Workforce Management (WFM) In Manufacturing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.65 Billion |

| Market Size (2031) | USD 2.59 Billion |

| Growth Rate (2026 - 2031) | 9.44% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Workforce Management (WFM) In Manufacturing Market Analysis by Mordor Intelligence

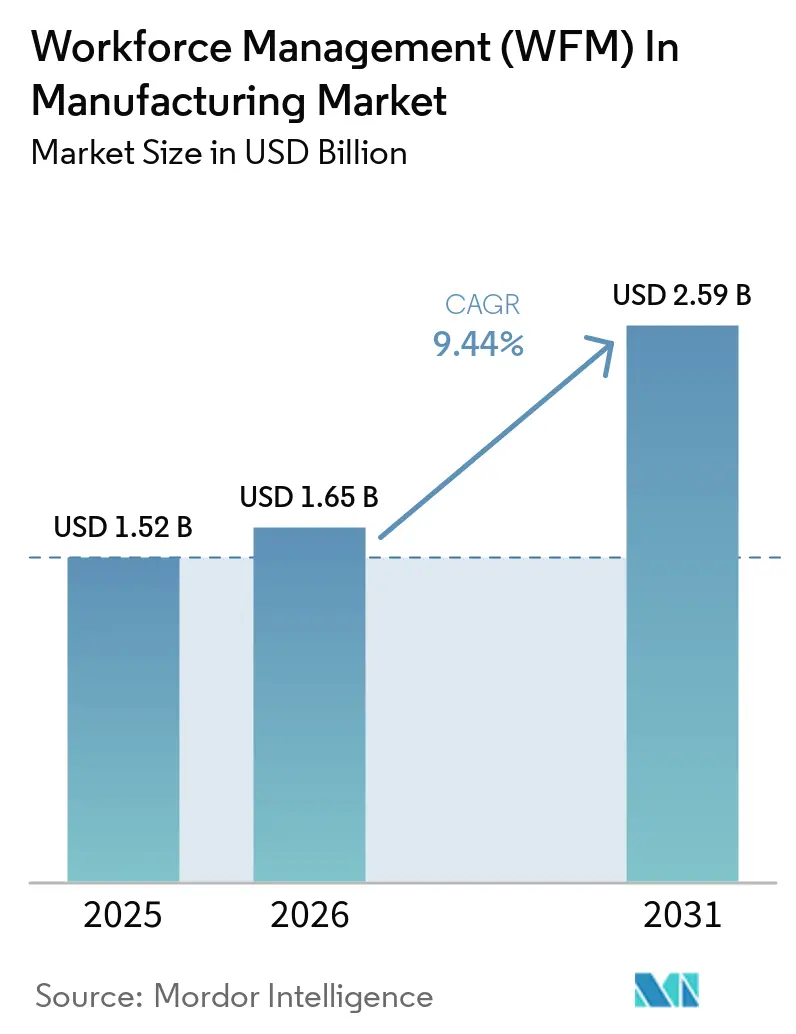

The workforce management (WFM) market in the manufacturing industry was USD 1.52 billion in 2025 and is forecast to reach USD 2.59 billion by 2031, at a CAGR of 9.44% during 2026-2031. Demand is being supported by labor shortages, rising compliance pressure, and the need to manage skills, attendance, and shift coverage more tightly across plants. Software remains the core revenue driver, while faster services growth shows that buyers increasingly need implementation, integration, and advisory support to make these systems work in older factory environments. Cloud deployment still leads adoption, but hybrid models are gaining traction because many manufacturers want modern analytics and employee access without giving up local control over sensitive plant data and workflows. North America leads current demand, while Asia-Pacific is expanding faster as smart-factory programs, labor aging, and industrial digitalization advance. Competition remains fragmented, which is keeping feature development active, even as legacy ERP complexity, unionized operating models, and AI governance rules continue to shape deployment risk and vendor differentiation.

Key Report Takeaways

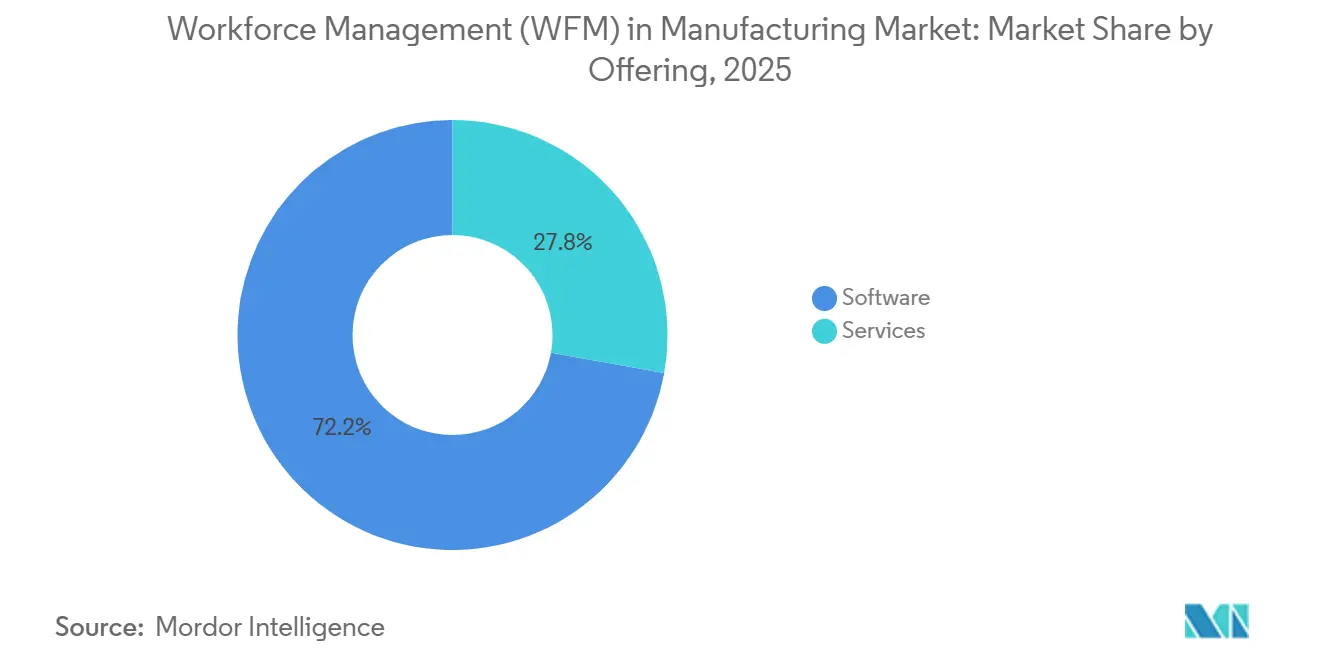

- By offering, software held 72.18% of the workforce management (WFM) in manufacturing market in 2025, while services are forecast to expand at a 13.12% CAGR through 2031.

- By deployment mode, cloud held 61.47% of the WFM in manufacturing market in 2025, while hybrid is forecast to grow at a 14.37% CAGR through 2031.

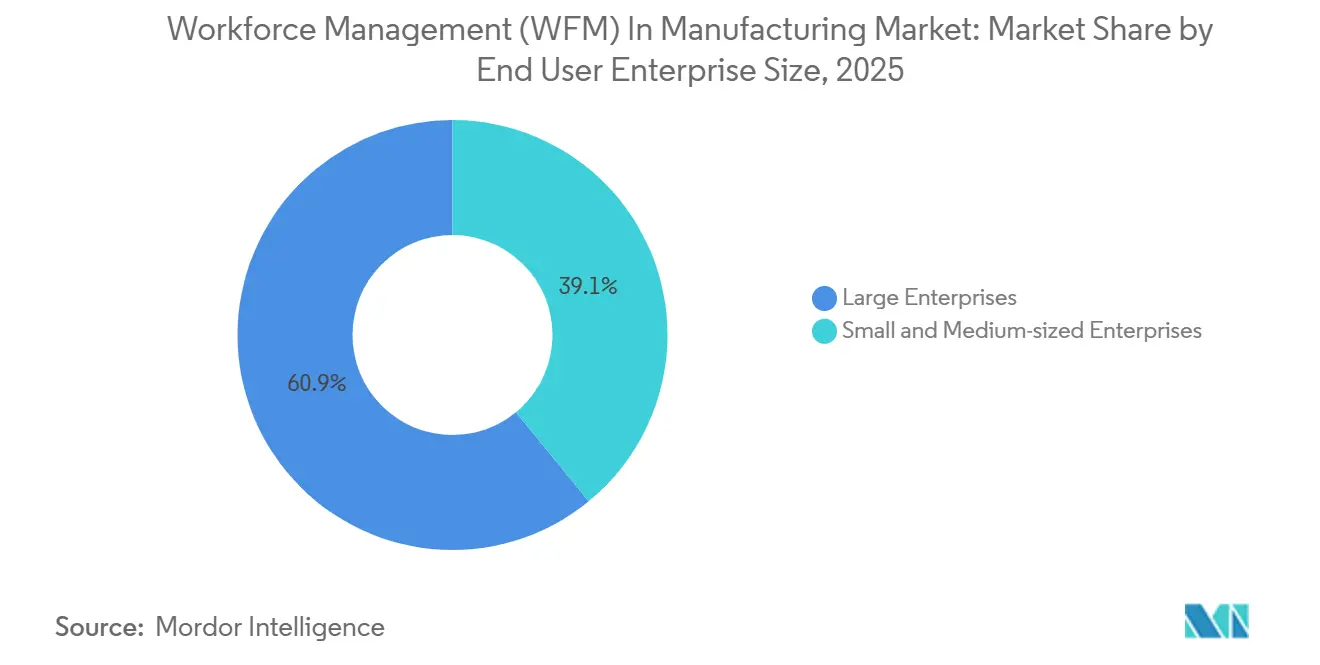

- By enterprise size, large enterprises held 60.93% of the workforce management in manufacturing market in 2025, while SMEs are projected to grow at a 15.48% CAGR through 2031.

- By end-user industry, automotive held 20.61% share of the WFM in manufacturing market in 2025, while electronics and semiconductors are forecast to grow at a 13.99% CAGR through 2031.

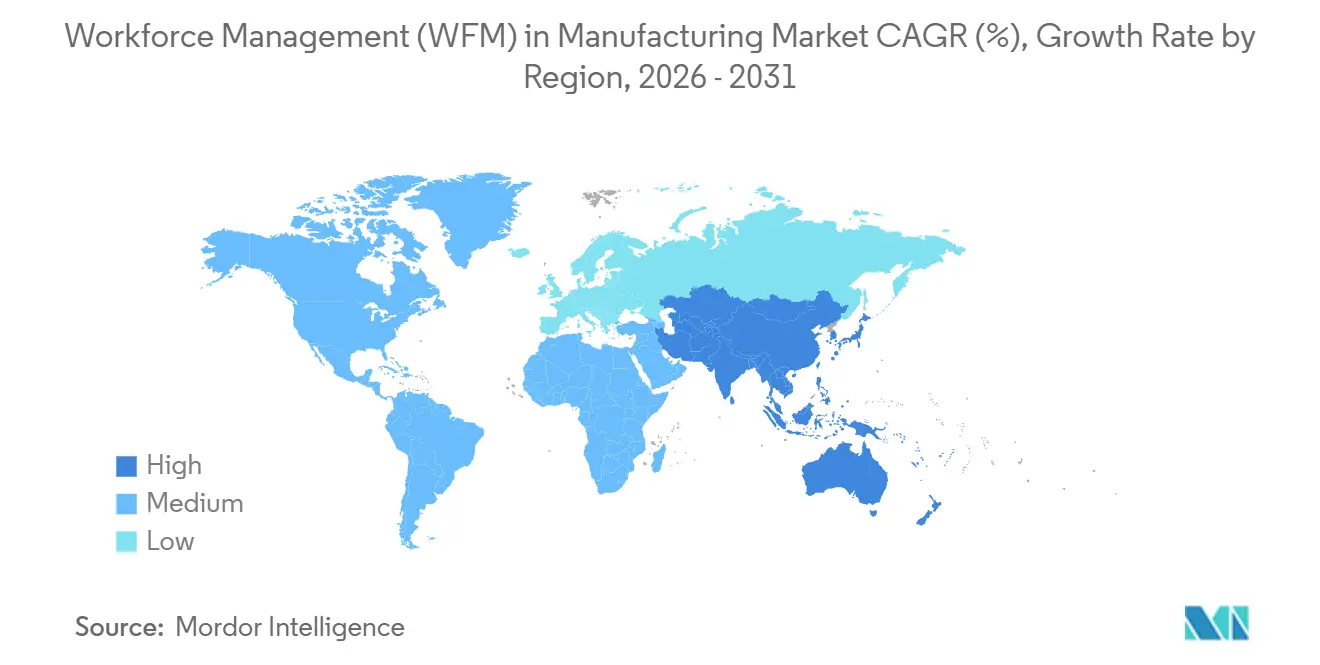

- By geography, North America held 39.12% of the workforce management market in 2025, while Asia-Pacific is forecast to expand at a 15.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Workforce Management (WFM) In Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| iver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Labor Shortages and Aging Shop-Floor Workforce | +2.8% | Global, most acute in North America, Europe, and Japan | Short term (≤ 2 years) |

| Industry 4.0 Programs Requiring Dynamic Labor Orchestration | +2.2% | North America, Europe, and China | Medium term (2-4 years) |

| Tighter Overtime, Break, Fatigue and Payroll Compliance | +1.6% | North America, Europe, and Australia | Short term (≤ 2 years) |

| Demand for Real-Time Labor Visibility and Cost Control | +1.2% | Global | Medium term (2-4 years) |

| Edge and IoT-Triggered Rescheduling from Production Events | +0.8% | APAC, North America | Long term (≥ 4 years) |

| Growth of Contractor, Agency and Cross-Trained Labor Pools | +0.5% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortages and Aging Shop-Floor Workforce

In the workforce management (WFM) in the manufacturing market, labor scarcity is pushing workforce planning closer to daily production control. Manufacturers are facing a long replacement cycle for skilled roles, and it is projected that 3.8 million positions will open in U.S. manufacturing through 2033, with 1.9 million potentially unfilled.[1]NAM News Room, “The State of the Manufacturing Workforce in 2025,” National Association of Manufacturers, nam.org That pressure makes skill mapping, shift coverage visibility, and cross-training workflows more valuable because plants cannot rely on informal scheduling decisions when critical roles are hard to backfill. In the workforce management in the manufacturing market, these tools are increasingly used to show who is qualified, who is available, and where single-point skill gaps sit before they disrupt production. The need is strongest in multi-shift operations where every uncovered position raises overtime risk and puts output stability under pressure. This is why the WFM in manufacturing market is being drawn deeper into continuity planning, retention efforts, and plant-level risk control, rather than remaining limited to back-office administration.

Industry 4.0 Programs Requiring Dynamic Labor Orchestratio

In the manufacturing workforce management (WFM) market, smart-factory investments are driving demand for labor systems that can respond to machine and production signals in real time. When IIoT data, line events, or edge alerts indicate a disruption, digital scheduling tools can move qualified labor faster than spreadsheet-based planning. Research published in 2025 showed that AI-driven scheduling on cloud-edge infrastructure reduced the recharging frequency of industrial mobile equipment by up to 31.35%, demonstrating how better orchestration can eliminate wasted time in complex production settings.[2]Mario Lepore, Domenico Serra, and Raffaele Maccioni, “Leveraging Artificial Intelligence and Optimization for Agile AGV Scheduling in an Edge-to-Cloud Manufacturing Framework,” Soft Computing, link.springer.com A lighthouse factory workforce management solution was also launched, built around IIoT, AI, big data, and cloud computing for real-time labor scheduling in manufacturing environments. In the workforce management market for manufacturing, that linkage is driving buyer interest in platforms that combine labor availability, certification status, and production change signals into a single operating layer. It also supports the growing interest in hybrid architectures, as many manufacturers seek to run analytics and user access in the cloud while keeping parts of operational control close to the plant.

Tighter Overtime, Break, Fatigue and Payroll Compliance

In the manufacturing workforce management market, compliance has become one of the clearest drivers of investment in time, attendance, and scheduling systems. The U.S. Department of Labor raised the standard salary threshold for overtime exemption to USD 58,656 per year, effective January 2025, forcing many employers to revisit workforce classification and time-recording processes. Fatigue control is also increasingly difficult to manage manually, as employers need stronger oversight of long hours, night work, breaks, and shift design in high-risk operations. The UK Health and Safety Executive requires that fatigue risk from shift work and excessive hours be assessed, which supports demand for automated alerts and policy-based scheduling controls. In workforce management for the manufacturing market, time and attendance software is often the first module adopted because payroll auditability and overtime exception control are the most visible compliance gaps. This keeps compliance-led buying strong in North America and Europe, where enforcement expectations and documentation requirements are already well defined.[3]GaiaWorks, “2025 Challenges in Manufacturing Smart Scheduling Technology,” GaiaWorks, gaiaworks.cn

Demand for Real-Time Labor Visibility and Cost Control

In the manufacturing workforce management market, plants are placing greater value on current labor data because scheduling gaps now affect output, overtime, and service levels almost immediately. An electronics assembly plant reduced scheduling conflicts by 90% and labor costs by 15% after deploying smart scheduling, showing why labor visibility is being treated as an operating control rather than a reporting tool. Manufacturers are also investing in scheduling technology that more closely connects labor coverage, employee experience, and production continuity. In the manufacturing workforce management market, buyers increasingly expect a single view of attendance, skills, and shift demand so supervisors can respond before missed coverage becomes extra labor costs or lost throughput. This direction was reinforced in late 2025 with the launch of a Workforce Intelligence Hub designed to unify scheduling, time, hiring, performance, and pay data to provide stronger labor insights. Real-time visibility, therefore, remains central to product roadmaps across workforce management (WFM) in manufacturing market, as cost control and operational response now depend on the same data layer.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Plant Systems and Difficult Integrations | -2.5% | Global, most severe in North America and Europe | Short term (= 2 years) |

| High Change-Management Burden in Unionized Multisite Plants | -1.8% | North America, Europe | Medium term (2-4 years) |

| Data Residency and Algorithmic Transparency Limits for AI Scheduling | -1.2% | Europe, APAC | Long term (= 4 years) |

| Weak Digital Readiness in Mid-Market Plants | -0.9% | APAC core, spill-over to Middle East and Africa and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy Plant Systems and Difficult Integrations

In the manufacturing workforce management market, integration remains the biggest barrier to adoption because many plants still operate across disconnected ERP, MES, and local attendance systems. In 2025, it was reported that 75% of manufacturing enterprises still relied on manual scheduling methods, with data fragmentation across systems leading to a 30% rework rate when plans changed after production events.[4]UAW, “UAW - Ultium Cells Local Agreement Local 1853 - Feb 2025,” UAW, uaw.org That problem increases project costs because vendors often need custom interfaces, data cleanup, and staged deployments before a site can trust automated scheduling outputs. In the manufacturing workforce management market, the hardest environments are usually the most complex plants, since they offer the greatest optimization upside but also the most fragmented technology estates. Buyers often delay wider rollouts until payroll rules, production events, and skill records are aligned across sites, which lengthens implementation cycles and slows revenue conversion for vendors. This restraint also explains why services are growing faster than software in the workforce management market for manufacturing, because integration and configuration work remain essential for real deployment success.

High Change-Management Burden in Unionized Multisite Plants

In the manufacturing workforce management market, unionized and multisite operations add a dense rule layer that generic scheduling systems do not always handle well. The February 2025 UAW-Ultium Cells local agreement for the Spring Hill facility documented more than 12 work-schedule variants, shift premium tiers, and overtime equalization requirements across a single plant. The Lockheed Martin-UAW 2025 contract memorandum also set a July 31, 2025, deadline for implementing a new overtime management system at a designated facility, showing that workforce technology can become part of formal labor obligations. In the manufacturing workforce management market, variations across plants, unions, and jurisdictions increase the effort required to configure, test, and govern a single platform consistently. Joint consultation rules can also slow rollout when scheduling practices change, since plant leaders cannot treat automation as a simple software switch. This makes change management nearly as important as product functionality for large, unionized programs in the manufacturing workforce management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Leads Revenue While Services Gain Speed

Software accounted for 72.18% of the workforce management (WFM) in manufacturing market share in 2025, keeping it at the center of purchasing decisions across factories. Time and attendance management was the largest software sub-segment at 28.31% of total software revenue, reflecting that payroll auditability and attendance control remain the first pain points many manufacturers seek to address. In workforce management in the manufacturing market, this layer is often funded first because it affects every shift, every employee record, and every payroll cycle. Overtime rules, break tracking, and fatigue-related controls have also made core time systems more important in regulated manufacturing settings. Once this base is in place, manufacturers usually expand into employee scheduling, forecasting, absence management, workforce analytics, task management, and self-service communication, as these functions work more effectively when they share a single labor data backbone.

Services are projected to grow at a 13.12% CAGR through 2031, making it the fastest-growing offering type in the workforce management in manufacturing market. That growth reflects the implementation complexity in older plants, where software alone cannot address connector design, plant-rule configuration, union logic, or change-management needs. In the workforce management in the manufacturing market, vendors that can pair software with manufacturing-specific service teams are better placed to reduce deployment risk and improve time to value. An October 2024 acquisition underlined this point by strengthening coverage for deskless, hourly, unionized, and multi-site workforces that usually require deeper configuration support. This is also where workforce management in manufacturing industry rewards providers that combine product capability with plant-ready execution rather than selling a light implementation model that works only in simpler service environments.

By Deployment Mode: Cloud Stays Ahead While Hybrid Gains Ground

Cloud deployment accounted for 61.47% of the market in 2025, indicating that SaaS-based delivery is now the primary route for new workforce management (WFM) in manufacturing market rollouts. Manufacturers are drawn to cloud systems because they simplify compliance updates, mobile access, employee self-service, and centralized oversight across multiple sites. Cloud and subscription revenues grew 30% year over year to EUR 44.1 million, or USD 47.6 million, in H1 2025, while cloud’s share of total software revenue increased from 39% to 48% over 12 months. That result shows that recurring cloud revenue is becoming increasingly important even as customers remain cautious about broader enterprise technology spending. In the manufacturing workforce management market, cloud also helps vendors deliver consistent rules, employee-facing tools, and analytics across geographically dispersed operations.

Hybrid deployment is projected to grow at a 14.37% CAGR through 2031, the fastest among deployment modes in the WFM in manufacturing market. Its appeal lies in balance: manufacturers can keep sensitive workflow logic or local data processing near the plant while using the cloud for self-service, dashboards, and broader planning access. This model fits plants that cannot fully retire on-premise systems but still want to modernize workforce control and user experience. In the manufacturing industry, hybrid adoption often signals a maturity phase in which buyers seek modern operating flexibility without sacrificing local governance over critical processes.

By Enterprise Size: Large Enterprises Lead While SMEs Expand Faster

Large enterprises held 60.93% of the market in 2025, giving them the largest role in current workforce management (WFM) in manufacturing market. These organizations can fund multi-module deployments, absorb long implementation cycles, and dedicate teams to union rule mapping, system integration, and process redesign. They also gain greater benefits from advanced WFM because broad labor pools, multiple plants, and complex shift structures create greater savings potential once a common platform is in place. In the manufacturing workforce management market, large enterprises also tend to keep systems longer because switching away from embedded pay logic, labor rules, and qualification records is disruptive. This makes the enterprise tier important for vendor revenue stability, even when sales cycles remain long and procurement scrutiny remains high.

SMEs are forecast to expand at a 15.48% CAGR through 2031, making them the fastest-growing buyer group in the manufacturing workforce management market. Cloud-native delivery has reduced implementation timelines from 12-18 months to a matter of weeks, making adoption more realistic for smaller plants with lean IT and HR resources. In February 2026, it was reported that manufacturers using digital HR and attendance systems achieved more than 99% accuracy in employee data collection, which helps explain why smaller factories are turning to digital workflows that reduce manual administration. In the manufacturing workforce management market, subscription pricing has also lowered the barrier to entry for SMEs by replacing heavy upfront spending with manageable operating budgets. This is the second place where WFM in manufacturing industry is expanding its user base, since smaller factories can now buy tools that were once practical mainly for major enterprise deployments.

By End-User Industry: Automotive Holds Scale While Electronics and Semiconductors Move Faster

Automotive contributed 20.61% of the market in 2025, making it the largest end-user vertical in the workforce management (WFM) in manufacturing market. The sector depends on tightly coordinated multi-shift operations, detailed labor rules, and rising EV-related process complexity, all of which increase the value of reliable scheduling and attendance control. The UAW-Ultium Cells agreement for the Spring Hill battery plant demonstrated that one facility can accommodate more than 12 schedule variants and overtime equalization rules, creating a strong use case for configurable WFM tools. A 2025 manufacturing recognition program also highlighted that compliance-led deployments in automotive settings are producing measurable operating value for customers. In the workforce management market, other verticals such as pharmaceuticals, aerospace and defense, food and beverage, and industrial machinery each bring different priorities, but all need stronger alignment between labor availability and production discipline.

Electronics and semiconductors are forecast to grow at a 13.99% CAGR through 2031, the fastest rate among end-user industries in the WFM in manufacturing market. This vertical is highly sensitive to skill mismatches, absence risk, and line disruption, so buyers place strong value on labor visibility and precise assignment control. An electronics assembly plant using intelligent scheduling reduced scheduling conflicts by 90%, lowered labor costs by 15%, and raised the multi-skilled employee ratio by 30% within one implementation cycle. Those outcomes show why electronics is becoming a major growth engine for the workforce management in the manufacturing market, as advanced assembly and semiconductor operations place tighter demands on labor orchestration.

Geography Analysis

North America held 39.12% of the workforce management in manufacturing market share in 2025, making it the largest regional contributor. The region benefits from labor scarcity, strict wage-and-hour enforcement, and a mature base of digital manufacturing investment. U.S. manufacturing continues to face open roles, with projections showing that 3.8 million positions will open through 2033, and 1.9 million of those positions may remain unfilled. That keeps the workforce management (WFM) in manufacturing market relevant not only for payroll accuracy but also for coverage planning, cross-training visibility, and overtime control. South America remained smaller, but Brazil’s automotive base still generated focused demand, driving multinational standards that pushed local suppliers toward stronger scheduling and labor governance practices.

Europe remained a structurally important region in the workforce management in the manufacturing market, led by Germany, the United Kingdom, and France. Strong cloud momentum was reported in 2025, with cloud and subscription revenues reaching EUR 44.1 million (USD 47.6 million) in H1 2025 and cloud’s share of software revenue rising to 48%. European product design is also being shaped by tighter expectations for transparency and explainability in automated workforce decisions, favoring vendors with deeper local compliance. In the workforce management market for manufacturing, country-specific labor expertise and audit-ready rule engines are more important in Europe than a generic scheduling feature set alone.

Asia-Pacific is projected to expand at a 15.23% CAGR through 2031, making it the fastest-growing region in the WFM in manufacturing market. Growth is being driven by factory digitalization in China, industrial expansion in India, and demographic pressure in Japan and South Korea. In February 2026, it was reported that manufacturers using digital HR and attendance systems achieved more than 99% accuracy in employee data collection, which supports adoption in Japan’s compliance-sensitive manufacturing base. Chinese vendors are also pushing innovation, with GaiaWorks launching a lighthouse factory workforce management solution that links IIoT, AI, big data, and cloud computing for real-time labor scheduling. The Middle East and Africa remain longer-horizon opportunities in the workforce management in the manufacturing market, where adoption is likely to follow factory build-outs and industrial expansion rather than lead them.

Competitive Landscape

The workforce management market in manufacturing remained moderately fragmented in 2026, with global HCM suites, dedicated WFM specialists, and regional vendors competing for plant budgets. UKG, Dayforce, and WorkForce Software, now part of ADP, anchor the enterprise tier through broad coverage across scheduling, time, payroll, and compliance. In the manufacturing workforce management market, region-specific strengths still matter because manufacturers often buy based on local labor rules, installed systems, and industry-specific deployment needs. ATOSS has maintained a strong manufacturing position in DACH, while GaiaWorks has gained relevance in China through IIoT-linked scheduling and lighthouse-factory positioning. This structure keeps pricing pressure active in the manufacturing workforce management market, making plant-specific depth more valuable than broad, generic HR coverage.

Consolidation has accelerated because large vendors are buying specialized capabilities rather than building every manufacturing workflow in-house. UKG completed its acquisition of Shiftboard in May 2025, adding manufacturing and energy scheduling, fatigue management, and union compliance capabilities used by clients such as BASF and Shell. ADP completed its acquisition of WorkForce Software in October 2024, deepening coverage for deskless, hourly, unionized, and multi-site workforces at a global scale. Dayforce also expanded its planning capabilities with the October 2025 launch of Strategic Workforce Planning, accelerated by the acquisition of Agentnoon. These moves show that buyers in the workforce management (WFM) in manufacturing market are rewarding vendors that can connect daily labor execution with broader planning, compliance, and skills visibility.

Product differentiation is now shifting toward AI architecture and ecosystem connectivity in the manufacturing workforce management market. UKG’s October 2025 partnership with Google Cloud added Gemini Enterprise, Vertex AI, and BigQuery to its WFM, HR, and payroll stack, extending its ability to support agentic AI workflows. Dayforce’s February 2026 product release added machine learning demand forecasting and four AI agents covering pay, time off, job descriptions, and manager communication, showing how AI is moving into routine workforce decisions. The clearest white space in the WFM in manufacturing market remains the mid-market plant base, which needs ISA-95-aware integrations, deeper union rule support, and practical deployment models without the cost and complexity of the largest enterprise suites.

Workforce Management (WFM) In Manufacturing Industry Leaders

UKG Inc.

Dayforce, Inc.

WorkForce Software, LLC

ATOSS Software SE

TimeClock Plus, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Legion Technologies announced the integration of its AI demand forecasting and labor optimization platform with SAP SuccessFactors, extending AI-native scheduling capabilities directly into the SAP enterprise environment and representing a strategic push into large-enterprise manufacturing ERP ecosystems where SAP commands widespread installed base.

- March 2026: Deputy Corporation announced reaching 1 billion shifts scheduled on its platform, doubling from 500 million in 2023, and simultaneously introduced Deputy AI, an embedded intelligence layer designed to interpret demand signals, apply labor regulations, and optimize shift scheduling in real time across 380,000 workplaces in more than 100 countries.

- February 2026: Dayforce, Inc. released its February 2026 product update, introducing machine learning-powered demand forecasting for WFM incorporating historical patterns, special events, and external signals such as weather data, alongside 4 new AI agents covering pay, time off, job description generation, and manager communications.

- November 2025: UKG Inc. unveiled the Workforce Intelligence Hub at its UKG Aspire 2025 conference, an AI-driven operational command center built on UKG Bryte AI that unifies scheduling, time tracking, hiring, performance, and pay data with manufacturing-specific benchmarks, enterprise availability commenced in the first half of 2026.

Global Workforce Management (WFM) In Manufacturing Market Report Scope

The Workforce Management (WFM) in Manufacturing Market refers to software and service platforms that streamline workforce operations across manufacturing enterprises. These solutions cover employee scheduling, time and attendance management, workforce analytics and forecasting, leave and absence management, task execution, and employee self-service communication. Deployed via cloud, on-premise, or hybrid models, WFM platforms serve both large and small manufacturers across industries such as automotive, electronics, industrial machinery, pharmaceuticals, food and beverage, and aerospace. They enhance productivity, ensure compliance, optimize labor costs, and support operational efficiency in global manufacturing environments.

The Workforce Management (WFM) in Manufacturing Market Report is segmented by Offering (Software [Employee Scheduling and Labor Optimization, Time and Attendance Management, Workforce Analytics and Forecasting, Leave and Absence Management, Task and Execution Management, and Employee Self-service and Communication] and Services), Deployment Mode (Cloud, On-premise, and Hybrid), End-user Enterprise Size (Large Enterprises and Small and Medium-sized Enterprises), End-user Industry (Automotive, Electronics and Semiconductors, Industrial Machinery and Equipment, Pharmaceuticals and Chemicals, Food and Beverage, and Aerospace and Defense), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | Employee Scheduling and Labor Optimization |

| Time and Attendance Management | |

| Workforce Analytics and Forecasting | |

| Leave and Absence Management | |

| Task and Execution Management | |

| Employee Self-service and Communication | |

| Services |

| Cloud |

| On-premise |

| Hybrid |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Automotive |

| Electronics and Semiconductors |

| Industrial Machinery and Equipment |

| Pharmaceuticals and Chemicals |

| Food and Beverage |

| Aerospace and Defense |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Offering | Software | Employee Scheduling and Labor Optimization |

| Time and Attendance Management | ||

| Workforce Analytics and Forecasting | ||

| Leave and Absence Management | ||

| Task and Execution Management | ||

| Employee Self-service and Communication | ||

| Services | ||

| By Deployment Mode | Cloud | |

| On-premise | ||

| Hybrid | ||

| By End User Enterprise Size | Large Enterprises | |

| Small and Medium-sized Enterprises | ||

| By End-user Industry | Automotive | |

| Electronics and Semiconductors | ||

| Industrial Machinery and Equipment | ||

| Pharmaceuticals and Chemicals | ||

| Food and Beverage | ||

| Aerospace and Defense | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of workforce management (WFM) in manufacturing market ?

The workforce management (WFM) in manufacturing market was valued at USD 1.52 billion in 2025 and is forecast to reach USD 2.59 billion by 2031, growing at a 9.44% CAGR during 2026-2031.

Which region leads demand for workforce management tools in manufacturing plants?

North America led with 39.12% share in 2025, supported by labor scarcity, compliance pressure, and a mature base of digital manufacturing investment.

Which deployment model is growing fastest across manufacturing WFM platforms?

Hybrid deployment is growing fastest at a 14.37% CAGR through 2031 because manufacturers want cloud flexibility while retaining local control over sensitive plant data and workflows.

Why are manufacturers buying more workforce management software now?

The main reasons are labor shortages, overtime and fatigue compliance, real-time labor visibility, and the need to match workforce decisions with smart-factory operations.

Which manufacturing vertical is expanding fastest for workforce management adoption?

Electronics and semiconductors is the fastest-growing vertical at a 13.99% CAGR through 2031, supported by skill-intensive operations and the high cost of scheduling errors.

What kind of manufacturers are increasing adoption the fastest?

SMEs are growing fastest at a 15.48% CAGR through 2031 because cloud-native platforms have reduced implementation time and lowered upfront spending needs.

Page last updated on: