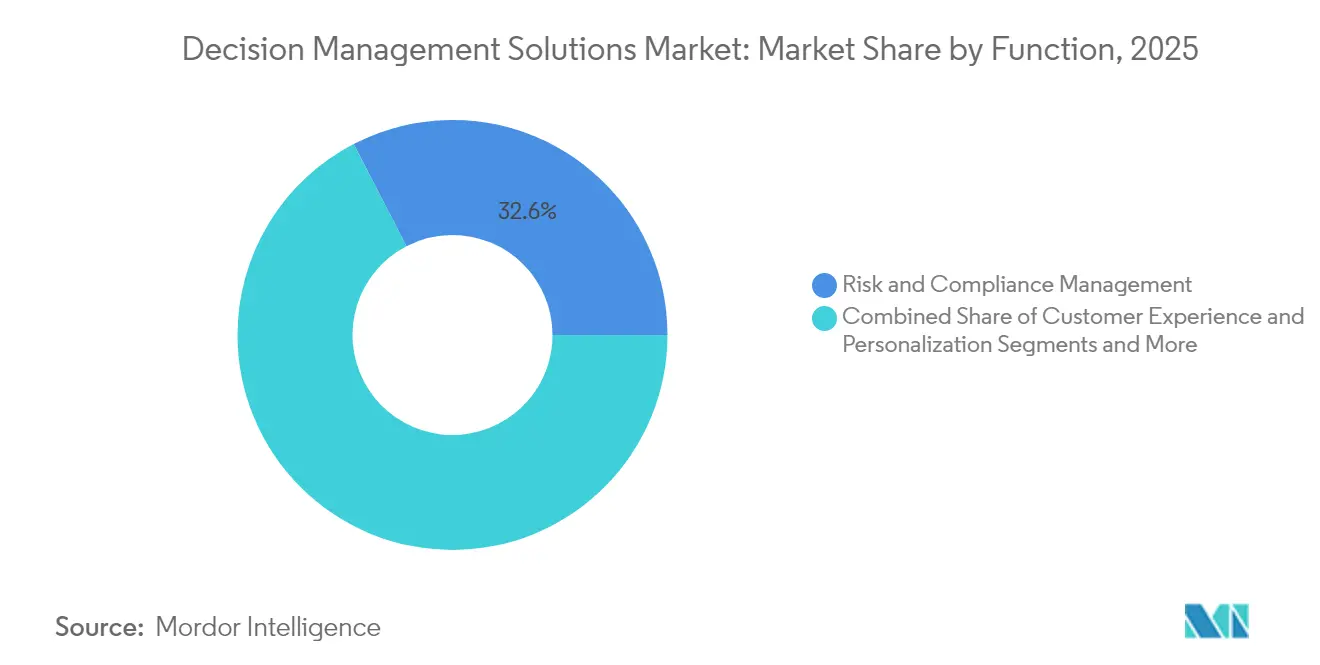

- By function, risk and compliance led with 32.60% of the management decision market size in 2025; fraud detection is the fastest-growing function at 23.68% CAGR through 2031.

- By end-user industry, banking, financial services, and insurance (BFSI) dominated with a 29.40% of the management decision market size in 2025; healthcare applications are set to grow at a 24.1% CAGR to 2031.

- By geography, North America accounted for 36.50% of the management decision market size in 2025, while the Asia-Pacific region is projected to rise at a 23.95% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Management Decision Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Need for Business Agility and Real-Time Insights | +5.8% | Global, led by North America and Western Europe | Short term (≤ 2 years) |

| Surge in Decision Analytics Adoption in BFSI | +4.9% | North America, Europe, APAC financial hubs | Medium term (2-4 years) |

| Compliance-Driven Demand for Explainable AI | +3.7% | Highly regulated markets in US, EU, UK | Medium term (2-4 years) |

| Low-Code/No-Code Platforms Widening User Base | +3.2% | Global, faster uptake in North America and APAC | Short term (≤ 2 years) |

| Embedded Decisioning in Edge and IoT Devices | +2.6% | North America, Europe, advanced APAC economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Need for Business Agility and Real-Time Insights

Market turbulence has turned real-time decisioning into a survival requirement. Modern platforms now fuse predictive analytics with rule engines, enabling organizations to act on signals before they disrupt performance. Enterprises are automating high-volume operational decisions such as pricing and routing through multi-agent systems that coordinate workflows without human delay. Decision flows span departments to keep execution aligned with evolving market conditions while preserving consistent policy enforcement.

Surge in Decision Analytics Adoption in Banking, Financial Services, and Insurance (BFSI)

Banks and insurers are embedding decision engines in credit approval, claims processing and customer interaction journeys. Automated credit decisioning processes loan applications within seconds and enforces uniform compliance checks. Firms are combining internal records with digital behavior to craft individualized financial offerings, extending services to previously underserved borrowers. End-to-end orchestration tools adjust product terms in real time when customer risk factors or market data shift, improving both portfolio quality and user experience.

Compliance-Driven Demand for Explainable Artificial Intelligence (AI)

Rules such as the European Union’s AI Act require transparency for high-risk automated systems. Enterprises, therefore, favor hybrid architectures that layer machine learning predictions with explicit rules so that every outcome can be traced. Governance frameworks document data lineage, model validation, and decision logic. Leading platforms now deliver natural-language explanations that translate algorithmic output into business language, supporting audits and building stakeholder trust.[2]European Commission, “AI Act Regulation Text,” europa.eu

Low-Code/No-Code Platforms Widening User Base

Visual authoring interfaces allow business specialists to craft and update decision logic without writing code, shortening release cycles and improving model accuracy. Citizen developers gain autonomy while centralized controls maintain standards. Mid-market firms use subscription-based cloud services to access enterprise-grade capabilities once restricted to large Information Technology (IT) teams. As user communities broaden, vendors embed role-based guardrails so multiple contributors can safely collaborate on decision assets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation and integration cost | -3.2% | Global, with greater impact in emerging markets | Medium term (2-4 years) |

| Shortage of domain-specific data for model training | -2.8% | Global, with higher impact in less digitized industries | Medium term (2-4 years) |

| Vendor lock-in concerns with cloud-native stacks | -2.1% | Global, with greater sensitivity in regulated industries | Long term (≥ 4 years) |

| Regulatory uncertainty around automated decisions | -1.9% | Global, with particular impact in EU, UK, and US | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Implementation and Integration Cost

Comprehensive decision programs demand sizable outlays for platform licenses, process redesign and change management. Integration can be complex where legacy systems lack standard Application Programming Interfaces (APIs), forcing middleware development and prolonged testing. Smaller firms bear a higher cost burden relative to their budgets, which slows adoption. A phased approach that first targets a few high-value use cases helps generate quick wins and funds expansion while building internal expertise.

Shortage of Domain-Specific Data for Model Training

The effectiveness of AI-powered management decision systems depends heavily on the availability of high-quality, domain-specific training data that accurately represents the decision context. Many organizations struggle to accumulate sufficient historical decision examples, particularly for rare but critical scenarios that most benefit from decision support. This challenge is compounded by data privacy regulations that restrict the use of personal information for model training, forcing organizations to develop synthetic data generation capabilities or federated learning approaches. The data quality issue is particularly acute in sectors undergoing rapid transformation, where historical patterns may not reflect emerging realities. Organizations are addressing this constraint through active learning approaches that prioritize human review of edge cases, gradually building more comprehensive decision models while maintaining operational performance. The most successful implementations combine machine learning with explicit business rules that encode domain knowledge where data is insufficient, creating hybrid systems that leverage both data-driven insights and human expertise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominates, Services Accelerate

Software accounted for a commanding 67.20% management decision market share in 2025, underpinned by engines that merge rule management with analytics and natural-language interfaces. Vendors increasingly embed generative AI that suggests rule optimizations and flags compliance gaps. Services, though smaller, are on a 21.95% CAGR path as organizations seek advisory, deployment, and continuous optimization expertise. Providers are evolving industry accelerators that compress rollout timelines by packaging proven decision templates.

Implementation partners redesign processes, create governance playbooks, and run managed optimization programs that keep decision performance aligned with changing regulations and business goals. Firms lacking in-house data science tap these offerings to maintain decision quality. As AI scaling tops executive agendas, demand for continuous model monitoring and recalibration services is rising, supporting sustained expansion for service specialists.

By Deployment Type: Cloud Preference Deepens

Cloud captured 79.30% of the management decision market in 2025 and is growing at 21.56% CAGR through 2031 as organizations favor elastic capacity and consumption-based pricing. Cloud platforms allow instant scaling to meet volatile decision workloads, important for seasonal transaction spikes. Even regulated sectors adopt virtual private clouds to meet sovereignty requirements. Some enterprises, however, repatriate sensitive workloads to private environments, creating hybrid estates that blend cloud flexibility with on-premise control.

Decision architects now evaluate each workload along criteria such as latency, data locality, and licensing commitments rather than choosing a single hosting model. Multi-cloud adoption is rising to avoid lock-in and to exploit specialized capabilities from different providers. Vendors respond with portable services built on container technology so clients can shift deployments without rewriting decision logic.

By Organization Size: Small and Medium Enterprises (SMEs) Gain Momentum

Large enterprises owned 61.40% of the market in 2025, leveraging mature data ecosystems and budget depth to embed decision management widely. They coordinate decisions across units via centralized governance groups that ensure policy alignment. Complex environments demand orchestration layers capable of chaining multiple decision services into a coherent execution flow.

SMEs are catching up, expanding at a 21.25% CAGR as subscription-based cloud platforms lower entry costs. Low-code authoring and industry-specific templates help firms with modest IT staff deploy robust decision flows. Vendors courting the mid-market emphasize simplified pricing, guided configuration and managed services that shoulder model upkeep, closing the capability gap between small and large enterprises.

By Function: Fraud Detection Surges

Risk and compliance remained the largest function with 32.60% of 2025 revenue, as institutions require consistent regulatory adherence and proactive risk mitigation. Platforms ingest legal texts, convert requirements into executable logic and flag non-compliance before issues escalate. Natural-language features help compliance teams update rules swiftly when regulations change.

Fraud detection is the fastest-growing use case, advancing at 23.68% CAGR through 2031. Machine-learning models monitor transaction streams and behavioral biometrics in milliseconds, blocking illicit activity while keeping false positives low. Multimodal analytics that analyse text, images and geospatial signals are emerging to counter sophisticated synthetic-identity and deepfake schemes. Organizations report steep drops in chargebacks and substantial rises in approved orders when AI-driven fraud engines are deployed, further propelling adoption.

By End-User Industry: Healthcare Accelerates Adoption

BFSI held a leading 29.40% share in 2025, embedding decision platforms in credit origination, pricing, liquidity management, and customer engagement. Banks combine predictive models with rule frameworks to personalize offers, speed approvals, and prove compliance. The sector’s appetite grows as firms compete with fintech challengers and face increasingly complex regulatory mandates.

Healthcare is expanding fastest at a 24.1% CAGR as providers deploy decision support to improve care quality and revenue integrity. Clinical systems surface treatment recommendations and flag adverse drug interactions, while revenue cycle tools automate coding, prior-authorizatio,n and denial management. The US Department of Health and Human Services' strategic plan highlights AI as a catalyst for equitable, efficient health delivery, encouraging hospitals to embed decision intelligence across operations.

Geography Analysis

North America dominated the management decision market with 36.50% revenue in 2025. Early adoption of AI, deep cloud infrastructure, and a concentration of leading vendors underpin leadership. Financial institutions use decision engines to refine credit scoring and fraud controls, while hospitals apply them to clinical pathways and billing. Regulatory focus on algorithmic fairness reinforces demand for transparent, governable decision platforms. Business specialists increasingly adopt low-code tools, broadening the user community beyond IT and amplifying regional growth momentum.

Asia-Pacific is the fastest-growing region, set to advance at a 23.95% CAGR from 2026 to 2031. Governments across China, Japan, and India invest heavily in AI infrastructure and skills, fostering an environment conducive to large-scale decision deployments. Banks deploy real-time credit and fraud engines to expand financial inclusion, manufacturers embed decision logic in digital production lines, and public agencies roll out citizen-facing services powered by automated decisions. Diverse regulatory regimes spur the adoption of configurable governance modules that adapt to local compliance mandates without fragmenting enterprise standards.

Europe retains a significant share on the back of stringent regulatory frameworks that prioritize explainability. The EU AI Act imposes rigorous obligations for high-risk systems, prompting financial and healthcare organizations to adopt platforms capable of detailed audit trails and natural-language rationale. Multinational firms require cross-border decision consistency, driving demand for centralized rule repositories and language-agnostic governance. Strong implementation partner ecosystems with domain and compliance expertise support steady growth across the region.

Competitive Landscape

The management decision market features moderate concentration. IBM Corporation, Oracle Corporation, SAS Institute Inc., and FICO (Fair Isaac Corporation) anchor the field with broad platforms, global service networks, and deep industry templates. They bundle business rules, optimization, machine learning, and monitoring in unified suites and leverage longstanding enterprise relationships. Cloud-native entrants and AI-first startups compete with lighter, domain-focused offerings that emphasize speed of deployment and low-code configurability. Differentiation increasingly hinges on industry content, governance depth, and ease of use for non-technical roles.

Partnerships are critical as vendors integrate data ingestion, process automation, and monitoring components into end-to-end solutions. Leading providers cultivate marketplaces where specialist partners contribute decision assets such as risk scorecards or healthcare pathways. Mid-market customers are a priority segment where simplified pricing and turnkey accelerators resonate. Established vendors respond with modular packaging and consumption-based billing to repel insurgent competitors.

Generative AI both disrupts and enriches the competitive arena. Vendors introduce features that convert natural-language policies into executable rules or summarize model behavior for auditors. Leaders embed guardrails to prevent model drift and ensure reproducibility, maintaining trust. Players that balance innovation with rigorous governance are poised to capture share as enterprises scale decision automation across critical functions.

Management Decision Industry Leaders

IBM Corporation

Oracle Corporation

SAS Institute Inc.

TIBCO Software Inc.

FICO (Fair Isaac Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: IBM launched Watson Decision Platform 2.0, bringing generative AI to automate model creation from natural-language policies while offering a shared workspace for joint business-IT governance.

- May 2025: Lucinity upgraded its case management suite with AI that cuts compliance investigation times by up to 70% and reduces false positives dramatically.

- April 2025: Backbase unveiled an AI-powered banking platform that unifies customer service and digital sales, using an intelligence fabric to automate operations and accelerate revenue generation.

- April 2025: Nected launched a decision management platform that integrates rules, predictive analytics and optimization in a customizable, cost-efficient package.

- March 2025: The U.S. Department of Health and Human Services issued a strategic plan outlining seven domains where AI will enhance healthcare delivery, public health and workforce development.

- January 2025: FICO released Decision Optimizer X, combining simulation, machine learning and prescriptive analytics so firms can balance risk, profitability and customer experience in one environment.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the management decision market as the aggregate revenue from commercially sold software platforms and their allied integration or support services that ingest data, apply rules or machine-learning models, and automatically trigger or recommend actions inside business workflows such as credit scoring, pricing, and fraud alerts.

Scope Exclusion: Custom-built in-house tools that are not licensed externally are kept out of scope.

Segmentation Overview

- By Component

- Software

- Services

- By Deployment Type

- On-premises

- Cloud

- By Organization Size

- Large Enterprises

- Small and Medium-size Enterprises (SMEs)

- By Function

- Risk and Compliance Management

- Customer Experience and Personalization

- Fraud Detection and Prevention

- Pricing and Revenue Optimization

- Other Function

- By End-User Industry

- Banking, Financial Services, and Insurance (BFSI)

- Information Technology (IT) and Telecom

- Healthcare

- Retail and E-commerce

- Manufacturing

- Government and Public Sector

- Other End-User Industry

- By Geography

- North America

- United States

- Canada

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with platform product leads, banking risk officers, and regional system integrators across North America, Europe, and Asia. These interviews clarified adoption triggers, regional price spreads, and service attachment rates that were only partially visible in secondary data.

Desk Research

We used public datasets from bodies such as the US Bureau of Labor Statistics, Eurostat, Japan MIC, and OECD ICT indicators to size digital spend pools. Company 10-Ks, investor decks, and product catalogs yielded average selling prices, while patent filings highlighted emerging rule-engine use cases. Select paid resources, including D&B Hoovers for supplier financials and Dow Jones Factiva for deal flow, rounded out the evidence base. The sources listed are illustrative; many additional materials supported data collection and cross-checks.

Market-Sizing & Forecasting

We began with a top-down cut of global enterprise software spending and isolated the decision-automation slice using penetration ratios confirmed during primary calls. Supplier roll-ups of sampled ASP x installation counts provided a bottom-up reasonableness test before totals were finalized. Key drivers modeled include cloud workload share, industry-specific regulatory mandates, digital customer-interaction volumes, average rules executed per decision flow, and decline in on-premises license renewals. A multivariate regression blended with ARIMA smoothing projected these drivers through 2030 and informed scenario bounds. Gaps in vendor-level data were bridged with benchmark margins from comparable suppliers.

Data Validation & Update Cycle

Outputs undergo peer review, variance checks against quarterly earnings releases, and reconciliation with trade shipment signals. Models refresh annually, while interim updates are triggered whenever cumulative variance exceeds five percent.

Why Mordor's Management Decision Baseline Commands Reliability

Published estimates often diverge because each study adopts different component mixes, currency bases, and refresh cadences.

Key Gap Drivers: Several publishers count only software revenue, whereas our view adds recurring services. Some hold a 2022 exchange rate constant, inflating growth. Longer refresh cycles outside Mordor fail to capture rapid cloud uptake.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.70 B (2025) | Mordor Intelligence | - |

| USD 6.20 B (2023) | Global Consultancy A | Excludes services; older base year |

| USD 6.76 B (2024) | Industry Association B | Limited geography; assumes flat ASP |

These comparisons show that by pairing refreshed scope with transparent driver selection, Mordor Intelligence delivers a balanced, traceable baseline that decision-makers can rely on.

Key Questions Answered in the Report

What is the current value of the management decision market?

The market is valued at USD 8.05 billion in 2026 and is on track to reach USD 20.19 billion by 2031.

Which component segment is growing fastest?

Services are expanding at a 21.95% CAGR through 2031 due to rising demand for implementation, governance and continuous optimization expertise.

Why is Asia-Pacific the fastest-growing region?

Strong government support for AI infrastructure, rapid digital transformation in banking and manufacturing, and a need for adaptable governance frameworks drive a 23.95% regional CAGR.

How are low-code platforms affecting adoption?

Visual authoring tools let business specialists build and update decision logic without coding skills, widening the user base and accelerating deployment across industries.

What makes explainable AI important for decision management?

Regulations such as the EU AI Act require that organizations can justify automated outcomes, so platforms that provide natural-language explanations and documented data lineage are preferred.

Which end-user industry shows the highest growth potential?

Healthcare is forecast to advance at a 24.1% CAGR as providers deploy decision support for clinical pathways and revenue cycle optimization while aligning with new AI guidelines.

Page last updated on: